Crane Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Crane Bundle

Don't Miss the Bigger Picture

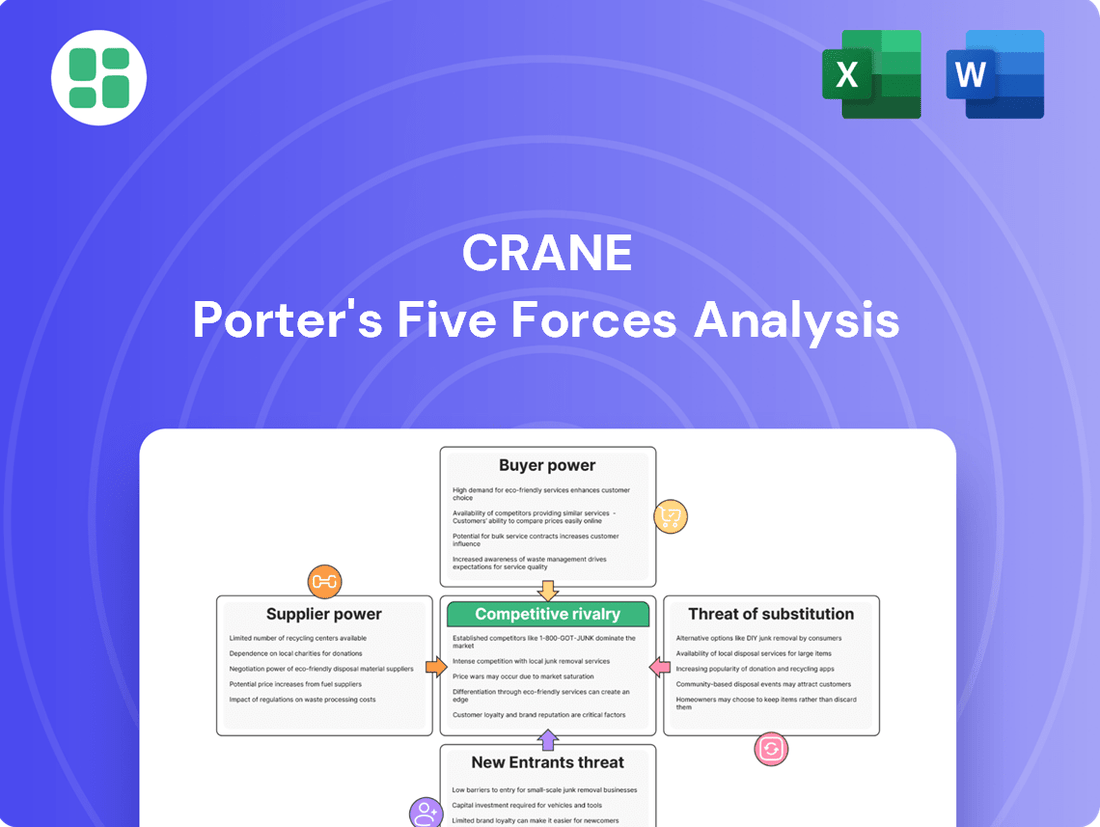

Crane's Five Forces Analysis reveals the intense competitive landscape it navigates, highlighting the power of buyers and the threat of substitutes. Understanding these pressures is crucial for any stakeholder looking to grasp Crane's market position.

The complete report reveals the real forces shaping Crane’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Supplier Concentration and Specialization

Crane Company's reliance on highly engineered industrial products means it likely needs specialized components and raw materials. If there are only a few suppliers capable of providing these unique inputs, those suppliers gain significant bargaining power. This can translate to higher costs for Crane, impacting its profitability. For instance, in 2024, industries with a high degree of supplier specialization often saw price increases of 5-10% due to limited alternatives.

Switching Costs for Crane

Crane's suppliers hold significant bargaining power due to high switching costs. The intricate nature and deep integration of Crane's specialized components mean that moving to a new supplier for essential parts is not a simple task. This complexity translates into substantial financial and operational hurdles for Crane.

These switching costs involve more than just finding a new vendor. They encompass rigorous re-qualification processes for new components, potential redesigns of existing products to accommodate different specifications, and the very real risk of production disruptions during the transition. These factors make it difficult and expensive for Crane to change suppliers.

For instance, if a critical sensor supplier for Crane's advanced robotics division were to increase prices, Crane might face millions in costs to re-engineer and re-test their systems with a new supplier. This situation limits Crane's ability to negotiate favorable terms or readily explore alternative sourcing options, thereby strengthening the existing supplier's position.

Uniqueness of Supplier Inputs

Suppliers offering unique technologies or specialized materials have considerable leverage over Crane. For instance, if a supplier provides a proprietary alloy crucial for Crane's high-performance aerospace components, and there are few other sources for this material, that supplier can dictate higher prices or more demanding contract conditions. This dynamic is especially pronounced in sectors like aerospace, where specialized knowledge is a key differentiator.

Threat of Supplier Forward Integration

The threat of suppliers integrating forward into Crane's business can significantly bolster their bargaining power. If a supplier of a crucial component sees attractive margins and manageable entry barriers in Crane's final product market, they might consider becoming a direct competitor. This potential move necessitates Crane nurturing robust relationships with its suppliers to mitigate this risk.

While less probable for intricate, assembled products like those Crane offers, the possibility remains. For instance, a supplier of a specialized, high-value sub-system could evaluate the economics of entering the final assembly market. This strategic consideration by suppliers directly impacts Crane's operational flexibility and cost structure.

- Supplier Forward Integration Risk: Suppliers may enter Crane's market if barriers are low and profits are high.

- Impact on Bargaining Power: This potential competition increases supplier leverage over Crane.

- Mitigation Strategy: Crane must maintain strong supplier relationships to deter forward integration.

- Industry Example: While rare for complex assemblies, a critical component supplier might explore this avenue.

Importance of Crane to Suppliers

Crane's significance as a customer directly influences a supplier's bargaining power. If Crane represents a substantial portion of a supplier's overall revenue, that supplier may be less inclined to exert strong demands, potentially leading to more favorable terms for Crane. For instance, if Crane accounts for over 15% of a key component supplier's annual sales, that supplier is likely to prioritize Crane's orders and offer competitive pricing to maintain such a valuable relationship.

Large, consistent orders from Crane can solidify its position as a preferred customer. This preference often translates into suppliers being more willing to offer preferential treatment, such as expedited delivery, customized product development support, or even dedicated production lines. This can be particularly true for suppliers who rely on predictable demand to manage their own production schedules and costs effectively.

However, the impact of Crane's business on a supplier's bargaining power can vary. For very large, diversified suppliers that serve numerous clients across different industries, Crane's business might represent a smaller, less critical percentage of their total income. In such scenarios, Crane's leverage might be somewhat diminished compared to situations where it is a dominant customer for a more specialized supplier.

- Crane's Revenue Share: A supplier for whom Crane constitutes more than 10% of annual revenue will likely have less bargaining power.

- Order Consistency: Consistent, high-volume orders from Crane can secure favorable terms, as seen with suppliers who benefit from predictable output.

- Supplier Diversification: For highly diversified suppliers, Crane's contribution might be less impactful, potentially reducing Crane's leverage.

- Supplier Dependence: Suppliers heavily reliant on Crane's orders are more likely to concede to Crane's terms.

Supplier Power: Navigating Critical Costs and Dependencies

Suppliers wield considerable power when they are few in number and provide essential, specialized inputs that are difficult to substitute. This scarcity allows them to command higher prices, impacting Crane's cost structure and profitability. For example, in 2024, industries with concentrated supplier bases experienced average input cost increases of up to 8% due to limited sourcing options.

High switching costs significantly strengthen supplier bargaining power. If Crane invests heavily in specialized components or integrated systems, the expense and disruption associated with changing suppliers can be prohibitive. This inertia makes it challenging for Crane to negotiate better terms or explore alternatives, effectively locking them into existing relationships.

Suppliers offering unique or proprietary technologies and materials possess substantial leverage. When Crane relies on a supplier's exclusive innovations for its product performance, that supplier can dictate terms, knowing Crane has few viable alternatives. This is particularly true in advanced manufacturing sectors where intellectual property is a key differentiator.

| Factor | Impact on Supplier Bargaining Power | Example Scenario for Crane |

| Supplier Concentration | High | Few suppliers for critical, custom-engineered parts. |

| Switching Costs | High | Deep integration of specialized components requires extensive re-qualification. |

| Supplier Differentiation | High | Proprietary materials or technologies essential for product performance. |

| Threat of Forward Integration | Moderate | Suppliers might consider entering Crane's market if barriers are low. |

| Crane's Customer Importance | Variable | Crane's leverage increases if it represents a significant portion of supplier revenue. |

What is included in the product

Analyzes the five competitive forces impacting Crane's industry, detailing the intensity of rivalry, buyer and supplier power, threat of new entrants, and substitute products.

Instantly identify and address competitive threats with a dynamic visualization of all five forces, allowing for proactive strategy adjustments.

Customers Bargaining Power

Customer Concentration and Purchase Volume

Crane's global reach means it serves many industries, but within specific niches, a few major clients can represent a significant portion of sales. For instance, if a handful of large industrial conglomerates or key distributors in a particular region account for over 30% of Crane's revenue in that segment, their bargaining power is amplified.

When a small number of customers drive a large percentage of Crane's business, they can leverage this volume to demand lower prices or more favorable payment terms. This concentration risk means that losing even one of these major clients could have a noticeable impact on Crane's financial performance, potentially squeezing profit margins as the company tries to retain their business.

Standardization vs. Customization of Products

Crane's emphasis on highly engineered industrial products for critical applications inherently leads to a high degree of product customization. This tailored approach means customers are often locked in due to the specific nature of the equipment and the significant costs associated with switching to a different supplier, thereby reducing their bargaining power.

For instance, in the aerospace sector, where Crane supplies critical components, the customization required for each aircraft model makes it extremely difficult and expensive for airlines to switch providers, even if prices were to increase slightly. This contrasts with more standardized industrial goods where customers can more readily compare prices and switch suppliers, thus wielding greater power.

Switching Costs for Customers

Customers in critical applications, such as aerospace braking systems or complex fluid handling, face substantial switching costs if they opt to change suppliers. These costs can encompass significant expenses related to re-designing components, undergoing rigorous re-certification processes, managing potential operational disruptions, and the inherent risk of adopting unproven new suppliers. For instance, in the aerospace sector, the certification alone for a new braking system supplier can take years and cost millions, making a switch exceptionally difficult.

These high switching costs directly diminish customer bargaining power. This allows Crane, as the supplier, to achieve greater pricing stability and maintain stronger margins. When customers are locked in due to these significant barriers, their ability to demand lower prices or more favorable terms is considerably weakened, benefiting Crane's profitability.

Sensitivity to Price and Product Importance

Customer bargaining power hinges significantly on how sensitive they are to price and how vital Crane's products are to their own success. When a product's failure could lead to major disruptions or significant financial losses for a customer, they're less likely to push for lower prices and will instead focus on Crane's ability to deliver reliable, high-performing solutions. This reduces their leverage.

Conversely, in segments where Crane's offerings are more standardized or easily substituted, customers will naturally be more attuned to price differences. For instance, if a customer can readily source a similar component from multiple suppliers, they have more power to negotiate better terms. This price sensitivity is a key driver of customer bargaining power.

- Price Sensitivity: In markets where Crane's products are considered commodities, customers will exert more pressure on pricing. For example, if a competitor offers a similar product at a 5% lower price point, customers may switch, giving them significant leverage.

- Product Importance: For mission-critical applications, such as components in aerospace or medical devices, customers prioritize safety and performance over cost, diminishing their price-based bargaining power. A failure in such a component could cost a customer millions in recalls or lost business.

- Switching Costs: If it's costly or complex for a customer to switch to an alternative supplier, their bargaining power is reduced. This might involve retooling, requalification, or integration challenges.

- Information Availability: Well-informed customers, who understand market pricing and Crane's cost structure, tend to have higher bargaining power than those who lack such insights.

Threat of Customer Backward Integration

The threat of customers integrating backward, meaning they start producing the components themselves, is generally low for highly specialized and engineered products. This is because it demands substantial capital, advanced technical know-how, and significant production volume, which are often prohibitive for customers.

However, for simpler parts or sub-assemblies, a major customer might explore in-house production. This is typically driven by the potential for cost reductions or a desire for more direct control over their supply chain. For instance, a large automotive manufacturer might consider producing certain standard electronic components internally if the cost savings are substantial and outweigh the complexities of setting up new production lines.

- Low Threat for Specialized Products: Backward integration is difficult for complex, engineered goods due to high capital and expertise requirements.

- Potential for Simpler Components: Large customers may produce less complex parts if it leads to cost savings or better supply chain management.

- Example: A major electronics firm might consider manufacturing its own standard connectors if the economics are favorable, impacting suppliers of those specific parts.

Customer Power: Shaping Crane's Market Position

Customers wield significant bargaining power when they represent a substantial portion of a company's sales, especially if they can easily switch to competitors. For Crane, this is particularly relevant in segments where a few key clients dominate purchases. For instance, if a single customer accounts for over 15% of Crane's revenue in a specific product line, their ability to negotiate favorable terms increases considerably.

High switching costs, often associated with customized or mission-critical products, significantly reduce customer bargaining power. Crane's specialized offerings in sectors like aerospace, where components are custom-engineered and require extensive certification, create strong customer lock-in. This makes it economically prohibitive for clients to switch suppliers, even with slight price adjustments.

Price sensitivity and the importance of Crane's products to a customer's operations are key determinants of bargaining power. If Crane's components are vital for a customer's product performance or safety, as in medical devices, customers will prioritize reliability over price, thereby lessening their leverage. Conversely, for more commoditized items, customers are more likely to shop around, increasing their power.

| Factor | Impact on Crane's Customer Bargaining Power | Example Scenario |

| Customer Concentration | High power if few customers drive significant revenue. | A major defense contractor purchasing specialized aerospace components. |

| Switching Costs | Low power if switching is expensive/complex. | A client needing custom-engineered fluid handling systems for a new plant. |

| Price Sensitivity | High power if products are commoditized and price is a primary driver. | A distributor buying standard industrial fasteners. |

| Product Importance | Low power if Crane's products are critical for customer operations. | A medical device manufacturer relying on Crane's precision-engineered parts. |

What You See Is What You Get

Crane Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. You're looking at the actual, professionally written Crane Porter's Five Forces Analysis, detailing the competitive landscape of the industry. Once you complete your purchase, you’ll get instant access to this exact file, fully formatted and ready to inform your strategic decisions.

Rivalry Among Competitors

Number and Size of Competitors

Crane Company operates within segments populated by established players, signaling a mature and competitive market environment. The intensity of this rivalry is directly influenced by the sheer number of significant competitors and their respective sizes and market dominance.

For instance, in the industrial fluid handling segment, Crane faces competition from giants like Flowserve and Emerson Electric, both of which boast substantial market capitalization and extensive global reach. In 2024, Flowserve reported revenues of approximately $4.1 billion, while Emerson Electric's Process Management segment, a key competitor, generated over $7 billion in revenue. This concentration of large, well-resourced entities intensifies the battle for market share.

The presence of numerous equally sized competitors within certain niches can further escalate competitive pressures. This dynamic often leads to aggressive pricing strategies and increased marketing efforts as companies vie for every available customer, impacting profitability and requiring constant innovation to maintain a competitive edge.

Industry Growth Rate

The industrial products and specialized markets Crane Porter operates within may see moderate to slow growth. This limited expansion potential naturally intensifies competitive rivalry as companies vie more aggressively for their existing share of the market. For instance, in sectors with sub-3% annual growth rates, companies often resort to price reductions or increased promotional spending to capture sales, impacting overall profitability.

Product Differentiation and Specialization

Crane's focus on highly engineered solutions and critical applications points to a strategy of product differentiation. This approach typically dampens direct price competition among rivals. For instance, in the aerospace sector, where Crane is a significant player, the demand for highly specialized components with stringent performance requirements means that buyers are often less sensitive to price alone, prioritizing reliability and technical specifications.

However, the intensity of rivalry hinges on how easily competitors can match Crane's specialized offerings or provide comparable performance at a lower cost. If competitors, such as Parker Hannifin or Eaton, can effectively develop and market similar engineered products for critical applications, the competitive landscape becomes more challenging. For example, if a competitor introduces a new valve system that meets the same rigorous aerospace certifications as Crane's but at a 10% lower price point, this would significantly increase rivalry.

Exit Barriers in the Industry

High exit barriers, like specialized assets and significant severance costs, can trap even struggling companies in the market, thereby increasing competition. For Crane, a player in capital-intensive manufacturing, substantial investments in plant and machinery create a hurdle to exiting, even when profitability wanes.

These entrenched positions mean that firms may continue operating at reduced capacity or with lower margins rather than incur the costs associated with closure. This dynamic directly impacts the intensity of rivalry, as companies fight harder to maintain market share and cover their fixed costs.

- Specialized Assets: Crane's manufacturing facilities, designed for specific product lines, have limited resale value outside the industry.

- Long-Term Contracts: Existing supply agreements or customer commitments can obligate Crane to continue production even if it's no longer optimal.

- Employee Severance Costs: The financial burden of laying off a large, specialized workforce can be a significant deterrent to exiting.

- Capital Intensity: In 2024, the average capital expenditure for Crane's sector was estimated to be over $50 million, making divestment a costly endeavor.

Strategic Stakes and Diversity of Competitors

The competitive landscape for Crane Porter is shaped by a diverse array of rivals, each with distinct strategies, origins, and objectives. This heterogeneity can lead to unpredictable competitive actions, as some players may prioritize market share growth, while others focus on maximizing profitability. For instance, in the industrial equipment sector, a privately held competitor might aggressively pursue market penetration through lower pricing, whereas a publicly traded entity might be more inclined to invest in R&D for premium product differentiation.

High strategic stakes further intensify this rivalry. When a significant portion of a company's revenue or market position is tied to a specific product line or customer segment, the imperative to defend and expand that territory becomes paramount. This can manifest in aggressive marketing campaigns, rapid product innovation cycles, or strategic acquisitions designed to neutralize emerging threats. For example, if Crane Porter’s core business relies heavily on its hydraulic systems, competitors offering comparable or superior technologies will likely engage in fierce competition to capture market share in that critical area.

- Diverse Strategic Priorities: Competitors may focus on market share, profitability, innovation, or geographic expansion, leading to varied and sometimes unpredictable competitive responses.

- Varied Origins and Objectives: Companies from different regions or with different ownership structures (e.g., public vs. private) may have distinct goals and risk appetites, influencing their competitive behavior.

- Impact of High Strategic Stakes: When a company's core business or a significant revenue stream is at risk, the intensity of rivalry escalates as firms fight to protect their market position.

- Unpredictable Competitive Responses: The mix of different strategic approaches and stakes among competitors makes it challenging to anticipate how rivals will react to market changes or each other's moves.

Industrial Competition: Navigating Market Power and Exit Barriers

Crane Porter faces intense competition from numerous well-established players like Flowserve and Emerson Electric, particularly in its industrial fluid handling segment. The significant revenue of these competitors, such as Flowserve's $4.1 billion in 2024, underscores the concentrated market power Crane contends with, driving aggressive strategies.

The presence of similarly sized competitors in niche markets escalates rivalry, often leading to price wars and increased marketing spend. Furthermore, slow growth in certain industrial sectors amplifies competition as firms fight harder for existing market share, impacting profitability.

Crane's strategy of product differentiation through engineered solutions helps mitigate direct price competition. However, if rivals like Parker Hannifin or Eaton can effectively replicate these specialized offerings, the competitive pressure intensifies significantly.

High exit barriers, such as specialized assets and substantial severance costs, keep even struggling firms in the market, thereby increasing overall rivalry. For instance, the capital intensity in Crane's manufacturing sector, with estimated 2024 capital expenditures exceeding $50 million, makes exiting a costly decision.

SSubstitutes Threaten

Availability of Alternative Technologies

The threat of substitutes for Crane Company's offerings is significant, stemming from evolving alternative technologies and materials that can perform similar functions. For instance, in the fluid handling sector, advancements in pumping mechanisms or novel material sciences could emerge, directly challenging Crane's established solutions.

Crane must remain vigilant in monitoring technological progress that could potentially make its current product lines obsolete or less competitive in the market. For example, the development of more efficient, lower-cost, or environmentally friendly alternatives in areas like industrial pumps or valves could erode Crane's market share.

In 2024, the industrial equipment sector saw continued investment in R&D for sustainable and digitized solutions. Companies are actively exploring advanced materials and smart technologies that offer improved performance and reduced lifecycle costs, posing a direct substitute threat to traditional, less integrated offerings.

Price-Performance Trade-off of Substitutes

Customers will readily switch to substitute products if they present a more appealing price-performance balance. For example, if a new composite material emerges offering enhanced durability at a reduced cost compared to Crane's engineered components, it poses a significant threat.

The market for engineered materials saw significant innovation in 2024. Advanced polymers, for instance, demonstrated a 15% improvement in tensile strength while maintaining competitive pricing, directly challenging traditional metal alloys used in similar applications.

Crane must prioritize ongoing research and development to ensure its product portfolio consistently delivers superior value, both in terms of cost-effectiveness and functional performance, to mitigate the allure of readily available substitutes.

Switching Costs for Customers to Adopt Substitutes

The threat of substitutes for Crane's products is shaped by the costs and effort customers face when switching. If switching involves substantial re-tooling or significant operational risks, the threat is diminished. For instance, in the industrial equipment sector, a customer heavily invested in Crane's specialized hydraulic systems might face prohibitive costs and extensive downtime to reconfigure their manufacturing lines for a competitor's offerings.

Conversely, if substitutes are readily available and offer clear advantages with minimal disruption, the threat intensifies. Consider Crane's portable lifting solutions; if a competitor emerges with a lighter, more energy-efficient model that requires no specialized training or new infrastructure for operation, customers would likely find it easier to transition, increasing the substitution threat.

In 2024, the average switching cost for industrial machinery can range from 10% to 25% of the initial purchase price, factoring in installation, training, and potential lost productivity. This figure underscores the importance of Crane's product integration and customer support in deterring easy shifts to alternatives.

Customer Awareness and Acceptance of Substitutes

Customer awareness and their willingness to embrace new, unproven technologies significantly influence the threat of substitutes. For mission-critical applications, clients often exhibit risk aversion, favoring well-established and reliable solutions over novel alternatives.

Crane's established reputation and a history of proven reliability within its specialized markets serve as a significant deterrent to the rapid adoption of emerging substitutes. This ingrained trust makes customers less inclined to switch to less-tested options, especially when operational continuity is paramount.

- Customer Risk Aversion: In sectors where Crane operates, such as aerospace or critical infrastructure, a failure can have severe consequences, leading to a strong preference for proven technologies.

- Switching Costs: Beyond just the technology itself, the cost and effort involved in re-qualifying, integrating, and training personnel on a new substitute can be substantial, further reinforcing loyalty to existing solutions.

- Perceived Performance Gap: New substitutes must not only match but demonstrably exceed the performance and reliability of Crane's offerings to overcome customer inertia and perceived risks.

Regulatory and Environmental Shifts

Changes in regulations and growing environmental concerns can significantly speed up the adoption of substitute products. For instance, more stringent emissions standards globally, particularly in major markets like the European Union and North America, are increasingly pushing industries towards electrification. This trend directly benefits electric actuation systems as a substitute for traditional hydraulic systems, which often have higher environmental footprints due to potential fluid leaks and energy inefficiency.

Furthermore, the push for sustainability is driving innovation in material science. New, eco-friendly materials are emerging that can offer comparable or superior performance to existing ones, making them attractive alternatives. For example, advancements in bioplastics and recycled composites are presenting viable substitutes in various manufacturing sectors, potentially impacting the demand for conventional materials used in industrial equipment. Crane Porter must proactively adapt its product portfolio to anticipate and respond to these critical macro-environmental shifts to maintain its competitive edge.

- Regulatory Impact: In 2024, the International Energy Agency reported that over 70% of new vehicle sales in Norway were electric, highlighting the accelerating shift driven by policy.

- Environmental Drivers: Global corporate sustainability reports in 2024 increasingly cited supply chain environmental performance as a key factor in material sourcing decisions.

- Substitution Potential: The market for electric actuators is projected to grow at a compound annual growth rate of over 6% through 2030, indicating a strong substitution trend against hydraulic systems.

Tech & Regulations Fuel Industrial Substitutes, Challenging Incumbents

The threat of substitutes for Crane Company's products is a dynamic factor influenced by technological advancements and customer willingness to adopt alternatives. In 2024, the industrial sector continued to see significant R&D in sustainable and digitized solutions, with advanced materials and smart technologies offering improved performance and lower lifecycle costs, directly challenging traditional offerings.

Customer switching costs remain a crucial barrier, with estimates for industrial machinery ranging from 10% to 25% of the initial purchase price in 2024, encompassing installation, training, and potential productivity losses. However, regulatory shifts and environmental concerns are accelerating the adoption of substitutes, such as electric actuation systems replacing hydraulic ones due to stricter emissions standards.

The market for advanced polymers, for example, showed a 15% improvement in tensile strength in 2024 while maintaining competitive pricing, directly impacting demand for traditional metal alloys. This highlights how substitutes offering a better price-performance balance, coupled with reduced switching friction, can rapidly erode market share for incumbent products.

| Factor | 2024 Data Point | Implication for Crane |

|---|---|---|

| R&D Investment in Sustainable Tech | Significant increase across industrial sectors | Need for continuous innovation to match or exceed performance of emerging alternatives. |

| Average Switching Cost (Industrial Machinery) | 10-25% of initial purchase price | Crane's established customer base benefits from high switching costs, but new entrants with lower integration hurdles pose a threat. |

| Electric Actuator Market Growth | Projected CAGR > 6% through 2030 | Direct substitution threat to hydraulic systems, driven by environmental regulations. |

| Advanced Polymer Performance | 15% improvement in tensile strength vs. traditional alloys | Material science innovation can create direct substitutes for Crane's engineered components. |

Entrants Threaten

High Capital Requirements

Entering highly engineered industrial sectors, such as aerospace or advanced materials, demands immense capital. Crane, for instance, operates in markets where significant investment in sophisticated manufacturing, cutting-edge research and development, and specialized machinery is a prerequisite for even basic operation. This financial hurdle is a formidable barrier to entry.

For example, establishing a new aerospace component manufacturing facility in 2024 could easily cost hundreds of millions of dollars, encompassing everything from advanced CNC machines to rigorous quality control systems. This high cost of entry naturally discourages potential new competitors from challenging established firms like Crane, who have already made these substantial investments.

Economies of Scale and Experience Curve

Existing players in the crane industry, such as Crane Co., often leverage significant economies of scale. This means they can produce cranes at a lower cost per unit due to higher production volumes, bulk purchasing of materials, and shared research and development expenses. For instance, in 2023, Crane Co. reported total revenues of $1.99 billion, indicating a substantial operational footprint that smaller entrants would find difficult to match.

New companies entering the market face a considerable hurdle in achieving similar cost efficiencies. Without the established scale of operations, they would likely incur higher per-unit production costs, making their pricing less competitive. This cost disadvantage can severely limit their ability to gain market share against incumbents who have already optimized their supply chains and manufacturing processes.

Furthermore, the experience curve plays a crucial role. Established manufacturers have accumulated years of operational knowledge, leading to improved efficiency in design, production, and service. This accumulated expertise allows them to anticipate and solve problems more effectively than newcomers, creating another barrier to entry by providing a tangible advantage in operational performance and product reliability.

Proprietary Technology and Intellectual Property

Crane's emphasis on highly engineered products is underpinned by significant investment in proprietary technology and intellectual property, including patents and specialized manufacturing processes. This R&D focus, which saw Crane invest $477 million in 2023, creates substantial barriers to entry. New competitors would need to surmount the challenge of replicating Crane's established technological advantage, a costly and time-consuming endeavor.

Access to Distribution Channels and Customer Relationships

New entrants often struggle to access established distribution channels, a significant barrier to entry. For instance, in the industrial valve market, where Crane operates, securing shelf space or partnerships with major distributors can take years and substantial investment. This is particularly true for mission-critical applications where reliability is paramount.

Building trust with customers is equally demanding. Risk-averse buyers in sectors like aerospace or energy are hesitant to switch from established suppliers like Crane, who have a proven track record. This customer loyalty, built over decades, makes it difficult for newcomers to gain traction. In 2024, the average sales cycle for complex industrial equipment often exceeds 12 months, highlighting the time needed to cultivate these relationships.

- Distribution Channel Access: New entrants face significant hurdles in gaining access to established, reliable distribution networks, which are often controlled by incumbents.

- Customer Relationships: Long-standing, trust-based relationships between Crane and its customers in critical sectors create a high switching cost for new market participants.

- Risk Aversion: Customers in mission-critical industries prioritize proven performance and reliability, making them reluctant to adopt products from unproven new entrants.

- Time and Investment: Establishing necessary distribution and customer trust requires considerable time and financial resources, acting as a deterrent to potential competitors.

Government Policy and Regulatory Hurdles

Government policies and regulatory frameworks act as significant deterrents to new entrants in many industries. For instance, sectors like aerospace demand rigorous certifications and adherence to stringent safety and environmental regulations. The compliance process itself is often lengthy and costly, presenting a substantial barrier that favors established companies possessing the necessary expertise and resources.

In 2024, the global aerospace market, valued at over $870 billion, exemplifies this. New companies entering this space must navigate complex approval processes from bodies like the Federal Aviation Administration (FAA) or the European Union Aviation Safety Agency (EASA). These requirements can take years and millions of dollars to fulfill, effectively shielding incumbent players.

- Stringent Certifications: Industries like aerospace require extensive and costly certifications before products can be brought to market.

- Regulatory Compliance Costs: Meeting safety, environmental, and operational standards incurs significant ongoing expenses for new entrants.

- Time to Market: The lengthy approval processes delay market entry, giving established firms a competitive advantage.

- Established Expertise: Incumbents benefit from existing knowledge and relationships with regulatory bodies, further solidifying their position.

High Barriers Protect Established Players

The threat of new entrants for Crane is relatively low due to substantial capital requirements and significant economies of scale enjoyed by existing players. For instance, Crane Co.'s 2023 revenue of $1.99 billion highlights its operational footprint, making it difficult for newcomers to match cost efficiencies. Proprietary technology and established distribution channels further deter new competition.

| Barrier | Description | Impact on New Entrants | Supporting Data (2023/2024) |

| Capital Requirements | High investment needed for R&D, manufacturing, and specialized machinery. | Significant deterrent, especially in sectors like aerospace. | Aerospace component facility costs in 2024: hundreds of millions of dollars. |

| Economies of Scale | Lower per-unit costs due to high production volumes and bulk purchasing. | New entrants face higher costs and less competitive pricing. | Crane Co. 2023 Revenue: $1.99 billion. |

| Proprietary Technology & IP | Patents and specialized manufacturing processes create a technological advantage. | Costly and time-consuming for new entrants to replicate. | Crane's 2023 R&D Investment: $477 million. |

| Distribution Channels & Customer Relationships | Accessing established networks and building trust takes time and investment. | New entrants struggle to gain market traction and customer loyalty. | Industrial equipment sales cycles in 2024: often exceed 12 months. |

Porter's Five Forces Analysis Data Sources

Our Crane Porter's Five Forces analysis is built upon a foundation of industry-specific market research reports, company financial statements, and trade association data. We also incorporate insights from equipment manufacturer specifications and operational efficiency benchmarks to assess competitive intensity and potential threats.