South Indian Bank Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

South Indian Bank Bundle

A Must-Have Tool for Decision-Makers

South Indian Bank navigates a competitive landscape shaped by the collective power of its customers and the constant threat of new entrants. Understanding these forces is crucial for any strategic decision.

The full analysis reveals the nuanced interplay of supplier power and the intensity of rivalry within the banking sector, offering a comprehensive view of South Indian Bank's market position.

Ready to gain a deeper understanding of the factors influencing South Indian Bank's success? Unlock the complete Porter's Five Forces Analysis to uncover actionable insights and strategic advantages.

Suppliers Bargaining Power

Depositors

Depositors exert moderate to high bargaining power, particularly large institutional and high-net-worth individuals who control substantial capital. South Indian Bank, like its peers, depends heavily on deposits for funding, granting these major depositors significant influence.

For smaller retail depositors, bargaining power is somewhat limited by low switching costs, as they can easily move funds to competing banks or digital platforms. In 2024, the Indian banking sector saw deposit growth, with South Indian Bank aiming to attract and retain these crucial funds through competitive interest rates and services.

Technology Providers

The bargaining power of technology providers for South Indian Bank is on the rise. This is largely because banks, including South Indian Bank, are increasingly dependent on sophisticated digital systems, robust cybersecurity, and cutting-edge AI and machine learning tools to stay competitive and drive their digital transformation efforts. For instance, the global banking software market was valued at approximately USD 35 billion in 2023 and is projected to grow significantly, indicating high demand for these specialized services.

This growing reliance grants specialized tech vendors considerable leverage, as South Indian Bank needs these solutions to enhance its digital offerings and maintain operational efficiency. However, this power isn't absolute. The presence of numerous vendors in the market and South Indian Bank's strategic approach to developing certain technological capabilities internally can help to temper the influence these suppliers wield.

Human Capital

South Indian Bank faces significant bargaining power from skilled human capital, especially in high-demand areas like digital banking and data analytics. The competition for these specialized roles in India's banking sector is intense, often leading to increased salary expectations and recruitment challenges.

In 2024, the average salary for experienced data scientists in Indian banking saw a notable increase, reflecting the tight labor market. This trend directly impacts South Indian Bank's ability to attract and retain top talent, potentially affecting its operational agility and its capacity to drive innovation in a rapidly evolving digital landscape.

Interbank Market and Financial Institutions

The interbank market and other financial institutions are crucial suppliers of liquidity and wholesale funding for banks like South Indian Bank. When liquidity is scarce or risk appetite diminishes, their bargaining power increases, translating to higher borrowing costs. For instance, during periods of global financial stress, interbank lending rates can spike significantly, impacting a bank's profitability.

South Indian Bank's financial health plays a role in mitigating this supplier power. A strong capital adequacy ratio, such as South Indian Bank's reported 14.03% as of March 31, 2024, demonstrates its ability to absorb losses and reduces its reliance on potentially expensive wholesale funding. Similarly, maintaining high asset quality, evidenced by a Gross NPA ratio of 4.14% in the same period, signals stability and can lead to more favorable terms from funding providers.

- Interbank Market as Supplier: Provides essential liquidity and wholesale funding.

- Supplier Power Drivers: Tight liquidity and increased risk perception elevate borrowing costs.

- South Indian Bank's Resilience: Strong capital adequacy (14.03% as of March 31, 2024) and good asset quality (4.14% Gross NPA as of March 31, 2024) offer a buffer against supplier pressure.

Regulatory Bodies

Regulatory bodies, such as the Reserve Bank of India (RBI), wield significant influence over South Indian Bank, even though they aren't traditional suppliers. Their power stems from setting licensing requirements, enforcing compliance, and introducing policy shifts that directly affect operations. For instance, RBI's directives on capital adequacy ratios, like the Basel III norms, mandate specific levels of capital banks must hold, impacting their lending capacity and profitability.

These stringent norms on asset quality and digital lending practices compel banks to invest in robust risk management systems and technology upgrades. The RBI's ongoing emphasis on financial stability and strengthening intermediaries means South Indian Bank must remain agile, continuously adapting its strategies and operations to meet evolving regulatory landscapes. In 2023, the Indian banking sector saw increased regulatory scrutiny, with the RBI issuing new guidelines for digital lending and cybersecurity, underscoring the continuous need for adaptation.

- RBI's Capital Adequacy Norms: Banks like South Indian Bank must maintain specific capital-to-risk-weighted assets ratios, influencing their lending activities.

- Compliance Costs: Adhering to regulations incurs operational costs for technology, reporting, and personnel.

- Policy Changes: Sudden policy shifts, like interest rate adjustments or new lending guidelines, can immediately impact a bank's revenue and strategic direction.

- Digital Lending Regulations: The RBI's focus on fair practices and data protection in digital lending necessitates compliance investments.

Bank Supplier Power: A Multifaceted Analysis

The bargaining power of suppliers for South Indian Bank is a multifaceted issue, with key players including depositors, technology providers, and the interbank market. While large depositors and high-net-worth individuals hold considerable sway due to the bank's reliance on their funds, retail depositors have less power. Technology vendors are gaining leverage as banks increasingly depend on digital solutions.

Skilled human capital, particularly in digital banking and data analytics, represents another significant supplier group with growing bargaining power. The interbank market and other financial institutions also exert influence, especially during periods of tight liquidity, which can drive up borrowing costs for South Indian Bank. Regulatory bodies, while not traditional suppliers, significantly impact operations through their policy directives and compliance mandates.

| Supplier Group | Bargaining Power Level | Key Factors Influencing Power |

|---|---|---|

| Depositors (Large/HNI) | Moderate to High | Substantial capital control, bank's reliance on deposits |

| Depositors (Retail) | Limited | Low switching costs, ease of moving funds |

| Technology Providers | Rising | Increasing dependence on digital systems, AI, cybersecurity |

| Skilled Human Capital | High | Intense competition for digital/data talent, rising salaries |

| Interbank Market/Financial Institutions | Variable (increases with scarcity) | Liquidity availability, risk perception, wholesale funding needs |

| Regulatory Bodies (e.g., RBI) | High (Indirect) | Policy mandates, compliance requirements, capital adequacy norms |

What is included in the product

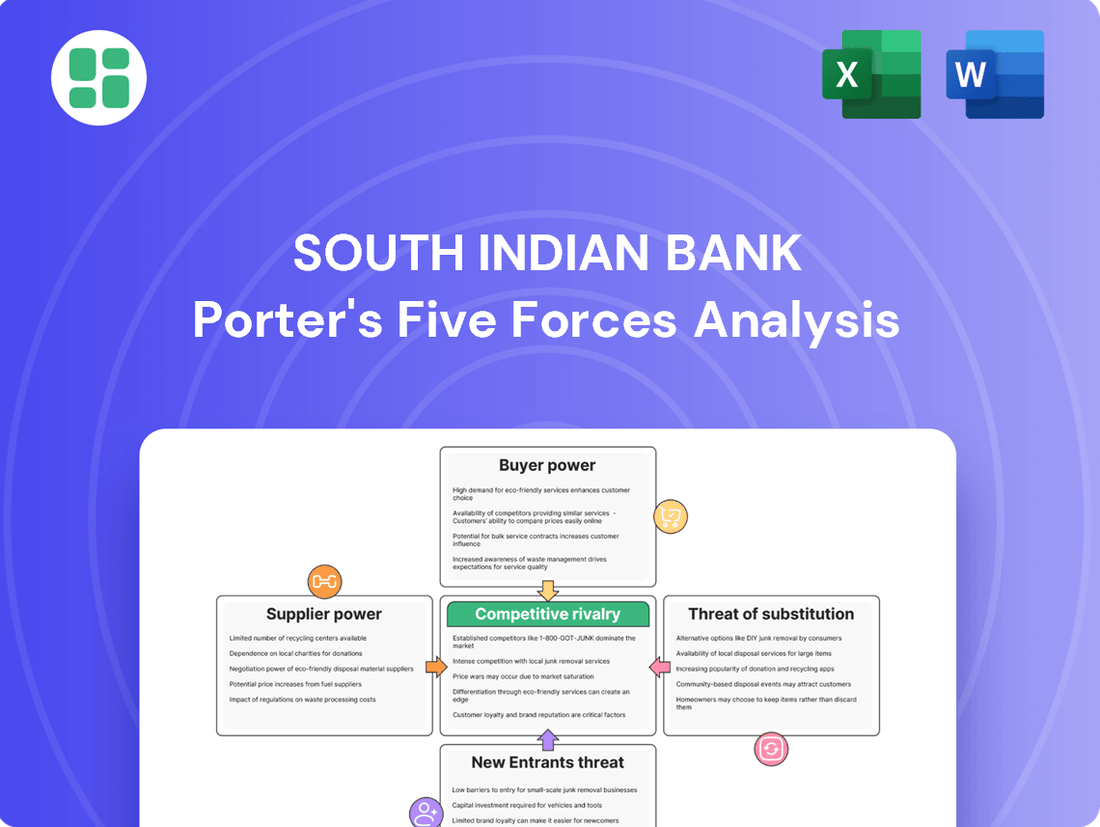

This analysis of South Indian Bank's competitive environment examines the intensity of rivalry, the bargaining power of customers and suppliers, the threat of new entrants, and the impact of substitute products and services.

Instantly understand competitive pressures on South Indian Bank with a clear, visual representation of each Porter's Five Forces factor.

Easily adapt the analysis to reflect changing market dynamics and new competitive threats impacting South Indian Bank.

Customers Bargaining Power

Retail Customers

Retail customers wield considerable bargaining power, largely due to the ease with which they can switch between banking providers. With numerous public, private, and small finance banks, alongside a growing number of fintech solutions, consumers have a wide array of choices. This competitive landscape means South Indian Bank must continuously innovate its offerings, from competitive interest rates to enhanced digital experiences and tailored financial products, to retain and attract this crucial customer base.

The digital age has significantly amplified the influence of retail customers. Increased financial literacy, coupled with readily available information on banking products and services, empowers individuals to make informed decisions. They can easily compare offerings and select institutions that best align with their financial goals and service expectations. For instance, in 2023, the Indian banking sector saw a significant surge in digital transactions, with UPI alone processing over 11 billion transactions, highlighting the customer's preference for and adoption of digital channels, a trend South Indian Bank must actively cater to.

Corporate Customers

South Indian Bank's corporate customers wield significant bargaining power, driven by their substantial transaction volumes and sophisticated financial requirements. These large entities, often dealing with multiple banking partners, can leverage this to negotiate favorable terms on loans, treasury services, and customized financial products. For instance, in 2023, the bank's corporate loan portfolio accounted for a significant portion of its business, highlighting the importance of retaining these clients through competitive offerings.

Institutional Customers

Institutional customers, like mutual funds and insurance companies, hold substantial bargaining power, particularly for large transactions or when demanding bespoke financial instruments. Their focus is on competitive pricing, service efficiency, and strong risk management. South Indian Bank must effectively meet these sophisticated demands.

Digital Natives and Tech-Savvy Users

Digital natives and tech-savvy users represent a growing segment with significant bargaining power. They expect intuitive mobile banking apps, instant transaction capabilities through platforms like UPI, and personalized financial solutions. This preference puts pressure on established institutions to enhance their digital offerings.

South Indian Bank, like many traditional banks, faces this challenge. Customers in this demographic are more likely to switch to fintech companies or neobanks that provide superior digital experiences and innovative products. For instance, the rapid adoption of UPI in India saw over 12 billion transactions in the first half of 2024, highlighting the demand for seamless digital payments.

- Digital-native customers demand seamless user experiences and instant services.

- Fintechs and neobanks often lead in offering innovative digital financial products.

- UPI transactions are a key indicator of this segment's preference for digital efficiency.

- The willingness to switch providers based on digital capabilities increases customer bargaining power.

Customers in Underserved and Rural Areas

While individual customers in underserved and rural areas might appear to have less bargaining power, their collective demand can be substantial, particularly with government initiatives promoting financial inclusion. For instance, India's Pradhan Mantri Jan Dhan Yojana has brought millions into the formal banking system, creating a significant customer base in these regions. South Indian Bank's strategic focus on expanding its agent banking network and offering services in local languages helps tap into this collective demand.

The ability to serve these markets effectively translates into a competitive advantage. However, this segment of customers typically expects highly affordable and easily accessible banking services. This expectation inherently caps the bank's ability to charge premium prices or extract high margins from these customers, thus moderating their bargaining power in terms of pricing flexibility.

- Collective Demand: Government financial inclusion programs like PMJDY have significantly expanded the customer base in rural and underserved areas.

- Accessibility Focus: Banks leveraging agent banking and vernacular interfaces gain an edge in reaching these customers.

- Affordability Expectation: Customers in these segments prioritize low-cost and accessible services, limiting margin potential for banks.

- Market Penetration: South Indian Bank's efforts to penetrate these markets are crucial for leveraging the collective demand.

Customer Power Shapes Bank Strategy in a Digital Era

The bargaining power of South Indian Bank's customers is significant, driven by the availability of numerous alternatives and increasing digital savviness. Retail customers can easily switch banks due to a competitive landscape featuring public, private, and fintech players. This necessitates continuous innovation in pricing and digital services to retain them. For example, the widespread adoption of UPI, with over 12 billion transactions in the first half of 2024, underscores customer preference for efficient digital channels, directly influencing bank strategies.

| Customer Segment | Bargaining Power Drivers | Impact on South Indian Bank |

|---|---|---|

| Retail Customers | High switching ease, digital literacy, numerous alternatives | Pressure on interest rates and service quality; need for enhanced digital offerings. |

| Corporate Clients | Large transaction volumes, sophisticated needs, multiple banking partners | Ability to negotiate favorable loan terms and service fees; retention is key. |

| Institutional Investors | Significant transaction sizes, demand for specialized financial instruments | Focus on competitive pricing, efficiency, and robust risk management. |

| Digital Natives | Expectation of seamless digital experience, instant services | Need to compete with fintechs on app functionality and payment speed. |

Full Version Awaits

South Indian Bank Porter's Five Forces Analysis

This preview shows the exact South Indian Bank Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. It delves into the bargaining power of buyers and suppliers, the threat of new entrants and substitutes, and the intensity of rivalry within the banking sector, providing a comprehensive strategic overview.

Rivalry Among Competitors

Presence of Diverse Banking Institutions

The Indian banking sector is a crowded field, featuring public sector banks, major private players, foreign banks, and smaller institutions. This diversity fuels intense competition, directly impacting South Indian Bank.

Giants like HDFC Bank and ICICI Bank are aggressively growing their market share and product portfolios, creating significant pressure on banks like South Indian Bank to innovate and maintain competitiveness.

Aggressive Digital Adoption and Innovation

The banking sector is experiencing heightened competition due to the rapid embrace of digital tools and ongoing innovation from major banks and fintech companies. These entities are channeling significant funds into artificial intelligence, machine learning, and open banking to deliver tailored customer experiences, optimize internal processes, and improve overall service delivery.

Leading players are focusing on AI-driven personalized banking, with many aiming to increase their digital customer base by over 20% in 2024. For instance, some banks reported a 30% surge in digital transactions in the last fiscal year, highlighting the shift in customer preference. South Indian Bank needs to match this pace of technological evolution to maintain its competitive edge in this dynamic digital environment.

Product and Service Homogenization

The banking sector, particularly for core products like savings accounts and fixed deposits, sees significant product and service homogenization. This means customers often perceive little difference between offerings from various banks, leading to intense competition primarily on price. For South Indian Bank, this translates to a constant need to offer competitive interest rates and fees to attract and retain customers.

This low differentiation compels South Indian Bank to emphasize efficient service delivery and cultivate robust customer relationships. For instance, in the fiscal year 2023-24, the bank reported a net profit of ₹1,113 crore, indicating operational efficiency. Building loyalty through personalized service and niche offerings becomes crucial to stand out in a crowded market.

Focus on Asset Quality and Credit Growth

The intense competition compels banks like South Indian Bank to prioritize superior asset quality and strong credit growth. This means a keen focus on expanding lending in profitable areas such as retail, corporate, and gold loans. South Indian Bank's approach is to build a resilient loan portfolio by acquiring high-quality assets, which is crucial for maintaining consistent profitability.

This strategic emphasis is particularly important given the ongoing challenges some banks face with non-performing assets (NPAs). For instance, in the fiscal year ending March 31, 2024, the Indian banking sector has seen a general improvement in asset quality, with gross NPAs for public sector banks declining. South Indian Bank's commitment to quality assets directly addresses this competitive pressure.

- Asset Quality Focus: South Indian Bank aims to maintain a high standard of asset quality across its loan book.

- Credit Growth Segments: Key growth areas include retail, corporate, and gold loans, reflecting market demand and profitability.

- Resilience Strategy: The bank's strategy centers on building a resilient loan book to ensure sustained profitability.

- NPA Management: A proactive approach to asset quality helps mitigate the risks associated with non-performing assets, a common challenge in the banking sector.

Regulatory Landscape and Consolidation

The regulatory environment, shaped by the Reserve Bank of India's (RBI) focus on financial stability and strengthening intermediaries, significantly impacts competitive dynamics within the Indian banking sector. These measures, while promoting a healthier financial ecosystem, also implicitly push for consolidation and greater operational efficiency.

Larger, more robustly capitalized banks are often better positioned to adapt to and benefit from evolving regulatory frameworks. This can translate into increased competitive pressure on smaller or regional banks, such as South Indian Bank, as the playing field shifts towards scale and compliance capabilities.

- Regulatory Measures: The RBI's ongoing efforts to enhance prudential norms and risk management practices are a key factor influencing competitive intensity.

- Consolidation Trend: Policies that encourage mergers and acquisitions can lead to fewer, larger players, potentially altering market share dynamics.

- Impact on South Indian Bank: As a regional bank, South Indian Bank must navigate these evolving regulations and competitive pressures by focusing on its niche strengths and operational efficiencies.

Regional Banks Navigate Intense Competition and Digital Transformation

The Indian banking landscape is fiercely competitive, with South Indian Bank facing pressure from public sector banks, large private players like HDFC and ICICI, and agile fintech firms. This intense rivalry is amplified by a strong push towards digital transformation, with many banks investing heavily in AI and machine learning to enhance customer experiences and streamline operations, aiming for significant digital customer base growth in 2024.

Product and service homogenization, especially for core offerings like savings and fixed deposits, forces banks to compete primarily on price, making competitive interest rates and fees crucial for customer acquisition and retention. South Indian Bank's net profit of ₹1,113 crore in FY 2023-24 underscores its operational efficiency, but building customer loyalty through personalized service remains vital.

The sector's focus on asset quality and credit growth, particularly in retail, corporate, and gold loans, is a key competitive battleground. South Indian Bank's commitment to acquiring high-quality assets, while the overall banking sector saw improved asset quality with declining NPAs for public sector banks by March 31, 2024, is essential for sustained profitability.

Regulatory oversight from the RBI, aimed at financial stability, can favor larger, well-capitalized banks, potentially increasing competitive pressure on regional players like South Indian Bank. Navigating these evolving regulations requires a strategic focus on niche strengths and operational efficiencies.

| Key Competitor | Market Share (Approx.) | Digital Push Focus | Recent Performance Indicator (FY24) |

|---|---|---|---|

| HDFC Bank | 15-20% | AI-driven personalization, expanding digital offerings | Strong profit growth, significant digital transaction increase |

| ICICI Bank | 12-17% | Open banking, digital lending platforms | Robust net interest margins, growing CASA deposits |

| Public Sector Banks (Aggregate) | 50-55% | Digitalizing services, improving customer onboarding | General improvement in asset quality, reduced NPAs |

| South Indian Bank | 1-2% | Enhancing digital channels, focus on retail and gold loans | Net profit of ₹1,113 crore, focus on asset quality |

SSubstitutes Threaten

Fintech Companies and Digital Wallets

Fintech companies and digital wallets pose a substantial threat of substitution for traditional banking services. These innovative players offer streamlined payment solutions, accessible lending options, and user-friendly investment platforms, often at a lower cost. For instance, the widespread adoption of Unified Payments Interface (UPI) in India has dramatically shifted consumer behavior, with UPI transactions in India reaching an astounding 13.42 billion in the first quarter of 2024, significantly reducing reliance on conventional bank transfers and challenging established players like South Indian Bank.

Non-Banking Financial Companies (NBFCs)

Non-Banking Financial Companies (NBFCs) present a significant threat of substitution for South Indian Bank, particularly in specialized lending segments. NBFCs often provide more agile and tailored financial solutions, such as quicker loan approvals and flexible repayment schedules, which can be highly attractive to borrowers, especially Micro, Small, and Medium Enterprises (MSMEs) and individual consumers seeking personal loans. For instance, the NBFC sector in India saw its assets under management grow by approximately 10% in the fiscal year 2023-24, reaching over INR 35 trillion, indicating their expanding reach and competitive pressure on traditional banks.

Peer-to-Peer (P2P) Lending Platforms

Peer-to-peer (P2P) lending platforms present a growing threat of substitutes for South Indian Bank. These platforms directly link borrowers with lenders, bypassing traditional financial institutions for specific loan needs. For instance, in 2023, the Indian P2P lending market saw significant activity, with platforms facilitating billions in loans, offering an alternative to bank credit for individuals and SMEs.

Capital Markets and Direct Investments

The threat of substitutes for South Indian Bank is significant, particularly for businesses and high-net-worth individuals. Capital markets offer alternatives to traditional bank financing, such as issuing corporate bonds or raising equity. For instance, in 2023, Indian companies raised over ₹1.5 lakh crore through public equity issuances, showcasing a robust alternative to bank loans.

Direct investments in financial instruments also pose a substitute threat. Customers can bypass bank-offered investment products by directly investing in mutual funds, stocks, or exchange-traded funds through various online brokerage platforms. The Indian mutual fund industry saw its assets under management (AUM) cross ₹50 lakh crore by May 2024, indicating strong customer adoption of direct investment channels.

To counter this, South Indian Bank must focus on differentiating its offerings. This includes providing superior financial advisory and personalized wealth management services. By offering expert guidance and tailored solutions, the bank can retain customers who might otherwise seek alternatives in the capital markets or through direct investment platforms.

- Capital Markets as a Substitute: Businesses can raise capital through bond issuances and equity financing, bypassing traditional bank loans. In 2023, Indian IPOs alone raised over ₹60,000 crore.

- Direct Investment Alternatives: Individuals and entities can invest directly in stocks, mutual funds, and ETFs via online brokerages, offering more control and potentially higher returns than bank-managed products.

- South Indian Bank's Strategy: To retain customers, the bank needs to enhance its comprehensive financial advisory and wealth management services, offering personalized guidance that substitutes can't easily replicate.

- Market Trends: The growth in direct investment avenues, with the Indian mutual fund industry's AUM reaching ₹50 lakh crore by May 2024, highlights the competitive landscape and the need for value-added banking services.

Emergence of Neobanks and Challenger Banks

The rise of neobanks and challenger banks presents a significant threat of substitution for traditional banks like South Indian Bank. These digital-first institutions, often operating without physical branches, can offer streamlined, tech-savvy customer experiences and potentially lower fees due to reduced overhead. For instance, in India, while the regulatory landscape for full-fledged neobanks is still developing, their ability to attract younger, digitally inclined customers with innovative products and services is a growing concern.

These new entrants are particularly adept at leveraging technology to offer competitive advantages. They often focus on specific customer segments or niche services, such as simplified account opening, personalized financial management tools, and faster transaction processing. This can draw customers away from traditional banking models that may be perceived as slower or less user-friendly. By mid-2024, the digital banking adoption rate in India continued its upward trajectory, with a significant portion of the population under 35 years old preferring online channels for their banking needs.

South Indian Bank must proactively address this threat by continuing to invest in and enhance its own digital banking capabilities. This includes improving its mobile banking app, expanding its online service offerings, and potentially exploring partnerships or developing its own digital-only banking solutions. The bank's ability to offer a seamless, intuitive digital experience comparable to or better than neobanks will be crucial in retaining and attracting customers in the evolving financial landscape.

- Neobanks offer digital-only banking with lower overheads, potentially leading to more competitive pricing.

- In India, neobanks are gaining traction among tech-savvy demographics, posing a substitution threat to traditional branch-based models.

- South Indian Bank needs to bolster its digital offerings to compete with the innovation and customer experience provided by challenger banks.

- The increasing preference for digital channels among younger Indian consumers underscores the urgency for traditional banks to adapt.

Financial Alternatives: Reshaping the Banking Sector

The threat of substitutes for South Indian Bank is multifaceted, encompassing fintech innovations, specialized NBFCs, P2P lending, capital markets, and direct investments. These alternatives often provide greater agility, lower costs, or more tailored solutions, drawing customers away from traditional banking services.

Fintech and digital wallets, powered by platforms like UPI, are fundamentally altering payment and lending behaviors. NBFCs are expanding their reach in specialized lending, while P2P platforms offer direct credit alternatives. Businesses increasingly turn to capital markets for funding, and individuals bypass bank investment products for direct market access.

| Substitute Category | Key Characteristics | Impact on South Indian Bank | Example Data (2024) |

|---|---|---|---|

| Fintech & Digital Wallets | Streamlined payments, accessible lending, lower costs | Reduced reliance on traditional transfers, competition in payments | UPI transactions in India reached 13.42 billion in Q1 2024 |

| NBFCs | Agile lending, flexible terms, specialized finance | Competition in MSME and personal loans | NBFC AUM grew ~10% in FY23-24, exceeding INR 35 trillion |

| P2P Lending | Direct borrower-lender connection, bypasses banks | Alternative credit source for individuals and SMEs | Significant activity in Indian P2P market in 2023 |

| Capital Markets | Bond issuance, equity financing | Alternative to bank financing for businesses | Indian companies raised over ₹1.5 lakh crore via public equity in 2023 |

| Direct Investments | Stocks, mutual funds, ETFs via online brokers | Customer shift from bank-managed products | Indian mutual fund AUM crossed ₹50 lakh crore by May 2024 |

Entrants Threaten

High Capital Requirements

The banking sector in India presents a formidable barrier to entry, primarily due to the substantial capital requirements stipulated by the Reserve Bank of India (RBI). Aspiring banks must demonstrate significant financial strength to obtain a license and build the essential operational infrastructure, a hurdle that naturally limits the number of new competitors.

For instance, in 2023, the RBI's guidelines for new bank licenses often necessitate a minimum net worth of ₹500 crore, with plans to increase this over time. This considerable financial commitment effectively deters many potential entrants, thereby safeguarding established players like South Indian Bank from immediate, intense competitive pressure.

Strict Regulatory Landscape

The Reserve Bank of India (RBI) maintains a stringent regulatory environment for new banking entrants, prioritizing stability, robust governance, and financial inclusion. This meticulous oversight, as evidenced by the RBI's cautious approach to new bank licenses, makes market entry a complex and lengthy undertaking. For instance, the application process involves rigorous scrutiny of capital adequacy, risk management frameworks, and promoter qualifications, effectively deterring less prepared entities.

Established Brand Reputation and Trust

South Indian Bank, like other established financial institutions, enjoys a significant advantage due to its long-standing brand reputation and the trust it has cultivated over many years. This deep-rooted credibility is a formidable barrier for any new entrant aiming to capture market share in the Indian banking sector.

New players would require substantial financial resources and considerable time to replicate the level of trust and recognition that South Indian Bank currently commands. For instance, as of March 31, 2024, South Indian Bank reported a customer base exceeding 10 million, a testament to its established presence and customer loyalty.

This ingrained brand loyalty, built through consistent service and reliability, makes it challenging for newcomers to attract and retain customers. Overcoming this established trust is a major hurdle, demanding extensive marketing efforts and a proven track record that takes years to develop.

Extensive Distribution Networks

The threat of new entrants for South Indian Bank is significantly mitigated by the extensive distribution networks already established by traditional banks. These networks, encompassing a wide array of branches and ATMs, offer unparalleled accessibility, particularly in less urbanized regions where digital penetration might be lower. For instance, as of March 31, 2024, South Indian Bank operated 930 branches and 1,300 ATMs, a physical footprint that new digital-first competitors would find incredibly costly and time-consuming to replicate.

While the digital banking landscape is evolving rapidly, the importance of a physical presence cannot be overstated for certain customer demographics and transaction types. Many customers, especially those in semi-urban and rural areas, still rely on in-person interactions for services like cash deposits, withdrawals, and personalized financial advice. The capital investment and operational complexity required to build and maintain a comparable physical infrastructure present a substantial barrier for any aspiring new entrant seeking to compete directly with established players like South Indian Bank.

- Vast Physical Footprint: Established banks boast extensive branch and ATM networks, providing broad customer reach.

- Customer Reliance on Physical Presence: Many customer segments still depend on physical touchpoints for transactions and services.

- High Barrier to Entry: Replicating such extensive networks requires immense capital and time investment for new players.

Economies of Scale and Scope

Incumbent banks, including South Indian Bank, benefit significantly from established economies of scale. This allows them to spread fixed costs across a larger volume of transactions, leading to lower per-unit operational expenses in areas like technology infrastructure and marketing. For instance, in 2023, South Indian Bank reported operating expenses of ₹5,977.63 crore, which are absorbed by its extensive customer base and transaction volumes.

New entrants face a substantial hurdle in matching these cost efficiencies. They would need to invest heavily in building a comparable operational and technological framework, making it challenging to achieve competitive pricing or offer a full spectrum of services without incurring significant initial losses. This inherent cost disadvantage acts as a strong deterrent.

- Economies of Scale: South Indian Bank leverages its large operational base to reduce per-unit costs in technology, marketing, and service delivery, a significant barrier for new entrants.

- Cost Disadvantage for Newcomers: Start-up banks would struggle to achieve similar cost efficiencies, requiring substantial upfront investment to compete on price or service breadth.

- Competitive Pricing Power: Established players like South Indian Bank can offer more attractive pricing due to their lower cost structure, making it difficult for new entrants to gain market share.

- Operational Efficiency: The sheer volume of business handled by incumbent banks allows for greater efficiency in processing and customer service, further solidifying their competitive position.

India's Banking Sector: A Fortress Against New Entrants

The threat of new entrants into the Indian banking sector, impacting South Indian Bank, is considerably low due to stringent regulatory capital requirements, with the RBI often mandating a minimum net worth of ₹500 crore for new licenses as of 2023. Furthermore, established players like South Indian Bank benefit from a deeply ingrained brand trust and extensive physical distribution networks, comprising 930 branches and 1,300 ATMs as of March 31, 2024, which are prohibitively expensive and time-consuming for newcomers to replicate.

| Factor | Impact on New Entrants | South Indian Bank's Position |

| Regulatory Capital Requirements | High Barrier (e.g., ₹500 crore minimum net worth in 2023) | Established compliance and financial strength |

| Brand Reputation & Customer Trust | Difficult to replicate; requires years of consistent service | Over 10 million customers as of March 31, 2024, indicating strong loyalty |

| Distribution Network | Costly and time-consuming to build comparable scale | Extensive network of 930 branches and 1,300 ATMs (as of March 31, 2024) |

| Economies of Scale | New entrants lack cost efficiencies; higher per-unit costs | Leverages large customer base to reduce operational expenses (e.g., ₹5,977.63 crore operating expenses in 2023) |

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis for South Indian Bank is built upon a robust foundation of data, including the bank's annual reports, investor presentations, and official filings with regulatory bodies like the Reserve Bank of India. We also incorporate insights from reputable financial news outlets, industry-specific research reports, and macroeconomic data to provide a comprehensive view of the competitive landscape.