Iluka Boston Consulting Group Matrix

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Iluka Bundle

See the Bigger Picture

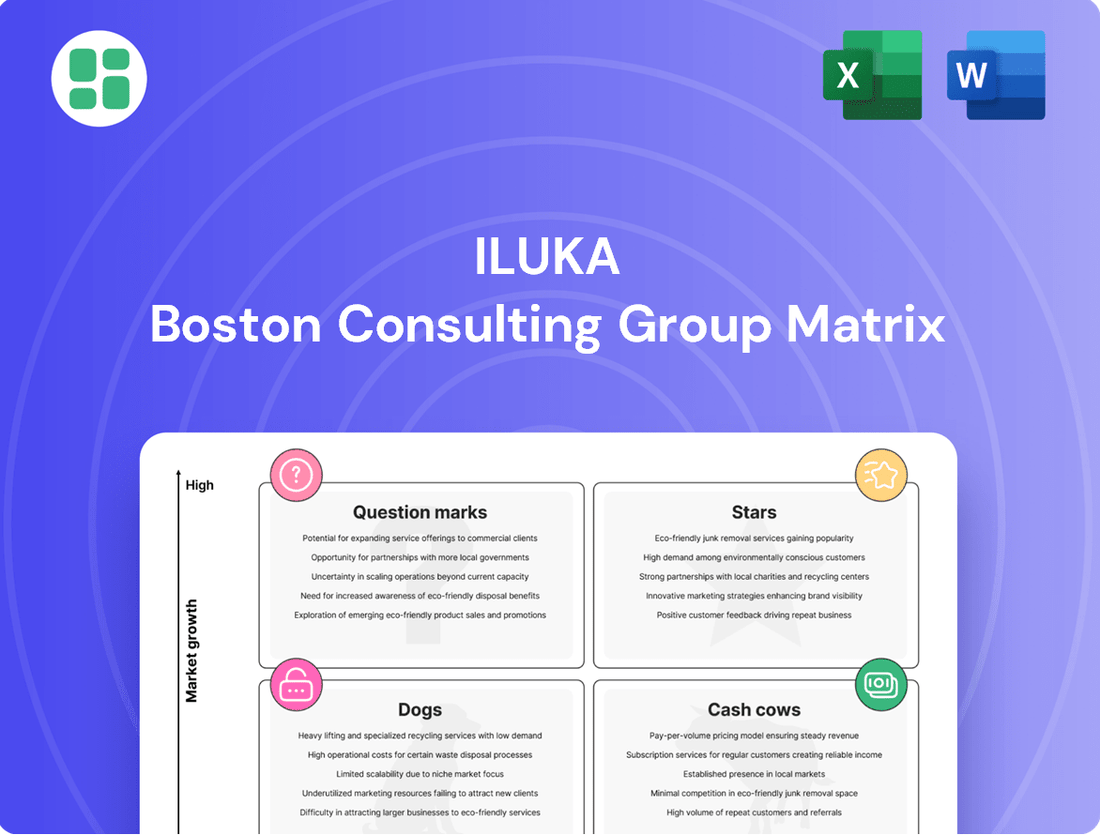

Curious about Iluka's strategic positioning? This glimpse into their BCG Matrix highlights key product categories, but the real power lies in understanding the nuances of their Stars, Cash Cows, Dogs, and Question Marks. Purchase the full report for a comprehensive breakdown and actionable insights to drive your own strategic decisions.

Stars

Eneabba Rare Earths Refinery Output

Iluka's Eneabba Rare Earths Refinery, slated for full commissioning in 2027, is set to become a major Western producer of separated light and heavy rare earth oxides. This facility will supply critical elements like dysprosium and terbium, essential for technologies such as electric vehicles and wind turbines.

The global demand for rare earths is escalating, with the market projected to reach approximately $10 billion by 2030, fueled by the green energy transition. Eneabba's output is positioned as a Star in Iluka's BCG Matrix due to its strategic role in meeting this demand and its potential to capture significant market share in a high-growth sector.

Premium Zircon Products

Iluka's premium zircon products are crucial for demanding industries such as ceramics, refractories, and fused zirconia, where their quality is paramount. These specialized applications ensure a stable, high-value market for Iluka's offerings.

Despite some headwinds in the broader mineral sands sector during 2024, the demand for premium zircon, particularly for its specialized industrial applications, has remained strong. This resilience highlights the product's essential nature in niche markets.

Iluka's ongoing commitment to product quality and nurturing key market relationships solidifies its leading position in this segment. This strategic focus supports a market characterized by consistent, though sometimes fluctuating, growth, underscoring the long-term value of their premium zircon.

High-Grade Rutile & Synthetic Rutile

Iluka's high-grade rutile and synthetic rutile are vital for industries like pigment manufacturing, aerospace, and medical devices. These titanium feedstocks are essential for creating durable and high-performance products.

While the titanium dioxide market can be volatile, the fundamental requirement for advanced materials provides a stable, long-term demand. For instance, the global titanium dioxide market was valued at approximately $28.5 billion in 2023 and is projected to grow, underscoring the consistent need for these feedstocks.

Iluka's strong market position and efficient production processes for these critical minerals place them as a leader in their respective industrial applications. Their ability to reliably supply these high-quality materials is a significant competitive advantage.

Balranald Project Production

The Balranald project, anticipated to begin operations in the latter half of 2025, is positioned to supply high-grade zircon and possibly rare earth concentrates. This venture utilizes advanced underground mining techniques, aiming for efficient and potentially cost-effective extraction.

Entering a market characterized by robust demand for critical minerals, Balranald's innovative approach could quickly elevate its production to Star status. The project's success hinges on its ability to deliver high-quality output reliably.

Key aspects of the Balranald project include:

- Expected commissioning in H2 2025.

- Production of high-grade zircon and potential rare earth concentrates.

- Utilizes innovative underground mining technology.

- Addresses strong market demand for critical minerals.

Strategic Diversification into Critical Minerals

Iluka's strategic diversification into critical minerals, particularly rare earths, marks it as a Star in the BCG Matrix. This move taps into high-growth sectors vital for the global energy transition. For instance, Iluka's investment in the Eneabba Rare Earths refinery in Western Australia, projected to commence operations in late 2024 or early 2025, signifies a substantial commitment to this burgeoning market. This refinery is expected to process feedstock from Iluka's own operations and potentially third-party suppliers, positioning the company as a key player in the Western world's rare earths supply chain. The global demand for rare earths, driven by electric vehicles and wind turbines, is forecast to grow significantly, with some estimates suggesting a near doubling by 2030.

- Strategic Pivot: Iluka is actively expanding beyond its traditional mineral sands, targeting critical minerals like rare earths.

- Growth Sectors: This diversification positions Iluka to capitalize on the rapidly expanding markets for materials essential to energy transition and advanced technologies.

- Market Leadership: By investing in projects like the Eneabba Rare Earths refinery, Iluka aims to secure a leading role in the critical minerals supply chain.

- Financial Outlook: The company's commitment to rare earths is supported by anticipated strong demand and favorable market dynamics for these essential commodities.

Iluka's Strategic Moves in the Rare Earths Market

Iluka's rare earths venture, particularly the Eneabba refinery, is a prime example of a Star in the BCG Matrix. This strategic expansion into a high-growth sector, driven by global demand for materials in electric vehicles and wind turbines, positions the company for significant market capture. The refinery's projected full commissioning in 2027, with initial operations earlier, underscores Iluka's commitment to becoming a key Western producer of critical rare earth oxides.

The Balranald project, set to commence operations in the latter half of 2025, also fits the Star profile. Its focus on high-grade zircon and potential rare earth concentrates, coupled with innovative mining techniques, targets robust market demand. This project's ability to deliver quality output reliably is crucial for its Star trajectory.

Iluka's premium zircon operations, while perhaps not experiencing explosive growth, are a strong Cash Cow. The consistent demand from specialized industrial applications like ceramics and refractories ensures stable, high-value revenue streams. The company's focus on quality and market relationships reinforces its leadership in this segment.

High-grade rutile and synthetic rutile, vital for pigment manufacturing and aerospace, represent another Cash Cow for Iluka. Despite potential volatility in the broader titanium dioxide market, the fundamental need for these advanced materials ensures long-term demand, supported by a global market valued at approximately $28.5 billion in 2023.

| Product Segment | BCG Category | Key Market Drivers | Iluka's Position | 2024/2025 Outlook |

|---|---|---|---|---|

| Rare Earths (Eneabba Refinery) | Star | Green energy transition, EV and wind turbine demand | Emerging Western producer, strategic investment | Commissioning expected late 2024/early 2025, full commissioning 2027 |

| Zircon (Premium) | Cash Cow | Ceramics, refractories, fused zirconia | Leading supplier, strong market relationships | Resilient demand in niche markets, stable high-value |

| Rutile/Synthetic Rutile | Cash Cow | Pigment manufacturing, aerospace, medical devices | Efficient production, reliable supplier | Long-term demand in advanced materials, TiO2 market ~$28.5bn (2023) |

| Balranald Project | Star (Potential) | Critical minerals demand, innovative mining | New entrant, high-grade output | Expected operations H2 2025 |

What is included in the product

The Iluka BCG Matrix categorizes business units by market share and growth rate, guiding strategic decisions for each quadrant.

Iluka's BCG Matrix provides a clear, one-page overview, instantly relieving the pain of strategic uncertainty by placing each business unit in its optimal quadrant.

Cash Cows

Established Zircon Production (Jacinth-Ambrosia & Cataby)

Iluka's established zircon production from Jacinth-Ambrosia and Cataby are prime examples of Cash Cows within its portfolio. These operations are characterized by their long history, consistent output, and efficient infrastructure, allowing them to generate substantial and reliable cash flow.

In 2024, these mature assets continued to be a bedrock of Iluka's financial performance. Despite some market volatility, the Jacinth-Ambrosia and Cataby mines demonstrated resilience, maintaining healthy profit margins and contributing significantly to the company's overall revenue generation.

Long-Term Synthetic Rutile Contracts

Iluka's long-term synthetic rutile contracts function as classic Cash Cows within the BCG matrix. These take-or-pay agreements guarantee a baseline of revenue, insulating Iluka from short-term market fluctuations in titanium dioxide feedstocks.

This contractual stability translates into predictable cash flow, allowing Iluka to efficiently generate funds from its synthetic rutile operations. For instance, in the first half of 2024, Iluka reported that its synthetic rutile segment continued to benefit from these secure offtake arrangements, underpinning consistent financial performance.

Mature Rutile Operations

Iluka's natural rutile operations are a prime example of a Cash Cow. These mature assets, focused on producing high-quality titanium dioxide feedstock, consistently generate substantial cash flow. In 2024, Iluka reported significant rutile production volumes, contributing to its strong financial performance.

Despite some market pressures from international competitors, Iluka's premium rutile feedstock commands resilient pricing due to its superior quality and the consistent demand from its established industrial client base. This stability ensures a predictable revenue stream for the company.

These established mining and processing facilities require minimal new capital expenditure for expansion or market development, allowing the substantial cash generated to be reinvested elsewhere or returned to shareholders. This low investment need is a hallmark of a true Cash Cow.

Existing Mineral Sands Portfolio

Iluka's existing mineral sands operations, encompassing zircon, rutile, and synthetic rutile, function as a significant cash cow within its BCG matrix. This portfolio benefits from Iluka's established global market leadership and deep operational expertise.

Despite facing some market headwinds, these operations consistently deliver strong EBITDA margins. For instance, in the first half of 2024, Iluka reported a robust EBITDA margin for its Mineral Sands segment, underscoring the profitability of these established assets.

- Global Market Leadership: Iluka holds a leading position in the global mineral sands market, providing a competitive advantage.

- Operational Expertise: Decades of experience in mining and processing mineral sands ensure efficient and cost-effective production.

- Profitability: The portfolio continues to generate strong EBITDA margins, contributing significantly to Iluka's overall financial performance.

- Focus on Efficiency: Iluka prioritizes maintaining and optimizing these existing assets to maximize cash generation and shareholder returns.

Efficient Processing Infrastructure

Iluka's efficient processing infrastructure, including its Narngulu mineral separation plant and synthetic rutile kilns (SR1/SR2), exemplifies its cash cow business. These facilities represent substantial, mature capital investments that consistently generate strong returns. Their operational efficiency translates into cost-effective production of diverse mineral sands products, underpinning the profitability of Iluka's core operations.

These established processing assets are critical to Iluka's success, enabling high-volume, low-cost processing of mined materials. For instance, Iluka reported that its synthetic rutile production capacity is approximately 240,000 tonnes per annum, a testament to the scale and efficiency of its infrastructure. This robust processing capability directly supports the overall financial health and cash generation of the mineral sands segment.

- Narngulu Mineral Separation Plant: A cornerstone of Iluka's processing capabilities, handling a significant volume of mineral sands.

- Synthetic Rutile Kilns (SR1/SR2): These facilities are vital for producing synthetic rutile, a key product with established market demand, contributing significantly to cash flow.

- Cost Efficiency: The established nature and operational optimization of these plants allow for lower per-unit production costs, enhancing profit margins.

- High-Volume Output: Their capacity supports consistent, large-scale production, ensuring reliable cash generation from mineral sands sales.

Iluka's Cash Cows: Jacinth-Ambrosia & Cataby Thrive

Iluka's established zircon and rutile operations, particularly those at Jacinth-Ambrosia and Cataby, are classic cash cows. These mature assets benefit from existing infrastructure and operational expertise, consistently generating substantial and predictable cash flow with minimal reinvestment needs. In 2024, these operations continued to be a financial bedrock for Iluka, demonstrating resilience and strong EBITDA margins despite market fluctuations.

| Asset/Operation | Product | 2024 Performance Indicator | Significance as Cash Cow |

|---|---|---|---|

| Jacinth-Ambrosia | Zircon | Consistent production, strong demand | Reliable cash generation, mature asset |

| Cataby | Zircon, Rutile | High EBITDA margins reported | Stable revenue stream, operational efficiency |

| Synthetic Rutile Contracts | Synthetic Rutile | Take-or-pay agreements | Predictable cash flow, insulation from market volatility |

| Natural Rutile Operations | Natural Rutile | Premium pricing, established client base | Consistent revenue, low capital expenditure needs |

Preview = Final Product

Iluka BCG Matrix

The Iluka BCG Matrix preview you are viewing is the exact, unwatermarked, and fully formatted document you will receive upon purchase. This comprehensive strategic tool is ready for immediate download and application in your business planning. You can confidently use this preview as a direct representation of the high-quality, analysis-ready report that will be yours to leverage for critical decision-making.

Dogs

Zircon-in-Concentrate (ZIC) Production Run-Down

Iluka has signaled a strategic shift by planning a run-down of its Zircon-in-Concentrate (ZIC) production. This approach indicates that ZIC is viewed as a product line with diminishing strategic significance and potentially reduced profitability, prompting its gradual discontinuation.

With minimal output anticipated for 2026, these operations are likely being scaled back due to limited future growth potential or market share. This strategic decision aligns with a focus on optimizing resource allocation towards more promising business segments within Iluka's portfolio.

Lower-Value Titanium Dioxide Products (e.g., HyTi)

Iluka Resources also offers lower-value titanium dioxide products, such as HyTi, which command a lower price point compared to premium rutile. If these products also possess a small market share and are subject to significant competitive pressures, they would likely be categorized as Dogs within the BCG Matrix.

For these Dog products, Iluka's strategy would typically involve minimizing further investment and considering divestment if their performance remains consistently weak. This approach aims to free up capital and resources for more promising segments of the business.

Legacy Exploration Assets with Limited Potential

Iluka Resources, like many established mining companies, likely holds legacy exploration assets that fall into the Dogs category of the BCG matrix. These are older exploration tenements or minor, undeveloped deposits that have been retained but show consistently low prospectivity or uneconomic grades. For instance, in 2024, Iluka's exploration expenditure across its portfolio was $39 million, a portion of which would have been allocated to maintaining these less promising areas.

These "dog" assets tie up valuable capital in holding costs and ongoing exploration expenditure without contributing meaningfully to current or future production. This can represent a drain on resources that could be better deployed in more promising ventures. The company's strategy for such assets typically involves a rigorous review process to determine if they warrant continued investment or if divestment or a write-down is the more prudent financial decision.

Non-Core By-products with Minimal Market Demand

Iluka Resources, a major mineral sands producer, generates various by-products during its operations. While some, like activated carbon, have established markets, others may face limited demand. If by-products such as gypsum or iron concentrate consistently exhibit very low market interest and yield revenues that don't offset their processing and handling expenses, they would fall into the Non-Core By-products category within a BCG Matrix framework. For Iluka, this classification would signal a need to intensely focus on reducing the costs associated with these materials or exploring entirely new applications to make them economically viable.

For instance, during 2023, Iluka reported that while its primary mineral sands products like zircon and titanium dioxide feedstock were strong performers, certain minor by-products contributed minimally to overall revenue. While specific figures for individual by-products with negligible demand are not always granularly disclosed, the company's operational reports often highlight efforts to optimize the recovery and sale of all materials. The strategy for these non-core items would prioritize cost efficiency, potentially through integrated waste management or by-product synergy with other industries, rather than market development.

- By-product Classification: Non-Core By-products with Minimal Market Demand

- Examples: Activated carbon, gypsum, iron concentrate (if demand is consistently low)

- Strategic Focus: Cost minimization, finding alternative uses, or disposal optimization

- Financial Implication: Negligible revenue relative to handling costs, requiring efficiency gains

Inefficient or High-Cost Older Operations

Small, legacy mining or processing units can become uneconomical. This often happens when ore grades decrease, operational costs rise, or environmental rules become stricter. For instance, if a mine's production cost per tonne significantly exceeds the market price of the commodity, it falls into this category.

While not always explicitly labeled as such in Iluka's current public disclosures, these inefficient operations would typically be candidates for phasing out or being put on care and maintenance. Continuing to operate them often drains resources, acting as a cash trap that could be better invested elsewhere.

- Declining Ore Grades: A mine experiencing a drop in the concentration of valuable minerals makes extraction less profitable.

- Increased Operational Costs: Factors like higher energy prices or labor expenses can erode margins.

- Environmental Compliance: Meeting new or more stringent regulations can add significant capital and operating expenditures.

- Market Price Volatility: A sustained low commodity price environment can render previously viable operations unprofitable.

Iluka's "Dogs": Assets Facing Dim Prospects

Iluka's Zircon-in-Concentrate (ZIC) production is being planned for a run-down, indicating it's likely a Dog in the BCG Matrix. This means it has low market share and low growth potential, leading to minimal output expected by 2026.

Similarly, lower-value titanium dioxide products like HyTi, if facing intense competition and low market share, would also be classified as Dogs. For such products, Iluka's strategy would focus on minimizing investment and potentially divesting to reallocate capital to more promising business areas.

Legacy exploration assets with consistently low prospectivity or uneconomic grades also fit the Dog category. In 2024, Iluka's exploration expenditure was $39 million, a portion of which likely maintained these less promising areas, tying up capital without significant returns.

These "dog" assets, including potentially uneconomical legacy mining or processing units due to declining ore grades or increased operational costs, represent a drain on resources. Iluka's strategy for these would involve rigorous review for divestment or write-down to optimize resource allocation.

| BCG Category | Iluka Example | Strategic Implication | 2024 Data Point |

| Dogs | Zircon-in-Concentrate (ZIC) Production | Minimize investment, consider divestment | Planned run-down of ZIC production |

| Dogs | Low-value TiO2 products (e.g., HyTi) | Focus on cost efficiency, potential divestment | Low market share and high competition |

| Dogs | Legacy Exploration Assets | Rigorous review, divestment, or write-down | $39 million exploration expenditure in 2024 |

| Dogs | Uneconomical Mining/Processing Units | Phase out or place on care and maintenance | Declining ore grades, increased operational costs |

Question Marks

Eneabba Rare Earths Refinery (Pre-Commissioning Phase)

The Eneabba Rare Earths Refinery, currently in its pre-commissioning phase, represents a significant investment for Iluka Resources. While the project holds substantial long-term promise, its current stage means it's a capital drain without immediate revenue generation.

The global market for separated rare earth oxides is experiencing robust growth, a key factor positioning Eneabba as a potential Star. However, Iluka's current market share in this refined product segment is nil, highlighting the project's future-oriented nature.

The success of this multi-billion dollar venture, with Iluka having committed approximately AUD 1.2 billion to the project as of early 2024, critically depends on its successful commissioning, targeted for 2027, and the establishment of firm offtake agreements.

Balranald Project (Pre-Commissioning Phase)

The Balranald project, a substantial capital undertaking for Iluka, is currently in its pre-commissioning phase, focusing on advanced underground mining for zircon and rare earths. This innovative approach targets a market experiencing robust demand.

As of mid-2025, Balranald has no current market share because it is still awaiting its commercial operational start in the second half of 2025. This lack of established presence, coupled with its significant investment, positions it as a Question Mark within Iluka's BCG matrix.

The project's success hinges on a smooth ramp-up and its ability to capture market share in a competitive environment. Iluka's investment in Balranald reflects a strategic bet on future growth, but its current status necessitates careful monitoring and execution.

Wimmera Project (Feasibility & Development)

The Wimmera project in Victoria, Australia, is a significant undertaking for Iluka Resources, focusing on its substantial rare earths and mineral sands deposits. Currently, the project is deep in the definitive feasibility study stage, with a particular emphasis on rare earths extraction and processing. This strategic focus aligns with the burgeoning global demand for rare earth elements, crucial for technologies like electric vehicles and renewable energy.

While Wimmera sits within a high-growth sector, it is still in the development phase and is several years away from commencing production. Consequently, it currently contributes zero market share to Iluka's portfolio. Iluka is actively exploring innovative processing solutions, especially for the Wimmera zircon component, highlighting the considerable capital investment required to unlock the project's full potential and bring its resources to market.

New Rare Earths Exploration & Development

Beyond its established Eneabba refinery, Iluka Resources is actively pursuing new rare earth exploration and development projects. These initiatives aim to secure future supply and diversify feedstock sources, potentially including third-party opportunities. This strategic move positions Iluka to capitalize on the growing demand for critical minerals essential for advanced technologies.

These early-stage exploration ventures are inherently high-risk, high-reward. While operating in a market projected for significant growth, Iluka's current market share in these new areas is negligible. Substantial capital investment is necessary to assess and prove the commercial viability of these deposits, making them a significant drain on cash resources in the short term.

- Exploration Focus: Iluka is exploring deposits beyond Eneabba, seeking new sources of rare earth elements.

- Market Position: These new ventures are in a high-growth market but currently hold low or no market share.

- Investment Needs: Significant capital is required to prove commercial viability, indicating substantial risk and cash consumption.

- Strategic Importance: These projects represent Iluka's commitment to future growth and diversification in the rare earths sector.

Advanced Material Processing Innovations

Iluka Resources is actively investing in advanced material processing, a key component of its strategic growth. This includes significant research and development into novel technologies aimed at improving efficiencies and creating new product forms. For instance, their exploration of an underground mining method at the Balranald operation exemplifies this focus on innovation.

These advancements, while promising for future market needs and operational advantages, are inherently capital-intensive. The commercial viability of these cutting-edge technologies often remains uncertain until they are successfully scaled and proven in real-world applications. This places them firmly in the question mark quadrant of the BCG matrix, representing strategic bets on future potential.

- Investment in Advanced Processing: Iluka's commitment to R&D for new material processing technologies.

- Balranald Underground Mining: A specific example of innovation in operational methods.

- Capital Intensity and Risk: High upfront costs and uncertain returns until scaled.

- Strategic Future Focus: Targeting future market demands and operational competitive advantages.

High-Growth Bets: Question Marks in the Making

Iluka's Balranald and Wimmera projects, along with its broader exploration initiatives, are classic examples of Question Marks in the BCG matrix. These ventures are in high-growth markets, particularly for rare earths, but currently lack established market share. Significant capital investment is being channeled into these projects, such as the AUD 1.2 billion committed to Eneabba as of early 2024, to prove their commercial viability and develop new processing technologies. Their future success hinges on effective execution, securing offtake agreements, and navigating competitive landscapes, making them strategic bets with uncertain outcomes.

BCG Matrix Data Sources

Our BCG Matrix is built on verified market intelligence, combining financial data, industry research, official reports, and expert commentary to ensure reliable, high-impact insights.