Tokai Carbon Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Tokai Carbon Bundle

A Must-Have Tool for Decision-Makers

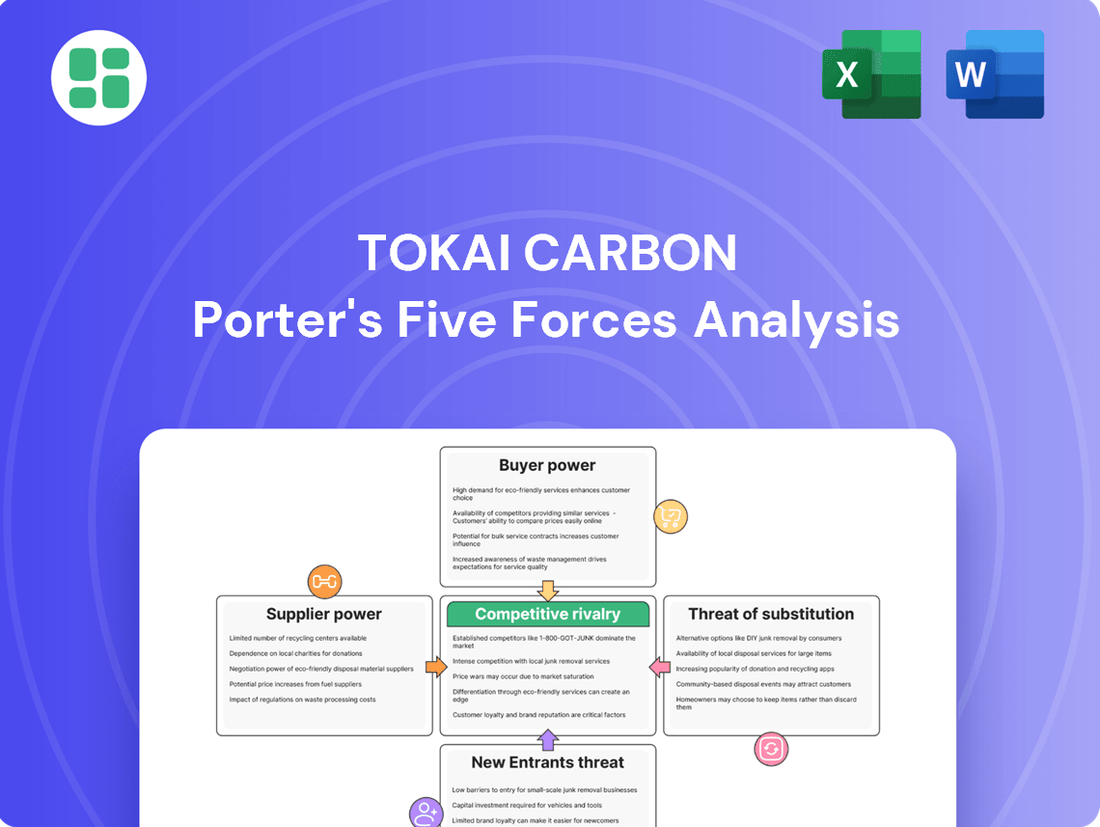

Tokai Carbon navigates an industry shaped by intense rivalry and the constant threat of substitutes for its carbon products. Understanding the leverage held by its powerful suppliers and the bargaining power of its diverse customer base is crucial for strategic advantage. The barriers to entry, while significant, still present a dynamic competitive landscape.

The complete report reveals the real forces shaping Tokai Carbon’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Concentration of Raw Material Suppliers

Tokai Carbon's reliance on a concentrated group of suppliers for essential raw materials like petroleum needle coke and coal tar pitch grants these suppliers considerable bargaining power. For instance, in 2024, the market for high-purity petroleum needle coke, a critical component for graphite electrodes, is dominated by a limited number of producers, some of whom also supply Tokai Carbon directly.

This concentration means Tokai Carbon may face fewer alternatives for securing these specialized inputs, potentially leading to increased costs or supply disruptions if supplier relationships sour. The global nature of this supply chain, with a significant portion of high-quality needle coke originating from a handful of countries, further amplifies this dependency and supplier leverage.

Specialized Nature of Inputs

Tokai Carbon's reliance on highly specialized raw materials for products like fine carbon and specialty graphite for semiconductors significantly influences supplier bargaining power. These materials often have stringent quality specifications that are not easily met by a broad range of suppliers.

The specialized nature of these inputs means that finding alternative suppliers can be a complex and time-consuming process. This can lead to high switching costs for Tokai Carbon, as new materials would likely require extensive qualification and testing to ensure they meet the critical performance requirements for advanced applications.

For instance, in the semiconductor industry, even minor variations in material purity or consistency can impact the performance and yield of critical components. This necessity for precision gives suppliers of these specialized carbons a considerable advantage in price negotiations and terms of supply.

Impact of Energy Costs

Energy represents a significant cost for Tokai Carbon, as its manufacturing processes for carbon and graphite products are highly energy-intensive. For instance, the global average cost of electricity for industrial consumers in 2024 hovered around $0.15 per kWh, a figure that can substantially impact Tokai Carbon's bottom line.

Consequently, swings in global energy prices, influenced by supply dynamics or geopolitical events, directly affect Tokai Carbon's production expenses and overall profitability. This makes energy suppliers a powerful force, capable of dictating terms and impacting the company's financial performance.

Supplier's Ability to Forward Integrate

Tokai Carbon's suppliers could increase their bargaining power if they were to integrate forward into manufacturing carbon or graphite products. This would directly compete with Tokai Carbon, giving them more leverage in pricing and supply negotiations. While not a prevalent threat currently, it's a crucial long-term strategic consideration for supply chain resilience.

This potential for forward integration by suppliers is a significant factor in assessing their bargaining power. If a supplier, for instance, a specialized graphite electrode producer, were to move into Tokai Carbon's core business areas, it would fundamentally shift the power dynamic. This could manifest in several ways:

- Increased Competition: Direct competition from a former supplier would fragment the market further.

- Supply Chain Disruption: A supplier’s focus on its own downstream products could reduce its commitment to supplying Tokai Carbon.

- Price Pressure: A vertically integrated supplier could dictate terms more aggressively, potentially impacting Tokai Carbon's margins.

Availability of Substitutes for Raw Materials

The bargaining power of suppliers for Tokai Carbon is significantly influenced by the availability of substitutes for their key raw materials. The primary inputs, such as petroleum coke and pitch, are crucial for producing graphite electrodes and carbon black, core products for Tokai Carbon. Limited viable alternatives for these specific materials mean that suppliers hold considerable sway.

This scarcity of cost-effective substitutes for essential raw materials like petroleum coke and pitch directly enhances supplier power. Tokai Carbon's dependence on these particular inputs restricts its ability to switch to other materials, thereby granting suppliers a stronger negotiating position.

- Limited Substitutes: Petroleum coke and pitch are vital for graphite electrodes and carbon black, with few readily available and economically viable alternatives.

- Supplier Leverage: This lack of substitutes allows suppliers to dictate terms, potentially increasing costs for Tokai Carbon.

- Impact on Tokai Carbon: Tokai Carbon's reliance on these specific raw materials strengthens the bargaining power of its suppliers.

Supplier Grip: Specialized Materials & Energy Costs Squeeze Tokai Carbon

Tokai Carbon's bargaining power with its suppliers is constrained by the specialized nature of its key raw materials, such as high-purity petroleum needle coke and coal tar pitch. In 2024, the limited number of global producers for these critical inputs, particularly for graphite electrodes, grants suppliers significant leverage. This concentration, coupled with stringent quality requirements for advanced applications like semiconductors, means Tokai Carbon faces high switching costs and potential supply vulnerabilities.

The energy-intensive production processes of Tokai Carbon also amplify the bargaining power of energy suppliers. With industrial electricity costs in 2024 averaging around $0.15 per kWh globally, fluctuations in energy prices directly impact Tokai Carbon's operational expenses and profitability, allowing energy providers to exert considerable influence over terms.

The bargaining power of Tokai Carbon's suppliers is further bolstered by the scarcity of viable substitutes for essential raw materials like petroleum coke and pitch. This dependency limits Tokai Carbon's flexibility in sourcing, empowering suppliers to dictate pricing and supply conditions.

| Raw Material | Key Use | Supplier Concentration (2024 Estimate) | Impact on Tokai Carbon |

|---|---|---|---|

| Petroleum Needle Coke (High Purity) | Graphite Electrodes | Dominated by a few global producers | High dependency, price sensitivity |

| Coal Tar Pitch | Binder for electrodes, carbon black | Concentrated global supply | Limited alternatives, supplier leverage |

| Electricity | Manufacturing processes | Regional energy market dynamics | Significant cost factor, price volatility |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Tokai Carbon's position in the graphite electrode and carbon materials market.

Instantly visualize competitive pressures with a dynamic Porter's Five Forces analysis, allowing Tokai Carbon to proactively address strategic challenges.

Customers Bargaining Power

Customer Concentration and Purchase Volume

Tokai Carbon's major clients are significant industrial entities within the steel, automotive, and semiconductor industries. These substantial customers frequently procure goods in high quantities, granting them considerable leverage to negotiate reduced prices or more advantageous contract conditions.

For instance, in 2023, the automotive sector represented a crucial market for Tokai Carbon, and shifts in demand or pricing pressures from major automotive manufacturers could directly impact Tokai Carbon's revenue and profitability due to the sheer volume of their purchases.

Price Sensitivity in Commoditized Segments

For Tokai Carbon's more standardized products, like basic carbon black or certain graphite electrodes, customers are quite sensitive to price. This means they can readily switch to another supplier if the price is better, creating a very competitive environment that pushes prices down.

Switching Costs for Specialty Products

For high-performance specialty graphite and fine carbon crucial in sectors like semiconductors, customers face significant switching costs. These costs stem from rigorous qualification procedures, exact performance specifications, and the absolute necessity for uniform material characteristics, thereby diminishing customer leverage.

Customers' Ability to Backward Integrate

Large customers, particularly those in demanding sectors like steel and automotive, could theoretically develop the financial muscle and technical expertise to produce certain carbon or graphite components in-house. This backward integration, while requiring substantial capital outlay, presents a significant bargaining chip for these buyers during price negotiations.

The threat of customers backward integrating, though not a common occurrence for Tokai Carbon’s products, acts as a persistent leverage point. For instance, a major automotive manufacturer might explore producing specific graphite electrodes if the cost and complexity become prohibitive, thereby influencing Tokai Carbon’s pricing strategies.

- Potential for Backward Integration: Large industrial customers possess the financial and technical capacity to produce certain carbon and graphite components internally.

- Leverage in Negotiations: This capability grants customers increased bargaining power, influencing pricing and contract terms with suppliers like Tokai Carbon.

- High Capital Investment Barrier: While a theoretical threat, the significant capital expenditure required for backward integration often limits its practical application.

Impact of End-User Industry Health

The financial health and demand patterns within Tokai Carbon's primary customer sectors—steel, automotive, and semiconductors—are critical determinants of customer bargaining power. For instance, a noticeable slowdown in the global steel market during 2024, characterized by reduced production and pricing pressures, directly translates to increased leverage for steel manufacturers as buyers. This situation forces suppliers like Tokai Carbon to contend with intensified competition, potentially leading to concessions on pricing and terms to secure business.

This dynamic is further amplified when these end-user industries experience broader economic headwinds. A downturn in automotive production, for example, stemming from factors like supply chain disruptions or decreased consumer spending, means fewer orders for carbon products. In such a scenario, major automotive manufacturers can exert greater influence, demanding more favorable contract conditions from their carbon material suppliers.

- Steel Industry Impact: The steel sector, a significant consumer of Tokai Carbon's products, faced challenges in 2024 with fluctuating demand and overcapacity concerns in some regions, enhancing buyer power.

- Automotive Sector Trends: While the automotive industry saw some recovery, persistent supply chain issues and evolving consumer preferences continued to create a variable demand landscape, influencing negotiations with suppliers.

- Semiconductor Market Dynamics: The semiconductor industry, a growth area, generally exhibits strong demand. However, cyclical downturns within this sector can still empower large chip manufacturers to negotiate more aggressively for critical carbon materials.

Customer Bargaining Power: Impact on Industrial Suppliers

The bargaining power of Tokai Carbon's customers is a significant factor, particularly for its large industrial clients in sectors like steel, automotive, and semiconductors. These major buyers often purchase in high volumes, giving them substantial leverage to negotiate lower prices or more favorable terms.

For standardized products, customers are highly price-sensitive and can easily switch suppliers, intensifying competition and driving down prices. However, for specialized, high-performance materials crucial in industries like semiconductors, customers face high switching costs due to stringent qualification processes and performance requirements, thus reducing their bargaining power.

The financial health and demand within these key customer sectors directly influence their negotiating strength. For instance, a slowdown in the steel market during 2024, marked by reduced production and pricing pressures, empowers steel manufacturers to negotiate more aggressively with suppliers like Tokai Carbon.

| Customer Sector | 2024 Market Conditions Impacting Bargaining Power | Tokai Carbon's Product Relevance |

|---|---|---|

| Steel | Fluctuating demand, overcapacity concerns in some regions. | Graphite electrodes for steel production. |

| Automotive | Variable demand due to supply chain issues and consumer spending. | Carbon black for tires and other components. |

| Semiconductors | Generally strong demand, but cyclical downturns can empower large buyers. | High-purity graphite for semiconductor manufacturing. |

Preview Before You Purchase

Tokai Carbon Porter's Five Forces Analysis

This preview shows the exact Tokai Carbon Porter's Five Forces Analysis you'll receive immediately after purchase, offering a comprehensive examination of the competitive landscape. You'll gain insights into the bargaining power of buyers and suppliers, the threat of new entrants and substitute products, and the intensity of rivalry within the carbon products industry. This detailed analysis is ready for your immediate use, providing valuable strategic information.

Rivalry Among Competitors

Number and Diversity of Competitors

The global carbon and graphite products market features a mix of large, established companies like GrafTech International, SGL Carbon SE, and Nippon Carbon, alongside many smaller, regional players. This broad spectrum of competitors, each often specializing in different product niches, fuels a highly competitive environment.

Product Differentiation and Specialization

While standard carbon black and graphite electrodes can be seen as commodities, Tokai Carbon strategically competes in more specialized areas like fine carbon and high-performance specialty graphite. This differentiation shifts the competitive landscape from price wars to a focus on technological advancements and tailored customer solutions.

In these advanced segments, competition hinges on factors such as product performance and the ability to develop custom solutions for specific client needs. For instance, in 2023, Tokai Carbon's specialty graphite business, which serves sectors like semiconductors and advanced manufacturing, likely saw demand driven by innovation rather than simple cost considerations, reflecting the premium placed on specialized materials.

Industry Growth Rate

The carbon and graphite market is showing robust growth, with projections indicating a compound annual growth rate (CAGR) of around 5% through 2028, fueled by the burgeoning electric vehicle (EV) sector, advancements in energy storage, and the expanding electronics industry. This expansion, however, doesn't negate the impact of competitive rivalry.

While the overall market is expanding, intense competition can still exert significant price pressure. This is particularly evident in segments experiencing oversupply. For instance, the graphite electrode market in China faced considerable price erosion in early 2024 due to an overabundance of production capacity, even as broader market demand remained strong.

High Fixed Costs and Capacity Utilization

Tokai Carbon operates in an industry characterized by substantial capital requirements for its manufacturing facilities. This means that building and maintaining plants for carbon and graphite products demands significant upfront investment, resulting in high fixed costs for all players. For instance, the construction of a new electrode production facility can easily run into hundreds of millions of dollars.

To offset these high fixed costs and achieve economies of scale, companies like Tokai Carbon often strive for high capacity utilization. Operating at near-full capacity helps spread the fixed costs over a larger volume of output, thereby lowering the per-unit cost. This is crucial for remaining competitive in the market.

However, this reliance on high capacity utilization can intensify competitive rivalry, especially during economic downturns or periods of reduced demand. When demand softens, companies may resort to aggressive pricing strategies to keep their production lines running and avoid the severe financial consequences of idle capacity. This can lead to price wars, impacting profitability across the industry.

- High Capital Investment: The carbon and graphite manufacturing sector requires substantial capital for plant and machinery, creating a significant barrier to entry and contributing to high fixed costs for existing firms.

- Economies of Scale Drive: Companies aim for high capacity utilization to reduce per-unit production costs, making price competition a key factor in market share battles.

- Pricing Pressure in Downturns: When demand falls, the need to cover high fixed costs can force companies to lower prices aggressively to maintain production volumes, intensifying rivalry.

- Example of Cost Structure: For a major graphite electrode producer, fixed costs related to depreciation, maintenance, and utilities can represent a substantial portion of their total operating expenses, often exceeding 40% of total costs.

Strategic Alliances and Acquisitions

The carbon materials industry is characterized by ongoing strategic alliances and market consolidation, signaling a dynamic competitive environment. These moves aim to bolster market share, expand product portfolios, and drive innovation.

Tokai Carbon has actively participated in this trend, pursuing acquisitions and forming joint ventures for technology development. For instance, in 2023, the company announced its intention to acquire a significant stake in a specialized graphite electrode manufacturer, aiming to enhance its production capacity and technological capabilities in a key segment.

- Strategic Alliances: Partnerships focus on joint research and development, particularly in areas like advanced carbon materials for electric vehicles and renewable energy storage.

- Market Consolidation: Acquisitions are driven by the need to achieve economies of scale, secure raw material access, and gain a competitive edge in high-growth markets.

- Tokai Carbon's Strategy: The company's acquisition activities in 2023 and early 2024 were geared towards strengthening its position in specialized carbon products and improving its global supply chain efficiency.

- Impact on Competition: These strategic moves intensify rivalry by creating larger, more integrated players and pushing smaller competitors to specialize or seek their own alliances.

Carbon & Graphite: Innovation and Consolidation Fuel Intense Rivalry

Competitive rivalry within the carbon and graphite sector is robust, driven by a mix of large global players and specialized regional firms. Tokai Carbon differentiates itself by focusing on high-performance specialty graphite, moving beyond commodity-like products. This strategic positioning means competition is less about price and more about technological innovation and tailored customer solutions.

The industry's high capital investment requirements and the pursuit of economies of scale through high capacity utilization intensify rivalry. When demand dips, the pressure to cover fixed costs can lead to aggressive pricing, particularly in segments like graphite electrodes, as seen with price erosion in China in early 2024 due to oversupply.

Strategic alliances and market consolidation, including Tokai Carbon's acquisition activities in 2023, further shape the competitive landscape. These moves create larger, integrated competitors, pushing others to specialize or form their own partnerships to maintain market share and technological relevance.

SSubstitutes Threaten

Alternative Materials in Steelmaking

While graphite electrodes are essential for Electric Arc Furnaces (EAFs) in steel production, the long-term threat from alternative steelmaking methods or increased use of different raw materials could dampen demand. For instance, advancements in direct reduced iron (DRI) technology, which uses natural gas or hydrogen, could reduce reliance on scrap steel and, consequently, EAFs. However, the global trend, supported by environmental mandates, is a move towards EAFs, which currently bolsters graphite electrode demand.

Emerging Technologies in Batteries

While graphite is the current king of battery anodes, especially for electric cars, new technologies are on the horizon. Researchers are actively developing silicon-dominant anodes and even lithium metal anodes, which could eventually offer better performance. This innovation presents a potential long-term threat of substitution for traditional graphite.

However, it's important to note that even with these advancements, graphite often remains a crucial component within these next-generation battery designs. For instance, silicon anodes are frequently blended with graphite to improve stability and conductivity. This suggests that while the landscape is evolving, graphite may not be entirely replaced but rather integrated into new material combinations.

New Materials in Automotive and Aerospace

The automotive and aerospace industries are constantly seeking lighter, stronger materials. This drive fuels the development of alternatives to traditional carbon products. For instance, advanced alloys and carbon fiber composites are increasingly being adopted for their superior strength-to-weight ratios.

Emerging nanomaterials like graphene and carbon nanotubes also present a significant threat. These materials, while still in development for widespread commercial use, offer exceptional properties that could displace carbon in certain high-performance applications. By 2024, the global advanced composites market, a key area for substitution, was projected to reach over $25 billion, indicating substantial investment and growth in these alternative material sectors.

Substitution in Friction Materials

Friction materials, crucial for automotive braking, face potential substitution from novel braking technologies or alternative material formulations that move away from carbon-based components. While the automotive industry is always exploring advancements, the unique performance benefits of carbon in demanding, high-temperature conditions present a significant barrier to widespread replacement. For instance, advanced ceramic composites, while offering excellent heat dissipation, often come with higher manufacturing costs and different wear characteristics that may not be universally suitable for all braking applications.

The threat of substitutes for friction materials, particularly those incorporating carbon, is moderate. While new technologies like regenerative braking in electric vehicles (EVs) can reduce wear on traditional friction brakes, they are unlikely to eliminate them entirely, especially in heavy-duty applications or for emergency stopping. The inherent properties of carbon, such as its thermal stability and low friction coefficient across a wide temperature range, remain highly valued. For example, in 2023, the global automotive friction material market was valued at over $15 billion, with carbon-based materials holding a significant share due to their proven efficacy.

- Technological Advancements: Emerging braking systems, including those utilizing advanced composites or entirely new physical principles, pose a potential substitution threat.

- Performance Replication: The difficulty in cost-effectively replicating carbon's high-temperature and high-stress performance characteristics limits the immediate impact of many substitutes.

- Market Share: Despite ongoing innovation, carbon-based friction materials continue to command a substantial portion of the automotive market, indicating customer trust and proven reliability.

- EV Integration: While EVs reduce reliance on friction brakes through regenerative braking, the need for conventional friction systems persists for safety and performance redundancy.

Sustainability-Driven Material Shifts

Increasing environmental concerns and the global push for sustainable solutions present a significant threat of substitutes for traditional carbon products. As industries seek greener alternatives, bio-based or recycled materials could emerge as viable replacements in various applications, potentially impacting demand for Tokai Carbon's offerings.

For instance, the automotive sector, a key consumer of carbon black for tires, is exploring natural rubber and alternative fillers to reduce its environmental footprint. In 2024, several major tire manufacturers announced increased investment in sustainable materials research, aiming to incorporate higher percentages of recycled content and bio-derived components into their products.

- Growing Demand for Recycled Content: The market for recycled carbon black is expanding, driven by regulatory pressures and corporate sustainability goals.

- Development of Bio-Based Alternatives: Research into materials like lignin and cellulose as substitutes for carbon black in certain applications is gaining momentum.

- Tokai Carbon's Recycling Initiatives: Tokai Carbon is actively engaged in carbon black recycling projects, recognizing the need to adapt to this evolving market dynamic and mitigate the threat of substitutes.

Carbon's Future: Emerging Substitutes and Market Adaptation

The threat of substitutes for Tokai Carbon's products is multifaceted, driven by technological innovation and environmental pressures. While carbon-based materials offer unique performance advantages, the continuous search for lighter, stronger, and more sustainable alternatives across industries like automotive, aerospace, and electronics presents a persistent challenge. Emerging materials and evolving manufacturing processes could potentially displace traditional carbon applications, necessitating ongoing adaptation and innovation from Tokai Carbon.

In the realm of steel production, while graphite electrodes are crucial for Electric Arc Furnaces (EAFs), the long-term threat from alternative steelmaking methods or different raw materials could impact demand. Advancements in direct reduced iron (DRI) technology, for example, might lessen reliance on scrap steel and, consequently, EAFs. However, the global trend toward EAFs, driven by environmental mandates, currently supports graphite electrode demand.

For battery anodes, while graphite remains dominant, research into silicon-dominant and lithium metal anodes poses a potential future substitution threat. Yet, even these next-generation anodes often incorporate graphite for stability and conductivity, suggesting integration rather than outright replacement.

The automotive and aerospace sectors are actively exploring advanced alloys and carbon fiber composites for their superior strength-to-weight ratios, presenting a substitution threat to traditional carbon products. Furthermore, nanomaterials like graphene and carbon nanotubes, though still in development for widespread use, could displace carbon in high-performance applications. The global advanced composites market, a key area for substitution, was projected to exceed $25 billion in 2024.

Friction materials, particularly those using carbon, face potential substitution from novel braking technologies or alternative formulations. While regenerative braking in EVs reduces wear on conventional brakes, it's unlikely to eliminate them entirely, especially in heavy-duty scenarios. The global automotive friction material market was valued at over $15 billion in 2023, with carbon-based materials holding a significant share due to their proven efficacy.

Environmental concerns are also driving the search for greener alternatives, such as bio-based or recycled materials, which could substitute traditional carbon products. The automotive sector, for instance, is exploring natural rubber and alternative fillers for tires. By 2024, major tire manufacturers were increasing investment in sustainable materials research, aiming for higher percentages of recycled and bio-derived components.

| Industry Segment | Potential Substitute | Impact on Carbon Products | Key Drivers | 2024 Market Insight |

|---|---|---|---|---|

| Steelmaking (EAFs) | DRI technology (hydrogen-based) | Reduced demand for graphite electrodes | Environmental regulations, decarbonization | EAFs remain dominant for scrap recycling, supporting graphite demand. |

| Batteries (Anodes) | Silicon-dominant anodes, Lithium metal anodes | Potential long-term displacement of graphite | Performance enhancement (energy density) | Graphite often integrated into new anode designs. |

| Automotive/Aerospace | Advanced alloys, Carbon fiber composites | Displacement of traditional carbon components | Lightweighting, strength-to-weight ratio | Global advanced composites market projected >$25 billion in 2024. |

| Automotive (Friction Materials) | Regenerative braking, Ceramic composites | Reduced wear on carbon friction brakes | EV adoption, material performance | Global friction material market >$15 billion in 2023; carbon holds significant share. |

| Tires (Carbon Black) | Natural rubber, bio-derived fillers, recycled content | Reduced demand for virgin carbon black | Sustainability, environmental footprint reduction | Increased investment in sustainable materials research by tire manufacturers. |

Entrants Threaten

High Capital Investment Requirements

High capital investment requirements act as a significant deterrent to new entrants in the carbon and graphite manufacturing sector. Establishing state-of-the-art production facilities, acquiring specialized machinery, and ensuring compliance with stringent environmental regulations demand substantial upfront financial commitment.

For instance, building a new graphite electrode plant can easily cost hundreds of millions of dollars, making it difficult for smaller companies or those without deep pockets to compete. This financial hurdle effectively limits the number of potential new players, thereby reducing the threat of new entrants for established firms like Tokai Carbon.

Proprietary Technology and R&D

Tokai Carbon's strong position in fine carbon and high-performance specialty graphite, crucial for sectors like semiconductors, is built upon significant investment in research and development and unique manufacturing techniques. Potential new entrants face a substantial hurdle, needing to commit considerable resources to R&D to match Tokai Carbon's technological capabilities or to acquire the necessary expertise.

Established Customer Relationships and Supply Chains

Tokai Carbon's deep-rooted relationships with major industrial clients, including those in the steel, automotive, and semiconductor sectors, create a formidable barrier for any new competitor. These aren't just transactional relationships; they are built on trust and years of reliable supply, making it extremely difficult for newcomers to gain a foothold.

New entrants would struggle to replicate Tokai Carbon's established supply chain qualifications. These qualifications are often rigorous and time-consuming to achieve, requiring extensive testing and validation processes that new companies simply haven't undergone. For instance, in the semiconductor industry, supplier qualification can take years and involve stringent quality control measures.

The loyalty of existing customers to Tokai Carbon is a significant deterrent. These customers have integrated Tokai's products into their own manufacturing processes and have likely invested in optimizing those processes. Switching suppliers would involve substantial costs, risk, and re-qualification efforts, making them hesitant to consider new, unproven entrants.

Regulatory Hurdles and Environmental Compliance

The carbon and graphite industry faces significant regulatory hurdles, particularly concerning environmental compliance. These stringent rules, stemming from the nature of manufacturing processes and raw material handling, demand substantial capital investment and specialized knowledge to navigate. For instance, in 2024, companies in this sector are increasingly investing in advanced emission control technologies, with the global environmental compliance market expected to reach hundreds of billions of dollars, demonstrating the scale of these requirements.

These compliance costs act as a formidable barrier to entry for potential new competitors. Newcomers must not only absorb the capital expenditure for state-of-the-art pollution control systems but also maintain ongoing operational expenses related to monitoring and reporting. This financial and technical burden significantly limits the number of new companies that can realistically enter the market and compete effectively with established players like Tokai Carbon.

- Environmental Regulations: Strict rules on emissions and waste management are common.

- Capital Investment: Compliance often requires significant upfront spending on technology.

- Expertise Needed: Navigating and adhering to regulations demands specialized knowledge.

- Barrier to Entry: These factors collectively deter new companies from entering the market.

Economies of Scale and Cost Advantages

Existing large-scale manufacturers, like Tokai Carbon, leverage significant economies of scale, translating into lower per-unit production costs. For instance, in 2023, Tokai Carbon's revenue reached ¥208.9 billion, indicating a substantial operational footprint that smaller competitors cannot easily replicate.

New entrants would find it challenging to match these cost efficiencies from the outset. This cost disadvantage makes competing on price, especially in segments like graphite electrodes where commoditization is higher, a formidable barrier.

- Economies of Scale: Tokai Carbon's established production capacity allows for lower per-unit costs, a significant hurdle for new market entrants.

- Cost Advantages: Existing players benefit from optimized supply chains and bulk purchasing power, which new entrants would struggle to achieve initially.

- Price Competition: The difficulty in matching cost structures means new entrants would likely face intense price pressure in commoditized product lines.

Carbon & Graphite: A Fortress Against New Competitors

The threat of new entrants in the carbon and graphite industry is considerably low due to substantial capital requirements, advanced technological expertise, and established customer relationships. For instance, Tokai Carbon's 2023 revenue of ¥208.9 billion highlights the scale of operations required to compete effectively.

Stringent environmental regulations, demanding significant investment in pollution control technology and specialized knowledge, further deter new players. The cost and complexity of compliance, especially in 2024 with increasing environmental scrutiny, create a high barrier.

Economies of scale enjoyed by established firms like Tokai Carbon, which translate into lower per-unit production costs, make it difficult for newcomers to compete on price. This cost advantage, coupled with long-standing customer loyalty and rigorous supplier qualification processes, effectively shields incumbent companies.

| Factor | Impact on New Entrants | Tokai Carbon's Advantage |

|---|---|---|

| Capital Investment | Very High | Established infrastructure and scale |

| Technology & R&D | High Barrier | Proprietary manufacturing techniques |

| Customer Relationships | Difficult to Replicate | Years of trust and integration |

| Regulatory Compliance | Costly & Complex | Experience and existing systems |

| Economies of Scale | Significant Cost Disadvantage | ¥208.9 billion (2023) revenue |

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis for Tokai Carbon leverages comprehensive data from annual reports, investor presentations, and industry-specific market research. We also incorporate insights from trade publications and financial databases to provide a robust understanding of the competitive landscape.