British Land Company Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

British Land Company Bundle

From Overview to Strategy Blueprint

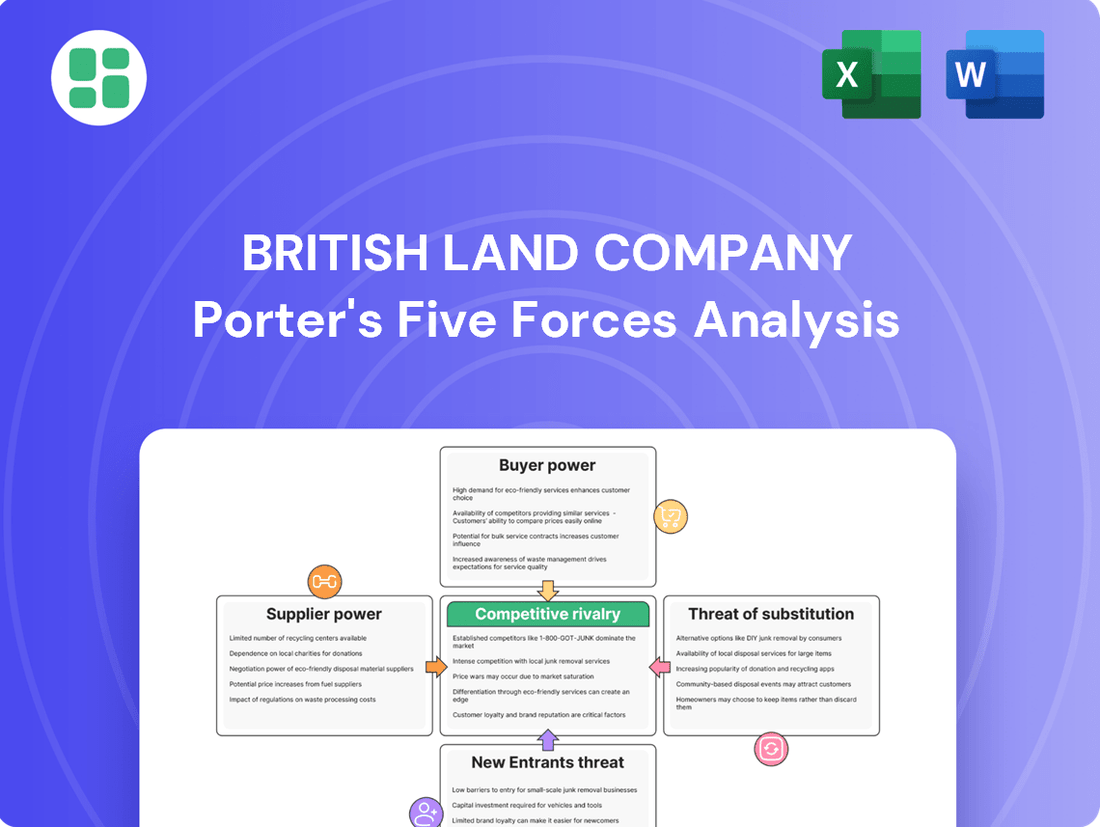

Porter's Five Forces analysis reveals that British Land Company faces moderate bargaining power from buyers due to the availability of alternative commercial properties. The threat of new entrants is also a significant factor, as the real estate market can attract new developers. Understanding these dynamics is crucial for strategic planning.

The complete report reveals the real forces shaping British Land Company’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Concentration of Specialised Contractors

The market for highly specialized construction services, crucial for British Land's urban regeneration and sustainable building projects, often has a limited pool of qualified contractors. This scarcity can give these suppliers substantial bargaining power, especially for large, custom developments where changing contractors mid-project is costly and complex. Their unique skills and capacity allow them to negotiate premium pricing and more advantageous terms.

Availability of Prime Land Parcels

Landowners, particularly those controlling prime development sites in desirable urban centers or key logistics areas, wield significant bargaining power. For British Land, this scarcity and the unique attributes of these parcels can translate to fewer viable alternatives, thus driving up acquisition costs. In 2024, prime commercial land in London, for instance, continued to command premium prices, with average per-square-foot costs remaining exceptionally high, reflecting this inherent scarcity and demand.

Cost of Raw Materials Volatility

The cost of raw materials like steel, concrete, and timber is subject to considerable volatility. Global commodity market swings, unforeseen supply chain interruptions, and evolving trade agreements can all lead to significant price fluctuations for these essential construction inputs. For British Land, this means that the cost of developing new projects can be directly impacted by the ability of its suppliers to pass on these increased costs, affecting overall project profitability and development budgets.

Access to Development Finance

Financial institutions that provide development finance are key suppliers for British Land, influencing project feasibility through their lending terms. Their power is significant because real estate development requires substantial capital, and these institutions control crucial aspects like interest rates and loan covenants. For instance, during periods of economic slowdown, such as the cautious lending environment observed in early 2024, banks may tighten credit availability, potentially increasing the cost of capital for developers like British Land.

The bargaining power of these financial suppliers is amplified by the capital-intensive nature of the real estate sector. Access to development finance dictates the scale and pace of new projects. In 2024, the cost of borrowing remained a significant factor, with central bank policy rates influencing the overall cost of debt for companies like British Land. This means that the terms offered by lenders can directly impact project profitability and the company's strategic expansion plans.

- Access to Development Finance: Banks and investment funds are critical suppliers, providing the capital necessary for large-scale property development.

- Lending Terms and Interest Rates: Suppliers' bargaining power is derived from their ability to set interest rates, repayment schedules, and loan covenants, directly affecting British Land's financing costs.

- Economic Sensitivity: In tighter credit markets or periods of economic uncertainty, such as those experienced in late 2023 and early 2024, lenders can impose more stringent conditions, potentially hindering British Land's project funding.

- Impact on Project Viability: The cost and availability of development finance are paramount, influencing British Land's capacity to initiate and complete new developments and manage its portfolio growth.

Reliance on Specialist Consultants

British Land's reliance on specialist consultants, such as architects and urban planners, can grant these firms significant bargaining power. This is particularly true when their expertise is niche or highly sought after, as seen in the growing demand for sustainability consultants in the real estate sector.

The limited availability of top-tier consultants with proven track records in complex projects, like large-scale urban regeneration, can drive up fees and reduce negotiation flexibility for British Land. For instance, in 2024, the average day rate for senior architectural consultants in the UK saw an increase of approximately 5-7% compared to the previous year, reflecting this demand.

- Niche Expertise: Consultants specializing in areas like ESG (Environmental, Social, and Governance) compliance or advanced BIM (Building Information Modeling) possess unique skills that are in high demand.

- Reputation and Track Record: Firms with a strong history of successful, high-profile developments command premium pricing and terms.

- Limited Supply: The pool of truly expert consultants in specialized fields is finite, intensifying their bargaining position.

Supplier Power: Impacting Development Costs

Suppliers of specialized construction services and prime development land hold considerable sway over British Land due to scarcity and unique attributes. For instance, in 2024, prime London commercial land prices remained exceptionally high, underscoring the power of landowners. Similarly, the limited pool of contractors with expertise in complex urban regeneration projects allows them to command premium pricing and favorable terms, directly impacting project costs for British Land.

The bargaining power of raw material suppliers, such as those providing steel and concrete, is amplified by market volatility. Global commodity price swings and supply chain disruptions in 2024 directly translated into increased input costs for developers. Furthermore, financial institutions acting as capital suppliers wield significant influence through lending terms and interest rates, particularly in tighter credit markets observed in early 2024, which can affect project feasibility and expansion plans.

| Supplier Type | Key Bargaining Factors | Impact on British Land | 2024 Data Point |

|---|---|---|---|

| Specialized Contractors | Niche expertise, project complexity, limited availability | Higher project costs, less negotiation flexibility | Average day rate for senior architectural consultants increased 5-7% |

| Landowners | Prime location, unique site attributes, scarcity | Increased land acquisition costs | Prime London commercial land prices remained exceptionally high |

| Raw Material Suppliers | Commodity price volatility, supply chain disruptions | Fluctuating development costs, potential impact on profitability | Steel prices saw moderate fluctuations throughout 2024 due to global demand shifts |

| Financial Institutions | Lending terms, interest rates, credit availability | Cost of capital, project financing feasibility | Central bank policy rates influenced borrowing costs for developers in 2024 |

What is included in the product

Analyzes the competitive intensity within the UK real estate sector, focusing on British Land's exposure to buyer power, supplier leverage, new entrants, substitutes, and rivalry.

Effortlessly identify and mitigate competitive threats by visualizing the intensity of each of Porter's Five Forces for British Land.

Gain a strategic advantage by quickly assessing the impact of supplier power and buyer bargaining on British Land's profitability.

Customers Bargaining Power

Tenant Market Conditions

The bargaining power of British Land's tenants, across retail, office, and urban logistics, is deeply tied to prevailing market conditions. When vacancy rates are high or there's an excess of a particular property type, tenants gain more sway to push for reduced rents, rent-free incentives, or more adaptable lease agreements. For instance, as of early 2024, the London office market saw a vacancy rate hovering around 9-10%, giving tenants more room to negotiate terms, particularly for older or less desirable spaces.

Diversification of Tenant Base

British Land’s diverse property portfolio, spanning campuses, retail, and urban logistics, significantly dilutes the bargaining power of any single customer group. This broad tenant base across various industries and scales means the company isn't overly dependent on a handful of major tenants. For instance, as of their latest reports, a substantial portion of their rental income comes from a wide array of occupiers, preventing any one tenant from dictating terms due to their sheer size.

Switching Costs for Tenants

While tenants might have several office space options, the practicalities of moving are significant. Consider that for a business, relocating involves substantial expenses like fitting out a new space, the inevitable disruption to daily operations, and the cost of marketing their new address. For example, in 2024, the average fit-out cost per square foot in prime London office markets, where British Land is a major player, can range from £60 to £100, adding considerably to the overall expense of a move.

These considerable switching costs effectively dampen the bargaining power of current tenants. It means they are less inclined to uproot their business simply for a small reduction in rent. This tenant inertia is a valuable asset for British Land, allowing them to better secure lease renewals and maintain consistent occupancy levels across their portfolio.

Demand for High-Quality, Sustainable Space

Customers are increasingly seeking out properties that offer not just space, but also high quality, a wealth of amenities, and strong sustainability credentials. British Land is actively catering to this demand by investing in the development and management of such spaces. For instance, in 2024, they continued to focus on their portfolio's sustainability, with a significant portion of their portfolio holding BREEAM ratings of Excellent or Very Good.

When tenants prioritize these sought-after features, the availability of truly comparable alternatives can be scarce. This scarcity inherently limits their ability to negotiate aggressively on price or terms, thereby reducing their bargaining power. British Land's strategic focus on creating desirable, well-managed environments enhances its differentiation in the market.

- Customer Demand: Growing preference for high-quality, amenity-rich, and sustainable office and retail spaces.

- Limited Alternatives: Scarcity of truly comparable properties reduces tenant leverage.

- British Land's Strategy: Investment in differentiation through superior space design and management.

- Pricing Power: Enhanced ability to command favorable pricing from discerning tenants.

Impact of E-commerce on Retail Tenants

The increasing prevalence of e-commerce has undeniably amplified the bargaining power of retail tenants. As consumers increasingly opt for online shopping, physical stores experience reduced footfall, putting pressure on retailers' profitability. This financial strain compels tenants to negotiate more favorable lease agreements with landlords like British Land, seeking concessions such as flexible lease terms, rent structures tied to turnover, or reduced physical space requirements.

British Land, in response to this evolving retail landscape, must strategically adapt its offerings. To retain and attract tenants, the company needs to focus on creating engaging, experiential retail environments that draw customers into physical spaces. Furthermore, integrating robust omnichannel strategies that seamlessly connect online and offline shopping experiences will be crucial to supporting the success of its retail partners.

- E-commerce Growth: Online retail sales in the UK reached an estimated £73.7 billion in 2023, representing a significant portion of total retail expenditure.

- Tenant Demands: Retailers are increasingly seeking shorter lease lengths and turnover-based rent agreements to mitigate risks associated with fluctuating consumer behaviour.

- Experiential Retail: A 2024 survey indicated that over 60% of consumers are more likely to visit a physical store if it offers unique experiences beyond just product availability.

- Omnichannel Integration: Retailers successfully leveraging click-and-collect services and in-store returns for online purchases reported an average 15% increase in customer loyalty.

Tenant Leverage: Market Forces vs. Strategic Property Value

The bargaining power of British Land's customers, primarily tenants, is influenced by market dynamics and their own strategic needs. While high vacancy rates can empower tenants to negotiate better terms, British Land's diversified portfolio across sectors like office, retail, and urban logistics spreads this risk. The significant costs associated with relocation, including fit-outs estimated at £60-£100 per square foot in prime London markets in 2024, create switching costs that anchor tenants and reduce their leverage.

Furthermore, tenants increasingly demand high-quality, sustainable, and amenity-rich spaces, a trend British Land is actively addressing. For instance, a substantial portion of their portfolio held BREEAM ratings of Excellent or Very Good in 2024. This focus on differentiation means that for tenants prioritizing these features, truly comparable alternatives are scarce, limiting their ability to drive down prices.

The retail sector faces unique pressures due to e-commerce growth, with online sales reaching an estimated £73.7 billion in the UK in 2023. This environment pushes retailers to seek flexible leases and turnover-based rents. However, a 2024 survey found over 60% of consumers favor stores offering unique experiences, highlighting British Land's strategy to create engaging environments that can mitigate tenant bargaining power.

| Factor | Impact on Tenant Bargaining Power | British Land's Mitigation Strategy |

|---|---|---|

| Market Vacancy Rates (e.g., London Office ~9-10% in early 2024) | Increases tenant leverage for concessions. | Diversified portfolio reduces reliance on single market segments. |

| Switching Costs (e.g., Fit-out costs £60-£100/sq ft in prime London 2024) | Decreases tenant willingness to relocate for minor gains. | Focus on long-term tenant relationships and portfolio quality. |

| Demand for Quality & Sustainability (e.g., BREEAM Excellent/Very Good in 2024) | Creates scarcity of comparable alternatives, reducing tenant leverage. | Strategic investment in high-quality, amenity-rich, and sustainable developments. |

| E-commerce Growth (UK online sales £73.7bn in 2023) | Increases pressure on retail tenants for flexible terms. | Development of experiential retail and omnichannel support for tenants. |

What You See Is What You Get

British Land Company Porter's Five Forces Analysis

The document you see here is the complete, professionally written Porter's Five Forces Analysis of the British Land Company, exactly as you will receive it upon purchase. This detailed analysis covers all five forces, providing actionable insights into the competitive landscape and strategic positioning of British Land. You can trust that what you preview is precisely what you will download, ready for immediate use in your business strategy or research.

Rivalry Among Competitors

Presence of Major UK REITs and Developers

The UK property market, especially for commercial real estate, is a crowded space with major players like Landsec, Segro, and Hammerson. These established REITs and developers are constantly vying for the same prime spots and types of properties.

This intense competition means British Land Company faces significant rivalry for acquiring land and development projects. For instance, in 2023, the UK commercial property market saw transaction volumes fluctuate, with significant investment activity in sectors like logistics and retail, areas where major REITs are active.

Such rivalry can push up the cost of land acquisition and put downward pressure on rental income growth as companies compete for desirable tenants. This dynamic directly impacts profitability and strategic positioning for companies like British Land.

Fragmented Ownership in Specific Segments

While the market for large, institutional-grade properties might see fewer players, certain niches within the UK property sector are characterized by a more fragmented ownership structure. This means numerous smaller developers and private investors are actively competing, particularly for smaller-scale projects or specialized properties.

This fragmentation can significantly ramp up rivalry in these specific segments. For British Land, this necessitates leveraging its considerable expertise, robust financial backing, and established reputation to stay ahead. The intensity of competition is not uniform across the board; it shifts based on the specific asset class and the geographical location of the property.

Capital-Intensive Nature of the Industry

The property development and investment sector demands substantial capital for land acquisition, construction, and property management. This capital intensity acts as a barrier for new entrants, but for established players like British Land, it means a constant need to secure funding and identify profitable ventures. In 2024, the UK commercial property market saw significant investment, with total investment volumes reaching an estimated £40 billion, highlighting the scale of capital deployed.

Differentiation Through Asset Quality and Management

British Land's competitive strategy hinges on more than just rental prices; it emphasizes the caliber of its properties and how effectively they are managed. The company distinguishes itself by prioritizing top-tier, sustainable buildings and cultivating dynamic environments. This approach aims to draw in high-value tenants and secure better rental income.

The company's focus on superior amenities, robust community involvement, and efficient property oversight serves as a significant differentiator in a highly competitive sector. For instance, as of early 2024, British Land reported a strong occupancy rate across its portfolio, demonstrating tenant demand for its well-managed and desirable spaces.

- Asset Quality: British Land invests in high-quality, sustainable buildings.

- Strategic Locations: Properties are situated in prime, desirable areas.

- Active Management: Emphasis on efficient property management and tenant engagement.

- Tenant Attraction: Differentiated offerings attract premium tenants and support higher rents.

Fluctuations in Economic Cycles

The property sector, including companies like British Land, experiences intensified competitive rivalry during economic downturns. As demand shrinks and property values decline, competition for available tenants and investment opportunities escalates. This can manifest as aggressive pricing strategies or the postponement of new development projects.

Conversely, during economic booms, the landscape shifts. Increased demand and appreciating property values often create a more favorable environment, potentially easing the intensity of rivalry as opportunities are more abundant for all participants. For instance, in 2024, the UK commercial property market saw varying performance across sectors, with office spaces in London facing headwinds due to flexible working trends, while industrial and logistics assets continued to show resilience, impacting the competitive dynamics for British Land.

- Economic Cycles Impact Rivalry: Property sector competition intensifies during downturns and can lessen during booms.

- Downturns Lead to Price Wars: Reduced demand and falling values force companies to compete more aggressively for tenants and investments.

- 2024 Market Trends: The UK commercial property market in 2024 showed mixed performance, with office spaces facing challenges and logistics remaining strong, influencing British Land's competitive environment.

UK Property Market: Intense Rivalry and Strategic Differentiation

British Land operates in a highly competitive UK property market, facing rivals like Landsec and Segro for prime assets and tenants. This rivalry intensifies during economic downturns, leading to pressure on rents and acquisition costs, as seen in 2024's mixed market performance where office spaces struggled while logistics remained robust.

The company differentiates itself through high-quality, sustainable properties and active management, aiming to attract premium tenants and secure better rental income, a strategy crucial for maintaining its edge against numerous competitors, both large and small.

| Competitor | Key Focus Areas | 2024 Market Activity Indication |

|---|---|---|

| Landsec | Urban regeneration, retail, and commercial | Active in London office development and retail asset management |

| Segro | Logistics and industrial properties | Continued expansion in key logistics hubs |

| Hammerson | Retail and urban development | Focus on mixed-use regeneration and retail portfolio optimization |

SSubstitutes Threaten

Remote and Hybrid Working Models

The rise of remote and hybrid work significantly threatens traditional office spaces. Companies are reassessing their needs, leading to smaller footprints or shifts to flexible co-working solutions. This directly impacts demand for long-term leases that British Land relies on.

In 2024, a significant portion of the workforce continued to operate under hybrid models. For instance, surveys indicated that over 50% of UK employees worked in a hybrid arrangement for at least part of the week. This sustained trend means that the substitution threat for conventional office space remains a potent challenge for property developers like British Land.

E-commerce and Online Retail Expansion

The relentless expansion of e-commerce presents a significant threat of substitution for British Land's traditional retail properties. As more consumers opt for online shopping, the fundamental need for extensive physical retail spaces diminishes, directly impacting demand for British Land's assets in this sector. For instance, in 2024, global e-commerce sales were projected to reach over $6.3 trillion, highlighting the scale of this shift.

This trend challenges the viability of large-format retail stores, a cornerstone of many retail portfolios. British Land is actively mitigating this threat by diversifying its strategy. The company is focusing on developing experiential retail, which offers unique in-person experiences that online shopping cannot replicate, and investing in urban logistics to support the growing online delivery infrastructure.

Furthermore, British Land is repurposing its retail parks to function as crucial last-mile delivery hubs. This adaptation allows them to capitalize on the e-commerce boom by facilitating efficient delivery operations, thereby evolving the traditional retail model to remain relevant in the digital age. This strategic pivot aims to transform potential liabilities into new revenue streams.

Virtual Reality and Metaverse Technologies

While still in early stages, the ongoing development of virtual reality and metaverse technologies presents a potential long-term threat of substitution for some physical real estate uses. These advancements could offer alternatives for events, meetings, and even certain retail experiences, impacting demand for traditional spaces. For instance, a significant portion of corporate training and team-building events, which previously required physical venues, are increasingly incorporating virtual elements, a trend that accelerated significantly in 2023 and is projected to continue growing.

Serviced Offices and Co-working Spaces

The rise of serviced offices and co-working spaces presents a significant threat of substitutes for British Land's traditional office portfolio. These flexible workspace solutions, such as those offered by WeWork or Regus, provide businesses with agile leasing options, lower initial capital outlay, and adaptable space that caters to fluctuating needs, especially for startups and growing enterprises. This directly challenges the long-term lease model that has historically underpinned British Land's revenue streams.

For instance, in 2023, the flexible workspace sector continued its expansion, with many providers reporting strong occupancy rates as companies sought to reduce fixed overheads and enhance workforce flexibility. This trend means that a business might opt for a co-working membership or a short-term serviced office lease instead of committing to a multi-year conventional office rental from a landlord like British Land.

- Threat of Substitutes: Serviced offices and co-working spaces offer flexible, short-term alternatives to traditional office leases.

- Impact on British Land: These substitutes can attract tenants, particularly smaller businesses and startups, away from British Land's conventional office offerings.

- Market Dynamics: The demand for agility and reduced upfront costs in office space fuels the growth of the substitute market.

- British Land's Response: The company is integrating flexible workspace solutions within its own developments to meet evolving tenant preferences and mitigate this threat.

Digital Logistics Platforms and On-demand Warehousing

Digital logistics platforms and on-demand warehousing present a growing threat by offering flexible alternatives to traditional long-term leases for storage. These services allow businesses to scale their warehousing needs up or down rapidly, potentially decreasing reliance on fixed, large-scale facilities. For instance, companies like Flexe and Stord have seen significant growth, facilitating access to a vast network of warehouse space on a pay-as-you-go model.

This shift impacts property owners like British Land by potentially reducing the demand for long-term commitments on their logistics assets. Businesses might opt for these agile solutions, especially those experiencing seasonal fluctuations or unpredictable supply chains, as seen across various sectors in 2024.

- Digital platforms offer flexible, short-term access to warehouse space, a direct substitute for long-term leases.

- Companies like Flexe and Stord are expanding, providing on-demand solutions that reduce the need for fixed logistics property.

- This trend can decrease overall demand for traditional, long-term warehousing leases in the logistics real estate market.

- British Land's strategy of focusing on urban logistics with prime locations aims to counter this by offering unique proximity and efficiency advantages.

E-commerce and Substitutes: Reshaping Real Estate

The threat of substitutes for British Land's traditional retail properties is significant due to the ongoing expansion of e-commerce. As consumers increasingly favor online shopping, the demand for physical retail spaces diminishes, directly impacting British Land's assets in this sector. Global e-commerce sales were projected to exceed $6.3 trillion in 2024, underscoring the scale of this shift.

This trend challenges the viability of large-format retail stores, a core component of many retail portfolios. British Land is actively addressing this by diversifying its strategy, focusing on experiential retail and urban logistics to support online delivery infrastructure.

The company is also repurposing retail parks as last-mile delivery hubs, transforming potential liabilities into new revenue streams by capitalizing on the e-commerce boom and facilitating efficient delivery operations.

| Substitute Type | Impact on British Land | Market Trend (2024 Data) | British Land's Mitigation Strategy |

| E-commerce | Reduced demand for physical retail space | Global e-commerce sales projected over $6.3 trillion | Focus on experiential retail, urban logistics, repurposing retail parks |

| Flexible Workspaces (Co-working) | Threat to traditional office leases | Continued expansion of serviced office sector | Integrating flexible workspace solutions within developments |

| Virtual/Metaverse Technologies | Potential long-term threat to physical space usage | Increasing adoption in corporate training and events | Monitoring technological advancements and potential future applications |

| On-demand Warehousing | Reduced need for long-term logistics leases | Growth of digital logistics platforms and pay-as-you-go models | Focus on prime urban logistics locations for efficiency |

Entrants Threaten

High Capital Requirements

The real estate development and investment sector is inherently capital-intensive. British Land, for instance, operates in an environment where substantial financial backing is a prerequisite for acquiring land, funding construction projects, and managing extensive property portfolios. This significant upfront investment acts as a formidable barrier, deterring many aspiring competitors who may not possess the necessary financial muscle.

For example, in 2024, major UK property developers often require hundreds of millions of pounds to initiate large-scale projects. This high capital requirement means that only well-established entities with robust access to equity, debt financing, and strong relationships with institutional investors can realistically enter the market. British Land's established financial health and diversified funding channels therefore present a significant advantage, effectively limiting the threat of new entrants.

Complex Planning and Regulatory Environment

The UK's property development landscape is notoriously intricate, demanding specialized knowledge and often lengthy approval timelines. Newcomers must contend with a web of environmental standards, building codes, and planning policies, making entry a significant hurdle.

British Land, with its decades of experience, possesses an intrinsic advantage in navigating this complex regulatory maze. Their established track record and deep understanding of the planning system, including a strong grasp of evolving ESG (Environmental, Social, and Governance) requirements, effectively deter less experienced competitors.

Access to Prime Development Sites

Securing prime development sites in desirable urban locations or strategic logistics hubs is increasingly challenging due to limited availability and intense competition. For instance, in 2024, the UK commercial property market saw continued demand for well-located assets, making acquisition more difficult for newcomers.

Established players like British Land often have pre-existing relationships with landowners, a strong track record, and the financial capacity to acquire such sites. In 2023, British Land reported a robust development pipeline, demonstrating their ability to secure future growth opportunities.

New entrants typically struggle to compete for these highly coveted locations, limiting their ability to build a competitive portfolio and establish a significant market presence.

Economies of Scale and Experience

Existing large property companies, like British Land, benefit significantly from economies of scale. This advantage is evident in their ability to secure better terms on procurement, manage large-scale projects more efficiently, and conduct more impactful property marketing campaigns. For instance, British Land's substantial portfolio allows for centralized management and operational efficiencies that smaller entities cannot easily replicate.

Furthermore, the extensive experience these established players possess in navigating market cycles, managing diverse property portfolios, and executing complex development projects translates into a distinct operational expertise. This deep-seated knowledge allows them to anticipate and mitigate risks more effectively than newcomers. New entrants would find it challenging to match these cost efficiencies and operational know-how without substantial time and capital investment.

Consider the capital requirements: developing large commercial properties, a core business for British Land, often requires billions in investment. In 2024, the UK commercial real estate market saw significant investment volumes, but access to such large-scale capital remains a barrier for new, unestablished entities. For example, large-scale office developments or major retail park redevelopments demand a level of financial backing and project management capability that is difficult for new entrants to muster quickly.

- Economies of Scale: British Land leverages its size for cost advantages in procurement and marketing.

- Experience Advantage: Years of navigating market cycles and managing complex developments offer a competitive edge.

- Capital Barriers: The significant capital required for large-scale property development deters new entrants.

- Operational Expertise: Established firms possess specialized skills in project management and portfolio optimization.

Brand Reputation and Tenant Relationships

British Land's strong brand reputation, built on developing and managing high-quality, sustainable properties, creates a significant barrier to new entrants. The company has fostered long-term relationships with key tenants, making it challenging for newcomers to quickly secure desirable occupiers and build a comparable portfolio. In 2024, British Land continued to emphasize its commitment to sustainability, with 95% of its portfolio certified BREEAM Excellent or Outstanding, reinforcing its appeal to environmentally conscious tenants and further deterring new competition.

The established trust and extensive network British Land possesses make it difficult for new players to attract anchor tenants or replicate its portfolio of high-value assets. This reputation for reliability and quality acts as a substantial hurdle for newcomers seeking to establish a foothold in the market.

- Established tenant relationships: British Land's long-standing partnerships with key occupiers are a significant deterrent to new entrants.

- Brand quality perception: The company's reputation for developing and managing high-quality, sustainable real estate is a strong competitive advantage.

- Sustainability credentials: In 2024, 95% of British Land's portfolio was BREEAM Excellent or Outstanding certified, enhancing its attractiveness to tenants.

- Portfolio value: The difficulty in replicating British Land's portfolio of high-value properties presents a substantial barrier for new market participants.

Fortifying the Market: British Land's Defense Against New Entrants

The threat of new entrants for British Land is generally low due to substantial capital requirements, with major UK property developments in 2024 often needing hundreds of millions of pounds. Navigating complex planning regulations and securing prime locations are significant hurdles that favor established players like British Land, which has a robust development pipeline as of 2023. Economies of scale and operational expertise further solidify this advantage, as newcomers struggle to match the cost efficiencies and project management capabilities of larger firms.

British Land's established brand reputation, bolstered by its 2024 commitment to sustainability with 95% of its portfolio BREEAM Excellent or Outstanding certified, also deters new competition. The company's strong tenant relationships and the difficulty in replicating its high-value asset portfolio present substantial barriers. This combination of financial, regulatory, operational, and reputational factors significantly limits the ease with which new companies can enter and compete effectively in the real estate development and investment sector.

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis for British Land Company leverages data from their annual reports, investor presentations, and stock exchange filings. We supplement this with industry-specific reports from reputable sources like the British Property Federation and market intelligence from firms such as Savills and CBRE.