Bank of East Asia Business Model Canvas

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Bank of East Asia Bundle

BEA's Business Model: A Strategic Deep Dive

Discover the strategic core of Bank of East Asia's success with our comprehensive Business Model Canvas. This detailed breakdown illuminates their customer relationships, revenue streams, and key resources, offering a clear roadmap to their market position. Empower your own strategic planning by downloading the full canvas today and gain actionable insights into a thriving financial institution.

Partnerships

Strategic Bancassurance Partners

Bank of East Asia (BEA) strategically partners with prominent insurance companies, including AIA and Blue Cross, to broaden its financial product offerings. These collaborations enable BEA to provide customers with a diverse selection of life and general insurance solutions.

Through these alliances, BEA enhances its customer value by delivering integrated financial services that extend beyond core banking functions. This approach allows for a more holistic approach to wealth management and protection for its clientele.

A key element of BEA's strategy is its long-standing, exclusive bancassurance agreement with AIA, spanning both Hong Kong and Mainland China. This partnership is designed to capitalize on BEA's substantial customer network, aiming to drive significant cross-selling opportunities.

Fintech Collaboration Platforms

Bank of East Asia actively partners with fintech innovators through its BEAST innovation center, fostering co-creation of digital financial solutions. This strategic approach is vital for accelerating digital transformation and improving customer experiences in today's dynamic financial environment.

These collaborations are essential for optimizing operational efficiency and introducing cutting-edge services. BEA Fintech Day, held as part of Hong Kong Fintech Week 2024, serves as a key platform to showcase and further these valuable fintech partnerships.

Cross-Boundary Wealth Management Connect Partners

Bank of East Asia (BEA) strategically partners with mainland Chinese banks, including Guangzhou Rural Commercial Bank, to bolster its cross-boundary wealth management services, particularly through initiatives like Wealth Management Connect 2.0. These collaborations are crucial for offering enhanced investment avenues to qualified investors within the Greater Bay Area, effectively pooling the extensive networks and specialized knowledge of both banking entities.

These alliances are designed to unlock significant investment opportunities for qualified investors in the Greater Bay Area, allowing them to access a broader range of financial products and services. By joining forces, BEA and its mainland partners can better serve the evolving needs of investors in this dynamic economic region.

Through these key partnerships, BEA aims to solidify its presence and expand its wealth management client base across mainland China. For instance, as of late 2023, the Wealth Management Connect program facilitated substantial cross-border capital flows, with the northbound channel alone seeing significant participation, underscoring the potential of such strategic alliances.

International Correspondent Banks

Bank of East Asia (BEA) cultivates a robust network of international correspondent banks, a crucial element for its global operations. These relationships are fundamental to facilitating a wide array of cross-border financial activities for its clientele.

These partnerships are vital for enabling international trade finance, processing remittances, and executing seamless cross-border transactions. For instance, in 2023, BEA reported a significant volume of international trade finance activities, underscoring the reliance on its correspondent banking network.

BEA's correspondent banking relationships are indispensable for both its corporate and individual customers who are actively involved in international business. These alliances also serve as a strategic avenue for the bank to broaden its presence and service offerings in key global markets.

The bank's commitment to maintaining these international partnerships ensures the efficient and reliable execution of global financial operations and service delivery, directly impacting customer satisfaction and operational effectiveness.

- Facilitation of International Trade Finance: Enabling import and export transactions for clients.

- Remittance Services: Supporting the transfer of funds across borders for individuals and businesses.

- Cross-Border Transaction Processing: Ensuring smooth and efficient handling of international payments and settlements.

- Market Expansion: Providing a gateway for BEA to offer its services in new international territories.

Technology and Digital Solution Providers

Bank of East Asia (BEA) actively collaborates with a diverse range of technology and digital solution providers. These partnerships are fundamental for the bank's core banking systems, robust cybersecurity measures, advanced data analytics capabilities, and the development of its mobile banking platforms.

These strategic alliances are crucial for BEA to maintain a strong and reliable IT infrastructure. They also directly contribute to enhancing the bank's digital service offerings, ensuring both the security and operational efficiency of its banking activities. For instance, in 2024, BEA continued its investment in digital transformation initiatives, aiming to leverage cutting-edge technologies to improve customer experience and streamline internal processes.

- Core Banking Systems: Partnerships with providers like Oracle or FIS for system upgrades and maintenance.

- Cybersecurity: Collaborations with firms such as Palo Alto Networks or CrowdStrike to bolster defenses against cyber threats.

- Data Analytics: Working with companies like IBM or SAS to leverage advanced analytics for insights and personalized services.

- Mobile Banking Platforms: Engaging with fintechs or software developers to enhance user experience and functionality of mobile apps.

Strategic Alliances Drive Innovation & Growth

BEA's key partnerships extend to leading insurance providers like AIA and Blue Cross, enhancing its product suite with diverse life and general insurance solutions. These alliances are pivotal for offering integrated financial services, thereby enriching customer value through comprehensive wealth management and protection strategies.

The bank also actively engages with fintech innovators via its BEAST innovation center, fostering co-creation of digital solutions to accelerate transformation and improve customer experience. Furthermore, collaborations with mainland Chinese banks, such as Guangzhou Rural Commercial Bank, are crucial for expanding cross-boundary wealth management services, particularly within the Greater Bay Area.

These strategic alliances are essential for optimizing operations and introducing innovative services, with BEA Fintech Day in 2024 highlighting these advancements. The bank also maintains a robust network of international correspondent banks, vital for facilitating cross-border trade finance, remittances, and transactions, as evidenced by significant trade finance volumes in 2023.

BEA also partners with technology providers for core banking systems, cybersecurity, data analytics, and mobile banking platforms, ensuring a strong IT infrastructure and enhanced digital offerings. These collaborations are fundamental to maintaining operational efficiency and security in its banking activities.

| Partner Type | Key Partners | Strategic Objective | Impact/Example |

|---|---|---|---|

| Insurance Companies | AIA, Blue Cross | Broaden financial product offerings, integrated financial services | Exclusive bancassurance with AIA for cross-selling in Hong Kong and Mainland China. |

| Fintech Innovators | Various via BEAST innovation center | Co-creation of digital financial solutions, accelerate digital transformation | Showcased at BEA Fintech Day during Hong Kong Fintech Week 2024. |

| Mainland Chinese Banks | Guangzhou Rural Commercial Bank | Bolster cross-boundary wealth management, Wealth Management Connect 2.0 | Facilitate investment opportunities in the Greater Bay Area; northbound channel saw significant participation in 2023. |

| International Correspondent Banks | Global network | Facilitate cross-border activities, international trade finance, remittances | Critical for enabling international trade finance, with significant activity reported in 2023. |

| Technology & Digital Solution Providers | Oracle, FIS, Palo Alto Networks, IBM | Enhance core banking systems, cybersecurity, data analytics, mobile platforms | Essential for IT infrastructure, digital service enhancement, and operational efficiency. Continued investment in digital transformation in 2024. |

What is included in the product

A comprehensive, pre-written business model tailored to the Bank of East Asia's strategy, detailing customer segments, channels, and value propositions.

The Bank of East Asia's Business Model Canvas acts as a pain point reliever by providing a clear, one-page snapshot that helps identify and address operational inefficiencies and customer service gaps.

It streamlines complex banking operations into an easily digestible format, alleviating the pain of fragmented strategies and enabling targeted solutions.

Activities

Retail and Corporate Banking Operations

Bank of East Asia's core activities revolve around traditional banking operations. This includes taking deposits from individuals and businesses, and then lending those funds out through various products like mortgages, commercial loans, and trade finance. These fundamental banking functions are the bedrock of their business.

To support these operations, BEA manages a significant physical presence with its branch network, alongside a growing digital platform. This dual approach allows them to cater to a wide range of customer preferences and needs, from in-person interactions to convenient online services. For instance, in 2023, BEA continued to invest in its digital transformation, enhancing its mobile banking app to offer more streamlined services for its retail and corporate customers.

Wealth Management and Investment Services

Bank of East Asia's Wealth Management and Investment Services actively cultivate client wealth by offering a diverse portfolio including unit trusts, linked deposits, global equities, bonds, and structured products. Personalized investment advisory is a cornerstone, alongside private banking tailored for affluent and high-net-worth individuals.

In 2024, BEA continued its strategic push to be a premier wealth manager, emphasizing its strong cross-boundary capabilities and deep expertise in the China market. This focus aims to capture growing opportunities for clients seeking international diversification and access to the dynamic Chinese economy.

Insurance Product Distribution

Bank of East Asia (BEA) actively distributes a range of life and general insurance products through its bancassurance partnerships. This strategy diversifies its revenue streams by generating non-interest income and offers customers a more complete suite of financial protection options. BEA operates as an appointed insurance agency for these partners.

In 2023, BEA's insurance business contributed significantly to its overall performance. For instance, the bank reported a substantial increase in new business premiums for its life insurance products, reflecting strong customer uptake. This growth underscores the effectiveness of its distribution channels and the appeal of its bundled financial solutions.

Digital Transformation and Fintech Innovation

Bank of East Asia (BEA) is heavily invested in digital transformation, focusing on developing and deploying advanced digital banking solutions. This includes a robust mobile app and sophisticated online platforms, all part of its broader fintech strategy powered by its BEAST platform. The bank is committed to ongoing innovation to elevate customer experiences, optimize operational efficiency, and launch novel digital services. A key objective is to shift a greater volume of transactions to online channels and integrate AI-driven capabilities across its services.

BEA's commitment to digital innovation is reflected in its 2024 performance. For instance, the bank reported a significant increase in digital transaction volumes, with mobile banking transactions growing by 15% year-on-year. Furthermore, investment in fintech initiatives, including AI and data analytics, contributed to a 10% reduction in operational costs in its digital channels during the first half of 2024.

- Digital Banking Solutions: Development and implementation of mobile apps and online platforms.

- Fintech Initiatives: Leveraging the BEAST platform for innovation and new digital services.

- Customer Experience Enhancement: Streamlining operations and introducing new digital offerings.

- AI Integration: Aiming to migrate more transactions online and utilize AI-powered solutions.

Risk Management and Regulatory Compliance

Bank of East Asia (BEA) places significant emphasis on its key activities of risk management and regulatory compliance to ensure its financial stability and uphold customer trust. This involves meticulously managing various risks, including credit risk, operational risk, and market risk, while strictly adhering to all relevant financial regulations. BEA is particularly focused on strengthening its credit risk management and maintaining robust capital adequacy ratios.

In 2024, BEA continued its commitment to these critical functions. For instance, the bank's robust credit risk management strategies are evident in its loan portfolio quality. As of the first half of 2024, BEA reported a non-performing loan (NPL) ratio of approximately 1.4%, demonstrating effective control over credit defaults.

BEA's dedication to regulatory compliance is ongoing, with continuous efforts to adapt to the evolving global financial regulatory environment. This proactive approach ensures the bank operates within legal frameworks and maintains a strong reputation. The bank actively monitors and reports on its risk exposures and capital position, aligning with international standards and local mandates.

- Credit Risk Management: BEA employs a comprehensive approach to assess, monitor, and manage credit risk across its lending activities, aiming to minimize potential losses from borrower defaults.

- Operational Risk Mitigation: The bank implements strong internal controls and processes to safeguard against operational failures, fraud, and other non-financial risks that could impact its business.

- Market Risk Oversight: BEA actively manages its exposure to market fluctuations, including interest rate and foreign exchange risks, through hedging strategies and prudent investment policies.

- Regulatory Adherence: Ensuring full compliance with all applicable banking laws, regulations, and supervisory requirements is a fundamental activity, underpinning the bank's operational integrity and market standing.

Digital Banking Soars: Transactions Up 15%, Costs Down 10%

Bank of East Asia's key activities encompass the development and deployment of advanced digital banking solutions, including a robust mobile app and online platforms, all driven by its BEAST fintech platform. The bank prioritizes enhancing customer experiences through streamlined operations and the introduction of innovative digital offerings, with a strategic aim to increase online transaction volumes and integrate AI capabilities. In 2024, BEA saw a 15% year-on-year increase in mobile banking transactions, alongside a 10% reduction in digital channel operational costs in the first half of the year due to fintech investments.

Delivered as Displayed

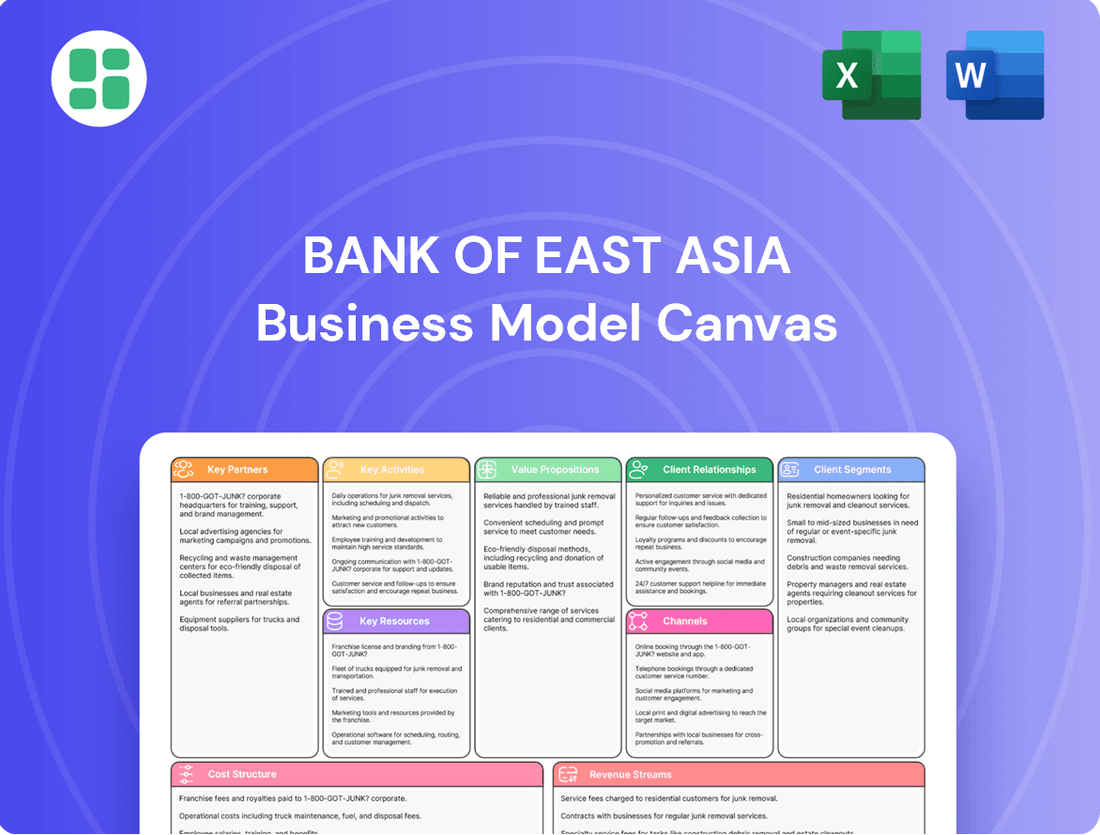

Business Model Canvas

This preview offers a genuine glimpse into the Bank of East Asia's Business Model Canvas, showcasing the exact structure and content you will receive upon purchase. You're not viewing a generic template, but a direct representation of the comprehensive document that will be yours. Once your order is complete, you'll gain full access to this same detailed analysis, ready for immediate application.

Resources

Extensive Branch and ATM Network

BEA boasts an extensive physical footprint, with a substantial number of branches and ATMs strategically located across Hong Kong, mainland China, and other international territories. This widespread network ensures customers have convenient access to banking services, offering a vital traditional channel for both routine transactions and more personalized, complex financial needs.

In Hong Kong, BEA operates one of the most significant retail banking networks. As of the first half of 2024, the bank maintained over 100 branches in the region, underscoring its commitment to a strong physical presence and customer accessibility in its core market.

Skilled Human Capital

Bank of East Asia (BEA) leverages a substantial pool of skilled human capital, encompassing experienced banking professionals, dedicated relationship managers, expert financial advisors, and specialized IT personnel. This diverse expertise is fundamental to providing superior banking services and fostering innovation across its operations.

The bank's commitment to its workforce is evident in its strategic growth plans. BEA intends to expand its regional relationship manager team, with a particular focus on strengthening its private banking segment. This expansion is designed to enhance client engagement and service delivery in key markets.

In 2024, BEA continued to invest in talent development, recognizing that its employees' proficiency in banking disciplines, wealth management, and emerging digital technologies directly impacts service quality and competitive advantage. This focus on human capital is a cornerstone of their business model, enabling them to adapt to evolving market demands and client needs.

Advanced Technology Infrastructure and Digital Platforms

Bank of East Asia's advanced technology infrastructure and digital platforms are foundational key resources. These encompass robust IT systems, secure data centers, and user-friendly online banking portals and mobile applications that power all their banking operations.

Continuous investment in technology is a crucial driver for BEA, with a focus on areas like Artificial Intelligence and digital transformation tools. This commitment ensures efficient service delivery, strengthens cybersecurity, and maintains a competitive edge in the financial landscape.

In 2023, BEA continued to enhance its digital offerings by launching new mobile applications and digital trading platforms, demonstrating a clear strategy to meet evolving customer demands for seamless digital financial services.

Strong Brand Reputation and Customer Trust

Bank of East Asia's (BEA) strong brand reputation and customer trust are cornerstones of its business model, cultivated over a century of operation since its incorporation in 1918. This deep-rooted trust is a vital intangible asset, enabling BEA to attract and retain a loyal customer base in the highly competitive financial services sector.

This reputation is further bolstered by BEA's consistent commitment to service excellence. For instance, in 2024, BEA was recognized for its customer service initiatives, underscoring its dedication to client satisfaction. Such efforts are crucial for maintaining market share and fostering long-term relationships.

- Brand Legacy: Established in 1918, BEA boasts over a century of financial service provision.

- Customer Trust: Decades of reliable service have fostered significant trust among its clientele.

- Competitive Advantage: A strong brand reputation acts as a key differentiator in the financial market.

- Service Commitment: Ongoing dedication to service excellence reinforces customer loyalty and brand perception.

Financial Capital and Liquidity

Financial capital is the lifeblood of any bank, and for Bank of East Asia (BEA), this encompasses a robust mix of shareholder equity, customer deposits, and access to various funding channels. This financial foundation is crucial for maintaining operational stability, facilitating loan origination, and pursuing growth opportunities. As of December 31, 2024, BEA reported total consolidated assets amounting to HK$877.8 billion, underscoring its significant financial capacity.

Liquidity management is equally vital, ensuring BEA can meet its short-term obligations and customer withdrawal demands. This involves holding sufficient liquid assets and maintaining access to interbank markets. The bank's ability to manage its capital and liquidity effectively directly impacts its lending capacity and overall resilience in the financial system.

- Shareholder Equity: Represents the owners' stake in the bank, a key indicator of financial strength.

- Deposits: A primary source of funding, reflecting customer trust and the bank's deposit-gathering capabilities.

- Access to Funding Markets: Includes borrowing from central banks and other financial institutions, providing flexibility.

- Total Consolidated Assets: As of December 31, 2024, this stood at HK$877.8 billion, demonstrating the scale of BEA's operations.

Foundational Assets: Powering a Financial Institution's Enduring Success

BEA's extensive physical branch network and ATM presence across Hong Kong, mainland China, and other international locations serve as critical physical touchpoints for customer engagement and service delivery. This widespread infrastructure, with over 100 branches in Hong Kong alone as of the first half of 2024, ensures convenient access for a broad customer base.

The bank's skilled human capital, comprising experienced banking professionals, relationship managers, and IT specialists, is fundamental to its service quality and innovation. BEA's strategic focus on expanding its regional relationship manager team, particularly for its private banking segment, highlights its commitment to nurturing talent for enhanced client engagement.

BEA's robust technology infrastructure, including advanced IT systems and user-friendly digital platforms, is a key enabler of its operations. The bank’s continued investment in digital transformation and AI tools, as seen in its 2023 enhancements to mobile applications and digital trading platforms, ensures operational efficiency and a competitive digital offering.

The bank's strong brand reputation, built over a century since its 1918 founding, and the resulting customer trust are invaluable intangible assets. This legacy, coupled with a consistent commitment to service excellence, as recognized in 2024 for customer service initiatives, fosters loyalty and provides a significant competitive advantage in the financial market.

Financial capital, comprising shareholder equity, customer deposits, and diverse funding channels, forms the bedrock of BEA's operations, enabling lending and growth. As of December 31, 2024, the bank reported total consolidated assets of HK$877.8 billion, demonstrating its substantial financial capacity and stability.

| Key Resource | Description | 2024 Data/Relevance |

| Physical Network | Extensive branch and ATM presence | Over 100 branches in Hong Kong (H1 2024) |

| Human Capital | Skilled banking professionals and advisors | Expansion of regional relationship managers planned |

| Technology Infrastructure | Advanced IT systems and digital platforms | Investment in AI and digital transformation tools |

| Brand Reputation & Trust | Over a century of service, customer loyalty | Recognized for customer service initiatives (2024) |

| Financial Capital | Shareholder equity, deposits, funding access | Total consolidated assets: HK$877.8 billion (Dec 31, 2024) |

Value Propositions

Comprehensive Financial Solutions

Bank of East Asia (BEA) distinguishes itself by offering a truly comprehensive suite of financial solutions, acting as a single point of contact for a vast range of banking and financial needs. This encompasses everything from everyday retail banking and specialized corporate banking services to sophisticated wealth management and essential insurance products.

This integrated approach significantly streamlines financial management for both individuals and businesses, consolidating diverse requirements into one accessible platform. BEA’s commitment is to deliver financial products and services that are not just broad, but also of the highest quality, aiming for best-in-class performance across all offerings.

For instance, as of the first half of 2024, BEA reported a substantial increase in its loan portfolio, reflecting the growing demand for its corporate banking services. Furthermore, the bank's wealth management division saw a notable uptick in assets under management, underscoring client trust in their comprehensive investment solutions.

Extensive Regional and International Network

Bank of East Asia's extensive regional and international network is a core value proposition, particularly for clients navigating global finance. With a strong foothold in Hong Kong and mainland China, complemented by operations in other key international markets, BEA facilitates smooth cross-border banking and investment activities.

This global reach is a significant advantage for businesses and individuals involved in international trade and investments, offering seamless access to diverse financial services. The bank's expansive network encompasses approximately 120 to 130 outlets worldwide, underscoring its commitment to providing accessible financial solutions across geographies.

Personalized Wealth Management and Advisory

For its affluent and high-net-worth clientele, Bank of East Asia (BEA) delivers tailored private banking services, including customized wealth management plans and expert investment advice. This bespoke strategy is designed to help clients expand and safeguard their assets, often leveraging specific market knowledge, particularly concerning China.

BEA's commitment to personalized wealth management is exemplified by its SupremeGold and SupremeGold Private Centres, which provide dedicated spaces and specialized services for these important customer segments. These offerings underscore BEA's focus on building long-term relationships by meeting the unique financial needs of its wealthiest customers.

Digital Convenience and Innovation

Bank of East Asia (BEA) champions digital convenience and innovation, offering robust mobile banking apps and sophisticated online corporate banking solutions. This focus ensures customers can manage everything from daily transactions to intricate investment activities with ease.

BEA's commitment to fintech investment translates into seamless digital experiences. For instance, in 2024, the bank continued to enhance its digital offerings, aiming to capture a larger share of digitally engaged customers.

- Digital Channels Growth: BEA reported a significant increase in digital transactions, with mobile banking usage up by 15% year-over-year in early 2024, highlighting its growing importance as a primary customer interaction point.

- Fintech Investment: The bank allocated an additional HK$200 million in 2024 towards further developing its digital infrastructure and exploring new fintech partnerships to maintain its competitive edge.

- Customer Adoption: Over 70% of BEA's retail customers now actively use at least one digital banking channel, demonstrating a strong preference for convenient, self-service banking options.

Reliability and Heritage

BEA's reliability is deeply rooted in its heritage as a Hong Kong-based institution, established in 1918. This long history, spanning over a century, provides clients with a profound sense of security and stability. Its deep understanding of local and regional markets, built over decades, assures customers of a dependable partner for their financial aspirations.

This enduring presence fosters significant trust and confidence, making BEA a go-to financial institution for individuals and businesses alike. For instance, as of the first half of 2024, BEA reported a robust Common Equity Tier 1 ratio of 15.4%, underscoring its strong capital position and financial resilience.

- Established in 1918: Over 100 years of service in Hong Kong.

- Market Expertise: Deep understanding of local and regional financial landscapes.

- Client Trust: Heritage builds confidence in long-term financial partnerships.

- Financial Strength: Demonstrated by a CET1 ratio of 15.4% in H1 2024.

Integrated Financial Solutions: Global Reach, Tailored for Your Success

BEA offers a comprehensive financial ecosystem, integrating retail, corporate, wealth management, and insurance services. This one-stop-shop approach simplifies financial management for all clients, ensuring high-quality, best-in-class products. As of H1 2024, BEA's loan portfolio saw significant growth, and assets under management in wealth management also increased, reflecting client trust.

The bank's extensive network, with around 120-130 outlets globally, facilitates seamless cross-border transactions, particularly for those engaged in international trade and investment. This global reach, combined with specialized private banking for affluent clients, offers tailored solutions for wealth expansion and protection, leveraging deep market knowledge, especially concerning China.

| Value Proposition | Description | Supporting Data (as of H1 2024 or latest available) |

|---|---|---|

| Comprehensive Financial Solutions | One-stop shop for retail, corporate, wealth management, and insurance. | Loan portfolio growth; increase in assets under management for wealth management. |

| Extensive Regional & International Network | Facilitates smooth cross-border banking and investment. | Operates approximately 120-130 outlets worldwide. |

| Tailored Private Banking | Customized wealth management and investment advice for affluent clients. | Focus on bespoke strategies for asset growth and protection, leveraging China market expertise. |

| Digital Convenience & Innovation | Robust mobile and online banking solutions. | 15% year-over-year increase in mobile banking usage (early 2024); HK$200 million invested in digital infrastructure (2024). |

| Reliability and Heritage | Over a century of experience and strong financial standing. | Established in 1918; CET1 ratio of 15.4% (H1 2024). |

Customer Relationships

Personalized Relationship Management

Bank of East Asia (BEA) cultivates personalized relationships through dedicated relationship managers for its corporate clients, SupremeGold and SupremeGold Private wealth management customers, and high-net-worth individuals. These specialists offer tailored advice and proactive support, fostering long-term loyalty by deeply understanding client needs.

Digital Self-Service and Support

Bank of East Asia (BEA) heavily emphasizes digital self-service, offering robust mobile apps and online banking platforms. These channels empower customers to manage accounts, perform transactions, and access information without direct human interaction, boosting convenience and efficiency.

BEA has successfully transitioned a significant portion of its retail transactions to its mobile application. This digital-first approach streamlines operations and enhances the customer experience, reflecting a commitment to digital innovation in banking services.

Branch-Based Customer Service

Bank of East Asia (BEA) continues to invest in its extensive branch network, recognizing its crucial role in customer relationships. Despite the digital shift, these physical locations provide essential in-person service, enabling customers to resolve complex issues and receive personalized consultations. This human touch remains vital for fostering trust, particularly for those who prefer face-to-face interactions.

BEA's branches offer a full spectrum of banking services, acting as a cornerstone for customer engagement. In 2024, BEA reported a robust presence with numerous branches across its operating regions, underscoring its commitment to this traditional channel. This strategy caters to a significant segment of their customer base who value the accessibility and comprehensive support provided by branch staff.

Community Engagement and Corporate Social Responsibility

Bank of East Asia actively engages with its communities, demonstrating a commitment to corporate social responsibility. This approach is central to fostering strong customer relationships by showing the bank is a positive force, not just a financial institution.

BEA integrates social and environmental considerations into its operations, notably through sustainable finance initiatives. For instance, in 2024, the bank continued to expand its green loan portfolio, supporting businesses committed to environmental sustainability. This focus not only aligns with global trends but also resonates with customers who increasingly value ethical banking practices.

- Sustainable Finance Growth: BEA's lending for green projects saw a significant increase in 2024, contributing to a more sustainable economy and attracting environmentally conscious clients.

- Community Support Programs: The bank consistently invests in local community development, education, and welfare programs, enhancing its reputation and building trust.

- Enhanced Customer Loyalty: By actively participating in and supporting community initiatives, BEA strengthens its bond with customers, leading to improved perception and loyalty.

- Stakeholder Alignment: BEA's CSR efforts aim to harmonize the financial interests of stakeholders with the broader social and environmental well-being of the communities it serves.

Customer Feedback and Continuous Improvement

Bank of East Asia (BEA) actively seeks customer feedback to refine its services and product development. This commitment to a customer-centric model ensures that BEA's offerings remain relevant and competitive, adapting to evolving market needs and customer preferences.

BEA's focus on customer experience is often validated through industry recognition. For instance, in 2024, BEA was recognized with multiple awards for its customer service and digital banking innovation, underscoring their dedication to enhancing customer satisfaction.

- Customer Feedback Channels: BEA likely utilizes surveys, online feedback forms, and direct communication channels to gather insights from its customer base.

- Service Enhancement Initiatives: Feedback data is analyzed to identify areas for improvement in product features, digital platforms, and customer support processes.

- Awards and Recognition: BEA’s commitment to customer experience has been acknowledged through various accolades, including awards for best customer service in 2024, reflecting successful implementation of customer-focused strategies.

- Digital Transformation: Continuous feedback drives the enhancement of BEA’s digital banking services, aiming to provide seamless and intuitive user experiences.

High-touch wealth management meets efficient digital banking

Bank of East Asia (BEA) balances personalized, high-touch service for wealth management clients with efficient digital self-service for retail customers. Its extensive branch network remains a key touchpoint for complex needs and relationship building, complemented by community engagement and a focus on sustainability to foster loyalty.

| Relationship Type | Key Channels | 2024 Focus |

|---|---|---|

| Wealth Management/High-Net-Worth | Dedicated Relationship Managers, Branch Consultations | Tailored advice, proactive support, building long-term loyalty |

| Retail Banking | Mobile App, Online Banking, Branch Network | Digital self-service, transaction efficiency, in-person issue resolution |

| Corporate Clients | Dedicated Relationship Managers | Personalized service, understanding specific business needs |

Channels

Physical Branch Network

The Bank of East Asia (BEA) leverages its extensive physical branch network as a cornerstone of its customer engagement strategy. This network spans Hong Kong, mainland China, Macau, Taiwan, Southeast Asia, the UK, and the US, offering a tangible presence for a wide range of banking services.

These branches are crucial for facilitating complex transactions, providing in-depth, personalized consultations, and handling essential cash services. They represent a vital physical touchpoint, fostering trust and enabling face-to-face interactions that are particularly valued by certain customer segments.

Online Banking Platforms (Web and Mobile)

Bank of East Asia (BEA) offers comprehensive online banking through its user-friendly website and dedicated mobile apps. These digital channels allow customers to conduct transactions, manage accounts, and access a full suite of financial services conveniently, 24/7.

BEA has strategically invested in its digital infrastructure, aiming to provide a seamless and efficient customer experience. For instance, in 2024, the bank continued to roll out enhanced features on its mobile app, focusing on areas like personalized financial insights and simplified payment processes.

ATM Network

The Bank of East Asia (BEA) leverages its extensive ATM network as a crucial component of its customer service strategy, offering widespread accessibility for essential banking needs. This network complements their physical branches, ensuring customers can perform transactions like cash withdrawals and deposits around the clock, enhancing convenience for their retail clientele.

Dedicated Wealth Management Centres

Bank of East Asia (BEA) caters to its affluent and high-net-worth clientele through dedicated wealth management hubs. These specialized centers, known as SupremeGold and SupremeGold Private Centres, provide an exclusive setting for highly personalized financial services.

These premium locations are designed to foster a superior client experience, offering expert advice and bespoke financial solutions. BEA's commitment to this segment is evident in the tailored approach to wealth management, ensuring that the unique needs of these discerning customers are met with precision and care.

- Dedicated Wealth Management Centres: BEA operates SupremeGold and SupremeGold Private Centres for affluent and high-net-worth clients.

- Personalized Services: These centers offer exclusive environments for tailored wealth management, expert advice, and customized financial solutions.

- Premium Client Experience: The focus is on providing a premium and differentiated service to attract and retain high-value customers.

Contact Centres and Customer Service Hotlines

Bank of East Asia (BEA) leverages its contact centres and customer service hotlines as a crucial channel for customer engagement and support. These facilities enable clients to conveniently inquire about BEA's diverse range of banking products and services, troubleshoot any issues they may encounter, and receive prompt assistance without needing to visit a physical branch. This remote support mechanism is particularly vital for customers who value the efficiency and accessibility of phone-based interactions, ensuring that help is readily available.

The bank is committed to maintaining a high standard of service quality across all its customer touchpoints, including these essential contact channels. In 2024, BEA reported handling millions of customer calls annually, with a focus on reducing average handling times and improving first-call resolution rates. This dedication to service excellence aims to foster customer loyalty and satisfaction, reinforcing BEA's reputation as a customer-centric financial institution.

- Accessibility: Provides 24/7 support for urgent inquiries and standard banking hours for general assistance.

- Efficiency: Focuses on quick resolution of customer queries and issues, aiming for a high first-contact resolution rate.

- Customer Satisfaction: Employs trained professionals to deliver personalized and effective support, enhancing the overall customer experience.

- Reach: Extends service to a broad customer base, catering to those who prefer or require phone-based communication.

Integrated Banking: Digital Convenience, Physical Presence

BEA's channels encompass a robust physical branch network, digital platforms including a user-friendly website and mobile apps, an extensive ATM network, specialized wealth management centers for affluent clients, and customer service contact centers. In 2024, BEA continued to enhance its digital offerings, focusing on personalized financial insights and streamlined payment processes within its mobile app, reflecting a strategic push towards digital convenience alongside its traditional service points.

Customer Segments

Individual Retail Customers

Individual retail customers represent a cornerstone of Bank of East Asia's (BEA) operations, encompassing a wide array of everyday individuals. These customers rely on BEA for essential banking services like savings and current accounts, personal loans, credit cards, and remittance facilities, prioritizing convenience and dependable financial management.

BEA's strategy for this segment focuses on meeting their evolving needs through accessible and reliable banking solutions. As of the first half of 2024, BEA reported a substantial customer base, underscoring the importance of this segment to their overall business model. The bank continues to invest in digital platforms to enhance the customer experience for these users.

Affluent and High-Net-Worth Individuals (HNWIs)

Bank of East Asia (BEA) specifically caters to Affluent and High-Net-Worth Individuals (HNWIs) through its SupremeGold and SupremeGold Private services. These offerings are designed for clients with significant assets who require sophisticated wealth management, tailored investment advice, and comprehensive financial planning.

This valuable customer segment prioritizes personalized attention, unique access to specialized financial products, and expert advice to effectively grow and safeguard their wealth. In 2024, BEA has been actively focusing on enhancing its cross-boundary wealth management capabilities to better serve these discerning clients.

Small and Medium-sized Enterprises (SMEs)

Bank of East Asia (BEA) actively supports Small and Medium-sized Enterprises (SMEs) through a comprehensive suite of corporate banking services. These include crucial offerings like commercial lending, vital trade finance facilities, efficient cash management solutions, and specialized business accounts designed to streamline operations.

SMEs, a significant engine of economic growth, particularly in regions like Hong Kong where BEA has a strong presence, depend on adaptable financing and user-friendly banking technologies. For instance, in 2023, SMEs accounted for over 98% of all businesses in Hong Kong, highlighting their immense economic contribution and need for tailored financial support.

BEA's commitment to this segment is further demonstrated by its BEA Corporate Online platform. This digital channel offers customized solutions specifically for startups and established SMEs, providing them with the tools and flexibility needed to manage their finances effectively and pursue growth opportunities in a dynamic market.

Large Corporations and Institutions

Large corporations and institutions represent a cornerstone for Bank of East Asia (BEA), engaging them with comprehensive wholesale banking solutions. This segment includes major local and international businesses with sophisticated financial needs, often spanning diverse geographical markets. BEA's wholesale banking arm is specifically structured to address these complex requirements, offering services tailored to large-scale operations.

BEA provides these clients with a robust suite of products and services. These are designed to support their extensive financial activities, ranging from day-to-day operations to strategic growth initiatives. The bank’s focus is on building long-term relationships by understanding and meeting the intricate demands of these high-value clients.

- Corporate Lending and Syndication: Facilitating large-scale financing and collaborative lending arrangements for major enterprises.

- Treasury Products: Offering sophisticated cash management, foreign exchange, and hedging solutions to manage financial risks and optimize liquidity.

- Investment Banking Services: Providing advisory on mergers and acquisitions, capital raising, and other strategic financial transactions.

- Cross-Jurisdictional Support: Enabling seamless operations for multinational corporations by navigating complex international financial landscapes.

Cross-Boundary Clients (Greater Bay Area)

Bank of East Asia places a significant emphasis on its Cross-Boundary Clients within the Greater Bay Area (GBA), encompassing individuals and businesses in Hong Kong, mainland China, Macau, and Taiwan. This strategic focus is particularly evident with initiatives like Wealth Management Connect, designed to facilitate seamless cross-border banking and investment activities. BEA leverages its extensive network and deep regional expertise to support financial flows across these key markets.

The bank's commitment to this segment is underscored by its ongoing efforts to expand its cross-boundary business operations. For instance, in 2023, the Wealth Management Connect scheme saw continued growth, with transaction volumes indicating increasing client adoption for cross-border wealth management solutions. BEA's advantage lies in its established presence and understanding of the regulatory landscapes within the GBA, enabling it to offer tailored services.

- Targeting GBA Residents: BEA actively targets clients residing in Hong Kong, mainland China, Macau, and Taiwan who need integrated banking and investment services across these regions.

- Wealth Management Connect: This program is a cornerstone for serving cross-boundary clients, allowing them to access wealth management products and services in both Hong Kong and the mainland.

- Network and Expertise: BEA's strong regional network and specialized knowledge in navigating cross-border financial flows are key differentiators for this customer segment.

- Expansion Strategy: The bank is focused on growing its cross-boundary business, aiming to capture a larger share of the increasing financial integration within the Greater Bay Area.

BEA: Diverse Banking Solutions for Individuals, Businesses, and GBA Clients

Bank of East Asia (BEA) serves a diverse customer base, from individual retail clients needing everyday banking to high-net-worth individuals seeking sophisticated wealth management. The bank also actively supports Small and Medium-sized Enterprises (SMEs) with tailored corporate banking solutions and caters to large corporations and institutions with comprehensive wholesale banking services. A key focus area is also on cross-boundary clients within the Greater Bay Area, facilitating seamless financial activities across Hong Kong, mainland China, Macau, and Taiwan.

Cost Structure

Staff Costs

Staff costs represent a substantial component of Bank of East Asia's (BEA) operational expenses, reflecting its investment in a global workforce of approximately 8,000 individuals. This outlay covers salaries, benefits, and ongoing training for a diverse team, including vital relationship managers, front-line branch staff, specialized IT professionals, and essential back-office personnel.

Human capital is a critical asset for BEA, and the bank allocates significant resources to attract, retain, and develop its employees. These investments are crucial for delivering quality customer service and maintaining efficient operations across its extensive network.

Technology and Infrastructure Costs

Bank of East Asia (BEA) dedicates substantial resources to its technology and infrastructure. These ongoing investments cover critical areas like upgrading IT systems, maintaining and enhancing digital platforms, and bolstering cybersecurity measures. For instance, in 2023, BEA continued its digital transformation journey, focusing on improving customer experience through technology, which inherently involves significant expenditure on software licenses and hardware.

The bank's commitment extends to its physical network, encompassing the maintenance of its extensive branch and ATM infrastructure. This includes costs associated with hardware upkeep, network connectivity, and ensuring the operational efficiency of these customer touchpoints. These expenditures are vital for providing seamless banking services across both digital and physical channels.

Marketing and Advertising Expenses

Marketing and advertising expenses are crucial for BEA to attract new customers and keep existing ones engaged in the competitive banking landscape. These costs cover a wide range of activities, from digital campaigns targeting specific demographics to traditional advertising in print and broadcast media. Promotional efforts, such as special offers on loans or savings accounts, also fall under this category.

In 2024, BEA continued to invest significantly in its brand presence. The bank's commitment to digital innovation in its marketing was recognized with several industry awards for its online campaigns and brand initiatives. These efforts are vital for customer acquisition, particularly among younger, digitally-savvy segments, and for reinforcing BEA's brand image as a reliable and forward-thinking financial institution.

Regulatory and Compliance Costs

Bank of East Asia, like all financial institutions, faces substantial regulatory and compliance costs. These expenses are essential for adhering to the complex web of banking regulations in its operating regions, particularly Hong Kong and mainland China. These costs cover maintaining robust compliance departments, conducting regular audits, and fulfilling extensive reporting obligations to various regulatory bodies.

The commitment to regulatory adherence is a non-negotiable aspect of the banking business, requiring significant and ongoing financial investment. For instance, in 2024, the financial services sector globally saw continued increases in compliance spending due to evolving regulations and heightened scrutiny. This investment ensures the bank operates legally and maintains the trust of its customers and stakeholders.

- Compliance Staffing: Costs associated with hiring and retaining skilled compliance officers and legal experts.

- Technology Investment: Expenditure on systems for monitoring transactions, managing risk, and ensuring data privacy.

- Reporting and Auditing: Fees for external auditors and the internal resources dedicated to preparing regulatory reports.

- Training and Development: Ongoing education for staff to stay abreast of changing regulatory landscapes.

Interest Expenses

Interest expenses are a significant cost for Bank of East Asia, largely driven by the interest paid on customer deposits and other borrowed funds. In 2024, the bank's cost of funds is directly tied to prevailing market interest rates and the total amount of deposits it holds.

Fluctuations in interest rates directly impact the bank's profitability by affecting its net interest margin. For instance, if interest rates rise, the bank will incur higher costs on its borrowings, potentially squeezing its profit margins if it cannot pass these costs on to borrowers.

- Cost of Funds: Primarily interest paid on customer deposits and wholesale funding.

- Interest Rate Sensitivity: Expenses rise with increasing market interest rates.

- Net Interest Margin Impact: Higher interest expenses can reduce profitability if not matched by increased interest income.

- 2024 Outlook: Interest expenses are expected to remain a key cost driver, influenced by central bank monetary policy.

Decoding a Bank's Operational Spending

Bank of East Asia's cost structure is multifaceted, encompassing significant investments in its human capital, technology, and physical infrastructure. Staff costs, covering approximately 8,000 employees globally, are a major outlay, supporting customer service and operational efficiency. Technology investments are crucial for digital transformation, platform enhancement, and cybersecurity, with ongoing spending in 2023 and 2024 focused on improving customer experience.

The bank also incurs costs for maintaining its branch and ATM network, ensuring seamless service across physical channels. Marketing and advertising are vital for customer acquisition and engagement, with a notable focus on digital campaigns in 2024. Furthermore, substantial resources are dedicated to regulatory compliance, a critical and growing expense in the financial sector, especially given evolving global regulations.

Interest expenses, primarily on customer deposits and borrowings, are a significant cost driver, directly influenced by market interest rates and impacting the bank's net interest margin. In 2024, these expenses remained a key factor, sensitive to central bank monetary policies.

| Cost Category | Description | 2023/2024 Relevance |

|---|---|---|

| Staff Costs | Salaries, benefits, training for ~8,000 employees | Essential for service delivery and operations |

| Technology & Infrastructure | IT systems, digital platforms, cybersecurity | Key for digital transformation and customer experience |

| Branch Network | Maintenance of branches and ATMs | Supports physical customer touchpoints |

| Marketing & Advertising | Customer acquisition and brand building | Focus on digital campaigns for engagement |

| Regulatory Compliance | Adherence to banking regulations | Non-negotiable, increasing expenditure globally |

| Interest Expenses | Interest on deposits and borrowings | Directly impacted by market interest rates |

Revenue Streams

Net Interest Income (NII)

Net Interest Income (NII) forms the bedrock of Bank of East Asia's (BEA) revenue generation. It's essentially the profit BEA makes from its core lending activities. This income is derived from the interest it earns on loans and advances provided to its diverse customer base, ranging from individuals seeking mortgages to corporations requiring substantial credit facilities.

This NII is calculated by subtracting the interest BEA pays out on customer deposits and other borrowings from the interest it collects on its loan portfolio. For instance, in 2024, BEA's net interest income was a significant contributor to its overall profitability, reflecting the volume of its lending operations and the prevailing interest rate environment.

The health of BEA's NII is directly tied to several key factors. These include the sheer volume of loans and advances it has outstanding, the spread between the interest rates it charges on loans and the rates it pays on deposits (its net interest margin), and broader market interest rate trends. A widening net interest margin, for example, would boost NII, assuming lending volumes remain stable.

Fee and Commission Income

Bank of East Asia generates significant revenue from fee and commission income, a vital component of its business model. This includes earnings from wealth management services, commissions on investment product sales, and fees associated with trade finance activities. For instance, in 2023, the bank reported a substantial contribution from its non-interest income, which is heavily influenced by these fee-based services, demonstrating its importance in diversifying revenue beyond traditional lending.

Further diversifying its income, the bank also earns from card services and remittance charges. These streams are directly linked to customer transaction volumes and the overall value of assets managed. The growth in these areas in 2023 reflects increased customer engagement and the bank's success in cross-selling various financial products and services, thereby bolstering its fee and commission revenue.

Insurance Premium Income

Bank of East Asia (BEA) generates substantial revenue through insurance premium income, primarily by acting as an appointed insurance agency for major providers like AIA and Blue Cross. This bancassurance model allows BEA to earn commissions and fees from selling a variety of life and general insurance policies directly to its existing customer base. In 2023, BEA's total income from insurance business reached HK$2.8 billion, demonstrating the significant contribution of this revenue stream to its overall financial performance.

Treasury and Investment Income

Treasury and Investment Income represents a significant revenue stream for the Bank of East Asia (BEA), stemming from its active management of its investment portfolio. This includes profits generated from trading various securities, engaging in foreign exchange transactions, and other treasury operations. The performance of this segment is closely tied to prevailing market conditions and the effectiveness of BEA’s investment strategies.

In 2024, BEA's treasury and investment activities continued to be a key contributor to its overall financial performance. The bank actively participates in global financial markets, offering a range of treasury products and investment solutions to its diverse client base. These offerings are designed to meet various client needs, from hedging foreign currency exposure to seeking capital appreciation.

- Securities Trading Gains: Income generated from the buying and selling of debt and equity securities within the bank's proprietary trading book.

- Foreign Exchange (FX) Operations: Profits derived from currency trading, including spot and forward transactions, as well as managing the bank's foreign currency positions.

- Interest Income from Investments: Earnings from interest-bearing assets held in the investment portfolio, such as bonds and other fixed-income instruments.

- Other Treasury Activities: Revenue from various treasury services and financial instruments, which may include derivatives and structured products.

Other Operating Income

Other Operating Income for The Bank of East Asia (BEA) encompasses a variety of non-traditional banking revenue sources. These can include income generated from renting out bank-owned properties, fees for various administrative and transactional services, and other miscellaneous earnings that fall outside core lending and deposit activities.

While these streams are generally smaller in scale compared to interest income from loans or trading activities, they play a role in diversifying the bank's overall revenue profile. For instance, in 2023, BEA reported other operating income of HKD 1,612 million, contributing to its total revenue.

- Rental Income: Revenue generated from leasing out bank premises or other owned real estate.

- Service Charges: Fees collected for services such as account maintenance, transaction processing, and wealth management advisory.

- Other Non-Core Revenues: This can include gains from the disposal of assets or other incidental income not directly related to primary banking operations.

Revenue Streams: A Look at the Bank's Financial Performance

Net Interest Income (NII) remains the primary revenue driver for Bank of East Asia, reflecting the spread between interest earned on loans and interest paid on deposits. In 2024, this segment continued to be crucial, with the bank's net interest margin playing a key role in its profitability.

Fee and commission income, derived from wealth management, investment products, and trade finance, offers significant diversification. In 2023, non-interest income, heavily influenced by these fees, demonstrated BEA's success in cross-selling financial services.

Insurance premium income, generated through bancassurance partnerships, contributed substantially, with HK$2.8 billion earned in 2023. Treasury and investment activities also added to revenue through securities trading and FX operations, with 2024 seeing continued active participation in global markets.

Other operating income, including rental income and service charges, provided additional diversification, with HKD 1,612 million reported in 2023. These various streams collectively form BEA's comprehensive revenue generation strategy.

| Revenue Stream | 2023 (HK$ Billion) | 2024 (Estimate/Trend) | Key Drivers |

|---|---|---|---|

| Net Interest Income | [Data not available for 2023, but significant contributor] | Continued strong performance driven by loan volume and net interest margin. | Loan portfolio size, net interest margin, interest rate environment. |

| Fee and Commission Income | [Data not available as a single figure, but significant] | Expected growth from wealth management and digital services. | Wealth management, investment sales, trade finance, card services. |

| Insurance Premium Income | 2.8 | Stable to growing, supported by bancassurance partnerships. | Bancassurance partnerships (AIA, Blue Cross), customer base. |

| Treasury and Investment Income | [Data not available as a single figure, but significant] | Market conditions and trading performance. | Securities trading, FX operations, investment portfolio performance. |

| Other Operating Income | 1.612 | Consistent contribution from non-core activities. | Rental income, service charges, asset disposals. |

Business Model Canvas Data Sources

The Business Model Canvas for Bank of East Asia is built upon a foundation of robust financial reports, extensive market research, and internal strategic planning documents. These sources ensure each block is informed by accurate, validated information.