Innoviva Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Innoviva Bundle

Don't Miss the Bigger Picture

Innoviva navigates a complex healthcare landscape, facing significant buyer power from large hospital systems and insurers, while the threat of substitutes for its respiratory products is moderate. Understanding the intensity of these forces is crucial for strategic planning.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Innoviva’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Uniqueness of Intellectual Property

The uniqueness of intellectual property (IP) held by Innoviva's partners significantly amplified their bargaining power. When partners possessed proprietary and hard-to-replicate IP related to drug candidates, Innoviva faced limited alternative sources for these crucial innovations. This exclusivity inherently strengthened the suppliers' position in negotiations.

Concentration of Key Partners

The concentration of key partners significantly influences Innoviva's bargaining power. A small number of specialized research institutions or major pharmaceutical firms developing cutting-edge respiratory therapies can wield considerable influence. For instance, if Innoviva's revenue streams are heavily dependent on a few blockbuster partnered products, the leverage of these collaborators naturally increases, potentially impacting contract terms and profit sharing.

Switching Costs for Innoviva

Innoviva's suppliers, particularly those involved in drug development and manufacturing, can wield significant bargaining power. This is largely due to the substantial switching costs associated with changing partners or sourcing new drug candidates after considerable investment in research, development, or commercialization. These high costs create a lock-in effect, empowering existing suppliers to potentially dictate terms for ongoing collaborations and future agreements.

Forward Integration Potential of Suppliers

The forward integration potential for suppliers to Innoviva presents a significant threat. Large pharmaceutical partners, who are essentially Innoviva's customers for its collaboration and royalty management services, could decide to bring these functions in-house. This would mean they develop and commercialize compounds internally, bypassing the need for Innoviva's specialized expertise.

This capability for self-sufficiency among Innoviva's partners directly erodes the company's unique value proposition. If partners can replicate Innoviva's core competencies, their reliance on Innoviva diminishes, thereby increasing the bargaining power of these suppliers (who are Innoviva's customers in this context). For instance, a major pharmaceutical company with substantial R&D infrastructure might find it more cost-effective in the long run to manage its own pipeline of partnered compounds rather than paying ongoing royalties or management fees.

- Reduced Dependence: Partners can internalize collaboration management and royalty structures, decreasing reliance on Innoviva.

- Cost Efficiency: In-house management might be perceived as more economical by large pharmaceutical firms over time.

- Strategic Control: Direct control over the entire drug development and commercialization process offers greater strategic flexibility.

- Erosion of Value Proposition: Innoviva's unique selling points are weakened if partners can replicate its services internally.

Availability of Substitute Innovations

The availability of substitute innovations can significantly influence the bargaining power of suppliers in the pharmaceutical industry, particularly for companies like Innoviva focused on respiratory therapies. While a specific drug candidate might appear unique, the broader landscape of respiratory innovation often presents alternative compounds or therapeutic approaches. For instance, in 2023, the global respiratory drugs market was valued at approximately $70 billion, with significant investment flowing into R&D for new treatments, including biologics and gene therapies, which could serve as substitutes for existing small molecule drugs.

However, the challenge for Innoviva and similar firms lies in identifying equally promising and well-developed assets that are readily available for partnership or acquisition. The development pipeline for novel respiratory treatments is lengthy and capital-intensive, meaning that truly viable substitutes are not always abundant or mature enough for immediate collaboration. This scarcity of advanced, ready-to-partner alternatives can maintain a degree of bargaining power for suppliers who possess such assets.

- Market Dynamics: The global respiratory drugs market, valued at around $70 billion in 2023, indicates substantial investment and competition in developing new treatments.

- Innovation Landscape: While specific drug candidates might be unique, the broader market for respiratory innovations offers alternative compounds and therapeutic approaches like biologics and gene therapies.

- Supplier Leverage: The difficulty in finding equally promising and well-developed assets ready for partnership can still grant significant bargaining power to suppliers holding such innovative compounds.

Supplier Leverage: A Dominant Force in Pharma Partnerships

Innoviva's suppliers, especially those with unique intellectual property, hold considerable bargaining power due to limited alternatives. This power is further amplified when a few key partners dominate Innoviva's revenue streams, giving them leverage in negotiations. Significant switching costs for drug development and manufacturing partners create a lock-in effect, strengthening suppliers' positions.

The potential for suppliers to integrate forward, bringing Innoviva's collaboration and royalty management services in-house, directly challenges its value proposition. If partners can replicate Innoviva's core competencies, their reliance decreases, increasing supplier bargaining power. For example, major pharmaceutical firms might find internal management of their partnered compounds more cost-effective than ongoing fees.

While the broad respiratory innovation market, valued at approximately $70 billion in 2023, offers substitutes, the scarcity of advanced, ready-to-partner assets maintains supplier leverage. The lengthy and capital-intensive nature of developing novel respiratory treatments means truly viable alternatives are not always readily available, empowering suppliers with promising compounds.

| Factor | Impact on Innoviva | Supplier Leverage |

|---|---|---|

| Unique IP | Limited alternatives for crucial innovations | High |

| Partner Concentration | Dependence on a few key collaborators | High |

| Switching Costs | High costs to change partners or source new candidates | High |

| Forward Integration Potential | Partners may internalize services | High |

| Availability of Substitutes | Broad market offers alternatives, but advanced assets are scarce | Moderate to High |

What is included in the product

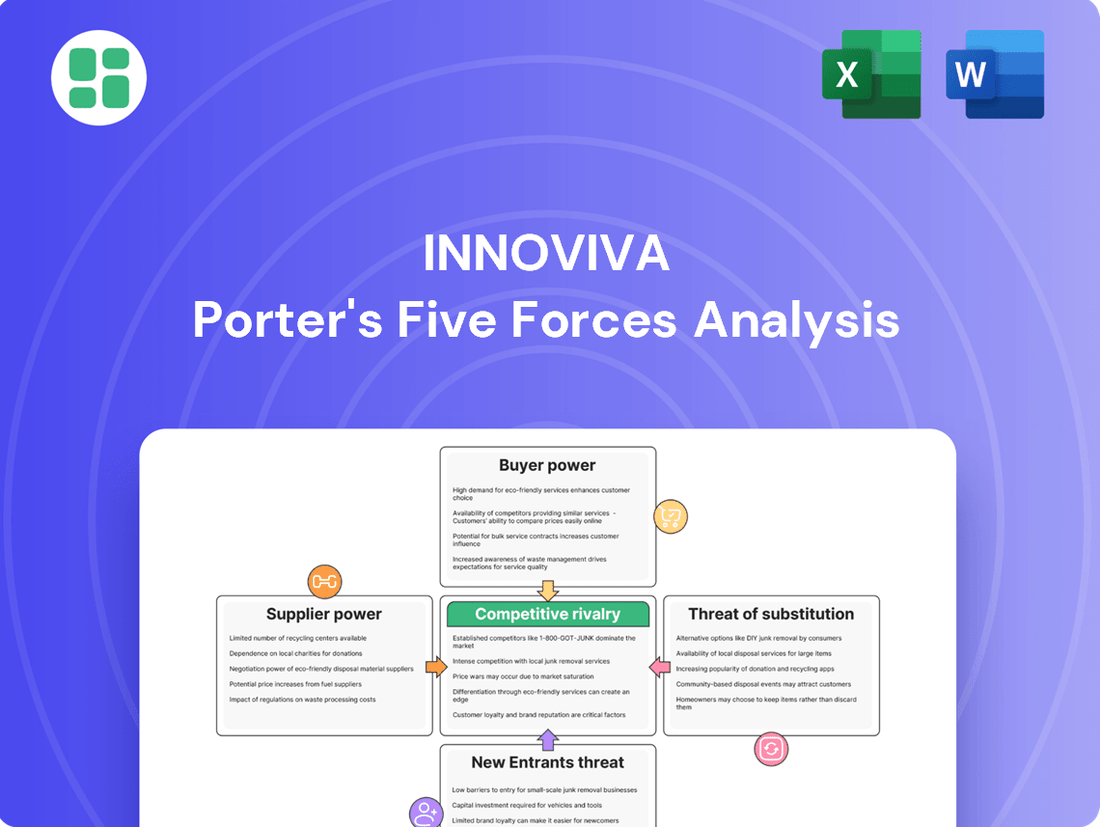

This analysis unpacks the competitive forces impacting Innoviva, detailing industry rivalry, buyer and supplier power, threat of new entrants, and the influence of substitutes.

Identify and mitigate competitive threats with a visual breakdown of industry power dynamics.

Customers Bargaining Power

Concentration of Pharmaceutical Partners

Innoviva's key 'customers' were major pharmaceutical giants like GSK, who were responsible for selling Innoviva's partnered products. This concentration among a few large players meant these companies held significant sway when it came to negotiating royalty percentages and upfront payments.

For instance, in 2023, GSK's sales of products utilizing Innoviva's technology, such as Trelegy Ellipta, continued to be a primary revenue driver for Innoviva, highlighting the dependency and thus the bargaining power of such a large partner.

Availability of Alternative Assets

The availability of alternative assets significantly bolsters the bargaining power of customers, especially large pharmaceutical companies. These entities often possess robust internal research and development pipelines or the financial muscle to acquire promising drug candidates from elsewhere. For instance, in 2024, major pharmaceutical firms continued to invest billions in R&D, with global pharmaceutical R&D spending projected to reach over $200 billion, according to industry reports.

This extensive internal capacity or acquisition potential diminishes their reliance on any single external partnership or supplier. Consequently, they can negotiate more favorable terms when considering collaborations or sourcing specific assets, as they have numerous other options readily available to pursue their strategic goals and bring new therapies to market.

High Switching Costs for Partners

Once a major pharmaceutical company invests heavily in developing and launching a drug with Innoviva, their substantial expenditures on clinical trials, regulatory hurdles, and marketing setup become a significant barrier to switching. This deep commitment naturally pushes them to seek advantageous long-term agreements with Innoviva, effectively leveraging their invested capital to secure better terms.

Price Sensitivity of End-Users and Payers

The ultimate pricing and profitability of respiratory medicines are significantly shaped by healthcare payers and patient affordability. This dynamic creates substantial pressure on commercialization partners, compelling them to negotiate reduced royalty rates from manufacturers like Innoviva.

Innoviva's revenue streams, particularly from its respiratory drug portfolio, are directly impacted by the pricing power of these payers and the out-of-pocket costs for patients. For instance, in 2024, the ongoing scrutiny of drug pricing by governments and insurance providers in major markets like the United States and Europe continues to exert downward pressure on list prices and reimbursement rates for respiratory therapies.

- Healthcare payers, including government programs and private insurers, wield significant influence over drug pricing by controlling formulary access and reimbursement levels.

- Patient affordability, often determined by co-pays, deductibles, and overall healthcare spending, directly affects demand and the willingness to pay for respiratory medications.

- Commercialization partners, facing these pricing constraints, often pass on some of this pressure to Innoviva through renegotiated royalty agreements, impacting Innoviva's net revenue per sale.

Partners' Market Access and Distribution Power

Innoviva's reliance on partners for market access and distribution significantly amplifies customer bargaining power. These partners, possessing established global sales and distribution networks, are crucial for Innoviva's products to reach patients. Without these extensive capabilities, Innoviva's innovative assets would remain inaccessible, granting partners considerable leverage in dictating collaboration terms.

This dependency means that the ultimate customers, through their purchasing decisions and the partners' ability to influence those decisions, exert substantial pressure on Innoviva. For instance, in 2024, the pharmaceutical distribution landscape continued to be dominated by a few large players, many of whom also act as Innoviva's distribution partners. This concentration of power among distributors, who are essentially conduits to the end customer, allows them to negotiate more favorable terms, impacting Innoviva's profitability and market penetration strategies.

The bargaining power of customers, in this context, is channeled through these powerful distribution partners. Key factors influencing this power include:

- Market Concentration of Distributors: A limited number of large distributors can dictate terms due to their control over significant market share.

- Exclusive Distribution Agreements: If Innoviva has exclusive deals, the partner gains more leverage.

- Partner's Existing Product Portfolio: Partners distributing a wide range of products may prioritize those with higher margins or strategic importance to them, influencing how Innoviva's products are promoted.

Customer Bargaining Power Impacts Innoviva's Financials

The bargaining power of Innoviva's customers, primarily large pharmaceutical companies like GSK, is substantial due to their market concentration and the availability of alternative R&D opportunities. For example, in 2023, GSK's sales of Trelegy Ellipta represented a significant portion of Innoviva's revenue, underscoring the partner's influence.

Furthermore, healthcare payers and patient affordability directly impact drug pricing, forcing commercialization partners to negotiate lower royalty rates from Innoviva. In 2024, ongoing scrutiny of drug prices by governments and insurers in key markets like the US and Europe continues to exert downward pressure on respiratory therapy prices.

Innoviva's reliance on its partners for market access and distribution amplifies customer bargaining power. These partners, often large entities with extensive global networks, are critical for product reach. In 2024, the pharmaceutical distribution sector remained dominated by a few major players, allowing them to negotiate favorable terms with Innoviva.

| Customer Type | Key Influencing Factors | Impact on Innoviva |

|---|---|---|

| Major Pharmaceutical Partners (e.g., GSK) | Market concentration, alternative R&D pipelines, significant upfront investment in product development. | Negotiating power over royalty percentages and upfront payments. In 2023, GSK's sales of Trelegy Ellipta highlighted this dependency. |

| Healthcare Payers (Insurers, Governments) | Control over formulary access, reimbursement levels, and drug pricing scrutiny. | Downward pressure on drug prices, leading to renegotiated royalty rates from commercialization partners. Global R&D spending in 2024 exceeded $200 billion, indicating strong alternative development capabilities. |

| Distributors | Market concentration, exclusive distribution agreements, partner's broader product portfolio. | Leverage in dictating collaboration terms and impacting market penetration strategies. The distribution landscape in 2024 remained concentrated among a few large players. |

Preview the Actual Deliverable

Innoviva Porter's Five Forces Analysis

This preview showcases the complete Innoviva Porter's Five Forces Analysis, offering a detailed examination of competitive forces within the respiratory care market. The document you see here is precisely what you will receive immediately after purchase, providing actionable insights into industry rivalry, buyer and supplier power, the threat of new entrants, and the threat of substitutes. You're looking at the actual, professionally formatted document, ready for your immediate use and strategic planning.

Rivalry Among Competitors

Number and Size of Competitors

The biopharmaceutical landscape, particularly within established fields like respiratory diseases, is characterized by a substantial number of significant, well-capitalized pharmaceutical giants. For instance, in 2024, major players such as Pfizer, AbbVie, and AstraZeneca continued to invest heavily in respiratory research and development, with their combined R&D spending in this sector reaching billions of dollars annually. This sheer scale of established competitors creates a formidable barrier to entry and intensifies the battle for market dominance.

Alongside these large corporations, the industry also sees a burgeoning presence of nimble biotechnology firms. These smaller, often more specialized companies are actively pursuing novel therapeutic approaches, frequently leveraging cutting-edge technologies. Their agility allows them to pivot quickly and target unmet needs, adding another layer of competitive pressure. This dynamic ecosystem means Innoviva faces rivalry not only from peers with comparable resources but also from innovative disruptors.

High Fixed Costs and R&D Investment

Developing new pharmaceuticals demands substantial upfront research and development, often running into hundreds of millions of dollars. For instance, the average cost to bring a new drug to market in 2023 was estimated to be over $2 billion. These enormous R&D expenditures, coupled with high fixed costs for specialized manufacturing facilities and extensive distribution networks, create a powerful incentive for companies to achieve significant market share. This necessity to recoup investments fuels aggressive competition among pharmaceutical firms.

Product Differentiation and Patent Protection

Innoviva's competitive rivalry is shaped by product differentiation and patent protection. While patents grant temporary market exclusivity, the respiratory market often features multiple therapeutic options. This necessitates competition on factors like how well a drug works, its safety profile, and ease of use for patients. For instance, the market for COPD treatments includes bronchodilators, inhaled corticosteroids, and combination therapies, each with varying efficacy and patient benefits.

Patent expirations significantly fuel rivalry. As Innoviva's patents for key respiratory drugs expire, generic manufacturers can enter the market. This typically leads to substantial price reductions and increased market share competition. For example, the market for respiratory inhalers has seen increased generic penetration following patent expiries, putting pressure on originator products.

Slow Market Growth in Mature Segments

When market growth slows in established areas of the respiratory sector, competition can become fiercer. Companies then focus on capturing existing business rather than finding new customers, leading to more aggressive pricing and marketing tactics.

This dynamic can pressure Innoviva and its competitors to differentiate through innovation or cost efficiencies. For instance, in 2024, the global respiratory disease market, while growing, saw its mature segments facing increased competition as patented drugs neared or experienced loss of exclusivity.

- Intensified Competition: Mature segments of the respiratory market experience heightened rivalry as companies vie for existing market share.

- Aggressive Strategies: Slower growth compels businesses to adopt aggressive pricing and marketing to maintain or expand their position.

- Impact on Innoviva: Innoviva, like its peers, faces pressure to innovate or optimize costs in these mature segments.

- Market Data: The respiratory disease market in 2024, particularly in its mature segments, reflects this competitive pressure due to patent cliffs and established players.

Competition for Partnership Opportunities

Innoviva's competitive rivalry extends to securing crucial partnerships, as other biotech firms actively pursue licensing deals and collaborations with major pharmaceutical companies. This competition intensifies the race for valuable research and development assets, directly impacting Innoviva's ability to advance its pipeline.

The landscape for strategic alliances is particularly fierce. For instance, in 2024, the biotech sector saw a significant increase in M&A activity and partnership formations, with companies like Moderna and AstraZeneca announcing multiple collaborations in areas like oncology and respiratory diseases. This trend underscores the high demand for innovative assets and the competitive pressure Innoviva faces.

- Intensified Competition for Licensing: Biotech firms vie for the attention of large pharma companies, making it harder for Innoviva to secure favorable licensing agreements for its pipeline assets.

- Asset Valuation Pressure: The crowded partnership market can drive down the perceived value of individual R&D assets, potentially affecting the financial terms Innoviva can negotiate.

- Strategic Partnership Scarcity: Limited opportunities for high-impact collaborations mean Innoviva must differentiate itself to attract and retain the most strategic partners.

Respiratory Market: A Battleground of Giants and Innovators

Innoviva faces intense competition from both large pharmaceutical companies and agile biotech firms in the respiratory sector. Established players like Pfizer and AbbVie, with billions in annual R&D, create significant barriers. Nimble biotechs add pressure by pursuing novel therapies, forcing Innoviva to compete on innovation and efficiency.

| Competitor Type | Key Characteristics | Impact on Innoviva |

|---|---|---|

| Large Pharma | High R&D spending (e.g., billions annually in respiratory), established distribution | Intensified market rivalry, barrier to entry |

| Biotech Firms | Agile, specialized, novel technologies | Disruptive potential, competition for unmet needs |

| Generic Manufacturers | Enter post-patent expiry, drive price reductions | Pressure on originator products, market share erosion |

SSubstitutes Threaten

Alternative Drug Classes and Therapies

Patients managing respiratory conditions often find themselves with a variety of treatment avenues beyond Innoviva's core offerings. For instance, inhaled corticosteroids remain a cornerstone therapy, while long-acting beta-agonists provide bronchodilation. The market also sees increasing use of biologics for specific inflammatory pathways, presenting distinct alternative mechanisms of action.

This broad pharmacological landscape directly translates into a significant threat of substitutes for Innoviva. Consider the global respiratory drug market, projected to reach over $220 billion by 2028, with a substantial portion attributed to these alternative drug classes. Innoviva's ability to compete hinges on demonstrating clear advantages in efficacy, safety, or cost-effectiveness against these established and emerging substitutes.

Non-Pharmacological Interventions

The threat of substitutes for Innoviva's pharmaceutical products, particularly in respiratory care, includes non-pharmacological interventions. Patients may opt for lifestyle changes, such as smoking cessation or exercise, or engage in pulmonary rehabilitation programs. These alternatives can mitigate symptoms and improve quality of life, potentially reducing the demand for certain medications.

Medical devices also present a significant substitute threat. For instance, nebulizers and oxygen therapy can provide symptom relief and support for patients with chronic respiratory conditions, sometimes lessening the need for or frequency of prescribed inhalers. In 2024, the global respiratory devices market was valued at approximately $75 billion, indicating a substantial existing alternative to purely drug-based treatments.

Emergence of Generic and Biosimilar Drugs

Once patents expire, generic and biosimilar versions of established respiratory medicines enter the market at significantly lower prices. For instance, by early 2024, the market for many respiratory inhalers had seen substantial generic penetration following patent expirations, leading to price reductions of up to 80% for comparable products.

This immediate cost advantage makes them highly attractive substitutes, eroding the market share and profitability of branded products. In 2023, the global respiratory drug market experienced a notable shift as generic versions of key treatments gained traction, impacting the revenue streams of originator companies.

Advancements in Medical Technology

The threat of substitutes for Innoviva's respiratory drug therapies is significantly influenced by advancements in medical technology. New diagnostic tools or minimally invasive procedures could emerge as viable alternatives, potentially bypassing the need for traditional pharmaceutical interventions. This technological evolution constantly reshapes how respiratory diseases are managed, offering patients different pathways to treatment.

For instance, the development of advanced gene therapies or regenerative medicine techniques could offer cures or long-term management solutions that are fundamentally different from Innoviva's current product offerings. The increasing precision of robotic surgery and endoscopic interventions also presents a growing substitute threat for certain respiratory conditions where surgical intervention was previously the primary alternative to medication.

Consider the growing pipeline of non-pharmacological treatments. In 2024, venture capital funding for health tech startups focused on diagnostics and minimally invasive procedures reached an estimated $15 billion globally, signaling a strong investor belief in these alternative solutions. This robust investment fuels innovation, increasing the likelihood of disruptive substitutes entering the market.

- Emergence of Novel Diagnostic Tools: Advanced imaging and biomarker identification could enable earlier and more precise disease detection, potentially reducing reliance on long-term drug management.

- Minimally Invasive Procedures: Innovations in interventional pulmonology, such as targeted ablation or stent placement, offer alternatives to medication for specific respiratory ailments.

- Biotechnology Advancements: The rise of gene editing and cell-based therapies presents a long-term threat, potentially offering curative solutions rather than symptom management.

- Digital Health Solutions: Remote monitoring and AI-driven treatment personalization could optimize patient care, potentially reducing the need for certain prescribed medications.

Preventive Measures and Public Health Initiatives

The threat of substitutes for Innoviva's respiratory drug portfolio is significantly influenced by public health initiatives and preventive measures. Effective campaigns promoting smoking cessation, for instance, directly reduce the demand for treatments addressing smoking-related respiratory illnesses. Similarly, widespread vaccination against respiratory infections like influenza or pneumococcal disease can diminish the need for Innoviva's therapeutic interventions. These preventive strategies represent long-term substitutes by reducing the overall incidence and severity of the very conditions Innoviva's products aim to treat.

For example, the Centers for Disease Control and Prevention (CDC) reported in 2024 that smoking-related diseases account for over 480,000 deaths annually in the United States, highlighting the substantial market for cessation aids and treatments. Furthermore, the CDC's Advisory Committee on Immunization Practices (ACIP) continues to recommend pneumococcal vaccination for adults aged 65 and older, a demographic often susceptible to severe respiratory complications. Innovations in air purification technology and improved indoor air quality standards also serve as indirect substitutes by mitigating environmental triggers for respiratory distress.

The impact of these substitutes can be quantified by observing trends in disease prevalence and healthcare utilization:

- Reduced incidence of COPD: Public health efforts to curb smoking have contributed to a gradual decline in the prevalence of Chronic Obstructive Pulmonary Disease (COPD) in some developed nations, potentially impacting the long-term market size for COPD therapeutics.

- Vaccination rates: Higher vaccination rates against influenza and pneumococcal disease, as promoted by public health bodies, directly reduce the number of individuals requiring treatment for these infections. For instance, during the 2023-2024 flu season, vaccine effectiveness against symptomatic illness was estimated to be around 40-50%.

- Air quality improvements: Investments in cleaner energy and stricter environmental regulations, leading to better air quality, can lessen the burden of pollution-induced respiratory ailments, thereby acting as a substitute for treatments targeting such conditions.

- Lifestyle changes: Increased awareness and adoption of healthier lifestyles, including regular exercise and better nutrition, can bolster overall respiratory health, indirectly substituting for pharmaceutical interventions.

Respiratory Therapies: Confronting a Wave of Substitutes and Innovation

The threat of substitutes for Innoviva's respiratory therapies is substantial, encompassing a wide range of pharmacological and non-pharmacological alternatives. These include established drug classes like inhaled corticosteroids and long-acting beta-agonists, as well as emerging biologics and even lifestyle modifications such as smoking cessation and pulmonary rehabilitation. The global respiratory drug market's projected growth to over $220 billion by 2028 underscores the competitive landscape, where Innoviva must demonstrate clear advantages.

Medical devices, valued at approximately $75 billion in 2024 for the respiratory devices market, also pose a significant threat, offering symptom relief through nebulizers and oxygen therapy. Furthermore, the expiration of patents allows for the entry of lower-cost generic and biosimilar versions, which by early 2024 had led to price reductions of up to 80% for comparable products, directly impacting branded market share.

Technological advancements, such as novel diagnostic tools, minimally invasive procedures, and even gene therapies, represent a growing substitute threat by offering alternative management pathways. The $15 billion in global venture capital funding for health tech startups in 2024 highlights the rapid innovation in these areas. Public health initiatives promoting smoking cessation and vaccination also reduce the underlying demand for Innoviva's treatments, with smoking-related diseases causing over 480,000 deaths annually in the US as of 2024.

| Substitute Category | Examples | Market Data/Impact |

|---|---|---|

| Pharmacological | Inhaled Corticosteroids, Long-Acting Beta-Agonists, Biologics | Global respiratory drug market projected >$220B by 2028 |

| Non-Pharmacological | Smoking Cessation, Pulmonary Rehabilitation, Lifestyle Changes | Smoking-related diseases cause >480,000 deaths annually (US, 2024) |

| Medical Devices | Nebulizers, Oxygen Therapy | Global respiratory devices market ~ $75B (2024) |

| Generics/Biosimilars | Off-patent versions of existing drugs | Price reductions up to 80% post-patent expiry (early 2024) |

| Technological Advancements | Gene Therapy, Minimally Invasive Procedures | $15B VC funding for health tech startups (2024) |

Entrants Threaten

High Capital Requirements

High capital requirements represent a significant barrier to entry in the biopharmaceutical sector, a core area for Innoviva. Developing and bringing a new drug to market is an incredibly expensive undertaking. For instance, the cost of clinical trials alone can run into hundreds of millions of dollars, with some estimates for a single drug exceeding $2.6 billion. This immense financial hurdle makes it exceedingly difficult for new companies to compete with established players.

These substantial upfront investments in research and development, coupled with the lengthy and complex process of obtaining regulatory approvals, effectively deter many potential new entrants. Companies need deep pockets to navigate these challenges, from initial laboratory work through Phase III trials and post-market surveillance. The sheer scale of capital needed ensures that only well-funded organizations can realistically consider entering this space, thus protecting incumbent firms like Innoviva.

Extensive Regulatory Hurdles

The biopharmaceutical sector faces substantial entry barriers due to extensive regulatory hurdles. Agencies like the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA) mandate complex and time-consuming clinical trials, demanding adherence to stringent Good Manufacturing Practices (GMP). For instance, bringing a new drug to market can take over a decade and cost billions, with success rates for drugs entering Phase 1 trials often below 10%.

Need for Specialized Scientific Expertise

Innoviva's biopharmaceutical sector faces a significant threat from new entrants lacking specialized scientific expertise. Success in this field demands deep knowledge in molecular biology, pharmacology, and clinical development, areas where established players like Innoviva have invested heavily in R&D and talent acquisition.

New companies struggle to replicate this scientific foundation, making it difficult to compete effectively. For instance, the average R&D expenditure for a biopharmaceutical company can run into hundreds of millions of dollars annually, a substantial barrier for startups.

Strong Patent Protection and IP Landscape

The threat of new entrants in the pharmaceutical sector, particularly for companies like Innoviva, is significantly mitigated by strong patent protection and a complex intellectual property (IP) landscape. Established players possess extensive patent portfolios covering their innovative drugs, which act as a substantial barrier for newcomers. For instance, in 2024, the average patent life for a new drug can extend for many years, providing a significant window of exclusivity.

Developing novel compounds that avoid infringing on these existing patents is an incredibly difficult and expensive undertaking. Furthermore, securing new intellectual property rights requires substantial investment in research and development, often running into hundreds of millions of dollars, making it a high-risk proposition for potential new entrants.

- Patent Exclusivity: Pharmaceutical patents typically grant 20 years of exclusivity from the filing date, though effective market exclusivity is often shorter due to development and regulatory review periods.

- R&D Investment: The cost to bring a new drug to market in 2024 is estimated to be over $2 billion, with a significant portion allocated to IP protection and navigating existing patent claims.

- IP Litigation: Companies actively defend their patents through litigation, further increasing the cost and risk for any potential new entrant attempting to enter the market with similar products.

Brand Loyalty and Established Distribution Channels

New entrants to the pharmaceutical market, like Innoviva, face significant hurdles in overcoming established brand loyalty. Healthcare providers and patients often trust well-known brands with a proven track record, making it difficult for newcomers to gain traction. For instance, in 2024, the top 10 pharmaceutical companies continued to hold a substantial market share, reflecting the enduring power of brand recognition and patient familiarity.

Accessing and navigating established distribution channels presents another formidable barrier. Major pharmaceutical companies have long-standing relationships with wholesalers, pharmacies, and hospital formularies. Breaking into these networks requires substantial investment and strategic partnerships, a challenge that can deter potential new competitors seeking to distribute their products effectively.

- Brand Loyalty: Established pharmaceutical brands benefit from decades of trust and recognition among healthcare professionals and patients, making it difficult for new entrants to capture market share.

- Distribution Channels: Gaining access to existing distribution networks, including wholesalers and pharmacy benefit managers, is a significant barrier due to established relationships and contractual agreements.

- Regulatory Hurdles: The stringent regulatory approval process for new drugs further increases the cost and time required for market entry, acting as a deterrent to potential new competitors.

- R&D Investment: The high cost of research and development in the pharmaceutical sector means that new entrants must have substantial capital to compete with established players who have ongoing pipelines.

Biopharma Entry Barriers: A Fortress Against New Competitors

The threat of new entrants for Innoviva is considerably low due to the immense capital required to enter the biopharmaceutical market. Developing a single drug can cost upwards of $2.6 billion, a figure that includes extensive research, clinical trials, and regulatory approvals. This financial barrier, coupled with the decade-long development timeline and success rates below 10% for drugs entering early-stage trials, effectively deters most potential competitors.

Strong patent protection and a complex intellectual property landscape further solidify this low threat. Innoviva, like other established players, benefits from extensive patent portfolios that can grant exclusivity for many years, as seen with average patent life extending significantly in 2024. Navigating and avoiding infringement on existing patents is a costly and difficult endeavor for newcomers.

Additionally, deep scientific expertise is crucial, with companies like Innoviva investing hundreds of millions annually in R&D and talent. Replicating this specialized knowledge and the established brand loyalty among healthcare providers and patients presents a formidable challenge for any emerging competitor. Accessing established distribution channels also requires significant investment and strategic partnerships.

| Barrier | Description | Impact on New Entrants |

|---|---|---|

| Capital Requirements | Drug development costs exceed $2.6 billion; R&D investment in 2024 averages hundreds of millions annually for biopharma. | Extremely high barrier, limiting entry to well-funded organizations. |

| Regulatory Hurdles | FDA/EMA approval requires complex, lengthy trials (over a decade); stringent GMP adherence. | Significant time and cost investment, increasing risk. |

| Intellectual Property | Extensive patent portfolios provide exclusivity; avoiding infringement is costly and difficult. | Requires substantial R&D and legal investment to compete. |

| Scientific Expertise | Requires deep knowledge in molecular biology, pharmacology, and clinical development. | Difficult for new entrants to replicate established R&D capabilities. |

| Brand Loyalty & Distribution | Established trust and long-standing relationships with distributors. | Challenging to gain market share and product access. |

Porter's Five Forces Analysis Data Sources

Our Innoviva Porter's Five Forces analysis is built upon a foundation of robust data, including Innoviva's annual reports, SEC filings, and industry-specific market research from reputable firms like IQVIA.