RBL Bank Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

RBL Bank Bundle

A Must-Have Tool for Decision-Makers

RBL Bank navigates a complex competitive landscape, where the bargaining power of buyers and the threat of substitutes significantly shape its strategic options. Understanding these forces is crucial for any stakeholder looking to grasp the bank's market position.

The complete report reveals the real forces shaping RBL Bank’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

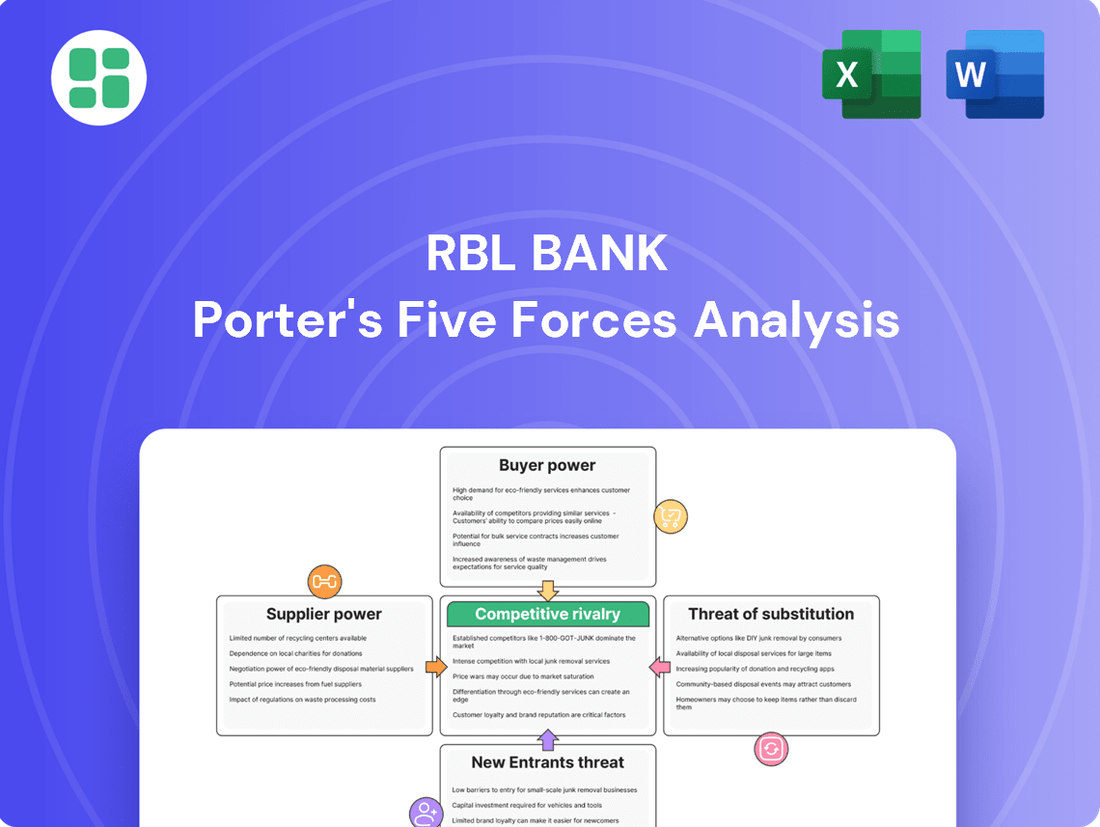

Suppliers Bargaining Power

Technology Vendors

RBL Bank depends on technology vendors for critical functions like core banking, digital services, and cybersecurity. The bargaining power of these suppliers is often moderate to high, particularly for specialized or proprietary software and hardware. This is because switching to a different vendor can involve substantial costs and require specialized expertise for integration and ongoing support.

Human Capital

Skilled human capital, especially in digital banking, data analytics, and risk management, is a key supplier for RBL Bank. The ability of these specialized employees to command higher salaries and better benefits due to demand significantly impacts the bank's operational costs and strategic execution.

In the competitive Indian banking sector, talent acquisition and retention are paramount. For instance, as of early 2024, the demand for data scientists and cybersecurity experts in finance remained exceptionally high, with salary premiums often exceeding 20% for specialized roles compared to generalist positions.

RBL Bank must therefore invest heavily in competitive compensation packages, continuous learning, and career advancement programs to secure and retain this vital human capital. Failure to do so could lead to increased recruitment costs and a potential dip in service quality and innovation.

Funding Sources (Depositors)

Depositors are RBL Bank's lifeblood, providing the essential funds for its operations. While most retail depositors have little sway, larger institutional investors or wealthy individuals can negotiate for better interest rates, particularly when the market for funds tightens. For instance, as of March 31, 2024, RBL Bank's total deposits stood at ₹77,778 crore, with its retail deposit base showing steady growth, aiming to reduce reliance on more volatile bulk deposits.

Interbank and Capital Markets

RBL Bank relies on interbank and capital markets for funding, meaning these markets are significant suppliers of capital. The cost and availability of these funds are directly impacted by market liquidity, Reserve Bank of India (RBI) interest rate policies, and RBL Bank's own creditworthiness. For instance, in early 2024, the RBI maintained its repo rate, influencing borrowing costs across the financial system.

The bargaining power of these financial market suppliers can shift considerably. Factors like global economic sentiment and evolving regulatory frameworks can either increase or decrease the leverage these suppliers hold over banks like RBL. A tightening of liquidity, for example, would empower these suppliers, potentially raising funding costs for the bank.

- Interbank and Capital Market Funding: RBL Bank sources capital from interbank lending and by issuing debt or equity in capital markets.

- Influencing Factors: Fund availability and cost are shaped by market liquidity, RBI monetary policy, and RBL Bank's credit ratings.

- Supplier Power Dynamics: The bargaining power of these financial suppliers fluctuates with broader economic conditions and regulatory changes.

- Market Conditions Impact: In periods of reduced liquidity or increased risk aversion, these suppliers gain more leverage, potentially increasing RBL Bank's cost of capital.

Regulatory Bodies

Regulatory bodies, such as the Reserve Bank of India (RBI), wield substantial influence over RBL Bank, akin to powerful suppliers. These institutions dictate crucial operational parameters, including capital adequacy ratios and compliance mandates, directly affecting the bank's cost structure and strategic flexibility. For instance, the RBI's directives on asset quality and provisioning can significantly impact profitability and the need for capital infusions.

These regulatory impositions translate into tangible costs for RBL Bank. Compliance with evolving Know Your Customer (KYC) norms, data localization requirements, and cybersecurity standards necessitates ongoing investment in technology and personnel. In 2024, the banking sector, including RBL Bank, continued to navigate a landscape shaped by these regulatory demands, impacting operational expenses and strategic planning.

- RBI's Capital Adequacy Framework: RBL Bank must adhere to Basel III norms, requiring specific capital ratios to be maintained, influencing lending capacity and risk appetite.

- Compliance Costs: Investments in technology for fraud detection, AML (Anti-Money Laundering), and cybersecurity are ongoing, driven by regulatory expectations.

- Operational Standards: RBI's guidelines on digital lending, customer grievance redressal, and data privacy directly shape RBL Bank's service delivery and risk management practices.

Unpacking RBL Bank's Supplier Influence: Tech, Talent, and Funding

The bargaining power of suppliers for RBL Bank is multifaceted, encompassing technology providers, skilled labor, depositors, capital markets, and regulatory bodies.

Technology vendors offering specialized core banking or cybersecurity solutions can exert significant influence due to high switching costs and the need for integrated expertise.

Skilled talent, particularly in areas like data analytics and digital banking, commands premium salaries, impacting RBL Bank's operational expenses and innovation capacity, with demand for data scientists remaining exceptionally high in early 2024.

While retail depositors have limited individual power, institutional investors can negotiate better rates, especially during tight market liquidity, as RBL Bank aims to balance its ₹77,778 crore deposit base (as of March 31, 2024) between retail and bulk funding.

| Supplier Type | Influence Factors | Impact on RBL Bank |

|---|---|---|

| Technology Vendors | Switching costs, specialized expertise | Moderate to high power, affects operational efficiency |

| Skilled Human Capital | High demand for specialized skills (e.g., data science) | Increased salary costs, talent retention challenges |

| Depositors (Institutional) | Market liquidity, bank's creditworthiness | Negotiation of interest rates, funding cost |

| Capital Markets | RBI policy, global economic sentiment | Cost and availability of funding |

| Regulatory Bodies (e.g., RBI) | Capital adequacy norms, compliance mandates | Operational costs, strategic flexibility |

What is included in the product

This Porter's Five Forces analysis for RBL Bank examines the intensity of rivalry, the bargaining power of buyers and suppliers, the threat of new entrants, and the threat of substitute products within the Indian banking sector.

Instantly identify and address competitive threats with a clear, actionable breakdown of RBL Bank's market pressures.

Customers Bargaining Power

Retail Customers

Retail customers, though individually possessing limited bargaining power due to the standardized nature of banking products and services, wield considerable collective influence. This is particularly true as RBL Bank actively competes for their deposits and loan business, employing strategies like product innovation, digital accessibility, and attractive interest rates to capture market share.

The increasing prevalence of digital banking and the ease with which customers can switch between financial institutions, including newer fintech players, further amplify their overall leverage. For instance, by mid-2024, reports indicated that a significant percentage of retail banking transactions were conducted digitally, highlighting the customer's reliance on and preference for convenient, accessible platforms.

Corporate and Institutional Clients

Large corporate and institutional clients wield significant bargaining power with RBL Bank. Their substantial transaction volumes and sophisticated financial needs mean they can demand highly tailored solutions, competitive pricing on loans and deposits, and specialized services like treasury management or trade finance. For instance, a large corporation seeking a multi-million dollar loan facility can negotiate terms more effectively than a small business. RBL Bank's strategy must focus on providing these customized offerings and cultivating robust, long-term relationships to secure and retain such high-value clients.

Digital Natives and Fintech Users

Digital natives and fintech users represent a growing segment of RBL Bank's customer base, wielding significant bargaining power. These customers, accustomed to seamless digital interactions and instant gratification, demand competitive pricing and innovative financial solutions. For instance, by mid-2024, over 60% of RBL Bank's new customer acquisitions were through digital channels, highlighting the importance of meeting these expectations.

Price Sensitivity

Customers in the banking sector often exhibit significant price sensitivity, particularly for straightforward products such as savings accounts or common loan types. This means RBL Bank must carefully manage its pricing to remain competitive while still achieving its profit objectives. The sheer volume of choices available to consumers intensifies this pressure.

For instance, in 2024, the average interest rate offered on savings accounts across major Indian banks hovered around 3.5% to 4.5%, with some niche players offering slightly higher rates. This narrow band of differentiation makes it difficult for banks like RBL to command premium pricing based solely on interest rates for basic deposit products.

- Price Sensitivity Impact: Customers readily switch banks for even minor interest rate advantages on deposits or lower fees on transactions.

- Competitive Landscape: The presence of numerous public sector, private sector, and small finance banks means RBL Bank faces constant pressure to align its pricing.

- Product Commoditization: Basic banking services are increasingly seen as commodities, reducing RBL Bank's ability to differentiate on price alone.

- Profitability Challenge: Balancing the need for competitive pricing with maintaining healthy profit margins is a continuous strategic hurdle for RBL Bank.

Switching Costs

Switching costs for RBL Bank customers have been notably reduced, particularly with the proliferation of digital banking platforms. While setting up new direct debits or updating Know Your Customer (KYC) documents can involve some effort, these are generally manageable. For instance, in 2024, the ease of account aggregation services allows customers to view multiple bank accounts in one place, simplifying the comparison of offerings.

The widespread adoption of interoperable payment systems, such as India's Unified Payments Interface (UPI), has further diminished switching friction. UPI transactions, which saw over 130 billion transactions in FY24, allow for seamless fund transfers between different banks, making it easier for customers to move their banking relationships without disrupting essential payment flows. This technological advancement directly empowers customers by lowering the practical barriers to changing their bank.

- Reduced Friction: Digital banking and UPI have made it simpler for customers to switch financial institutions.

- Interoperability Boost: UPI's widespread use in 2024 facilitates easy fund transfers across banks, lowering switching hurdles.

- Customer Empowerment: Lower switching costs give customers more leverage to seek better banking products and services.

Empowered Customers: The New Banking Force

The bargaining power of customers for RBL Bank is significant, driven by increasing price sensitivity and the commoditization of basic banking services. Customers can easily switch for better rates or lower fees, especially with digital platforms and interoperable payment systems like UPI lowering switching costs. This forces RBL Bank to maintain competitive pricing and focus on value-added services to retain its customer base.

| Factor | Impact on RBL Bank | 2024 Data/Observation |

| Price Sensitivity | High pressure on pricing for deposits and loans. | Average savings account rates around 3.5%-4.5% across major Indian banks in 2024. |

| Switching Costs | Low, particularly with digital banking and UPI. | Over 130 billion UPI transactions in FY24, indicating ease of fund transfer between banks. |

| Product Commoditization | Reduced differentiation for basic services. | Customers often compare banks based on minimal interest rate differences or transaction fees. |

| Digital Adoption | Empowers customers with information and ease of comparison. | Over 60% of RBL Bank's new customer acquisitions in 2024 were through digital channels. |

Same Document Delivered

RBL Bank Porter's Five Forces Analysis

This preview showcases the comprehensive RBL Bank Porter's Five Forces Analysis, detailing the competitive landscape and strategic positioning within the banking sector. The document you see here is the exact, fully formatted analysis you will receive immediately after purchase, providing actionable insights without any placeholders or alterations. You're looking at the actual document, meaning once you complete your purchase, you’ll get instant access to this precise file, ready for immediate use and strategic planning.

Rivalry Among Competitors

Fragmented Banking Sector

The Indian banking sector's fragmentation is a key driver of intense rivalry for RBL Bank. With a mix of large public sector banks, established private players, small finance banks, and emerging fintech companies, competition for customers and deposits is fierce across all market segments. This diverse landscape means RBL Bank must continuously innovate and offer competitive pricing and services to maintain its market position.

Aggressive Product Innovation

RBL Bank faces intense competition as rivals aggressively innovate, particularly in digital offerings. Competitors are rolling out features like instant loan approvals, tailored wealth management services, and frictionless payment systems, forcing RBL Bank to keep pace. For instance, in 2023, the Indian digital lending market saw significant growth, with fintechs and established banks alike launching new credit products, often leveraging AI for faster processing.

To stay relevant, RBL Bank must prioritize its own continuous innovation. This means not only matching but exceeding competitor offerings in areas like personalized customer experiences and advanced digital banking solutions. The bank’s ability to adapt its product suite to evolving customer needs, especially in the rapidly expanding digital segment, is crucial for retaining market share and attracting new clientele.

Digitalization and Fintech Disruption

The banking sector, including RBL Bank, faces intense rivalry from nimble fintech firms. These disruptors are rapidly gaining market share in key areas like digital payments and lending. For instance, India's digital payments market is projected to reach $1 trillion by 2026, a significant portion of which is handled by non-bank entities.

Fintechs often offer more user-friendly interfaces and specialized services, forcing established players like RBL Bank to innovate quickly. This competitive pressure necessitates significant investment in digital infrastructure and a re-evaluation of traditional business models to remain relevant and competitive.

Market Share Dynamics

Competitive rivalry in the Indian banking sector is intense, with large private banks like HDFC Bank, ICICI Bank, and Axis Bank holding substantial market shares. This dominance creates a challenging environment for smaller institutions such as RBL Bank to achieve rapid expansion. For instance, as of the fiscal year ending March 2024, these larger banks consistently reported robust asset growth and market penetration, making it difficult for RBL Bank to significantly alter the existing landscape.

RBL Bank is strategically focusing on key growth areas to navigate this competitive intensity. Its efforts are concentrated on expanding its retail and commercial banking segments. A significant part of this strategy involves increasing its share of granular deposits, which are typically smaller, retail customer deposits, providing a more stable funding base.

- Dominant Players: HDFC Bank, ICICI Bank, and Axis Bank command a significant portion of the market.

- RBL Bank's Strategy: Focus on growing retail and commercial banking.

- Deposit Growth: Aiming to increase the share of granular deposits for a stable funding base.

- Competitive Landscape: Intense rivalry makes market share gains challenging for smaller banks.

Regulatory Environment

The Reserve Bank of India (RBI) actively shapes the banking landscape, with its directives impacting competitive pressures. For example, the RBI's push for financial inclusion and the growth of digital payment systems, such as UPI, has opened doors for new fintech players and innovative banking models. This regulatory environment encourages broader competition, forcing established banks like RBL Bank to adapt their strategies to remain competitive in a rapidly evolving market.

These regulations, while designed for stability, can also intensify rivalry. By promoting digital channels and customer-centric approaches, the RBI indirectly fuels competition from entities that can leverage technology more nimbly. In 2024, the continued emphasis on digital transformation means that banks failing to innovate risk losing market share to more agile competitors.

- RBI's Financial Inclusion Mandate: Encourages new entrants and digital-first models, increasing competitive intensity.

- Digital Payment Growth: Initiatives like UPI adoption in 2023-2024 have lowered barriers to entry for fintech firms.

- Regulatory Adaptation: Banks like RBL must invest in technology and customer experience to counter new competitive threats.

RBL Bank's Strategic Play in India's Competitive Banking Arena

RBL Bank operates in a highly competitive Indian banking sector, characterized by the dominance of large private banks like HDFC Bank, ICICI Bank, and Axis Bank. These established players, as of March 2024, consistently demonstrate strong market penetration and asset growth, making it challenging for RBL Bank to significantly alter the competitive landscape.

The rise of agile fintech companies further intensifies this rivalry, particularly in digital payments and lending. India's digital payments market, projected to reach $1 trillion by 2026, sees significant contributions from non-bank entities, forcing traditional banks like RBL to innovate rapidly to retain market share.

RBL Bank's strategy to counter this involves focusing on retail and commercial banking growth, with a specific emphasis on increasing its share of granular deposits to build a more stable funding base. This strategic focus is crucial for navigating the intense competition and adapting to evolving customer demands, especially in the digital banking space.

| Competitor | Market Share (Approx. FY24) | Key Strengths | RBL Bank Focus |

|---|---|---|---|

| HDFC Bank | 15-17% | Digital innovation, strong retail presence | Retail and commercial banking growth |

| ICICI Bank | 12-14% | Digital banking, diversified services | Increasing granular deposits |

| Axis Bank | 10-12% | Corporate banking, digital transformation | Stable funding base |

| Fintech Companies | Growing rapidly in specific niches (e.g., payments, lending) | Agility, user-friendly interfaces, specialized services | Matching digital offerings, personalized experiences |

SSubstitutes Threaten

Digital Payment Platforms

The rise of digital payment platforms, especially India's Unified Payments Interface (UPI), presents a strong threat of substitutes for RBL Bank. UPI's seamless, real-time transactions bypass traditional banking infrastructure, offering customers a more convenient alternative for everyday payments.

As of early 2024, UPI has processed over 120 billion transactions annually, demonstrating its massive adoption and displacing a significant volume of card and net banking transactions. This shift means customers increasingly use these platforms for services traditionally offered by banks, reducing direct engagement and potential for cross-selling.

Non-Banking Financial Companies (NBFCs)

Non-Banking Financial Companies (NBFCs) present a significant threat of substitutes for RBL Bank. These entities, like Bajaj Finance or HDFC Ltd., often provide specialized lending products such as personal loans, vehicle financing, and microfinance. They can be particularly attractive to customer segments that traditional banks might overlook or to those prioritizing speed in loan disbursement. For instance, in 2023, the NBFC sector in India saw its assets under management grow by approximately 10-12%, indicating their expanding reach and competitive capability against banks like RBL.

Fintech Lending and P2P Platforms

Fintech lending and peer-to-peer (P2P) platforms present a significant threat of substitutes for RBL Bank. These digital channels offer alternative borrowing and investment avenues, often with more streamlined processes and potentially better rates than traditional banks.

For instance, by mid-2024, the Indian P2P lending market was projected to reach a substantial size, indicating a growing preference for these alternative financing methods. Platforms like Faircent and LenDenClub have facilitated billions in loans, directly competing with RBL Bank's core lending business.

The agility of fintech lenders in adapting to market demands and their ability to leverage data analytics for faster credit assessments make them attractive substitutes, potentially siphoning off both borrowers and investors seeking quicker, more convenient financial solutions.

Wealth Management and Investment Firms

For RBL Bank's wealth management and investment services, customers have a wide array of alternatives beyond traditional bank offerings. These substitutes include independent financial advisors who can offer tailored advice, dedicated mutual fund houses providing specialized investment vehicles, and the option for direct participation in equity and debt markets. This broadens the competitive landscape significantly for RBL Bank's wealth management segment.

The availability of these substitutes means clients can often find more specialized services or potentially lower fees compared to what a large bank might offer. For instance, in 2024, the Indian mutual fund industry saw substantial inflows, indicating a strong preference for these alternative investment avenues among retail investors.

- Independent Financial Advisors: Offer personalized, fee-based advice, often unbundled from product sales.

- Mutual Fund Houses: Provide a diverse range of investment products across asset classes, managed by specialized fund managers.

- Direct Market Participation: Investors can directly buy stocks and bonds, bypassing intermediaries for greater control and potentially lower costs.

- Fintech Platforms: Robo-advisors and online investment platforms offer accessible and often lower-cost wealth management solutions.

Digital Wallets and Neo-banks

Digital wallets and neo-banks present a significant threat of substitution for RBL Bank. These fintech alternatives offer streamlined payment solutions and basic banking functionalities, often with a more intuitive digital interface. For instance, by July 2024, the digital payments market in India, a key area for RBL Bank, was projected to see continued robust growth, with mobile wallets accounting for a substantial portion of transactions.

These platforms can siphon off customer engagement, particularly for transactional banking needs, which are foundational to customer relationships. While neo-banks typically partner with established institutions like RBL Bank for regulatory compliance, their enhanced user experience can draw customers away from traditional banking apps. This shift in customer preference can impact RBL Bank's ability to cross-sell higher-margin products and services.

- Growing Digital Payments Adoption: India's digital payments market is expanding rapidly, with mobile wallets expected to handle a significant share of transactions by mid-2024, directly competing with RBL Bank's payment services.

- Enhanced User Experience: Fintechs like digital wallets and neo-banks often provide a superior, user-friendly interface, attracting customers who prioritize convenience and ease of use over traditional banking channels.

- Customer Engagement Diversion: These substitutes can divert customer interaction away from RBL Bank's core platforms, potentially reducing opportunities for deeper customer relationships and cross-selling of other financial products.

Digital Alternatives Disrupt Traditional Banking Models

The threat of substitutes for RBL Bank is substantial, driven by the rapid evolution of digital financial services and alternative investment avenues. These substitutes directly challenge the bank's traditional revenue streams and customer engagement models.

Fintech platforms, including UPI, digital wallets, neo-banks, and P2P lending sites, offer seamless, often faster, and user-friendlier alternatives for payments, lending, and even basic banking. By mid-2024, UPI alone was processing over 120 billion transactions annually, a clear indicator of its dominance in the payments space. Similarly, the NBFC sector's assets under management grew by 10-12% in 2023, highlighting their increasing competitiveness in lending.

Furthermore, for wealth management, independent financial advisors, mutual fund houses, and direct market participation provide specialized services and potentially lower costs, attracting a significant portion of retail investors. The robust inflows into the Indian mutual fund industry in 2024 underscore this trend.

| Substitute Category | Key Offerings | Impact on RBL Bank | Market Trend (2023-2024) |

| Digital Payment Platforms (e.g., UPI) | Real-time, convenient payments | Reduces reliance on bank-led payment systems, limits cross-selling | UPI transactions exceeded 120 billion annually (early 2024) |

| NBFCs | Specialized lending (personal, vehicle, microfinance) | Competes for loan market share, especially with speed-focused customers | NBFC AUM grew 10-12% in 2023 |

| Fintech Lending & P2P Platforms | Streamlined borrowing/investment | Siphons off borrowers and investors seeking efficiency | Projected substantial growth in Indian P2P lending market (mid-2024) |

| Wealth Management Alternatives | Independent advice, mutual funds, direct market access | Diversifies investment choices away from bank offerings | Strong inflows into Indian mutual funds (2024) |

Entrants Threaten

High Regulatory Barriers

The Indian banking sector is heavily regulated by the Reserve Bank of India (RBI), demanding substantial capital reserves, rigorous licensing procedures, and strict adherence to evolving compliance standards. These stringent requirements act as a significant deterrent for potential new entrants seeking to establish full-fledged banking operations.

For instance, the RBI's guidelines for new bank licenses, as seen in past application rounds, necessitate a minimum net worth of INR 500 crore, with plans to increase this significantly to INR 1,000 crore for universal banks and INR 300 crore for small finance banks by 2024. This financial hurdle, coupled with the extensive operational and governance compliances, makes it exceptionally difficult for new players to enter and compete effectively.

Capital Requirements

Establishing a new bank demands immense capital, covering everything from physical branches and advanced technology to meeting stringent regulatory capital adequacy ratios. For instance, as of early 2024, Indian banks are generally required to maintain a Capital Adequacy Ratio (CAR) well above the Basel III minimums, often in the double digits, to ensure financial stability.

This significant financial hurdle makes it incredibly challenging for aspiring new entrants to enter the banking sector and compete effectively with established institutions like RBL Bank, effectively deterring potential new competitors.

Brand Reputation and Trust

Banking is fundamentally an industry built on trust, and established institutions like RBL Bank have cultivated this through years of consistent service and customer interaction. Newcomers must overcome the significant hurdle of building a comparable reputation, a process that takes considerable time and investment, especially when dealing with people's finances.

Technological Advancements Lowering Niche Entry Barriers

Technological advancements are significantly lowering the barriers to entry for specialized financial services, impacting traditional banks like RBL Bank. While establishing a full-fledged bank remains capital-intensive and highly regulated, nimble fintech startups are increasingly able to enter specific market niches. These niches can include areas such as digital payments, peer-to-peer lending, or specialized wealth management platforms.

These agile fintech players often leverage innovative technologies and lean operating models to offer targeted services, sometimes at a lower cost or with greater convenience than incumbents. For instance, the rise of digital payment gateways and buy-now-pay-later services has seen significant growth, with the Indian digital payments market projected to reach $1 trillion by 2026, according to various industry reports. This allows these new entrants to carve out profitable segments of the banking value chain.

- Fintechs targeting specific niches: Companies focusing on digital wallets, cross-border remittances, or micro-financing can bypass the extensive licensing requirements of full-service banking.

- Lower capital requirements for specialized services: Unlike establishing a full bank, a fintech can launch a payment app or a lending platform with comparatively less initial capital.

- Increased competitive pressure: By capturing lucrative parts of the value chain, these specialized entrants can indirectly increase competitive pressure on RBL Bank, forcing it to innovate and adapt its offerings.

- Data analytics and AI: Advanced analytics and AI enable new entrants to offer personalized financial products and manage risk more effectively in their chosen niches.

Established Distribution Networks

Established banks, including RBL Bank, benefit from deeply entrenched distribution networks. As of 2024, RBL Bank operates hundreds of branches and a robust digital banking platform, offering extensive customer reach and service points throughout India.

Newcomers face a substantial hurdle in replicating this established infrastructure. The capital expenditure required to build a comparable network of physical branches and sophisticated digital channels presents a significant barrier to entry for potential competitors in the Indian banking sector.

- Extensive Branch Network: RBL Bank's physical presence across numerous Indian cities and towns provides immediate customer access and trust.

- Digital Channel Dominance: Advanced mobile banking apps and online platforms offer seamless customer interaction, a crucial element for attracting and retaining customers.

- High Replicability Cost: The financial outlay and time needed for new entrants to establish a comparable distribution and service ecosystem are considerable, deterring many.

Fintechs target niches; full banking entry faces high capital barriers

While establishing a full-fledged bank is highly regulated and capital-intensive, the threat of new entrants is evolving due to fintech innovations. These agile players can bypass extensive licensing by targeting specific financial niches, such as digital payments or peer-to-peer lending, leveraging technology and lean models. The Indian digital payments market, projected to reach $1 trillion by 2026, highlights the lucrative potential of these specialized segments, indirectly pressuring established banks like RBL Bank to adapt.

The significant capital requirements and stringent licensing by the RBI, including minimum net worth thresholds of INR 1,000 crore for universal banks by 2024, create a formidable barrier for new full-service banks. Coupled with the need to build trust and replicate extensive distribution networks, the threat from entirely new, large-scale banking competitors remains relatively low for incumbents like RBL Bank.

Porter's Five Forces Analysis Data Sources

Our RBL Bank Porter's Five Forces analysis is built upon a foundation of diverse and credible data sources, including RBL Bank's annual reports, investor presentations, and filings with the Reserve Bank of India (RBI). We also incorporate insights from reputable financial news outlets, industry analysis reports from firms like CRISIL and ICRA, and macroeconomic data from sources such as the World Bank and IMF to provide a comprehensive view of the competitive landscape.