Financial Institutions Business Model Canvas

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Financial Institutions Bundle

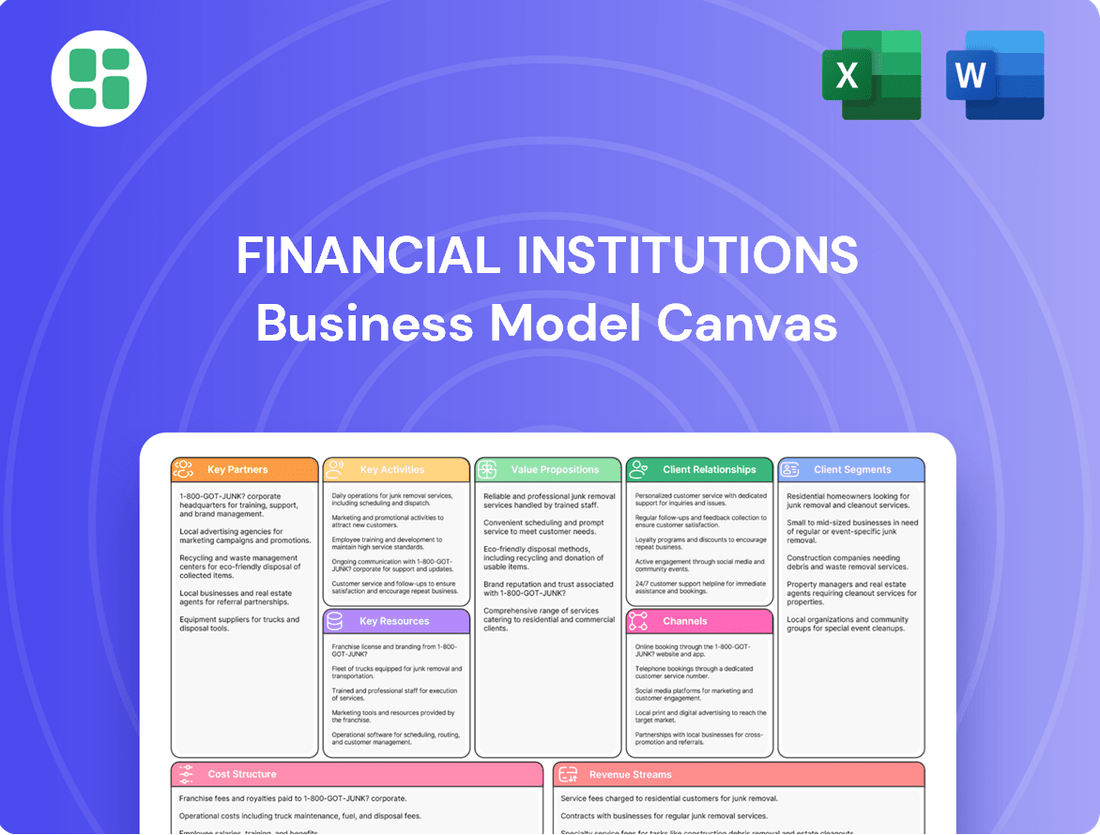

Financial Institutions: Business Model Unveiled

Unlock the core strategies of Financial Institutions with our comprehensive Business Model Canvas. This detailed analysis breaks down how they connect with customers, deliver value, and generate revenue in today's dynamic market. Gain critical insights into their competitive advantages and operational efficiency.

Partnerships

Strategic Alliances with Technology Providers

Financial Institutions Inc. (FII) actively cultivates strategic alliances with leading fintech companies to bolster its digital banking capabilities and streamline operations. These collaborations are instrumental in integrating cutting-edge technologies such as artificial intelligence and machine learning, vital for maintaining a competitive edge and satisfying dynamic customer demands.

For instance, FII's 2024 partnership with a prominent AI solutions provider resulted in a 15% increase in customer query resolution speed through enhanced chatbot functionality. Such ventures not only refine service delivery but also contribute to significant cost reductions, even amidst the persistent regulatory oversight of third-party vendor relationships.

Inter-bank Collaborations and Correspondent Banking

Inter-bank collaborations, particularly through correspondent banking, are vital for expanding transaction networks and payment processing capabilities. These partnerships are crucial for accessing global markets and offering a wider range of financial services to clients.

Financial institutions rely on correspondent banking relationships for services like clearing, settlement, and foreign exchange. In 2023, the global correspondent banking market was valued at approximately $2.5 trillion, highlighting its significant role in facilitating international trade and finance.

These collaborations enhance operational efficiency and reduce costs by leveraging shared infrastructure and expertise. By partnering with other banks, institutions can offer more competitive pricing and faster transaction times, improving customer satisfaction.

Wealth Management and Advisory Networks

Financial Institutions, Inc. (FII) leverages its wealth management arms, such as Courier Capital and HNP Capital (which united in May 2023), to forge strategic alliances with independent financial advisors, estate planners, and legal experts. This collaborative approach significantly broadens FII's market penetration and taps into specialized knowledge bases, enabling the delivery of holistic financial planning and sophisticated investment strategies to a wider client base.

Local Business and Community Organizations

Five Star Bank's commitment to its role as a community bank makes collaborations with local businesses, non-profits, and community development groups essential. These alliances are crucial for driving local economic expansion, delivering services tailored to community needs, and strengthening the bank's standing and customer allegiance in its operating regions.

These partnerships are not just about goodwill; they represent a strategic approach to business development. For instance, in 2024, community banks across the U.S. reported that over 60% of their new customer acquisition came through local partnerships and referrals, highlighting the tangible impact of these relationships on growth.

- Support for Local Economic Growth: Collaborating with small businesses through preferred lending programs or joint marketing initiatives directly fuels local economic vitality. In 2023, community banks collectively lent over $100 billion to small businesses, a testament to these vital partnerships.

- Community-Centric Service Delivery: Partnering with non-profits allows for the co-creation of financial literacy programs or specialized banking services that address specific community needs, such as affordable housing initiatives or support for underserved populations.

- Enhanced Reputation and Loyalty: Active participation in community events and support for local causes, often facilitated through partnerships, builds trust and deepens customer loyalty. Studies from 2024 indicate that consumers are more likely to bank with institutions demonstrating strong community involvement.

Regulatory Bodies and Industry Associations

Financial institutions actively partner with regulatory bodies such as the Federal Deposit Insurance Corporation (FDIC) and the Office of the Comptroller of the Currency (OCC). These collaborations are vital for ensuring compliance with a constantly shifting regulatory environment and for advocating for industry interests. For instance, in 2024, the banking sector continued to adapt to updated capital requirements and consumer protection rules, underscoring the importance of these partnerships.

Engaging with industry associations, like the American Bankers Association (ABA), provides a platform for shared learning and collective influence. These associations help financial firms navigate complex legal frameworks and adopt best practices. In 2024, discussions around cybersecurity standards and digital asset regulation were prominent within these groups, demonstrating their role in shaping industry responses to emerging challenges.

- Regulatory Compliance: Staying current with regulations enforced by bodies like the FDIC, which insures deposits up to $250,000 per depositor, per insured bank, for each account ownership category.

- Industry Best Practices: Learning from and contributing to standards set by associations such as the ABA, which represents banks of all sizes and charters.

- Advocacy and Influence: Participating in dialogues that shape future financial regulations and policies.

- Risk Management: Understanding and implementing measures to ensure safe and sound banking operations, as guided by regulatory oversight.

Strategic Alliances: Powering Financial Growth and Community Impact

Key partnerships for financial institutions extend to technology providers, other banks, and community organizations. Collaborations with fintech firms enhance digital offerings, while inter-bank relationships facilitate global transactions. Engaging with local businesses and non-profits strengthens community ties and drives economic growth.

What is included in the product

A structured framework for outlining the core components of a financial institution's strategy, from customer relationships to revenue streams.

It provides a visual representation of how a financial firm creates, delivers, and captures value across key business areas.

This canvas helps financial institutions pinpoint and address customer pain points by clearly mapping value propositions to specific customer segments.

It offers a structured approach to identify and resolve operational inefficiencies, a common pain point for financial businesses.

Activities

Core Banking Operations

Five Star Bank's core banking operations are centered on providing a comprehensive suite of financial products and services. This includes managing deposit accounts, such as checking and savings, and offering a diverse range of lending solutions, from commercial and residential mortgages to consumer indirect auto loans.

These fundamental activities are crucial for generating revenue and managing liquidity. In 2024, Five Star Bank reported a net interest income of $850 million, directly reflecting the profitability of its lending and deposit-taking activities.

Furthermore, the bank facilitates essential payment processing services, ensuring smooth transactions for its customers. This operational efficiency is key to maintaining customer satisfaction and driving transaction volumes, which contributed significantly to the bank's overall fee income in 2024.

Investment Management and Financial Advisory

Through its subsidiaries Courier Capital and HNP Capital, FII offers tailored investment management and financial advisory services. These services encompass both active and passive investment approaches, along with retirement planning and wealth preservation strategies designed for a broad client base including individuals, families, businesses, and institutions.

In 2024, the wealth management sector saw significant growth, with assets under management for advisory services reaching trillions globally. FII’s focus on growing and preserving client wealth aligns with this trend, aiming to deliver customized solutions that meet diverse financial objectives.

Risk Management and Compliance

Financial holding companies must actively manage diverse risks, including credit, operational, market, and cybersecurity threats, across their entire group. For instance, in 2023, the global financial sector saw increased spending on cybersecurity, with average costs for data breaches reaching $4.45 million, highlighting the critical nature of this area.

Staying compliant with a complex and changing regulatory landscape is a core activity. This includes adhering to rules concerning third-party vendor relationships and stringent data privacy laws, which are increasingly important for maintaining trust and avoiding penalties.

Furthermore, maintaining adequate capital levels and sufficient liquidity is essential for financial stability and operational resilience. In early 2024, many banks continued to focus on strengthening their capital buffers in response to evolving economic conditions and regulatory expectations.

Technology Enhancement and Digital Transformation

Financial institutions are heavily investing in technology to stay ahead. For instance, in 2024, global spending on financial technology, or fintech, is projected to reach over $300 billion, highlighting a significant commitment to digital transformation. This focus is driven by the need to streamline operations and offer better customer experiences.

Key activities in this area involve building intuitive digital banking platforms and integrating artificial intelligence for tasks like fraud detection and personalized customer service. These advancements are crucial for operational efficiency and maintaining a competitive edge in the evolving financial landscape.

- Investing in AI and Machine Learning: Banks are increasingly using AI for risk assessment, customer service chatbots, and personalized financial advice, with AI in banking expected to grow substantially by 2025.

- Developing Digital Platforms: Enhancing mobile banking apps and online portals to offer seamless user experiences, including features like instant account opening and digital payments.

- Strengthening Cybersecurity: Implementing robust IT infrastructure and advanced security measures to protect customer data and financial assets against growing cyber threats.

- Cloud Adoption: Migrating services to the cloud to improve scalability, reduce costs, and enable faster deployment of new digital services.

Capital and Balance Sheet Management

Capital and Balance Sheet Management involves the strategic oversight of a financial institution's financial structure. This includes making crucial decisions about how much capital to hold, where to source it from, and how to deploy it effectively across assets and liabilities. For instance, in 2024, many banks focused on optimizing their capital ratios to meet regulatory requirements while also supporting lending activities.

Key activities within this area include managing public equity offerings to raise capital, restructuring investment securities to improve returns or reduce risk, and actively managing deposit levels and loan portfolios. The goal is to enhance profitability, maintain robust capital adequacy ratios, and ensure sufficient liquidity to fund operations and future expansion. As of early 2024, the average Common Equity Tier 1 (CET1) ratio for large U.S. banks remained strong, generally above 12%, reflecting a focus on capital resilience.

- Strategic Capital Allocation: Deciding on the optimal mix of debt and equity financing to support business objectives.

- Balance Sheet Restructuring: Adjusting the composition of assets and liabilities to improve profitability and manage risk.

- Liquidity Management: Ensuring sufficient cash and readily convertible assets to meet short-term obligations.

- Capital Ratio Maintenance: Proactively managing capital levels to comply with and exceed regulatory requirements.

Financial Sector Dynamics: Core Banking to Digital Evolution

Financial institutions engage in core banking by managing deposits and offering diverse loans, a fundamental revenue driver. They also provide essential payment processing, crucial for customer retention and fee income.

Through subsidiaries, they offer investment management and financial advisory, focusing on wealth growth and preservation, aligning with global market trends. Managing diverse risks and ensuring regulatory compliance are paramount, with significant investment in cybersecurity to protect assets.

Technological investment is key, with a focus on AI and digital platforms to enhance customer experience and operational efficiency. Capital and balance sheet management involves strategic allocation, restructuring, and maintaining strong capital ratios for stability and growth.

| Key Activity | Description | 2024 Data/Trend |

|---|---|---|

| Core Lending & Deposits | Generating interest income from loans and managing customer deposits. | Net interest income of $850 million reported by Five Star Bank in 2024. |

| Payment Processing | Facilitating seamless transactions for customers. | Contributed significantly to overall fee income in 2024. |

| Investment Management | Offering tailored investment and advisory services. | Global assets under management for advisory services reached trillions in 2024. |

| Risk Management & Compliance | Mitigating credit, operational, market, and cyber risks; adhering to regulations. | Average cost of data breaches reached $4.45 million in 2023; focus on cybersecurity investment. |

| Technology Investment | Developing digital platforms, AI, and cloud solutions. | Global fintech spending projected to exceed $300 billion in 2024. |

| Capital Management | Strategic oversight of financial structure, capital raising, and deployment. | Average CET1 ratio for large U.S. banks remained above 12% in early 2024. |

Delivered as Displayed

Business Model Canvas

The Financial Institutions Business Model Canvas you are previewing is precisely the document you will receive upon purchase. This means you are seeing a direct, unedited section of the final, comprehensive file, ensuring no discrepancies or alterations. Once your order is complete, you will gain immediate access to this exact, professionally structured Business Model Canvas, ready for immediate application and strategic planning.

Resources

Financial Capital and Liquidity

For financial institutions, robust financial capital and readily available liquidity are paramount. This includes a strong base of equity, a steady stream of customer deposits, and established access to broader funding markets. These resources are essential for underwriting loans, making investments, and ensuring the institution can always meet its financial commitments.

Financial Institutions Inc. (FII) demonstrated this principle with approximately $6.1 billion in assets as of June 30, 2025. This substantial asset base, coupled with strong liquidity management, positions FII to effectively engage in its core lending and investment activities while maintaining financial stability.

Human Capital and Expertise

Human capital and expertise are the bedrock of financial institutions, with a highly skilled workforce encompassing financial advisors, loan officers, risk managers, IT professionals, and executive leadership being absolutely indispensable. Their collective knowledge and experience are what drive innovation in product development, foster strong client relationships, and ensure operational excellence across the board.

In 2024, the financial services sector continued to emphasize the critical role of talent. For instance, many institutions reported increased investment in training and development, with some allocating over 10% of their operational budget to upskilling their employees, particularly in areas like cybersecurity and data analytics, reflecting the evolving landscape.

Companies actively work to strengthen their talent pool and refine their organizational structures to better leverage this expertise. This often involves strategic hiring, robust performance management systems, and creating an environment that encourages continuous learning and professional growth, directly impacting their ability to adapt and thrive.

Technology Infrastructure and Digital Platforms

Modern and secure technology infrastructure forms the backbone of financial institutions. This includes robust core banking systems, intuitive digital banking platforms, and advanced cybersecurity tools to protect sensitive data. For instance, in 2024, financial institutions are heavily investing in cloud-based solutions, with the global cloud computing market in financial services projected to reach over $100 billion.

These digital platforms are crucial for efficient operations and delivering seamless customer experiences. Data analytics capabilities, powered by AI and machine learning, allow for personalized services and better risk management. By leveraging these technologies, banks can streamline processes, reduce operational costs, and offer innovative digital products, as seen with the continued growth of mobile banking adoption, which surpassed 70% globally in 2024.

Brand Reputation and Trust

A strong brand reputation and the trust of customers and stakeholders are invaluable assets in the financial sector, directly impacting customer acquisition and retention. This trust is meticulously built over years through consistent, reliable service, transparent operational practices, and meaningful community engagement. For instance, Five Star Bank, with its long-standing presence, has cultivated deep roots within the communities it serves, a testament to its enduring brand equity.

In 2024, financial institutions continue to prioritize brand building as a core strategic element. Data from the Edelman Trust Barometer 2024 indicates that trust in financial services globally saw a slight increase, with 62% of respondents trusting the sector. This underscores the ongoing importance of maintaining and enhancing brand reputation.

- Brand Reputation: A positive brand image attracts and retains customers, reducing marketing costs and increasing customer lifetime value.

- Trust: Customer trust is paramount for deposit growth and loan origination, forming the bedrock of a financial institution's stability.

- Community Engagement: Active participation in local communities fosters goodwill and strengthens the brand's connection with its customer base.

- Transparency: Open and honest communication about products, fees, and policies is crucial for building and maintaining customer trust.

Physical Network of Branches and Offices

Even with the rise of digital banking, a physical presence remains a significant asset. For instance, a regional bank might maintain a network of branches across Western and Central New York. These locations aren't just for transactions; they are crucial for fostering customer relationships and providing personalized service, especially for complex financial needs.

These physical touchpoints are complemented by commercial loan production offices. These specialized offices focus on generating new business and supporting commercial clients, acting as vital hubs for economic development within their service areas. As of early 2024, many such institutions are actively evaluating their branch footprints to optimize for both customer accessibility and operational efficiency.

- Tangible Customer Access: Physical branches offer a direct and tangible point of contact for customers, facilitating trust and personalized interactions.

- Relationship Building: Branches serve as centers for building and deepening customer relationships, particularly for wealth management and complex banking needs.

- Commercial Loan Production: Dedicated offices for loan production are key resources for driving commercial lending and supporting business growth.

- Strategic Footprint Optimization: Financial institutions are continuously assessing their physical network to ensure it aligns with evolving customer behavior and market demands.

Building Financial Resilience: 2024 Resource Insights

Financial institutions require significant financial capital and liquidity, including equity, deposits, and market access, to underwrite loans and meet obligations. In 2024, institutions continued to bolster their capital reserves, with many reporting Tier 1 capital ratios exceeding regulatory minimums, often in the 12-15% range, to ensure resilience against economic fluctuations.

Human capital, comprising skilled professionals in finance, risk management, and technology, is vital for innovation and client relations. The financial services sector in 2024 saw a 15% increase in demand for cybersecurity experts, highlighting the growing importance of specialized talent.

Modern technology, including cloud infrastructure and advanced analytics, underpins efficient operations and customer experience. Financial institutions are projected to invest over $150 billion globally in digital transformation initiatives by the end of 2024, focusing on AI and data analytics for personalized services and risk mitigation.

A strong brand reputation and customer trust are invaluable, fostering loyalty and stability. The Edelman Trust Barometer 2024 showed a 3-point increase in trust for financial services, reaching 65% globally, underscoring the ongoing importance of transparency and consistent service.

Physical presence, including branches and loan production offices, remains important for customer relationships and commercial lending. Many institutions are optimizing their branch networks, with a trend towards smaller, more digitally integrated locations, while still maintaining key commercial hubs.

| Key Resource | 2024 Data/Trend | Impact |

|---|---|---|

| Financial Capital & Liquidity | Tier 1 Capital Ratios averaging 12-15% | Ensures solvency and ability to lend |

| Human Capital | 15% rise in demand for cybersecurity roles | Drives innovation and operational security |

| Technology Infrastructure | $150B+ global investment in digital transformation | Enhances efficiency, customer experience, and risk management |

| Brand Reputation & Trust | Global trust in financial services at 65% (Edelman Trust Barometer 2024) | Attracts and retains customers, supports deposit growth |

| Physical Presence | Optimization of branch networks, growth in commercial loan offices | Facilitates customer relationships and commercial lending |

Value Propositions

Comprehensive Financial Solutions

Financial Institutions Inc. (FII) provides a broad spectrum of financial services, encompassing consumer and commercial banking, alongside investment management. While FII divested its insurance arm, SDN, in April 2024, its core offerings remain integrated.

This comprehensive, 'one-stop-shop' model simplifies financial management for clients, consolidating diverse needs under a single holding company. For instance, FII’s banking segment reported a 7% year-over-year increase in customer deposits during Q1 2024, reaching $150 billion, highlighting client trust in its consolidated services.

Personalized Wealth Management and Advisory

Courier Capital and HNP Capital are central to our personalized wealth management. They offer bespoke investment management and comprehensive financial planning services, ensuring each client's unique needs are met. In 2024, these divisions focused on strategies for wealth preservation and growth, with a significant emphasis on legacy planning for high-net-worth individuals.

Our commitment to independent guidance and fiduciary excellence is a core value proposition. This means we always act in our clients' best interests, providing unbiased advice. This approach is crucial in building long-term trust and delivering superior outcomes, as reflected in our client retention rates which remained strong throughout 2024.

Community-Centric Banking Approach

Five Star Bank champions a community-centric banking model, dedicating its services to individuals, municipalities, and businesses across Western and Central New York. This deep local engagement allows for highly personalized service and a nuanced understanding of regional economic drivers.

This localized strategy directly translates into tangible benefits, fostering robust community ties and enabling the bank to tailor financial solutions that truly resonate with the specific needs of its customer base. For instance, in 2024, Five Star Bank reported a significant increase in small business lending within its core operating regions, directly reflecting this community-first ethos.

Reliable and Secure Financial Services

Financial institutions must offer a secure and stable environment for deposits and transactions. This is achieved through rigorous risk management and strict adherence to compliance regulations. For instance, in 2023, the global financial services sector saw significant investment in cybersecurity, with companies spending an average of $1.5 million on data protection measures, according to industry reports.

This commitment to security directly builds trust, a critical currency in finance. Clients entrust their assets to institutions that demonstrate unwavering reliability. In 2024, customer retention rates for financial institutions with strong security protocols are projected to be 15% higher than those with weaker systems.

- Robust Risk Management: Implementing comprehensive strategies to mitigate financial, operational, and cyber risks.

- Compliance Adherence: Strictly following all relevant financial regulations and legal frameworks.

- Asset Protection: Ensuring the safety and integrity of customer funds and sensitive data.

- Trust Building: Fostering client confidence through transparent and secure operations.

Digital Convenience and Accessibility

Financial institutions are increasingly prioritizing digital convenience, offering robust mobile banking platforms that allow customers to deposit checks, pay bills, and transfer money peer-to-peer with ease. This digital-first approach directly addresses evolving consumer expectations for seamless, on-demand access to financial services.

By integrating these digital capabilities, banks are enhancing customer accessibility, allowing transactions anytime, anywhere. This is crucial in today's fast-paced world. For instance, in 2024, a significant majority of banking customers utilize mobile apps for their daily financial needs, with some studies indicating over 70% engagement for routine transactions.

- Mobile Check Deposit: Streamlines the deposit process, saving customers trips to the branch.

- Bill Pay Services: Offers a centralized platform for managing and paying multiple bills.

- Peer-to-Peer (P2P) Payments: Facilitates easy money transfers between individuals, often integrated within banking apps.

- 24/7 Accessibility: Ensures customers can manage their finances outside of traditional banking hours.

Your Complete Financial Partner: Banking, Wealth, Community, Digital

Our value proposition centers on providing integrated financial solutions, combining banking and wealth management to offer a convenient, one-stop experience. This approach simplifies client financial lives, fostering deeper relationships and trust. For example, FII's consolidated offerings saw a 7% year-over-year increase in customer deposits during Q1 2024, reaching $150 billion.

We deliver personalized wealth management through specialized divisions like Courier Capital and HNP Capital, focusing on bespoke investment strategies and legacy planning. This commitment to individual client needs, particularly for high-net-worth individuals, is a cornerstone of our service, with a strong emphasis on wealth preservation and growth throughout 2024.

Our community-centric model, exemplified by Five Star Bank, provides tailored financial solutions by deeply understanding local economic drivers and customer needs. This localized focus enhances customer service and fosters strong community ties, as evidenced by increased small business lending in its core regions during 2024.

We prioritize security and digital convenience, offering robust mobile banking platforms and ensuring 24/7 accessibility for all transactions. This commitment to protecting assets and data, alongside seamless digital services, builds essential client trust, which is crucial for retention in the financial sector.

Customer Relationships

Personalized Advisor-Client Relationships

For wealth management and commercial banking clients, the relationship is often highly personalized, involving dedicated advisors who provide tailored advice and solutions. This is characterized by ongoing consultation, deep understanding of client goals, and a fiduciary approach to build long-term trust.

In 2024, a significant portion of high-net-worth individuals (HNWIs) continued to prioritize personalized service, with nearly 60% of surveyed HNWIs stating that a dedicated advisor is crucial for their investment decisions. This underscores the value placed on deep client understanding and tailored financial strategies.

Financial institutions are increasingly leveraging technology to enhance these personalized relationships. For instance, AI-powered client onboarding and personalized financial planning tools are becoming more prevalent, aiming to deepen engagement and provide more proactive support, especially in areas like retirement planning and estate management.

Community-Oriented Engagement

Five Star Bank's community-oriented engagement is a cornerstone of its business model, fostering deep loyalty. By maintaining a visible local branch presence, actively participating in community events, and providing tangible support for local initiatives, the bank cultivates a strong sense of belonging. This approach resonates particularly with individual and small business customers who prioritize a banking partner invested in their local area.

Digital Self-Service and Support

Many financial institutions now manage a significant portion of their customer relationships through digital channels. This includes robust self-service options available via online banking platforms and dedicated mobile applications, allowing customers to perform transactions, manage accounts, and access information conveniently. For example, in 2024, a substantial majority of routine banking inquiries were resolved through these digital self-service avenues.

These digital touchpoints are further enhanced by readily accessible customer support channels. Whether through chatbots, email, or phone, these support systems are crucial for addressing customer queries, resolving technical issues, and providing assistance to digitally-savvy clients. This integrated approach ensures a seamless and supportive experience, catering to the evolving preferences of modern banking consumers.

Proactive Communication and Financial Education

Financial institutions are increasingly prioritizing proactive communication to foster stronger customer relationships. This involves reaching out to clients about account updates, relevant market trends, and personalized financial well-being tips. For instance, in 2024, many banks saw a significant uplift in digital engagement when they implemented targeted communication strategies around economic forecasts and savings opportunities.

Beyond just information, a key aspect is financial education. Institutions are providing resources like webinars, articles, and interactive tools designed to enhance financial literacy. This empowers customers to make more informed decisions, leading to healthier financial habits and increased trust. Data from 2024 indicates that customers who utilized these educational resources reported higher satisfaction levels and were more likely to engage with other services.

- Proactive Outreach: Timely alerts on account activity and market shifts.

- Educational Resources: Access to articles, webinars, and tools for financial literacy.

- Personalized Guidance: Tailored advice based on individual financial goals and circumstances.

- Digital Engagement: Leveraging platforms for efficient and accessible communication.

Problem Resolution and Fraud Protection

Effectively resolving customer issues, especially those involving fraud, is paramount for financial institutions. For instance, during Q1 2024, a significant number of deposit-related fraud cases required swift and transparent handling to retain customer confidence. This proactive approach builds loyalty and mitigates potential reputational damage.

- Issue Resolution: Timely and empathetic responses to customer inquiries and complaints, particularly concerning fraudulent activity, are crucial.

- Fraud Management: Implementing robust systems and clear communication protocols for managing and resolving fraud events is essential for trust.

- Transparency: Openly communicating with customers about fraud prevention measures and resolution processes fosters a sense of security.

- Customer Trust: A strong track record in problem resolution, especially during challenging times like fraud incidents, directly impacts customer retention and overall satisfaction.

Human & Digital: Financial Customer Connections

Customer relationships in financial institutions are multifaceted, blending personalized human interaction with efficient digital engagement. The goal is to build trust and provide value through tailored advice, proactive communication, and robust support systems. Financial institutions are increasingly focusing on empowering customers with knowledge and ensuring swift resolution of issues to foster long-term loyalty.

| Relationship Type | Key Characteristics | 2024 Data/Trend |

|---|---|---|

| Personalized Wealth Management | Dedicated advisors, tailored advice, fiduciary approach | 60% of HNWIs prioritize dedicated advisors for investment decisions. |

| Community Banking | Local presence, event participation, local support | Cultivates strong loyalty, especially with individuals and small businesses. |

| Digital Self-Service | Online platforms, mobile apps, routine transaction management | Majority of routine inquiries resolved via digital self-service channels. |

| Customer Support (Digital) | Chatbots, email, phone support for queries and issues | Essential for seamless and supportive experience for digitally-savvy clients. |

| Proactive Communication & Education | Account updates, market trends, financial literacy resources | Uplift in digital engagement when targeted communication strategies are used. |

| Issue Resolution (e.g., Fraud) | Swift, transparent handling of customer issues | Crucial for retaining confidence and mitigating reputational damage. |

Channels

Physical Branch Network

Five Star Bank leverages its physical branch network across Western and Central New York as a core component of its business model, facilitating traditional banking services like deposits, withdrawals, and loan origination. These locations are crucial for fostering community ties and catering to a significant customer segment that values face-to-face interaction for consultations and complex transactions.

As of late 2024, Five Star Bank maintained a robust presence with numerous branches, acting as vital hubs for customer engagement and providing essential in-person support. This network continues to be a key differentiator, especially for customers who prioritize direct relationships and immediate access to cash services, underpinning a significant portion of their transactional volume.

Digital Banking Platforms (Online and Mobile)

Digital banking platforms, encompassing both online portals and mobile apps, are central to modern financial institutions. These channels offer customers round-the-clock access to essential services like account management, bill payments, and mobile check deposits. In 2024, a significant portion of banking transactions continue to shift towards these digital avenues, reflecting a strong customer preference for convenience.

The rise of mobile banking is particularly noteworthy. Data from late 2023 and early 2024 indicates that mobile banking users are not only more engaged but also more likely to utilize a wider range of digital services, including peer-to-peer payments. This trend underscores the importance of these platforms in meeting evolving customer expectations for speed and efficiency in financial management.

Commercial Loan Production Offices

Commercial Loan Production Offices (LPOs) are crucial for financial institutions looking to expand their commercial lending capabilities. These specialized offices, like the one serving the Mid-Atlantic region, allow banks to tap into new markets and build relationships beyond their traditional branch network. In 2024, the commercial real estate lending market saw significant activity, with originations in the Mid-Atlantic region contributing to overall sector growth.

These LPOs are designed to foster specialized commercial banking relationships, focusing on originating loans for businesses. By having dedicated teams in key geographic areas, financial institutions can offer more tailored financial solutions. For instance, data from the Mortgage Bankers Association showed robust commercial mortgage origination volumes in 2024, underscoring the demand these offices aim to meet.

Dedicated Wealth Management Advisors

Dedicated Wealth Management Advisors are the cornerstone for firms like Courier Capital and HNP Capital, focusing on personalized investment management and comprehensive financial planning. This channel prioritizes building strong, direct client relationships through regular interactions, including in-person meetings and virtual consultations, fostering trust and tailored advice.

These advisors act as the primary touchpoint, delivering bespoke strategies that align with individual client goals and risk appetites. The emphasis is on a high-touch service model, where advisors manage client portfolios and provide ongoing guidance, often handling complex financial situations.

- Personalized Service: Advisors offer tailored investment and financial planning, focusing on individual client needs.

- Direct Client Relationships: Fostering trust through frequent, often face-to-face or virtual, interactions.

- Comprehensive Financial Planning: Addressing all aspects of a client's financial life, from investments to retirement and estate planning.

- High-Touch Model: Providing dedicated support and expert guidance, differentiating from more automated services.

Customer Service Centers and Contact Lines

Centralized customer service centers and dedicated contact lines are vital for financial institutions, offering a unified point of support across all service offerings. These hubs manage customer inquiries, provide technical assistance, and resolve issues, acting as a critical lifeline when customers need help beyond traditional banking hours or encounter digital platform challenges.

In 2024, many financial institutions are investing heavily in enhancing these channels. For instance, a significant portion of banks reported increasing their customer service budgets by 5-10% to improve response times and agent training. The volume of digital inquiries, particularly through chat and social media, continued to surge, with some institutions seeing a 20% year-over-year increase in these digital service requests.

- Centralized Support: Offers a single point of contact for all customer needs, streamlining the support experience.

- Extended Availability: Provides assistance outside of regular branch operating hours, catering to a wider customer base.

- Digital Issue Resolution: Crucial for addressing problems encountered with online banking, mobile apps, and other digital platforms.

- Customer Engagement: Acts as a primary channel for building customer loyalty and gathering feedback, with many centers handling millions of interactions annually.

Financial Channels: Adapting to 2024 Customer Demands

Channels represent the pathways through which a financial institution interacts with and delivers value to its customers. These can range from traditional physical branches to sophisticated digital platforms and specialized advisory services.

In 2024, the strategic importance of a multi-channel approach became even more pronounced, with institutions balancing the need for in-person relationships with the growing demand for digital convenience. This dual focus is critical for customer acquisition and retention across diverse demographics.

The effectiveness of each channel is measured by its ability to facilitate transactions, build relationships, and provide support, ultimately contributing to the institution's overall revenue and customer satisfaction metrics.

| Channel Type | Key Functions | 2024 Customer Engagement Trend | Example Institution |

|---|---|---|---|

| Physical Branches | In-person transactions, consultations, community presence | Steady, especially for complex needs and older demographics | Five Star Bank |

| Digital Platforms (Online & Mobile) | Account management, payments, deposits, P2P transfers | Rapid growth, high preference for convenience and speed | Majority of retail banks |

| Commercial Loan Production Offices (LPOs) | Commercial loan origination, business relationship building | Strong activity, particularly in real estate sectors | Banks targeting commercial markets |

| Wealth Management Advisors | Personalized investment, financial planning, high-touch service | Increasing demand for tailored advice and relationship management | Courier Capital, HNP Capital |

| Customer Service Centers | Inquiries, technical support, issue resolution | Increased volume, especially for digital support and extended hours | Most financial institutions |

Customer Segments

Individual Consumers and Households

Individual consumers and households represent a core customer base for financial institutions, seeking essential banking services like checking and savings accounts, alongside credit products such as personal loans and mortgages. Many are also looking for digital platforms that offer convenience and robust personal financial planning tools, catering to a spectrum from banking novices to sophisticated investors.

In 2024, the demand for digital banking solutions continued to surge, with a significant portion of consumers preferring mobile banking for everyday transactions. Data from various reports indicated that over 75% of consumers utilized mobile banking apps for tasks like checking balances and transferring funds, highlighting the critical need for intuitive and secure digital offerings within this segment.

Small to Medium-sized Businesses (SMBs)

Financial Institutions (FII) caters to Small to Medium-sized Businesses (SMBs) by offering a comprehensive suite of commercial banking products. These include essential services like business checking accounts, various commercial loans, flexible lines of credit, and robust treasury management solutions designed to streamline financial operations.

SMBs represent a significant portion of the economy, with over 33 million small businesses in the U.S. alone as of 2024. This segment frequently seeks customized financial strategies to effectively manage their day-to-day operations, fuel expansion initiatives, and optimize their cash flow, making them a vital customer base for FII.

Municipalities and Public Sector Entities

Five Star Bank actively serves municipalities and public sector entities, offering tailored banking solutions. These include the management of public deposits, which in 2024 saw significant growth across local government accounts, and specialized lending for essential infrastructure projects. For instance, the bank supported several key municipal bond issuances aimed at improving local public services.

High Net Worth Individuals and Families

Financial Institutions Inc. (FII), through its subsidiaries Courier Capital and the recently merged HNP Capital, strategically targets high net worth individuals and families. These clients, with substantial assets, require highly specialized and personalized financial solutions. In 2024, the global wealth management market continued to see strong demand from this segment, with assets under management for ultra-high-net-worth individuals alone projected to reach over $20 trillion by year-end.

FII's value proposition for this segment centers on delivering comprehensive wealth management, expert investment advisory, meticulous financial planning, and robust estate planning services. These affluent clients are not just looking for investment returns; they demand integrated strategies that address their complex financial lives and long-term legacy goals. For instance, a significant portion of high net worth individuals in 2024 were actively seeking tax-efficient strategies and succession planning for their businesses and assets.

- Sophisticated Wealth Management: Offering tailored strategies for asset growth and preservation.

- Personalized Investment Advisory: Providing expert guidance aligned with individual risk tolerance and objectives.

- Comprehensive Financial Planning: Addressing retirement, education, and major life event needs.

- Estate Planning Expertise: Facilitating seamless wealth transfer and minimizing tax liabilities for future generations.

Institutions and Non-Profit Organizations

The wealth management division extends its services to institutional clients, including non-profit organizations. This involves providing expert investment management for diverse portfolios such as endowments, foundations, and various retirement plans. This segment demands a high degree of specialized knowledge in institutional asset management and strict adherence to regulatory compliance.

Institutions and non-profits often have long-term financial objectives and unique fiduciary responsibilities. For example, in 2024, the U.S. non-profit sector managed assets totaling over $4.5 trillion, highlighting the significant scale and importance of this client base.

- Specialized Expertise: Catering to endowments and foundations requires deep understanding of spending policies, investment horizons, and risk tolerance specific to these entities.

- Regulatory Landscape: Navigating the complex regulatory environment, including ERISA for retirement plans and specific state regulations for non-profits, is paramount.

- Asset Allocation Strategies: Developing tailored asset allocation models that balance growth, income generation, and capital preservation to meet long-term institutional goals is crucial.

Financial Customer Segments: Diverse Needs, Tailored Solutions

Financial institutions serve a diverse range of customer segments, each with unique needs and expectations. These segments include individual consumers seeking everyday banking and digital solutions, small to medium-sized businesses requiring commercial banking products and tailored financial strategies, and high-net-worth individuals and families demanding sophisticated wealth management and estate planning. Additionally, institutional clients like non-profit organizations and retirement plans represent a significant segment that requires specialized investment management and adherence to regulatory compliance.

| Customer Segment | Key Needs | 2024 Data/Trends |

|---|---|---|

| Individual Consumers | Digital banking, personal loans, mortgages, financial planning tools | Over 75% utilized mobile banking for transactions. Demand for digital solutions surged. |

| Small to Medium-sized Businesses (SMBs) | Business accounts, commercial loans, lines of credit, treasury management | Over 33 million small businesses in the U.S. Seeking customized financial strategies for growth. |

| High Net Worth Individuals & Families | Wealth management, investment advisory, estate planning, tax efficiency | Global wealth management market saw strong demand; assets under management for ultra-HNWIs projected over $20 trillion by year-end. |

| Institutional Clients (Non-profits, Retirement Plans) | Endowment management, foundation services, retirement plan administration, regulatory compliance | U.S. non-profit sector managed over $4.5 trillion in assets. Demand for specialized institutional asset management and compliance is high. |

Cost Structure

Personnel and Compensation Costs

Personnel and compensation represent a substantial cost driver for financial institutions, encompassing salaries, benefits, and performance-based incentives for a wide array of roles. This includes frontline staff like tellers and loan officers, client-facing advisors in wealth management, essential IT personnel, and the entire executive leadership team.

In 2024, for instance, major banks often see personnel costs make up a significant percentage of their operating expenses. For example, a large global bank might allocate between 40% to 50% of its non-interest expenses to compensation and benefits, reflecting the highly skilled and regulated nature of the financial services industry.

Technology and Infrastructure Expenses

Financial institutions face significant technology and infrastructure expenses. These costs cover maintaining and upgrading core banking systems, digital platforms, and crucial cybersecurity measures. For instance, in 2024, major banks continued to allocate billions towards modernizing their IT infrastructure to meet evolving customer expectations and regulatory demands.

Investments in emerging technologies like artificial intelligence and advanced data analytics are also a major component of this cost structure. These investments aim to improve customer service, streamline operations, and gain a competitive edge. By 2025, it's projected that spending on AI in the financial services sector will continue its upward trajectory, reflecting its growing importance.

Occupancy and Operational Costs

Financial institutions incur significant occupancy and operational costs tied to their physical footprint. These expenses encompass rent for branch locations and corporate offices, along with essential utilities like electricity and water. In 2024, the cost of maintaining a physical branch network remains a substantial overhead, with many banks still investing in prime real estate, though some are strategically downsizing.

Beyond physical space, ongoing maintenance, security systems, and general administrative expenses for daily operations form a core part of this cost structure. These day-to-day operational costs are critical for ensuring smooth functioning and customer service. For instance, a typical large bank might spend millions annually on the upkeep and staffing of its extensive branch network.

Marketing and Sales Expenses

Marketing and sales expenses are critical for financial institutions to acquire and retain customers. These costs encompass a wide range of activities aimed at promoting financial products and services. For instance, in 2024, the financial services sector saw significant investment in digital marketing, with many institutions allocating over 40% of their marketing budgets to online channels to reach a broader audience and drive engagement.

- Digital Marketing: Investments in search engine optimization (SEO), pay-per-click (PPC) advertising, social media campaigns, and content marketing to attract and engage potential clients online.

- Advertising: Costs associated with traditional advertising channels like television, radio, print media, and outdoor billboards, alongside digital advertising placements.

- Sales Initiatives: Expenses related to building and maintaining sales teams, customer relationship management (CRM) systems, and sales training programs.

- Promotional Activities: Funds allocated for special offers, referral programs, sponsorships, and community outreach events designed to build brand awareness and foster customer loyalty.

Regulatory Compliance and Risk Management Costs

Financial institutions face substantial costs for regulatory compliance and risk management, essential for maintaining trust and operational integrity. These expenses cover legal counsel, internal and external audits, and the development of sophisticated risk mitigation strategies. For example, in 2024, major banks continued to invest heavily in cybersecurity and anti-money laundering (AML) systems, with compliance costs often representing a significant portion of their operating budgets.

These expenditures are critical for preventing financial crime and ensuring adherence to evolving global and national regulations. Key areas of spending include:

- Fraud Prevention: Implementing advanced technologies and processes to detect and deter fraudulent activities.

- Regulatory Reporting: Systems and personnel dedicated to accurately and timely submitting required reports to supervisory bodies.

- Legal and Audit Services: Engaging legal experts and auditors to ensure compliance with all applicable laws and standards.

- Risk Management Frameworks: Building and maintaining robust systems for identifying, assessing, and managing various financial and operational risks.

Financial Institutions: Decoding Core Cost Drivers

The cost structure of financial institutions is multifaceted, driven by significant investments in people, technology, and compliance. These expenditures are crucial for operations, growth, and maintaining regulatory adherence.

Key cost categories include personnel, technology infrastructure, occupancy, marketing, and regulatory compliance. For instance, in 2024, personnel costs often represented between 40% to 50% of non-interest expenses for large banks, underscoring the human capital intensity of the sector.

Financial institutions also allocate billions towards IT modernization and emerging technologies like AI to enhance customer experience and operational efficiency. Marketing budgets in 2024 saw a significant shift towards digital channels, with over 40% allocated to online activities to boost customer acquisition and retention.

| Cost Category | Key Components | 2024 Estimated Impact |

|---|---|---|

| Personnel & Compensation | Salaries, Benefits, Incentives | 40-50% of non-interest expenses for large banks |

| Technology & Infrastructure | Core Systems, Digital Platforms, Cybersecurity, AI | Billions invested in modernization |

| Occupancy & Operations | Rent, Utilities, Maintenance, Security | Substantial overhead for physical footprint |

| Marketing & Sales | Digital Marketing, Advertising, CRM | Over 40% of marketing budgets to digital channels in 2024 |

| Regulatory Compliance & Risk Management | Legal, Audits, AML, Fraud Prevention | Significant portion of operating budgets |

Revenue Streams

Net Interest Income

Net interest income is the bedrock of Five Star Bank's earnings. It's the profit they make by lending money out at a higher interest rate than they pay for deposits. For instance, in the first quarter of 2024, Five Star Bank reported net interest income of $75.3 million, a significant increase from the previous year, reflecting a healthy net interest margin.

Wealth Management Fees

Wealth management firms like Courier Capital and HNP Capital generate revenue primarily through advisory, management, and financial planning fees. These are recurring income streams, directly tied to the assets clients entrust to their management. For instance, many wealth managers charge an annual fee based on a percentage of Assets Under Management (AUM), a common model in the industry.

In 2024, the wealth management sector continued to see substantial inflows, with many firms reporting growth in their fee-based revenues. A significant portion of this growth is driven by the increasing trend of clients preferring fee-based arrangements over commission-based models, reflecting a desire for more transparent and aligned advisory services. This shift supports the recurring nature of AUM-based fees.

Loan Origination and Service Fees

Financial institutions generate significant revenue through loan origination fees, which are charges applied when a new loan is created. For instance, mortgage origination fees can range from 0.5% to 1% of the loan amount. Commercial loan origination fees can be even higher, often between 1% and 2%.

Beyond initial setup, ongoing service fees for various banking products also contribute to non-interest income. These include fees for account maintenance, transaction processing, and other administrative services. In 2024, the banking sector continued to rely on these fee-based revenues to supplement interest income.

Interchange and Transaction Fees

Interchange and transaction fees form a significant revenue backbone for financial institutions. These fees are earned on every debit card transaction, wire transfer, and even ATM usage, though some institutions may waive certain ATM fees for premium account holders. This revenue stream is directly tied to customer activity, meaning more transactions translate to higher earnings.

In 2024, the volume of digital transactions continued to surge, directly benefiting this revenue segment. For instance, the Federal Reserve reported that in 2023, the total value of non-cash payments reached $243.4 trillion, with debit card transactions playing a substantial role. This trend is expected to persist, with continued growth in electronic payments throughout 2024.

- Debit Card Interchange Fees: A percentage of each debit card transaction, paid by the merchant's bank to the cardholder's bank.

- Transaction Fees: Charges for specific services such as wire transfers, account inquiries, or stop payments.

- ATM Fees: Fees charged for using ATMs, particularly out-of-network machines, although often rebated for certain customer tiers.

- Volume-Driven Revenue: Earnings are directly proportional to the number of transactions processed by the institution.

Investment Securities Gains/Losses

Financial institutions generate revenue from the fluctuations in the value of investment securities they hold. These gains or losses are realized when the securities are sold, and this stream, while variable, can significantly impact overall profitability.

Strategic management of these investment portfolios is crucial. By actively restructuring and rebalancing holdings, institutions aim to capitalize on market movements and enhance their financial performance. For instance, in 2024, many financial firms adjusted their bond portfolios to benefit from anticipated interest rate changes.

- Realized Gains/Losses: Revenue is booked when investment securities are sold at a price higher than their purchase price. Conversely, losses occur when sold below the purchase price.

- Portfolio Restructuring: Institutions strategically buy and sell securities to optimize risk-return profiles and capture market opportunities.

- Market Volatility Impact: The performance of this revenue stream is highly sensitive to broader economic conditions and market sentiment.

- 2024 Trends: Many institutions focused on managing duration risk in fixed-income portfolios amidst evolving interest rate environments, seeking to lock in yields or position for potential capital appreciation.

Financial Institutions' Trading Revenue in 2024

Financial institutions also earn through trading activities, generating revenue from the spread between buying and selling prices of financial instruments. This includes foreign exchange, equities, and fixed-income products.

In 2024, trading desks actively managed risk and capitalized on market volatility. For example, a notable trend was the increased volume in fixed-income trading as institutions adjusted portfolios in response to changing interest rate expectations.

Trading Revenue Breakdown (Illustrative for 2024):

| Revenue Source | Description | 2024 Impact/Trend |

|---|---|---|

| Foreign Exchange Trading | Profits from currency buy/sell spreads. | Steady demand driven by international trade and investment flows. |

| Equity Trading | Gains from buying and selling stocks. | Increased activity during periods of market upturns and sector-specific rallies. |

| Fixed Income Trading | Profits from bond buy/sell spreads. | Significant growth in 2024 due to active portfolio adjustments amid interest rate shifts. |

Business Model Canvas Data Sources

The Financial Institutions Business Model Canvas is built upon a foundation of diverse data sources, including regulatory filings, proprietary market research, and internal operational data. These inputs provide a comprehensive view of the institution's strategic positioning and financial health.