Axis Capital Holdings Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Axis Capital Holdings Bundle

Go Beyond the Preview—Access the Full Strategic Report

Axis Capital Holdings operates in a market shaped by intense competition and evolving customer demands. Understanding the power of buyers and the threat of substitutes is crucial for navigating this landscape. Our analysis delves into these forces, revealing the strategic levers available to Axis Capital Holdings.

The complete report reveals the real forces shaping Axis Capital Holdings’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Capital Providers

The global reinsurance market demonstrated robust capitalization in 2024, with significant capital inflows bolstering the sector. This trend is expected to continue into 2025, fueled by strong industry earnings and renewed investor optimism. Axis Capital, like its peers, benefits from this ample supply of capital, which includes a substantial $113 billion from alternative capital sources, thereby moderating the bargaining power of capital providers.

While the abundance of capital generally lessens its leverage, the cost of this capital remains a critical factor influencing the industry's pricing strategies and overall profitability. This dynamic means that even with plentiful funding options, reinsurers must carefully manage their cost of capital to maintain competitive pricing and healthy returns.

Specialized Talent

The insurance and reinsurance sectors, especially when dealing with intricate and developing risks like cyber threats or environmental damage, rely heavily on specialized professionals. Think of expert underwriters, actuaries, and claims handlers; they are indispensable suppliers. Axis Capital Holdings, like its peers, needs to secure and keep this talent to stay competitive and maintain strong underwriting practices.

The scarcity of individuals with deep expertise in these niche areas grants these skilled professionals significant leverage. For instance, in 2024, the demand for cybersecurity insurance underwriters continued to outstrip supply, a trend expected to persist as cyber threats evolve.

Technology and Data Providers

As Axis Capital invests heavily in its 'How We Work' program and embraces advanced technology, the bargaining power of technology and data providers is on the rise. These firms offer critical tools for risk modeling, underwriting, and boosting operational efficiency, making them indispensable for staying competitive in the evolving insurance market. For instance, the global market for AI in insurance is projected to reach $10.2 billion by 2025, highlighting the increasing reliance and thus, the leverage of these tech suppliers.

Retrocessionaires

Retrocessionaires, who provide reinsurance for reinsurers like Axis Capital, hold significant bargaining power. The availability and cost of this retrocessional capacity are heavily influenced by market conditions and the frequency of large insured events, which can lead to price volatility. Axis's active management of these relationships, including recent loss portfolio transfers, demonstrates the importance of these arrangements.

The bargaining power of retrocessionaires stems from their ability to influence the supply and pricing of reinsurance capacity. This power is amplified during periods of heightened risk or following major catastrophe events, as capacity can become scarce. For instance, in the first half of 2024, the global reinsurance market continued to see hardening rates, particularly for property catastrophe risks, which directly impacts the cost and availability of retrocession for companies like Axis.

- Supply and Demand Dynamics: The availability of retrocessional capacity is a key driver of supplier power. When fewer reinsurers offer retrocessional coverage, or when demand from primary insurers and reinsurers surges, retrocessionaires can command higher prices.

- Market Cycles and Loss Events: Major insured losses, such as those experienced in 2023 with significant natural catastrophe events, can reduce the appetite of retrocessionaires to take on risk, thereby increasing their bargaining power.

- Capital Availability: The amount of capital available in the retrocession market, including from alternative capital providers like insurance-linked securities (ILS) funds, influences pricing and terms. Changes in ILS market performance can shift bargaining power.

Financial Market Conditions

Broader financial market conditions, particularly interest rates, are a crucial factor for insurers like Axis Capital Holdings. As of early 2024, the Federal Reserve maintained a target range for the federal funds rate, influencing investment yields across the market. For reinsurers, higher interest rate environments typically translate to increased investment income, which directly bolsters their overall profitability and financial strength.

The impact of these conditions on investment income is substantial. For instance, a rise in yields can significantly boost the returns generated from an insurer's large investment portfolios. This increased investment income can offset underwriting losses or enhance overall profitability, making the financial market environment a key determinant of an insurer's performance.

- Interest Rate Environment: Higher interest rates in 2024 generally improved investment income for insurers, contributing positively to their financial results.

- Investment Yields: For example, the average yield on U.S. Treasury bonds saw notable increases in early 2024 compared to previous periods, directly benefiting insurers' investment portfolios.

- Capital Attractiveness: Fluctuations in market conditions can alter the cost and availability of capital for the insurance industry, impacting strategic decisions and growth opportunities.

Supplier Power Shapes Reinsurer Costs and Capacity

Axis Capital Holdings, like other reinsurers, faces bargaining power from suppliers of specialized talent, particularly in niche areas like cyber risk underwriting. The scarcity of these experts in 2024 meant they could command higher compensation and more favorable terms. This trend is expected to continue as evolving risks demand specialized knowledge.

Technology and data providers also exert significant influence, as demonstrated by the projected $10.2 billion global market for AI in insurance by 2025. Axis's investment in advanced tools for risk modeling and operational efficiency highlights its reliance on these suppliers, granting them considerable leverage.

Retrocessionaires, who reinsure reinsurers, hold substantial power, especially following periods of high insured losses. In the first half of 2024, hardening rates in the property catastrophe reinsurance market directly increased the cost and reduced the availability of retrocessional capacity for companies like Axis.

| Supplier Type | Key Factor Influencing Power | Impact on Axis Capital | 2024/2025 Data Point |

|---|---|---|---|

| Specialized Talent | Scarcity of expertise in niche risks | Increased labor costs, retention challenges | High demand for cyber underwriters |

| Technology & Data Providers | Criticality of tools for risk modeling/efficiency | Reliance on vendor solutions, potential price increases | Global AI in insurance market projected at $10.2B by 2025 |

| Retrocessionaires | Availability and cost of reinsurance capacity | Higher retrocession costs, potential capacity constraints | Hardening rates in property catastrophe market (H1 2024) |

What is included in the product

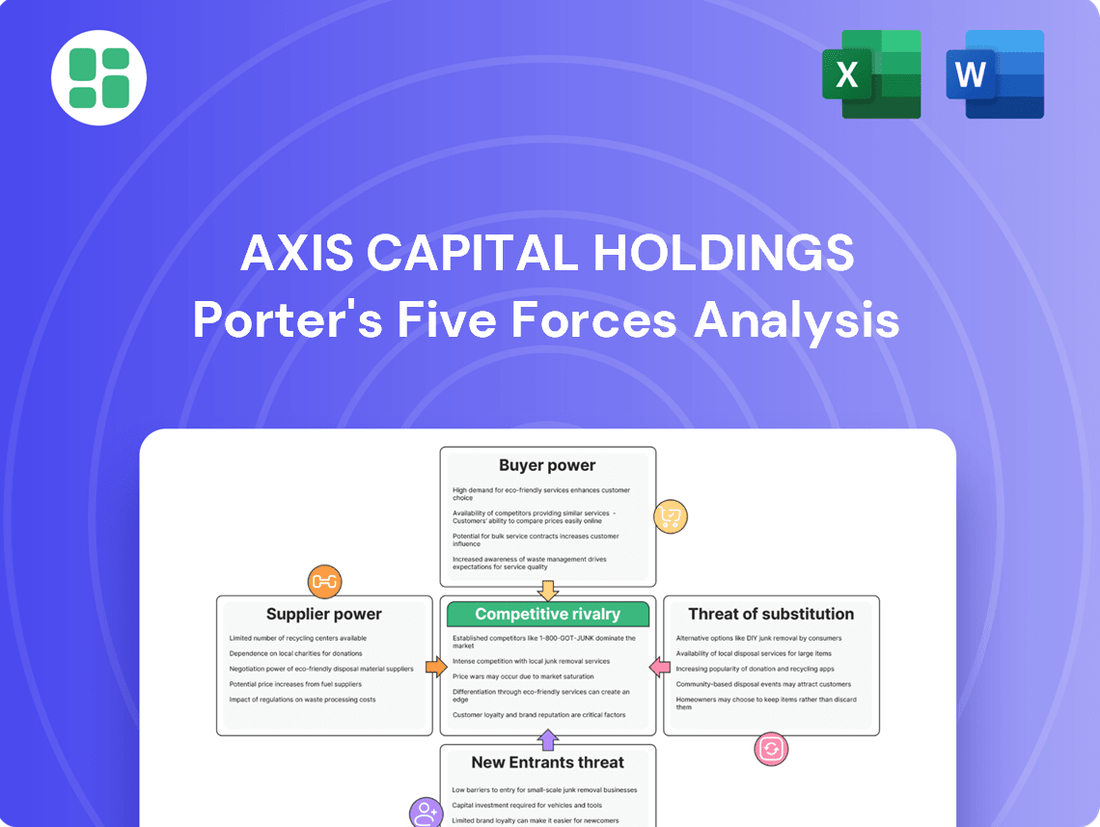

This analysis unpacks the competitive forces shaping Axis Capital Holdings' market, focusing on industry rivalry, buyer and supplier power, new entrant threats, and the impact of substitutes.

Instantly identify and strategize around competitive pressures with a clear, actionable Porter's Five Forces analysis, designed to pinpoint and alleviate market-related pain points for Axis Capital Holdings.

Customers Bargaining Power

Large Corporate and Insurer Clients

Axis Capital Holdings primarily serves large corporate clients, primary insurers, and governmental bodies looking for specialized insurance and reinsurance. These sophisticated clients, especially large corporations and primary insurers, wield considerable bargaining power. This strength stems from the sheer volume of premiums they contribute, enabling them to negotiate favorable terms and conditions.

Their ability to manage risk effectively and their access to a wide array of alternative insurance providers further bolster their negotiating position. For instance, in the specialty insurance market, clients with substantial risk portfolios can often demand customized coverage and competitive pricing, directly impacting Axis Capital's profitability.

Market Capacity and Pricing Trends

The reinsurance market's increasing capacity, with projections of softer conditions by 2025, significantly bolsters customer bargaining power. Primary insurers are actively seeking more advantageous pricing and improved terms, particularly in property reinsurance where rate moderation is already evident.

This transition away from a hard market empowers cedents to negotiate better terms, thereby exerting downward pressure on reinsurers' profit margins. For instance, reports indicate a notable increase in available capital in the reinsurance sector, potentially exceeding $650 billion by the end of 2024, a key factor enabling customers to demand more competitive offerings.

Demand for Specific Coverage

Even with broad market shifts, there's a persistent and growing appetite for specialized insurance. This is particularly true for newer, more complex risks such as cyberattacks and the fallout from climate change. This strong demand for niche coverage gives providers like Axis Capital significant leverage.

When clients need coverage for unique or high-risk situations where specialized expertise is rare, their bargaining power diminishes. This is especially evident in the reinsurance market, where insurers are actively seeking coverage for emerging product lines, directly fueling the demand for facultative reinsurance services.

Underwriting Discipline and Portfolio Management

Axis Capital's commitment to underwriting discipline directly impacts customer bargaining power. By meticulously managing risk selection and ensuring premium adequacy, Axis can resist pressure for lower rates, particularly on less attractive business segments. This strategic approach allows them to maintain profitable pricing and select clients that align with their risk appetite.

In 2024, a focus on disciplined underwriting by companies like Axis Capital, which aims for premium growth while managing exposure, can limit the power of customers seeking significant price concessions. For instance, if the market experiences a hardening cycle, customers have less leverage to demand lower premiums, especially for specialized insurance products where Axis demonstrates expertise.

- Underwriting Discipline: Axis Capital prioritizes rigorous risk assessment and pricing to ensure profitability, thereby limiting customer leverage for lower rates.

- Portfolio Management: By shaping a resilient portfolio, Axis can better withstand market fluctuations and reduce customer power in less profitable lines.

- Premium Adequacy: Maintaining adequate premiums allows Axis to push back against excessive customer demands, especially when market conditions are favorable for insurers.

- Risk Selection: The ability to select risks that meet profitability targets directly curtails the bargaining power of customers seeking unfavorable terms.

Financial Strength and Ratings

Customers, particularly major primary insurers, place significant emphasis on the financial strength and credit ratings of reinsurers. This focus stems from the need to ensure the reinsurer's ability to pay claims and maintain long-term stability. Axis Capital Holdings, with its strong financial ratings, including an A+ (Superior) financial strength rating from AM Best as of early 2024, demonstrates a key competitive advantage.

This robust financial standing directly impacts the bargaining power of customers. When clients perceive a reinsurer as financially sound and well-capitalized, their leverage is diminished. They are less likely to demand concessions when they trust the reinsurer's capacity to meet its obligations, thereby reinforcing Axis Capital's position.

- Financial Strength Ratings: Axis Capital Holdings maintains strong credit ratings from major agencies, reflecting its solid financial health and claims-paying ability. For example, as of early 2024, AM Best affirmed Axis Capital's A+ (Superior) financial strength rating.

- Capital Adequacy: The company consistently demonstrates strong capital adequacy ratios, providing a substantial buffer against potential losses and ensuring stability. This capital position is a critical factor for large institutional clients.

- Customer Preference for Stability: Primary insurers often prioritize reinsurers that offer a high degree of financial security and predictability to safeguard their own balance sheets and long-term operational continuity.

- Reduced Customer Leverage: Axis Capital's financial robustness translates into reduced bargaining power for its customers, as they are more inclined to partner with a secure and reliable reinsurer, limiting their ability to negotiate unfavorable terms.

Reinsurance Client Power: Capacity, Niche Expertise, and Financial Stability

The bargaining power of customers for Axis Capital Holdings is significant, particularly among large corporate clients and primary insurers. These sophisticated buyers leverage their substantial premium volumes and ability to access alternative markets to negotiate favorable terms and pricing. For instance, the increasing capacity in the reinsurance market, projected to exceed $650 billion by the end of 2024, empowers cedents to demand more competitive offerings, thereby pressuring reinsurers' profit margins.

Axis Capital's strong financial standing, evidenced by its A+ (Superior) financial strength rating from AM Best as of early 2024, mitigates some of this customer leverage. Clients are often willing to accept less favorable terms when they trust a reinsurer's financial stability and claims-paying ability, reinforcing Axis Capital's market position.

However, the demand for specialized insurance covering complex risks like cyber threats and climate change provides Axis Capital with a counterbalancing advantage. In these niche areas where specialized expertise is scarce, customer bargaining power diminishes, allowing Axis to command better pricing and terms.

| Factor | Impact on Customer Bargaining Power | Axis Capital's Response/Mitigation |

|---|---|---|

| Premium Volume & Market Access | High | Underwriting discipline, risk selection |

| Reinsurance Market Capacity (2024 projection: >$650B) | Increasing | Focus on premium adequacy, portfolio management |

| Demand for Specialized Coverage | Low | Leverage niche expertise, facultative reinsurance |

| Financial Strength (AM Best A+ rating, early 2024) | Low | Emphasize stability and reliability to clients |

Preview Before You Purchase

Axis Capital Holdings Porter's Five Forces Analysis

This preview showcases the complete Porter's Five Forces analysis for Axis Capital Holdings, offering a detailed examination of industry competitiveness and profitability. You are viewing the exact, professionally formatted document that will be delivered to you instantly upon purchase, providing immediate strategic insights.

Rivalry Among Competitors

Global Specialty Market Players

Axis Capital Holdings faces intense competition in the global specialty insurance and reinsurance sector. Major players like Allianz, AXA, Chubb, and QBE possess significant financial strength and broad market reach, directly challenging Axis for market share across various specialty lines. This crowded landscape means rivalry is a constant factor.

Market Stability and Profitability

The reinsurance market is enjoying a period of robust profitability, with projections indicating that reinsurers will likely earn their cost of capital in 2024 and 2025. This favorable environment, supported by strong capital positions and enhanced underwriting performance, naturally spurs existing participants to aggressively seek out growth.

This heightened pursuit of profitable business within a stable market can intensify competitive rivalry among established reinsurers. As all players aim to capitalize on favorable conditions, the competition for attractive contracts and market share becomes more pronounced.

Pricing Pressures and Underwriting Discipline

While certain short-tail insurance lines have experienced favorable pricing, competitive pressures are causing a moderation, and in some cases, softening of rates, especially within property reinsurance. This dynamic demands robust underwriting discipline from firms like Axis Capital to sustain profitability.

Axis Capital's ability to manage its combined ratio effectively is paramount in navigating this competitive pricing landscape. For instance, in the first quarter of 2024, Axis Capital reported an insurance segment combined ratio of 88.7%, demonstrating strong operational performance despite market pressures.

Product Differentiation and Specialization

Axis Capital Holdings actively differentiates itself by concentrating on specialty insurance products and employing specialized underwriting. This strategy diminishes direct competition in more standardized insurance segments.

The company's strategic expansion into emerging sectors such as energy transition and cybersecurity, coupled with focused growth in high-demand specialty markets, enables it to establish distinct market positions and achieve more favorable pricing.

- Specialty Focus: Axis Capital's emphasis on niche markets like terrorism, political risk, and aviation insurance reduces head-to-head competition with insurers focused on broader, less specialized lines.

- Underwriting Expertise: By developing deep expertise in complex risks, Axis Capital can offer tailored solutions that generalist insurers may not be equipped to provide, thereby commanding a pricing premium.

- Market Share in Specialties: In 2024, Axis Capital continued to hold significant market share in several key specialty lines, demonstrating its competitive strength in these differentiated areas. For instance, in the aviation insurance market, its share remained robust, reflecting its specialized capabilities.

Consolidation and M&A Activity

The insurance market, including specialty lines where Axis Capital operates, is indeed seeing a significant wave of consolidation. This trend means that rather than entirely new, disruptive companies entering the fray, existing, larger players are acquiring or merging with others to bolster their scale and market share. For instance, in 2024 alone, the global insurance M&A market saw substantial activity, with deals valued in the tens of billions of dollars, reflecting this drive for consolidation.

This increased M&A activity means fewer, but larger, competitors are emerging. These strengthened entities often possess greater financial clout and broader product offerings, intensifying the competitive landscape for companies like Axis Capital. Axis Capital's own participation in or response to these consolidation moves directly influences its competitive positioning.

- Market Consolidation: The insurance sector is experiencing a trend where mergers and acquisitions are more prevalent than the rise of entirely new market entrants.

- Strengthened Incumbents: Existing large players are enhancing their market positions through these M&A activities, leading to fewer, but more powerful, competitors.

- Increased Scale and Power: The remaining entities after consolidation often gain significant scale and market power, altering the competitive dynamics.

- Axis Capital's Role: Axis Capital's strategic decisions, whether as an acquirer or target, are integral to this ongoing consolidation trend.

Reinsurance Profitability Fuels Fierce Market Share Battles

Axis Capital Holdings operates in a highly competitive global specialty insurance and reinsurance market. The profitability observed in the reinsurance sector during 2024 and early 2025 incentivizes existing players to aggressively pursue market share, intensifying rivalry. While Axis focuses on specialty lines, which offers some differentiation, the overall market consolidation trend means fewer but larger, more powerful competitors are emerging, demanding continuous strategic adaptation.

SSubstitutes Threaten

Self-Insurance and Captive Solutions

Large corporations and governmental bodies, significant clients for Axis Capital, increasingly explore self-insurance or establish captive insurance companies. This allows them to internalize risk management, especially for predictable or substantial liabilities, thereby retaining premiums and enhancing control. For instance, by 2024, the global captive insurance market was projected to exceed $200 billion in premiums written, highlighting the scale of this alternative.

Alternative Risk Transfer (ART) Mechanisms

The increasing availability of Alternative Risk Transfer (ART) mechanisms, like catastrophe bonds and other Insurance-Linked Securities (ILS), poses a substantial threat to traditional reinsurance. These ARTs enable capital markets to directly absorb insurance-related risks, offering policyholders alternative and often more economical protection, particularly for major property catastrophe events. For instance, the ILS market saw significant growth, with total ILS capacity reaching approximately $90 billion by the end of 2023, demonstrating a clear shift towards these capital markets solutions.

Enhanced Risk Management and Prevention

Clients are increasingly investing in robust internal risk management and loss prevention. This trend directly impacts the demand for external insurance and reinsurance, as companies aim to self-insure more effectively. For instance, in 2024, many large corporations allocated a greater portion of their operational budgets to advanced cybersecurity measures and supply chain resilience programs, anticipating fewer claims.

Technological advancements, particularly in data analytics and predictive modeling, are empowering businesses to proactively manage their risks. This enhanced capability can diminish the perceived need for traditional risk transfer mechanisms. Companies are leveraging AI-driven insights to identify potential vulnerabilities, thereby reducing their reliance on third-party coverage providers.

Government-Backed Programs and Pools

Government-backed programs and industry pools can significantly limit the appeal of private specialty insurers, especially for systemic or catastrophic risks. For instance, in the United States, the National Flood Insurance Program (NFIP) provides flood coverage that is often a substitute for private flood insurance, particularly in high-risk areas. This program, managed by FEMA, had approximately 4.7 million policies in force as of early 2024, demonstrating its substantial market presence.

Similarly, programs like the Terrorism Risk Insurance Act (TRIA) in the US create a backstop for terrorism-related losses, reducing the demand for purely private terrorism coverage. TRIA's effectiveness in providing a safety net means that private insurers face a reduced opportunity to offer standalone, high-premium terrorism insurance. This governmental intervention directly impacts the market size for private reinsurers specializing in such perils.

- Government programs like the NFIP provide a direct substitute for private flood insurance, impacting market penetration for private insurers.

- TRIA acts as a government backstop for terrorism risk, diminishing the market for private terrorism insurance offerings.

- These publicly sponsored alternatives limit the pricing power and market share of private specialty insurers in specific, high-risk segments.

Financial Derivatives and Hedging Tools

Financial derivatives and hedging tools present a subtle but present threat to traditional insurance offerings, particularly in specialized markets. While not a complete replacement for comprehensive insurance, these instruments can mitigate specific financial risks, potentially diverting demand for certain insurance products.

For instance, companies facing currency fluctuations might opt for forward contracts or currency options instead of seeking foreign exchange insurance. Similarly, commodity producers could use futures or options to hedge against price volatility, reducing their reliance on commodity-linked insurance. The global derivatives market is substantial; for example, the Bank for International Settlements reported in 2022 that the notional amount outstanding of over-the-counter (OTC) derivatives was USD 600 trillion, highlighting the scale of these alternative risk management tools.

- Derivatives as substitutes: Financial derivatives like futures, options, and swaps allow companies to manage specific market risks such as currency, interest rate, and commodity price fluctuations.

- Reduced demand for specialty insurance: The availability of these hedging instruments can diminish the need for certain specialty insurance products designed to cover these same risks.

- Market size: The global OTC derivatives market, valued in the hundreds of trillions of dollars, demonstrates the significant capacity of these financial tools to absorb risk.

- Risk mitigation focus: While insurance provides broad protection, derivatives offer targeted mitigation for particular financial exposures.

Risk Transfer Redefined: New Market Dynamics

The threat of substitutes for Axis Capital arises from entities choosing to manage their own risks or utilize alternative financial instruments. Large corporations increasingly opt for self-insurance or establish captive insurance companies, retaining premiums and control over their liabilities. By 2024, the global captive insurance market was projected to surpass $200 billion in premiums written, underscoring the significant scale of this alternative.

Alternative Risk Transfer (ART) mechanisms, such as catastrophe bonds and Insurance-Linked Securities (ILS), directly compete with traditional reinsurance. These instruments allow capital markets to absorb insurance risks, offering potentially more economical protection, especially for major catastrophe events. The ILS market capacity reached approximately $90 billion by the end of 2023, indicating a growing reliance on these capital markets solutions.

Furthermore, advances in data analytics and predictive modeling empower businesses to enhance their internal risk management and loss prevention strategies. This reduces the perceived necessity for external insurance coverage, as companies become more adept at identifying and mitigating potential vulnerabilities proactively.

| Substitute Type | Description | Market Indicator / Data Point | Impact on Axis Capital |

| Self-Insurance/Captives | Companies managing their own risks internally. | Global captive insurance market projected >$200 billion in premiums (2024). | Reduces demand for traditional insurance and reinsurance. |

| Alternative Risk Transfer (ART) / ILS | Capital markets directly absorbing insurance risks. | ILS market capacity approx. $90 billion (end of 2023). | Offers alternative, potentially cheaper, risk transfer options. |

| Internal Risk Management | Enhanced internal capabilities reducing reliance on external providers. | Increased corporate spending on advanced risk mitigation technologies. | Diminishes the need for certain insurance products. |

Entrants Threaten

High Capital Requirements

Entering the specialty insurance and reinsurance market, where Axis Capital Holdings operates, demands significant upfront capital. This high barrier to entry means new companies need substantial financial resources to even begin operations, effectively limiting the number of potential competitors.

Establishing the necessary underwriting capacity and maintaining the robust solvency ratios required by regulators and rating agencies, such as those overseen by bodies like the NAIC in the US or equivalent international organizations, necessitates considerable financial strength. For instance, in 2024, many specialty insurers are expected to maintain risk-based capital ratios well above regulatory minimums, often in the hundreds of percentage points, to ensure stability and investor confidence.

Stringent Regulatory Environment

The insurance and reinsurance sectors are globally subject to rigorous regulatory frameworks. These include demanding licensing procedures, stringent solvency capital requirements, and extensive compliance mandates that vary significantly across different countries. For instance, in 2024, the European Union continued to enforce Solvency II directives, which dictate capital adequacy and risk management for insurers, requiring substantial upfront investment for any new entrant aiming to operate within its member states.

This complex web of regulations creates a substantial barrier to entry for potential new competitors. Establishing the necessary legal and compliance infrastructure to navigate these rules demands considerable financial resources and specialized expertise. Axis Capital Holdings, as a global player, must adhere to these diverse and often overlapping regulatory requirements in each market it serves, underscoring the high cost and complexity of entering this industry.

Need for Specialized Expertise and Reputation

The need for specialized expertise and a strong reputation presents a significant barrier to entry in the insurance sector. Building a credible underwriting team with deep knowledge in niche specialty lines, alongside a proven track record in claims handling and financial stability, requires substantial investment and time. Newcomers would find it challenging to immediately rival established entities like Axis Capital, which benefits from a long history and well-cultivated client relationships.

Access to Distribution Channels

Access to established distribution channels, particularly broker networks and direct client relationships, presents a significant barrier to entry in the specialty insurance and reinsurance sector. Axis Capital, like its peers, benefits from decades of cultivating these vital connections.

New entrants struggle to replicate the deep-rooted trust and preferred access that incumbents enjoy with clients and brokers. This makes it challenging for them to build a substantial book of business quickly, as gaining initial traction requires overcoming established loyalties and distribution agreements.

For instance, in 2024, the insurance brokerage market continued to consolidate, with major players like Marsh McLennan and Aon reporting strong revenue growth, further solidifying their control over distribution. This trend amplifies the difficulty for new specialty insurers to secure placement for their offerings.

- Broker Network Dominance: Established insurers have long-standing, often exclusive, relationships with key insurance brokers who control client access.

- Client Relationships: Direct client relationships built over time foster loyalty and make it difficult for new entrants to attract business.

- Cost of Access: Gaining access to these channels can involve significant upfront investment in marketing, relationship building, and potentially paying fees or commissions.

- Market Inertia: Clients and brokers are often hesitant to switch from established, trusted providers to unproven new entrants, even with competitive pricing.

Market Concentration and Competitive Response

The specialty insurance and reinsurance sector is characterized by significant market concentration, with a few large, established firms holding considerable sway. For instance, in 2024, the top five global reinsurers, including giants like Munich Re and Swiss Re, continued to dominate market share, reflecting this ongoing concentration.

While there has been an influx of capital into the insurance industry, particularly in recent years, this hasn't translated into a significant threat of new entrants capable of disrupting established market discipline. Instead, the prevailing trend points towards consolidation among existing players, as firms seek economies of scale and enhanced market positioning.

- Market Concentration: The specialty insurance and reinsurance market remains highly concentrated, with dominant players controlling a substantial portion of the industry.

- Capital Influx vs. New Entrants: Despite increased capital availability, new entrants are not anticipated to significantly challenge existing market discipline.

- Consolidation Trend: The more probable outcome of increased capital is further consolidation among existing firms, rather than new market disruptors.

- Established Firm Response: Incumbent companies possess the financial strength and market leverage to effectively counter any emerging threats, thereby raising the barrier to entry for newcomers.

High Barriers Protect Specialty Insurance Market

The threat of new entrants in the specialty insurance and reinsurance market, where Axis Capital Holdings operates, remains relatively low. Significant capital requirements, stringent regulatory hurdles, and the need for specialized expertise act as substantial barriers. Furthermore, established distribution channels and client relationships are difficult for newcomers to replicate, reinforcing the dominance of existing players.

| Barrier Type | Description | Impact on New Entrants |

| Capital Requirements | High upfront capital needed for solvency and operations. | Limits the number of well-funded entrants. |

| Regulatory Compliance | Complex licensing, solvency, and compliance mandates globally. | Increases cost and time to market. |

| Specialized Expertise | Need for deep underwriting knowledge and claims handling skills. | Challenging to build a credible team quickly. |

| Distribution Channels | Dominance of established broker networks and client relationships. | Difficult to gain access and build business. |

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis for Axis Capital Holdings is built upon a robust foundation of data, including their annual reports, SEC filings, and investor presentations. We also incorporate insights from reputable industry research firms and financial news outlets to capture the broader competitive landscape.