Helmerich & Payne Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Helmerich & Payne Bundle

Go Beyond the Preview—Access the Full Strategic Report

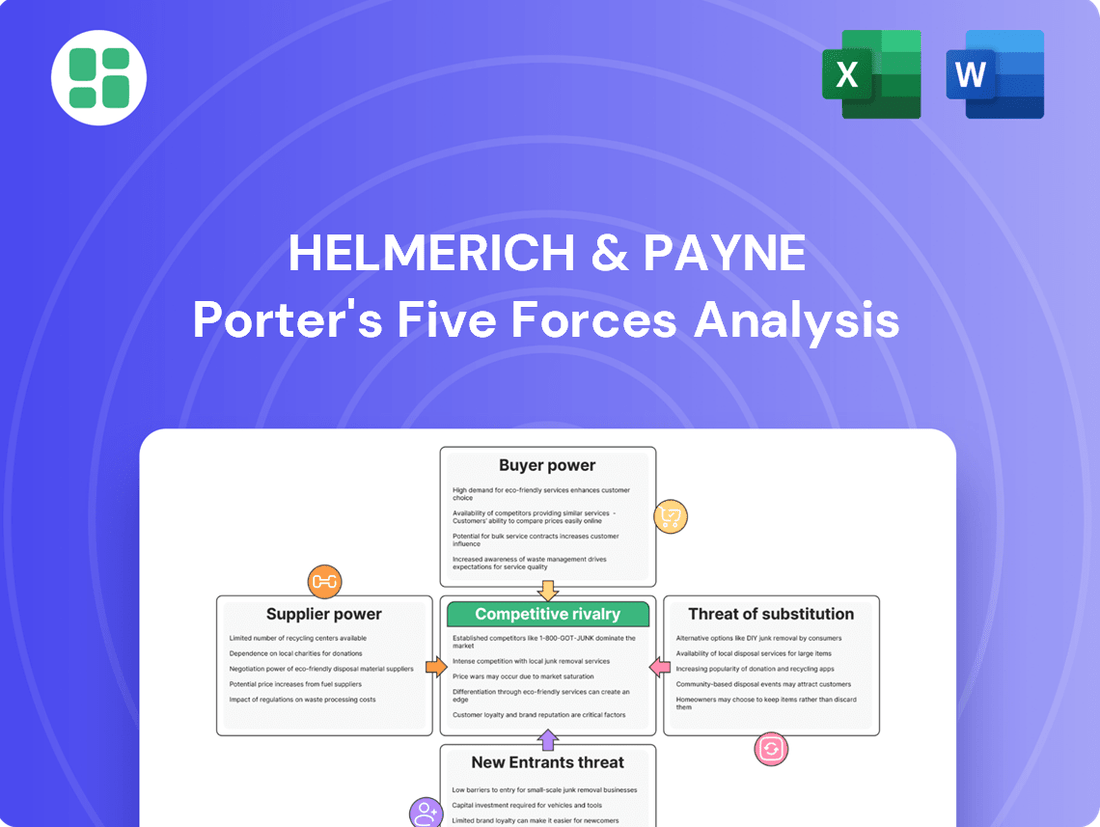

Helmerich & Payne operates in a dynamic oilfield services sector, where understanding the competitive landscape is crucial for success. Our Porter's Five Forces analysis delves into the bargaining power of both buyers and suppliers, the threat of new entrants and substitute products, and the intensity of rivalry within the industry.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Helmerich & Payne’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Supplier Concentration and Specialization

The oil and gas drilling sector, including companies like Helmerich & Payne, often depends on a limited number of suppliers for highly specialized equipment and services. This specialization, ranging from advanced drilling components to sophisticated IT solutions and skilled labor, inherently concentrates power among these providers. For instance, unique drilling muds or specialized cement formulations have demonstrated more consistent pricing in 2024, reflecting the supplier's leverage in these niche markets.

Availability of Skilled Labor

The availability of a skilled workforce, especially for specialized roles like directional drillers, directly impacts supplier power. A shortage in these critical skill sets amplifies the leverage of labor suppliers and specialized service providers.

Helmerich & Payne, like many in the oil and gas sector, has navigated a persistent skillset gap. This scarcity means that companies relying on these specialized services often face increased costs and potentially less favorable terms from suppliers who can command higher prices due to demand.

The industry's push for automation, aimed at improving efficiency and consistency, also highlights the importance of skilled labor. As automation helps address the need for repeatable results, the demand for the human expertise to manage and optimize these advanced systems remains high, further strengthening the bargaining position of those possessing these in-demand skills.

Cost of Key Raw Materials and Components

Suppliers of essential raw materials like steel for drilling rigs and various consumables hold significant bargaining power, largely dictated by the volatility of commodity prices. For instance, while the cost of Oil Country Tubular Goods (OCTG) and sand saw notable decreases in 2024, other critical inputs such as drilling mud and cement maintained more stable pricing, showcasing a differentiated supplier influence across the input spectrum.

Switching Costs for H&P

Helmerich & Payne's significant investments in proprietary rig designs and advanced technologies, particularly its FlexRig fleet, can lead to substantial switching costs for critical components and integrated software. This technological integration means that changing suppliers for these deeply embedded systems would likely involve considerable expense and operational disruption.

For instance, if a key supplier for H&P's advanced drilling automation software or specialized downhole tools were to increase prices, H&P might find it economically challenging to switch to an alternative. This dependency grants suppliers a degree of bargaining power, as the cost and complexity of integrating new systems can be prohibitive.

In 2023, Helmerich & Payne reported capital expenditures of $621 million, a substantial portion of which would have been allocated to the development and maintenance of its technologically advanced fleet. This investment underscores the embedded nature of its supplier relationships and the potential switching costs involved.

- Technological Integration: H&P's proprietary rig designs, like the FlexRig, often utilize highly integrated components and software.

- Supplier Dependency: This deep integration can create a reliance on specific suppliers whose products are essential for H&P's operational efficiency.

- Switching Cost Barrier: Changing suppliers for these specialized or proprietary elements would likely incur significant costs related to re-engineering, testing, and implementation.

- Supplier Bargaining Power: The high switching costs empower suppliers, giving them leverage in price negotiations or contract terms.

Potential for Forward Integration by Suppliers

While less common, some large, integrated oilfield service companies that supply equipment might consider forward integrating into contract drilling. This move could potentially increase their bargaining power by offering a more comprehensive service package. However, the substantial capital expenditure required to own and operate drilling rigs presents a significant barrier for most suppliers looking to enter this market.

The capital intensity of contract drilling is a key factor. For instance, a new land drilling rig can cost upwards of $20 million, with offshore rigs costing significantly more. This high upfront investment makes it challenging for equipment suppliers to absorb the costs associated with operating a fleet of drilling rigs, thereby limiting their ability to forward integrate and exert greater influence.

- High Capital Costs: The purchase and maintenance of drilling rigs represent a major financial commitment, deterring many suppliers from forward integration.

- Operational Expertise: Contract drilling requires specialized operational knowledge and management, which may not be a core competency for equipment manufacturers.

- Market Dynamics: The cyclical nature of the oil and gas industry can make the investment in drilling operations risky for companies primarily focused on equipment supply.

Supplier Power: A Key Factor in Drilling Costs

Suppliers of specialized drilling components and advanced technology for companies like Helmerich & Payne often wield considerable bargaining power due to industry concentration and high switching costs. This is particularly evident with proprietary software and integrated systems, where the expense and complexity of replacement limit H&P's ability to seek alternative providers. For example, in 2024, prices for certain specialized drilling muds and cement formulations remained firm, reflecting the supplier's leverage in these niche markets, despite some commodity price decreases.

The scarcity of highly skilled labor, such as directional drillers, further amplifies supplier power, as companies compete for limited expertise, driving up costs. Helmerich & Payne's 2023 capital expenditures of $621 million highlight the significant investment in its advanced fleet, underscoring the embedded nature of these supplier relationships and the associated switching costs.

While forward integration by equipment suppliers into contract drilling is limited by the substantial capital requirements, estimated at over $20 million per land rig, the bargaining power of specialized component and technology providers remains a key factor for H&P.

| Factor | Impact on Supplier Bargaining Power | Example for Helmerich & Payne |

| Supplier Concentration | High for specialized equipment/services | Limited number of providers for advanced drilling automation software |

| Switching Costs | High due to technological integration | Significant costs to replace proprietary FlexRig components or software |

| Labor Scarcity | High for skilled drilling personnel | Increased costs for specialized labor like directional drillers |

| Commodity Price Volatility | Mixed; some inputs stable, others volatile | Stable pricing for drilling muds in 2024 vs. fluctuating OCTG costs |

What is included in the product

Tailored exclusively for Helmerich & Payne, analyzing its position within its competitive landscape by evaluating the intensity of rivalry, buyer and supplier power, threat of new entrants, and the impact of substitutes.

Instantly identify and address competitive threats with a dynamic "what-if" scenario planner for each force.

Customers Bargaining Power

Customer Concentration and Size

Helmerich & Payne's (H&P) customer base is largely comprised of significant exploration and production (E&P) companies, encompassing both major oil corporations and independent producers. This concentration means H&P frequently engages with a select few, very powerful buyers.

The upstream sector has seen substantial consolidation, with notable megamergers occurring in key areas like the Permian Basin. This trend further concentrates H&P's customer base, amplifying the bargaining power of these large, consolidated entities who can demand advanced, scalable services.

Customers' Ability to Switch Contractors

Customers in the drilling sector can switch between contractors, with this ease influenced by rig availability, contract specifics, and the unique skills each company brings. Helmerich & Payne's (H&P) advanced rigs and technology are designed to make switching harder, but the market in 2024 saw declining day rates, indicating customers still have significant sway.

Importance of Drilling Services to Customer Operations

Drilling services are absolutely vital for exploration and production (E&P) companies to get oil and gas out of the ground. This means companies like Helmerich & Payne (H&P) provide a service that's hard to live without. In 2024, E&P companies are really zeroing in on keeping costs down and hitting their profit targets. They're looking for ways to drill more efficiently, often meaning they need fewer rigs to get the job done, which puts pressure on service providers.

Customers' Access to Information and Pricing Transparency

Customers in the drilling services sector, particularly major oil and gas companies, are often sophisticated buyers. They possess considerable market knowledge, enabling them to readily compare pricing and service offerings from various providers. This access to information, especially concerning rig availability and prevailing day rates in active basins, significantly bolsters their negotiating position.

For instance, in 2024, the North American land drilling market saw intense competition among contract drillers. Customers could easily obtain quotes and benchmark day rates, with some reports indicating that average day rates for premium land rigs fluctuated based on demand and rig type, but transparency allowed for informed negotiation. This transparency means customers can effectively leverage competitive bids to secure more favorable terms.

- Informed Negotiation: Customers can compare day rates and service quality across multiple drilling contractors, leading to more competitive pricing.

- Market Data Access: Sophisticated clients have access to industry reports and real-time data on rig utilization and day rates, enhancing their bargaining leverage.

- Competitive Landscape: In basins with numerous drilling service providers, customers benefit from a highly competitive environment that drives down costs.

- Contract Flexibility: Increased information empowers customers to negotiate more flexible contract terms, aligning with their project needs and market outlook.

Potential for Backward Integration by Customers

The potential for customers, particularly large Exploration and Production (E&P) companies, to engage in backward integration by operating their own drilling rigs poses a significant bargaining chip. While the substantial capital investment and specialized knowledge needed make this rare, its mere possibility acts as a latent threat, influencing Helmerich & Payne's pricing power.

For instance, in 2024, the average cost to acquire and outfit a new land drilling rig can range from $15 million to $30 million, a considerable barrier to entry for most E&P firms. Furthermore, the operational expertise required for efficient and safe drilling operations is a highly specialized field, often necessitating dedicated teams and ongoing training.

- Customer Integration Threat: Large E&P companies could, in theory, bring drilling operations in-house.

- Capital Intensity Barrier: Acquiring and maintaining drilling rigs requires significant financial outlay, estimated in the tens of millions of dollars per rig in 2024.

- Operational Expertise Gap: The specialized skills needed for efficient rig operation are a deterrent to self-operation for many E&P firms.

- Pricing Negotiation Leverage: The theoretical ability of customers to integrate backward can influence their willingness to negotiate pricing with rig service providers like Helmerich & Payne.

Client Power Shapes Drilling Service Pricing

Helmerich & Payne's customers, primarily large E&P companies, wield significant bargaining power due to market consolidation and their sophisticated understanding of drilling services. In 2024, the competitive landscape, marked by fluctuating day rates, allowed these clients to leverage market data and benchmark pricing effectively, securing more favorable contract terms. This informed negotiation capability, coupled with the potential for backward integration, keeps pressure on H&P's pricing strategies.

| Customer Type | Bargaining Power Factors | 2024 Market Impact |

|---|---|---|

| Major E&P Companies | Market consolidation, informed negotiation, potential backward integration | Ability to drive down day rates, demand for efficient services |

| Independent Producers | Access to market data, rig availability comparisons | Negotiate based on competitive bids, seek flexible contract terms |

| Overall Customer Base | High switching potential (influenced by rig tech), focus on cost efficiency | Pressure on service providers to offer value-added solutions and competitive pricing |

What You See Is What You Get

Helmerich & Payne Porter's Five Forces Analysis

This preview showcases the complete Helmerich & Payne Porter's Five Forces Analysis, detailing the competitive landscape for the company. The analysis meticulously examines the bargaining power of buyers and suppliers, the threat of new entrants and substitutes, and the intensity of rivalry within the oil and gas drilling sector. What you see here is the exact, professionally formatted document you will receive immediately after purchase, ready for your strategic review.

Rivalry Among Competitors

Number and Size of Competitors

The contract drilling market, especially within the U.S. land rig sector where Helmerich & Payne is a major force, features several significant, long-standing companies such as Nabors Industries and Patterson-UTI Energy. These key competitors actively compete for market dominance, fueling a highly competitive environment.

In 2024, the U.S. land drilling market saw a notable number of active rigs. For instance, as of early 2024, the number of active land rigs in the U.S. hovered around the 600-650 mark, with Helmerich & Payne, Nabors, and Patterson-UTI consistently operating a substantial portion of these fleets. This concentration among a few large players intensifies the rivalry for contracts and operational efficiency.

Industry Growth and Rig Utilization

The oil and gas drilling sector is inherently cyclical, and the global onshore market is projected for a relatively flat performance between 2024 and 2025. While some areas might see modest upticks in rig and well activity, the overall picture suggests limited expansion.

This environment directly impacts competitive rivalry. In December 2024, U.S. rig utilization rates dipped to 74.01%, a clear indicator of an oversupplied market and softened demand. This oversupply forces drilling companies to compete more aggressively for the available work, putting downward pressure on pricing and margins.

High Fixed Costs and Exit Barriers

The oil and gas drilling sector, including companies like Helmerich & Payne, is inherently capital-intensive. Significant investments are required for advanced drilling rigs, specialized equipment, and supporting infrastructure, resulting in substantial fixed costs. For instance, a modern land rig can cost tens of millions of dollars, and offshore rigs even more.

These high upfront investments create considerable exit barriers. Once a company has committed these vast sums, it becomes economically challenging to simply cease operations, even when market conditions are unfavorable. This compels firms to continue drilling and incurring operating expenses, which can intensify competition and pressure day rates, particularly during industry downturns.

In 2024, the industry experienced fluctuating demand for drilling services, influenced by global energy prices and geopolitical events. Despite some recovery, the substantial fixed cost base meant that companies often had to operate at lower utilization rates to maintain market share, further exacerbating the impact of high fixed costs on profitability.

Differentiation of Rigs and Technology

Helmerich & Payne (HP) actively differentiates its offerings through cutting-edge technology, notably its super-spec rigs and advanced automation features. This focus on technological superiority allows HP to deliver enhanced operational efficiency and execution, which in turn supports premium day rates and performance-based contracts. For instance, in 2024, the company continued to emphasize its technologically advanced FlexRig® fleet, designed for optimal performance in complex drilling environments.

While HP invests heavily in these technological advancements, the competitive landscape necessitates that rivals also pursue similar innovations. This creates a dynamic where differentiation is a continuous effort, as competitors are also deploying advanced rig designs and automation solutions to capture market share. The industry sees a constant push to integrate digital technologies and improve rig capabilities, making it challenging to maintain a sustained technological edge.

- Technological Edge: HP's super-spec rigs and automation aim for superior operational execution and efficiency.

- Rate Impact: This differentiation allows for higher day rates or performance-based contracts.

- Competitive Response: Competitors are also investing in similar technological advancements, intensifying rivalry.

- Industry Trend: The ongoing integration of digital technologies and rig enhancements is a key industry trend in 2024.

Pricing Strategies and Contract Models

Competitive rivalry in the oil and gas drilling sector is intense, significantly impacting pricing strategies. In 2024, U.S. composite day rates experienced a decline for eleven consecutive months, underscoring the pressure on service providers.

Helmerich & Payne is adapting by shifting from traditional day-rate contracts to performance-based agreements. This model incentivizes exceeding specific operational metrics, offering bonuses for superior performance.

- Pricing Pressure: U.S. composite day rates saw a decline for 11 consecutive months in 2024.

- Contract Evolution: Helmerich & Payne is moving towards performance-based contracts.

- Margin Protection: This strategy aims to safeguard profit margins in a competitive landscape.

- Service Differentiation: Performance incentives help differentiate H&P's offerings.

U.S. Land Rig Market: Fierce Competition and Declining Rates

Competitive rivalry in the contract drilling market, particularly in the U.S. land rig sector, is fierce due to the presence of established players like Nabors Industries and Patterson-UTI Energy. In 2024, the U.S. land rig market, with approximately 600-650 active rigs, saw a utilization rate dip to 74.01% by December, indicating oversupply and intensified competition for contracts.

This intense competition, coupled with high fixed costs associated with capital-intensive drilling equipment, forces companies to operate aggressively, often at lower utilization rates, to maintain market share. Helmerich & Payne's strategy of focusing on technologically advanced rigs and shifting towards performance-based contracts aims to mitigate pricing pressures and differentiate its services in this challenging environment.

| Metric | 2024 Data Point | Implication for Rivalry |

|---|---|---|

| U.S. Active Land Rigs | ~600-650 | Concentration of fleet among major players intensifies competition. |

| U.S. Rig Utilization (Dec 2024) | 74.01% | Oversupply leads to aggressive pricing and competition for work. |

| Day Rate Trend (2024) | 11 consecutive months of decline (composite) | Significant downward pressure on pricing due to rivalry. |

| HP's Strategic Shift | Performance-based contracts | Attempt to capture value and differentiate beyond price. |

SSubstitutes Threaten

Alternative Hydrocarbon Extraction Methods

While direct substitutes for drilling new oil and gas wells are scarce, existing production can be extended through alternative hydrocarbon extraction methods. Enhanced Oil Recovery (EOR) techniques, such as waterflooding or gas injection, can boost output from mature fields, thereby reducing the immediate demand for new drilling. For instance, in 2023, EOR projects continued to be a significant part of production strategies for many major oil producers, contributing to overall supply without requiring entirely new well construction.

Growth of Renewable Energy Sources

The increasing viability and widespread adoption of renewable energy sources represent a significant long-term threat to companies like Helmerich & Payne. As global investments surge into low-carbon technologies, the fundamental demand for oil and gas drilling services could diminish over time. For instance, in 2024, global renewable energy capacity additions were projected to reach record levels, with solar PV and wind power leading the charge, impacting the long-term outlook for fossil fuel extraction.

Increased Efficiency in Drilling Operations

Technological advancements are significantly boosting drilling efficiency. For instance, by late 2023, the average U.S. land rig could achieve production targets that previously required 1.5 to 2 rigs, a testament to improved drilling techniques and equipment.

This enhanced productivity means exploration and production (E&P) companies can meet their output goals with a smaller fleet of active rigs. This trend effectively substitutes the need for additional drilling services, as existing capacity is leveraged more effectively.

In 2024, the average U.S. land rig count hovered around 500-600, a notable decrease from earlier peaks, reflecting this operational efficiency. This reduction in demand for rigs directly impacts companies like Helmerich & Payne, as fewer active rigs translate to fewer contracted services.

Customer Shift to Different Energy Sources

Exploration and Production (E&P) companies, Helmerich & Payne's primary customers, are increasingly diversifying their energy portfolios. This shift is driven by a confluence of factors, including evolving environmental regulations and growing investor demand for sustainable practices. For instance, in 2024, global investment in renewable energy sources continued its upward trajectory, with projections indicating significant growth in solar and wind power capacity additions.

This strategic pivot by E&P firms means they may prioritize investments in renewable energy projects or focus on maximizing the efficiency of their existing oil and gas assets rather than initiating new drilling campaigns. This represents a substantial long-term threat, as it directly reduces the demand for traditional drilling services that Helmerich & Payne provides.

The changing energy landscape presents a clear substitute threat to the conventional oil and gas drilling market. Consider the following implications:

- Reduced Demand for Drilling Services: As E&P companies allocate capital to renewables, the need for new well construction, a core service for Helmerich & Payne, diminishes.

- Focus on Asset Optimization: Instead of expanding, companies may focus on enhancing the output of existing fields, requiring different types of services.

- Commodity Price Volatility: Fluctuations in oil and gas prices can accelerate or decelerate this shift, making long-term demand forecasting more challenging.

- Investor Pressure for ESG: Environmental, Social, and Governance (ESG) mandates are pushing companies to demonstrate a commitment to cleaner energy, influencing capital allocation decisions away from fossil fuel exploration.

Economic Viability and Maturity of Substitutes

The economic viability and technological maturity of alternative energy sources and extraction methods are constantly changing. While conventional drilling is still crucial for meeting today's worldwide energy needs, the decreasing cost and improving performance of renewable energy options, alongside efficiency advancements in current operations, present a significant and growing threat from substitutes.

For instance, by the end of 2023, global renewable energy capacity saw a substantial increase, with solar and wind power leading the charge. The International Energy Agency (IEA) reported that renewable energy sources accounted for over 80% of new power capacity additions globally in 2023. This ongoing expansion and cost reduction in renewables directly challenge the long-term demand for traditional oil and gas extraction services.

- Technological Advancements: Innovations in solar panel efficiency and wind turbine technology continue to lower the levelized cost of electricity (LCOE) for renewables.

- Investment Trends: Global investment in clean energy reached record highs in 2023, surpassing $1.7 trillion according to the IEA, signaling a strong market preference for alternatives.

- Energy Transition Policies: Government mandates and incentives worldwide are accelerating the adoption of renewable energy, further diminishing reliance on fossil fuels.

- Cost Competitiveness: In many regions, new solar and wind power projects are now cheaper to build and operate than new fossil fuel power plants.

Renewables and Efficiency: The Evolving Threat to Drilling Services

The threat of substitutes for oil and gas drilling services is evolving, primarily driven by the growth of renewable energy and increased efficiency in existing operations. As renewable energy sources become more cost-competitive and widely adopted, they directly reduce the long-term demand for fossil fuels, and consequently, for the drilling services required to extract them. For example, global investment in clean energy surpassed $1.7 trillion in 2023, indicating a significant shift in capital allocation away from traditional energy sources.

Technological advancements in drilling itself also act as a substitute, allowing E&P companies to achieve higher production with fewer rigs. By late 2023, improvements meant a single U.S. land rig could accomplish what previously needed 1.5 to 2 rigs. This operational efficiency means fewer active rigs are contracted, directly impacting demand for drilling companies like Helmerich & Payne. The average U.S. land rig count in 2024, hovering around 500-600, reflects this trend of optimized operations.

Furthermore, Exploration and Production companies are diversifying their portfolios towards renewables due to investor pressure for ESG compliance and evolving regulations. This strategic shift means less capital is allocated to new drilling campaigns, further diminishing the market for traditional drilling services. The increasing viability of alternatives, coupled with efficiency gains, presents a growing substitute threat.

| Substitute Factor | Impact on Drilling Demand | 2023/2024 Data Point |

|---|---|---|

| Renewable Energy Growth | Reduces long-term demand for fossil fuels | Global clean energy investment exceeded $1.7 trillion in 2023. |

| Drilling Efficiency | Decreases the number of rigs needed | Improved rig productivity by late 2023 allowed 1 rig to do the work of 1.5-2 previously. |

| E&P Portfolio Diversification | Shifts capital away from new drilling | Projected record additions in solar PV and wind capacity in 2024. |

Entrants Threaten

High Capital Requirements

The oil and gas drilling sector, particularly for advanced rigs, necessitates massive upfront capital. For instance, a single modern drilling rig can cost tens of millions of dollars, with super-spec rigs easily exceeding $30 million. This immense financial hurdle significantly deters new companies from entering the market and competing with established players like Helmerich & Payne.

Proprietary Technology and Know-how

Helmerich & Payne (H&P) benefits significantly from its proprietary technology and extensive operational know-how, built over many years in the industry. This deep expertise, particularly in areas like advanced drilling automation and rig management systems, represents a substantial hurdle for potential new entrants. For instance, H&P's investment in its flagship FlexRig technology, a highly automated and efficient drilling platform, showcases this advantage.

The complexity and capital intensity required to develop and implement similar advanced systems mean that new companies cannot easily replicate H&P's technological edge. This creates a formidable barrier, as new entrants would need to invest heavily and spend considerable time acquiring the necessary skills and patents to compete effectively. In 2024, H&P continued to refine these technologies, aiming to further enhance efficiency and reduce operational costs for its clients, solidifying its position against emerging competitors.

Regulatory Hurdles and Environmental Compliance

The oil and gas sector faces significant regulatory hurdles, particularly concerning environmental protection and safety. For instance, in 2024, the U.S. Environmental Protection Agency (EPA) continued to enforce strict methane emission standards for oil and gas facilities, requiring substantial investments in leak detection and repair technologies.

New companies entering the drilling services market must navigate a complex web of permits and compliance protocols, which can be both time-consuming and expensive. These requirements often necessitate specialized expertise and technology, acting as a substantial barrier to entry for smaller or less capitalized firms.

Compliance costs in 2024 remained a significant factor, with companies investing heavily in technologies and processes to meet evolving environmental regulations, such as those related to carbon capture and storage, further increasing the capital needed to enter the market.

Established Customer Relationships and Contracts

Helmerich & Payne's (HP) established customer relationships and contracts present a significant barrier to new entrants. Long-standing ties with major exploration and production (E&P) companies, coupled with the common practice of long-term drilling contracts, create a stable revenue stream and a distinct competitive advantage for incumbent players like HP.

New companies would find it exceedingly difficult to secure substantial contracts. This is primarily due to the requirement of a proven operational history, a modern and advanced drilling fleet, and the necessity of building trust and reliable relationships within the industry. For instance, in 2023, HP reported a significant portion of its revenue was derived from long-term contracts, underscoring the stickiness of these customer relationships.

- Customer Loyalty: Deep-rooted relationships with major E&P firms foster high customer loyalty, making it challenging for new entrants to displace established providers.

- Contractual Commitments: The prevalence of long-term contracts locks in existing customers, reducing the immediate market opportunity for newcomers.

- Track Record Requirement: New entrants must demonstrate a consistent, high-quality service record, which takes considerable time and investment to build.

Economies of Scale and Experience Curve

Existing large-scale contract drillers, like Helmerich & Payne (HP), leverage significant economies of scale. This advantage is evident in their fleet management, where optimized maintenance schedules and bulk purchasing of parts reduce per-unit costs. For instance, in 2023, HP reported a fleet utilization rate of 79%, showcasing efficient deployment of their assets, which directly contributes to lower operating expenses per rig compared to a smaller, less utilized fleet.

New entrants would face a substantial cost disadvantage. Building a comparable fleet and matching the operational efficiency gained through years of experience, often referred to as the experience curve, requires immense capital investment. This means a new player would likely incur higher costs for procurement, training, and initial operational setup, making it challenging to compete on price with established firms that have already amortized much of their initial investment and refined their processes.

- Economies of Scale: Large players benefit from lower per-unit costs in operations, maintenance, and procurement due to their size.

- Experience Curve: Established firms have learned to optimize processes over time, leading to greater efficiency and lower costs.

- Capital Intensity: Entering the contract drilling market requires significant upfront investment in rigs and infrastructure.

- Cost Disadvantage for Newcomers: New entrants must overcome the scale and experience advantages of incumbents to achieve cost parity.

Unpacking the Formidable Barriers to Entry in Contract Drilling

The threat of new entrants in the contract drilling sector, particularly for advanced rigs, is significantly mitigated by the immense capital required. A modern drilling rig can cost tens of millions of dollars, with super-spec rigs easily exceeding $30 million, creating a substantial financial barrier for newcomers. In 2024, the industry continued to see high capital expenditure needs for technological upgrades, further solidifying this barrier.

Helmerich & Payne's (HP) proprietary technology and extensive operational know-how, especially in areas like rig automation, represent a formidable hurdle. The company's investment in its FlexRig technology, for example, showcases this advantage, as replicating such advanced systems requires significant time and capital. By 2024, HP continued to refine these technologies, enhancing efficiency and reinforcing its competitive edge against potential entrants.

Stringent regulatory requirements, including environmental protection and safety standards, also act as a deterrent. In 2024, the EPA's continued enforcement of methane emission standards, for instance, necessitated substantial investments in compliance technologies. New companies must navigate complex permits and protocols, adding to the cost and time required to enter the market.

Established customer relationships and long-term contracts are critical barriers. New entrants struggle to secure significant contracts without a proven track record and modern fleet, which takes considerable time and investment to build. In 2023, HP reported a substantial portion of its revenue was derived from these long-term contracts, highlighting customer loyalty and contractual commitments as key advantages.

Economies of scale enjoyed by established players like HP, including optimized fleet management and bulk purchasing, create a significant cost disadvantage for new entrants. New companies face higher costs for procurement, training, and initial operations, making it difficult to compete on price with incumbents who have already amortized investments and refined processes.

| Barrier Type | Description | Impact on New Entrants | Example for HP |

|---|---|---|---|

| Capital Requirements | High cost of acquiring advanced drilling rigs. | Significant financial hurdle, limiting the number of potential entrants. | Super-spec rigs costing over $30 million. |

| Technology & Know-how | Proprietary automation and operational expertise. | Difficult to replicate, requiring substantial R&D and learning curves. | FlexRig technology and advanced rig management systems. |

| Regulatory Compliance | Navigating environmental and safety regulations. | Increases costs and time-to-market due to permits and specialized tech. | Meeting methane emission standards and investing in leak detection. |

| Customer Relationships & Contracts | Long-standing ties and long-term drilling agreements. | Reduces immediate market opportunities and requires building trust. | High percentage of revenue from long-term contracts in 2023. |

| Economies of Scale | Lower per-unit costs due to large fleet and operations. | New entrants face higher operating costs and a competitive price disadvantage. | Efficient fleet utilization (79% in 2023) leading to lower per-rig expenses. |

Porter's Five Forces Analysis Data Sources

Our Helmerich & Payne Porter's Five Forces analysis is built upon a foundation of publicly available company filings, including annual reports and SEC submissions. We supplement this with data from industry-specific market research reports and reputable financial news outlets to capture a comprehensive view of the competitive landscape.