ALPHAWAVE SEMI Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

ALPHAWAVE SEMI Bundle

From Overview to Strategy Blueprint

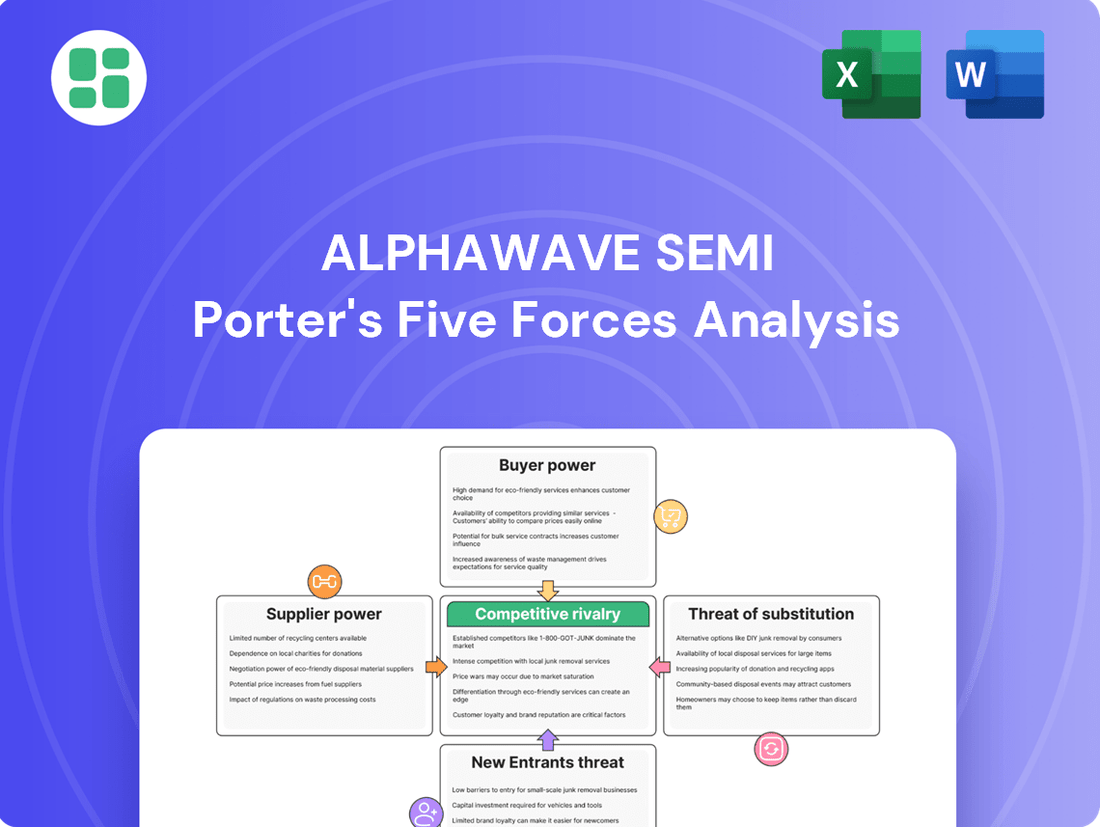

ALPHAWAVE SEMI operates in a dynamic semiconductor market, facing intense rivalry and significant buyer power from its large clientele. Understanding these forces is crucial for strategic planning.

The complete report reveals the real forces shaping ALPHAWAVE SEMI’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Reliance on Advanced Foundries

Alphawave Semi, a fabless semiconductor company, faces significant supplier bargaining power due to its reliance on advanced foundries. These foundries, such as TSMC, Samsung, and Intel, are the sole providers of manufacturing capabilities for Alphawave's cutting-edge silicon IP and chiplets at critical process nodes like 3nm and 2nm.

The concentrated nature of these advanced foundries, coupled with their immense technological expertise and substantial capital investments, gives them considerable leverage. For instance, TSMC, a key partner for many fabless companies, reported capital expenditures of approximately $28 billion in 2023, highlighting the scale of investment required to maintain leadership in advanced manufacturing.

This dependency means that Alphawave Semi must adhere to the terms and pricing set by these foundries to access the essential manufacturing processes needed to deliver its high-performance solutions for AI and data center applications.

High Switching Costs for Foundry Partners

Alphawave Semi faces significant challenges when considering a switch in foundry partners due to the inherently complex and expensive nature of this process. The company must undertake extensive redesign, re-verification, and re-qualification of its silicon IP, which translates into substantial financial investments and potential setbacks in bringing new products to market.

These high switching costs create a formidable barrier, effectively bolstering the negotiation leverage of Alphawave Semi's current foundry suppliers. For instance, the typical cost to qualify a new semiconductor foundry can range from millions to tens of millions of dollars, not to mention the extended timelines that can add months to product development cycles.

Dominance of EDA Tool Providers

Alphawave Semi's ability to design complex, high-speed connectivity solutions is critically dependent on access to advanced Electronic Design Automation (EDA) tools. The EDA market is highly concentrated, with a few dominant players like Siemens EDA, Synopsys, and Cadence controlling the landscape. This limited supplier base grants these companies significant bargaining power, as access to their cutting-edge software is essential for semiconductor innovation.

Specialized IP and Component Suppliers

Alphawave Semi, while boasting a substantial in-house silicon IP library, may still rely on external providers for highly specialized or foundational IP blocks and components. The scarcity of alternative suppliers for these unique elements grants significant leverage to these specialized providers. This reliance underscores the importance of maintaining strong relationships with these niche suppliers to secure critical technological advantages.

The bargaining power of these specialized IP and component suppliers is amplified by the intricate nature of their offerings and the limited competitive landscape. For Alphawave Semi, securing access to these cutting-edge components is crucial for maintaining its technological edge in specific market segments. For instance, in 2024, the semiconductor industry continued to see consolidation among IP providers, potentially increasing the power of remaining specialized entities.

- Reliance on Niche Providers: Certain foundational IP, essential for advanced chip design, may only be available from a select few companies, giving them substantial influence.

- High Switching Costs: Integrating specialized IP into a complex chip design involves significant time and resources, making it costly and difficult for Alphawave Semi to switch suppliers.

- Intellectual Property Protection: Suppliers with proprietary and well-protected IP can command higher prices and dictate terms due to the unique value they bring.

- Industry Trends: The ongoing demand for advanced functionalities in areas like AI and high-speed connectivity in 2024 means that suppliers of enabling IP are in a strong position.

Scarcity of Highly Skilled Talent

The scarcity of engineers and specialists in areas like high-speed connectivity, advanced silicon IP design, and chiplet integration significantly boosts supplier bargaining power. This limited pool of expertise means that companies like Alphawave Semi face intense competition for top talent, driving up compensation and benefits. In 2024, the global semiconductor talent shortage continued to be a major concern, with demand for specialized chip designers outstripping supply.

This talent crunch directly impacts Alphawave Semi’s ability to innovate and scale. The limited availability of these highly skilled professionals gives them considerable leverage. For instance, a report in early 2024 indicated that experienced chip design engineers could command salary increases of 15-20% or more when moving between companies due to high demand.

- Talent Scarcity: The pool of engineers with expertise in high-speed connectivity, advanced silicon IP, and chiplet integration is highly specialized and limited.

- Increased Bargaining Power: This limited availability grants these professionals significant leverage in negotiations.

- Talent Retention Investment: Alphawave Semi must prioritize investments in talent development and retention to secure essential human capital for ongoing innovation and business expansion.

- Market Dynamics: In 2024, the semiconductor industry faced a persistent shortage of skilled design engineers, impacting recruitment and retention efforts across the sector.

Supplier Power Dynamics in Advanced Semiconductor Manufacturing

Alphawave Semi's reliance on a concentrated group of advanced foundries, such as TSMC, for critical manufacturing processes significantly enhances supplier bargaining power. These foundries possess unique technological capabilities and substantial capital investments, making it difficult and costly for Alphawave to switch. For example, TSMC's 2023 capital expenditure of approximately $28 billion underscores the immense resources required to maintain leadership in advanced semiconductor manufacturing.

The bargaining power of specialized IP and component providers is also considerable, particularly for foundational IP essential for advanced chip designs. In 2024, industry consolidation among IP providers further strengthened the position of remaining niche suppliers. Switching these specialized components involves significant redesign and re-verification, with qualification costs potentially reaching tens of millions of dollars and adding months to product development timelines.

The scarcity of highly skilled engineers in areas like high-speed connectivity and advanced silicon IP design in 2024 further amplifies supplier bargaining power. This talent crunch leads to increased compensation demands, with experienced engineers potentially seeing 15-20% salary increases when changing employers. Alphawave Semi must invest in talent retention to secure the expertise needed for innovation.

| Supplier Category | Key Suppliers (Examples) | Factors Enhancing Bargaining Power | Impact on Alphawave Semi | Relevant 2024 Data/Trends |

|---|---|---|---|---|

| Advanced Foundries | TSMC, Samsung, Intel | Concentrated market, high capital investment, proprietary technology | Limited foundry choice, price dictates, adherence to terms | TSMC's 2023 capex ~$28B; ongoing demand for leading-edge nodes |

| Specialized IP/Components | Niche IP providers | Proprietary technology, high switching costs, limited alternatives | Higher IP costs, integration challenges, dependence on key IP | IP provider consolidation; 2024 demand for AI/connectivity IP |

| EDA Tools | Siemens EDA, Synopsys, Cadence | Highly concentrated market, essential for design | Subscription costs, limited negotiation leverage | Continued dominance of top EDA vendors |

| Skilled Talent | Semiconductor Engineers | Talent scarcity in specialized areas | Increased labor costs, retention challenges | 2024 talent shortage; salary increases of 15-20% for experienced engineers |

What is included in the product

This analysis unpacks the competitive forces impacting ALPHAWAVE SEMI, revealing threats from rivals, buyer power, supplier leverage, new entrants, and substitutes.

Instantly visualize competitive pressures with a dynamic, interactive dashboard that highlights key threat areas.

Customers Bargaining Power

Concentration of Key Customers

Alphawave Semi's customer base is notably concentrated, with key clients being major hyperscalers and leading semiconductor firms operating in high-growth sectors like AI, data centers, and 5G. This concentration means a few large customers hold significant sway.

In 2024, the company's top five end-customers represented a substantial 36% of its total revenue. This high percentage underscores the considerable bargaining power these major clients possess, as their business is crucial to Alphawave Semi's financial performance.

Criticality of Connectivity IP for Customer Products

Alphawave Semi's high-speed connectivity IP and chiplets are absolutely essential for their customers' cutting-edge products, like those powering AI and data centers. These advanced interconnects are the backbone, directly impacting the performance and capabilities of the final devices, making Alphawave's technology hard to replace.

This deep integration means customers are heavily reliant on Alphawave's solutions for their product's core functionality. For instance, in the rapidly expanding AI hardware market, where performance gains are paramount, the quality of connectivity directly translates to competitive advantage for the end-product manufacturer.

Long-term Engagements and Customization

Alphawave Semi's customer relationships are often characterized by long-term intellectual property (IP) licensing agreements and bespoke silicon development projects. These engagements necessitate significant customer investment in integration and co-development, fostering deep partnerships. For instance, in 2023, Alphawave reported that a substantial portion of its revenue was derived from multi-year contracts, highlighting the sticky nature of its customer base.

The extensive customization and deeply embedded nature of Alphawave's solutions create considerable switching costs for its clientele. Once a customer has integrated Alphawave's technology into their products and workflows, the effort and expense required to transition to a different supplier become prohibitive. This lock-in effect directly diminishes the bargaining power of these customers.

Potential for In-House Development

The potential for very large customers, especially hyperscalers, to develop high-speed connectivity IP in-house presents a significant bargaining power lever. These entities often have substantial R&D budgets and the technical expertise to replicate or even surpass existing solutions. For instance, major cloud providers are known to invest heavily in custom silicon to optimize their data center operations. This capability acts as a constant pressure on Alphawave Semi.

This threat compels Alphawave Semi to maintain a competitive edge through continuous innovation and cost optimization. Failing to offer superior performance or value could incentivize these powerful clients to pursue internal development routes. In 2024, the trend of hyperscalers increasing their custom silicon efforts, particularly in AI and networking, underscores this dynamic.

- In-house Development Threat: Large customers like hyperscalers can leverage their financial and technical resources to develop critical IP internally.

- Competitive Pressure: This capability forces Alphawave Semi to constantly innovate and offer superior, cost-effective solutions to retain business.

- Market Trend: Hyperscalers' increasing investment in custom silicon in 2024 highlights the growing relevance of this bargaining power.

Customer Switching Costs

Once Alphawave Semi's intellectual property (IP) is deeply embedded within a customer's intricate chip design, the hurdles to switching to an alternative provider become considerable. These switching costs encompass not only the direct expenses of re-designing the chip but also the significant effort and time required for extensive re-validation processes. Furthermore, such transitions can lead to unwelcome delays in bringing new products to market, a critical factor in the fast-paced semiconductor industry.

These substantial switching costs serve as a powerful anchor, making it economically and operationally challenging for customers to move away from Alphawave Semi's solutions. This sticky customer base significantly strengthens Alphawave Semi's bargaining power, as the cost of disengagement outweighs the potential benefits of switching for many clients.

- High Re-design Expenses: Integrating new IP into an existing chip architecture requires significant engineering resources and time, often running into millions of dollars.

- Extensive Re-validation Needs: Chip designs must undergo rigorous testing and certification to ensure functionality and reliability, a process that can take many months.

- Time-to-Market Penalties: Delays caused by switching IP providers can result in missed market opportunities and lost revenue for customers.

- Alphawave Semi's 2023 Revenue: The company reported revenues of $375.9 million in 2023, demonstrating its established presence and the value customers derive from its IP.

Navigating Customer Power: Deep Ties vs. In-House Threats

While Alphawave Semi's customers are concentrated, their bargaining power is somewhat mitigated by the deep integration and high switching costs associated with Alphawave's essential connectivity IP. The company's reliance on long-term licensing and co-development agreements further solidifies customer relationships, making it difficult for clients to easily switch providers without incurring significant re-design and re-validation expenses.

The threat of in-house development by large customers, particularly hyperscalers, remains a key factor. These entities possess the financial and technical capabilities to create their own high-speed connectivity solutions. This pressure compels Alphawave Semi to continuously innovate and offer compelling value propositions to retain its crucial client base, especially as hyperscalers intensified their custom silicon efforts in 2024.

| Customer Characteristic | Bargaining Power Impact | Alphawave Semi's Response/Mitigation |

|---|---|---|

| Customer Concentration (Top 5 = 36% of 2024 Revenue) | High | Deep integration, long-term agreements, high switching costs |

| Essential Technology (AI, Data Centers, 5G) | Low | Critical performance enabler, difficult to substitute |

| Switching Costs (Re-design, Re-validation, Time-to-Market) | Low | Significant financial and operational barriers to switching |

| In-house Development Threat (Hyperscalers) | High | Continuous innovation, competitive pricing, superior performance |

Full Version Awaits

ALPHAWAVE SEMI Porter's Five Forces Analysis

The document you see here is the complete, professionally written ALPHAWAVE SEMI Porter's Five Forces Analysis, offering a thorough examination of competitive forces within the semiconductor industry. What you're previewing is precisely the same document that will be available to you instantly after purchase, ensuring you receive the full, unedited analysis. This means no placeholders or samples; you get the exact, ready-to-use report for your strategic decision-making.

Rivalry Among Competitors

Presence of Established Industry Players

The high-speed connectivity and semiconductor IP market is a battleground, with giants like ARM, Synopsys, Cadence, and Rambus already firmly entrenched. These established players possess significant brand recognition, extensive patent portfolios, and deep customer relationships, making it challenging for newer entrants to gain traction.

Alphawave Semi operates within this fiercely competitive landscape, directly challenging these incumbents for market share. For instance, ARM's dominance in CPU IP is well-known, while Synopsys and Cadence lead in design tools and IP for complex SoCs. This means Alphawave Semi must constantly innovate and offer compelling value propositions to differentiate itself.

High Market Growth Driving Competition

The semiconductor IP market is booming, with projections indicating it will reach USD 11.2 billion by 2029, growing at a compound annual growth rate of 8.5% from 2024. This robust expansion fuels intense rivalry among players eager to secure significant market share.

Specifically, the high-speed interface IP segment is a hotbed of competition, expected to grow at an impressive CAGR of 13.50% between 2025 and 2032. Such rapid growth naturally attracts more competitors, intensifying the battle for innovation and market dominance.

Differentiation Through Continuous Innovation

Competitive rivalry in the semiconductor industry, particularly for companies like Alphawave Semi, is intensely fueled by the relentless pursuit of technological advancement. The focus is squarely on leading-edge process nodes, such as the highly sought-after 3nm and upcoming 2nm technologies, which dictate performance and efficiency. Furthermore, the race for higher data transmission speeds, exemplified by the move to 224G and 1.6T capabilities, and the adoption of new architectural paradigms like chiplets and the Universal Chiplet Interconnect Express (UCIe) standard, are critical battlegrounds.

Alphawave Semi strategically positions itself by highlighting its prowess in these advanced technological domains. Securing design wins with major customers is paramount, as these victories serve as tangible proof of their technological leadership and are essential for establishing and maintaining a competitive advantage in this fast-paced market. For instance, in 2023, the company announced significant design wins in the data center and enterprise networking sectors, underscoring their ability to capture market share through innovation.

Strategic Partnerships and Ecosystem Building

Competitive rivalry in the semiconductor industry is intensified by strategic partnerships, which allow companies to expand their market reach and enhance their product portfolios. Alphawave Semi actively cultivates these alliances to bolster its competitive position.

Alphawave Semi's strategic collaborations are crucial for building a robust ecosystem and achieving deeper market penetration. These partnerships are not merely transactional; they represent a commitment to co-innovation and shared growth within the broader semiconductor landscape.

- Key Partnerships: Alphawave Semi has established significant relationships with industry leaders like Siemens EDA, TSMC, Arm, and GlobalFoundries.

- Ecosystem Development: These alliances are fundamental to developing a comprehensive ecosystem that supports Alphawave Semi's advanced connectivity solutions.

- Market Penetration: Through these strategic collaborations, Alphawave Semi aims to accelerate its market penetration and solidify its presence across various segments of the semiconductor market.

Pressure on Pricing and Margins

Even with specialized high-speed IP, Alphawave Semi faces pricing pressure due to intense competition and the need to win crucial design contracts. This rivalry can squeeze profit margins, especially in more commoditized IP segments.

While Alphawave Semi is strategically focusing on higher-margin IP and custom silicon solutions built on advanced process nodes, the inherent competitive pressure remains a factor. This necessitates a constant drive for operational efficiency to maintain profitability.

- Competitive Intensity: The semiconductor IP market, while specialized, sees significant competition from established players and emerging companies, leading to pressure on pricing for IP licenses.

- Design Win Focus: The critical need to secure design wins with major semiconductor manufacturers can force IP providers to offer more competitive pricing structures.

- Margin Impact: Despite a strategic shift towards higher-margin offerings, the underlying competitive dynamics can still affect overall profitability and require careful cost management.

Semiconductor IP: High-Speed Growth Fuels Intense Rivalry

Competitive rivalry is a defining characteristic of the semiconductor IP sector, with Alphawave Semi contending against formidable established players like ARM, Synopsys, and Cadence. The market's rapid growth, projected to reach USD 11.2 billion by 2029, intensifies this competition, particularly in high-speed interface IP, which is expected to grow at a 13.50% CAGR from 2025 to 2032. This dynamic necessitates continuous innovation and strategic partnerships to secure design wins and maintain market share.

| Competitor | Key IP Areas | Market Position |

|---|---|---|

| ARM | CPU IP, System IP | Dominant in CPU IP, broad IP portfolio |

| Synopsys | Design Tools, SoC IP | Leader in EDA and IP for complex SoCs |

| Cadence | Design Tools, IP Solutions | Strong in EDA and IP for advanced chip design |

| Alphawave Semi | High-Speed Connectivity IP, Custom Silicon | Challenging incumbents with advanced interface IP |

SSubstitutes Threaten

In-House IP Development by Large Customers

A significant threat of substitution arises from large technology companies and hyperscalers. These entities have substantial financial backing and the technical prowess to develop their own high-speed connectivity intellectual property (IP).

For mission-critical or highly specialized components, these powerful customers might choose to build solutions in-house rather than licensing them from external providers like Alphawave Semi. This trend can be observed as hyperscalers increasingly design their own custom silicon for data centers, aiming for greater control and optimization.

Emergence of Alternative Interconnect Technologies

While high-speed data transfer currently leans on electrical and optical interconnects, the threat of substitutes looms from emerging technologies. Breakthroughs in areas like quantum communication or advanced wireless links could offer entirely new ways to transmit data, potentially bypassing traditional silicon IP reliance.

New material science discoveries could also pave the way for alternative interconnect solutions. For instance, research into novel conductive materials or advanced photonic integrated circuits might offer performance gains or cost advantages over existing technologies, impacting the demand for current interconnect solutions.

Standardization and Commoditization Risk

The increasing adoption of industry standards, like UCIe for chiplet interconnects, while fostering ecosystem growth, also carries the risk of commoditization. This standardization could make high-speed IP less unique, allowing more competitors to offer similar solutions. Consequently, Alphawave Semi's proprietary technologies might face a greater threat from substitutes if differentiation diminishes.

Lower-Performance, Cost-Effective Alternatives

For certain applications, customers may choose less sophisticated, more budget-friendly connectivity options if they don't need Alphawave Semi's top-tier performance. These alternatives, while not identical, can appeal to market segments where advanced IP is unnecessary, potentially reducing Alphawave Semi's available market. For instance, in the embedded systems market, where cost is a primary driver, simpler microcontrollers with integrated basic connectivity might be preferred over high-performance chipsets. The global embedded systems market was valued at approximately USD 100 billion in 2023 and is projected to grow, indicating a substantial segment where cost-effective alternatives are prevalent.

These lower-performance substitutes can exert pressure by offering a "good enough" solution at a significantly lower price point. This is particularly relevant in markets where the total cost of ownership is a critical factor. Consider the automotive sector, where the demand for advanced connectivity is rising, but cost constraints in lower-end vehicle models can still favor less feature-rich solutions. In 2024, the automotive semiconductor market faced pricing pressures, with some segments seeing increased demand for cost-optimized components.

The threat is amplified when these alternatives are readily available and meet the basic functional requirements of a significant portion of the market. For example, standard Ethernet or USB solutions can serve many data transfer needs without the specialized high-speed SerDes technology Alphawave Semi offers. This means that while Alphawave Semi dominates high-bandwidth applications, a substantial market share for basic connectivity remains accessible to competitors with more commoditized offerings.

- Market Segmentation: Lower-performance alternatives are most effective in market segments where cost is a primary concern and extreme bandwidth is not required.

- Cost Sensitivity: Applications with tight budget constraints are more likely to adopt these substitutes, impacting Alphawave Semi's pricing power.

- Availability of Alternatives: The widespread availability of simpler, cheaper connectivity solutions creates a constant competitive pressure.

- "Good Enough" Principle: If an alternative meets the core functional needs of a customer, the premium for higher performance may not be justified.

Shifts in Computing Architectures

A fundamental shift in computing architectures, moving away from current chiplet-based or traditional SoC designs, could represent a long-term threat to Alphawave Semi. If future computing paradigms significantly reduce the need for discrete high-speed interconnect IP, or integrate it differently within a system, the demand for Alphawave Semi's core offerings could diminish.

For instance, the rise of specialized AI accelerators or novel processing units might consolidate interconnect functions, lessening reliance on external IP providers. In 2024, the semiconductor industry continued to see significant R&D investment, with companies exploring new architectures to boost performance and energy efficiency. This ongoing innovation creates the potential for disruptive changes that could alter the market landscape for interconnect solutions.

- Computing Architecture Evolution: The industry is actively researching alternatives to current chiplet and SoC designs, potentially impacting the need for discrete interconnect IP.

- Demand Reduction Risk: If future architectures integrate interconnects internally or reduce their necessity, Alphawave Semi's core product demand could decline.

- R&D Investment: Significant R&D in 2024 focused on new computing paradigms, highlighting the potential for disruptive shifts in semiconductor design.

High-Speed IP Faces Diverse Substitute Threats

The threat of substitutes for Alphawave Semi's high-speed connectivity IP is multifaceted. Large technology companies and hyperscalers, with their deep pockets and technical expertise, are increasingly developing their own custom silicon, potentially bypassing third-party IP providers. This trend is particularly evident in data center designs where control and optimization are paramount.

Emerging technologies like quantum communication and advanced wireless links present entirely new paradigms for data transmission, potentially rendering current silicon IP reliance obsolete. Furthermore, breakthroughs in material science could yield alternative interconnect solutions with superior performance or cost advantages, directly challenging existing technologies.

The growing adoption of industry standards, such as UCIe for chiplets, while beneficial for ecosystem growth, also risks commoditizing high-speed IP. This standardization could erode the unique value proposition of proprietary technologies, making it easier for competitors to offer similar solutions and increasing the threat from substitutes. In 2024, the semiconductor industry saw continued focus on standardization efforts, underscoring this evolving competitive landscape.

Lower-performance, cost-effective alternatives also pose a significant threat, particularly in market segments where extreme bandwidth is not a necessity. For example, the global embedded systems market, valued around USD 100 billion in 2023, often prioritizes cost, making simpler connectivity solutions attractive. Similarly, in the automotive sector, cost constraints in lower-end models can favor less feature-rich components, a trend that saw pricing pressures in the automotive semiconductor market in 2024.

| Threat Category | Description | Impact on Alphawave Semi | Example | 2024 Market Context |

|---|---|---|---|---|

| In-house Development | Large tech firms designing custom silicon | Reduced demand for licensed IP | Hyperscalers designing custom data center chips | Continued investment in custom silicon by major cloud providers |

| Emerging Technologies | New communication methods | Potential obsolescence of current IP | Quantum communication, advanced wireless links | Significant R&D in next-generation communication technologies |

| Material Science | Novel conductive materials, photonics | Disruption of existing interconnect solutions | Advanced photonic integrated circuits | Ongoing research into new semiconductor materials and manufacturing techniques |

| Standardization | Industry-wide protocols like UCIe | Commoditization of IP, reduced differentiation | Chiplet interconnect standards | Increased focus on interoperability and open standards in chip design |

| Lower-Performance Alternatives | Cost-effective, less advanced solutions | Market share erosion in cost-sensitive segments | Standard Ethernet, USB for basic connectivity | Pricing pressures in cost-sensitive semiconductor markets like automotive |

Entrants Threaten

High Research and Development Investment

The semiconductor IP market, particularly for high-speed connectivity solutions, demands enormous and ongoing investment in research and development. Companies like Alphawave Semi operate in an environment where developing next-generation IP and chiplets for advanced manufacturing nodes requires substantial capital for specialized equipment, highly skilled engineering talent, and lengthy development cycles. This creates a significant financial hurdle for any potential new competitor seeking to enter the space.

Access to Advanced Foundry Capacity

New entrants face a formidable barrier in accessing advanced foundry capacity. Leading-edge semiconductor manufacturing is concentrated among a few key players, such as TSMC, Samsung, and Intel, with their advanced nodes often booked years in advance. For instance, TSMC's 3nm capacity for 2024 was largely allocated to major clients like Apple and Nvidia, leaving little room for newcomers.

Extensive IP Portfolio and Patent Protection

The threat of new entrants is significantly mitigated by Alphawave Semi's extensive intellectual property (IP) portfolio, which boasted over 240 silicon IPs by the close of 2024. This deep well of patented technology creates a substantial barrier for any new player attempting to enter the market.

Developing a comparable IP portfolio from scratch or acquiring the necessary licenses would be a monumental and costly undertaking for newcomers. Furthermore, navigating and avoiding infringement on Alphawave Semi's robust patent protection adds another layer of complexity, making it difficult for new entrants to establish a competitive foothold in this IP-driven industry.

Necessity of Established Customer Relationships

Gaining significant traction in the semiconductor market, particularly within the high-performance computing and AI sectors, hinges on cultivating deeply embedded relationships with Tier-1 customers and hyperscalers. These crucial partnerships are often characterized by protracted sales cycles and intricate, multi-stage design-in processes that can span years.

New entrants face a formidable barrier in replicating these established connections. Without the benefit of years of successful engagements, proven reliability, and the inherent trust that accompanies such history, market penetration becomes exceedingly challenging. For instance, a new chip manufacturer would struggle to displace incumbents who have secured multi-year supply agreements with major cloud providers, agreements often built on extensive co-development and rigorous qualification.

The difficulty for new entrants is amplified by the significant investment required to navigate these complex customer onboarding procedures.

- Long Sales Cycles: Semiconductor sales to major clients can take 18-36 months from initial contact to secured order.

- Design-In Processes: Integrating a new chip into a hyperscaler's product requires extensive testing and validation, often involving custom modifications.

- Customer Loyalty: Existing relationships foster loyalty, making it hard for new companies to break into the supply chain.

- High Switching Costs: For hyperscalers, changing chip suppliers involves significant re-engineering and recertification, increasing the barrier for new entrants.

Rigorous Qualification and Certification Processes

The semiconductor industry, particularly for products powering AI, data centers, and 5G infrastructure, is characterized by exceptionally rigorous qualification and certification processes. These aren't just formalities; they are critical gatekeepers ensuring the reliability, performance, and safety of components in demanding environments. For instance, qualifying a new chip for a major AI accelerator could involve thousands of hours of testing and validation, often costing millions of dollars.

New entrants face a significant hurdle in navigating these time-consuming and expensive procedures. A new company would need to invest heavily in testing equipment, personnel, and the certification fees themselves, significantly delaying their ability to bring products to market and compete effectively with established players who have already met these stringent requirements.

- Rigorous Testing: Products must pass extensive reliability, performance, and environmental stress tests, often exceeding industry standards.

- Customer Qualification: Major customers, like hyperscale data center operators or leading AI hardware manufacturers, have their own demanding qualification protocols that new suppliers must satisfy.

- Time and Cost: The entire qualification process can take 12-24 months and cost upwards of $5 million per product family, acting as a substantial barrier to entry.

Semiconductor IP: High Barriers Shield Established Players

The threat of new entrants in the semiconductor IP sector is considerably low due to the immense capital investment required for R&D, advanced manufacturing access, and building a robust IP portfolio. Alphawave Semi's extensive IP library, exceeding 240 silicon IPs by the end of 2024, acts as a significant deterrent, making it economically unfeasible for newcomers to replicate or license comparable technology.

Established relationships with Tier-1 customers and hyperscalers, coupled with lengthy sales cycles and rigorous qualification processes, further solidify existing market positions. For instance, securing a design win with a major cloud provider can take 18-36 months and involve millions in qualification costs, a hurdle most new entrants cannot overcome.

| Barrier Type | Description | Impact on New Entrants | Alphawave Semi's Position (as of 2024) |

| Capital Requirements | High R&D, advanced manufacturing access, specialized equipment | Extremely high | Significant investment in R&D and advanced node technology |

| Intellectual Property | Extensive patent portfolio, complex licensing | Very high | Over 240 silicon IPs, strong patent protection |

| Customer Relationships & Qualification | Long sales cycles, deep integration, rigorous testing | Very high | Established partnerships with Tier-1 customers and hyperscalers |

Porter's Five Forces Analysis Data Sources

Our ALPHAWAVE SEMI Porter's Five Forces analysis is built upon a robust foundation of data, drawing from industry-specific market research reports, financial filings from key semiconductor players, and expert analyses from reputable financial institutions.