BlackRock Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

BlackRock Bundle

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

BlackRock navigates a complex financial landscape where buyer power from institutional investors is significant, and the threat of new entrants, while present, is tempered by high capital requirements. Understanding these dynamics is crucial for anyone looking to grasp BlackRock's competitive position.

The complete report reveals the real forces shaping BlackRock’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

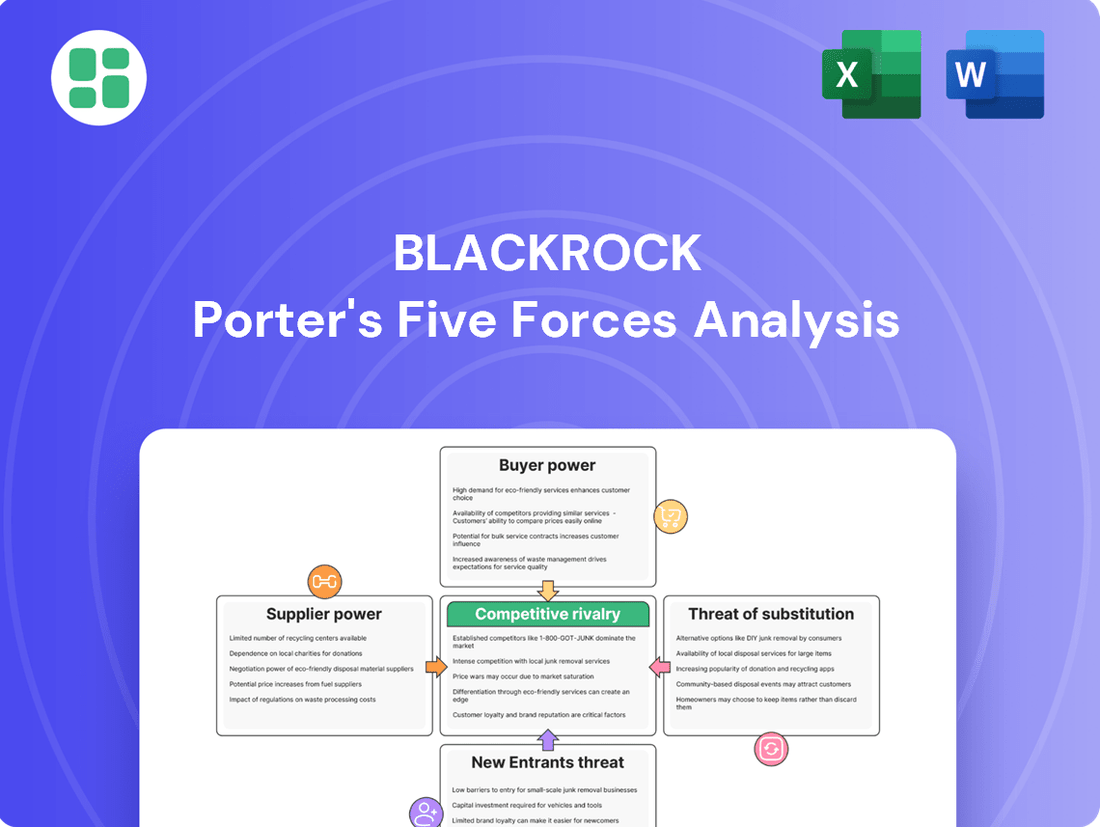

Suppliers Bargaining Power

Specialized Technology and Data Providers

Suppliers of highly specialized financial technology and market data, crucial for platforms like BlackRock's Aladdin, wield moderate to high bargaining power. The proprietary nature and intricate integration of these systems create significant switching costs for BlackRock. For instance, the development and ongoing maintenance of a system as comprehensive as Aladdin represent a substantial investment, making it challenging and expensive to replace key technology providers.

Human Capital and Talent Acquisition

BlackRock's reliance on highly skilled financial professionals, portfolio managers, and technology experts means these individuals are key suppliers of human capital. The intense competition for top-tier talent, particularly in burgeoning fields like artificial intelligence and private markets, significantly amplifies their bargaining power.

Financial Infrastructure Providers

Financial infrastructure providers, such as exchanges and custodians, wield significant bargaining power over BlackRock. These entities are critical for BlackRock's core functions like trading execution and the safekeeping of assets. While BlackRock's immense scale provides some negotiation advantage, the fundamental nature and limited substitutability of these services inherently strengthen the suppliers' position.

Regulatory and Compliance Services

Suppliers of legal, audit, and regulatory compliance services wield significant influence over BlackRock. The financial sector's highly regulated environment necessitates expert and dependable compliance support, making these services critical. For instance, in 2024, the global regulatory technology market was valued at approximately $12.7 billion, highlighting the substantial investment in compliance infrastructure and services.

- High Barrier to Entry for Suppliers: Specialized knowledge and certifications are required to offer legal and compliance services in the financial industry, limiting the number of qualified providers.

- Criticality of Services: Non-compliance can lead to severe penalties, reputational damage, and operational disruptions, underscoring the indispensable nature of these supplier services for BlackRock.

- Limited Substitutes: While technology can assist, the core expertise of legal and compliance professionals remains largely irreplaceable for navigating complex regulatory landscapes.

Office Space and Real Estate

For a global financial powerhouse like BlackRock, landlords and real estate service providers are essential suppliers. The bargaining power of these suppliers can vary significantly. While the office real estate market offers many options, securing premium locations or large, consolidated spaces can shift leverage towards landlords. This is particularly true in major financial hubs where demand for prime office space remains robust.

In 2024, major cities continued to see high demand for quality office spaces. For instance, average office rents in New York City's prime Manhattan markets hovered around $70-$80 per square foot annually, demonstrating the significant cost associated with desirable locations. BlackRock's global footprint, with offices in over 30 countries, means managing these supplier relationships across diverse markets, each with its own real estate dynamics.

- High Demand in Prime Locations: Landlords in globally recognized financial centers like London, New York, and Singapore often possess considerable bargaining power due to intense competition for limited prime real estate.

- Scale of Requirements: BlackRock's substantial office space needs can sometimes provide leverage, allowing for negotiation on lease terms and services, especially when consolidating operations.

- Specialized Services: Beyond raw space, the need for specialized building services, security, and maintenance can also empower certain suppliers if unique expertise is required.

Critical Supplier Dependencies Shaping Financial Operations

Suppliers of critical financial data and specialized technology, such as those providing market analytics or proprietary trading platforms, hold significant leverage over BlackRock. The integration complexity and high switching costs associated with these systems, like BlackRock's Aladdin platform, mean that disruptions from these suppliers could be substantial. For example, the market for financial data services is highly concentrated, with a few key players dominating.

| Supplier Category | Bargaining Power Level | Key Factors |

|---|---|---|

| Financial Data & Tech Providers | Moderate to High | Proprietary systems, high switching costs, concentration in market |

| Human Capital (Talent) | High | Competition for AI/private markets expertise, specialized skills |

| Financial Infrastructure (Exchanges, Custodians) | High | Essential services, limited substitutes, scale provides some leverage |

| Legal, Audit & Compliance Services | High | Regulatory environment, high penalties for non-compliance, limited substitutes |

| Real Estate & Facilities Management | Varies (Moderate to High) | Demand in prime locations, scale of needs, specialized building services |

What is included in the product

Analyzes the competitive intensity within the asset management industry, focusing on BlackRock's strategic positioning against rivals, buyer power, supplier influence, and the threat of new entrants and substitutes.

Effortlessly identify and mitigate competitive threats with a visual breakdown of BlackRock's industry landscape, enabling proactive strategy adjustments.

Customers Bargaining Power

Large Institutional Clients

BlackRock's largest institutional clients, including major pension funds, sovereign wealth funds, and endowments, hold substantial sway. These clients collectively manage trillions of dollars, giving them considerable leverage to negotiate fees and demand customized investment strategies. For instance, as of the first quarter of 2024, BlackRock's total assets under management (AUM) reached approximately $10.5 trillion, with institutional clients representing a significant portion of this figure.

Retail Investors and ETF Purchasers

While a single retail investor or iShares ETF purchaser holds minimal individual bargaining power, their collective decision to shift assets to rival platforms or funds significantly influences the market. This aggregated influence is amplified by the increasing availability of low-cost index funds and ETFs, which fosters intense price competition and directly benefits these investors.

Aladdin Platform Clients

Clients of BlackRock's Aladdin platform, typically large financial institutions, possess moderate bargaining power. The platform's integrated nature and extensive functionalities create significant switching costs, making it challenging for clients to move to alternative solutions. For instance, in 2023, BlackRock reported that Aladdin served over 40,000 users across more than 200 institutions, highlighting its deep integration into client operations.

Fee Sensitivity and Performance Expectations

Customers today are keenly aware of fees and expect top-tier performance, especially when markets are unpredictable. This heightened sensitivity directly impacts BlackRock, forcing it to keep its pricing competitive and consistently deliver strong returns to retain business and safeguard its revenue.

BlackRock's asset management fees are a key revenue driver. For instance, in 2023, BlackRock reported total revenue of $17.9 billion, with advisory and administration fees making up a significant portion. The pressure to maintain competitive fee structures while meeting investor performance benchmarks is a constant challenge.

- Fee Sensitivity: Investors are scrutinizing management fees more closely, seeking value for their money.

- Performance Demands: A significant portion of BlackRock's AUM (Assets Under Management) is tied to performance-based fees, making consistent returns crucial. As of Q1 2024, BlackRock managed $10.5 trillion in AUM.

- Competitive Landscape: The asset management industry is highly competitive, with numerous firms vying for investor capital, further intensifying fee pressure.

- Impact on Revenue: Lower fees or underperformance can directly reduce BlackRock's fee income and potentially lead to outflows of assets under management.

Diversified Client Base

BlackRock's extensive diversification across institutional, retail, and technology services, coupled with a broad geographic reach, significantly dilutes the bargaining power of any single client group. This wide client spread means no particular segment holds a disproportionate sway over the company's revenue streams, lessening reliance on any one customer base.

As of the first quarter of 2024, BlackRock managed approximately $10.5 trillion in assets under management (AUM), showcasing the sheer scale and breadth of its client relationships. This vast AUM is spread across numerous client types, including pension funds, sovereign wealth funds, endowments, insurance companies, and individual investors, preventing any single client or small group of clients from dictating terms.

- Diversified Revenue Streams: BlackRock's revenue is not overly dependent on any one client segment, with institutional clients, iShares ETFs, and technology services each contributing substantial portions.

- Global Footprint: Operating in over 100 countries ensures that client concentration risk is minimized, as demand for BlackRock's services is spread across diverse economic and regulatory environments.

- Scale Advantage: The sheer size of BlackRock's operations and AUM provides a natural barrier against individual client demands that could significantly impact profitability or service offerings.

Client Power: Shaping BlackRock's Strategy and Fees

BlackRock's institutional clients, managing trillions, possess significant bargaining power, influencing fees and demanding tailored strategies. For example, as of Q1 2024, BlackRock's $10.5 trillion AUM includes substantial institutional assets, giving these clients leverage. While individual retail investors have little power, their collective asset shifts to competitors due to low-cost options can impact BlackRock. Clients of the Aladdin platform face moderate power due to high switching costs, as evidenced by its use by over 200 institutions in 2023.

| Client Type | Estimated Influence | Key Drivers of Influence |

| Large Institutional Investors (Pension Funds, Sovereign Wealth Funds) | High | Significant AUM, fee negotiation, demand for customization |

| Retail Investors (ETF purchasers) | Low (individually), Moderate (collectively) | Price sensitivity, availability of low-cost alternatives |

| Aladdin Platform Clients (Financial Institutions) | Moderate | Switching costs, platform integration, operational dependence |

Preview the Actual Deliverable

BlackRock Porter's Five Forces Analysis

This preview displays the complete BlackRock Porter's Five Forces Analysis, offering an in-depth examination of the competitive landscape for the world's largest asset manager. The document you see here is precisely what you'll receive immediately after purchase, ensuring full transparency and value. It meticulously details each of the five forces, providing actionable insights into BlackRock's strategic positioning and the external factors influencing its industry.

Rivalry Among Competitors

Dominant Market Position

BlackRock, the undisputed leader in asset management with assets under management (AUM) projected between $11.5 trillion and $12.5 trillion for 2024-2025, operates in a fiercely competitive landscape. Its dominant market position, bolstered by its extensive iShares ETF suite and the powerful Aladdin technology platform, makes it a prime target for both established financial institutions and emerging fintech players.

'Big Three' Index Fund Competition

BlackRock's iShares faces intense rivalry from Vanguard and State Street in the index fund and ETF space, forming the 'Big Three'. This competition drives down fees significantly, as seen with the ongoing price wars that have made many broad-market index funds virtually free for investors.

The focus on scale is paramount; as of early 2024, Vanguard managed over $8.1 trillion in assets, while BlackRock's iShares held approximately $4.1 trillion, and State Street's SPDR ETFs had around $4 trillion. This sheer volume allows them to operate at lower costs, further intensifying the pressure on profit margins.

Broad Asset Management Landscape

BlackRock faces intense competition from a diverse range of asset managers, including giants like Fidelity, JPMorgan, and Schwab, as well as specialized global investment firms. This rivalry spans all major asset classes, from traditional equities and fixed income to the increasingly important alternative and private markets.

The sheer volume of assets under management (AUM) among competitors highlights the competitive pressure. For instance, in 2024, Fidelity managed over $4.5 trillion in AUM, while Schwab oversaw more than $8 trillion in client assets, demonstrating the scale of rivals BlackRock must contend with across the financial landscape.

Technological Edge and Innovation

BlackRock's competitive rivalry is significantly influenced by a technological arms race. The firm actively enhances its Aladdin platform, a key differentiator, and is integrating artificial intelligence to refine analytics and client service. This focus on innovation is crucial as competitors are also channeling substantial resources into technology to gain an advantage in areas like data analysis and operational efficiency.

The ongoing investment in technology by rivals creates a dynamic environment where maintaining a technological edge is a continuous challenge. For instance, in 2024, many asset managers are prioritizing AI-driven insights and cloud-based infrastructure to offer more sophisticated solutions and streamline operations. This makes technological advancement a primary battleground for market share.

- Aladdin Platform Enhancements: BlackRock continues to invest in its proprietary Aladdin platform, a cornerstone of its technological advantage, aiming to provide integrated risk management, portfolio management, and trading solutions.

- AI Integration: The firm is actively incorporating artificial intelligence and machine learning across its operations to improve investment decision-making, enhance client engagement, and optimize operational processes.

- Competitor Technology Investments: Other major players in the asset management industry are also making significant capital expenditures on technology, focusing on areas like big data analytics, cybersecurity, and digital client interfaces to remain competitive.

- Industry Trend: Digitalization: The broader financial services industry is witnessing a strong push towards digitalization, with firms across the board seeking to leverage technology to reduce costs, increase scalability, and deliver superior client experiences.

Strategic Acquisitions and Diversification

BlackRock's competitive rivalry is significantly shaped by its strategic acquisitions and diversification efforts. In 2024 and early 2025, the company made substantial moves, including the acquisition of Global Infrastructure Partners and HPS Investment Partners. These deals, valued in the billions, are designed to bolster BlackRock's presence in rapidly expanding sectors like infrastructure and private markets.

This aggressive expansion strategy intensifies rivalry by allowing BlackRock to offer a more comprehensive suite of services, reinforcing its 'one-stop-shop' model. By integrating new capabilities and market access through these acquisitions, BlackRock directly challenges competitors who may specialize in narrower asset classes.

- Acquisition of Global Infrastructure Partners (GIP): A major move in 2024, significantly boosting BlackRock's infrastructure and private equity offerings.

- Acquisition of HPS Investment Partners: Further strengthens BlackRock's private credit and alternative asset management capabilities.

- Diversification into High-Growth Areas: These acquisitions target sectors experiencing strong investor demand, increasing competitive pressure on existing players.

- 'One-Stop-Shop' Ambition: Broadening its service portfolio through M&A allows BlackRock to capture a larger share of investor assets.

Asset Management: The Battle for Trillions

Competitive rivalry is intense for BlackRock, driven by its market leadership and the sheer scale of its operations. The asset management industry is characterized by numerous players, from established giants to agile fintech firms, all vying for investor assets. This dynamic is amplified by a constant drive for lower fees, particularly in the passive investing space.

The 'Big Three' – BlackRock, Vanguard, and State Street – dominate the ETF market, engaging in aggressive price competition that has made many index funds nearly free. For instance, as of early 2024, Vanguard managed over $8.1 trillion, BlackRock's iShares held around $4.1 trillion, and State Street's SPDR ETFs had approximately $4 trillion, illustrating the scale advantage that fuels this rivalry.

Beyond the passive space, BlackRock faces significant competition from active managers like Fidelity, which managed over $4.5 trillion in AUM in 2024, and Schwab, overseeing more than $8 trillion in client assets. This competition spans all asset classes, including the rapidly growing alternative investments sector, where BlackRock's recent acquisitions of Global Infrastructure Partners and HPS Investment Partners in 2024 aim to strengthen its position.

| Competitor | Approximate AUM (Early 2024) | Key Competitive Area |

|---|---|---|

| Vanguard | $8.1 trillion+ | Index Funds, ETFs, Low Fees |

| State Street (SPDR) | $4 trillion+ | ETFs, Institutional Services |

| Fidelity | $4.5 trillion+ | Active Management, Retail Services |

| Charles Schwab | $8 trillion+ (Client Assets) | Brokerage, Retirement, ETFs |

SSubstitutes Threaten

Direct Investing by Individuals and Institutions

The increasing accessibility of online brokerage platforms and readily available financial data empowers both individual and institutional investors to manage their portfolios directly. This trend bypasses traditional asset managers, presenting a significant substitute for services like those offered by BlackRock, particularly for more liquid investment types. In 2023, the global fintech market, which fuels these platforms, was valued at over $115 billion and is projected to grow substantially.

Alternative Investment Vehicles

Investors have a growing array of alternative investment vehicles beyond traditional managed funds, including direct real estate, private equity from competing firms, hedge funds, and cryptocurrencies. For instance, the global alternative investment market was valued at approximately $13.7 trillion in 2023, a significant figure highlighting the breadth of choices available.

This proliferation of substitutes directly challenges BlackRock by offering investors alternative avenues for capital allocation. The sheer diversity means clients can bypass BlackRock's offerings if they perceive better returns or lower fees elsewhere.

BlackRock is actively working to counter this threat by expanding its presence in private markets and developing tokenized funds. These strategic moves aim to capture investor interest in newer, less traditional asset classes, thereby broadening BlackRock's appeal and reducing the reliance on its core managed fund products.

Robo-Advisors and Digital Platforms

The rise of robo-advisors and digital investment platforms presents a significant threat of substitutes for BlackRock. These platforms, offering automated portfolio management at lower fees, cater to a growing segment of investors prioritizing cost-effectiveness and simplicity. For instance, by the end of 2023, the assets under management in robo-advisory services globally were projected to surpass $2.5 trillion, indicating a substantial shift in investor preferences.

Internal Investment Management Capabilities

Large institutional clients, like pension funds and sovereign wealth funds, are increasingly developing their internal investment management capabilities. This trend presents a significant threat of substitution for external asset managers such as BlackRock. For instance, a substantial portion of institutional assets could be brought in-house, directly competing with services BlackRock offers, especially for more straightforward asset classes.

The ability of these large clients to manage assets internally reduces their need for outsourced solutions. This can lead to a decline in assets under management (AUM) for firms like BlackRock if a significant number of clients shift their strategies. In 2024, institutional investors continued to explore cost efficiencies and greater control over their portfolios, making internal management a more attractive proposition.

- Growing demand for in-house asset management among institutional investors.

- Potential reduction in BlackRock's AUM as clients internalize investment functions.

- Core asset classes are particularly vulnerable to this substitution threat.

Bank Deposits and Fixed-Income Alternatives

Bank deposits and fixed-income alternatives pose a significant threat, especially when interest rates rise. During periods of high interest rates, such as those seen in late 2023 and early 2024, investors may find safer, guaranteed returns in Certificates of Deposit (CDs) or money market funds more appealing than potentially volatile investment funds. This shift can divert substantial capital away from managed assets.

For instance, as of early 2024, yields on short-term Treasury bills and high-yield savings accounts were offering competitive returns, often exceeding 4-5%, making them attractive substitutes. This directly impacts the assets under management for investment firms.

- Increased attractiveness of low-risk alternatives: Higher interest rates make bank deposits and short-term fixed-income products more competitive.

- Capital outflow from managed funds: Investors may move money from investment funds to these safer, higher-yielding options.

- Impact on asset management industry: This trend can lead to reduced assets under management and fee revenue for investment firms.

- Data point: In Q4 2023, retail deposits in US commercial banks saw a notable increase as yields on savings accounts and CDs rose significantly.

Investment Substitutes: A Rising Threat

The threat of substitutes for BlackRock is significant, stemming from readily available financial data, online brokerage platforms, and a growing array of alternative investment vehicles. These substitutes offer investors choices beyond traditional managed funds, including direct real estate, private equity from competing firms, hedge funds, and cryptocurrencies.

The rise of robo-advisors and digital investment platforms further intensifies this threat, providing automated portfolio management at lower fees. Additionally, institutional investors are increasingly building in-house capabilities, reducing their reliance on external asset managers like BlackRock, particularly for core asset classes.

Periods of rising interest rates also bolster the appeal of lower-risk alternatives such as bank deposits and fixed-income products, diverting capital from managed assets.

| Substitute Category | Key Drivers | Impact on BlackRock | 2023/2024 Data Point |

|---|---|---|---|

| Online Brokerages & Fintech | Accessibility, Lower Fees, Data Availability | Bypassing traditional asset managers | Global Fintech Market valued >$115 billion (2023) |

| Alternative Investments | Diversification, Higher Potential Returns | Capital allocation away from managed funds | Global Alternative Investment Market valued ~$13.7 trillion (2023) |

| Robo-Advisors | Cost-effectiveness, Simplicity | Catering to cost-conscious investors | Robo-advisory AUM projected >$2.5 trillion (end of 2023) |

| In-house Institutional Management | Cost efficiencies, Greater Control | Reduced demand for outsourced solutions | Institutional investors exploring internal capabilities (2024) |

| Bank Deposits & Fixed Income | Higher Interest Rates, Lower Risk | Capital outflow from managed assets | Competitive yields on short-term Treasuries/savings accounts (early 2024) |

Entrants Threaten

High Capital Requirements and Economies of Scale

Entering the global asset management arena, particularly to compete with giants like BlackRock, demands substantial capital. We're talking about billions needed for robust technology infrastructure, extensive marketing campaigns, and the sheer operational costs of managing vast sums of money. For instance, in 2023, BlackRock's total assets under management (AUM) reached an impressive $9.08 trillion, a figure that highlights the scale new players must aim for.

Newcomers struggle to match the cost efficiencies enjoyed by established firms. Incumbents, benefiting from massive economies of scale, can spread their fixed costs over a much larger AUM base, allowing them to offer more competitive management fees. This cost advantage makes it incredibly difficult for smaller, newer firms to attract clients solely on price, a crucial factor in asset allocation decisions.

Regulatory and Compliance Hurdles

The financial industry is a minefield of regulations, making it tough for newcomers. Think about the sheer volume of rules BlackRock, for instance, has to follow. In 2023, the company reported $28.1 trillion in assets under management, all operating within strict global financial oversight. These extensive legal and compliance requirements act as a significant barrier, deterring potential competitors from even entering the market.

Navigating this intricate web of global regulations and securing the necessary licenses is a daunting task for any new player. For example, obtaining approval from bodies like the SEC in the US or the FCA in the UK requires significant investment in legal expertise and time. This complexity and the associated costs create a formidable hurdle that new entrants must overcome before they can even begin to compete with established firms like BlackRock.

Brand Reputation and Trust

BlackRock's formidable brand reputation and the deep trust it has cultivated over decades present a significant barrier for new entrants. Building a comparable level of credibility, especially with large institutional investors who entrust billions, takes considerable time and consistent performance.

This established trust is not easily replicated. For instance, in 2023, BlackRock managed approximately $9.1 trillion in assets under management, a testament to the confidence clients place in its brand and services. New players would find it exceptionally challenging to attract such substantial capital without a proven track record and a similarly robust reputation.

Proprietary Technology and Distribution Networks

BlackRock's proprietary Aladdin platform presents a formidable barrier to entry for potential competitors, as replicating its sophisticated risk management and portfolio analysis capabilities requires substantial investment and expertise. This technological moat makes it incredibly challenging for new firms to offer comparable services, effectively deterring many from even attempting to enter the market.

Furthermore, BlackRock benefits from deeply entrenched distribution networks that have been cultivated over years of operation and client relationship building. New entrants struggle to gain access to these established channels, which are crucial for reaching a broad investor base and securing assets under management. As of early 2024, BlackRock managed over $10 trillion in assets, a testament to the strength of these networks.

- Aladdin's Technological Superiority: The platform's advanced analytics and integrated workflows are difficult and costly for new entrants to replicate.

- Established Distribution Channels: BlackRock's extensive relationships with institutional investors and financial advisors create significant hurdles for newcomers.

- High Capital Requirements: Developing technology comparable to Aladdin and building out a competitive distribution network demands immense capital.

- Brand Recognition and Trust: BlackRock's established reputation fosters trust, a factor that new entrants must work hard to build.

Talent Acquisition and Retention

The threat of new entrants in the asset management space, particularly concerning talent acquisition and retention, poses a significant challenge. New firms must compete with established players like BlackRock for highly skilled financial analysts, portfolio managers, and technology experts. BlackRock's strong brand recognition and substantial compensation packages, often including lucrative bonuses and equity, make it a highly desirable employer, creating a considerable hurdle for emerging competitors trying to attract and keep top-tier talent.

In 2024, the demand for specialized skills, especially in areas like artificial intelligence and data science within finance, intensified. For instance, reports indicated that average salaries for senior quantitative analysts in major financial hubs could exceed $250,000 annually, plus bonuses. New entrants often lack the financial muscle to match these compensation structures, making it difficult to lure away experienced professionals from industry giants.

- Talent War: New entrants face an uphill battle against established firms like BlackRock in securing top financial and technological talent.

- Compensation Disparity: The ability of larger firms to offer more competitive salaries and benefits creates a significant disadvantage for new market entrants.

- Reputation Advantage: BlackRock's established reputation as a leading global investment manager enhances its appeal to potential employees, further complicating talent acquisition for newcomers.

Asset Management: A Fortress for New Entrants

The threat of new entrants into the global asset management industry is significantly low, largely due to the immense capital requirements and regulatory hurdles. BlackRock's scale, with over $10 trillion in assets managed as of early 2024, necessitates comparable investment in technology and operations for any new player to be competitive.

Established firms benefit from significant economies of scale, allowing them to offer lower fees than newcomers can realistically match. Furthermore, BlackRock's strong brand reputation and the trust it has built over decades, managing approximately $9.1 trillion in 2023, create a formidable barrier for any firm seeking to attract substantial client assets.

| Barrier | Description | Impact on New Entrants |

|---|---|---|

| Capital Requirements | Billions needed for technology, marketing, and operations. | Extremely high; deters many potential entrants. |

| Economies of Scale | Lower cost per unit of AUM for incumbents. | Makes price competition difficult for new firms. |

| Regulatory Compliance | Complex and costly to navigate global financial rules. | Significant time and financial investment required for licensing. |

| Brand & Trust | Decades of proven performance and client relationships. | Difficult and time-consuming for new entrants to replicate. |

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis for BlackRock leverages data from their annual reports, investor presentations, and SEC filings. We also incorporate insights from industry-specific market research reports and financial news outlets to capture competitive dynamics.