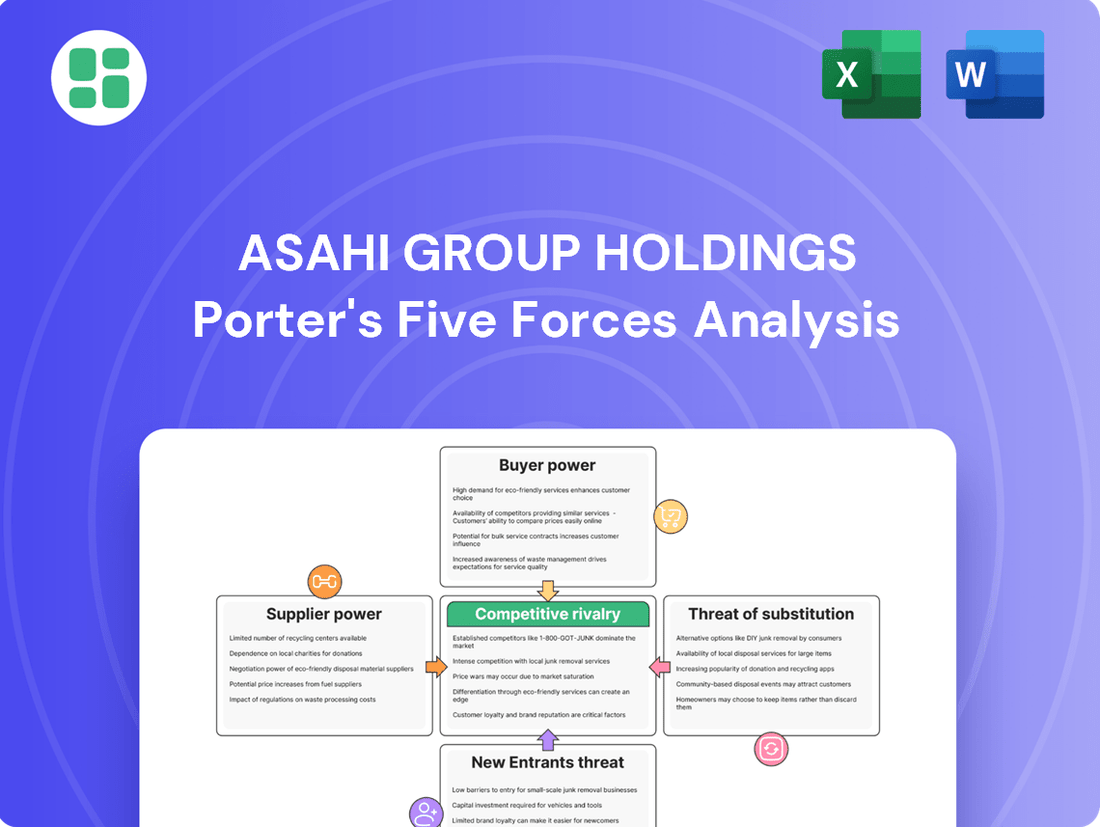

Asahi Group Holdings Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Asahi Group Holdings Bundle

From Overview to Strategy Blueprint

Asahi Group Holdings navigates a dynamic beverage and food landscape, where intense rivalry and the threat of substitutes significantly shape its strategic decisions.

The complete report reveals the real forces shaping Asahi Group Holdings’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Diversified Raw Material Sourcing

Asahi Group Holdings procures a broad spectrum of raw materials, such as malt, hops, water, and diverse components for its beverage and food lines. For widely available commodities, Asahi's substantial purchasing power likely grants considerable influence, thereby diminishing supplier leverage.

However, for specialized ingredients or distinctive hop varieties, the bargaining power of suppliers could be more pronounced. This scenario underscores the critical need for robust supplier relationships and proactive diversification strategies to mitigate potential risks and maintain cost stability.

Impact of Packaging Material Suppliers

Suppliers of essential packaging materials like glass bottles, aluminum cans, and PET plastics exert a degree of bargaining power, particularly as global demand for sustainable packaging solutions escalates. Asahi Group Holdings' strategic objective to incorporate more recycled content and transition to reusable or fully recyclable packaging by 2030 directly influences its reliance on suppliers who can provide these advanced, eco-friendly materials. This dependency can amplify the leverage of suppliers offering innovative and environmentally compliant packaging options.

Energy and Water Resource Dependence

Energy and water are fundamental to Asahi Group Holdings' production processes, making their cost and consistent availability significant factors in supplier leverage. The company's proactive approach to securing these resources is crucial for managing this aspect of supplier power.

Asahi is making substantial investments in sustainability, targeting 100% renewable electricity for all production facilities by the close of 2025. Furthermore, they are implementing rigorous water conservation programs across their operations to bolster resource security and reduce dependence on external utility providers.

Leverage of Global Procurement Initiatives

Asahi's establishment of Asahi Global Procurement Pte. Ltd. (AGPRO) in 2023 significantly enhances its leverage in global procurement. This initiative aims to consolidate purchasing power across its diverse operations, directly impacting supplier bargaining power.

AGPRO is projected to deliver substantial annual savings between 2024 and 2028. By centralizing procurement, Asahi can negotiate more favorable terms, effectively reducing the ability of individual suppliers to dictate prices or conditions.

- Centralized Procurement: AGPRO streamlines purchasing across regions and business units.

- Cost Optimization: The initiative targets significant annual savings, aiding in managing variable costs.

- Reduced Supplier Leverage: Consolidated purchasing power weakens individual supplier negotiation strength.

Labor Market Influence

The availability and cost of skilled labor, especially for specialized brewing and manufacturing positions, significantly influence supplier power in the labor market. Asahi Group Holdings, like many global companies, faces the challenge of rising labor costs, particularly evident in key operational regions such as Japan.

For instance, in 2024, Japan continued to experience labor shortages in various sectors, driving up wages. This trend puts pressure on companies to manage their workforce costs effectively. Asahi's strategic focus on attracting and retaining top talent, coupled with its ongoing global expansion and efforts to enhance operational efficiencies, serves as a crucial countermeasure to mitigate the impact of this supplier power.

- Skilled Labor Availability: Shortages in specialized brewing and manufacturing roles can increase labor costs.

- Rising Labor Costs: Increases in wages, particularly in markets like Japan, are a significant factor in 2024.

- Talent Management: Asahi's ability to attract and retain skilled employees is key to managing labor costs.

- Operational Efficiencies: Global expansion and efficiency improvements help offset rising labor expenses.

Supply Chain Leverage: Balancing Power and Dependency

Asahi Group Holdings' bargaining power with suppliers is a mixed bag. While its sheer scale and the establishment of AGPRO in 2023 grant significant leverage over common raw materials, specialized inputs and advanced packaging materials present a different dynamic. The company's commitment to sustainability, including its 2025 goal for 100% renewable electricity, means suppliers offering eco-friendly solutions hold more sway. Furthermore, rising labor costs, particularly in Japan where shortages were noted in 2024, also empower labor suppliers.

| Supplier Category | Asahi's Leverage Factors | Supplier Leverage Factors | Impact on Asahi |

|---|---|---|---|

| Common Raw Materials (e.g., malt) | High purchasing volume, AGPRO consolidation | Low (widely available) | Favorable pricing, reduced cost volatility |

| Specialized Ingredients/Hops | Long-term contracts, supplier diversification | Moderate (unique offerings) | Potential for higher costs, need for strong relationships |

| Packaging Materials (sustainable) | Commitment to sustainability goals | High (innovative, eco-friendly solutions) | Dependency on suppliers, potential cost increases |

| Energy & Water | Proactive resource management, conservation programs | Moderate (essential utilities) | Need for secure supply chains, cost management |

| Skilled Labor | Talent attraction/retention, operational efficiencies | Moderate to High (labor shortages, rising wages) | Increased labor costs, focus on workforce management |

What is included in the product

Asahi Group Holdings' Porter's Five Forces analysis reveals the intense competition in the beverage and food industry, the significant bargaining power of its buyers, and the moderate threat of new entrants, all of which shape its strategic landscape.

A dynamic dashboard that visualizes Asahi Group Holdings' Porter's Five Forces, instantly highlighting areas of intense competitive pressure and potential strategic vulnerabilities.

Customers Bargaining Power

Influence of Large Retail Chains and Distributors

Major retailers and distributors hold considerable sway over Asahi Group Holdings due to their substantial purchasing power. For instance, in 2024, large supermarket chains in Japan, key customers for Asahi's beverages, accounted for over 60% of domestic retail sales for many fast-moving consumer goods. This concentration means these entities can negotiate for better pricing and promotional support, directly influencing Asahi's profitability.

These powerful retail partners control crucial shelf space and distribution channels, giving them leverage in discussions about price adjustments. Asahi's ability to secure favorable terms for price revisions, a common practice to offset rising input costs, is often dependent on maintaining strong, long-term relationships with these key accounts. Failure to do so could limit market penetration and sales volume.

The bargaining power of these large customers can directly impact Asahi's profit margins. In 2023, industry reports indicated that major retailers in some European markets, where Asahi has significant operations, successfully pushed back against price increases from beverage manufacturers, leading to compressed margins for suppliers.

Consumer Price Sensitivity and Value Seeking

Individual consumers, though scattered, wield significant influence through their collective buying habits. In 2024, a notable increase in price sensitivity was observed across many markets, driven by ongoing economic pressures. Consumers are actively seeking the best value, readily switching to competitors if Asahi's pricing is perceived as unfavorable or if more attractive alternatives appear.

Shifting Consumer Preferences Towards Health and Wellness

Consumers are increasingly seeking out healthier beverage choices, such as low-alcohol, non-alcoholic, and functional drinks. This growing demand gives them more leverage, pushing companies like Asahi to adapt their product lines to meet these health-conscious preferences. For example, Asahi's 2023 revenue from its non-alcoholic beverages segment saw a significant uptick, reflecting this market shift.

Brand Loyalty and Premiumization Strategy

Asahi Group Holdings leverages a robust portfolio of globally recognized premium brands, including Asahi Super Dry and Peroni Nastro Azzurro, to foster strong consumer loyalty. This loyalty directly translates into reduced price sensitivity and a lower propensity for customers to switch brands, thereby mitigating their bargaining power.

Asahi's strategic commitment to premiumization, evident in its ongoing investments, further solidifies this brand equity. For example, in 2023, Asahi continued to focus on its core premium brands, with Asahi Super Dry seeing consistent growth in key international markets, reinforcing its premium positioning and customer attachment.

- Brand Strength: Asahi's premium brands like Asahi Super Dry and Peroni Nastro Azzurro command significant consumer recognition and preference.

- Reduced Price Sensitivity: Strong brand loyalty lessens the impact of price increases on consumer purchasing decisions.

- Lower Switching Behavior: Loyal customers are less likely to switch to competitors, even if offered lower prices.

- Premiumization Investment: Continued investment in marketing and product development for premium offerings reinforces brand value and customer commitment.

Information Availability and Digital Engagement

The digital age has dramatically amplified customer bargaining power by offering vast amounts of information. Consumers can now easily compare prices, read reviews, and research product features across numerous platforms, empowering them to make more informed purchasing decisions. This ease of access means customers are less reliant on individual brands for information and more likely to seek out the best value.

Digital engagement further shifts the balance. Customers actively interact with brands through social media, online forums, and direct messaging, providing immediate feedback and influencing purchasing trends. Asahi Group Holdings must actively participate in these digital conversations, building strong brand communities and demonstrating responsiveness to customer preferences to foster loyalty and mitigate the impact of increased customer power. For instance, in 2024, brands with strong social media engagement often see higher customer retention rates.

- Information Access: Customers can readily access competitor pricing and product details online.

- Digital Feedback: Online reviews and social media comments directly influence purchasing decisions.

- Brand Engagement: Asahi needs to actively manage its digital presence to build loyalty.

- Evolving Preferences: Rapidly changing consumer tastes, often identified through digital trends, require agile responses.

Retailer Power & Consumer Sensitivity Shape Beverage Markets

Major retailers and distributors hold considerable sway over Asahi Group Holdings due to their substantial purchasing power, directly influencing pricing and promotional terms. For example, in 2024, large supermarket chains in Japan, key customers for Asahi's beverages, accounted for over 60% of domestic retail sales for many fast-moving consumer goods, giving them significant leverage.

These powerful retail partners control crucial shelf space and distribution channels, impacting Asahi's ability to secure favorable terms for price revisions. Failure to maintain strong relationships with these key accounts could limit market penetration, as seen in 2023 when major European retailers successfully pushed back against price increases from beverage manufacturers, compressing supplier margins.

Individual consumers, while scattered, wield significant influence through collective buying habits and increasing price sensitivity, especially in 2024 due to economic pressures. Asahi's premium brands like Asahi Super Dry help mitigate this by fostering loyalty, reducing price sensitivity and the likelihood of customers switching, a strategy reinforced by continued investment in premiumization, as demonstrated by Super Dry's consistent growth in key international markets in 2023.

Preview the Actual Deliverable

Asahi Group Holdings Porter's Five Forces Analysis

This preview displays the comprehensive Porter's Five Forces analysis for Asahi Group Holdings, detailing the competitive landscape and strategic implications. The document you see here is the exact, professionally formatted analysis you will receive immediately after purchase, ensuring no discrepancies or missing information. It thoroughly examines the bargaining power of buyers and suppliers, the threat of new entrants and substitutes, and the intensity of rivalry within the beverage and food industries.

Rivalry Among Competitors

Intense Competition from Global and Local Players

The beverage sector Asahi Group Holdings operates in is incredibly competitive, with both massive global companies and smaller, regional businesses vying for market share. This intense rivalry spans across alcoholic drinks, non-alcoholic beverages, and even food items.

Asahi faces formidable competition from giants such as AB InBev, Heineken, Kirin, Sapporo, Coca-Cola, and PepsiCo. For instance, in 2023, AB InBev reported revenues of over $60 billion, highlighting the sheer scale of some of Asahi's rivals.

This competition is particularly sharp in established markets where expansion opportunities might be limited, forcing companies to fight harder for every consumer. In 2024, the global beverage market is projected to continue its growth, but the battle for dominance remains a constant challenge for all players.

High Stakes in Product Differentiation and Premiumization

Competitive rivalry within the alcoholic beverage industry, particularly for companies like Asahi Group Holdings, is intense, driven by a strong emphasis on product differentiation, innovation, and premiumization. This strategic focus aims to carve out distinct market positions and cater to discerning consumers.

Asahi's approach centers on elevating its high-value-added brands, with Asahi Super Dry serving as a prime example of its global premiumization strategy. By continuously enhancing the quality and unique appeal of such offerings, Asahi seeks to capture a larger share of the market and maintain healthy profit margins.

This premiumization push is crucial for Asahi as it navigates a competitive landscape where consumers are increasingly willing to pay a premium for superior taste, brand heritage, and unique consumption experiences. For instance, the global premium beer segment, which Asahi Super Dry targets, has shown consistent growth, with sales in key markets often outpacing the overall beer market.

Market Saturation and Consolidation Trends

Established markets, especially for traditional beer, are showing signs of maturity and saturation, resulting in slower volume growth. This sluggish growth environment often prompts industry consolidation through mergers and acquisitions as companies aim to increase their market share and benefit from economies of scale.

Asahi Group Holdings has been a proactive participant in this consolidation trend. For example, in 2016, Asahi completed the acquisition of SABMiller's European beer brands, including Peroni, Grolsch, and Meantime, for €2.55 billion. More recently, in 2024, Asahi continued its expansion by acquiring a majority stake in Australia's CUB (Carlton & United Breweries) from Anheuser-Busch InBev for approximately A$16.1 billion.

Innovation in Emerging Beverage Categories

Competitive rivalry in emerging beverage categories like non-alcoholic beer, functional drinks, and ready-to-drink (RTD) cocktails is fierce. Companies are in a constant race to launch new products and unique flavors to appeal to changing consumer tastes. For instance, the global RTD market was valued at approximately USD 26.9 billion in 2023 and is projected to grow significantly. Asahi Group Holdings needs to keep pace with this rapid innovation to maintain its market position.

This intense competition means that staying ahead requires continuous investment in research and development. Competitors are actively introducing novel ingredients and health-focused options, driving up the pace of product cycles.

- The non-alcoholic beer market alone saw substantial growth, with global sales reaching over USD 11 billion in 2023.

- Functional beverages, focusing on benefits like hydration and immunity, are also a major growth area, with the market expected to exceed USD 200 billion by 2027.

- Asahi's ability to adapt its portfolio and introduce compelling new offerings is critical to navigating this dynamic landscape.

Marketing, Distribution, and Brand Investment

The beverage industry, particularly for a company like Asahi Group Holdings, sees intense rivalry fueled by substantial investments in marketing, distribution, and brand building. Companies battle for consumer attention through extensive advertising campaigns and high-profile sponsorships. For instance, Asahi Super Dry and Peroni, key brands for Asahi, have leveraged global sports sponsorships to boost their international presence and drive sales growth. This focus on brand visibility is a critical element in differentiating products in a crowded market.

Distribution networks and strong relationships with retailers are equally crucial for competitive advantage. Ensuring products are readily available and prominently displayed on shelves is paramount. Asahi's strategic approach involves not only creating demand through marketing but also securing the physical presence of its beverages across diverse markets. Success in this area directly impacts market share and revenue generation, making it a constant area of focus for all major players.

- Marketing Investment: Asahi Group Holdings allocated approximately ¥100 billion (around $700 million USD based on recent exchange rates) to marketing and sales promotion expenses in its 2023 fiscal year, a notable increase from previous years, reflecting the heightened competition.

- Brand Sponsorships: The company's commitment to global sports sponsorships, including its prominent role with brands like Asahi Super Dry in events such as the Rugby World Cup, demonstrates a strategic effort to enhance brand equity and reach a wider audience.

- Distribution Reach: Asahi maintains a robust distribution network spanning over 100 countries, with particular strength in Asia and Oceania, supported by strategic partnerships and acquisitions to expand its market penetration and ensure product availability.

- Retailer Relationships: Building and maintaining strong relationships with key retailers, including major supermarket chains and convenience stores, is a cornerstone of Asahi's strategy, ensuring prime shelf space and promotional opportunities for its product portfolio.

Asahi's Global Battle: Intense Rivalry in Beverages

The competitive rivalry Asahi Group Holdings faces is intense, driven by global giants and regional players across alcoholic, non-alcoholic, and food sectors. This battle for market share is particularly fierce in mature markets, pushing companies towards premiumization and innovation in emerging categories like non-alcoholic beer and functional drinks.

Asahi's strategy includes acquiring brands and investing heavily in marketing and distribution to maintain its edge. For instance, its 2024 acquisition of CUB for A$16.1 billion and a ¥100 billion marketing budget in 2023 underscore the significant resources dedicated to staying competitive.

| Competitor | 2023 Revenue (Approx.) | Key Market Focus |

|---|---|---|

| AB InBev | $60+ billion | Global (Strong in Americas, Europe) |

| Heineken | €26.5 billion (2023) | Global (Strong in Europe, Asia) |

| Kirin Holdings | ¥2.0 trillion (approx. $13.3 billion USD in 2023) | Japan, Australia, Brazil |

| Sapporo Holdings | ¥368 billion (approx. $2.45 billion USD in 2023) | Japan, USA |

| Coca-Cola | $45.8 billion (2023) | Global (Non-alcoholic beverages) |

| PepsiCo | $91.5 billion (2023) | Global (Non-alcoholic beverages, snacks) |

SSubstitutes Threaten

Rise of Non-Alcoholic and Low-Alcohol Alternatives

The most substantial threat of substitutes for Asahi Group Holdings stems from the rapidly growing non-alcoholic (NA) and low-alcohol (LA) beverage sector. This includes a diverse range of products like NA beers, innovative functional drinks, and sophisticated mocktails, all catering to evolving consumer preferences.

These alternatives are gaining traction due to significant health and wellness trends and the rise of the 'sober-curious' movement, offering consumers comparable social experiences without the presence of alcohol. For instance, the global non-alcoholic beer market was valued at approximately USD 25.1 billion in 2023 and is projected to grow substantially.

Asahi is actively responding to this threat by strategically expanding its portfolio of NA and LA products, aiming to capture a share of this expanding market and mitigate the impact of substitutes on its traditional alcoholic beverage sales.

Competition from Other Beverage Categories

Asahi Group Holdings faces a significant threat from substitutes beyond direct beer and spirits competitors. A vast array of other beverages, including water, juices, teas, coffees, and energy drinks, can satisfy consumer needs for hydration and refreshment. The growing diversity and functional attributes of these alternatives, such as enhanced hydration or added vitamins, present a compelling case for consumers to shift their spending away from Asahi's core offerings.

Shift in Consumer Lifestyle and Health Consciousness

A significant societal shift towards healthier living and a heightened awareness regarding sugar and alcohol consumption are compelling consumers to explore alternatives. This trend affects both alcoholic beverages and sweet carbonated drinks, steering demand toward options perceived as more beneficial for well-being. For instance, the global low-alcohol and no-alcohol beverage market was valued at approximately $11.5 billion in 2023 and is projected to grow substantially, indicating a clear consumer preference for reduced alcohol intake.

This evolving consumer mindset directly challenges Asahi Group Holdings, as it influences purchasing decisions across its diverse product lines. The increasing demand for products with lower sugar content and reduced alcohol levels means that traditional offerings might face substitution from beverages like sparkling water, herbal teas, and functional drinks. Asahi needs to adapt its product development and marketing strategies to resonate with these changing consumer values and effectively counter the threat of substitutes.

Home Consumption and DIY Trends

The rise of home consumption and DIY trends presents a subtle but growing threat of substitutes for Asahi Group Holdings, particularly within the beverage sector. For dedicated craft beer enthusiasts, the ability to home brew or create homemade beverages offers a direct alternative to commercially produced options.

While this DIY movement doesn't pose a significant threat to Asahi's mass-market beer sales, it highlights a consumer desire for personalization and unique experiences. This trend could potentially impact Asahi's premium or niche product segments, where customization is more highly valued.

- Home Brewing Growth: The global homebrewing market, while niche, has seen steady growth, with many enthusiasts seeking to replicate or even surpass commercial offerings.

- DIY Beverage Kits: The availability of sophisticated DIY beverage kits, including those for beer, cider, and even spirits, makes it easier for consumers to experiment at home.

- Impact on Premium Segments: For Asahi's craft or specialty brands, the appeal of a unique, self-made beverage could draw some consumers away from purchasing premium products.

Cost-Effective Alternatives

In periods of economic strain, such as the inflation experienced in 2023 and continuing into 2024, consumers are increasingly drawn to more budget-friendly beverage options. This includes a noticeable shift towards private label brands offered by retailers or generic alternatives that provide similar products at a lower price point. This trend directly impacts Asahi Group Holdings by presenting a significant threat of substitution, as the emphasis on affordability can overshadow brand loyalty.

Asahi's strategic response involves a delicate balance between maintaining its premium brand image and adjusting pricing to reflect market realities. For instance, in 2023, Asahi Beverages in Australia implemented price increases on some of its key products, a move aimed at offsetting rising input costs while attempting to preserve perceived value. This premiumization strategy, coupled with careful price revisions, seeks to retain customers who may otherwise switch to cheaper substitutes.

- Consumer Shift to Value: Economic uncertainty and inflation in 2023-2024 have driven consumers toward more affordable beverage choices, including private label and generic brands.

- Brand Loyalty Erosion: The prioritization of cost savings over brand preference weakens the competitive advantage of established brands like those within Asahi's portfolio.

- Asahi's Counter-Strategy: Asahi Group Holdings is employing premiumization and strategic price adjustments to mitigate the threat of substitutes by emphasizing quality and managing value perception.

Beverage Substitutes: A Growing Market Challenge

The threat of substitutes for Asahi Group Holdings is multifaceted, extending beyond traditional alcoholic beverage competitors. A significant driver is the expanding non-alcoholic (NA) and low-alcohol (LA) beverage market, fueled by health consciousness and the sober-curious movement. For example, the global NA beer market reached approximately USD 25.1 billion in 2023, demonstrating substantial consumer interest in alternatives.

Beyond NA and LA options, a wide array of other beverages like water, juices, teas, coffees, and energy drinks can satisfy basic consumer needs for hydration and refreshment. These alternatives are increasingly offering functional benefits, further enticing consumers to shift spending away from Asahi's core products.

Economic pressures, such as the inflation experienced in 2023 and continuing into 2024, also bolster the threat of substitutes. Consumers are increasingly opting for more budget-friendly private label or generic brands, which can erode brand loyalty for established players like Asahi. This necessitates strategic pricing and value perception management.

| Beverage Category | 2023 Market Value (USD Billion) | Key Substitute Drivers |

|---|---|---|

| Non-Alcoholic Beer | ~25.1 | Health trends, sober-curious movement |

| Low/No Alcohol Beverages (Global) | ~11.5 | Wellness focus, reduced alcohol consumption |

| Other Refreshments (Water, Juice, Tea, Coffee) | Varies widely | Hydration, functional benefits, affordability |

Entrants Threaten

High Capital Investment Requirements

The beverage industry, especially large-scale brewing and bottling operations, demands significant upfront capital. Think about the cost of building and equipping breweries, setting up extensive distribution networks, and securing shelf space. For instance, establishing a modern brewery with a capacity of 1 million hectoliters can easily cost upwards of $100 million, a substantial hurdle for any newcomer.

These high capital requirements act as a powerful deterrent, effectively blocking many potential competitors from entering the market at a scale that could meaningfully challenge established giants like Asahi Group Holdings. This barrier ensures that only well-funded entities can even consider entering, thereby protecting existing market share.

Established Brand Loyalty and Marketing Spend

Established brand loyalty is a significant barrier for new entrants. Asahi Group Holdings, for instance, has cultivated decades of consumer recognition and trust, making it challenging for newcomers to gain market share. This loyalty is often reinforced by substantial marketing expenditures, which new companies must match or exceed to build comparable awareness and credibility.

Extensive Distribution Networks

New companies entering the beverage market face a formidable barrier in replicating Asahi's extensive distribution networks. These networks, encompassing everything from major retail chains to smaller convenience stores and on-premise establishments like bars and restaurants, represent years of relationship building and infrastructure investment. For instance, in 2024, Asahi's strong presence in key Asian markets like Japan and Australia meant that over 90% of their target consumer touchpoints were already secured.

Regulatory and Licensing Hurdles

The alcoholic beverage sector faces substantial regulatory and licensing barriers. For instance, in 2024, obtaining a liquor license in many U.S. states can take months and involve significant fees, sometimes exceeding tens of thousands of dollars depending on the jurisdiction and type of license. These stringent requirements, coupled with varying regional taxes and advertising prohibitions, substantially increase the capital and time investment needed for new entrants, thereby limiting the threat of new companies entering the market.

These complexities act as a significant deterrent. New players must navigate a labyrinth of compliance rules, which can include product safety standards, distribution channel regulations, and age verification protocols. For example, the Alcohol and Tobacco Tax and Trade Bureau (TTBT) in the United States imposes detailed labeling and advertising regulations that require careful adherence, adding another layer of operational complexity and cost.

The financial implications are considerable. Beyond licensing fees, new entrants must factor in the costs associated with legal counsel, compliance officers, and potentially lobbying efforts to understand and adapt to evolving regulations. This financial burden, combined with the time-consuming nature of regulatory approval processes, effectively raises the barrier to entry for potential competitors looking to challenge established players like Asahi Group Holdings.

Key aspects of these hurdles include:

- Licensing Fees: Costs can range from a few hundred to tens of thousands of dollars per license, varying by state and municipality.

- Compliance Costs: Investment in legal, regulatory, and quality control personnel and systems.

- Advertising Restrictions: Limitations on marketing channels and messaging can hinder brand building efforts.

- Taxation: Federal, state, and local excise taxes significantly impact pricing and profitability.

Economies of Scale and Cost Advantages

Asahi Group Holdings leverages its substantial global presence to achieve significant economies of scale. This translates into lower per-unit costs across production, raw material procurement, and research and development efforts. For instance, in 2023, Asahi's consolidated net sales reached ¥2,534.2 billion, indicating a vast operational footprint that smaller competitors cannot easily replicate.

These cost advantages present a formidable barrier for new entrants. Building a comparable production capacity and supply chain network would require massive capital investment, making it difficult for newcomers to compete on price. Asahi's established market share and operational efficiencies create a high hurdle for any potential new player aiming to gain a foothold.

- Economies of Scale: Asahi's global operations, with ¥2,534.2 billion in net sales in 2023, allow for cost efficiencies in production and procurement.

- Cost Advantages: Lower per-unit costs due to scale create a significant price competitiveness barrier for new entrants.

- R&D Efficiency: Shared research and development costs across a large organization reduce overall investment per innovation.

- Capital Investment Barrier: New entrants face substantial capital requirements to match Asahi's scale and cost structure.

Industry Fortress: Capital, Loyalty, & Scale Block New Competitors

The threat of new entrants for Asahi Group Holdings is generally considered low due to several significant barriers. High capital requirements for establishing production facilities, distribution networks, and securing market presence represent a substantial financial hurdle. For example, building a modern brewery can cost well over $100 million, a figure that deters many potential competitors from entering the market at a competitive scale.

Furthermore, established brand loyalty and extensive distribution networks, cultivated over years of operation, make it difficult for newcomers to gain traction. Asahi's strong market position in key regions, like Japan and Australia, where over 90% of consumer touchpoints are secured as of 2024, underscores this challenge. The regulatory landscape, including licensing and compliance, also adds complexity and cost, further limiting the ease of entry.

Economies of scale achieved by Asahi, supported by ¥2,534.2 billion in consolidated net sales in 2023, provide significant cost advantages that new entrants struggle to match. These factors collectively create a formidable barrier, protecting Asahi's market share from new competition.

| Barrier | Description | Impact on New Entrants | Example/Data Point |

|---|---|---|---|

| Capital Requirements | High upfront investment for breweries, distribution, and marketing. | Significant financial deterrent. | Brewery setup cost: >$100 million. |

| Brand Loyalty | Established consumer trust and recognition. | Requires substantial marketing to overcome. | Decades of brand building by Asahi. |

| Distribution Networks | Extensive reach across retail and on-premise channels. | Difficult to replicate, limiting market access. | Asahi's 90%+ consumer touchpoint coverage in key markets (2024). |

| Regulatory Hurdles | Licensing, compliance, taxes, and advertising restrictions. | Increases time, cost, and operational complexity. | US liquor license fees: Tens of thousands of dollars. |

| Economies of Scale | Lower per-unit costs due to large-scale operations. | Creates price competitiveness challenges. | Asahi's 2023 Net Sales: ¥2,534.2 billion. |

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis for Asahi Group Holdings is built upon a robust foundation of data, including Asahi's annual reports, investor presentations, and public financial statements. We supplement this with industry-specific market research reports and data from reputable financial information providers to capture the competitive landscape.