First Financial Holding Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

First Financial Holding Bundle

Go Beyond the Preview—Access the Full Strategic Report

First Financial Holding operates within a dynamic financial services landscape, where understanding the interplay of competitive forces is paramount. Our analysis reveals the significant influence of buyer power and the constant threat of substitutes, shaping the company's strategic landscape.

The complete report reveals the real forces shaping First Financial Holding’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

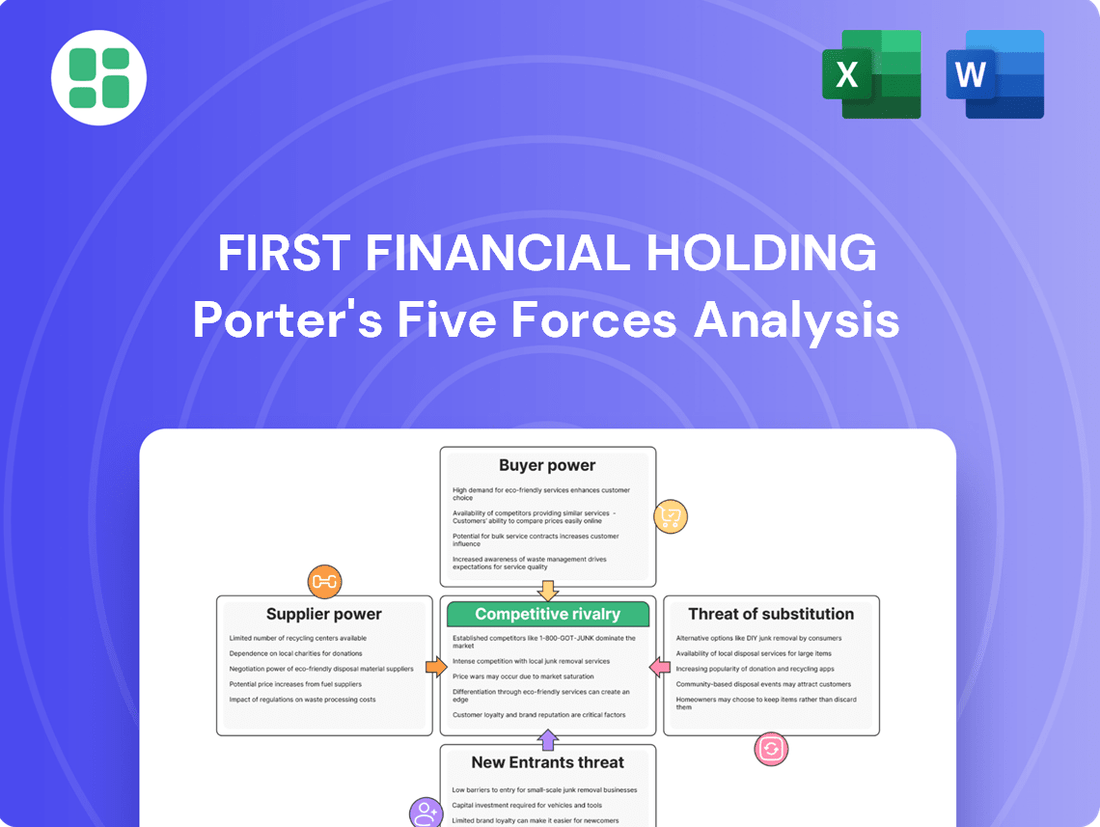

Suppliers Bargaining Power

Concentrated Technology Providers

First Financial Holding Company's reliance on specialized technology, from digital banking to cybersecurity, means a few key fintech providers hold considerable sway. These concentrated technology providers can exert significant bargaining power because switching to a new system is often costly and complex, disrupting critical operations. For instance, the global fintech market was valued at over $1.1 trillion in 2023, with a significant portion driven by core banking and digital transformation solutions, underscoring the dependence on a select group of innovators.

Skilled Labor and Talent Pool

The financial services sector, particularly with advancements in fintech and AI, heavily relies on specialized skills. This includes expertise in data science, cybersecurity, and financial product development.

In 2024, Taiwan's tech talent market, crucial for these areas, faced ongoing competition. For instance, demand for AI specialists outstripped supply, pushing average salaries for experienced AI engineers upwards by an estimated 15-20% year-on-year, significantly impacting recruitment costs for firms like First Financial Holding.

When a limited pool of highly sought-after talent exists, whether in Taiwan or globally, the bargaining power of these skilled employees intensifies. This translates directly into increased wage expectations and higher expenses associated with attracting and retaining top performers in critical roles.

Capital and Funding Sources

First Financial Holding, like other financial institutions, taps into a diverse range of capital and funding sources. While personal and corporate deposits in Taiwan offer a stable bedrock, the company also accesses broader financial markets. This reliance on external funding means that large institutional investors and international lenders can exert influence, potentially dictating terms, especially during periods of economic uncertainty or when evaluating First Financial's risk. For instance, in early 2024, global interest rate hikes influenced the cost of wholesale funding for many financial firms.

Information and Data Service Providers

Information and Data Service Providers wield considerable influence over First Financial Holding. Access to real-time market data, credit ratings, and financial intelligence is absolutely vital for First Financial's core businesses, including asset management, securities brokerage, and risk management.

These providers, often large global corporations, possess significant bargaining power. This strength stems from the unique, proprietary nature of their comprehensive databases and the substantial expense involved in duplicating such extensive information resources. For instance, Bloomberg terminals, a common tool in financial services, represent a significant recurring cost for firms.

- High Switching Costs: Migrating to alternative data providers can be complex and costly due to integration challenges and retraining needs.

- Proprietary Data: Many providers offer unique datasets or analytical tools that are difficult to replicate.

- Concentration: The market for financial data is often concentrated among a few dominant players, reducing competitive pressure.

- Essential Inputs: Reliable and timely data is not a luxury but a fundamental requirement for First Financial's operations and decision-making.

Regulatory Compliance and Legal Services

The financial sector in Taiwan is heavily regulated, requiring First Financial Holding to consistently allocate resources to legal and compliance professionals. This is crucial for navigating changes in regulations, like those concerning anti-money laundering (AML) or virtual asset service providers (VASPs). For instance, in 2024, the Financial Supervisory Commission (FSC) continued to refine AML regulations, impacting operational procedures.

Specialized legal firms and compliance software providers hold significant bargaining power. Their niche expertise is indispensable, and the financial penalties for non-compliance are substantial. In 2023, fines for regulatory breaches in Taiwan's financial sector reached hundreds of millions of New Taiwan Dollars, underscoring the importance of robust compliance.

- Regulatory Landscape: Taiwan's financial industry is subject to stringent oversight from bodies like the FSC, necessitating continuous adaptation to new rules.

- Compliance Costs: Investments in legal counsel and compliance technology are significant, driven by the need to avoid penalties and maintain operational integrity.

- Supplier Power: Specialized legal and compliance service providers leverage their expertise and the high cost of errors to command strong pricing power.

- Risk Mitigation: Effective navigation of regulations, supported by expert external services, is critical for First Financial Holding to mitigate operational and reputational risks.

Supplier Power: Driving Costs and Shaping Financial Services

Suppliers of specialized technology, critical talent, and essential data services can significantly impact First Financial Holding's costs and operational flexibility. The concentration of providers in areas like fintech solutions and financial data analytics, coupled with high switching costs, grants these suppliers considerable leverage. For instance, global fintech market growth, exceeding $1.1 trillion in 2023, highlights the dependence on a few key innovators.

The bargaining power of suppliers is amplified by the essential nature of their products or services and the difficulty in finding viable alternatives. In 2024, Taiwan's competitive tech talent market saw AI specialist salaries rise by an estimated 15-20%, directly increasing recruitment expenses for firms like First Financial Holding.

Furthermore, regulatory compliance necessitates reliance on specialized legal and compliance firms, whose expertise is indispensable. The substantial fines for non-compliance, which reached hundreds of millions of New Taiwan Dollars in 2023 for the sector, underscore the significant power these service providers hold.

| Supplier Category | Key Dependencies for First Financial | Supplier Bargaining Power Factors | 2024 Impact Example |

|---|---|---|---|

| Fintech & Technology Providers | Digital banking platforms, cybersecurity solutions | High switching costs, proprietary technology, market concentration | Increased costs for upgrading core banking systems |

| Specialized Talent | Data scientists, AI engineers, cybersecurity experts | Scarcity of skills, high demand, competitive salary environment | Wage inflation impacting recruitment and retention budgets |

| Financial Data & Information Services | Real-time market data, credit ratings, financial intelligence | Unique datasets, high cost of data replication, essential for operations | Recurring subscription fees for market data terminals |

| Legal & Compliance Services | Regulatory advice, AML/VASP expertise, compliance software | Niche expertise, high cost of non-compliance, regulatory complexity | Increased spending on legal counsel to navigate evolving regulations |

What is included in the product

This analysis dissects the competitive landscape for First Financial Holding, examining the intensity of rivalry, the power of buyers and suppliers, the threat of new entrants and substitutes, and the overall industry attractiveness.

Instantly identify and address competitive threats with a visual breakdown of First Financial Holding's market position, allowing for proactive strategy adjustments.

Customers Bargaining Power

Diverse Customer Segments

First Financial Holding's customer base is incredibly varied, encompassing individuals saving in banks, companies trading securities, individuals insured, and institutions managing assets. This wide array of client types means no single group can easily dictate terms.

While the sheer number of retail customers dilutes individual power, significant clients like major corporations or very wealthy individuals can exert more influence. For instance, a large corporate client depositing billions or utilizing extensive financial services might negotiate more favorable rates or terms due to the substantial business they represent.

Low Switching Costs for Basic Services

For basic banking products like deposits and standard loans in Taiwan, customers generally face low switching costs. This is particularly true as digital banking platforms simplify account opening and management. For instance, in 2023, the average time to open a new bank account digitally in Taiwan was reported to be under 10 minutes for many institutions, significantly reducing the friction for customers to move their funds.

Price Sensitivity and Transparency

In Taiwan's crowded financial services landscape, customers are keenly aware of prices, especially for straightforward products like basic savings accounts or standard loans. This heightened price sensitivity means they're more likely to switch providers for even small differences in fees or interest rates.

The rise of online platforms and comparison websites has significantly boosted transparency. For instance, by mid-2024, numerous financial comparison sites in Taiwan allowed consumers to easily see and contrast interest rates, fees, and product features across multiple banks and financial institutions. This accessibility empowers customers to negotiate better terms and makes it harder for First Financial Holding to maintain higher prices without justification.

Availability of Alternatives

Customers today have an expansive range of financial service providers available, far beyond just traditional banks. This includes numerous other financial holding companies, specialized standalone banks, member-owned credit unions, and a rapidly expanding ecosystem of fintech companies offering everything from digital payments to investment platforms.

The sheer volume of these alternatives, both within domestic markets and increasingly from international players, directly amplifies customer bargaining power. When a financial institution’s offerings are not competitive on price, service, or innovation, customers can readily switch to a substitute provider, making it easier for them to secure better terms or find solutions that better meet their specific needs.

For instance, in 2024, the global fintech market was projected to reach over $2.1 trillion, highlighting the significant growth and accessibility of alternative financial solutions. This robust competitive landscape means customers are less reliant on any single institution.

- Broad Choice: Customers can select from traditional banks, credit unions, and a growing number of fintech providers.

- Ease of Switching: Lower switching costs and readily available digital platforms facilitate easy movement between providers.

- Market Competition: The proliferation of financial technology and challenger banks intensifies competition, giving customers more leverage.

- Price Sensitivity: With many options, customers are more likely to compare fees, interest rates, and service charges, driving down margins for institutions.

Influence of Digital Platforms and Aggregators

The rise of digital platforms and financial aggregators significantly amplifies customer bargaining power. These tools offer unprecedented transparency, allowing consumers to easily compare pricing, features, and customer reviews across various financial institutions. For instance, in 2024, a significant portion of consumers actively used comparison websites before making financial decisions, driving down the cost of customer acquisition for banks and financial service providers.

This increased access to information directly combats information asymmetry, a traditional barrier that favored financial firms. Customers can now readily identify the best deals and switch providers with minimal friction, forcing companies to compete more aggressively on price and service quality. This shift means that First Financial Holding, like its peers, must continuously innovate and offer competitive terms to retain its customer base in a digitally-enabled marketplace.

- Digital Comparison Tools: Websites and apps allow easy comparison of financial products, increasing customer knowledge.

- Reduced Switching Costs: Online processes simplify moving between providers, enhancing customer leverage.

- Information Transparency: Digital platforms diminish information gaps, empowering informed customer choices.

- Competitive Pressure: Easy comparison forces companies to offer better value to attract and keep customers.

Customer Power: A Force in Financial Services

First Financial Holding faces moderate bargaining power from its customers. While individual retail customers have limited influence due to the sheer volume of clients, larger corporate or high-net-worth individuals can negotiate better terms. The ease of switching, especially with digital banking, and the increasing price sensitivity of Taiwanese consumers, driven by readily available comparison tools, further empower customers.

| Factor | Impact on First Financial Holding | Evidence/Data (2023-2024) |

|---|---|---|

| Customer Concentration | Low for retail, Moderate for large clients | Taiwan's banking sector has millions of retail customers, diluting individual power. However, large corporate deposits can represent significant portions of a bank's balance sheet. |

| Switching Costs | Low to Moderate | Digital account opening in Taiwan averaged under 10 minutes in 2023, reducing friction. |

| Price Sensitivity | High | Consumers actively use comparison sites for financial products, seeking better rates and lower fees. |

| Availability of Substitutes | High | The global fintech market, projected to exceed $2.1 trillion in 2024, offers numerous alternatives to traditional banking services. |

Preview the Actual Deliverable

First Financial Holding Porter's Five Forces Analysis

This preview showcases the complete Porter's Five Forces Analysis for First Financial Holding, offering an in-depth examination of competitive forces within its industry. The document you see here is the exact, professionally formatted analysis you will receive immediately upon purchase, ensuring no discrepancies or missing information. You can confidently expect to download this comprehensive strategic tool, ready for immediate application to your business insights.

Rivalry Among Competitors

Highly Fragmented Market

Taiwan's financial services sector is incredibly crowded, with over 400 financial institutions catering to a population of roughly 23 million. This high density means the market is highly fragmented, intensifying competition for every customer and every dollar across all financial product lines.

This intense fragmentation directly fuels aggressive competition among banks, insurance companies, and securities firms. They are constantly vying for market share, often through aggressive pricing, innovative product offerings, and extensive marketing campaigns to stand out in a saturated landscape.

Pressure on Profit Margins

Intense competition in the banking sector, especially in Taiwan, has historically compressed First Financial Holding's net interest margins, pushing them to some of the lowest in Asia. For instance, in Q1 2024, the average net interest margin for Taiwanese banks hovered around 1.1%, a figure that directly impacts profitability.

This persistent pressure compels First Financial and its competitors to aggressively pursue operational efficiencies and develop unique service offerings to stand out. The need to innovate and cut costs becomes paramount when core revenue streams are under such strain.

Diversification and Cross-Selling Strategies

First Financial Holding actively combats competitive rivalry by broadening its financial services beyond traditional banking. In 2024, the company continued to expand its securities, insurance, and asset management arms to capture a larger share of the market and reduce reliance on core banking revenues. This diversification aims to create significant synergies across its various subsidiaries, allowing for more effective cross-selling of products and services to a wider customer base.

Rapid Digital Transformation and Innovation

The financial services landscape is intensely competitive, with digital transformation and innovation acting as major catalysts. Companies are pouring resources into fintech, artificial intelligence, and big data analytics. This investment aims to streamline operations, enhance customer interactions, and pioneer novel payment solutions. For instance, in 2024, global investment in fintech was projected to reach over $150 billion, highlighting the scale of this digital race.

First Financial Holding's strategic emphasis on fintech development and fostering API partnerships directly addresses this dynamic. By embracing these technologies, the company seeks to stay ahead of rivals who are also leveraging digital advancements to gain market share. This approach is crucial for maintaining relevance and offering competitive services in an evolving market.

- Digital Investment Surge: Global fintech investment is a key indicator of competitive intensity, with significant growth anticipated through 2025.

- AI and Big Data Adoption: Financial institutions are increasingly using AI and big data to personalize services and improve operational efficiency.

- API Economy Growth: Open banking initiatives and API partnerships are creating new avenues for collaboration and competition among financial players.

- First Financial's Strategy: The company's focus on fintech and APIs positions it to compete effectively in this digitally driven environment.

Regulatory Efforts and Consolidation Trends

Taiwan's financial sector has seen persistent regulatory efforts aimed at fostering banking consolidation to mitigate market overcrowding, yet actual progress has been gradual. For instance, while the Financial Supervisory Commission (FSC) has encouraged mergers, the number of operating banks remained substantial through 2024, reflecting the slow pace of consolidation.

Recent regulatory adjustments, including the push for an Asian Asset Management Center, signal a drive to bolster the industry's global competitiveness. However, the Taiwanese banking landscape continues to be characterized by high saturation. The introduction of digital-only banks in recent years, such as LINE Bank and Rakuten Bank, has further intensified this competition, potentially fragmenting market share.

- Regulatory Push for Consolidation: Taiwanese authorities have long advocated for fewer, larger financial institutions to improve efficiency and stability.

- Slow Consolidation Pace: Despite these efforts, the number of banks operating in Taiwan has remained high, indicating a slow realization of consolidation goals.

- Market Saturation Persists: The market is still considered overbanked, with numerous players vying for a limited customer base.

- Digital Banks Increase Competition: The emergence of digital-only banks in 2024 has introduced new competitive dynamics, challenging traditional players.

Digital Race Heats Up Taiwan's Crowded Financial Landscape

The competitive rivalry within Taiwan's financial sector is exceptionally fierce due to market saturation and a high density of institutions. This intense fragmentation forces players like First Financial Holding to constantly innovate and manage costs to maintain profitability, as evidenced by compressed net interest margins. The ongoing digital transformation, with significant global fintech investments projected to exceed $150 billion in 2024, further escalates this rivalry, compelling firms to adopt AI and big data solutions.

Despite regulatory encouragement for consolidation, the Taiwanese banking market remains crowded, with new digital-only banks like LINE Bank and Rakuten Bank entering the fray in 2024, intensifying competition. First Financial's strategy of diversifying into securities, insurance, and asset management, alongside its focus on fintech and API partnerships, is a direct response to this challenging environment, aiming to capture broader market share and enhance customer offerings.

| Metric | Value (Q1 2024) | Trend/Implication |

| Number of Financial Institutions in Taiwan | Over 400 | High market fragmentation, intense competition. |

| Average Net Interest Margin (Taiwanese Banks) | ~1.1% | Compressed profitability, pressure for efficiency. |

| Projected Global Fintech Investment (2024) | >$150 billion | Accelerated digital race, need for technological adoption. |

SSubstitutes Threaten

Fintech Solutions and Digital Payments

The threat of substitutes for traditional banking services, like those offered by First Financial Holding, is substantial and growing, primarily driven by the fintech revolution. Digital payment platforms, peer-to-peer lending services, and online investment and advisory platforms provide increasingly convenient and often lower-cost alternatives for consumers and businesses. These fintech solutions allow users to manage transactions, access credit, and invest without necessarily engaging with established financial institutions.

Taiwan's proactive stance in promoting electronic and mobile payments further amplifies this threat. The Financial Supervisory Commission (FSC) has been actively encouraging the adoption of these technologies. For instance, by the end of 2023, the total value of electronic payments in Taiwan had already surpassed NT$3 trillion, indicating a significant shift in consumer behavior away from traditional cash and card transactions, directly impacting the transaction-based revenue streams of banks.

Cryptocurrencies and Virtual Assets

Cryptocurrencies and virtual assets are emerging as potential substitutes for traditional financial services, though regulatory frameworks in Taiwan are still developing. As of early 2024, global cryptocurrency market capitalization has seen significant fluctuations, with major coins like Bitcoin and Ethereum demonstrating volatility but also continued investor interest, suggesting a growing, albeit nascent, alternative for wealth storage and transfer.

Direct Investment and Crowdfunding Platforms

The rise of direct investment and crowdfunding platforms poses a significant threat of substitution for traditional financial institutions like First Financial Holding. These platforms, particularly popular with younger demographics and small businesses, offer a more accessible and often cheaper route for capital raising and investment compared to conventional brokerages and banks. For instance, by mid-2024, crowdfunding platforms facilitated billions in funding for startups and small enterprises, demonstrating their growing appeal as a viable alternative to traditional bank loans and equity offerings.

In-house Corporate Finance Departments

For large corporations, robust in-house finance departments can act as a significant substitute for external financial services. These departments often manage treasury functions, foreign exchange operations, and even certain capital raising activities internally, diminishing the need to engage with institutions like First Financial Holding for these services. This internal capability directly impacts the demand for First Financial's corporate banking offerings.

The trend towards professionalizing internal finance functions is notable. In 2024, a survey indicated that over 60% of Fortune 500 companies have dedicated treasury departments capable of managing complex financial instruments and international transactions. This internal capacity reduces their reliance on external banks for services such as hedging currency risk or managing liquidity. Consequently, First Financial Holding faces a reduced market for these specific corporate banking products.

- Internal Treasury Management: Large firms increasingly handle their own cash management, optimizing working capital without external banking support.

- In-house Capital Markets Expertise: Sophisticated finance teams can structure and execute certain debt or equity issuances, bypassing traditional investment banking roles.

- FX and Hedging Capabilities: Many corporations now possess the internal expertise and systems to manage foreign exchange exposure and execute hedging strategies.

- Reduced Outsourcing: The growing self-sufficiency of corporate finance departments directly substitutes for services traditionally offered by financial institutions.

Non-Financial Service Providers Offering Financial Products

Large technology companies and e-commerce platforms are increasingly embedding financial services directly into their offerings. For instance, companies like Amazon and Apple now provide payment solutions and consumer credit, acting as direct substitutes for traditional banking services. This trend is amplified by their massive existing customer bases and sophisticated data analytics capabilities, allowing them to offer highly personalized and convenient financial products.

These non-traditional providers can significantly disrupt the financial services landscape by leveraging their technological infrastructure and customer loyalty. By integrating financial products seamlessly, they lower the switching costs for consumers and create a more convenient user experience. For example, in 2023, the global embedded finance market was valued at over $6.4 trillion, showcasing the substantial growth and adoption of these substitute offerings.

- Embedded Payments: Tech giants offer payment processing and digital wallets, bypassing traditional card networks and banks.

- Consumer Credit: Companies provide point-of-sale financing and buy-now-pay-later options, competing with bank loans and credit cards.

- Insurance Products: E-commerce platforms are beginning to offer insurance directly at the point of purchase, substituting for traditional insurance brokers.

- Data Leverage: Access to vast customer data allows for more targeted and competitive product development, a key advantage over many incumbent financial institutions.

Financial Substitutes: A Growing Threat to Traditional Banking

The threat of substitutes for First Financial Holding is significant, stemming from fintech innovations and evolving consumer preferences. Digital payment systems and peer-to-peer lending platforms offer convenient, often cheaper alternatives to traditional banking. Taiwan's push for electronic payments, with transactions exceeding NT$3 trillion by the end of 2023, highlights this shift.

Emerging digital assets like cryptocurrencies also present a nascent but growing substitute for wealth storage and transfer, despite regulatory uncertainties. Furthermore, direct investment and crowdfunding platforms are increasingly drawing in both individuals and businesses seeking capital, bypassing conventional financial intermediaries.

Large corporations are also reducing their reliance on external financial services by building robust in-house treasury and capital markets expertise. By mid-2024, a substantial portion of major companies managed their own complex financial operations, including FX and hedging, directly impacting the demand for corporate banking products from institutions like First Financial Holding.

Tech giants embedding financial services into their platforms, such as payment solutions and consumer credit, pose another formidable substitute. The global embedded finance market, valued at over $6.4 trillion in 2023, underscores the rapid adoption of these integrated offerings, leveraging customer loyalty and data analytics.

Entrants Threaten

High Capital Requirements

Entering the traditional financial services sector, like banking and insurance, demands immense capital. For instance, in 2024, the average minimum capital requirement for a new national bank in the United States can range from tens of millions to hundreds of millions of dollars, depending on the charter type and state regulations. This substantial financial hurdle significantly deters many potential new players.

Stringent Regulatory Hurdles and Licensing

The financial services industry in Taiwan, including entities like First Financial Holding, faces significant barriers to entry due to rigorous regulatory oversight. The Financial Supervisory Commission (FSC) and the Central Bank mandate complex licensing procedures and ongoing compliance, making it challenging for new players to establish themselves. For instance, in 2023, the FSC continued to emphasize robust capital adequacy ratios and stringent risk management frameworks for all financial institutions, effectively raising the bar for any prospective entrants.

Established Brand Loyalty and Trust

Established brand loyalty and trust present a significant barrier to new entrants in the financial services sector. Existing institutions like First Financial Holding have cultivated decades of customer confidence, often reinforced by extensive physical branch networks and a long history of reliable service. For instance, in 2023, traditional banks continued to hold a substantial share of customer deposits, demonstrating the enduring appeal of established brands for core financial needs.

Digital-Only Banks and Fintech Startups

The threat of new entrants in Taiwan's financial sector, particularly concerning digital-only banks and fintech startups, is a significant consideration. While traditional banking faces substantial regulatory barriers, the Financial Supervisory Commission (FSC) has actively fostered an environment conducive to digital innovation. This includes the approval of digital-only banks and a general encouragement of fintech solutions, which has, in effect, lowered the entry threshold for digitally-native competitors.

These emerging players often possess a distinct advantage by operating without the encumbrance of legacy infrastructure. This allows them to be more agile and competitive, particularly in areas like cost structure, customer convenience, and the development of specialized digital financial products and services. For instance, by mid-2024, several digital banks in Taiwan had reported substantial user growth, indicating a strong market appetite for their offerings.

- Regulatory Facilitation: The FSC's proactive stance on digital banking and fintech has created pathways for new, digitally-focused financial institutions.

- Cost and Convenience Advantages: New entrants, unburdened by physical branch networks, can offer more competitive pricing and streamlined digital experiences.

- Specialized Digital Offerings: Fintech startups often excel at providing niche financial services through advanced technology, attracting specific customer segments.

- Market Traction: By early 2024, digital banks in Taiwan were demonstrating significant customer acquisition, validating the market's openness to these new models.

Access to Distribution Channels and Networks

New entrants face significant hurdles in accessing established distribution channels. First Financial Holding, like many established financial institutions, benefits from a robust network of physical branches and a widespread ATM presence, which are crucial for customer acquisition and service delivery in many markets. For example, as of the end of 2023, major banks in the US operated tens of thousands of branches, a physical footprint that is difficult and expensive for newcomers to replicate.

Building a comparable reach requires substantial capital investment in infrastructure or strategic alliances with existing players, both of which can be time-consuming and financially demanding. In 2024, the cost of establishing a new bank branch can range from several hundred thousand to over a million dollars, not including ongoing operational expenses. This high barrier to entry limits the number of new competitors that can effectively challenge incumbents like First Financial Holding.

The reliance on partnerships can also introduce complexities and costs, potentially diminishing the profit margins for new entrants. Furthermore, existing players often have exclusive agreements or preferential terms with third-party distributors, further restricting access for those trying to enter the market.

- Established Infrastructure: Incumbents possess extensive physical branch networks and ATM accessibility, critical for customer reach.

- High Investment Costs: New entrants need significant capital to build comparable distribution or secure costly partnerships.

- Partnership Dependencies: Reliance on third-party channels can be expensive and time-consuming, impacting profitability.

- Exclusive Agreements: Existing players may hold preferential terms with distributors, blocking new entrants.

Taiwan's Digital Banking Surge Reshapes Financial Competition

While traditional financial services face high capital and regulatory barriers, the threat of new entrants in Taiwan's financial sector is amplified by the rise of digital-only banks and fintech startups. The Financial Supervisory Commission (FSC) has actively encouraged these innovations, lowering entry barriers for digitally-native competitors.

These new players leverage agility and lower costs, offering specialized digital products and attracting customers with convenience. By mid-2024, several digital banks in Taiwan reported substantial user growth, indicating a strong market appetite for their offerings, thus presenting a dynamic competitive landscape for established institutions like First Financial Holding.

| Factor | Impact on New Entrants | Example (2023-2024 Data) |

| Capital Requirements | High barrier for traditional banking | US national bank minimums: $10M - $100M+ |

| Regulatory Compliance | Complex licensing and ongoing oversight | Taiwan FSC: Emphasis on capital adequacy & risk management |

| Brand Loyalty & Trust | Established players have decades of customer confidence | Traditional banks retain significant deposit market share |

| Digital Innovation | Lowered entry for fintech and digital banks | Taiwan FSC fostering digital banking growth |

| Distribution Channels | Incumbents have extensive physical networks | US banks operate tens of thousands of branches |

Porter's Five Forces Analysis Data Sources

Our First Financial Holding Porter's Five Forces analysis is built upon a foundation of comprehensive data, including the company's annual reports, investor presentations, and public financial statements. We also incorporate industry-specific research from reputable financial news outlets and market analysis firms to capture the broader competitive landscape.