Coal India Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Coal India Bundle

From Overview to Strategy Blueprint

Coal India operates within a complex energy landscape, where the bargaining power of buyers and the threat of substitutes significantly shape its profitability. Understanding these forces is crucial for navigating the competitive environment.

The full Porter's Five Forces Analysis delves into the intensity of each of these pressures, revealing the true competitive dynamics at play for Coal India. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Limited Supplier Power for Key Inputs

While suppliers of specialized mining equipment and proprietary technology might wield some influence due to the unique nature of their products, Coal India's immense procurement volume significantly curtails the bargaining power of most suppliers. For instance, in 2023-24, Coal India procured vast quantities of essential materials and services, allowing it to negotiate favorable terms, effectively limiting individual supplier leverage.

Labor Unions and Wage Negotiations

Powerful labor unions within the mining sector, including those representing Coal India's workforce, act as significant suppliers of labor. Their considerable bargaining power directly influences wage levels, benefit packages, and overall working conditions. For instance, in 2023, wage revisions and agreements with unions can significantly alter Coal India's operational expenditure, impacting profitability.

These negotiations have a direct effect on production costs and the company's ability to adapt its operational strategies. The influence of government policies, such as minimum wage laws and labor standards, further shapes the landscape of these bargaining dynamics, setting a baseline for negotiations and potentially increasing labor costs.

Land Acquisition Challenges

Land acquisition for new mining projects or expansions in India presents significant hurdles, often becoming a politically charged affair. This complexity inherently empowers landowners and local communities, as their consent is crucial for project commencement or continuation. For instance, in 2023-24, Coal India faced ongoing land acquisition challenges impacting several of its planned projects, leading to potential delays and increased capital expenditure estimates for these ventures.

The protracted nature of land acquisition processes, coupled with escalating compensation demands from landowners, directly translates into substantial impacts on project timelines and overall costs. This situation effectively grants considerable bargaining power to a wide array of 'suppliers' – the individuals and communities providing the essential land resource for Coal India's operations.

Technology and Digitalization Providers

As coal mining increasingly adopts advanced technologies and digitalization for efficiency, safety, and environmental compliance, specialized technology and software providers are gaining some leverage. Their unique solutions and proprietary systems can create switching costs for Coal India, making it less straightforward to change providers once integrated. For instance, the adoption of AI-powered predictive maintenance for heavy machinery can lead to significant upfront investment and training, binding the user to the specific vendor.

Coal India's immense scale, however, allows for significant bargaining power through bulk purchasing agreements and the ability to negotiate custom solutions. This scale can reduce the per-unit cost of technology adoption and allows CIL to demand tailored features that better suit its operational needs, thereby mitigating some of the suppliers' influence. In 2023, Coal India's capital expenditure on technology and modernization initiatives was reported to be in the billions of rupees, providing substantial negotiation leverage with technology partners.

- Increased reliance on specialized mining technology enhances supplier bargaining power due to potential switching costs.

- Coal India's substantial scale enables bulk purchasing and customized solutions, which can significantly reduce supplier leverage.

- The strategic importance of digitalization in mining operations means technology providers are becoming more critical partners.

- Negotiating favorable terms for proprietary software and hardware is crucial for managing costs in technology adoption.

Infrastructure and Logistics Providers

Infrastructure and logistics providers, particularly those managing railway networks and port facilities, exert a degree of bargaining power over Coal India Limited (CIL). CIL's extensive reliance on these services for the timely and cost-effective transportation of its coal output means that disruptions or unfavorable pricing from these suppliers can significantly impact its operational efficiency and profitability. For instance, delays in rail wagon availability or increased port charges directly affect CIL's ability to meet delivery commitments.

However, this power is somewhat mitigated by CIL's close working relationships with many government-owned infrastructure entities. These collaborations often involve long-term agreements and strategic planning, which can help balance the negotiating leverage. Despite these partnerships, the inherent need for robust logistics infrastructure means that CIL must remain attentive to the terms and conditions offered by these critical service providers.

In 2023-24, CIL faced challenges related to logistics, with reports indicating that a significant portion of its production was held up due to transportation constraints. For example, during certain periods, pithead stocks exceeded 40 million tonnes, highlighting the critical nature of efficient logistics for managing inventory and sales. The cost of logistics, including rail freight, represents a substantial component of CIL's overall operational expenditure, underscoring the importance of favorable terms from infrastructure providers.

- Logistics Dependence: Coal India relies heavily on railway networks and port facilities for transporting its vast coal production, making these providers influential.

- Operational Impact: Disruptions or unfavorable terms from infrastructure suppliers can lead to increased costs and delivery delays for CIL.

- Mitigating Factors: CIL's close collaborations with government-owned logistics entities help to moderate the bargaining power of these suppliers.

- Cost Significance: Logistics costs, particularly rail freight, form a substantial part of CIL's operational expenses, emphasizing the need for competitive supplier terms.

Coal India's Supplier Power Dynamics: A 2023-24 Analysis

The bargaining power of suppliers for Coal India is generally moderate, primarily due to the company's massive scale and its ability to dictate terms through bulk procurement. However, specific suppliers of specialized equipment, proprietary technology, and critical labor unions can exert significant influence.

In 2023-24, Coal India's procurement of essential materials and services allowed it to negotiate favorable terms, limiting the leverage of most suppliers. Yet, powerful labor unions, representing a significant supply of labor, directly impact wage levels and working conditions, influencing operational costs.

Land acquisition for mining projects remains a key area where suppliers, namely landowners and local communities, hold considerable power due to the politically sensitive nature of land rights and escalating compensation demands.

| Supplier Type | Bargaining Power Level | Key Factors Influencing Power | Impact on Coal India | 2023-24 Data/Context |

|---|---|---|---|---|

| General Materials & Services | Low to Moderate | Coal India's scale, bulk purchasing | Favorable pricing, standardized terms | Vast procurement volumes negotiated favorable terms. |

| Specialized Mining Equipment/Technology | Moderate to High | Proprietary nature, switching costs, integration complexity | Higher costs for advanced solutions, potential vendor lock-in | Billions of rupees in capex for technology adoption provided negotiation leverage. |

| Labor (Unions) | High | Union strength, wage agreements, government labor policies | Increased wage bills, impact on operational costs and flexibility | Wage revisions in 2023 significantly altered operational expenditure. |

| Landowners/Local Communities | High | Land scarcity, political sensitivity, compensation demands | Project delays, increased capital expenditure, operational disruptions | Ongoing land acquisition challenges impacted several planned projects in 2023-24. |

| Infrastructure & Logistics (Rail, Port) | Moderate to High | Reliance on services, potential for disruptions, freight costs | Impact on delivery times, operational efficiency, and overall costs | Logistics constraints led to over 40 million tonnes of pithead stocks at times in 2023-24. |

What is included in the product

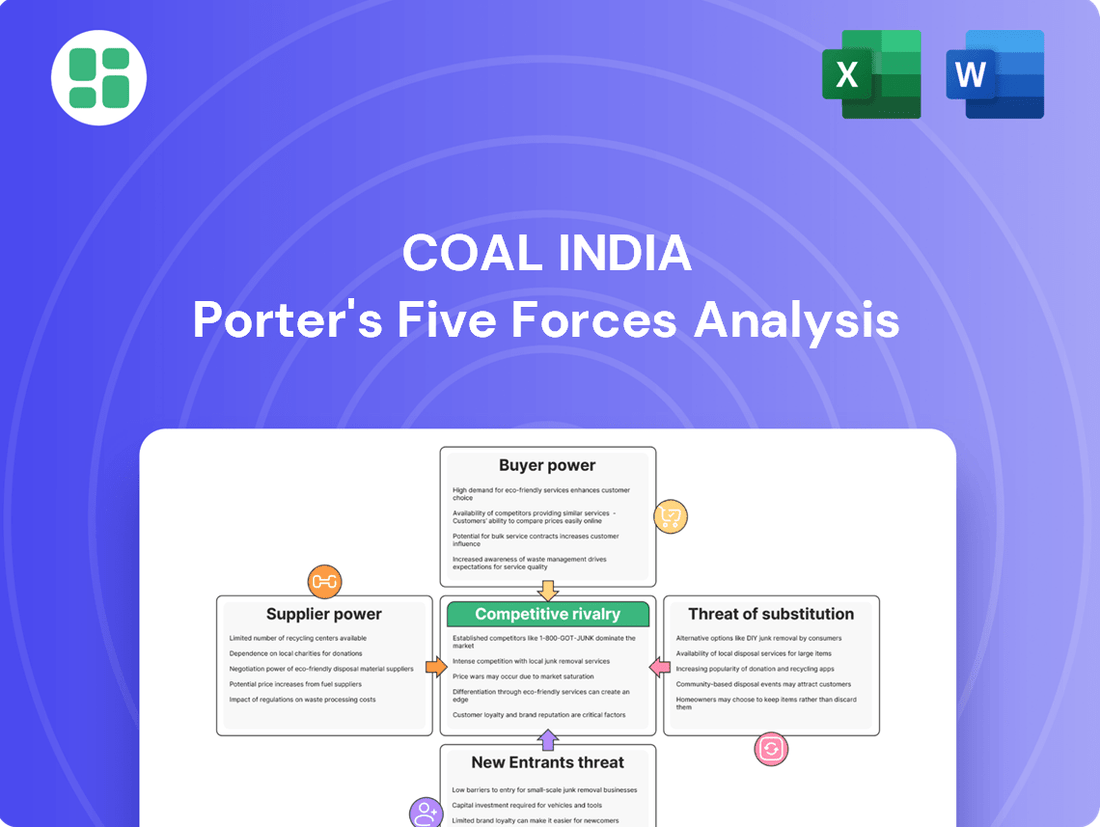

This analysis dissects Coal India's competitive environment by examining the bargaining power of buyers and suppliers, the threat of new entrants and substitutes, and the intensity of rivalry within the coal industry.

Navigate the complex competitive landscape of Coal India with a clear, one-sheet summary of all five forces—perfect for quick strategic decision-making.

Customers Bargaining Power

Large, Concentrated Customer Base

Coal India's customer base is highly concentrated, primarily consisting of large state-owned or private power generators, steel plants, and cement manufacturers. These entities are few in number but represent substantial demand, absorbing massive volumes of coal. For instance, power generation alone accounted for over 80% of Coal India's total sales in the fiscal year 2023-24.

This concentration of large buyers grants them significant bargaining power. Their substantial procurement volumes enable them to negotiate favorable prices and supply terms, directly impacting Coal India's revenue and profit margins. In 2023, the average selling price realization for Coal India was approximately ₹1,750 per tonne, a figure influenced by these customer negotiations.

Importance of Coal as a Raw Material

Coal's role as a primary fuel for India's power sector gives Coal India (CIL) considerable leverage. In 2023-24, coal accounted for approximately 70% of the country's electricity generation, highlighting the limited substitutability for many industrial and power consumers. This deep reliance means customers often lack immediate or cost-effective alternatives, diminishing their bargaining power.

Price Sensitivity and Cost Pass-Through

Customers, especially power generation companies, are highly sensitive to coal prices because they operate in regulated sectors where keeping electricity costs down is a priority. This means they actively push to minimize their input expenses, directly affecting Coal India's pricing power.

The ability of these power companies to pass on any increases in coal costs to the end consumer is often restricted, further intensifying their pressure on Coal India to maintain competitive pricing. For instance, in 2023, the average price of coal in India remained a significant factor in power generation cost structures, with utilities closely monitoring these expenses.

Threat of Backward Integration by Customers

Large industrial consumers, particularly in the power and steel industries, are increasingly investigating or initiating their own captive coal mining operations. This strategy aims to guarantee a stable supply and lessen reliance on external suppliers like Coal India. For instance, as of early 2024, several major power producers have announced plans or are in advanced stages of developing captive mines to meet a significant portion of their coal requirements.

This credible threat of backward integration significantly bolsters the bargaining power of these customers. It pressures Coal India to maintain competitive pricing and service levels to retain these key accounts. The government's ongoing promotion of commercial coal mining further empowers customers by making it more feasible for them to pursue these independent mining ventures.

- Captive Mining Exploration: Power and steel sectors are actively exploring captive coal mining.

- Supply Security Driver: Customers seek backward integration for supply chain stability.

- Competitive Pressure: Threat of integration forces Coal India to offer competitive terms.

- Government Support: Policy encouraging commercial mining facilitates customer integration.

Government Regulation and Allocation Policies

The Indian government's substantial influence on coal allocation and pricing for critical sectors like power generation significantly shapes the bargaining power of Coal India's customers. These regulatory interventions can override pure market forces, dictating supply terms and conditions.

This regulatory framework often serves to balance the power dynamic between Coal India and its primary customers, ensuring the consistent supply of coal to essential industries. For instance, in 2023-24, Coal India supplied approximately 773.7 million tonnes of coal to the power sector, highlighting the government's role in managing this crucial resource flow.

- Government-determined pricing mechanisms can limit the ability of customers to negotiate lower rates.

- Allocation policies ensure that key sectors, such as power generation, receive a predictable supply, reducing their reliance on market fluctuations and thus their individual bargaining leverage.

- Regulatory oversight can also introduce conditions that customers must meet to secure supply, indirectly influencing their negotiating position.

Major Coal Buyers Exert Strong Bargaining Power

Coal India's customers, primarily large power plants and industrial users, possess considerable bargaining power due to their significant demand volumes and the essential nature of coal for their operations. In fiscal year 2023-24, the power sector alone consumed over 80% of Coal India's output, underscoring customer concentration.

Customers' ability to negotiate prices is influenced by their sensitivity to input costs, especially in regulated sectors like power generation where price pass-throughs are often limited. This pressure is evident in the average selling price realization for Coal India, which was around ₹1,750 per tonne in 2023, reflecting these negotiations.

The threat of backward integration, such as customers pursuing captive mining operations, further amplifies their bargaining leverage. As of early 2024, several major power producers were advancing plans for captive mines, aiming to secure supply and reduce reliance on external suppliers like Coal India.

Government policies also play a role, balancing power dynamics through allocation and pricing mechanisms for critical sectors. For instance, Coal India supplied approximately 773.7 million tonnes to the power sector in 2023-24, demonstrating the government's influence on supply to essential industries.

| Customer Segment | Demand Share (FY23-24 est.) | Average Selling Price (2023 est.) | Key Bargaining Factor |

|---|---|---|---|

| Power Sector | >80% | ~₹1,750/tonne | High volume, price sensitivity, regulatory environment |

| Steel & Cement | ~10-15% | Negotiated rates | Significant individual purchase size, alternative fuel exploration |

| Other Industries | ~5-10% | Market-driven pricing | Smaller volumes, less concentrated power |

Preview Before You Purchase

Coal India Porter's Five Forces Analysis

This preview showcases the comprehensive Coal India Porter's Five Forces Analysis, detailing the competitive landscape, including the threat of new entrants, the bargaining power of buyers and suppliers, the threat of substitutes, and the intensity of rivalry within the industry. The document displayed here is the part of the full version you’ll get—ready for download and use the moment you buy, providing actionable insights for strategic decision-making.

Rivalry Among Competitors

Dominant Market Share and State Ownership

Coal India Limited (CIL) commands an overwhelming presence in the Indian coal sector, consistently producing over 80% of the nation's total coal output. For instance, in the fiscal year 2023-24, CIL produced approximately 773.6 million tonnes of coal, underscoring its near-monopolistic grip. This substantial market share inherently dampens direct competitive rivalry among domestic players, as CIL's scale and operational capacity are difficult for smaller entities to match.

As a state-owned enterprise, CIL benefits from significant advantages, including preferential allocation of mining leases and strong backing from the government. This state ownership translates into preferential access to critical resources and a more favorable regulatory environment. These factors create substantial barriers to entry for potential new competitors, further solidifying CIL's dominant position and limiting the intensity of competitive rivalry within India.

Limited Domestic Competition from Private Miners

While India has opened its doors to commercial coal mining, the landscape still sees a limited number of large-scale private players capable of matching Coal India's (CIL) extensive operational footprint. As of early 2024, CIL continues to dominate the domestic market, producing over 773 million tonnes in the fiscal year 2022-23.

Emerging private mines, though growing, tend to focus on catering to specific industrial demands or niche market segments. They are not yet positioned to challenge CIL's comprehensive product range and widespread distribution network, indicating that this competition, while present, remains nascent and not a significant immediate threat to CIL's market dominance.

Competition from Imported Coal

While Coal India Limited (CIL) holds a dominant position in the domestic market, it encounters indirect rivalry from imported coal. This is particularly true for power plants situated along India's coastlines and for industrial consumers who may find imported coal more cost-effective or suitable for their specific grade requirements. For instance, in the fiscal year 2023-24, India's coal imports stood at approximately 238.5 million tonnes, indicating a significant alternative supply available to consumers.

The fluctuating global coal prices and associated shipping costs directly impact the competitiveness of CIL's domestically produced coal. When international prices are low, imported coal becomes a more attractive option for certain segments of the market, offering customers an alternative to CIL's supply. This dynamic creates a competitive pressure, forcing CIL to remain mindful of its pricing and efficiency to retain market share.

High Fixed Costs and Exit Barriers

The coal mining sector, including Coal India, faces substantial fixed costs. These costs are tied to exploration, developing mines, and acquiring and maintaining heavy machinery. These significant capital outlays act as a strong deterrent for potential new companies looking to enter the market, effectively limiting the number of competitors.

These high fixed costs also contribute to significant exit barriers. Once a company has invested heavily in infrastructure and equipment, it becomes very difficult and costly to divest or shut down operations, even if the business is not performing well. This immobility can actually lessen the intensity of rivalry by keeping less efficient players in the market rather than allowing them to exit and free up resources.

- Coal India's extensive infrastructure represents a massive sunk cost, estimated in billions of dollars, making it challenging for them to exit specific mining operations.

- The capital expenditure for developing a new coal mine can range from hundreds of millions to over a billion dollars, creating a high barrier to entry.

- In 2023-24, Coal India's capital expenditure was ₹19,090 crore (approximately $2.3 billion USD), highlighting the ongoing investment in fixed assets.

Commodity Nature of Coal

The commodity nature of coal means that it is largely undifferentiated, making price the dominant factor in customer choices. This intensifies rivalry, as competitors often vie for market share by offering lower prices, pushing companies like Coal India to prioritize cost efficiency.

Despite Coal India's significant economies of scale, the lack of product differentiation creates vulnerability. A new entrant capable of supplying coal at a lower cost could quickly attract customers, underscoring the constant pressure on Coal India to maintain its operational efficiency and cost leadership.

- Price Sensitivity: As a commodity, coal's value is primarily determined by its price, meaning buyers will gravitate towards the most cost-effective options.

- Limited Differentiation: Unlike specialized products, coal offers few unique features, making it difficult for any single producer to command premium pricing.

- Operational Efficiency is Key: Coal India's strategy must heavily rely on optimizing its production and logistics to remain competitive against price-focused rivals.

India's Coal: Over 80% Market Share by a Single Entity

Competitive rivalry within India's coal sector is notably subdued due to Coal India Limited's (CIL) overwhelming market dominance, producing over 80% of the nation's coal. In fiscal year 2023-24, CIL's production reached approximately 773.6 million tonnes, a figure that makes it exceedingly difficult for smaller domestic players to compete on scale.

While private commercial mining has been introduced, the number of large-scale private operators capable of challenging CIL's extensive footprint remains limited. Emerging private mines often serve niche markets, and as of early 2024, CIL's comprehensive product range and distribution network are largely unchallenged by these smaller ventures.

Indirect rivalry stems from imported coal, particularly for coastal power plants and industries seeking cost-effective or specific grades. India's coal imports in fiscal year 2023-24 were around 238.5 million tonnes, highlighting a significant alternative supply that influences CIL's market position and pricing strategies.

The commodity nature of coal intensifies rivalry, as price becomes the primary differentiator, compelling producers like CIL to focus intensely on operational efficiency and cost leadership to retain market share.

| Metric | Coal India (FY 2023-24) | Indian Coal Imports (FY 2023-24) |

|---|---|---|

| Domestic Production Share | ~80% | N/A |

| Total Production (Million Tonnes) | ~773.6 | N/A |

| Total Imports (Million Tonnes) | N/A | ~238.5 |

SSubstitutes Threaten

Growing Renewable Energy Adoption

The most substantial long-term threat to coal comes from renewable energy sources such as solar, wind, and hydropower. These alternatives are rapidly becoming more appealing due to growing environmental awareness and falling prices, with global renewable energy capacity expected to increase significantly in the coming years. For instance, the International Energy Agency (IEA) reported that renewable energy sources accounted for over 80% of new global power capacity additions in 2023.

Government policies worldwide are actively promoting a transition away from fossil fuels, directly encouraging a move towards renewables. This policy support, including subsidies and mandates, is a key driver in reducing the demand for coal in power generation. In 2024, many nations continued to set ambitious renewable energy targets, further solidifying this trend.

This increasing adoption of renewables presents a fundamental structural challenge to coal's historical dominance in the energy sector. As renewables become more cost-competitive and widely deployed, they directly erode the market share and future growth potential for coal-fired power plants.

Natural Gas as a Cleaner Alternative

Natural gas presents a moderate threat as a substitute for coal in India, primarily due to its cleaner combustion properties for power generation and industrial uses. As of early 2024, India's natural gas consumption was projected to grow significantly, with the government aiming to increase its share in the energy mix.

While natural gas is currently more costly and less readily available than coal within India, its environmental advantages are a key driver for potential future adoption. The expansion of natural gas infrastructure, including pipelines and LNG regasification terminals, is crucial for its competitiveness.

Government policies and incentives aimed at promoting gas-based industries and power plants could further accelerate the substitution process. For instance, initiatives to develop a national gas grid and encourage domestic exploration are vital factors influencing this threat's evolution.

Nuclear Power and Hydroelectric Projects

Large-scale nuclear and hydroelectric projects are significant long-term substitutes for coal-fired power, despite their high upfront costs and lengthy development timelines. For instance, as of early 2024, India's nuclear power capacity stood at over 6,700 MW, with several new projects under construction, signaling a commitment to this alternative energy source.

Government initiatives are actively promoting energy diversification, explicitly aiming to decrease dependence on fossil fuels like coal. This strategic shift is evident in national energy policies that encourage substantial investment in renewable and nuclear energy infrastructure, with the goal of creating a more resilient and sustainable power sector.

These alternative sources, including nuclear and hydro, offer the distinct advantage of providing consistent, base-load power generation without contributing to carbon emissions. This is a crucial factor as countries worldwide strive to meet climate targets and reduce their environmental footprint, making them increasingly attractive alternatives to coal.

Energy Efficiency and Conservation

Improvements in energy efficiency across industrial and residential sectors are significantly reducing the overall demand for energy, acting as a direct substitute for coal consumption. For instance, advancements in building insulation and smart grid technologies in 2024 are making energy use far more economical.

Government policies actively promoting energy conservation and the adoption of more efficient technologies, such as incentives for LED lighting and high-efficiency appliances, are tempering the growth in coal demand. The International Energy Agency reported in early 2025 that global energy intensity improvements averaged 2.2% in 2024, a notable acceleration.

- Reduced Demand: Efficiency gains mean less energy is needed overall, directly impacting coal's market share.

- Policy Impact: Government mandates and incentives for conservation further suppress coal consumption.

- Market Size: This systemic shift shrinks the potential market size for coal.

- Technological Advancement: Innovations in energy-saving technologies create viable alternatives to coal-powered energy.

Technological Advancements in Energy Storage

Technological advancements in energy storage, particularly in battery technology, are significantly increasing the competitiveness of renewable energy sources against coal. Improvements in lithium-ion and emerging battery chemistries are driving down costs, making renewables a more viable alternative for consistent power generation.

For instance, the global average cost of utility-scale solar PV electricity generation, including storage, is projected to fall by over 50% between 2023 and 2030, according to the International Renewable Energy Agency (IRENA). This cost reduction directly challenges coal's position, especially for base-load power where reliability was once coal's primary advantage.

- Decreasing Storage Costs: Falling battery prices make renewables more economically attractive for grid-scale applications.

- Enhanced Renewable Reliability: Storage solutions improve the consistency of intermittent sources like solar and wind.

- Increased Grid Integration: Advanced storage enables greater penetration of renewables, directly substituting for coal-fired power plants.

Coal's Market Share Erodes: Alternatives Drive Shift

The threat of substitutes for coal is significant and multifaceted, primarily driven by the rise of renewable energy, natural gas, and improvements in energy efficiency. These alternatives are increasingly viable due to falling costs, supportive government policies, and growing environmental concerns, directly impacting coal's market share and future growth prospects.

Renewable energy sources like solar and wind are becoming increasingly cost-competitive, with global renewable capacity seeing substantial growth. For example, renewables accounted for over 80% of new global power capacity additions in 2023, according to the IEA. Government policies worldwide are actively promoting this transition, with many nations setting ambitious renewable energy targets in 2024.

Natural gas offers a cleaner alternative to coal for power generation and industrial use, with India's consumption projected to grow significantly. While currently facing availability and cost challenges, infrastructure expansion and government incentives are key to its increasing competitiveness.

Energy efficiency measures also act as a direct substitute by reducing overall energy demand. Global energy intensity improvements averaged 2.2% in 2024, a notable acceleration, supported by government policies promoting conservation and efficient technologies.

| Substitute Type | Key Drivers | Impact on Coal | Relevant Data/Trends |

|---|---|---|---|

| Renewable Energy (Solar, Wind) | Falling costs, environmental concerns, government policies | Directly displaces coal in power generation | 80%+ of new global power capacity in 2023; ambitious 2024 targets |

| Natural Gas | Cleaner combustion, government promotion | Moderate threat, especially with infrastructure development | Projected significant growth in India's consumption |

| Energy Efficiency | Technological advancements, conservation policies | Reduces overall energy demand, lowering coal consumption | 2.2% global energy intensity improvement in 2024 |

Entrants Threaten

High Capital Intensity and Sunk Costs

The coal mining sector is characterized by exceptionally high capital intensity. Establishing a new coal mine demands substantial upfront investment, often running into billions of dollars, for everything from geological surveys and land acquisition to the purchase of heavy-duty mining equipment and infrastructure development. For instance, new large-scale mining projects globally frequently require initial capital outlays exceeding $1 billion.

These significant capital requirements, coupled with the substantial sunk costs associated with mine development and specialized machinery, create a formidable barrier to entry. Once invested, these costs are largely irrecoverable, making the decision to enter the market a high-stakes gamble that only the most financially secure entities can afford to consider, thereby significantly deterring potential new competitors.

Extensive Regulatory Hurdles and Approvals

The Indian coal sector is a minefield of regulatory complexities, demanding a multitude of permits, environmental clearances, and land acquisition approvals. These processes are not only intricate and time-consuming but also susceptible to political sway, creating a formidable barrier for any potential new entrant aiming to establish operations.

Furthermore, the government's direct control over coal blocks adds another significant layer of difficulty, limiting access and increasing the overall cost and effort required to enter the market. For instance, in 2023-24, the Ministry of Coal allocated 100 coal blocks for commercial mining, underscoring the centralized nature of resource allocation.

Access to Coal Blocks and Reserves

The threat of new entrants into India's coal sector, particularly concerning access to coal blocks and reserves, remains moderate. Historically, government control and Coal India's (CIL) preferential access created significant barriers. While the auctioning of coal blocks for commercial mining has increased competition, securing economically viable and easily accessible reserves is still a hurdle for newcomers.

In 2023-24, the Ministry of Coal successfully auctioned 35 coal blocks, attracting bids from both public and private sector companies. However, CIL, with its vast existing reserves and established infrastructure, continues to hold a substantial advantage. For instance, as of March 31, 2024, CIL held over 50 billion tonnes of reserves, a scale difficult for new entrants to replicate quickly.

Economies of Scale and Cost Advantages

Coal India Limited (CIL) benefits significantly from massive economies of scale in its operations, from mining to distribution. This scale allows CIL to produce coal at a lower per-unit cost, creating a substantial barrier for any potential new entrant. For instance, in the fiscal year 2023-24, CIL produced 773.6 million tonnes of coal, a figure that is incredibly difficult for a new player to replicate.

New companies entering the coal market would face immense challenges in matching CIL's cost efficiency. Without comparable scale, they would likely have higher per-unit production and logistical costs, making it hard to compete on price. This cost disadvantage is a primary deterrent, as achieving similar operational efficiencies and infrastructure would require enormous capital investment and time.

- Economies of Scale: CIL's vast production capacity, exceeding 773 million tonnes in FY 2023-24, provides significant cost advantages.

- Cost Advantages: Lower per-unit costs due to scale in production, logistics, and distribution make it difficult for new entrants to compete on price.

- Operational Footprint: CIL's extensive network of mines and infrastructure across India offers a substantial cost advantage.

- Barriers to Entry: The capital required to establish a comparable operational scale and achieve cost parity is a major hurdle for new competitors.

Infrastructure Requirements and Logistics

The capital investment needed to establish the necessary infrastructure for coal mining, including extraction equipment, processing plants, and transportation links like railway sidings and washeries, presents a formidable barrier for new entrants. This is compounded by the significant lead times involved in securing permits and constructing these facilities. For instance, developing a new mine often takes years and requires billions in upfront capital. Coal India's established and integrated logistical network, encompassing vast rail infrastructure and port access, provides a substantial competitive advantage that is extremely difficult and costly for newcomers to replicate.

New players must not only fund mine development but also secure or build extensive logistics to move coal efficiently. This includes access to dedicated railway lines, loading facilities, and potentially port infrastructure for exports. Coal India's existing logistical backbone, developed over decades, provides a significant cost and operational efficiency advantage. In 2023-24, Coal India reported capital expenditure of INR 17,897 crore, a substantial portion of which is directed towards infrastructure development and modernization, highlighting the scale of investment required.

- Capital Intensity: Developing coal extraction, processing, and transportation infrastructure demands massive upfront capital, making it a significant hurdle for new companies.

- Logistics Network: Securing or building extensive logistics networks, including rail, road, and port access, is a critical and costly requirement for market entry.

- Coal India's Advantage: Coal India's existing, integrated logistical backbone offers a substantial competitive edge in terms of cost and operational efficiency.

India's Coal Sector: A Fortress Against New Competition

The threat of new entrants in India's coal sector is generally considered moderate, primarily due to substantial barriers. These include extremely high capital requirements for mine development and infrastructure, which can easily exceed $1 billion for large projects globally. Additionally, navigating complex regulatory landscapes and securing government-allocated coal blocks presents significant hurdles, as exemplified by the 100 coal blocks allocated for commercial mining in 2023-24.

Coal India Limited's (CIL) dominant position, underpinned by massive economies of scale and an established logistical network, further deters new players. CIL's production of 773.6 million tonnes in FY 2023-24 and its vast reserves of over 50 billion tonnes create cost advantages that are difficult for newcomers to match. The capital expenditure of INR 17,897 crore by CIL in 2023-24 on infrastructure highlights the scale of investment required to compete.

| Factor | Description | Impact on New Entrants |

|---|---|---|

| Capital Intensity | High upfront investment for mining and infrastructure. | Formidable barrier, requiring billions for new projects. |

| Regulatory Hurdles | Complex permits, clearances, and land acquisition. | Time-consuming and costly, influenced by political factors. |

| Economies of Scale | CIL's production of 773.6 MT in FY24. | Creates significant cost advantages, difficult to replicate. |

| Logistics Infrastructure | CIL's integrated network of rail and transport. | Costly for new entrants to build comparable efficiency. |

| Government Control | Allocation of coal blocks for commercial mining. | Limits direct access to reserves, increasing entry complexity. |

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis for Coal India is built upon a foundation of publicly available data, including Coal India's annual reports, investor presentations, and filings with regulatory bodies like the Securities and Exchange Board of India (SEBI).