SK Telecom Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

SK Telecom Bundle

Go Beyond the Preview—Access the Full Strategic Report

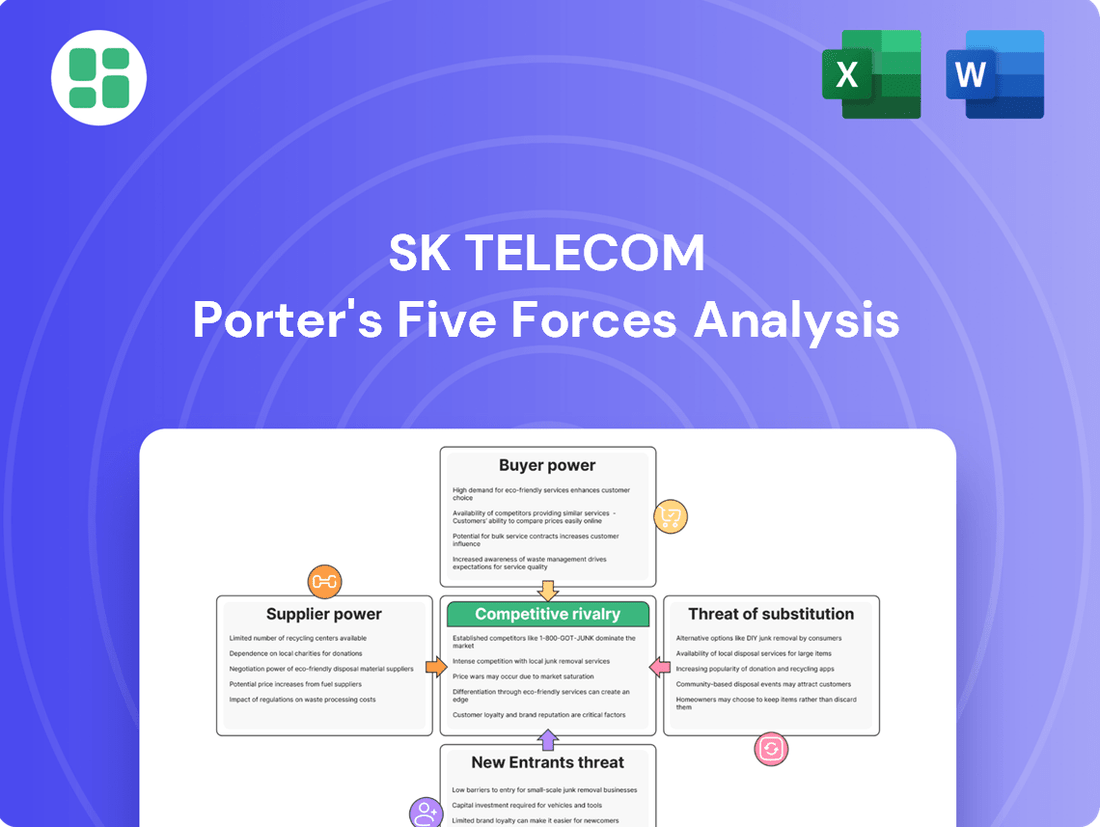

SK Telecom operates in a dynamic telecom landscape where intense rivalry among existing players significantly shapes its market position. Understanding the bargaining power of both its suppliers and its diverse customer base is crucial for strategic planning. Furthermore, the constant threat of new entrants and the availability of substitutes for its services present ongoing challenges.

Ready to move beyond the basics? Get a full strategic breakdown of SK Telecom’s market position, competitive intensity, and external threats—all in one powerful analysis.

Suppliers Bargaining Power

Concentration of Key Suppliers

The telecommunications sector, including SK Telecom, depends on a select group of global suppliers for vital network hardware and software, such as 5G equipment. Companies like Ericsson, Nokia, and Samsung Networks are major players in this space.

This limited number of suppliers, often referred to as an oligopoly, gives them considerable leverage. They can influence pricing and contract terms, especially when providing advanced technologies crucial for network upgrades.

Consequently, SK Telecom might encounter increased expenses or less advantageous conditions for acquiring these essential components due to this concentrated supplier market. For instance, in 2024, the global 5G infrastructure market was dominated by a few key vendors, allowing them to command premium pricing.

Switching Costs for Infrastructure

SK Telecom faces significant supplier bargaining power due to the high switching costs associated with its network infrastructure. Replacing existing, deeply integrated hardware and software platforms requires immense capital expenditure, intricate technical integration, and can cause considerable operational disruptions. This makes it difficult and costly for SK Telecom to switch to alternative suppliers, thereby strengthening the position of its current vendors.

These substantial switching costs, often exacerbated by long-term contracts and the use of proprietary technologies, effectively lock SK Telecom into existing supplier relationships. For instance, the rollout of 5G infrastructure, which began in earnest in 2019, involved massive investments in new base stations and core network components from a limited number of major global vendors. These initial investments create a strong dependency, giving suppliers considerable leverage in future negotiations and pricing discussions.

Uniqueness of Technology and Inputs

Suppliers offering unique technologies like advanced AI or IoT modules vital for SK Telecom's expansion into new service areas hold significant leverage. If these inputs are proprietary and lack readily available substitutes, suppliers can dictate pricing and terms, impacting SK Telecom's operational costs and innovation pace.

Threat of Forward Integration

While direct forward integration by core telecom infrastructure suppliers is uncommon, the threat emerges from content and platform providers. These entities might bypass SK Telecom to offer services directly to consumers, potentially impacting SK Telecom's revenue streams in media and enterprise solutions. This possibility, however low, subtly influences supplier negotiations by adding a layer of strategic consideration.

For instance, in 2024, the growth of Over-The-Top (OTT) services, many of which are offered by content providers with direct consumer access, highlights this dynamic. These platforms, by controlling the user interface and content delivery, can reduce reliance on traditional telecom carriers for monetization. This shifts some bargaining power back to these content creators, even if they aren't directly integrating into network infrastructure.

- Content providers bypassing carriers: Platforms like Netflix or Disney+ directly serve consumers, reducing reliance on telecom infrastructure for customer relationships and revenue.

- Impact on SK Telecom's services: This bypass can affect SK Telecom's own media offerings and enterprise solutions that rely on content partnerships.

- Negotiation leverage: Even a low probability of forward integration by key suppliers can influence SK Telecom's terms with them.

Regulatory and Spectrum Dependencies

SK Telecom's bargaining power with suppliers is significantly influenced by regulatory and spectrum dependencies. The South Korean government, as the allocator of essential radio spectrum, holds considerable sway. This governmental control over a critical resource dictates licensing terms, fees, and usage rights, inherently limiting SK Telecom's negotiation leverage for this fundamental input.

The scarcity and government-controlled allocation of radio spectrum mean that SK Telecom, along with its competitors, must adhere to the terms set forth by the Ministry of Science and ICT. For instance, in the 2024 spectrum auction for 28 GHz band, the government set base prices and specific conditions, showcasing its supplier-like power. SK Telecom's ability to secure and utilize this spectrum directly impacts its service offerings and competitiveness, making the government a de facto powerful supplier.

- Governmental Spectrum Allocation: The South Korean government controls the allocation and licensing of radio spectrum, a vital resource for mobile network operators like SK Telecom.

- Regulatory Influence on Terms: Licensing fees, usage conditions, and renewal terms for spectrum are determined by government regulations, directly impacting SK Telecom's operational costs and strategic planning.

- Limited Negotiation Power: Due to the monopolistic nature of spectrum provision by the government, SK Telecom has minimal bargaining power in negotiating the terms of access to this essential input.

Suppliers Hold the Cards: SK Telecom's Bargaining Power Constraints

SK Telecom faces substantial bargaining power from its suppliers, particularly those providing advanced network hardware and software. The limited number of major global vendors for 5G equipment, such as Ericsson, Nokia, and Samsung Networks, creates an oligopoly, allowing them to dictate pricing and terms. This is further amplified by the high switching costs associated with deeply integrated network infrastructure, making it difficult and expensive for SK Telecom to change suppliers. For example, the significant investments made in 2024 for 5G network expansion solidified these dependencies.

Suppliers offering unique, proprietary technologies also wield considerable influence, as their components are critical for SK Telecom's innovation and expansion into new service areas. While direct forward integration by infrastructure suppliers is rare, the rise of Over-The-Top (OTT) content providers in 2024, who can bypass carriers to reach consumers directly, subtly shifts some negotiation leverage towards these content creators, impacting SK Telecom's revenue models.

The South Korean government, through its control over radio spectrum allocation, acts as a powerful de facto supplier. The terms, fees, and conditions set by the Ministry of Science and ICT for spectrum usage, as seen in the 2024 auctions, significantly limit SK Telecom's bargaining power for this essential resource.

| Supplier Type | Key Players | Bargaining Power Factors | Impact on SK Telecom |

|---|---|---|---|

| Network Hardware & Software | Ericsson, Nokia, Samsung Networks | Oligopolistic market, high switching costs, proprietary technology | Increased costs, less favorable terms, dependency on innovation pace |

| Content & Platform Providers | Netflix, Disney+, etc. | Direct consumer access, control over user interface | Potential revenue stream impact, reduced reliance on telecom infrastructure monetization |

| Government (Spectrum) | Ministry of Science and ICT (South Korea) | Monopolistic control over essential radio spectrum | Dictated licensing terms, fees, and usage rights; limited negotiation leverage |

What is included in the product

This analysis of SK Telecom's competitive landscape reveals the intense rivalry among mobile carriers, the significant bargaining power of customers and suppliers, the high barriers to entry for new players, and the constant threat of substitutes and new technologies.

SK Telecom's Porter's Five Forces analysis provides a clear, one-sheet summary of all competitive forces, perfect for quick strategic decision-making regarding market positioning and potential threats.

Customers Bargaining Power

High Customer Churn Potential

South Korea's mobile market, with a penetration rate exceeding 100% as of 2024, is highly saturated. This maturity fuels fierce competition among SK Telecom, KT, and LG U+, making customer retention a critical challenge.

Mobile number portability is a significant factor, allowing customers to switch providers with minimal hassle. This ease of switching directly amplifies customer bargaining power, as they can readily seek better deals or services elsewhere.

SK Telecom's customers are highly price-sensitive and actively seek value-added services. In 2023, average monthly revenue per user (ARPU) for the Korean mobile market hovered around 30,000 KRW, indicating that even small price differences can influence switching decisions.

Availability of Substitutes for Communication

The widespread availability of Over-The-Top (OTT) communication applications significantly amplifies the bargaining power of SK Telecom's customers. Services like KakaoTalk, WhatsApp, and FaceTime offer free or low-cost alternatives to traditional voice and SMS, directly impacting the perceived value of core telecom offerings.

In 2024, the continued dominance of these OTT platforms means customers can easily bypass standard carrier charges for messaging and calls, provided they have data access. This shift empowers consumers to seek better deals on data plans, as the essential communication function is increasingly fulfilled by third-party applications, thereby reducing customer loyalty to a single provider based on basic communication features alone.

Transparency of Information

Customers today have unprecedented access to information about mobile service plans, pricing, and ongoing promotions from all major carriers. This readily available data, often found on dedicated comparison websites and through extensive advertising campaigns, significantly empowers consumers.

This transparency directly impacts SK Telecom by increasing customer bargaining power. With easy access to competitor offerings, customers can quickly identify the best value, forcing SK Telecom to maintain competitive pricing and attractive deals to retain subscribers.

For instance, in 2024, the widespread use of online comparison tools means a customer can see, in real-time, how SK Telecom's 5G plans stack up against KT and LG Uplus. This direct comparison makes it harder for any single provider to command premium pricing without offering demonstrably superior service or unique benefits.

Bundling of Services

SK Telecom's bundling strategy, integrating mobile, fixed-line, broadband, and media services, presents a dual impact on customer bargaining power. By creating a more integrated and potentially cost-effective package, SK Telecom aims to increase customer loyalty and raise switching costs. However, this also means customers are evaluating the entire bundle's value proposition.

This bundling approach can empower customers if they perceive a superior alternative from a competitor. For instance, if another provider offers a more compelling combined package, customers gain significant leverage to negotiate better terms or switch, thereby increasing their bargaining power.

SK Telecom's 2024 performance highlights the importance of these bundles. In Q1 2024, SK Telecom reported a significant increase in its broadband subscriber base, partly attributed to its bundled offerings. This suggests that while bundling can create customer stickiness, the overall market competitiveness and the attractiveness of rival bundles remain critical factors influencing customer power.

- Bundling creates customer stickiness by increasing switching costs, but also makes customers evaluate the total value.

- A more attractive bundle from a competitor empowers customers to demand better terms or switch.

- SK Telecom's Q1 2024 broadband subscriber growth indicates the effectiveness of bundled services in retaining customers.

Large Enterprise Customer Influence

Large enterprise customers wield considerable influence over SK Telecom due to their substantial contract volumes and intricate requirements for digital infrastructure and specialized solutions. These clients often demand customized offerings, dedicated technical support, and aggressive pricing, enabling them to secure more advantageous terms for SK Telecom's business services.

For instance, in 2023, SK Telecom reported that its enterprise solutions segment continued to grow, driven by demand from large corporations for 5G private networks and AI-powered B2B services. The ability of these major clients to switch providers or consolidate services if terms are not met directly translates into significant bargaining power.

- High Switching Costs for Enterprises: Large enterprises often invest heavily in integrating SK Telecom's services into their existing infrastructure, making switching to a competitor costly and disruptive.

- Volume-Based Discounts: The sheer volume of services consumed by enterprise clients allows them to negotiate significant volume-based discounts, impacting SK Telecom's revenue per user for these segments.

- Demand for Customization: Enterprise clients frequently require bespoke solutions, giving them leverage as SK Telecom must allocate resources to meet these specific needs, often in exchange for long-term commitments.

Customer Bargaining Power Shapes South Korea's Mobile Landscape

The bargaining power of SK Telecom's customers is substantial, driven by market saturation and the availability of alternatives. In South Korea's highly competitive mobile landscape, where penetration rates exceeded 100% in 2024, customers can easily switch providers thanks to mobile number portability. This ease of switching, coupled with the widespread adoption of Over-The-Top (OTT) communication apps like KakaoTalk, significantly reduces customer reliance on traditional carrier services for basic communication.

Customers are also empowered by increased price transparency. In 2024, readily available information on competitor pricing and promotions through comparison websites forces SK Telecom to offer competitive deals. Even small differences in monthly charges, with 2023 ARPU around 30,000 KRW, can influence switching decisions. SK Telecom's bundling strategies, while aiming to increase loyalty, also mean customers evaluate the entire package, granting them leverage if a competitor offers a more attractive bundle.

| Factor | Impact on SK Telecom | Customer Leverage |

|---|---|---|

| Market Saturation (>100% penetration in 2024) | Intensified competition, focus on retention | High ability to switch for better offers |

| Mobile Number Portability | Reduced switching costs for customers | Easy access to competitor plans |

| OTT App Dominance (KakaoTalk, WhatsApp) | Reduced perceived value of basic voice/SMS | Focus shifts to data plans, less loyalty to core services |

| Price Sensitivity (2023 ARPU ~30,000 KRW) | Need for competitive pricing | Leverage to negotiate lower prices or better value |

| Information Transparency (Comparison Websites) | Pressure to maintain competitive pricing and promotions | Ability to quickly identify best deals |

| Bundling Strategies | Potential for increased switching costs, but also evaluation of total value | Power to demand better terms if rival bundles are superior |

Same Document Delivered

SK Telecom Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. This comprehensive Porter's Five Forces analysis of SK Telecom delves into the competitive landscape, assessing the bargaining power of buyers and suppliers, the threat of new entrants and substitutes, and the intensity of rivalry within the South Korean telecommunications market. The detailed examination provides actionable insights into SK Telecom's strategic positioning and potential challenges.

Rivalry Among Competitors

Market Saturation and Penetration

The South Korean telecom market is incredibly crowded, with mobile penetration exceeding 100% and broadband penetration also very high. This means SK Telecom, along with rivals KT and LG U+, are mostly fighting over the same customers rather than finding new ones. In 2023, SK Telecom reported a total mobile subscriber base of approximately 31.3 million, highlighting the intense competition for each user.

Homogeneity of Core Services

While SK Telecom strives to differentiate through advanced 5G, AI services, and unique content offerings, the fundamental mobile and broadband services remain largely commoditized. This homogeneity means that for many consumers, the core functionality offered by SK Telecom, KT, and LG Uplus is quite similar, pushing competition towards price and promotional deals. For instance, in 2023, the South Korean mobile market saw intense price wars, with carriers offering significant discounts on plans and device subsidies to attract and retain subscribers, impacting overall ARPU.

High Fixed Costs and Capacity

SK Telecom, like other major telecom players, faces intense competition driven by high fixed costs. Building and maintaining robust network infrastructure, securing expensive spectrum licenses, and investing heavily in R&D for advanced technologies such as 5G and AI represent substantial capital outlays. For instance, in 2023, SK Telecom invested approximately 1.1 trillion Korean won in its network infrastructure, a significant portion of which goes towards 5G expansion.

These massive fixed costs necessitate high capacity utilization to achieve profitability. Consequently, companies aggressively compete to acquire and retain subscribers, aiming to spread these costs over a larger customer base. This dynamic inherently fuels fierce rivalry as each player strives to capture market share and maximize the return on their substantial investments, making price wars and aggressive marketing campaigns common tactics.

Aggressive Innovation and Diversification

SK Telecom and its competitors are heavily investing in areas beyond traditional mobile services. This includes significant outlays in artificial intelligence (AI), the Internet of Things (IoT), cloud computing, and immersive metaverse platforms. For instance, SK Telecom's AI focus is evident in its AI semiconductor development and AI-powered services, aiming to differentiate itself in these nascent markets.

This strategic diversification into new technological frontiers creates intense competition. Companies are locked in a race to develop and deploy cutting-edge solutions, necessitating substantial research and development (R&D) budgets and the formation of key strategic alliances. The pursuit of leadership in these emerging sectors means rivals are constantly pushing the boundaries to secure future market share and technological advantage.

- AI Investment: SK Telecom reported significant investments in AI, with its AI semiconductor business showing growth potential.

- IoT Expansion: The company continues to expand its IoT offerings, connecting more devices and services across various industries.

- Metaverse Ventures: SK Telecom is actively developing its metaverse platform, aiming to capture early market share in this evolving digital space.

Regulatory Influence and Market Structure

The South Korean government, through agencies like the Ministry of Science and ICT, significantly influences SK Telecom's competitive environment. Spectrum allocation decisions, for instance, can create advantages or disadvantages for carriers. In 2024, the government continued its focus on 5G network expansion and spectrum efficiency, potentially impacting the cost of spectrum for all players.

South Korea's mobile market is an oligopoly, dominated by SK Telecom, KT, and LG Uplus. Regulatory policies aim to foster fair competition and prevent monopolistic practices. For example, regulations around wholesale access or pricing can alter the competitive balance, even within an oligopolistic structure. This external oversight is a critical factor in strategic planning.

Regulatory interventions can also drive technological advancements. Government incentives or mandates for deploying next-generation technologies like 6G or specific IoT solutions can shape investment priorities for SK Telecom and its rivals. These policy directions are crucial for understanding future competitive pressures and opportunities.

Key regulatory influences include:

- Spectrum Allocation: The government determines which frequency bands are available and to whom, impacting network capacity and deployment strategies.

- Pricing Regulations: While generally a market-driven sector, regulators can intervene on service pricing or interconnection fees if deemed unfair.

- Market Entry Policies: Rules governing new entrants or mergers and acquisitions can alter the existing market structure.

- Technology Mandates: Government push for specific technological rollouts, such as 5G or future 6G development, guides carrier investment.

South Korea's Telecom Battle: A Fight for Every Subscriber

Competitive rivalry within South Korea's telecom sector is exceptionally intense, primarily due to a saturated market where SK Telecom, KT, and LG Uplus vie for the same customer base. With mobile penetration exceeding 100%, the focus shifts from acquisition to retention, fueling aggressive competition. In 2023, SK Telecom’s 31.3 million subscribers underscore the battle for each user.

The core mobile and broadband services are largely commoditized, leading rivals to compete fiercely on price and promotions. This is evident in the 2023 market dynamics, characterized by significant discounts and device subsidies, which directly impact average revenue per user (ARPU).

SK Telecom and its competitors face substantial fixed costs associated with network infrastructure, spectrum licenses, and R&D. For instance, SK Telecom’s 2023 network investment of approximately 1.1 trillion Korean won for 5G expansion highlights these capital demands. High capacity utilization is crucial for profitability, intensifying the drive to capture market share.

| Metric | SK Telecom (2023) | KT (2023) | LG Uplus (2023) |

|---|---|---|---|

| Mobile Subscribers (Millions) | 31.3 | 22.2 | 18.1 |

| Network Investment (KRW Trillion) | ~1.1 (5G focused) | ~1.0 (estimated) | ~0.9 (estimated) |

| ARPU (KRW) | ~25,000-26,000 (estimated) | ~24,000-25,000 (estimated) | ~23,000-24,000 (estimated) |

SSubstitutes Threaten

Over-The-Top (OTT) Communication Services

Over-the-top (OTT) communication services, such as KakaoTalk, WhatsApp, and Signal, present a significant threat by offering free messaging and voice/video calls via the internet. This directly competes with SK Telecom's traditional SMS and voice services. For instance, in 2023, the global OTT messaging market was valued at over $100 billion, highlighting its substantial reach.

While these OTT platforms depend on SK Telecom's data infrastructure, they cannibalize revenue streams previously generated from per-minute or per-message charges. This shift compels SK Telecom to reorient its business model, focusing on data consumption as the primary revenue driver rather than traditional voice and messaging fees.

Wi-Fi and Public Hotspot Connectivity

The widespread availability of free or low-cost Wi-Fi in homes, offices, and public spaces significantly reduces the demand for cellular data. In 2024, a substantial portion of internet usage, particularly for data-intensive tasks, occurs over Wi-Fi, diminishing the necessity of cellular plans for many users.

This trend directly impacts SK Telecom by diverting data traffic away from its cellular networks. Users increasingly opt for Wi-Fi to avoid data charges or overage fees, especially when indoors or in areas with readily accessible Wi-Fi, thereby eroding a key revenue stream for the company.

Alternative Entertainment and Media Platforms

The rise of streaming services like Netflix, YouTube, and Disney+ presents a significant threat of substitutes for traditional pay-TV and even SK Telecom's own on-demand content offerings. These platforms provide extensive libraries and cater to diverse user preferences, directly competing for consumer attention and entertainment budgets.

While SK Telecom has its own media platforms, the sheer accessibility and variety of third-party streaming options can dilute customer engagement with carrier-specific media. This trend directly impacts the appeal of bundled services that include traditional media and can erode potential content revenue streams for SK Telecom.

For instance, in 2023, global streaming service revenue was projected to exceed $100 billion, highlighting the massive scale and consumer adoption of these alternatives. This robust market growth underscores the competitive pressure SK Telecom faces in retaining subscribers for its bundled media packages.

Enterprise Private Networks and Cloud Solutions

The increasing adoption of private 5G networks and direct cloud connectivity presents a significant threat of substitutes for SK Telecom's enterprise private network services. Businesses can now establish their own dedicated networks, particularly for specialized use cases like industrial IoT or mission-critical operations, thereby reducing their reliance on public telecom infrastructure.

This shift allows enterprises to bypass traditional connectivity offerings, opting for tailored solutions that may provide greater control and performance for specific needs. For instance, a manufacturing plant might deploy a private 5G network to ensure ultra-low latency for its robotic automation systems, a service that could be challenging to guarantee on a shared public network.

This trend directly impacts SK Telecom's B2B revenue streams, as companies invest in on-premise or edge computing solutions that integrate private network capabilities. By 2024, the global private wireless market, encompassing private LTE and 5G, was projected to reach substantial figures, indicating a growing appetite for these alternative connectivity models.

- Reduced Dependency: Enterprises can achieve greater autonomy over their network infrastructure for critical applications.

- Tailored Solutions: Private networks offer customized performance characteristics, such as guaranteed low latency and high bandwidth, often exceeding public network capabilities for specific use cases.

- Cost-Effectiveness: For high-volume data users or specific operational needs, private networks can become more cost-effective in the long run compared to paying for extensive public network services.

- Market Growth: The private wireless market is expanding rapidly, with analyst reports in 2024 forecasting significant growth, underscoring the viability of these substitutes.

Evolving Communication Technologies

Emerging communication technologies, like satellite internet services such as Starlink, pose a potential long-term threat of substitution for traditional mobile network operators like SK Telecom. While currently more focused on providing internet access in remote areas, the continued development and expansion of these technologies could eventually offer alternative connectivity solutions, even in more populated regions.

These evolving technologies, including advancements in mesh networking, could provide decentralized and potentially more resilient communication options. For instance, satellite internet providers are rapidly expanding their global coverage, aiming to reach millions of new users. As of early 2024, Starlink alone has activated over 2.7 million subscribers globally, demonstrating significant market penetration and technological capability.

- Satellite Internet Growth: Starlink's subscriber base exceeded 2.7 million globally by early 2024, indicating a growing alternative to terrestrial networks.

- Mesh Network Potential: Future mesh network deployments could offer localized, off-grid communication alternatives.

- Underserved Market Impact: These technologies are particularly disruptive in areas where traditional infrastructure is lacking or costly to deploy.

- Long-Term Competitive Pressure: While not an immediate threat to SK Telecom's core urban market, these substitutes could erode market share over time if they become more competitive on price and performance.

Telecom Revenue Under Siege: OTT, Wi-Fi, Streaming, Private 5G

OTT communication services like KakaoTalk and WhatsApp offer free messaging and calls, directly impacting SK Telecom's traditional revenue from SMS and voice. The global OTT messaging market exceeded $100 billion in 2023, demonstrating its significant reach and competitive pressure.

The widespread availability of free Wi-Fi further erodes demand for cellular data, as users increasingly opt for Wi-Fi to avoid charges. This trend diverts data traffic from SK Telecom's networks, diminishing a key revenue source.

Streaming services like Netflix and YouTube substitute for traditional pay-TV and SK Telecom's own content offerings, with global streaming revenue projected to surpass $100 billion in 2023. This broad adoption challenges SK Telecom's ability to retain subscribers for bundled media services.

Private 5G networks and direct cloud connectivity are emerging as substitutes for SK Telecom's enterprise services, allowing businesses to build their own networks. The global private wireless market was projected for substantial growth in 2024, indicating a rising preference for these tailored, independent connectivity solutions.

Entrants Threaten

High Capital Investment Requirements

Establishing a nationwide telecommunications network, a necessity for competing with SK Telecom, demands astronomical capital expenditure. This includes securing crucial spectrum licenses, deploying extensive base stations, laying fiber optic cables, and building robust data centers. For instance, South Korea's 5G spectrum auctions alone have historically involved billions of dollars, creating an immense financial barrier.

This substantial upfront investment serves as the most significant deterrent for potential new entrants looking to challenge SK Telecom's market position. The sheer scale of capital required effectively shields incumbent players like SK Telecom from immediate new competition.

SK Telecom's already established and extensive infrastructure, built over years with continuous investment, represents a formidable competitive advantage. This existing network allows for economies of scale and operational efficiencies that new entrants would struggle to match without comparable capital outlays.

Strict Regulatory and Licensing Frameworks

The South Korean telecom sector presents a formidable barrier to entry due to its strict regulatory and licensing frameworks. Obtaining the necessary spectrum allocation and operational permits is a complex, lengthy, and often politically influenced process, significantly deterring new competitors.

For instance, in 2021, the South Korean government's auction for 5G spectrum saw significant investment, with the three major carriers committing billions of dollars. This high upfront cost and the rigorous qualification criteria underscore the substantial financial and administrative hurdles new entrants must overcome.

Established Brand Loyalty and Network Effects

SK Telecom, like other major telecom providers, benefits significantly from established brand loyalty and robust network effects. Incumbent players have cultivated strong brand recognition and customer bases over many years, often supported by extensive loyalty programs. For instance, as of early 2024, SK Telecom reported a subscriber base exceeding 30 million, a testament to its long-standing presence and customer retention efforts.

New entrants would face considerable difficulty in luring subscribers away from these deeply entrenched operators. The value of a mobile network increases with the number of users it has, a phenomenon known as network effects. This makes it harder for newcomers to achieve critical mass and offer a competitive value proposition from the outset, as their service would initially be less appealing due to a smaller user community.

Access to Distribution Channels

SK Telecom's formidable distribution network presents a significant barrier to new entrants. The company operates a vast array of retail stores, robust online sales channels, and strategic partnerships, all designed to reach a wide customer base efficiently. For instance, as of the first half of 2024, SK Telecom maintained over 1,000 physical retail locations across South Korea, complemented by a highly trafficked e-commerce platform.

Establishing a comparable distribution and customer support infrastructure requires substantial capital investment and time. New competitors would need to replicate this extensive physical and digital presence, a task that is both costly and complex. This difficulty in accessing and serving a broad market segment effectively deters potential new players from entering the telecommunications market.

The threat of new entrants specifically concerning access to distribution channels is therefore moderate to low. SK Telecom's established infrastructure, which includes its extensive retail footprint and digital engagement platforms, makes it challenging for newcomers to gain immediate market traction. This entrenched advantage limits the ease with which new companies can acquire customers and provide comprehensive service.

- Extensive Retail Presence: SK Telecom operates over 1,000 retail stores nationwide, providing a physical touchpoint for sales and customer service.

- Online Sales Channels: The company leverages a sophisticated e-commerce platform for direct sales and customer engagement.

- Partnership Networks: Strategic alliances further broaden SK Telecom's reach and service capabilities.

- High Barrier to Entry: Replicating this comprehensive distribution and support system demands significant investment and time, deterring new market entrants.

Economies of Scale and Experience Curve

Existing mobile operators, including SK Telecom, possess substantial economies of scale. This advantage is evident in their network infrastructure, equipment procurement, and customer service operations, enabling them to achieve lower per-unit costs. For instance, in 2023, SK Telecom reported substantial capital expenditures in network upgrades, a cost that would be prohibitively high for a new entrant to replicate at scale from inception.

New entrants would face a significant cost disadvantage, as they would need to build out their own infrastructure or lease capacity at higher initial rates. This lack of established scale makes it difficult to compete on price with incumbents who have amortized their network investments over millions of subscribers. In the first quarter of 2024, SK Telecom served over 32 million mobile subscribers, a user base that new entrants would take years to approach.

Furthermore, the experience curve plays a crucial role. SK Telecom and its peers have decades of experience in optimizing network performance, managing customer churn, and developing innovative services. This accumulated expertise translates into operational efficiencies and a deeper understanding of market dynamics that new players would lack, creating a substantial barrier to entry.

- Economies of Scale: SK Telecom's large subscriber base (over 32 million in Q1 2024) allows for cost efficiencies in network operations and procurement.

- Experience Curve Advantage: Decades of operational experience in network management and service delivery provide SK Telecom with a competitive edge.

- Capital Investment Barrier: The immense capital required to build a comparable network infrastructure presents a significant hurdle for potential new entrants.

- Cost Disadvantage for Newcomers: New entrants would initially operate at a higher cost per subscriber compared to established players.

South Korea's Telecom: A Fortress Against New Entrants

The threat of new entrants in South Korea's telecommunications market is significantly mitigated by the astronomical capital expenditure required to establish a nationwide network. This includes billions in spectrum licenses and infrastructure development, creating a substantial financial barrier. For example, 5G spectrum auctions alone represent immense upfront costs, effectively shielding incumbents like SK Telecom.

SK Telecom's established infrastructure, built over years, offers economies of scale and operational efficiencies that new entrants would struggle to match. Coupled with strict regulatory frameworks and licensing hurdles, these factors combine to make entry extremely challenging.

The company's extensive distribution network, with over 1,000 retail stores and a strong online presence as of mid-2024, further deters new players. Replicating this reach requires significant investment and time, limiting the ease with which newcomers can acquire customers.

Furthermore, SK Telecom benefits from decades of operational experience and a large subscriber base, exceeding 32 million in Q1 2024. This experience curve advantage and established network effects make it difficult for new entrants to compete effectively on price or service from the outset.

| Factor | Impact on New Entrants | SK Telecom's Position |

|---|---|---|

| Capital Expenditure | Extremely High (Spectrum, Infrastructure) | Established, Amortized Costs |

| Regulatory Environment | Complex and Lengthy Licensing | Experienced Navigators |

| Distribution Network | Difficult to Replicate (1,000+ Stores) | Extensive and Efficient |

| Economies of Scale | Cost Disadvantage (Lower Subscriber Base) | Significant Cost Efficiencies (32M+ Subscribers) |

| Experience Curve | Lack of Operational Expertise | Decades of Optimization |

Porter's Five Forces Analysis Data Sources

Our SK Telecom Porter's Five Forces analysis is built upon a foundation of diverse data sources, including SK Telecom's official annual reports, investor relations disclosures, and regulatory filings. We also incorporate insights from reputable industry research firms, market intelligence platforms, and economic databases to ensure a comprehensive understanding of the competitive landscape.