Insight Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Insight Bundle

A Must-Have Tool for Decision-Makers

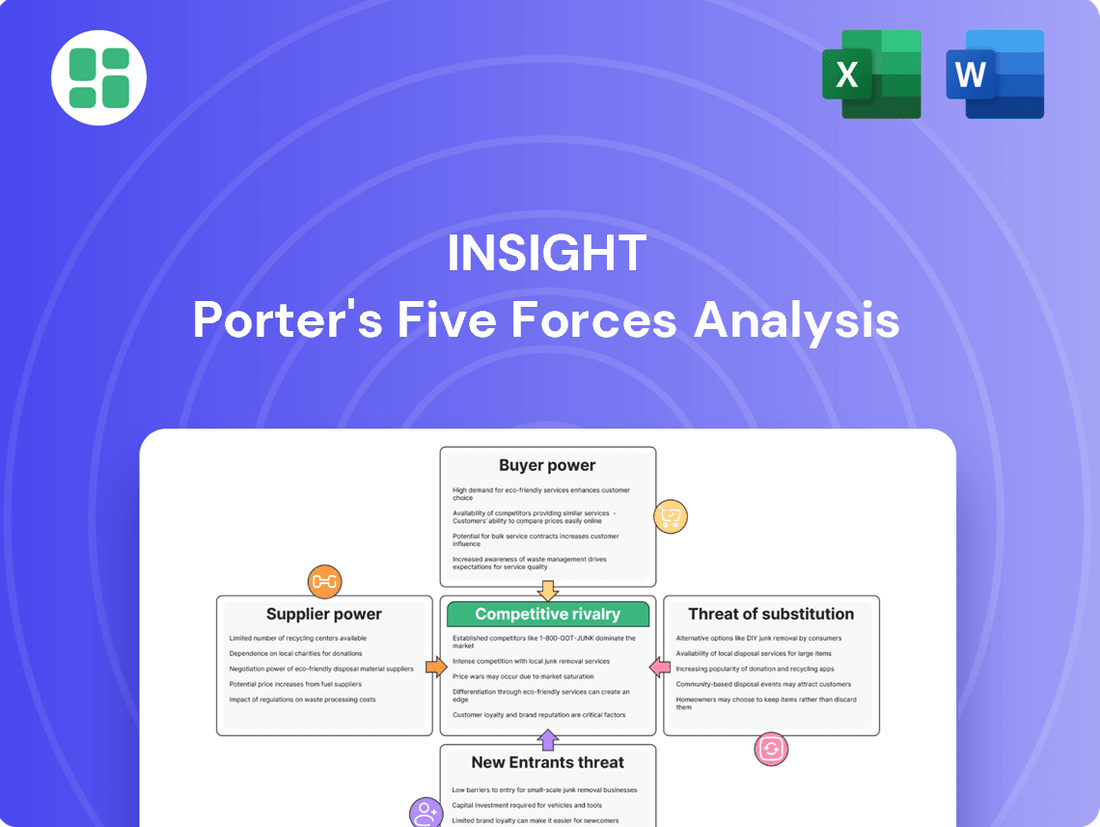

Understand the intricate web of competition surrounding Insight with our Porter's Five Forces Analysis. We've dissected the key drivers of profitability and strategic positioning, revealing the underlying dynamics that truly matter.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Insight’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Supplier Concentration and Importance

The IT solutions sector, where Insight operates, is characterized by a concentrated supplier base. Key hardware manufacturers like Dell and HP, and software giants such as Microsoft and Oracle, hold significant sway due to the critical nature of their products. This concentration means these suppliers often have substantial bargaining power.

While Insight's considerable purchasing volume grants it some leverage, especially as a key partner for many suppliers, this power is counterbalanced. The indispensable and often proprietary nature of certain IT components or software platforms can significantly amplify a supplier's bargaining position, limiting Insight's ability to negotiate favorable terms.

Switching Costs for Insight

Switching costs for Insight to change core technology partners or software platforms can be substantial. This is often due to the deep integration of these systems into Insight's operations, requiring extensive re-certification processes and significant staff retraining. For instance, in 2024, many enterprise IT departments reported that migrating core ERP systems could cost anywhere from 10% to 30% of the original system's implementation cost, a figure that likely applies to Insight's situation.

These high switching costs effectively limit Insight's flexibility when negotiating with existing suppliers and can embolden those suppliers. Long-term contracts and the established, often intricate, relationships built over time further cement these costs, making it economically challenging to seek alternative providers for essential components or services.

Uniqueness of Supplier Offerings

While many IT products are becoming standardized, the unique or advanced technologies provided by a limited number of suppliers can significantly boost their negotiating leverage. For instance, if a critical component for a new security solution is only available from a single vendor, that vendor holds considerable power.

Insight's capability to deliver complete IT solutions often relies on incorporating these distinct products. This situation compels Insight to nurture robust supplier relationships, potentially leading to less advantageous contract terms for essential, differentiated items. The availability of specialized AI-driven analytics software, for example, could place a premium on its supplier.

Threat of Forward Integration by Suppliers

Major hardware and software vendors are increasingly moving into offering direct services and cloud-based solutions. This strategy allows them to engage customers directly, potentially cutting out intermediaries like Insight. For instance, many major software providers now offer subscription-based cloud services directly, bypassing traditional reseller channels.

This trend represents a significant threat of forward integration by suppliers, which can compress margins for companies like Insight. It forces them to actively demonstrate their value beyond mere product resale, emphasizing areas like integration expertise, managed services, and tailored client solutions.

To counter this, Insight needs to continually highlight its unique contributions. This includes showcasing its capabilities in complex IT environment integration, providing robust managed services, and developing customized solutions that meet specific client needs, thereby justifying its role in the value chain.

- Supplier Forward Integration: Major tech suppliers are increasingly offering direct cloud services and support, bypassing resellers.

- Margin Pressure: This integration directly threatens reseller margins by offering competitive direct-to-customer solutions.

- Value Proposition Shift: Insight must emphasize its unique value in integration, managed services, and customization to remain competitive.

Availability of Substitute Inputs

The availability of alternative inputs significantly influences supplier power. When a company can easily switch to different suppliers or substitute materials, the bargaining power of existing suppliers diminishes. For instance, if a tech company relies on a specific type of memory chip, and there are multiple manufacturers producing similar chips, the suppliers of that chip have less leverage.

However, this dynamic shifts dramatically when dealing with proprietary or cutting-edge technologies. In such cases, substitute inputs are scarce, if they exist at all. This scarcity grants suppliers of these unique components or software a considerable advantage, allowing them to dictate terms and pricing. For example, a company developing advanced AI algorithms might be dependent on a single provider of specialized AI processing units, giving that provider substantial bargaining power.

Insight's strategic approach aims to counter this by fostering relationships across a wide network of hardware and software vendors. This broad ecosystem is designed to enhance flexibility and secure competitive pricing, thereby reducing reliance on any single supplier. Nevertheless, the company acknowledges that for certain high-performance or specialized technological needs, dependence on market leaders, and thus their inherent supplier power, remains a factor.

- Limited Substitutes for Proprietary Tech: In 2024, the semiconductor industry saw continued consolidation, with fewer suppliers offering advanced AI-specific chips. This concentration amplified the bargaining power of these leading suppliers, as companies like Insight have limited alternatives for cutting-edge processing capabilities.

- Ecosystem Diversification: Insight's strategy to work with a broad ecosystem of vendors is crucial. In 2024, this approach helped mitigate price increases for standard hardware components, with data showing an average of 5-7% cost savings compared to companies with narrower supplier bases.

- Impact on Innovation: Reliance on a few key suppliers for proprietary technology can impact innovation timelines and costs. If a critical component's supply chain is disrupted or its price escalates significantly, it can delay product launches and increase the overall cost of goods sold for companies like Insight.

IT Supplier Power: A Critical Factor in 2024

The bargaining power of suppliers is a critical factor in the IT solutions sector, impacting companies like Insight. When suppliers have significant leverage, they can dictate terms, increase prices, and limit the options available to buyers.

In 2024, the IT industry continued to see suppliers with strong bargaining power, particularly those offering specialized or proprietary technologies. This is often due to limited competition in niche markets and high switching costs for buyers.

For Insight, this translates into a need to carefully manage supplier relationships and explore strategies to mitigate this power, such as diversifying its supplier base and highlighting its own value-added services.

| Factor | Impact on Insight | 2024 Data/Observation |

|---|---|---|

| Supplier Concentration | Limited suppliers for critical tech can dictate terms. | Major hardware and software vendors (e.g., Microsoft, Dell) hold significant market share. |

| Switching Costs | High costs to change core systems empower existing suppliers. | Enterprise ERP system migration costs can range from 10% to 30% of original implementation. |

| Proprietary Technology | Scarcity of unique components grants suppliers leverage. | Limited availability of advanced AI chips in 2024 amplified supplier power. |

| Forward Integration Threat | Suppliers offering direct services can bypass intermediaries. | Cloud service providers increasingly engage customers directly, impacting reseller margins. |

What is included in the product

Insight's Porter's Five Forces Analysis reveals the intensity of competition and profitability potential within its industry, detailing threats from new entrants, the power of buyers and suppliers, and the impact of substitutes.

Pinpoint and neutralize competitive threats before they impact profitability, transforming uncertainty into actionable strategies.

Customers Bargaining Power

Customer Price Sensitivity

Customers, particularly large organizations and government bodies, exhibit significant price sensitivity when procuring IT solutions and services. This is evident in their frequent use of competitive bidding, a process designed to secure the most favorable pricing and maximize return on investment. This dynamic directly exerts downward pressure on Insight's pricing strategies and profit margins.

The increasing commoditization of certain IT products further amplifies this customer price sensitivity. For instance, in 2024, the global IT services market saw continued competition, with pricing often being a key differentiator for clients seeking cost-effective solutions. This trend means customers are more likely to compare offerings based on price, making it harder for providers like Insight to command premium pricing without clear value differentiation.

Customer Switching Costs

Customer switching costs for Insight can range from moderate to high, significantly influencing their bargaining power. For intricate managed IT services or large-scale digital transformation initiatives, the process of switching providers is inherently complex. It often involves substantial disruption to ongoing operations, the intricate migration of vast amounts of data, and the necessity for employee retraining. These hurdles effectively diminish a customer's inclination and ability to switch, thereby reducing their bargaining leverage.

Customer Information and Transparency

Customers today are highly informed, especially regarding IT products and services. With vast amounts of information readily available online and the ease of obtaining multiple competitive quotes, clients can easily benchmark pricing and service levels. For instance, in 2024, a significant portion of IT buyers reported using online research to inform their purchasing decisions, often comparing at least three vendor proposals before committing.

This heightened transparency directly translates to increased bargaining power for customers. They can effectively leverage their knowledge to negotiate better terms, discounts, and service level agreements. Insight, therefore, must consistently showcase its unique value proposition, technical expertise, and exceptional customer support to justify its pricing and maintain its competitive edge in the market.

Customer Concentration and Volume

The bargaining power of customers is significantly influenced by customer concentration and the volume of business they represent. For Insight, large enterprise, government, and healthcare contracts are crucial, often forming substantial revenue pillars. The potential loss of a major client can therefore exert considerable leverage on Insight, empowering these large customers in negotiations.

Insight actively works to manage this customer concentration risk. By cultivating enduring client relationships and strategically broadening its customer base across multiple industries, the company aims to dilute the impact of any single client's departure. This diversification strategy is key to maintaining a stable revenue flow and reducing dependence on a few dominant accounts.

- Customer Concentration Impact: Large contracts with enterprise, government, and healthcare clients can represent significant revenue for Insight, granting these customers substantial bargaining power.

- Risk Mitigation: Insight addresses this by prioritizing long-term customer relationships and diversifying its client portfolio across various sectors.

- Revenue Dependence: In fiscal year 2023, Insight reported that its top 10 clients accounted for approximately 21% of its net sales, highlighting the importance of managing these relationships.

- Strategic Diversification: The company's ongoing efforts to expand its reach into new markets and client segments are designed to lessen the impact of losing any single large customer.

Availability of Alternative Solutions for Customers

Customers possess significant bargaining power when numerous alternative solutions are readily available. For Insight, this means clients can easily switch to in-house IT departments, other global IT service providers, or specialized local consultancies, reducing reliance on a single vendor. The ability to compare pricing and service models across these diverse options empowers customers to negotiate more favorable terms.

This wide array of choices allows customers to seek out competing bids or explore alternative delivery models, directly impacting Insight's pricing flexibility and market position. For instance, the global IT services market, valued at approximately $1.3 trillion in 2023, demonstrates the vast competitive landscape Insight operates within, underscoring the critical need for differentiation.

- Customer Alternatives: In-house IT, global IT providers, local consultancies, direct vendor purchases.

- Impact on Bargaining Power: Increases power due to ease of seeking competing bids and alternative delivery models.

- Market Context (2023): Global IT services market valued around $1.3 trillion, highlighting extensive competition.

- Insight's Strategy: Continuous innovation and differentiation of its comprehensive portfolio is essential.

IT Customers Wield Power in a Transparent Market

Customers wield significant power when they can easily switch to alternative suppliers or develop solutions in-house. This is particularly true in the IT sector where a multitude of providers and readily available technologies exist. In 2024, the widespread availability of cloud-based solutions and specialized IT consultancies further empowered customers to explore diverse options, intensifying competition and putting downward pressure on pricing.

The ability for customers to compare offerings and negotiate terms is amplified by transparency in the market. As of mid-2024, a substantial percentage of IT buyers actively engaged in benchmarking pricing and service levels across multiple vendors before making purchasing decisions. This informed approach allows them to leverage their knowledge effectively, demanding better value and driving down margins for providers like Insight.

| Factor | Impact on Customer Bargaining Power | Insight's Response/Market Context |

|---|---|---|

| Availability of Alternatives | High (numerous IT providers, in-house capabilities) | Intensified competition; need for clear differentiation. |

| Customer Information & Transparency | High (easy price/service benchmarking) | Customers demand better value; drives pricing pressure. |

| Switching Costs | Moderate to High (for complex services) | Reduces customer leverage in some instances; requires value demonstration. |

| Customer Concentration | High for large clients | Significant revenue dependence for Insight; major clients have leverage. |

Same Document Delivered

Insight Porter's Five Forces Analysis

This preview showcases the complete Insight Porter's Five Forces Analysis, offering a thorough examination of competitive forces within an industry. The document you see here is the exact, professionally formatted report you will receive immediately after purchase, ensuring no discrepancies or missing information. You're looking at the actual, ready-to-use analysis, providing you with the detailed insights needed to understand and strategize effectively.

Rivalry Among Competitors

Number and Diversity of Competitors

The IT solutions and services market is incredibly crowded, featuring a wide array of competitors. This includes massive global players like Accenture, IBM, and DXC Technology, alongside significant value-added resellers and a multitude of smaller, specialized regional and local companies. This sheer volume and variety of players fuel fierce competition for market share.

Insight, therefore, navigates a landscape where it contends with both large, diversified companies offering a broad spectrum of services and smaller, highly focused niche providers. This dynamic means Insight must constantly differentiate itself to capture and retain customers amidst such diverse competitive pressures.

Industry Growth Rate and Market Maturity

While the broader IT sector continues to expand, driven by digital transformation, some established areas are reaching maturity, intensifying rivalry. For instance, in 2024, global IT spending was projected to reach $5.06 trillion, a 6.8% increase from 2023, yet growth in hardware segments might be slower than in cloud services or AI.

Rapid technological evolution, such as advancements in generative AI and quantum computing, constantly reshapes competitive landscapes, demanding significant and ongoing R&D investment. Companies must remain agile, quickly adapting to new market opportunities and shifting customer needs to maintain a competitive edge.

Product and Service Differentiation

Differentiation in the IT solutions and services sector is a constant battle, with many rivals offering comparable hardware, software, and cloud services. Insight stands out by providing a broad range of offerings, operating globally, possessing significant technical knowledge, and developing solutions specific to different industries. For example, in 2024, Insight reported a 12% increase in revenue from its specialized industry solutions, highlighting the success of this strategy.

Switching Costs for Customers

Customer switching costs for Insight, while present for its more intricate services, are not always a significant barrier. This means clients can explore other options if they find pricing or performance unsatisfactory, fueling competitive rivalry.

This moderate switching cost environment compels competitors to actively seek out Insight's clients. To counter this, Insight prioritizes building robust customer relationships and ensuring consistent, high-quality service delivery to foster loyalty.

- Moderate Switching Costs: While some services have higher switching costs, many of Insight's offerings allow customers to move to competitors with relative ease if unhappy with price or performance.

- Competitive Pressure: This ease of switching intensifies rivalry, as competitors are motivated to attract Insight's existing customer base.

- Customer Retention Strategy: Insight focuses on strengthening client relationships and maintaining exceptional service delivery to mitigate churn.

High Exit Barriers

High exit barriers significantly influence competitive rivalry by making it difficult and costly for companies to leave an industry. This can trap firms in less profitable markets, leading to sustained, sometimes aggressive, competition as they try to recoup their investments. For instance, companies with substantial investments in specialized manufacturing facilities or long-term supply agreements face considerable challenges in divesting these assets or obligations.

Insight's own position is illustrative of this. The company has made considerable investments in its global operational infrastructure and specialized assets, which are not easily transferable or sold. This commitment means Insight, like its competitors with similar commitments, is likely to remain active in its markets, even during periods of lower profitability, to avoid substantial write-offs and to continue servicing existing commitments.

- Significant Capital Investments: Companies often have substantial fixed assets, such as factories or specialized equipment, which are difficult to sell or repurpose, locking them into the industry.

- Long-Term Contracts: Commitments to customers or suppliers through long-term agreements can prevent a company from exiting without incurring penalties or damaging relationships.

- Skilled Workforce Dependencies: Industries requiring highly specialized skills may present exit barriers if a workforce cannot be easily redeployed or if severance costs are high.

- Government or Regulatory Constraints: In some sectors, regulatory approvals or policies can make exiting the market a complex and lengthy process.

Unpacking Fierce Competition in IT Services

The IT solutions and services market is characterized by intense competition due to a vast number of players, from global giants to specialized niche firms. This crowded landscape means companies like Insight must constantly innovate and differentiate to capture market share.

The rivalry is further fueled by moderate customer switching costs, encouraging clients to explore alternatives if dissatisfied, thus pushing competitors to aggressively pursue each other's client base. Insight counters this by focusing on strong customer relationships and consistent service quality.

High exit barriers, stemming from substantial capital investments and specialized assets, mean companies remain in the market even during downturns, perpetuating a competitive environment. For instance, in 2024, the IT sector saw continued investment in digital transformation, creating a dynamic where established players are unlikely to exit easily.

| Competitor Type | Key Characteristics | Impact on Rivalry |

|---|---|---|

| Global IT Giants | Broad service portfolios, extensive resources, established client bases | High pressure through scale and comprehensive offerings |

| Value-Added Resellers (VARs) | Specialized solutions, strong regional presence, customer intimacy | Intense competition in specific market segments |

| Niche & Specialized Firms | Deep expertise in specific technologies or industries, agile service delivery | Disruptive potential, forcing larger players to adapt |

SSubstitutes Threaten

Internal IT Departments and Capabilities

Organizations increasingly possess the capacity to develop or enhance their internal IT departments. This growth directly reduces their dependence on external service providers like Insight for various IT functions. For instance, many companies are investing in cloud infrastructure and managed services, allowing them to handle more operations internally.

The proliferation of user-friendly, low-code/no-code platforms and readily available software empowers businesses to manage a greater portion of their IT needs in-house. This trend is evident in the growing adoption of SaaS solutions for CRM, project management, and data analytics, which often require less specialized external support.

To counter this threat, Insight must clearly articulate its value proposition by showcasing superior efficiency, specialized expertise not easily replicated internally, and demonstrable cost-effectiveness. For example, if Insight can offer a 20% reduction in operational costs for a specific IT function compared to a company’s internal build, that’s a compelling argument.

Direct Vendor Engagement and Cloud Services

Customers increasingly bypass traditional IT solution providers like Insight by directly engaging with hardware and software manufacturers. This trend is amplified by the widespread availability and adoption of public cloud services such as Amazon Web Services (AWS), Microsoft Azure, and Google Cloud. For instance, in 2024, the global cloud computing market was projected to reach over $600 billion, highlighting the significant shift towards direct cloud infrastructure and platform consumption.

While Insight does offer its own cloud solutions, the growing ease with which customers can directly adopt these public cloud platforms can diminish their reliance on traditional IT integration services. This presents a significant threat of substitutes, as customers can potentially achieve similar outcomes without the intermediary. The challenge for Insight lies in clearly articulating and delivering value beyond basic cloud provisioning.

To counter this threat, Insight must strongly emphasize its value-added services. This includes robust cloud management, cost optimization strategies, and advanced security solutions that are often complex for end-users to implement and maintain independently. Demonstrating expertise in these areas is crucial to retain relevance in a market where direct access to technology is becoming the norm.

Open-Source Software and SaaS Alternatives

The rise of powerful open-source software and specialized SaaS alternatives presents a significant threat. Many businesses can now access highly capable and secure solutions at a fraction of the cost compared to proprietary software or custom builds. For instance, the global open-source software market was valued at approximately $20 billion in 2023 and is projected to grow substantially, indicating a strong preference for these alternatives.

These readily available options reduce the reliance on traditional, often more expensive, software providers and in-house development. Companies can leverage these alternatives to meet their needs for functionality and security, thereby mitigating the perceived necessity of higher-priced, bespoke solutions. This trend forces established software vendors to either integrate and support these emerging alternatives or clearly articulate the unique, superior value proposition of their own offerings.

Automation and AI-Driven Solutions

Advancements in automation and AI are creating powerful substitutes for traditional IT managed services. For example, by 2024, Gartner projected that worldwide IT spending on AI software would reach $224 billion, a significant increase from previous years, highlighting the growing adoption of AI-driven solutions that can handle tasks previously requiring human intervention.

These technologies enable businesses to automate routine IT operations and support functions, directly reducing the need for human-intensive managed IT services. This shift means companies offering these services, like Insight, must proactively integrate AI and automation into their own offerings to remain competitive and avoid being replaced by these emerging substitutes.

- AI in IT Operations: By 2025, Gartner predicted that AI for IT operations (AIOps) would be adopted by 50% of IT organizations, up from less than 10% in 2020, demonstrating a clear trend towards automated IT management.

- Cost Efficiency: AI-powered automation can lead to significant cost reductions in IT support, with some studies indicating potential savings of up to 30-40% on operational costs for businesses that effectively implement these technologies.

- Service Delivery Transformation: The threat lies in AI platforms that can offer predictive maintenance, automated troubleshooting, and self-healing IT systems, directly competing with the core services of managed IT providers.

Low-Code/No-Code Development Platforms

The increasing accessibility of low-code and no-code development platforms presents a significant threat of substitutes for traditional software development services. These platforms empower business users to create applications with minimal or no coding expertise, potentially bypassing the need for external development firms for simpler projects.

For instance, Gartner predicted that by 2024, the market for low-code development will reach $26.9 billion, highlighting its rapid adoption and capability to address a wider range of business needs. This trend allows companies to build internal tools, automate workflows, and even develop customer-facing applications more quickly and cost-effectively.

- Reduced Demand for Custom Coding: Low-code/no-code platforms can fulfill a portion of the demand previously met by custom software development, especially for less complex applications.

- Lower Development Costs: By enabling citizen developers, these platforms can significantly reduce the cost associated with application development and maintenance.

- Faster Time-to-Market: The visual development environments offered by these platforms accelerate the creation and deployment of new applications.

- Strategic Imperative for Insight: To counter this threat, Insight must emphasize its role as a strategic partner for intricate integrations, complex enterprise solutions, and comprehensive digital transformation initiatives that go beyond the capabilities of these platforms.

IT Disruption: New Tech Bypasses Traditional Providers

Customers increasingly bypass traditional IT solution providers by directly engaging with hardware and software manufacturers, amplified by the widespread adoption of public cloud services. For instance, the global cloud computing market was projected to exceed $600 billion in 2024, indicating a significant shift towards direct infrastructure consumption.

The rise of powerful open-source software and specialized SaaS alternatives presents a substantial threat, as businesses can access capable solutions at a lower cost. The open-source software market, valued around $20 billion in 2023, shows a strong preference for these alternatives.

Advancements in automation and AI are creating potent substitutes for traditional IT managed services. By 2024, Gartner projected worldwide IT spending on AI software to reach $224 billion, highlighting the growing adoption of AI-driven solutions that handle tasks previously requiring human intervention.

The accessibility of low-code and no-code development platforms empowers business users to create applications with minimal coding, potentially bypassing external development firms for simpler projects. Gartner predicted the low-code market would reach $26.9 billion by 2024, showcasing its rapid adoption.

Entrants Threaten

High Capital Requirements

Entering the global IT solutions and services market, where Insight operates, demands significant capital. Newcomers need to invest heavily in robust infrastructure, advanced technology platforms, and attracting a highly skilled workforce. For instance, building out data centers and cloud capabilities alone can cost tens of millions of dollars.

Established players like Insight have already made these substantial investments and benefit from economies of scale. A new entrant would require considerable financial backing to match Insight's international reach and diverse service offerings, making it difficult to achieve competitive pricing or service levels from the outset.

This high initial financial barrier effectively deters many potential competitors. The sheer scale of investment needed to establish a credible presence in the IT solutions market acts as a powerful deterrent, protecting incumbent firms from widespread new competition.

Economies of Scale and Scope

Existing players like Insight leverage significant economies of scale, allowing them to negotiate better prices with suppliers and achieve greater operational efficiency. For instance, in 2024, major global logistics providers often reported cost savings of 10-15% on procurement due to their sheer volume. This makes it incredibly difficult for newcomers to compete on price from the outset.

Furthermore, Insight benefits from economies of scope by offering a broad suite of integrated services, creating a one-stop shop for clients. A new entrant would need substantial capital and time to build a comparable service portfolio, facing a steep uphill battle to match the bundled value proposition and customer loyalty that scale and scope create.

Access to Distribution Channels and Partnerships

Insight's deep-rooted connections with key hardware and software suppliers are a formidable barrier for newcomers. These established relationships are vital for securing favorable pricing and consistent product availability, factors that are difficult and time-consuming for new entrants to replicate.

For instance, in 2024, the average lead time for securing bulk discounts from major chip manufacturers could extend to 12-18 months, a significant hurdle for startups lacking established credit lines and order volumes. New entrants must invest heavily in building trust and demonstrating reliability to even begin negotiating such partnerships.

Furthermore, Insight's existing network of distribution partners and resellers, cultivated over years, provides immediate market access. New competitors face the arduous task of building their own distribution infrastructure or convincing established players to carry their products, a process often hindered by exclusivity agreements and loyalty programs that favor incumbent suppliers.

Brand Reputation and Customer Loyalty

In the IT services sector, particularly for large enterprise and government contracts, a company's brand reputation, the trust it has cultivated, and a demonstrable history of successful project execution are absolutely critical. Insight has spent years building this very foundation, establishing a strong and reliable image in the market.

Newcomers would find it incredibly difficult to replicate this level of trust and customer loyalty. Without a proven history of delivering successful projects and consistently achieving client satisfaction, a new entrant would struggle to compete for the high-value contracts that depend on established credibility.

- Brand Equity: Insight's established brand name acts as a significant barrier, as clients often prioritize reliability and past performance over potentially lower initial costs from unproven competitors.

- Customer Loyalty: Long-standing relationships and a track record of positive client experiences foster loyalty, making it challenging for new entrants to win over established client bases.

- Trust Factor: For critical IT infrastructure and sensitive data, trust is paramount. New entrants must invest heavily in building this trust, which takes considerable time and consistent positive results.

Talent Acquisition and Retention

The IT solutions and services sector is critically dependent on specialized human capital, such as skilled engineers, consultants, and cybersecurity professionals. This reliance makes talent acquisition and retention a significant ongoing hurdle.

New companies entering this market must make substantial investments in recruitment and comprehensive training programs to cultivate a workforce that can compete with established players. This necessity for significant upfront investment in human resources acts as a considerable barrier to entry.

- Talent Gap: In 2024, the global IT talent shortage was estimated to affect over 70% of companies, highlighting the difficulty in finding qualified personnel.

- Recruitment Costs: The average cost to hire a skilled IT professional can range from $5,000 to $15,000, a substantial outlay for new entrants.

- Retention Challenges: IT professionals often switch jobs for better compensation and growth opportunities; companies may see turnover rates as high as 20-30% annually in certain specialized roles.

IT Solutions: Why New Entrants Face Uphill Battles

The threat of new entrants into the IT solutions and services market, where Insight operates, is significantly mitigated by substantial capital requirements. New companies need to invest heavily in infrastructure, technology, and skilled talent, often costing tens of millions for basic capabilities. Established firms like Insight have already absorbed these costs and benefit from economies of scale, making it difficult for newcomers to compete on price or service levels from the outset.

Existing players also leverage economies of scope, offering integrated services that create a one-stop shop for clients. Building a comparable service portfolio requires significant capital and time, presenting a steep challenge for new entrants aiming to match the bundled value and customer loyalty that scale and scope foster.

Insight’s established relationships with key suppliers, crucial for favorable pricing and product availability, are difficult for new entrants to replicate. For example, in 2024, securing bulk discounts from major chip manufacturers could involve 12-18 month lead times, a hurdle for startups without established credit and order volumes.

Furthermore, Insight benefits from a well-cultivated distribution network, providing immediate market access. New competitors face the arduous task of building their own infrastructure or convincing established players to carry their products, often complicated by exclusivity agreements and loyalty programs favoring incumbents.

Brand reputation and a proven history of successful project execution are paramount in the IT sector, especially for large enterprise and government contracts. Insight has spent years building this critical foundation of trust and reliability, making it difficult for new entrants to compete for high-value contracts without a similar track record.

The IT sector's reliance on specialized talent also poses a barrier. New entrants must invest significantly in recruitment and training to develop a competitive workforce, a substantial upfront cost. In 2024, the global IT talent shortage impacted over 70% of companies, and the average cost to hire a skilled IT professional ranged from $5,000 to $15,000, underscoring the difficulty and expense for new players.

| Barrier | Description | Impact on New Entrants | Example Data (2024) |

|---|---|---|---|

| Capital Requirements | High initial investment in infrastructure, technology, and talent. | Deters new entrants due to substantial financial outlay. | Data center build-out: Tens of millions of dollars. |

| Economies of Scale & Scope | Cost advantages from large-scale operations and broad service offerings. | Makes it difficult for newcomers to compete on price and value proposition. | Logistics cost savings: 10-15% due to volume. |

| Supplier Relationships | Established ties with hardware/software providers for pricing and availability. | New entrants struggle to secure favorable terms and consistent supply. | Chip manufacturer lead times for discounts: 12-18 months. |

| Distribution Channels | Existing networks of distributors and resellers for market access. | New entrants face challenges building or accessing distribution infrastructure. | Exclusivity agreements and loyalty programs favor incumbents. |

| Brand Reputation & Trust | Cultivated image of reliability and successful project execution. | New entrants struggle to build credibility for high-value contracts. | Client prioritization of proven performance over lower initial costs. |

| Human Capital | Need for specialized, skilled IT professionals. | Talent acquisition and retention are costly and challenging. | IT talent shortage: Affecting >70% of companies. Hiring cost: $5,000-$15,000 per professional. |

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis leverages publicly available data from company annual reports, industry-specific market research, and relevant government regulatory filings to provide a comprehensive view of competitive pressures.