Smulders Group Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Smulders Group Bundle

From Overview to Strategy Blueprint

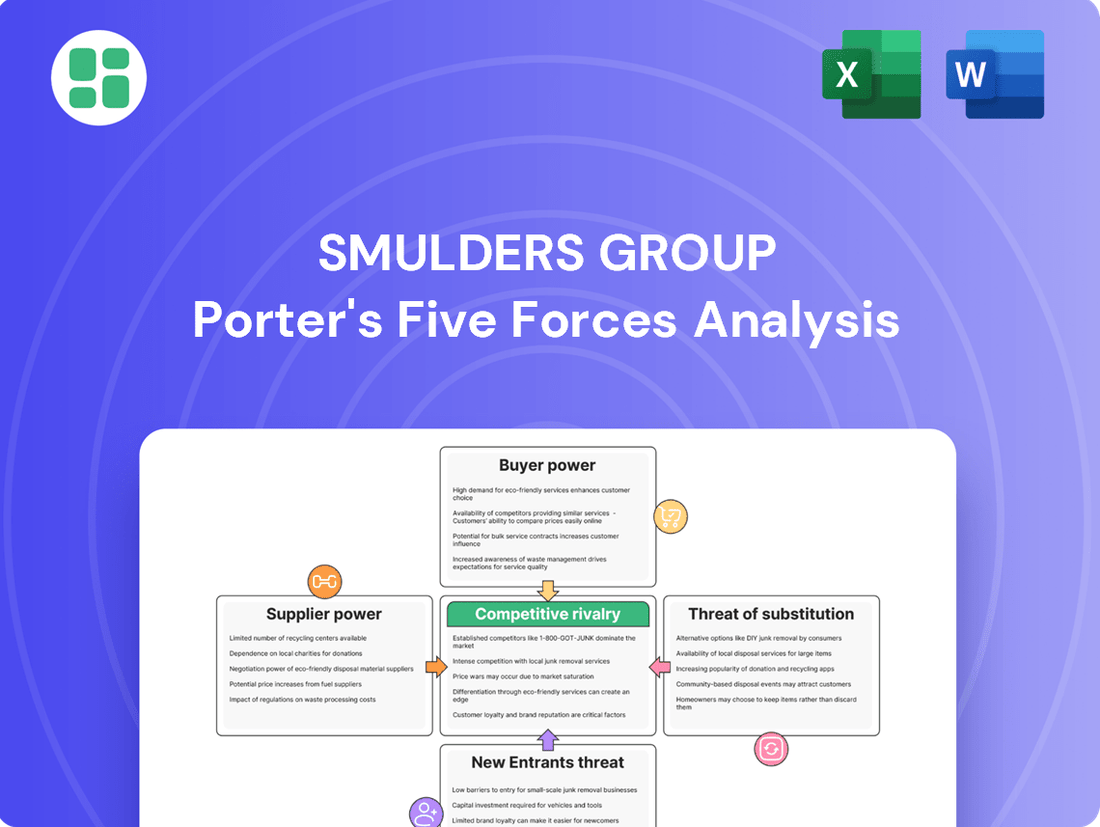

The Smulders Group operates in a landscape shaped by intense competition, with significant pressure from rivals and a constant threat of new entrants. Understanding the bargaining power of both suppliers and buyers is crucial for navigating this dynamic market.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Smulders Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Raw Material Suppliers

Smulders Group's reliance on steel for its intricate projects means that the bargaining power of steel suppliers is a key consideration. With a concentrated market of high-quality steel providers, these suppliers can indeed wield considerable influence over pricing, directly affecting Smulders' operational costs.

While the global steel market showed signs of stabilization by early 2025, it continued to grapple with price fluctuations and occasional supply limitations. For instance, benchmark steel prices, which saw significant increases in prior years, remained a critical factor in Smulders' procurement strategy, with potential for upward pressure impacting project margins.

Specialized Components and Technology

Suppliers of highly specialized components for offshore wind foundations and substations, like advanced electrical systems or unique fabrication machinery, can wield significant bargaining power. This is particularly true when there are limited alternative suppliers capable of meeting stringent technical specifications. For instance, the integration of high-voltage equipment, often a critical and specialized element, can be a focal point for supplier influence.

Labor Market Dynamics

The availability of skilled labor for engineering, fabrication, and assembly of complex steel structures, especially in specialized areas like offshore wind, significantly impacts supplier power. A scarcity of these specialized workers, a trend observed across the offshore wind sector, can drive up labor costs or cause project delays if not proactively managed.

Switching Costs for Inputs

Smulders faces considerable supplier power stemming from switching costs for essential inputs. Transitioning to a new supplier for critical materials or specialized services isn't a simple swap. It often involves extensive requalification of the new supplier's products, potential reconfiguration of Smulders' own manufacturing equipment to accommodate different specifications, and rigorous technical validation to ensure quality and compatibility. These processes represent significant investments of time and capital, effectively locking Smulders into existing supplier relationships and bolstering the bargaining leverage of incumbent suppliers.

The financial implications of these switching costs can be substantial. For instance, if a key component requires a supplier to meet very specific, proprietary technical standards, the cost to qualify a new supplier could run into hundreds of thousands of euros, potentially impacting project timelines and profitability. In 2024, the average cost for industrial companies to switch major suppliers, when factoring in integration and validation, has been estimated to be upwards of 15-20% of the annual contract value for critical components.

- High Requalification Costs: Specialized materials often demand rigorous testing and certification for new suppliers, adding significant overhead.

- Equipment Adaptation Expenses: Changes in input specifications may necessitate costly modifications or replacements of manufacturing machinery.

- Technical Validation Time: Ensuring new components meet Smulders' stringent quality and performance standards requires extensive engineering effort and testing periods.

- Impact on Project Timelines: Delays in supplier switching can directly affect project completion dates and associated revenue recognition.

Impact of Energy Costs

Steel production is incredibly energy-intensive, making energy costs a significant factor for suppliers. When global energy prices, like natural gas and electricity, surge, these increased operational costs are inevitably passed on to buyers, including companies like Smulders Group. This dynamic directly enhances the bargaining power of steel suppliers.

Even with advancements in energy-efficient technologies within the steel industry, the inherent volatility of energy markets remains a persistent driver of supplier leverage. For instance, the average price of Brent crude oil, a key indicator of global energy costs, experienced significant fluctuations throughout 2024, impacting upstream production expenses for steel manufacturers.

- Energy-Intensive Production: Steelmaking accounts for a substantial portion of global industrial energy consumption.

- Cost Pass-Through: Rising energy prices directly translate to higher raw material costs for steel buyers.

- Price Volatility Impact: Fluctuations in energy markets, such as those seen in 2024, empower suppliers who can adjust pricing accordingly.

- Technological Adoption: While efficiency gains are being made, they don't entirely negate the impact of energy price swings on supplier power.

High Supplier Power: Driving Up Costs for Key Materials

The bargaining power of suppliers for Smulders Group is notably high, particularly for specialized components and raw materials like steel. This stems from concentrated supplier markets, high switching costs, and the energy-intensive nature of steel production, which links supplier costs directly to volatile energy prices.

In 2024, the cost of key raw materials, including steel, remained a significant factor, with global steel prices experiencing upward pressure due to supply chain disruptions and increased demand in sectors like renewable energy infrastructure. For example, the average price of hot-rolled coil steel in Europe saw an approximate 10% increase year-over-year by Q3 2024, directly impacting Smulders' procurement expenses.

| Factor | Impact on Smulders | 2024 Data/Context |

|---|---|---|

| Supplier Concentration (Specialized Components) | Limited alternatives give suppliers leverage on price and terms. | Few manufacturers produce high-voltage transformers for offshore substations, leading to longer lead times and premium pricing. |

| Switching Costs | High costs to requalify suppliers and adapt equipment lock Smulders in. | Estimated 15-20% of contract value to switch major industrial suppliers, impacting project margins. |

| Energy Price Volatility | Increased energy costs for steel suppliers are passed on. | Brent crude oil prices averaged around $83 per barrel in 2024, contributing to higher steel production costs. |

What is included in the product

This Porter's Five Forces analysis for Smulders Group comprehensively examines the intensity of rivalry, the bargaining power of buyers and suppliers, the threat of new entrants, and the availability of substitutes within its operating environment.

Effortlessly identify and mitigate competitive threats with a visual breakdown of industry power dynamics.

Gain actionable insights into supplier leverage and customer bargaining power to optimize your strategic positioning.

Customers Bargaining Power

Large-Scale Project Nature

Smulders primarily serves clients in the offshore wind and oil & gas industries, sectors characterized by colossal, multi-billion euro projects. This inherently positions their customers, major developers and utility firms like Equinor and Polenergia, with significant leverage. Their ability to commit vast sums and their critical need for specialized infrastructure grants them considerable bargaining power.

Customer Concentration and Project Volume

Smulders Group's bargaining power of customers is influenced by customer concentration. While the company secured significant contracts, including those exceeding €1 billion in 2024, the pool of clients capable of commissioning such large-scale steel structures is relatively small. This limited number of major customers grants them considerable negotiation leverage.

Project-Specific Requirements and Customization

Smulders Group's customers often require highly specialized, turnkey solutions for complex steel structures, meaning each project is essentially unique. This bespoke nature of their work, involving custom engineering and fabrication, grants customers significant leverage in dictating design, specifications, and delivery timelines. For instance, in the offshore wind sector, a key market for Smulders, project developers meticulously define foundation designs and installation schedules to meet specific site conditions and regulatory approvals.

Availability of Alternative Suppliers

While Smulders Group holds a strong position as a European leader in offshore wind farm structures, the availability of alternative suppliers globally significantly influences customer bargaining power. Customers can source structural steel fabrication from a variety of international fabricators, particularly for more standardized components. This broadens their options and allows them to compare pricing and capabilities across multiple qualified providers.

The ease with which customers can solicit bids from numerous fabricators directly enhances their leverage. For instance, in 2024, the global market for offshore wind installation vessel components saw increased competition, with several emerging players from Asia offering competitive pricing. This competitive landscape means customers are not solely reliant on Smulders, enabling them to negotiate more favorable terms, especially when project scopes involve large volumes or less complex designs.

- Global Competition: The international market for offshore wind components offers numerous alternative suppliers to Smulders Group.

- Price Sensitivity: Customers can leverage multiple bids to secure more competitive pricing, especially for standardized structural elements.

- Supplier Diversification: The ability to source from various fabricators reduces customer dependence on any single supplier.

- Market Dynamics: Increased competition in 2024, particularly from Asian fabricators, has intensified customer bargaining power.

Customer's Financial Health and Industry Trends

The financial health of Smulders' customers, especially those in the burgeoning offshore wind sector, significantly shapes their purchasing power. As of early 2024, many offshore wind developers are grappling with increased project costs, with some reports indicating a rise of 20-30% for certain components compared to previous years. This financial pressure can translate into a stronger demand for more competitive pricing from suppliers like Smulders.

Industry trends further amplify this dynamic. Despite the long-term growth projections for offshore wind, a wave of project cancellations and delays in late 2023 and early 2024, driven by escalating interest rates and supply chain challenges, has put many developers in a precarious financial position. Consequently, their strategic priority shifts towards cost optimization, making them more inclined to negotiate harder on pricing with their partners.

- Customer Financial Strain: Rising interest rates and component costs in early 2024 have led to project delays and cancellations in the offshore wind sector, impacting developer profitability.

- Cost Sensitivity: Developers are actively seeking cost reductions, increasing their leverage to negotiate more favorable terms and pricing from suppliers.

- Market Volatility: Recent project postponements highlight the sensitivity of customer investment decisions to broader economic conditions, potentially weakening Smulders' pricing power.

Client Leverage: Billions at Stake

The bargaining power of Smulders' customers is substantial, driven by the concentrated nature of their client base in large-scale industrial projects. Given that these clients, often major energy developers, commission projects worth billions, they possess significant leverage. Smulders' 2024 contracts, some exceeding €1 billion, underscore the immense financial commitment and, consequently, the considerable negotiation power these clients wield.

| Customer Characteristic | Impact on Bargaining Power | Supporting Data/Observation (2024) |

| Customer Concentration | High | Limited pool of clients for multi-billion euro projects; contracts exceeding €1 billion secured. |

| Project Specialization & Customization | High | Bespoke engineering and fabrication for unique offshore wind foundations and oil & gas infrastructure. |

| Availability of Alternatives | Moderate to High | Global fabricators, including emerging Asian players offering competitive pricing for standardized components. |

| Customer Financial Health | Moderate to High | Project cost increases (20-30%) and market volatility (delays/cancellations) in early 2024 pressure developers for cost optimization. |

Preview Before You Purchase

Smulders Group Porter's Five Forces Analysis

This preview showcases the complete Smulders Group Porter's Five Forces Analysis, offering a thorough examination of competitive pressures within their industry. You're looking at the actual document, providing insights into the bargaining power of buyers and suppliers, the threat of new entrants and substitutes, and the intensity of rivalry among existing competitors. The document you see is your deliverable. It’s ready for immediate use—no customization or setup required.

Rivalry Among Competitors

Number and Capability of Competitors

Smulders faces intense competition from several large, established international players in the offshore wind sector. Companies like Sif Group, Bladt Industries, and EEW, among others, possess substantial engineering expertise and fabrication capacity for large-scale steel structures, directly challenging Smulders' market position.

The market for offshore wind foundations and substations is characterized by a limited number of highly specialized fabricators. For instance, in 2024, the demand for monopiles and jacket foundations remained robust, with major players like Sif Group reporting strong order books, indicating a concentrated competitive environment where only a few firms can handle the sheer scale and technical complexity of these projects.

High Fixed Costs and Capacity Utilization

The steel fabrication sector, particularly for large-scale projects like offshore wind foundations, demands significant upfront investment in specialized facilities, heavy-duty machinery, and a highly skilled workforce. These substantial fixed costs create a barrier to entry and pressure companies to operate at high capacity.

Smulders, like its peers, faces intense rivalry stemming from the need to achieve high capacity utilization to offset these fixed costs. This drives aggressive bidding and competition for every available project, as underutilization directly impacts profitability.

In 2023, the global offshore wind market saw significant investment, with new projects totaling over 15 GW being commissioned, creating demand for fabrication services. However, the industry's capacity is still catching up, leading to fierce competition among established players for these lucrative contracts.

Market Growth Rate and Strategic Importance

The offshore wind sector is booming, with projections indicating a substantial rise in installed capacity, reaching over 100 GW globally by 2025. This rapid expansion intensifies competition among established players like Smulders Group, as they vie for a larger slice of this growing market.

This dynamic environment fosters strategic moves, including mergers and acquisitions. For instance, Smulders Group’s acquisition of HSM Offshore Energy in 2023 highlights the trend of consolidation and capability enhancement driven by the sector's growth, aiming to bolster market position and secure future projects.

Product Differentiation and Specialization

Smulders distinguishes itself by concentrating on complex, heavy, and technically demanding steel structures, providing comprehensive engineering, construction, fabrication, and assembly services. This focus on turnkey solutions, particularly in specialized sectors like offshore wind foundations and substations, effectively reduces direct competition based purely on cost.

Their specialization allows Smulders to command a premium for their expertise and the high quality of their integrated offerings. For instance, in the offshore wind sector, the demand for highly engineered and robust foundations, often subjected to extreme environmental conditions, means that clients prioritize reliability and technical capability over the lowest price. Smulders' proven track record in delivering such projects reinforces this competitive advantage.

- Specialized Expertise: Smulders focuses on complex steel structures for demanding industries.

- Turnkey Solutions: Offers integrated services from engineering to assembly.

- Mitigating Price Rivalry: Specialization in areas like offshore wind foundations reduces direct price competition.

- Client Prioritization: Customers value technical capability and reliability over cost alone in specialized sectors.

Integration within Larger Groups

Being part of the larger Eiffage Group, Smulders gains significant advantages in competitive rivalry. This integration provides access to substantial financial backing and a wider array of resources, enabling Smulders to undertake larger, more complex projects. For instance, Eiffage's robust financial position, evidenced by its 2023 revenue of €21.2 billion, allows Smulders to invest more heavily in advanced fabrication technologies and expand its operational capacity. This can translate into more competitive bidding strategies against rivals who may not have the same level of group support.

The integration also means Smulders can leverage Eiffage's established reputation and extensive client network. This can lead to:

- Enhanced project pipeline: Access to Eiffage's broader project portfolio can secure a more consistent flow of work for Smulders.

- Improved bidding power: The financial stability of Eiffage allows Smulders to potentially offer more aggressive pricing or more comprehensive solutions.

- Synergies in expertise: Shared knowledge and resources within the Eiffage Group can lead to more efficient operations and innovative approaches.

Intense Rivalry Shapes Offshore Wind Foundation Market

Competitive rivalry for Smulders Group is fierce, driven by a concentrated market of specialized fabricators like Sif Group and Bladt Industries. These competitors possess significant engineering expertise and fabrication capacity for large-scale offshore wind structures. The high fixed costs associated with specialized facilities and machinery pressure all players to maintain high capacity utilization, leading to aggressive bidding for projects. In 2024, the demand for monopiles and jacket foundations remained strong, with major players reporting robust order books, underscoring the intense competition for these complex projects.

| Competitor | Key Offerings | 2024 Market Presence Indicators |

|---|---|---|

| Sif Group | Monopiles, Transition Pieces, Platforms | Strong order book, significant fabrication capacity |

| Bladt Industries | Foundations, Substructures, Offshore Substations | Active in European offshore wind projects |

| EEW | Monopiles, Transition Pieces, Offshore Wind Towers | Established player with large-scale fabrication capabilities |

SSubstitutes Threaten

Alternative Materials for Foundations

While steel dominates offshore wind foundations like jackets and transition pieces, concrete and hybrid designs are emerging as viable substitutes, especially for specific foundation types and varying water depths. The increasing sophistication of concrete formulations for large-scale marine applications presents a growing threat.

Evolution of Offshore Wind Technology

The rise of floating offshore wind technology presents a potential threat of substitution by altering the required expertise and infrastructure. While Smulders Group has a presence in this emerging sector, a swift and widespread adoption of floating foundations could necessitate significant investment in new fabrication and assembly capabilities, potentially diverting resources from their established fixed-bottom operations.

Onshore Wind and Other Renewable Energy Sources

Onshore wind and solar photovoltaic (PV) are significant substitutes for offshore wind from an energy generation standpoint. The cost-competitiveness of these alternatives directly influences investment flows into the offshore wind sector. For instance, in 2024, the levelized cost of energy (LCOE) for onshore wind continued to decrease, with some projects achieving figures as low as $25-30 per megawatt-hour (MWh), making it a very attractive option compared to offshore wind's higher initial capital outlays.

Furthermore, the speed of deployment for onshore renewables presents another challenge. Solar PV projects, in particular, can often be brought online much faster than large-scale offshore wind farms, which require extensive infrastructure development and longer lead times. This rapid deployment capability can divert capital and resources that might otherwise be allocated to offshore wind, indirectly impacting the demand for Smulders' specialized services in the offshore sector.

Modular Construction and Standardization

The increasing modularization and standardization of offshore wind components pose a potential threat by reducing the demand for highly specialized, complex steel fabrications. This shift could open the door for a wider array of manufacturers to compete, potentially eroding Smulders' premium on intricate structural engineering. For instance, the growing adoption of standardized foundation designs, like monopiles, means less differentiation in fabrication complexity.

However, Smulders' deep-seated expertise in engineering and fabricating highly complex, bespoke steel structures remains a significant competitive advantage. This capability is crucial for projects requiring unique solutions, such as jacket foundations or specialized transition pieces. In 2024, the offshore wind sector continued to see innovation in foundation types, with some developers exploring more complex designs to suit specific seabed conditions, thereby reinforcing the value of specialized fabricators.

The threat of substitutes is further amplified as technological advancements make simpler, more standardized installation methods more viable. This could lead to a greater reliance on readily available, less complex components. For example, advancements in floating wind technology are also driving new approaches to platform construction, which may offer alternative solutions to traditional fixed-bottom foundations.

- Standardization Risk: Increased modularity in offshore wind components could lower the barrier to entry for competitors.

- Value Shift: The market might increasingly value assembly and integration over complex fabrication.

- Smulders' Advantage: Expertise in complex, customized steel structures remains a key differentiator.

- Market Trends: 2024 saw continued development in diverse foundation types, some favoring specialization.

Energy Storage and Grid Improvements

Investments in advanced energy storage, like utility-scale battery systems, can lessen the need for new offshore wind capacity by smoothing out intermittent supply. For instance, the global energy storage market reached an estimated USD 230 billion in 2023, with projections indicating significant growth. This trend could reduce the demand for new foundations and substations Smulders Group supplies.

Improvements in grid infrastructure, such as enhanced transmission capabilities and smart grid technologies, also offer alternatives to building more offshore wind farms. The International Energy Agency reported in 2024 that grid modernization is a key focus for energy security and decarbonization efforts worldwide. Such upgrades might decrease the reliance on large-scale renewables, impacting Smulders Group's long-term project pipeline.

- Energy Storage Market Growth: The global energy storage market was valued at approximately USD 230 billion in 2023, with substantial expected expansion.

- Grid Modernization Focus: International bodies like the IEA are emphasizing grid improvements as crucial for energy transition in 2024.

- Impact on Demand: These advancements in storage and grid technology act as substitutes for new offshore wind farm development, potentially affecting Smulders Group's future order book.

Offshore Wind Faces Stiff Competition from Energy Alternatives

Onshore wind and solar PV are significant substitutes for offshore wind in energy generation. In 2024, onshore wind's decreasing levelized cost of energy (LCOE), with some projects reaching $25-30/MWh, makes it highly competitive against offshore wind's higher initial capital costs. Solar PV's rapid deployment capability also diverts capital and resources from offshore wind projects.

Technological advancements in energy storage and grid infrastructure present indirect substitution threats. The global energy storage market, valued around USD 230 billion in 2023, is expanding rapidly. Furthermore, the International Energy Agency highlighted grid modernization as a key 2024 focus for energy security, potentially reducing the need for new offshore wind capacity.

| Substitute Technology | Key Characteristic | 2024 Relevance/Data Point |

| Onshore Wind | Cost Competitiveness | LCOE as low as $25-30/MWh |

| Solar PV | Deployment Speed | Faster project commissioning than offshore wind |

| Energy Storage | Grid Stability | Global market ~USD 230 billion (2023) with strong growth |

| Grid Modernization | Transmission Efficiency | Key focus for energy security (IEA, 2024) |

Entrants Threaten

High Capital Investment

Smulders Group operates in a sector where the sheer cost of entry is a formidable deterrent. For instance, establishing a fabrication yard capable of producing massive offshore wind turbine foundations, like the jackets and monopiles Smulders specializes in, demands hundreds of millions of euros. This includes acquiring land, building specialized workshops, investing in heavy-duty cranes, and procuring advanced welding and cutting technology.

Extensive Expertise and Certifications

Smulders, as part of the Smulders Group, possesses extensive expertise in the engineering, construction, and assembly of highly complex steel structures, a capability honed over many years. This deep technical knowledge, coupled with a proven history of successful project execution, acts as a significant deterrent for potential new entrants. They would need to invest heavily in acquiring comparable skills and obtaining crucial industry certifications, a substantial hurdle.

Regulatory Hurdles and Environmental Approvals

The offshore wind sector presents substantial regulatory hurdles and demanding environmental approval processes. New entrants must contend with intricate legal frameworks and extensive environmental impact assessments, which are often lengthy and resource-intensive. For instance, the permitting process for offshore wind farms can span several years, with significant investment required for studies and compliance, thereby increasing the barrier to entry.

Established Customer Relationships and Reputation

Smulders Group, a dominant force in the offshore wind sector, boasts over €1 billion in orders for 2024, underscoring its deep-seated relationships with key industry players and a robust reputation built over years of successful project execution. This established trust is a significant barrier for any potential new entrant aiming to penetrate the market.

Newcomers would face considerable challenges in replicating Smulders' existing network of major developers and demonstrating the reliability and expertise necessary to win large, complex, and high-value contracts. The lengthy process of building credibility in this specialized field is a substantial hurdle.

- Established Trust: Smulders' long-standing partnerships with leading offshore wind developers create a significant competitive moat.

- Reputational Capital: A proven track record of delivering complex projects instills confidence, making it difficult for new entrants to gain traction.

- Market Access: Securing access to high-value contracts requires a level of established credibility that new companies typically lack.

- High Entry Barriers: The specialized nature of the industry and the capital required to compete effectively deter many potential new entrants.

Supply Chain Integration and Access to Specialized Suppliers

Smulders' established expertise in managing intricate supply chains for specialized offshore wind components presents a significant hurdle for newcomers. Their capacity to secure critical materials and components from a network of trusted, often niche, suppliers is a well-honed capability. For instance, in 2023, Smulders continued to leverage its deep relationships with key steel fabricators and component manufacturers, ensuring timely delivery for projects like the Hollandse Kust West project.

The recent acquisition of HSM Offshore Energy in late 2023 further bolsters Smulders' system integration prowess. This move allows them to bring more of the value chain in-house, enhancing control over project execution and quality. New market entrants will face considerable difficulty replicating this level of integration and securing access to the same specialized, high-quality suppliers that Smulders has cultivated over years of operation.

- Supply Chain Complexity: Smulders excels at navigating the complex logistics and sourcing requirements for large-scale offshore wind projects, a capability difficult for new entrants to replicate quickly.

- Specialized Supplier Access: The group's long-standing relationships with niche suppliers of critical components and materials create a significant barrier to entry.

- System Integration Capabilities: Smulders' strategic acquisition of HSM Offshore Energy in 2023 significantly enhances its ability to integrate various project components and systems, a key differentiator.

- Barriers to Entry: New companies would struggle to establish the necessary supplier networks and internal integration processes to compete effectively with Smulders' established operational model.

Offshore Wind: High Barriers Protect Established Players

The threat of new entrants for Smulders Group is considerably low due to extremely high capital requirements and specialized knowledge. Building offshore wind foundations, for example, demands hundreds of millions in investment for fabrication yards and advanced technology. Newcomers also face significant hurdles in acquiring the deep engineering expertise and industry certifications that Smulders possesses, a testament to years of dedicated development.

Regulatory and environmental approval processes further elevate entry barriers, often taking years and substantial resources to navigate. Smulders' established trust and relationships with major offshore wind developers, evidenced by over €1 billion in orders for 2024, create a formidable moat. Replicating this credibility and securing high-value contracts is a major challenge for any new player.

| Barrier Type | Description | Impact on New Entrants |

|---|---|---|

| Capital Requirements | Hundreds of millions of euros for fabrication yards, cranes, and technology. | Extremely High |

| Technical Expertise | Years of experience in complex steel structures and project execution. | Very High |

| Regulatory & Environmental Approvals | Lengthy, resource-intensive permitting processes. | High |

| Established Relationships & Reputation | Over €1 billion in 2024 orders; deep trust with key developers. | Very High |

| Supply Chain & System Integration | Complex supplier networks and enhanced integration via HSM acquisition (late 2023). | High |

Porter's Five Forces Analysis Data Sources

Our Smulders Group Porter's Five Forces analysis is built upon a foundation of publicly available company filings, industry-specific market research reports, and expert commentary from financial analysts. This comprehensive approach ensures a robust understanding of competitive pressures.