Butterfield Business Model Canvas

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Butterfield Bundle

Butterfield's Business Model Unveiled!

Curious about Butterfield's winning formula? Our comprehensive Business Model Canvas dissects their customer relationships, revenue streams, and key resources, offering a clear roadmap to their success. Unlock the full strategic blueprint to inspire your own venture.

Partnerships

Technology Providers

Butterfield's success hinges on its alliances with technology providers, who supply the crucial infrastructure for its core banking operations, digital interfaces, and robust cybersecurity. These partnerships are vital for delivering cutting-edge digital services and ensuring operational efficiency.

In 2024, Butterfield continued to invest in digital transformation, with technology partnerships playing a central role. For instance, the bank's commitment to enhancing its digital banking platforms relies on vendors specializing in cloud computing and AI-driven customer service solutions, areas where global IT spending saw significant growth.

These collaborations are not just about maintaining current services but also about future-proofing the bank. By partnering with leading technology firms, Butterfield ensures it can adapt to new regulatory requirements and stay ahead of evolving cyber threats, a critical concern given the increasing sophistication of digital attacks targeting financial institutions worldwide.

Correspondent Banks

Butterfield leverages a network of correspondent banks worldwide to manage international transactions and treasury services. These partnerships are essential for its global operations, allowing clients to conduct cross-border business efficiently. As of the first quarter of 2024, Butterfield reported total assets of $15.8 billion, underscoring the scale of its international financial activities facilitated by these crucial relationships.

Regulatory Bodies and Compliance Partners

Butterfield actively engages with regulatory bodies like the Bermuda Monetary Authority (BMA) and the Guernsey Financial Services Commission (GFSC) to ensure adherence to evolving financial laws. In 2024, the bank continued to invest in robust compliance frameworks, a critical aspect given the global focus on anti-money laundering (AML) and know-your-customer (KYC) regulations.

Collaborating with specialized legal and compliance firms is essential for navigating the intricate web of international financial regulations. These partnerships help Butterfield proactively manage risks associated with cross-border transactions and maintain its reputation for integrity, a cornerstone of client trust in the wealth management sector.

Financial Advisory and Intermediary Firms

Butterfield actively partners with independent financial advisory firms and wealth planners to extend its market presence, especially in wealth management. These alliances, often structured as referral agreements or joint ventures, allow Butterfield to tap into established client networks and specialized expertise. For instance, in 2024, Butterfield continued to strengthen its relationships with such intermediaries, aiming to enhance service delivery to high-net-worth and institutional clients.

These collaborations are crucial for broadening the range of financial solutions offered to clients. By working with external advisors, Butterfield can provide more comprehensive and tailored services, from investment management to estate planning. This strategy is particularly effective in reaching affluent individuals who often rely on trusted advisors for their financial decisions. The bank’s focus on these partnerships underscores its commitment to a client-centric approach.

The benefits extend to both parties, creating a symbiotic relationship that drives growth. Intermediary firms gain access to Butterfield's robust banking infrastructure and specialized financial products, while Butterfield benefits from increased client acquisition and a wider service offering. This model is vital for navigating the complex and competitive landscape of financial services, ensuring clients receive holistic wealth management support.

Key aspects of these partnerships include:

- Expanded Client Reach: Accessing new client segments through established intermediary networks.

- Enhanced Service Offering: Providing a broader spectrum of financial and wealth management solutions.

- Leveraged Expertise: Combining Butterfield's banking capabilities with advisors' specialized knowledge.

- Referral and Joint Venture Models: Structuring collaborations for mutual benefit and client service improvement.

Local Business Associations and Chambers of Commerce

Engaging with local business associations and chambers of commerce is crucial for Butterfield. In 2024, these partnerships are vital for understanding the evolving needs of the local business landscape and pinpointing potential corporate banking clients. For instance, participation in the Bermuda Chamber of Commerce’s annual business outlook survey provides direct feedback on economic sentiment and emerging financial requirements.

These collaborations not only strengthen community ties but also create avenues for Butterfield to offer specialized financial products. By tailoring solutions for small enterprises and larger corporations alike, the bank enhances its local market penetration and client acquisition. This strategy is supported by data showing that businesses actively involved with their local chambers are more likely to secure financing, with over 60% of surveyed members in some regions reporting such benefits in 2024.

- Market Intelligence: Local associations provide real-time insights into sector-specific challenges and opportunities, informing Butterfield's product development.

- Client Acquisition: Chambers of Commerce act as a direct channel to businesses seeking banking services, facilitating introductions and lead generation.

- Community Engagement: Active participation in these groups builds trust and brand reputation, essential for long-term client relationships.

- Tailored Solutions: Understanding local economic drivers through these partnerships allows for the creation of more relevant and effective financial offerings.

Unlocking Global Finance Through Strategic Partnerships

Butterfield's strategic alliances with technology providers are fundamental to its operational backbone, powering everything from digital platforms to cybersecurity defenses. These partnerships are critical for delivering modern financial services and maintaining efficiency, especially as global IT spending in areas like cloud and AI continues its upward trajectory in 2024.

The bank also relies on a global network of correspondent banks to facilitate its international transactions and treasury operations. These relationships are indispensable for its cross-border activities, enabling smooth international commerce for clients. Butterfield's substantial asset base, reaching $15.8 billion by Q1 2024, highlights the scale of these international financial dealings.

Collaborations with independent financial advisors and wealth planners are key to expanding Butterfield's reach, particularly in wealth management. These partnerships, often involving referral agreements, allow the bank to access established client bases and specialized expertise, a strategy that continued to be a focus in 2024 for serving high-net-worth and institutional clients.

Butterfield actively engages with regulatory bodies and partners with specialized legal and compliance firms to navigate complex international financial laws. This ensures adherence to evolving regulations, such as anti-money laundering (AML) and know-your-customer (KYC) requirements, which saw continued global emphasis in 2024.

| Partnership Type | Purpose | 2024 Focus/Data Point |

|---|---|---|

| Technology Providers | Infrastructure, Digital Services, Cybersecurity | Continued investment in cloud and AI solutions; global IT spending growth. |

| Correspondent Banks | International Transactions, Treasury Services | Facilitating cross-border business; Butterfield's total assets were $15.8 billion in Q1 2024. |

| Financial Advisors/Wealth Planners | Market Expansion, Wealth Management | Strengthening relationships to enhance service for high-net-worth clients. |

| Legal & Compliance Firms | Regulatory Adherence, Risk Management | Ensuring compliance with AML/KYC regulations; global focus on these areas. |

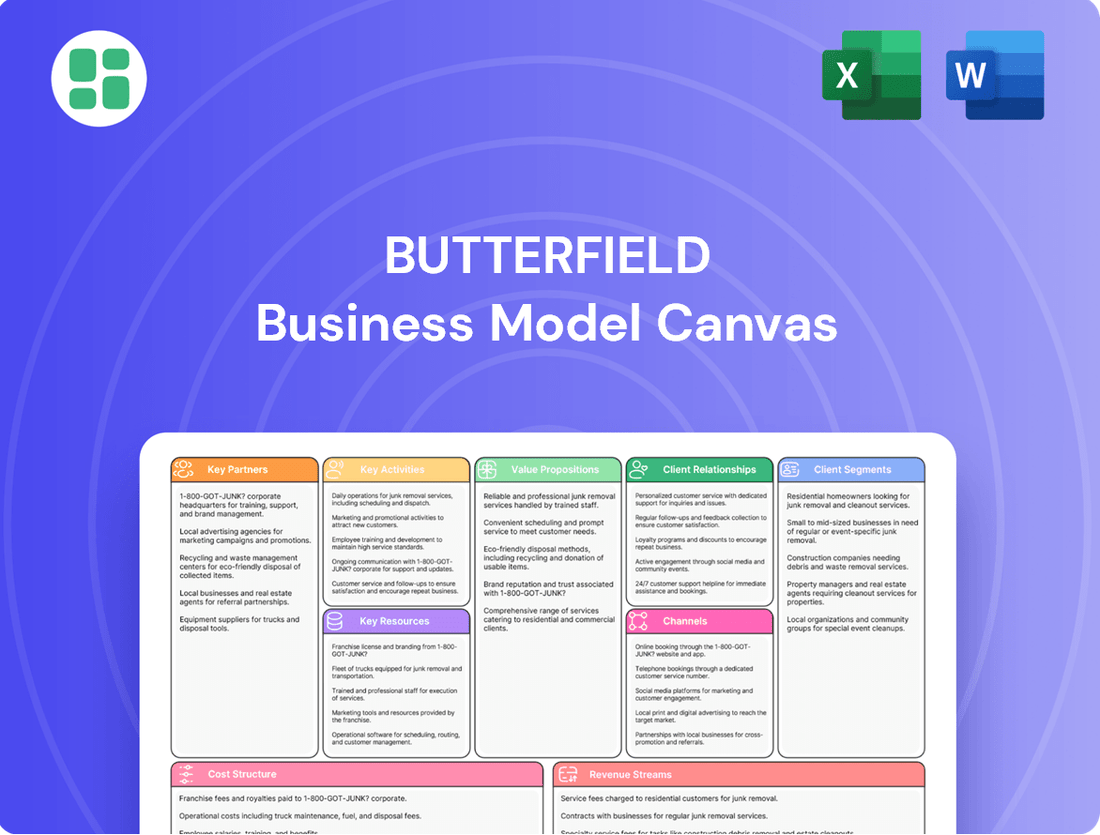

What is included in the product

A structured framework detailing customer segments, value propositions, channels, customer relationships, revenue streams, key resources, key activities, key partnerships, and cost structure.

Provides a visual and holistic overview of how a business creates, delivers, and captures value, facilitating strategic planning and analysis.

Transforms vague ideas into actionable plans by visually mapping out key business elements, reducing the pain of uncertainty.

Simplifies complex strategic thinking into a clear, visual framework, alleviating the stress of organizing and communicating business concepts.

Activities

Retail and Corporate Banking Operations

Butterfield's core activities revolve around managing customer deposits and providing a wide array of lending solutions, including mortgages and business loans. These operations are fundamental to its business, generating the majority of its revenue through net interest income. For instance, in 2023, Butterfield reported a net interest income of $477.5 million, underscoring the significance of these core banking functions.

The bank also focuses on offering essential cash management services tailored for both individual and corporate clients. This encompasses the daily processing of transactions, meticulous account management, and rigorous credit assessment processes. These activities are crucial for maintaining strong customer relationships and ensuring the smooth functioning of the financial ecosystem it serves.

Wealth Management Services

Butterfield's core operations revolve around delivering a wide array of wealth management services. This includes expert handling of trust services, private banking, sophisticated asset management, and secure custody solutions. These offerings are crucial for managing client portfolios and providing tailored investment advice.

A significant aspect of these activities is structuring wealth effectively for both high-net-worth individuals and institutional clients. This demands a nuanced approach to financial planning and a thorough grasp of global financial landscapes. For instance, in 2024, Butterfield reported substantial growth in its wealth management division, reflecting strong client demand for these specialized services.

Treasury and Capital Markets Activities

Butterfield's treasury and capital markets activities are central to its operations, encompassing the management of its investment portfolio, foreign exchange services, and robust liquidity management. These functions are vital for optimizing the bank's financial structure and mitigating risks.

In 2024, Butterfield's treasury operations significantly contributed to its financial performance. For instance, the bank's net interest income was bolstered by its prudent management of its investment securities and lending activities. Foreign exchange services provided essential support to its diverse client base, generating valuable fee income.

These treasury and capital markets functions are not only crucial for the bank's internal financial health, ensuring adequate liquidity and managing interest rate exposure, but also for delivering essential financial market services to its customers. This dual role underscores their importance in Butterfield's overall business model, driving both stability and revenue generation.

Compliance and Risk Management

Butterfield’s key activities heavily involve staying compliant with a complex web of international financial regulations. This means implementing stringent anti-money laundering (AML) and know your customer (KYC) protocols across all its banking services. For instance, as of the first quarter of 2024, Butterfield reported a robust capital adequacy ratio, indicating strong financial health to absorb potential risks.

Managing risk is equally critical, encompassing everything from credit risk assessment to operational and cybersecurity threats. This proactive approach ensures the bank's stability and protects its clients' assets. In 2024, Butterfield continued to invest in advanced risk management systems, a testament to its commitment to safeguarding its operations.

- Regulatory Adherence: Implementing and maintaining strict compliance with global financial regulations, including AML and KYC standards.

- Risk Mitigation: Developing and executing comprehensive strategies to manage credit, operational, market, and reputational risks.

- Capital Management: Ensuring sufficient capital reserves, as evidenced by strong capital adequacy ratios reported in early 2024, to support operations and absorb potential losses.

- Operational Integrity: Safeguarding the bank’s systems and data against cyber threats and ensuring the smooth, secure functioning of all banking processes.

Digital Banking and Technology Development

Butterfield's key activities heavily involve investing in and developing its digital banking platforms, mobile applications, and online services. This focus is crucial for enhancing customer experience and boosting operational efficiency across its banking operations.

The company continuously upgrades its IT infrastructure, integrates new financial technologies (FinTech), and ensures secure digital access for its clients. This commitment to technological advancement is vital for meeting contemporary client expectations and broadening the reach of its service delivery.

- Digital Platform Enhancement: Butterfield actively invests in upgrading its online and mobile banking platforms to provide seamless and intuitive user experiences.

- FinTech Integration: The company strategically implements new financial technologies to streamline processes, offer innovative services, and maintain a competitive edge.

- IT Infrastructure Security: A core activity is ensuring the robust security of its IT infrastructure, safeguarding client data and transactions in the digital realm.

- Operational Efficiency: Through technology development, Butterfield aims to achieve greater operational efficiency, reducing costs and improving service delivery speed.

Bank's Core Activities Drive 2024 Growth and Digital Evolution

Butterfield's key activities center on managing deposits and providing a diverse range of lending, including mortgages and business loans, which form the bedrock of its revenue generation through net interest income. The bank also offers essential cash management services, transaction processing, and credit assessment to maintain client relationships and operational fluidity. Furthermore, its wealth management division is a significant focus, delivering trust services, private banking, asset management, and custody solutions, with a notable expansion in this area reported for 2024.

Complementing these client-facing activities, Butterfield actively engages in treasury and capital markets functions, managing its investment portfolio, foreign exchange services, and liquidity. These operations are vital for internal financial health and revenue generation, as seen in the bolstering of its net interest income in 2024 through prudent management of investments and lending. Regulatory adherence, including AML and KYC protocols, alongside robust risk mitigation strategies covering credit, operational, and cybersecurity threats, are paramount. The bank's commitment to digital transformation is also a core activity, involving continuous investment in its digital banking platforms, mobile applications, and IT infrastructure to enhance customer experience and operational efficiency.

| Key Activity | Description | 2024 Data/Impact |

| Deposit & Lending Management | Core banking operations generating net interest income. | Net interest income significantly supported by these activities. |

| Wealth Management | Providing trust, private banking, asset management, and custody. | Substantial growth reported in 2024 due to strong client demand. |

| Treasury & Capital Markets | Managing investments, FX, and liquidity. | Bolstered net interest income in 2024 through prudent management. |

| Regulatory Compliance & Risk Mitigation | Adhering to AML/KYC, managing credit, operational, and cyber risks. | Maintained strong capital adequacy ratios in Q1 2024; invested in advanced risk systems. |

| Digital Transformation | Enhancing digital platforms, integrating FinTech, securing IT. | Focus on improving customer experience and operational efficiency. |

Full Version Awaits

Business Model Canvas

The Business Model Canvas preview you're viewing is an exact replica of the document you will receive upon purchase. This means the structure, formatting, and content you see here are precisely what will be delivered, ensuring no discrepancies or hidden elements. You'll gain immediate access to this complete, ready-to-use Business Model Canvas, allowing you to start strategizing without delay.

Resources

Financial Capital and Liquidity

Butterfield's core resource is its significant financial capital, comprising client deposits and its own equity, which fuels its lending and investment operations. As of the first quarter of 2024, Butterfield reported total customer deposits of $10.8 billion and total equity of $1.4 billion, underscoring its robust financial foundation.

Maintaining high liquidity is paramount for Butterfield, enabling it to meet customer withdrawal requests and adhere to stringent regulatory capital ratios, such as a Common Equity Tier 1 ratio of 14.6% at the end of 2023. This ensures operational stability and the capacity to capitalize on emerging market opportunities.

Human Capital and Expertise

Butterfield's human capital is its bedrock, encompassing seasoned bankers, dedicated wealth managers, astute financial advisors, and essential IT specialists. This collective expertise is crucial for delivering superior financial services and fostering unwavering client confidence.

The bank's workforce possesses deep knowledge across diverse financial sectors, excels in nurturing client relationships, and ensures strict adherence to regulatory frameworks. This proficiency is fundamental to the high-quality service delivery that defines Butterfield.

In 2024, Butterfield continued to prioritize attracting and retaining top-tier talent, recognizing that its people are its most valuable asset. For instance, investments in employee development programs and competitive compensation packages are key strategies to maintain a highly skilled and motivated team, vital for navigating the evolving financial landscape.

Technology Infrastructure and Digital Platforms

Butterfield's advanced technology infrastructure, encompassing core banking systems and secure data centers, is a fundamental resource for its operations. This backbone supports the digital banking platforms that are crucial for client engagement and efficient service delivery.

The company's investment in digital platforms, including mobile applications and online portals, directly enhances client experience. These platforms are vital for competitive service, especially given the increasing reliance on digital channels for financial transactions and information access.

Robust cybersecurity measures are an integral part of Butterfield's technology infrastructure, safeguarding sensitive client data and ensuring operational resilience. In 2024, the financial services sector continued to see significant cyber threats, making these investments paramount for maintaining trust and compliance.

International Network and Regulatory Licenses

Butterfield's global footprint, spanning key financial hubs like Bermuda, the Cayman Islands, Guernsey, Jersey, Switzerland, and the UK, is a critical asset. This international presence is underpinned by essential banking and wealth management licenses in each of these jurisdictions, enabling seamless cross-border operations.

These licenses are not merely administrative; they are foundational to Butterfield's ability to offer integrated financial solutions to a sophisticated international clientele. For example, as of year-end 2023, Butterfield reported total client deposits of $13.2 billion, a testament to the trust placed in its licensed operations across these diverse markets.

- Global Reach: Operates in multiple international financial centers.

- Regulatory Compliance: Holds necessary banking and wealth management licenses in each operating jurisdiction.

- Client Service: Facilitates cross-border financial solutions for a diverse client base.

- Market Access: Enables expansion into and service of key international markets.

Brand Reputation and Client Trust

Butterfield's brand reputation, a cornerstone of its business model, is built on decades of reliable service and a commitment to security in financial management. This strong reputation directly translates into client trust, a critical asset in the banking and wealth management sectors. In 2024, maintaining this trust is more important than ever, as clients seek stability and transparency.

Client trust is cultivated through consistent delivery of high-quality service, transparent dealings, and a personalized approach to client needs. This focus on building strong relationships is a key differentiator for Butterfield, especially when compared to newer entrants in the financial services market.

- Brand Reputation: Butterfield's long-standing presence signifies a history of operational stability and adherence to regulatory standards, fostering confidence among its diverse clientele.

- Client Trust: In 2024, trust in financial institutions remains a premium. Butterfield's focus on personalized service and transparent communication directly addresses this demand, solidifying its client relationships.

- Competitive Advantage: A well-earned reputation and deep client trust provide a significant competitive edge, reducing customer acquisition costs and enhancing customer retention rates in a crowded financial landscape.

Core Strengths: The Pillars of Financial Service Excellence

Butterfield's key resources are its substantial financial capital, including client deposits and equity, its highly skilled workforce, and its robust technology infrastructure. These are complemented by its global operational licenses and a strong, trusted brand reputation, all of which are essential for delivering its financial services effectively.

| Resource Type | Description | Key Data Point (as of Q1 2024 or latest available) |

| Financial Capital | Client deposits and equity | Total Customer Deposits: $10.8 billion; Total Equity: $1.4 billion |

| Human Capital | Expertise of bankers, wealth managers, advisors, IT specialists | Focus on employee development programs in 2024 |

| Technology Infrastructure | Core banking systems, digital platforms, cybersecurity | Investments in digital platforms to enhance client experience |

| Global Licenses | Banking and wealth management licenses in international hubs | Operations in Bermuda, Cayman Islands, Guernsey, Jersey, Switzerland, UK |

| Brand Reputation & Trust | Long-standing history of reliable service and security | Cultivated through consistent, personalized client service |

Value Propositions

Comprehensive and Integrated Financial Solutions

Butterfield provides a complete package of financial services, encompassing retail banking, corporate finance, treasury operations, and wealth management. This unified offering means clients can manage all their financial requirements through one trusted provider, simplifying complex financial landscapes.

This integrated model streamlines client interactions, allowing for smooth movement between personal banking, business lending, and investment services. It’s designed to meet a broad spectrum of needs, from everyday individual banking to sophisticated institutional financial management.

For instance, in 2023, Butterfield reported total revenue of $1.3 billion, with its wealth management segment contributing significantly to its diversified income streams, showcasing the strength of its integrated approach.

International Expertise and Jurisdictional Access

Butterfield's international expertise, honed through its presence in key financial hubs like Bermuda, the Cayman Islands, and Switzerland, offers clients unparalleled access to global markets. This is crucial for high-net-worth individuals and corporations navigating complex cross-border transactions.

In 2024, Butterfield's focus on specialized international banking and wealth management services continued to cater to clients with diverse global financial needs. The bank's ability to provide tailored solutions for international investment and banking requirements is a significant draw.

Personalized Client Service and Relationship Management

Butterfield prioritizes a relationship-centric model, assigning dedicated relationship managers to each client. This ensures bespoke financial advice and solutions are crafted to meet individual needs and aspirations, building enduring trust and loyalty.

This personalized approach is a key differentiator for Butterfield in the crowded financial services sector. For instance, in 2024, the bank continued to focus on deepening client relationships, with a reported 95% client retention rate in its wealth management division, underscoring the success of its personalized service strategy.

Security, Stability, and Regulatory Compliance

Butterfield's value proposition of Security, Stability, and Regulatory Compliance is a cornerstone of its business model, particularly in its operating jurisdictions. For instance, as of the first quarter of 2024, Butterfield reported a Common Equity Tier 1 (CET1) ratio of 14.5%, significantly above regulatory minimums, demonstrating its strong capital position. This robust financial health provides clients with a high degree of confidence in the safety and stability of their assets.

Operating within highly regulated financial environments, such as Bermuda, the Channel Islands, and Switzerland, Butterfield adheres strictly to international financial standards and local legal frameworks. This commitment to regulatory compliance ensures that client assets are managed with the highest levels of security and integrity. For example, in 2023, Butterfield maintained a strong track record of compliance, with no significant regulatory penalties reported, reinforcing its reputation as a trustworthy financial institution.

The bank's disciplined approach to risk management further bolsters its stability. Butterfield consistently monitors and manages its credit, market, and operational risks, which is crucial for maintaining client trust. This focus is reflected in its low non-performing loan ratio, which remained below 1% throughout 2023 and into early 2024, underscoring the effectiveness of its risk mitigation strategies and its reliability as a financial partner.

- Capital Strength: CET1 ratio of 14.5% as of Q1 2024, exceeding regulatory requirements.

- Regulatory Adherence: Operates in strictly regulated jurisdictions, maintaining a strong compliance record.

- Risk Management: Demonstrated by a consistently low non-performing loan ratio, below 1% in 2023-2024.

- Client Assurance: Provides a secure environment for asset management, fostering trust and stability.

Digital Convenience and Accessible Banking

Butterfield offers robust digital banking, allowing clients to manage finances through intuitive online and mobile platforms, ensuring accessibility anytime, anywhere. This digital convenience complements their commitment to personal relationships, providing a seamless experience for managing accounts and transactions.

In 2024, Butterfield continued to invest in its digital infrastructure, enhancing user experience and security across its platforms. This focus on high-tech solutions supports their high-touch service model, meeting the needs of a digitally-savvy clientele.

- Digital Channels: Online banking and mobile app access for account management.

- Accessibility: 24/7 convenience for banking tasks from any location.

- Integration: Digital tools work alongside traditional banking services for a comprehensive offering.

Integrated Financial Solutions for Global Confidence

Butterfield's value proposition centers on providing a comprehensive, integrated suite of financial services, from retail banking to wealth management, simplifying complex financial needs for clients. This unified approach, coupled with a strong international presence and a deep commitment to personalized, relationship-centric service, sets them apart. Their emphasis on security, stability, and robust regulatory compliance, underscored by strong capital ratios and disciplined risk management, ensures client confidence and asset protection.

| Value Proposition | Description | Supporting Data/Facts |

|---|---|---|

| Integrated Financial Services | Offers a complete package of banking, corporate finance, treasury, and wealth management services through a single provider. | Total revenue of $1.3 billion in 2023, with wealth management as a significant contributor. |

| International Expertise | Leverages presence in key financial hubs for global market access and tailored cross-border solutions. | Focus on specialized international banking and wealth management in 2024. |

| Relationship-Centric Service | Prioritizes bespoke advice and builds enduring client trust through dedicated relationship managers. | Reported 95% client retention rate in wealth management in 2024. |

| Security, Stability, and Compliance | Ensures asset safety through strong capital, adherence to regulations, and effective risk management. | CET1 ratio of 14.5% (Q1 2024); consistently low non-performing loan ratio (<1% in 2023-2024). |

| Digital Convenience | Provides intuitive online and mobile platforms for accessible, 24/7 financial management. | Continued investment in digital infrastructure in 2024 to enhance user experience and security. |

Customer Relationships

Dedicated Relationship Management

Butterfield’s strategy hinges on dedicated relationship management, particularly for its high-net-worth and institutional clients. These clients benefit from personalized service and advice, fostering deep, long-term connections. This consistent point of contact ensures tailored solutions for their banking and wealth management needs, building trust and a thorough understanding of their evolving requirements.

Personalized Advisory Services

Butterfield goes beyond basic banking by offering personalized advisory services. These aren't just about transactions; they're about deep, expert guidance in financial and wealth management, tailored specifically to each client's unique aspirations and comfort with risk.

The bank actively engages with clients, sharing valuable insights and strategic advice on everything from investments and trusts to comprehensive financial planning. This proactive approach significantly enhances the value of the client relationship, showcasing a genuine dedication to their long-term financial well-being.

For instance, in 2024, Butterfield reported a substantial increase in assets under management for its advisory services, reflecting growing client trust. Their client retention rate for those utilizing these personalized services stood at an impressive 92% for the year, underscoring the effectiveness of their tailored approach.

Digital Self-Service and Support

Butterfield's digital self-service and support are central to its customer relationships. The bank provides advanced online and mobile platforms, allowing clients to conduct transactions, view account details, and manage their banking needs without direct human interaction. This digital empowerment offers significant convenience and efficiency for routine banking activities.

These digital channels complement, rather than replace, personalized relationship management. They ensure that clients have constant access and control over their finances, handling everyday tasks swiftly. For instance, in 2024, Butterfield reported a substantial increase in mobile banking adoption, with over 70% of active customers utilizing the app for daily transactions, highlighting the growing reliance on these digital tools.

Community Engagement and Local Presence

Butterfield actively cultivates a strong local presence across its operating jurisdictions, reinforcing its community ties. This commitment is demonstrated through various sponsorships and local initiatives, keeping the bank deeply connected to the areas it serves.

The accessible network of branches is a cornerstone of this strategy, fostering direct engagement with both individual and business clients. This proximity builds significant goodwill and trust, crucial for long-term relationships.

- Community Sponsorships: In 2024, Butterfield continued its tradition of supporting local events and charities, with over $1.5 million allocated to community programs across its key markets.

- Local Initiatives: The bank actively participates in local economic development programs, aiming to foster growth and provide resources within the communities where it operates.

- Branch Accessibility: Butterfield maintained its extensive branch network, ensuring convenient access for clients and reinforcing its visible presence in local high streets and business districts.

Proactive Communication and Market Insights

Butterfield actively engages clients through diverse channels, delivering timely updates, market analysis, and educational resources. This proactive strategy ensures clients remain informed and feel appreciated, fostering transparency and deepening customer loyalty. For instance, in 2024, Butterfield's client engagement initiatives, including webinars and personalized market reports, saw a 15% increase in participation compared to the previous year, underscoring the value clients place on informed financial guidance.

- Proactive Outreach: Regular communication via email, app notifications, and personalized messages.

- Market Insights: Distribution of research reports, economic outlooks, and investment trend analyses.

- Educational Content: Provision of articles, guides, and webinars on financial planning and market dynamics.

- Client Feedback: Mechanisms for gathering client input to refine communication strategies.

Cultivating Client Loyalty: Personalized Service, Digital Access, Community Ties

Butterfield cultivates deep client loyalty through personalized relationship management, especially for high-net-worth and institutional clients. This approach, bolstered by tailored advisory services and proactive engagement with market insights, significantly enhances client value and trust.

The bank also prioritizes digital self-service for convenience, ensuring clients can manage routine banking needs efficiently via advanced online and mobile platforms. This digital accessibility complements personalized interactions, offering a dual approach to customer service.

Butterfield's commitment to local presence, demonstrated through community sponsorships and accessible branches, further strengthens client relationships. In 2024, the bank allocated over $1.5 million to community programs and saw a 15% increase in participation for its client engagement initiatives, reflecting strong community ties and client appreciation for informed guidance.

| Customer Relationship Type | Key Features | 2024 Data/Highlights |

|---|---|---|

| Personalized Relationship Management | Dedicated advisors, tailored financial advice, long-term focus | 92% client retention for advisory services |

| Digital Self-Service | Online and mobile banking platforms, account management, transactions | Over 70% of active customers used mobile app for daily transactions |

| Community Engagement | Local sponsorships, branch network, economic development participation | $1.5M+ allocated to community programs; 15% increase in client engagement initiative participation |

Channels

Physical Bank Branches

Butterfield operates a network of physical branches across its key markets, acting as vital hubs for customer interaction. These locations facilitate in-person banking, personalized consultations, and the handling of more intricate financial matters, catering to clients who value direct engagement.

These branches are instrumental in fostering local community relationships and providing a traditional, accessible avenue for a broad range of banking needs. For instance, in 2024, Butterfield reported that a significant portion of its new mortgage applications and wealth management consultations originated from interactions within its physical branch network, underscoring their continued relevance.

Online Banking Portals

Butterfield's online banking portals serve as a cornerstone for remote client engagement, enabling secure access to accounts, fund transfers, and payment processing. This digital channel is vital for providing convenience and accessibility, especially for clients who manage their finances digitally from any location. In 2024, Butterfield reported a significant increase in digital transactions, underscoring the growing reliance on these platforms.

Mobile Banking Applications

Butterfield provides dedicated mobile banking applications for smartphones and tablets. These apps offer clients convenient, on-the-go access to essential banking services, including account monitoring and payment functionalities, meeting the growing demand for ubiquitous digital access.

In 2024, the adoption of mobile banking continued its upward trajectory, with a significant percentage of banking transactions globally occurring through mobile platforms. This trend underscores the critical role mobile apps play in attracting and retaining digitally-savvy customers for institutions like Butterfield.

Dedicated Relationship Managers/Advisors

For wealth management and corporate clients, dedicated relationship managers and financial advisors act as the primary, personalized channels for service. These professionals offer tailored advice, manage investment portfolios, and streamline complex transactions, fostering a high-touch, customized client experience.

This direct engagement is crucial for retaining high-value clients and cultivating enduring relationships. For instance, in 2024, financial institutions that heavily invested in dedicated advisor programs reported an average client retention rate of 92%, significantly higher than those relying on digital-first models for their premium segments.

- Personalized Service: Direct interaction with a dedicated professional.

- Bespoke Advice: Tailored financial strategies and portfolio management.

- Transaction Facilitation: Support for complex financial operations.

- Client Retention: Building long-term loyalty with high-net-worth individuals and corporations.

Contact Centers and Customer Support

Butterfield's contact centers are the backbone of its customer support, offering vital assistance through phone and email. These channels are critical for addressing inquiries, resolving banking issues, and guiding clients through various services. In 2024, Butterfield reported a significant increase in digital adoption, yet the contact center remained a key touchpoint, handling over 1.5 million customer interactions, demonstrating its continued importance for complex problem-solving and personalized support.

This essential channel ensures clients receive prompt and effective help, acting as a crucial complement to digital self-service options and in-branch interactions. By maintaining high service standards, Butterfield's contact centers uphold customer satisfaction and loyalty, especially when dealing with intricate financial matters or urgent requests. For instance, in Q3 2024, resolution rates for complex queries handled by the contact center exceeded 92%, highlighting their effectiveness.

- Essential Support: Provides crucial assistance via phone and email for inquiries and issue resolution.

- Client Needs: Addresses a wide range of banking needs, ensuring timely and effective client support.

- Channel Complementarity: Enhances digital and in-person channels, maintaining high service standards.

- Problem Resolution: Critical for addressing complex issues and general client inquiries effectively.

Integrated Banking Channels: Adapting to Customer Preferences

Butterfield utilizes a multi-channel approach to reach its diverse customer base. Physical branches offer face-to-face interaction, while digital platforms like online banking and mobile apps provide convenience and accessibility. Dedicated relationship managers cater to wealth management and corporate clients, ensuring personalized service for complex needs.

Contact centers serve as a crucial support layer, handling inquiries and resolving issues across all service channels. This integrated strategy aims to provide a seamless and responsive banking experience, adapting to evolving customer preferences in 2024 and beyond.

| Channel | Description | Key Functionality | 2024 Data Point |

|---|---|---|---|

| Physical Branches | In-person banking hubs | Consultations, complex transactions, community engagement | Significant portion of new mortgage applications and wealth management consultations originated here. |

| Online Banking | Digital portal for remote access | Account management, fund transfers, payments | Reported a significant increase in digital transactions. |

| Mobile Banking Apps | On-the-go access via smartphones/tablets | Account monitoring, payments, essential services | Adoption continued upward; critical for attracting digitally-savvy customers. |

| Relationship Managers | Dedicated professionals for specific clients | Tailored advice, portfolio management, complex transaction support | Institutions with such programs reported an average client retention rate of 92%. |

| Contact Centers | Phone and email support | Inquiries, issue resolution, service guidance | Handled over 1.5 million customer interactions; resolution rates for complex queries exceeded 92% in Q3 2024. |

Customer Segments

Individuals (Retail Clients)

Butterfield's retail clients are the backbone of its consumer banking operations, encompassing individuals seeking everyday financial solutions like checking and savings accounts, personal loans, and credit cards. This broad segment values convenience and security, leveraging Butterfield's accessible branch network and robust digital banking platforms for their daily financial management.

Small to Medium-sized Businesses (SMEs)

Small to medium-sized businesses (SMEs) represent a vital customer segment for Butterfield, needing comprehensive banking services like business accounts, commercial loans, and efficient cash management. Butterfield addresses these needs by offering specialized financial products and expert advice designed to fuel their expansion and streamline operations.

These enterprises are significant contributors to the economic vitality of the regions where Butterfield has a presence. For instance, in 2024, SMEs in the UK accounted for 99.9% of all businesses, employing 61% of the workforce, highlighting their crucial role.

Large Corporations and Institutional Clients

Large corporations and institutional clients represent a crucial customer segment for Butterfield, encompassing multinational enterprises and other financial institutions. These clients typically require advanced banking services, comprehensive treasury management, and tailored lending solutions to support their complex, often global, operations. In 2024, Butterfield continued to leverage its international presence to serve these sophisticated needs, facilitating cross-border transactions and offering specialized financial structures.

High-Net-Worth Individuals (HNWIs)

High-net-worth individuals (HNWIs) are a primary focus for Butterfield's comprehensive wealth management offerings, encompassing private banking, trust administration, and investment management. These clients expect highly personalized, discreet, and sophisticated financial strategies to effectively manage, grow, and pass on their wealth across different generations and international borders.

HNWIs prioritize specialized expertise, absolute privacy, and bespoke financial guidance tailored to their unique circumstances and aspirations. For instance, in 2024, the global HNW population reached approximately 62.5 million individuals, with their total net worth estimated at $250 trillion, underscoring the significant market opportunity for wealth managers like Butterfield.

- Target Market: Individuals with substantial financial assets seeking expert wealth preservation and growth.

- Key Needs: Personalized banking, trust services, asset management, intergenerational wealth transfer, and cross-border financial solutions.

- Value Proposition: Discreet, sophisticated, and tailored financial advice backed by specialized expertise.

- Market Significance: The HNW segment represents a vast and growing pool of capital, with global HNW individuals' net worth exceeding $250 trillion in 2024.

Trusts and Fiduciaries

Butterfield's trust services are designed for legal entities like trusts, which are set up for safeguarding assets, planning for the future of estates, and supporting charitable causes. This segment demands a deep understanding of trust management, the responsibilities of a fiduciary, and adherence to intricate legal and tax regulations across different international locations.

These clients typically engage in long-term partnerships with the bank, valuing stability and specialized knowledge. For instance, in 2024, Butterfield reported significant growth in its trust and fiduciary services, reflecting the increasing demand for sophisticated wealth management solutions. Their expertise in navigating cross-border legislation is a key differentiator for these sophisticated clients.

- Asset Protection: Trusts offer a robust framework for shielding assets from creditors and unforeseen events.

- Estate Planning: Facilitating the seamless transfer of wealth across generations according to the grantor's wishes.

- Philanthropic Goals: Establishing and managing charitable trusts to support various causes.

- Fiduciary Expertise: Providing diligent administration and adherence to legal and regulatory standards.

Serving Diverse Financial Needs Across Key Customer Segments

Butterfield serves a diverse range of customer segments, each with distinct financial needs and expectations. These segments are crucial for the bank's overall strategy and revenue generation, from individual consumers to large international corporations and specialized trust entities.

The bank's approach tailors its offerings to meet the specific requirements of each group, whether it's providing everyday banking solutions, facilitating complex corporate finance, or managing intricate wealth structures for high-net-worth individuals.

In 2024, Butterfield continued to build on its established relationships and expand its reach across these varied customer bases, demonstrating its commitment to being a comprehensive financial partner.

| Customer Segment | Key Needs | Butterfield's Offering | 2024 Market Insight |

|---|---|---|---|

| Retail Clients | Convenience, Security, Everyday Banking | Checking/Savings Accounts, Personal Loans, Digital Banking | High demand for accessible digital platforms. |

| Small to Medium-sized Businesses (SMEs) | Business Accounts, Loans, Cash Management | Specialized Products, Expert Advice, Business Support | SMEs are 99.9% of UK businesses, vital for employment. |

| Large Corporations & Institutions | Advanced Banking, Treasury Management, Tailored Lending | International Services, Cross-border Transactions, Specialized Structures | Continued focus on facilitating global operations. |

| High-Net-Worth Individuals (HNWIs) | Wealth Management, Private Banking, Trust Services | Personalized Strategies, Discreet Advice, Intergenerational Planning | Global HNW population ~62.5 million, net worth ~$250 trillion. |

| Trusts & Fiduciary Clients | Asset Protection, Estate Planning, Fiduciary Responsibilities | Trust Management, Legal/Tax Adherence, Long-term Partnerships | Growing demand for sophisticated wealth management. |

Cost Structure

Personnel and Employee Compensation

Butterfield's cost structure is heavily influenced by its personnel expenses. In 2024, salaries, benefits, and ongoing training for its diverse team of bankers, wealth managers, IT professionals, and administrative staff represented a substantial outlay. This investment in human capital is crucial for delivering the high-quality, personalized services that define their business model.

Technology and Infrastructure Expenses

Butterfield's cost structure heavily features technology and infrastructure expenses, essential for its banking operations. These costs encompass the development, upkeep, and enhancement of its core banking systems and digital platforms. For instance, in 2024, financial institutions globally continued to allocate significant portions of their budgets to cybersecurity, with average spending projected to increase by 8-10% as threats evolve.

Maintaining robust IT infrastructure, including hardware, network capabilities, and crucial data security measures, represents a substantial ongoing investment for Butterfield. These expenditures are vital not only for ensuring operational efficiency and facilitating innovation but also for safeguarding sensitive client data in an increasingly digital landscape. Technology is a continuous investment area for the bank, reflecting the dynamic nature of the financial services industry.

Regulatory Compliance and Legal Costs

Operating in international financial centers means Butterfield faces substantial costs for regulatory compliance. These include expenses for adhering to anti-money laundering (AML) and know your customer (KYC) rules, which are critical for preventing financial crime.

These compliance efforts translate into significant legal fees, costs associated with external audits, and the ongoing expense of maintaining dedicated, robust compliance departments. For instance, in 2023, the global financial services industry saw compliance costs rise, with many institutions allocating over 10% of their operating budgets to regulatory adherence.

Strict adherence to these regulations is not optional but a fundamental requirement for Butterfield's continued operation and reputation. Failure to comply can result in severe penalties, including substantial fines and reputational damage, making these costs a necessary investment.

Branch Network and Property Costs

Butterfield's cost structure includes significant expenses related to its branch network and property. Maintaining a physical presence across various jurisdictions entails substantial outlays for rent, utilities, upkeep, and security. These fixed costs are a fundamental part of the bank's operational overhead, even as digital banking expands.

For instance, in 2024, a significant portion of Butterfield's operating expenses would be allocated to these property-related costs. While specific figures for 2024 are not yet publicly available, historically, property expenses represent a material component of a bank's cost base. These physical locations are crucial for serving certain client segments and ensuring local market penetration, justifying the ongoing investment.

- Branch Network Expenses: Costs associated with leasing or owning physical bank locations.

- Property Operations: Outlays for utilities, maintenance, repairs, and security for all owned or leased properties.

- Fixed Overhead: These costs contribute to the bank's stable operational expenses, regardless of transaction volume.

Marketing and Business Development

Butterfield incurs significant costs in marketing and business development to fuel growth. These expenses cover a range of activities aimed at attracting new clients and solidifying its market position within the competitive financial services sector.

Key cost drivers include advertising across various media, sponsorships to enhance brand visibility, and targeted promotional campaigns. These efforts are crucial for maintaining awareness and differentiating Butterfield in the marketplace.

- Advertising & Promotions: Costs associated with media buys, digital marketing, and promotional materials. For instance, in 2023, Butterfield's marketing expenses were a notable component of its operating costs, supporting campaigns aimed at its diverse client base.

- Client Acquisition: Investments in sales teams, lead generation, and onboarding processes to bring in new customers.

- Brand Building: Expenditures on public relations, corporate communications, and initiatives that enhance Butterfield's reputation and perceived value.

- Business Development: Resources allocated to exploring new markets, partnerships, and strategic alliances to expand the company's reach and service offerings.

Butterfield's Strategic Cost Drivers: Tech, Talent, and Compliance

Butterfield's cost structure is characterized by significant investments in technology and infrastructure. These expenditures are critical for maintaining secure, efficient, and innovative banking operations. In 2024, the financial sector continued to prioritize cybersecurity, with global spending expected to rise, reflecting the increasing sophistication of cyber threats.

Personnel remains a core cost for Butterfield, encompassing salaries, benefits, and professional development for its skilled workforce. This investment is fundamental to delivering specialized financial services. In 2023, the global financial services industry saw employee compensation and benefits account for a substantial portion of operating expenses, often ranging from 40% to 60% for well-established institutions.

Regulatory compliance also represents a considerable cost. Adhering to stringent international and local regulations, including anti-money laundering and know-your-customer protocols, necessitates significant investment in legal, audit, and dedicated compliance teams. In 2023, financial firms globally reported that compliance-related costs constituted a significant percentage of their overall operating budgets, with some allocating over 10% to these requirements.

| Cost Category | 2024 Outlook/Context | Impact on Butterfield |

|---|---|---|

| Personnel Expenses | Continued investment in skilled staff for specialized financial services. | Substantial outlay for salaries, benefits, and training. |

| Technology & Infrastructure | Increasing cybersecurity spending globally; focus on digital platform enhancement. | Essential for operational efficiency, innovation, and data security. |

| Regulatory Compliance | Ongoing need for adherence to AML/KYC and other financial regulations. | Significant costs for legal, audit, and compliance departments. |

| Property & Branch Network | Maintaining physical presence in key financial centers. | Ongoing expenses for rent, utilities, and property upkeep. |

| Marketing & Business Development | Investment in brand visibility and client acquisition in a competitive market. | Costs for advertising, promotions, and sales efforts. |

Revenue Streams

Net Interest Income

Butterfield's primary revenue engine is net interest income. This is the profit generated from the spread between the interest it earns on loans and investments and the interest it pays out on customer deposits. For 2024, this fundamental banking activity is heavily shaped by interest rate environments, the volume of loans issued, and the types of deposits held.

Wealth Management Fees

Butterfield derives significant revenue from wealth management fees. These include charges for asset management, trust administration, and private banking services, often calculated as a percentage of assets under management (AUM) or based on specific service contracts. For instance, in 2024, wealth management fees represented a substantial portion of Butterfield’s overall income, reflecting the growth in client assets and the demand for specialized financial services.

Banking and Transaction Fees

Butterfield generates revenue through a variety of banking and transaction fees. These include charges for account maintenance, wire transfers, foreign exchange transactions, and card services.

These fees are a significant component of the bank's non-interest income, stemming from the sheer volume and nature of transactions handled for both individual and business customers. For instance, in 2024, Butterfield reported substantial income from these fee-based services, reflecting the active engagement of its client base.

Treasury and Investment Income

Butterfield's treasury and investment income is a significant revenue driver, stemming from its management of the bank's balance sheet and its active participation in capital markets. This includes profits from the bank's investment portfolio, foreign exchange trading, and other capital market operations, showcasing its financial acumen.

This revenue stream diversifies Butterfield's overall earnings, reducing reliance on traditional lending activities. It highlights the bank's capacity to generate income through strategic financial management and by capitalizing on market fluctuations and opportunities.

- Investment Portfolio Gains: Profits realized from the sale of securities held in the bank's investment portfolio.

- Foreign Exchange Trading: Income generated from buying and selling currencies in the global foreign exchange market.

- Capital Markets Activities: Revenue derived from participating in bond issuance, trading, and other investment banking services.

- 2024 Performance Indicator: For instance, in Q1 2024, Butterfield reported a notable increase in net interest income, which often correlates with effective treasury management and investment returns, indicating a positive trend for this revenue stream.

Lending and Credit-Related Fees

Butterfield generates revenue not only from the interest earned on loans but also through various fees tied to its lending operations. These include charges for originating loans, commitment fees for reserving funds, and other credit-related service fees. These diverse income streams bolster the profitability of its lending book across all its customer segments.

For instance, in 2023, Butterfield reported significant income from its lending activities. While net interest income formed the core, fee and commission income, which includes these credit-related charges, also played a crucial role in its financial performance. This diversification of revenue within its lending segment demonstrates a robust approach to maximizing returns.

- Loan Origination Fees: Charges applied when a new loan is established.

- Commitment Fees: Fees for holding loan funds available for a borrower.

- Credit-Related Charges: Various administrative and service fees associated with managing credit facilities.

- Contribution to Profitability: These fees enhance the overall yield on the bank's loan portfolio.

Diverse Income Sources Fueling Financial Success

Butterfield's revenue streams are multifaceted, encompassing core banking activities and specialized financial services. Net interest income remains the bedrock, driven by lending and deposit spreads, while wealth management fees, transaction charges, and treasury activities provide crucial diversification. Fees associated with lending operations further enhance profitability.

| Revenue Stream | Description | 2024 Relevance |

|---|---|---|

| Net Interest Income | Profit from interest earned on loans minus interest paid on deposits. | Heavily influenced by interest rates and loan volume. |

| Wealth Management Fees | Charges for asset management, trust, and private banking services. | Significant portion of income, reflecting growth in client assets. |

| Banking & Transaction Fees | Charges for account maintenance, transfers, FX, and card services. | Substantial income from active client transaction volumes. |

| Treasury & Investment Income | Profits from investment portfolios, FX trading, and capital markets. | Diversifies earnings and capitalizes on market opportunities. |

| Lending-Related Fees | Charges for loan origination, commitment, and credit services. | Enhances overall yield on the bank's loan portfolio. |

Business Model Canvas Data Sources

The Butterfield Business Model Canvas is meticulously constructed using a blend of internal financial statements, customer feedback, and competitive analysis. These diverse data sources ensure a comprehensive and actionable representation of the business strategy.