Diversified Energy Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Diversified Energy Bundle

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Diversified Energy faces moderate bargaining power from its suppliers, as the company relies on a diverse range of energy sources and equipment. However, the threat of new entrants is relatively low due to significant capital requirements and regulatory hurdles in the energy sector. This snapshot only scratches the surface.

Unlock the full Porter's Five Forces Analysis to explore Diversified Energy’s competitive dynamics, market pressures, and strategic advantages in detail, including a deeper look at buyer power and the threat of substitutes.

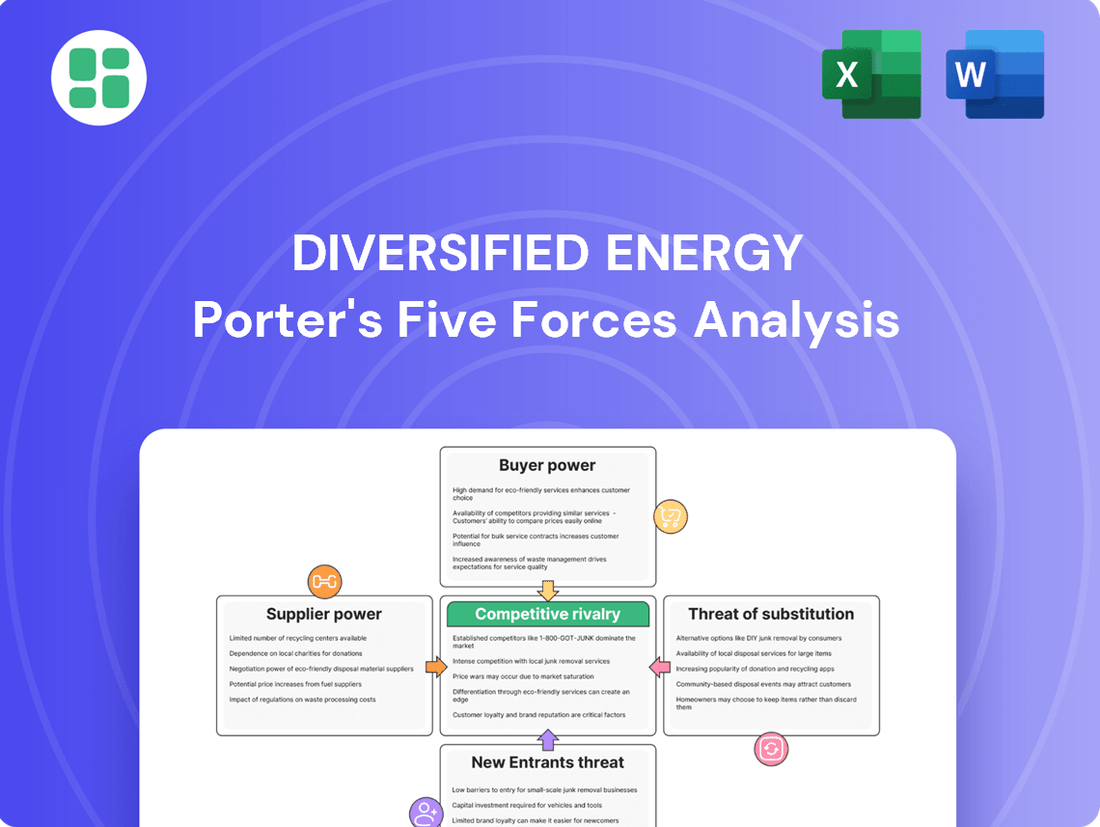

Suppliers Bargaining Power

Dependence on Specialized Oilfield Services and Equipment

Diversified Energy Company's reliance on specialized oilfield services for its operational efficiency, including well maintenance and upgrades, positions suppliers with significant bargaining power. The market for these essential services, encompassing drilling and well completion equipment, is seeing a trend towards consolidation and rapid technological evolution. This dynamic can directly translate into increased pricing leverage for key service providers.

The global oilfield equipment market is anticipated to expand, but specific to regions like the Appalachian Basin, the availability of highly specialized labor and proprietary technologies can empower certain service providers. This localized scarcity of unique expertise grants these suppliers considerable leverage when negotiating with operators such as Diversified Energy.

Commodity Price Impact on Supplier Costs

Suppliers in the energy sector often feel the pinch when oil and gas prices dip. For Diversified Energy, this can translate to suppliers needing to cut their own costs, which might mean less favorable contract terms for the company. For instance, during periods of low commodity prices, suppliers might be less willing to invest in new equipment or personnel, impacting their ability to service the industry efficiently.

Conversely, when commodity prices surge, like the observed recovery in natural gas prices heading into 2025, the situation often reverses. Higher prices boost activity and demand for services, giving suppliers more confidence and potentially strengthening their bargaining power. This increased demand can lead to suppliers commanding higher prices for their materials and services, directly impacting Diversified Energy's operational costs.

Limited Number of Niche Service Providers for Mature Assets

Diversified Energy's strategic focus on acquiring and optimizing mature, low-decline wells often necessitates specialized suppliers. This niche market can mean a limited number of service providers possessing the unique expertise and equipment required for such operations.

This scarcity of highly specialized suppliers, particularly those with proven track records in efficient operations and emissions reduction for mature assets, can translate to increased bargaining power for these providers. For instance, a supplier offering proprietary technology crucial for enhancing production from older wells or possessing highly experienced crews essential for regulatory compliance could command higher prices.

In 2023, Diversified Energy reported capital expenditures of $450 million, a significant portion of which would have been allocated to operational services. The reliance on a select group of these specialized suppliers for a substantial portion of these expenditures underscores their potential leverage.

Impact of Regulatory Compliance Costs on Suppliers

Suppliers to the energy sector, especially those focused on environmental services and well decommissioning, are navigating a landscape of escalating regulatory demands. For instance, in 2024, the U.S. Environmental Protection Agency (EPA) continued to enforce stricter methane emission regulations, impacting a wide range of upstream service providers.

The financial burden of meeting these evolving environmental standards, such as those related to orphaned well plugging and site remediation, can be substantial. These compliance costs often translate into higher prices for specialized services, which companies like Diversified Energy may have to absorb.

Consequently, this external pressure on suppliers can indirectly bolster their negotiating leverage. As suppliers invest more in technology and processes to adhere to stringent environmental protocols, their ability to dictate terms and pricing increases, potentially impacting Diversified Energy’s operational expenditures.

- Increased Environmental Scrutiny: In 2024, regulatory bodies globally intensified oversight on emissions and site restoration within the energy industry.

- Compliance Cost Pass-Through: Suppliers facing higher operational expenses due to new environmental mandates are likely to pass these costs onto their clients.

- Supplier Bargaining Power: The need for specialized, compliant services enhances the negotiating position of suppliers who can meet these stringent requirements.

Availability of Midstream and Transportation Infrastructure

Diversified Energy’s ability to get its natural gas and oil to market hinges on robust midstream and transportation infrastructure. While the company manages its own midstream and marketing, its reliance on third-party pipelines and services, particularly in regions facing limited takeaway capacity such as the Appalachian Basin, can significantly enhance the bargaining power of midstream operators.

For instance, in 2024, the Appalachian Basin continued to experience pipeline constraints, impacting transportation costs and availability for producers. This situation can force companies like Diversified to accept less favorable terms from pipeline companies.

- Midstream Reliance: Diversified Energy's operational success is directly tied to the availability and cost of transporting its produced hydrocarbons.

- Appalachian Constraints: Specific regions, like the Appalachian Basin, have historically faced takeaway capacity limitations, giving midstream providers leverage.

- Infrastructure Development: The ongoing construction of new pipelines and LNG export terminals is expected to ease these transportation bottlenecks over time, potentially reducing supplier bargaining power.

Suppliers & Midstream Hold Power Over Diversified Energy's Costs

Suppliers to Diversified Energy, particularly those providing specialized oilfield services and environmental compliance solutions, wield considerable bargaining power. This leverage stems from market consolidation, technological advancements, and the increasing stringency of environmental regulations, as seen with EPA methane emission standards in 2024. The limited availability of niche expertise, especially for optimizing mature assets and ensuring emissions reduction, further amplifies supplier influence, potentially leading to higher service costs for Diversified Energy.

The company's dependence on midstream infrastructure, particularly in regions with existing transportation constraints like the Appalachian Basin in 2024, also grants significant power to pipeline operators. As these operators are essential for market access, they can negotiate more favorable terms, especially when takeaway capacity is limited.

| Factor | Impact on Diversified Energy | Supporting Data/Trend (2024 Focus) |

| Specialized Services Demand | Increased supplier bargaining power due to niche expertise | Limited availability of proprietary technologies for mature wells |

| Environmental Regulations | Higher costs passed on by suppliers meeting compliance | Stricter EPA methane emission regulations impacting upstream providers |

| Midstream Capacity | Leverage for pipeline operators in constrained regions | Ongoing pipeline constraints in the Appalachian Basin affecting transport costs |

What is included in the product

This Porter's Five Forces analysis for Diversified Energy meticulously examines the competitive intensity within the energy sector, focusing on the bargaining power of buyers and suppliers, the threat of new entrants, the availability of substitutes, and the rivalry among existing players.

Instantly identify and mitigate competitive threats with a comprehensive overview of Diversified Energy's industry landscape.

Customers Bargaining Power

Large and Diverse Customer Base Reduces Individual Power

Diversified Energy's customer base, primarily composed of utility companies, industrial users, and marketers for its natural gas and oil production, is both large and highly fragmented. This broad distribution network means no single customer holds significant sway over pricing, as their individual demand is a small fraction of the total market. For instance, in 2024, Diversified Energy reported serving thousands of customers across its operations, underscoring this diversification.

Commodity Nature of Products and Price Sensitivity

The commodity nature of oil and natural gas means Diversified Energy's customers face little switching costs. This allows them to readily move to alternative suppliers if prices are more attractive, a key factor in their bargaining power.

Customers' high price sensitivity is amplified by the volatile energy markets. For instance, in early 2024, natural gas prices saw significant swings, driven by factors like colder-than-expected winters in some regions and global supply adjustments, directly impacting what customers are willing to pay.

This constant search for the best price puts considerable downward pressure on Diversified Energy's revenue per unit. In 2023, the average spot price for West Texas Intermediate (WTI) crude oil fluctuated, demonstrating the market's responsiveness to external factors and the leverage this gives to price-conscious buyers.

Increasing Demand for Natural Gas for Power Generation and Exports

The escalating demand for natural gas, fueled by power generation needs for data centers and AI growth, along with robust LNG exports, significantly bolsters Diversified Energy's market position. This surge in demand, with projections indicating record highs for natural gas consumption in 2025, directly translates to increased bargaining power for producers like Diversified Energy.

Long-Term Contracts and Hedging Strategies

Diversified Energy Company employs long-term contracts and sophisticated hedging strategies to manage its natural gas sales. These agreements, particularly those with major Gulf Coast LNG export facilities, lock in prices and volumes for extended periods. This approach significantly diminishes the bargaining power of customers by creating price and volume certainty.

These long-term fixed-price contracts are crucial for revenue stability and predictability, shielding Diversified Energy from the sharp swings often seen in commodity markets. For instance, in 2023, the company reported that approximately 70% of its natural gas production was hedged or covered by fixed-price contracts, providing a solid foundation for its financial performance.

- Revenue Stability: Long-term fixed-price contracts provide predictable revenue streams, reducing reliance on volatile spot market prices.

- Reduced Customer Power: By securing volumes and prices, Diversified Energy limits customers' ability to negotiate lower rates or switch suppliers.

- Commodity Price Protection: Hedging strategies, including swaps and options, mitigate the impact of extreme price fluctuations, ensuring consistent margins.

- Operational Certainty: These agreements allow for more reliable production planning and capital allocation, supporting consistent operational performance.

Geographic Concentration of Operations

Diversified Energy's operational footprint is heavily concentrated in the Appalachian Basin and the Central United States. This geographic focus, while enabling operational efficiencies, can potentially empower local customers by offering them more readily available alternative suppliers within those specific regions.

However, the bargaining power of customers is tempered by several factors. The continuous expansion of pipeline infrastructure is broadening the reach of Diversified Energy's supply. Furthermore, the growing demand for natural gas sourced from the Appalachian region, particularly for liquefied natural gas (LNG) exports, creates a wider market, thereby diluting the concentrated power of any single group of localized buyers.

- Geographic Concentration: Primarily Appalachian Basin and Central US.

- Potential Buyer Power: Localized alternatives may exist.

- Mitigating Factors: Expanding pipeline networks and increasing demand for Appalachian gas, including LNG exports.

Navigating Customer Power: Contracts, Hedging, and Market Strength

Diversified Energy's customers, primarily utilities and industrial users, possess moderate bargaining power due to the commodity nature of natural gas and oil, leading to low switching costs. However, this is significantly offset by the company's strategic use of long-term fixed-price contracts and hedging. For instance, in 2023, approximately 70% of Diversified Energy's natural gas production was hedged or under fixed-price agreements, providing revenue stability and limiting customers' ability to negotiate lower rates.

The company's broad customer base, serving thousands in 2024, prevents any single buyer from wielding significant influence. While geographic concentration in the Appalachian Basin could theoretically empower local buyers, expanding pipeline infrastructure and robust demand for Appalachian gas, especially for LNG exports, create a wider market. This increased demand, projected to reach record highs for natural gas consumption in 2025, further dilutes individual customer leverage.

| Factor | Impact on Customer Bargaining Power | Diversified Energy's Mitigation Strategy |

|---|---|---|

| Customer Base Size & Fragmentation | Low (Thousands of customers in 2024) | No single customer holds significant sway. |

| Switching Costs | Low (Commodity nature of products) | Long-term contracts and hedging lock in volumes and prices. |

| Price Sensitivity | High (Volatile energy markets) | Fixed-price contracts and hedging protect against price swings. |

| Geographic Concentration | Moderate (Appalachian Basin focus) | Expanding infrastructure and strong demand (e.g., LNG) broaden market reach. |

Full Version Awaits

Diversified Energy Porter's Five Forces Analysis

This preview showcases the comprehensive Porter's Five Forces analysis for Diversified Energy, detailing the competitive landscape and strategic implications. The document you are viewing is the exact, fully formatted report you will receive immediately after purchase, offering an in-depth examination of industry rivalry, buyer and supplier power, threat of new entrants, and substitute products. Rest assured, what you see is precisely what you will get—a ready-to-use strategic assessment for Diversified Energy.

Rivalry Among Competitors

Fragmented but Consolidating Industry Landscape

The U.S. onshore oil and gas sector, especially in established regions like Appalachia, features a multitude of independent producers, creating a fragmented market. This fragmentation means there are many players vying for attention and resources.

Despite the large number of companies, a clear trend towards consolidation is underway. Diversified Energy's strategic acquisitions, such as the purchase of Maverick Natural Resources, exemplify this movement. These deals are actively reducing the overall number of competitors in the industry.

As consolidation progresses, the rivalry among the remaining, larger entities intensifies. These dominant players compete more fiercely for market share and valuable upstream assets, driving a more concentrated competitive landscape.

Acquisition-Focused Business Models

Diversified Energy's competitive rivalry is shaped by its acquisition-focused model, where competition centers on securing mature, producing wells. This means companies vie for assets through bidding processes, emphasizing efficient integration and synergy realization. In 2023, Diversified Energy completed 14 acquisitions, adding approximately 1,500 wells to its portfolio, highlighting the active nature of this competitive landscape.

Commodity Pricing and Cost Efficiency

Diversified Energy, like many in the energy sector, faces intense competition due to the commodity nature of its products. This means companies are largely vying on price, making cost efficiency paramount for survival and profitability. In 2024, this pressure remains a significant factor as companies strive to maintain margins even when market prices fluctuate.

The company’s strategy of focusing on optimizing its existing asset base and realizing acquisition synergies directly tackles this rivalry. For instance, the cost savings achieved from the Maverick acquisition are a prime example of how Diversified aims to bolster its cost efficiency, a critical lever in this highly competitive landscape.

Access to Midstream Infrastructure and Export Markets

Competitive rivalry intensifies when companies have superior access to midstream infrastructure, such as pipelines, and to profitable export markets. Companies that can efficiently transport their products, especially to burgeoning liquefied natural gas (LNG) export terminals, secure a significant edge. For instance, in 2024, the expansion of LNG export capacity along the US Gulf Coast is a key driver, increasing demand for natural gas producers with direct pipeline connections.

Historically, pipeline capacity constraints, particularly in regions like Appalachia, have limited producer options. However, ongoing infrastructure projects in 2024 are enhancing takeaway capacity, thereby opening up wider markets and increasing the competition for access to these vital transportation networks. This improved access allows more producers to reach higher-value markets, thereby intensifying the competitive landscape.

- Improved Takeaway Capacity: In 2024, significant investments in new pipelines and expansions are boosting natural gas takeaway capacity from key producing regions, reducing historical bottlenecks.

- LNG Export Growth: The continued expansion of US LNG export facilities in 2024 is creating substantial demand for producers with direct pipeline access to these terminals, offering premium pricing.

- Market Access Competition: As infrastructure improves, competition for access to these enhanced transportation routes and lucrative export markets is becoming more pronounced among energy producers.

Environmental, Social, and Governance (ESG) Performance

Competitive rivalry increasingly extends to Environmental, Social, and Governance (ESG) performance, with a particular focus on methane emissions and well abandonment. Companies that excel in environmental stewardship, like Diversified Energy's proactive well retirement program, are better positioned to attract investors and navigate regulatory landscapes. This dimension introduces non-price competition, compelling firms to allocate resources towards sustainable operations and transparent reporting.

For instance, in 2024, the energy sector saw a notable increase in investor scrutiny regarding methane reduction targets. Companies with robust ESG strategies often report lower costs of capital and improved access to funding. Diversified Energy's commitment to retiring wells, a key ESG metric, directly addresses environmental liabilities and can enhance its long-term valuation.

- Methane Emissions: Stricter regulations and investor pressure are driving competition to reduce methane leaks.

- Well Abandonment: Companies are competing on the speed and environmental integrity of their well retirement programs.

- Investor Favor: Strong ESG performance, like Diversified Energy's, can attract capital and improve market perception.

- Non-Price Competition: Sustainability initiatives are becoming a critical differentiator beyond traditional cost and quality metrics.

Intensifying Energy Competition: Acquisitions & Infrastructure Edge

The competitive landscape for Diversified Energy is characterized by a large number of independent producers, particularly in established basins. This fragmentation leads to intense rivalry, often centered on acquiring mature, producing assets. While consolidation is reducing the overall number of players, the competition among the remaining, larger entities for market share and prime upstream assets is intensifying.

The commodity nature of oil and gas means price competition is a constant pressure, making cost efficiency crucial. Diversified Energy's strategy of optimizing existing assets and realizing acquisition synergies directly addresses this, aiming to bolster cost efficiency. In 2023, the company completed 14 acquisitions, adding approximately 1,500 wells, demonstrating the active pursuit of assets within this competitive environment.

Access to midstream infrastructure and export markets, especially LNG terminals, provides a significant competitive edge. In 2024, the expansion of US LNG export capacity heightens competition for producers with direct pipeline access. Improved takeaway capacity from regions like Appalachia in 2024 is also opening wider markets, increasing competition for access to these vital transportation networks.

| Metric | 2023 Data | 2024 Outlook/Trend |

|---|---|---|

| Number of Acquisitions by Diversified Energy | 14 | Continued focus on strategic acquisitions |

| Wells Added by Diversified Energy (2023) | ~1,500 | Expansion of portfolio through M&A |

| LNG Export Capacity Growth | Ongoing | Increased demand for pipeline-connected producers |

| Takeaway Capacity Improvements | Ongoing | Reduced bottlenecks, increased market access competition |

SSubstitutes Threaten

Growth of Renewable Energy Sources

The most significant long-term substitute for natural gas and oil is renewable energy, with solar and wind power leading the charge. In 2023, global renewable capacity additions reached a record high, exceeding 500 gigawatts, a substantial increase from previous years, signaling a robust growth trajectory.

While demand for natural gas continues to climb globally, particularly for power generation and industrial applications, the accelerating adoption of renewables presents a clear long-term threat. This rapid deployment is actively displacing fossil fuels in the energy sector, especially in electricity generation, which could lead to a future decline in natural gas demand.

Energy Efficiency and Conservation Measures

Improvements in energy efficiency and conservation are increasingly acting as a threat of substitutes for traditional energy sources like natural gas and oil. For instance, in 2024, the International Energy Agency (IEA) reported that energy efficiency measures saved the equivalent of over 2.3 billion tonnes of oil globally, a significant reduction in demand for fossil fuels.

While global energy demand is projected to grow, driven by sectors like artificial intelligence data centers, sustained efficiency gains can moderate this growth. In 2023, the IEA also noted that renewable energy sources, alongside efficiency, are expected to meet a substantial portion of this increased demand, further substituting for fossil fuels.

Coal and Nuclear Power as Alternatives for Electricity Generation

While natural gas has become a dominant force, coal remains a viable substitute for electricity generation, especially if gas prices surge. For instance, in 2023, coal still accounted for approximately 16% of U.S. electricity generation, demonstrating its persistent role.

Nuclear power presents another significant carbon-free alternative, offering a stable baseload power source. As of early 2024, nuclear energy provides about 19% of the United States' electricity, highlighting its importance in a diversified energy mix.

The competitive pricing and availability of coal and nuclear power directly impact the demand for natural gas, thus influencing Diversified Energy's market position and the attractiveness of its natural gas assets.

Electrification of Transportation and Industrial Processes

The growing adoption of electric vehicles (EVs) presents a significant substitute threat to Diversified Energy's core oil and natural gas products. By 2024, global EV sales are projected to exceed 15 million units, a substantial increase from previous years, directly reducing demand for gasoline and diesel fuel. This shift impacts not only transportation but also industrial processes increasingly powered by electricity instead of fossil fuels.

This trend poses a long-term challenge to Diversified Energy's revenue streams. As more consumers and industries embrace electrification, the demand for petroleum-based products will likely decline. For instance, the International Energy Agency (IEA) forecasts that EVs could displace over 6 million barrels per day of oil demand by 2030, a considerable portion of current consumption.

- EV Sales Growth: Global EV sales are expected to surpass 15 million units in 2024, indicating a strong substitution effect for gasoline and diesel.

- IEA Projections: The IEA estimates that EVs could reduce oil demand by more than 6 million barrels per day by 2030.

- Industrial Electrification: A broader move towards electric power in industrial operations further erodes the market for natural gas and other fossil fuels.

Development of Advanced Energy Storage Technologies

The ongoing development of advanced energy storage technologies, particularly large-scale batteries, is a significant threat of substitutes for traditional energy sources. These advancements improve the reliability and dispatchability of intermittent renewables like solar and wind. For instance, by mid-2024, the cost of lithium-ion battery packs for utility-scale applications had fallen by over 90% compared to a decade prior, making renewable energy more competitive. This enhanced capability allows renewables to better meet grid stability and peak demand requirements, directly challenging the role of natural gas-fired power plants.

As energy storage solutions mature and become more cost-effective, they increasingly enable renewable energy sources to act as viable substitutes for fossil fuels. This trend is particularly impactful in grid management, where previously the dispatchability of natural gas was a key advantage. By 2024, the installed capacity of grid-scale battery storage in the United States had surpassed 10 gigawatts, demonstrating a significant shift in the energy landscape and increasing the competitive pressure on conventional power generation.

The increasing viability of renewables, bolstered by energy storage, directly impacts the perception and utilization of natural gas as a bridge fuel. The ability of stored renewable energy to provide consistent power reduces the need for flexible natural gas plants to balance supply and demand. This dynamic suggests a diminishing long-term role for natural gas as the energy transition accelerates, with storage technologies playing a crucial part in this substitution.

- Advancement in Battery Technology: Significant cost reductions in battery technology, exceeding 90% for utility-scale lithium-ion packs by mid-2024, bolster renewable energy's competitiveness.

- Enhanced Grid Reliability: Energy storage improves the dispatchability of intermittent renewables, allowing them to more effectively compete with natural gas for grid stability and peak demand.

- Impact on Natural Gas: The growing effectiveness of renewables, supported by storage, challenges the role of natural gas as a bridge fuel, as renewables can increasingly fulfill its balancing functions.

- Growth in Storage Capacity: The US saw grid-scale battery storage capacity exceed 10 gigawatts by 2024, underscoring the rapid expansion and increasing threat of substitutes.

Renewables and Efficiency: The Growing Challenge to Natural Gas Demand

The threat of substitutes for natural gas is substantial, primarily driven by the accelerating growth of renewable energy sources like solar and wind. These alternatives are becoming increasingly cost-competitive and reliable. For instance, global renewable capacity additions reached a record high in 2023, exceeding 500 gigawatts, signaling a robust growth trajectory that directly challenges fossil fuel demand.

Energy efficiency measures also act as a significant substitute, directly reducing the overall demand for energy. In 2024, the International Energy Agency (IEA) reported that efficiency improvements saved the equivalent of over 2.3 billion tonnes of oil globally, highlighting their impact on curbing fossil fuel consumption.

Furthermore, the expanding adoption of electric vehicles (EVs) is directly impacting the demand for oil and, by extension, natural gas used in power generation. Global EV sales were projected to exceed 15 million units in 2024, a trend that the IEA forecasts could displace over 6 million barrels of oil per day by 2030, underscoring the growing substitution effect.

The increasing viability of renewables, bolstered by advancements in energy storage, further intensifies this substitution threat. By mid-2024, the cost of utility-scale lithium-ion battery packs had fallen by over 90% compared to a decade prior, making renewables more competitive and reducing the reliance on natural gas for grid stability.

| Substitute Category | Key Drivers | Impact on Natural Gas Demand | 2023/2024 Data Point |

| Renewable Energy | Cost reduction, policy support, technological advancements | Direct displacement in power generation | Global renewable capacity additions exceeded 500 GW in 2023 |

| Energy Efficiency | Technological improvements, consumer awareness | Reduced overall energy consumption | IEA: Saved over 2.3 billion tonnes of oil equivalent in 2024 |

| Electric Vehicles (EVs) | Falling battery costs, government incentives, environmental concerns | Reduced demand for gasoline and diesel, indirect impact on power generation | Global EV sales projected to exceed 15 million units in 2024 |

| Energy Storage | Battery cost declines, grid modernization | Enhanced reliability of renewables, reducing need for gas peaker plants | US grid-scale battery storage capacity surpassed 10 GW by 2024 |

Entrants Threaten

High Capital Costs and Access to Resources

The oil and gas industry, particularly the upstream segment focused on extraction, demands enormous capital for asset acquisition, drilling operations, and essential infrastructure development. Even for companies like Diversified Energy that specialize in purchasing existing wells, substantial upfront investment remains a necessity.

These considerable initial expenditures, coupled with the inherent difficulty in gaining access to profitable natural gas and oil reserves, create a formidable barrier for potential new competitors looking to enter the market.

Extensive Regulatory and Environmental Hurdles

New companies entering the diversified energy sector must contend with a formidable array of regulatory and environmental challenges. These include obtaining numerous permits, adhering to strict operational safety standards, and complying with evolving methane emissions regulations. For instance, in 2024, the U.S. Environmental Protection Agency continued to refine its methane emissions standards for the oil and gas industry, adding layers of complexity for potential new operators.

Meeting these requirements necessitates substantial investment in specialized expertise, extensive compliance processes, and significant upfront capital. This high barrier to entry effectively deters smaller or less experienced entities from challenging established players like Diversified Energy. Diversified Energy, with its existing infrastructure and established compliance frameworks, is well-positioned to manage these ongoing regulatory demands.

Proprietary Technology and Operational Expertise

Diversified Energy's success in optimizing mature oil and gas assets hinges on proprietary technologies and deep operational expertise. These capabilities are crucial for enhancing recovery rates and mitigating the natural decline of older fields. For instance, in 2024, Diversified Energy reported achieving significant operational efficiencies through its advanced artificial lift and production optimization techniques.

New entrants face a substantial hurdle in replicating this specialized knowledge and technological advantage. Developing or acquiring the necessary proprietary technologies and cultivating a highly skilled workforce capable of efficiently managing mature assets requires considerable time and investment, creating a significant barrier to entry and impacting potential profitability.

Economies of Scale and Integration

Diversified Energy's significant economies of scale present a substantial barrier to new entrants. Established players benefit from lower per-unit costs in operations, equipment procurement, and marketing due to their sheer size. For instance, in 2024, Diversified Energy reported operating expenses of approximately $1.2 billion, a figure that would be incredibly challenging for a new, smaller competitor to match on a per-unit basis.

The company's integrated business model, encompassing production, midstream infrastructure, and marketing, further solidifies this advantage. This integration allows for greater control over the entire value chain, leading to enhanced cost efficiencies and the ability to capture more margin. New entrants would face immense capital requirements and a lengthy time horizon to replicate such a comprehensive and efficient operational structure.

- Economies of Scale: Established companies like Diversified Energy leverage large-scale operations, leading to reduced per-unit costs in production and administration.

- Integrated Operations: Diversified Energy's control over midstream assets and marketing channels provides cost advantages and greater value capture compared to non-integrated rivals.

- Capital Intensity: New entrants would require substantial upfront investment to achieve comparable operational scale and integration, creating a significant financial hurdle.

- Procurement Power: Existing companies benefit from bulk purchasing of materials and services, securing more favorable pricing than smaller, newer entities.

Commodity Price Volatility and Market Access

New entrants in the diversified energy sector face significant hurdles due to commodity price volatility. Without sophisticated hedging strategies or pre-arranged long-term contracts, these newcomers are far more exposed to the unpredictable swings in oil, gas, and other energy prices. For instance, in early 2024, crude oil prices experienced notable fluctuations, with Brent crude trading within a range of approximately $75 to $85 per barrel, highlighting the inherent risk for unhedged participants.

Securing essential market access is another formidable barrier for new entrants. This often involves gaining access to pipeline capacity, refining capabilities, or established distribution networks, which can be both costly and difficult to obtain. In regions with existing infrastructure limitations, such as certain North American shale plays experiencing high utilization rates in 2024, the competition for available transport and processing capacity intensifies, further disadvantaging new players.

- Vulnerability to Price Swings: New entrants lack the established hedging programs that protect incumbent firms from sharp declines or increases in energy commodity prices.

- Market Access Challenges: Gaining entry into established markets requires significant investment in infrastructure or costly agreements for capacity, often unavailable or prohibitively expensive for newcomers.

- Infrastructure Bottlenecks: In 2024, certain energy-producing regions faced transportation constraints, making it harder and more expensive for new producers to get their commodities to market.

High Hurdles: Why New Entrants Struggle in Diversified Energy

The threat of new entrants in the diversified energy sector is significantly mitigated by the immense capital requirements for asset acquisition and infrastructure. Diversified Energy's established operational scale, with reported operating expenses around $1.2 billion in 2024, creates a substantial cost advantage that new, smaller competitors struggle to match.

Furthermore, proprietary technologies and deep operational expertise in optimizing mature assets, a key strength for Diversified Energy in 2024, are difficult and costly for newcomers to replicate. Regulatory compliance, including evolving methane emission standards in 2024, adds further complexity and expense, deterring less experienced entities.

Market access challenges, such as securing pipeline capacity amidst infrastructure bottlenecks observed in 2024, and vulnerability to commodity price volatility without established hedging programs also serve as significant barriers. These factors collectively ensure that the entry of new significant players remains a low threat for established companies like Diversified Energy.

Porter's Five Forces Analysis Data Sources

Our Diversified Energy Porter's Five Forces analysis is built on a foundation of robust data, drawing from company annual reports, SEC filings, and industry-specific trade publications to capture the competitive landscape.