Saudi Investment Bank Boston Consulting Group Matrix

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Saudi Investment Bank Bundle

See the Bigger Picture

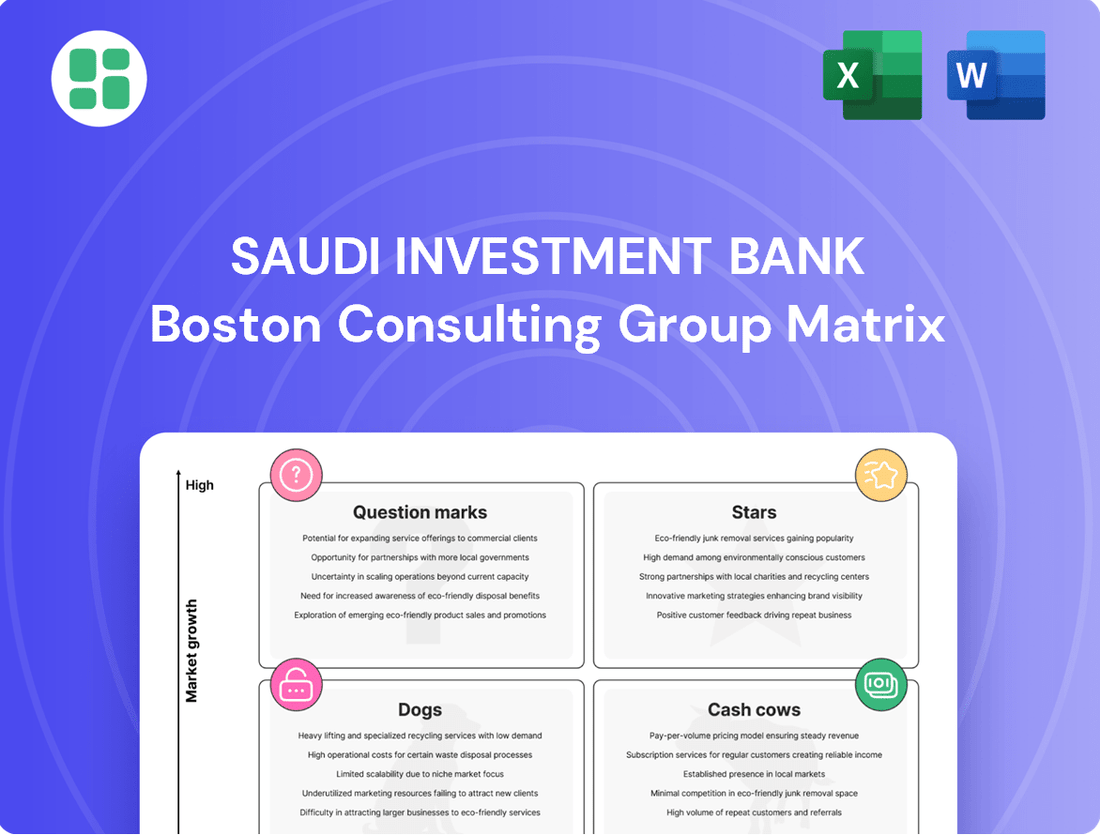

Curious about the Saudi Investment Bank's strategic positioning? Our BCG Matrix preview offers a glimpse into its product portfolio's potential, highlighting areas of strength and opportunity. Uncover which segments are driving growth and which may require a closer look.

To truly leverage this information, dive into the full BCG Matrix report. Gain a comprehensive understanding of each product's quadrant placement, access data-driven recommendations, and equip yourself with a clear roadmap for optimized investment and product development decisions.

Don't miss out on the complete strategic blueprint. Purchase the full BCG Matrix today to receive detailed quadrant analysis, actionable insights, and a powerful tool to navigate the competitive landscape with confidence.

Stars

SME Lending Portfolio

Saudi Investment Bank's (SAIB) focus on Small and Medium-sized Enterprise (SME) lending is strategically positioned within a robust growth environment. The market for MSME credit in Saudi Arabia demonstrated significant momentum, with facilities growing by 27.62 percent year on year in 2024, reaching SR351.7 billion. This upward trend continued into Q1 2025, with a further surge of 31 percent, bringing the total to SR383.2 billion.

SAIB is anticipated to experience substantial expansion in its SME lending portfolio, with projections indicating growth exceeding 15% for 2025. This forecast underscores SAIB's strong market standing within this dynamic and expanding sector.

Corporate Lending for Vision 2030 Projects

The corporate lending sector is a powerhouse, fueled by Saudi Arabia's ambitious Vision 2030 initiatives and its drive for economic diversification. This segment is outperforming personal lending, with corporate lending reaching SR1.75 trillion by May 2025, a substantial 21.73 percent increase from the previous year.

The Saudi Investment Bank (SAIB) plays a pivotal role in financing these large-scale projects. SAIB's own loan portfolio reflects this trend, demonstrating a significant 23% growth in fiscal year 2024 and a further 5% expansion in the first quarter of 2025. This robust performance suggests SAIB is capturing a considerable share of this rapidly expanding and strategically important market.

Advanced Digital Banking Services

Advanced Digital Banking Services represent a significant growth area for Saudi Investment Bank (SAIB). The Saudi banking sector's digital shift is accelerating, with online banking already holding a substantial 58.7% share of the retail market in 2024. This segment is expected to expand robustly, with a projected Compound Annual Growth Rate (CAGR) of 14.7% through 2030, highlighting the immense potential for SAIB's digital offerings.

SAIB's proactive approach to digital transformation, including the rollout of digital branches and ongoing investment in technology, positions it well to capitalize on this trend. This strategic focus demonstrates SAIB's commitment to enhancing its digital capabilities and expanding its footprint in this dynamic and rapidly growing market segment.

Specialized Investment Banking Services

Saudi Investment Bank (SAIB) actively provides specialized investment banking services, a crucial offering in Saudi Arabia's rapidly transforming financial landscape driven by Vision 2030. This sector is witnessing substantial capital inflows and increased corporate activity.

While precise market share figures for SAIB's investment banking division are not publicly delineated, the broader Saudi financial market experienced significant growth, with the number of listed companies reaching 353 by the close of 2024. This expansion highlights the increasing demand for sophisticated financial advisory and capital markets services.

SAIB's strategic emphasis on bolstering its treasury and investment segments indicates a proactive approach to capitalize on these growth opportunities. This focus positions the bank to play a significant role in facilitating capital raising and M&A activities.

- Capital Markets Advisory: Assisting companies in navigating IPOs and debt issuances.

- Mergers & Acquisitions (M&A): Facilitating strategic partnerships and corporate restructuring.

- Corporate Finance: Providing tailored financial solutions for business growth and development.

- Project Finance: Supporting large-scale infrastructure and industrial projects.

Sustainable Finance Initiatives

Saudi Investment Bank (SAIB) is making significant strides in sustainable finance, aligning with global trends and Saudi Arabia's Vision 2030. The bank is actively involved in green financing, channeling funds into renewable energy projects and embedding environmental, social, and governance (ESG) principles into its investment strategies.

This focus positions SAIB to capitalize on the burgeoning green economy. Saudi Arabia itself is making substantial investments in solar photovoltaic (PV) capacity, with plans to significantly expand its renewable energy portfolio. For instance, the Kingdom aims to reach 50% of its energy mix from renewables by 2030, a target that will require massive investment in solar and wind projects.

- Green Financing Growth: SAIB's commitment to green financing supports Saudi Arabia's ambitious renewable energy targets, estimated to attract billions in investment by 2030.

- ESG Integration: The bank's integration of ESG criteria into investment decisions reflects a growing demand from investors for sustainable and responsible financial products.

- Renewable Energy Focus: Funding for solar PV plants is a key area, tapping into a high-growth market driven by national environmental goals and global sustainability shifts.

- Market Leadership: SAIB's proactive investment strategy in sustainable initiatives aims to establish it as a leader in this rapidly evolving financial sector.

SAIB's Shining Stars: SME & Corporate Lending

Stars in the BCG Matrix represent business units with high market share in a high-growth industry. For Saudi Investment Bank (SAIB), this classification is most applicable to its Small and Medium-sized Enterprise (SME) lending and its Corporate Lending segments. These areas are experiencing robust growth, driven by national economic initiatives like Vision 2030, and SAIB is well-positioned to maintain and grow its market share within them.

The SME lending sector is a prime example, with facilities growing by 27.62 percent year on year in 2024 to SR351.7 billion, and further increasing by 31 percent in Q1 2025 to SR383.2 billion. SAIB's projected growth of over 15% in its SME portfolio for 2025 solidifies its Star status in this segment. Similarly, corporate lending, which reached SR1.75 trillion by May 2025 (a 21.73 percent increase), reflects a high-growth market where SAIB's 23% loan portfolio growth in 2024 and 5% in Q1 2025 indicates a strong, expanding presence.

The bank's strategic focus on these areas, coupled with the overall economic expansion in Saudi Arabia, positions both SME lending and Corporate Lending as Stars. They are generating significant revenue and are expected to continue to do so as the market matures and SAIB capitalizes on its strong market position.

| BCG Category | SAIB Business Segment | Market Growth | SAIB Market Share | Strategic Implication |

|---|---|---|---|---|

| Stars | SME Lending | High (27.62% YOY in 2024, 31% in Q1 2025) | Strong, growing | Invest for growth, maintain leadership |

| Stars | Corporate Lending | High (21.73% YOY in May 2025) | Strong, growing | Invest for growth, maintain leadership |

What is included in the product

Highlights which Saudi Investment Bank units to invest in, hold, or divest based on market share and growth.

The Saudi Investment Bank BCG Matrix offers a clear, one-page overview, simplifying complex business unit performance for strategic decision-making.

Cash Cows

Traditional Commercial Banking

Saudi Investment Bank's (SAIB) traditional commercial banking, encompassing services like current accounts and general corporate finance, is a strong Cash Cow. This segment operates within a mature market where SAIB enjoys a significant market share, ensuring reliable and steady revenue generation that bolsters the bank's profitability. The Saudi banking sector's robust performance, with consolidated net profits reaching SAR 79.6 billion in 2024, underscores the stability and earning power of core banking operations for established institutions like SAIB.

Transactional Accounts and Deposits

Transactional accounts, including checking and savings, are a cornerstone of retail banking. In 2024, these accounts held a significant 38.2% of the Saudi Arabia retail banking market share, acting as a consistent and cost-effective funding stream for financial institutions.

The Saudi Investment Bank (SAIB) demonstrates this strength, with its client deposits reaching SAR 101.66 billion in the first quarter of 2025. This figure represents a healthy 14.96% increase compared to the same period in the previous year.

This substantial and expanding deposit base offers SAIB a solid platform for its lending operations and other financial services. It reliably generates predictable cash flow, all while incurring minimal costs to maintain and grow, characteristic of a cash cow.

Credit Cards and Retail Loans

Credit cards and traditional retail loans represent a mature but vital segment for Saudi banks, including SAIB. The credit card market alone is projected to grow at a robust 12.6% annual rate until 2030, highlighting its ongoing importance. SAIB's diverse personal banking offerings in this area, such as loans and credit cards, cater to an established customer base.

These products are characterized by their ability to generate consistent interest income and fee revenue. This predictable cash flow makes them reliable contributors to the bank's overall financial health, fitting the profile of a cash cow in the BCG matrix.

Treasury Services

Saudi Investment Bank’s (SAIB) Treasury Services, covering liquidity management and foreign exchange, are vital for its corporate and institutional clients. This segment operates in a mature, stable market, meaning growth isn't explosive but income is consistent through fees and commissions. SAIB's Q1 2025 performance saw a 10% rise in net fee and other income, largely driven by increased foreign exchange activities, underscoring the reliable revenue stream from these treasury operations.

- Consistent Fee Income: Treasury services generate steady revenue through fees and commissions, reflecting their essential nature for clients.

- Foreign Exchange Contribution: A notable 10% increase in net fee and other income in Q1 2025 was significantly boosted by higher foreign exchange income.

- Mature Market Operations: These services function within a stable, established market, ensuring predictable performance rather than rapid expansion.

- Client Support Focus: SAIB's treasury operations are designed to support the liquidity and currency needs of its corporate and institutional customer base.

Established Asset Management Services

Saudi Investment Bank's established asset management services fit the Cash Cow quadrant of the BCG Matrix. This segment benefits from a high market share within a mature Saudi financial sector, where assets under management reached 26.3% of GDP in 2024, demonstrating a well-established and substantial market.

These services are characterized by recurring fee income derived from assets under management. This model provides a stable, predictable revenue stream with relatively low capital expenditure needs, making it a consistent profit generator for the bank.

- Mature Market Presence: SAIB leverages its established position in the Saudi financial market, which saw assets under management at 26.3% of GDP in 2024.

- Recurring Revenue Stream: Asset management generates consistent fee income based on assets under management, ensuring predictable earnings.

- Low Capital Expenditure: Compared to growth-oriented ventures, these services require less investment, contributing to higher profitability.

- Stable Profitability: The mature nature of the market and the fee-based model translate into a reliable and steady source of income for the bank.

SAIB's Banking Powerhouse: Cash Cows Driving Steady Growth!

Saudi Investment Bank's (SAIB) core commercial banking operations, including current accounts and corporate finance, are firmly established Cash Cows. These segments operate in a mature market where SAIB holds a significant share, ensuring consistent and reliable revenue generation. The overall Saudi banking sector's strong performance, with net profits reaching SAR 79.6 billion in 2024, highlights the stable earnings potential of such established banking services.

| SAIB Business Segment | BCG Category | Key Characteristics | Supporting Data (2024/2025) |

| Traditional Commercial Banking | Cash Cow | Mature market, high market share, stable revenue | Saudi banking net profits: SAR 79.6 billion (2024) |

| Transactional Accounts (Retail) | Cash Cow | Cost-effective funding, consistent deposit growth | Client deposits: SAR 101.66 billion (Q1 2025), up 14.96% YoY |

| Credit Cards & Retail Loans | Cash Cow | Steady interest income, established customer base | Credit card market growth: 12.6% annually (projected to 2030) |

| Treasury Services | Cash Cow | Recurring fee income, stable market, essential services | Net fee and other income: +10% (Q1 2025), driven by FX |

| Asset Management | Cash Cow | Fee-based recurring revenue, low capex, stable market | Assets under management: 26.3% of Saudi GDP (2024) |

Delivered as Shown

Saudi Investment Bank BCG Matrix

The Saudi Investment Bank BCG Matrix preview you are viewing is the complete, final document you will receive upon purchase. This means you'll get the fully formatted, analysis-ready report without any watermarks or demo content, ensuring immediate professional use.

Dogs

Underperforming Legacy IT Systems

Despite Saudi Investment Bank's (SAIB) significant strides in digital transformation, any persistent legacy IT systems that are expensive to maintain and hinder modern digital operations would fall into the 'Dog' category. These systems often drain valuable resources without offering a competitive edge or contributing to growth, directly opposing SAIB's strategic emphasis on IT modernization.

Underutilized Physical Branch Network

Saudi Investment Bank's extensive physical branch network, while historically a strength, is increasingly becoming a 'Dog' in its BCG Matrix. The rapid migration of customers to digital channels, with online and mobile banking now dominating customer interactions, leaves many branches underutilized.

The operational costs associated with maintaining this physical footprint, including rent, utilities, and staffing, are significant. These costs are not being offset by comparable revenue generation or customer engagement, particularly as digital payments represented 79% of retail transactions in 2024.

Niche or Outdated Product Offerings

Saudi Investment Bank (SAIB) may have certain niche or outdated product offerings that fall into the 'Dog' category of the BCG Matrix. These could be legacy financial products that have seen declining demand due to digital transformation or shifts in customer preferences. For instance, certain types of physical check processing services or less innovative loan products might be experiencing reduced uptake.

These 'Dog' products often tie up valuable bank resources and capital without generating significant returns or contributing to SAIB's strategic growth objectives. In 2023, the Saudi banking sector saw a continued push towards digital services, with a significant increase in mobile banking transactions, potentially leaving older, less digitized offerings further behind in market relevance.

Low-Margin, Highly Commoditized Basic Services

Certain fundamental banking services, characterized by their highly commoditized nature, present minimal profit margins and intense market rivalry. These offerings often lack distinct features, placing them in the "Dogs" category of the Saudi Investment Bank's BCG Matrix, especially if they don't function as a loss leader for more lucrative products. Such services might just cover their costs, offering little strategic advantage in a crowded financial landscape.

In 2024, the Saudi banking sector saw continued pressure on net interest margins for basic deposit and lending products. For instance, while overall Saudi bank profitability remained robust, the contribution from purely transactional services like basic current accounts or standard car loans often remained modest. These segments are highly sensitive to interest rate fluctuations and competitive pricing, making sustained high margins difficult.

- Low Profitability: Basic services often operate with net interest margins below 2% in competitive markets, barely covering operational costs.

- Intense Competition: Saudi banks, including the Saudi Investment Bank, face significant competition from both traditional players and emerging fintech solutions in these basic service areas.

- Limited Differentiation: Services like standard savings accounts or basic debit card offerings have minimal unique selling propositions, leading to price-based competition.

- Strategic Re-evaluation: Banks are increasingly looking to bundle these basic services with value-added digital platforms or more profitable investment products to mitigate their low strategic value.

Inefficient Internal Processes

Inefficient internal processes, characterized by manual workflows or excessive resource allocation without direct customer value, can significantly hinder a company's performance. For Saudi Investment Bank (SAIB), such inefficiencies might represent a 'Dog' in the BCG Matrix if they consume resources without generating commensurate returns or strategic advantage.

SAIB's stated strategy to enhance operational efficiency and bolster risk management indicates a proactive approach to addressing these potential 'Dogs'. By streamlining operations and reducing manual touchpoints, the bank aims to free up capital and human resources that can be redirected towards more profitable or strategically important areas.

- Focus on Automation: Implementing robotic process automation (RPA) for routine tasks like data entry and reconciliation can reduce errors and speed up processing times.

- Process Re-engineering: Analyzing and redesigning core banking processes to eliminate redundant steps and improve workflow. For instance, a 2024 report by McKinsey highlighted that banks focusing on digital transformation of back-office operations saw an average of 15-20% reduction in operational costs.

- Digital Transformation: Investing in modern IT infrastructure and digital platforms to support seamless operations and better data management.

SAIB's "Dogs": Legacy Systems, Branches, and Products

Legacy IT systems, underutilized physical branches, and outdated product offerings represent 'Dogs' for Saudi Investment Bank (SAIB). These areas consume resources without contributing significantly to growth or competitive advantage. For example, while digital payments dominated retail transactions at 79% in 2024, many physical branches remain costly to maintain.

| Category | Description | 2024/2023 Data Insight |

|---|---|---|

| Legacy IT Systems | Expensive to maintain, hinder digital operations. | Digital transformation efforts aim to phase out these systems. |

| Underutilized Branches | High operational costs, declining customer footfall. | Online and mobile banking now dominate, with digital transactions increasing year-on-year. |

| Outdated Products | Declining demand, low market relevance. | Saudi banking sector saw a significant increase in mobile banking transactions in 2023. |

| Commoditized Services | Low profit margins, intense competition. | Net interest margins for basic services remained modest, with pressure from fintech. |

Question Marks

New Fintech Venture Initiatives (e.g., SAIB Travel App)

Saudi Investment Bank's (SAIB) foray into new fintech ventures, exemplified by the SAIB Travel App launched in 2024 through its SAIB Venture Studio, positions these initiatives within the rapidly expanding Saudi fintech sector. This market is anticipated to grow at a compound annual growth rate of approximately 12.8% between 2025 and 2032, indicating substantial future potential.

Despite the promising market outlook, these new ventures are likely in their nascent stages, characterized by low current market share and profitability. Significant investment will be crucial for them to scale operations, gain traction, and transition into 'Stars' within the BCG matrix framework, moving from question marks to market leaders.

Expansion into Emerging Digital Payment Solutions

Saudi Arabia's digital payment landscape is booming, with digital payments accounting for a significant 79% of all retail transactions in 2024. This growth is further fueled by the Saudi Central Bank's (SAMA) continuous initiatives to enhance the digital payment ecosystem. For Saudi Investment Bank (SAIB), expanding into these emerging digital payment solutions represents a move into a high-growth market with substantial potential.

However, SAIB's current market share within specific, rapidly evolving digital payment niches might be relatively nascent. This positions these digital payment solutions as potential 'question marks' within the BCG Matrix, requiring substantial investment and strategic focus to capture a meaningful market share and capitalize on the sector's impressive growth trajectory.

Innovative AI/Data Analytics-Driven Lending Platforms

Saudi Investment Bank's (SAIB) foray into AI/data analytics-driven lending aligns with a significant trend in the MENA region. Banks are increasingly adopting these technologies to bridge the financing gap for Small and Medium Enterprises (SMEs). This strategic pivot is crucial, especially considering that in Q1 2025, a remarkable 97% of surveyed Saudi SMEs identified enhanced data and analytics tools as vital for their growth.

If SAIB has indeed launched or is developing advanced AI and data analytics platforms for lending, these initiatives represent a high-potential growth area. Such platforms are likely to offer more personalized and efficient loan products, catering to the specific needs of SMEs. However, these ventures typically start with a relatively low market share, necessitating significant investment to establish their value proposition and achieve scalability.

Specialized Micro-Lending Platforms

Specialized micro-lending platforms represent a significant growth opportunity within Saudi Arabia's financial sector. Micro-enterprises in Saudi Arabia experienced an impressive 82% surge in loan volumes during the first quarter of 2025, highlighting the dynamism of this market segment.

Given this substantial expansion, if Saudi Investment Bank (SAIB) has dedicated platforms or initiatives focused on micro-lending, and its current market share in this area is limited, these would be prime candidates for increased investment.

- High Growth Potential: The 82% year-on-year increase in micro-enterprise loan volumes in Q1 2025 signals a rapidly expanding market.

- Strategic Investment Focus: SAIB's micro-lending platforms, if currently holding a small market share, require focused investment to capture this growth.

- Market Penetration: Capitalizing on this segment can diversify SAIB's loan portfolio and reach underserved entrepreneurial segments.

Blockchain and Distributed Ledger Technology (DLT) Applications

The Saudi Investment Bank (SAIB) is actively exploring and investing in blockchain and Distributed Ledger Technology (DLT) to enhance its operational efficiency and explore new service avenues. This aligns with a broader trend in the financial sector where institutions are seeking to leverage these technologies for improved security, transparency, and speed in transactions.

While the potential for blockchain in financial services is significant, SAIB’s direct revenue-generating applications built on this technology are likely positioned in a nascent, high-growth market. This means that any current blockchain-based products or services would probably have a low market share, characteristic of a '?' (Question Mark) category in a BCG matrix, indicating high potential but requiring further investment and development to capture significant market share.

- SAIB's investment in innovative solutions like blockchain aims to streamline operations and explore new financial service models.

- The practical application and widespread adoption of blockchain in specific banking products are still in developmental stages for many institutions, including SAIB.

- Any direct revenue-generating blockchain products from SAIB would likely fall into a high-growth, low-market-share segment, classifying them as 'Question Marks' in the BCG matrix.

SAIB's Fintech Push: High Growth, Low Share

Saudi Investment Bank's (SAIB) ventures into areas like fintech, AI-driven lending, and blockchain are currently in high-growth, low-market-share phases, characteristic of Question Marks in the BCG matrix. These initiatives, such as the SAIB Travel App launched in 2024, are positioned to capitalize on Saudi Arabia's rapidly expanding digital economy, with digital payments already accounting for 79% of retail transactions in 2024. Significant investment is required for these emerging areas to mature into market leaders.

| BCG Category | SAIB Venture Example | Market Growth | Market Share | Strategic Implication |

|---|---|---|---|---|

| Question Mark | SAIB Travel App (Fintech) | High (Fintech sector CAGR ~12.8% 2025-2032) | Low | Requires significant investment to gain market share. |

| Question Mark | AI/Data Analytics Lending Platforms | High (SME financing gap in MENA) | Low | Needs development to capture the 97% of Saudi SMEs seeking better analytics tools (Q1 2025). |

| Question Mark | Blockchain/DLT Applications | High (Emerging technology adoption) | Low | Investment needed to translate potential into revenue-generating services. |

BCG Matrix Data Sources

Our Saudi Investment Bank BCG Matrix is built on verified market intelligence, combining financial data, industry research, official reports, and expert commentary to ensure reliable, high-impact insights.