Mowi Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Mowi Bundle

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

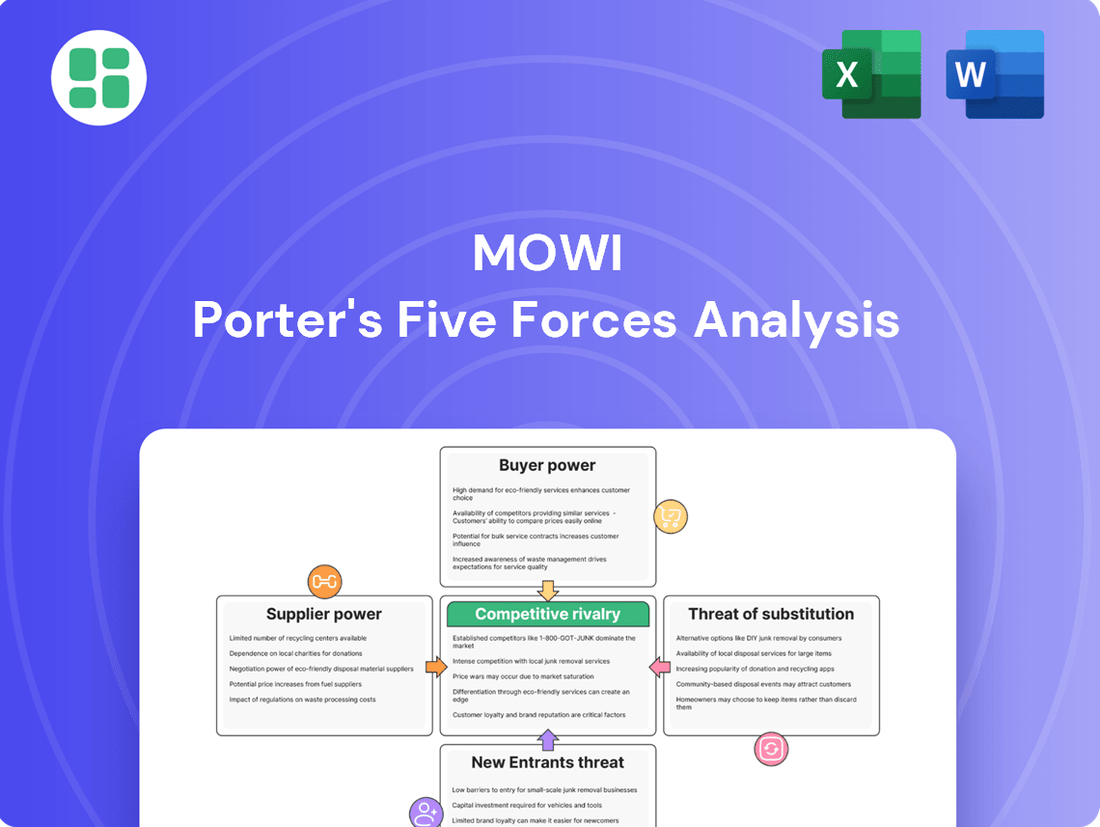

Mowi, a global leader in aquaculture, faces a dynamic competitive landscape shaped by five key forces. Understanding the intensity of buyer power, the threat of new entrants, the bargaining power of suppliers, the threat of substitutes, and the rivalry among existing competitors is crucial for strategic success.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Mowi’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated Feed Ingredient Suppliers

Mowi's reliance on concentrated feed ingredient suppliers, particularly for fishmeal and fish oil derived from wild-caught fish, grants these suppliers substantial bargaining power. The limited and often unpredictable availability of these essential resources means that suppliers can dictate terms, impacting Mowi's operational costs.

The volatile nature of wild fisheries directly influences the supply and price of key feed components. For instance, the cancellation of Peru's crucial anchovy fishing season in 2023 led to a dramatic 107% increase in fish oil prices, a significant cost shock for aquaculture operations like Mowi.

Integrated Feed Production Mitigates Power

Mowi's integrated feed production significantly dampens supplier bargaining power. By operating its own feed mills in Norway and Scotland, Mowi secures a substantial portion of its feed requirements internally. This vertical integration, a key strategic move, directly reduces Mowi's reliance on external feed suppliers, thereby strengthening its negotiating position.

This self-sufficiency in feed production allows Mowi to better control costs and ensure a consistent, stable supply of a critical input. For instance, in 2023, Mowi's feed division produced approximately 40% of the group's total feed volume, a testament to its integrated capabilities and a clear indicator of reduced dependence on outside sources.

Biological Input Suppliers (Smolt, Genetics)

Suppliers of high-quality smolt and advanced genetics wield considerable influence. This is because these biological inputs are foundational to Mowi's fish health, growth, and ultimately, its production efficiency. The specialized knowledge and proprietary nature of these offerings mean few can provide them, giving these suppliers leverage.

Mowi's strategic investments in developing its own genetics and expanding post-smolt utilization are direct responses to mitigate this supplier power. By internalizing more of the value chain related to these critical biological inputs, Mowi aims to gain greater control over quality, supply, and cost, thereby reducing its reliance on external suppliers.

Labor Market Dynamics

The availability of skilled labor in aquaculture and processing significantly impacts supplier power. In regions with a scarcity of specialized aquaculture expertise or tight labor markets, Mowi may face increased wage pressure from its workforce, effectively strengthening the bargaining power of labor as a supplier. This is particularly relevant as Mowi continues to focus on operational efficiency.

Mowi's strategic initiatives to optimize labor costs are evident. For instance, the company has reported on its ongoing productivity programs, which have included efforts to reduce Full-Time Equivalent (FTE) employees. In 2023, Mowi highlighted a reduction in FTEs as part of its cost-saving measures, demonstrating a proactive approach to managing labor expenses and mitigating the bargaining power of its labor suppliers.

- Skilled Labor Scarcity: Regions with a limited pool of experienced aquaculture technicians and processing plant workers can give labor a stronger negotiating position.

- Wage Pressures: Tight labor markets often translate to higher wage demands from employees, increasing Mowi's labor costs.

- Productivity Programs: Mowi's focus on efficiency, including FTE reductions, aims to offset potential increases in labor costs and maintain competitive pricing.

- 2023 FTE Reduction: Mowi's reported efforts to reduce FTEs in 2023 underscore its strategy to manage labor as a cost factor.

Energy and Equipment Suppliers

Mowi's reliance on energy and equipment suppliers presents a moderate bargaining power dynamic. While many inputs are commoditized, specialized aquaculture technology or significant regional energy price volatility can shift leverage towards suppliers. For instance, disruptions in global energy markets, as seen with fluctuating oil prices impacting shipping and processing costs, can increase supplier influence.

The bargaining power of energy and equipment suppliers for Mowi is influenced by several factors:

- Energy Price Volatility: Fluctuations in global energy prices, such as those impacting diesel for fishing vessels or electricity for processing plants, can give energy providers more leverage, especially during periods of high demand or supply chain disruptions.

- Specialized Equipment Dependence: Mowi's need for advanced, proprietary aquaculture equipment, like specialized feeding systems or advanced harvesting technology, can grant significant power to the few suppliers offering these critical components.

- Supplier Concentration: In specific equipment categories, a limited number of manufacturers may dominate the market, increasing their ability to dictate terms and prices to Mowi.

- Geographic Energy Markets: Regional differences in energy production and pricing mean that suppliers in certain Mowi operating regions might possess greater bargaining power due to local market conditions or resource availability.

Navigating Supplier Influence in Integrated Production

Mowi's bargaining power with suppliers is moderately influenced by its integrated feed production, which reduces reliance on external fishmeal and fish oil providers. However, the volatile nature of wild fisheries, as seen with the 2023 Peruvian anchovy season cancellation causing a 107% fish oil price surge, highlights the persistent leverage of key ingredient suppliers.

The company's internal smolt and genetics development also mitigates supplier power in these critical biological inputs, though specialized suppliers still hold influence due to the proprietary nature of their offerings. Mowi's strategic focus on these areas aims to enhance control over quality and supply chains.

Labor availability and skill levels in key operating regions directly impact the bargaining power of employees. Mowi actively manages this through productivity programs, including reported FTE reductions in 2023, to control labor costs and maintain competitiveness.

Energy and specialized equipment suppliers exert moderate influence, particularly during periods of energy price volatility or when Mowi requires proprietary aquaculture technology. Market concentration in certain equipment sectors can further empower these suppliers.

| Supplier Category | Key Factors Influencing Bargaining Power | Mowi's Mitigation Strategies | Impact on Mowi |

|---|---|---|---|

| Feed Ingredients (Fishmeal/Oil) | Wild fishery volatility, supplier concentration | Integrated feed production (40% of group volume in 2023), diversification | Moderate to High; Cost fluctuations impact margins |

| Smolt & Genetics | Proprietary technology, limited specialized providers | Internal R&D, expanded post-smolt utilization | Moderate; Ensures quality and supply stability |

| Labor | Skilled labor scarcity, regional market tightness | Productivity programs, FTE optimization (e.g., 2023 reductions) | Moderate; Wage pressures affect operational costs |

| Energy & Equipment | Energy price volatility, specialized equipment dependence | Long-term contracts, supplier diversification, technology adoption | Moderate; Affects operational and capital expenditures |

What is included in the product

This analysis dissects the competitive landscape for Mowi by examining the bargaining power of buyers and suppliers, the threat of new entrants and substitutes, and the intensity of rivalry within the salmon industry.

Instantly identify and quantify competitive threats with Mowi's Porter's Five Forces analysis, providing clarity on market pressures.

Customers Bargaining Power

Large Retailers and Food Service Channels

Mowi's customers, particularly large retailers and food service chains, wield considerable bargaining power. Their substantial order volumes allow them to negotiate favorable pricing, directly impacting Mowi's profit margins. For instance, major supermarket chains often demand price reductions to maintain their own competitive edge, forcing suppliers like Mowi to optimize costs.

Brand Strength and Product Differentiation

Mowi's strong MOWI brand and its wide array of products, from fresh and frozen salmon to smoked and ready-to-eat meals, significantly enhance its product differentiation. This variety allows Mowi to cater to diverse customer needs and preferences, reducing the likelihood of customers switching to competitors based solely on price.

By focusing on product innovation and maintaining a recognizable brand, Mowi can lessen customer price sensitivity. This is particularly true for its value-added products, where the brand name and perceived quality justify a premium, thereby strengthening Mowi's position against powerful buyers.

Global Demand for Salmon

Global consumer appetite for healthy, sustainable, and premium seafood, especially Atlantic salmon, is a significant tailwind for Mowi. This rising demand directly influences the bargaining power of customers; as demand grows, customers become more reliant on producers, thus reducing their leverage.

Projections for 2025 indicate that global salmon demand is set to outstrip supply. This imbalance is a powerful factor, likely leading to more favorable market prices for established producers like Mowi, further diminishing the ability of individual customers to negotiate lower prices.

Customer Diversification Across Markets

Mowi's extensive global distribution network, reaching numerous markets worldwide, significantly dilutes the bargaining power of individual customers. By operating across diverse geographical regions and serving a broad customer base, Mowi reduces its dependence on any single market or buyer. This strategic diversification of sales channels inherently balances customer power, as no single entity can exert undue influence over Mowi's pricing or terms.

This global presence is crucial for mitigating customer concentration risk. For instance, in 2023, Mowi reported that its sales were spread across Europe, North America, and Asia, with no single region accounting for more than 40% of its total revenue. This wide distribution means that even a large customer in one region has limited leverage over the company as a whole.

- Global Reach: Mowi's operations span multiple continents, including Europe, North America, and Asia.

- Diversified Customer Base: Sales are distributed across a wide array of customers, preventing over-reliance on any one buyer.

- Reduced Dependence: No single market or customer segment represents a disproportionately large share of Mowi's revenue.

- Balanced Bargaining Power: This diversification acts as a natural counterweight to the potential power of individual or group customers.

Sustainability and Traceability Demands

Customers, particularly in well-developed economies, are showing a heightened interest in sustainability and product traceability. Mowi's robust sustainability credentials and its transparent approach to the entire value chain position it favorably against competitors. This growing emphasis on Environmental, Social, and Governance (ESG) factors can foster stronger customer loyalty and a greater willingness to pay a premium for Mowi's responsibly sourced products.

For instance, Mowi achieved a score of 86 out of 100 in the 2024 Seafood Stewardship Index, highlighting its commitment to sustainable practices. This focus translates into tangible benefits, as studies in 2024 indicated that over 60% of consumers are willing to pay more for seafood with verifiable sustainability claims. Mowi's ability to meet these evolving consumer demands directly influences their bargaining power by creating a differentiated product offering.

- Growing Consumer Demand: An increasing number of consumers prioritize sustainability and traceability in their purchasing decisions.

- Mowi's Competitive Edge: Mowi's strong sustainability rankings and transparent value chain offer a distinct advantage.

- ESG Impact: A focus on ESG factors can enhance customer loyalty and support premium pricing strategies.

- Market Trends: Data from 2024 shows a significant willingness among consumers to pay more for sustainably sourced seafood.

Customer Power: Strategic Mitigation

Mowi's customers, particularly large retailers and food service chains, hold significant bargaining power due to their substantial order volumes, enabling them to negotiate favorable pricing and impacting Mowi's profit margins.

However, Mowi's strong brand differentiation and diverse product portfolio, coupled with growing global demand for sustainable salmon, mitigate this power.

By focusing on product innovation and verifiable sustainability claims, Mowi can command premium pricing, reducing customer price sensitivity and their leverage.

Mowi's global distribution network further dilutes customer concentration risk, as no single market or buyer represents an overwhelmingly large portion of revenue, balancing overall customer influence.

| Factor | Mowi's Position | Impact on Customer Bargaining Power |

|---|---|---|

| Customer Concentration | Low due to global reach and diversified sales channels. | Reduces individual customer leverage. |

| Product Differentiation | High through brand and product variety. | Decreases customer reliance on price alone. |

| Sustainability Focus | Strong, evidenced by a 2024 Seafood Stewardship Index score of 86/100. | Increases willingness to pay premium, lessening price negotiation power. |

| Market Demand | Projected to outstrip supply by 2025. | Shifts power towards producers like Mowi. |

Full Version Awaits

Mowi Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. It provides a comprehensive breakdown of Mowi's competitive landscape through Porter's Five Forces, detailing the intensity of rivalry, the power of buyers and suppliers, the threat of new entrants, and the bargaining power of substitutes. This analysis is crucial for understanding Mowi's strategic positioning and potential challenges within the global aquaculture industry.

Rivalry Among Competitors

Fragmented Global Salmon Market

Mowi, as the leading Atlantic salmon producer with a significant 20% global market share in 2024, still operates within a highly fragmented market. This means intense competition from other substantial players such as SalMar, AquaChile, Leroy Seafood Group, and Cermaq Group.

This fragmentation fuels aggressive rivalry, often manifesting as price wars. Companies constantly strive to gain or maintain market position, which can put pressure on profit margins across the industry.

Volume-Driven Growth Strategy

Mowi's pursuit of volume-driven growth, targeting 530,000 GWT by 2025 and 650,000 GWT by 2029, directly fuels competitive rivalry. This aggressive expansion strategy, coupled with ongoing cost reduction initiatives, forces competitors to similarly focus on efficiency and market share gains to remain viable. This creates an environment where price competition and operational excellence become paramount for all players in the salmon farming industry.

Biological Challenges and Regulatory Landscape

Competitive rivalry within the aquaculture industry is significantly shaped by regional biological challenges like sea lice and disease outbreaks, which can severely impact production yields and costs. For instance, in 2023, Norway, a major salmon farming nation, reported that sea lice treatments cost the industry an estimated NOK 2.5 billion (approximately $235 million USD). Companies that invest in advanced biological management and disease prevention technologies, such as advanced feeding systems and improved containment, often outperform competitors by minimizing losses and maintaining consistent supply.

The evolving regulatory landscape also intensifies rivalry, particularly in key farming regions like Norway and Canada. Stricter environmental regulations regarding waste discharge, fish welfare, and the use of chemicals can increase operational expenses and limit expansion opportunities. For example, new regulations in British Columbia, Canada, introduced in 2022, aim to phase out open-net pen salmon farming by 2025, forcing companies to adapt their business models or face significant disruption. Those that proactively adapt to or influence these regulatory changes, perhaps through innovation in land-based or closed-containment systems, gain a distinct advantage.

Product Differentiation and Value-Added Products

Competitors in the aquaculture industry actively differentiate themselves through superior product quality, robust branding, and the development of value-added processed goods. This strategy moves beyond competing solely on the price of raw commodities, aiming to capture greater consumer loyalty and command premium pricing.

Mowi's strategic emphasis on its MOWI brand and its consumer products segment highlights this differentiation approach. In 2024, Mowi reported record-high volumes and earnings in this segment, underscoring the success of its strategy to build brand equity and offer a wider range of convenient, higher-margin products to end consumers.

- Product Quality: Competitors focus on sourcing, farming practices, and feed to ensure higher quality fish.

- Branding: Strong brand recognition, like Mowi's, builds trust and allows for premium pricing.

- Value-Added Processing: Offering ready-to-cook meals, fillets, and other processed items increases consumer convenience and company margins.

- Mowi's Performance: Mowi's 2024 results in consumer products demonstrate the effectiveness of this value-added strategy.

Consolidation and Acquisitions

The aquaculture industry is experiencing significant consolidation, with major players acquiring smaller competitors to gain scale and market share. Mowi's own strategic move to increase its ownership in Nova Sea to 95% in 2025 exemplifies this trend. This consolidation leads to fewer, larger entities dominating the market.

These acquisitions fundamentally alter the competitive dynamics by increasing market concentration. For instance, the ongoing mergers and acquisitions activity in the salmon farming sector means that the top companies are controlling a larger portion of the global supply. This can lead to reduced price competition as fewer independent players remain.

- Industry Consolidation: Mowi's increased stake in Nova Sea to 95% in 2025 highlights a broader trend of consolidation.

- Market Concentration: Acquisitions lead to fewer, larger companies controlling a greater share of the market.

- Reshaped Landscape: Consolidation can reduce the number of independent competitors, intensifying rivalry among the remaining large entities.

Salmon Farming's Fierce Rivalry: Strategies, Challenges, and Consolidation

The competitive rivalry in the salmon farming sector is fierce, driven by a fragmented market and aggressive expansion strategies from major players like Mowi. This intense competition often results in price wars, pressuring profit margins across the industry. Companies are compelled to focus on operational efficiency and market share to remain competitive, especially as Mowi targets significant volume growth, aiming for 650,000 GWT by 2029.

Biological challenges and evolving regulations further intensify this rivalry. For example, sea lice treatments in Norway alone cost the industry approximately $235 million USD in 2023. Companies investing in advanced biological management, like Mowi's focus on improved containment and feeding systems, gain a competitive edge. Similarly, adapting to stricter environmental rules, such as Canada's planned phase-out of open-net pens by 2025, creates opportunities for innovators in alternative farming methods.

Differentiation through product quality, branding, and value-added processing is a key strategy to combat price-based competition. Mowi's success in its consumer products segment in 2024, with record volumes and earnings, demonstrates the effectiveness of building brand equity. This approach shifts the focus from raw commodity pricing to consumer loyalty and premium offerings.

Industry consolidation is also reshaping the competitive landscape. Mowi's move to increase its ownership in Nova Sea to 95% in 2025 exemplifies this trend, leading to fewer, larger entities dominating the market. This consolidation can reduce the number of independent competitors, intensifying rivalry among the remaining large players.

| Competitor | Estimated 2024 Market Share (%) | Key Strategy |

|---|---|---|

| Mowi | 20 | Volume growth, brand building, value-added products |

| SalMar | ~10-12 | Operational efficiency, vertical integration |

| AquaChile | ~8-10 | Geographic diversification, sustainability focus |

| Leroy Seafood Group | ~7-9 | Product innovation, strong distribution network |

| Cermaq Group | ~6-8 | Technological advancement, cost leadership |

SSubstitutes Threaten

Other Seafood Products

The threat of other seafood products as substitutes for salmon is significant. Consumers can easily switch to farmed or wild-caught alternatives like shrimp, cod, and tuna, especially if there are price differences or availability issues with salmon. For instance, global shrimp production reached approximately 5.4 million metric tons in 2022, highlighting a readily available alternative.

Alternative Protein Sources

Non-seafood proteins such as chicken, pork, and beef represent a substantial threat of substitution for Mowi. When economic conditions tighten or salmon prices climb, consumers often pivot to these more budget-friendly and readily accessible options. For instance, in 2023, the average retail price for boneless, skinless chicken breast in the US hovered around $4.00 per pound, significantly less than the retail price of many salmon cuts, making it an attractive alternative for many households.

Plant-Based and Lab-Grown Alternatives

Emerging alternative proteins, such as plant-based seafood and cultivated (lab-grown) fish, pose a growing long-term threat to traditional aquaculture. While these alternatives are currently in niche markets, ongoing technological advancements are improving their taste, texture, and production scalability. By 2024, the global plant-based seafood market was estimated to be worth over $2 billion, with projections indicating significant growth as consumer acceptance and product innovation continue.

Wild-Caught Salmon Supply Fluctuations

While Mowi's primary focus is farmed salmon, the threat of substitutes, particularly wild-caught salmon, warrants consideration. Fluctuations in wild salmon catches, such as those experienced by the Alaska sockeye fishery, can influence overall salmon supply dynamics and subtly shift consumer preferences. For instance, in 2023, the Alaska sockeye salmon run saw a significant decrease, impacting availability for certain markets.

However, the volume of wild-caught salmon, while important for niche markets and consumer perception, remains considerably lower than the global farmed salmon output. This disparity means that even substantial swings in wild salmon availability are unlikely to fundamentally disrupt the broader farmed salmon market or Mowi's production capacity. The market share of wild salmon is a fraction of the total salmon consumed globally.

- Wild-caught salmon represents a small percentage of the total global salmon market.

- Fluctuations in specific wild fisheries, like the Alaska sockeye, have limited impact on overall salmon supply.

- Farmed salmon production volumes far exceed wild-caught volumes, mitigating the threat of substitution.

Consumer Health and Environmental Concerns

Consumer health and environmental concerns represent a significant threat of substitutes for Mowi's products. As consumers become more aware of the environmental footprint of aquaculture and seek specific nutritional benefits, they may turn to alternative protein sources. For instance, a growing segment of consumers is exploring plant-based diets or choosing wild-caught fish perceived as more sustainable or healthier. In 2023, the global plant-based food market was valued at over $30 billion and is projected to grow substantially, indicating a strong consumer shift towards alternatives.

Mowi actively mitigates this threat by emphasizing its robust sustainability initiatives and certifications. The company holds numerous certifications, including ASC (Aquaculture Stewardship Council) and GlobalG.A.P., which assure consumers of responsible farming practices. These efforts aim to build trust and differentiate Mowi from less transparent or less sustainable competitors. For example, Mowi's commitment to reducing its carbon footprint is a key part of its strategy to appeal to environmentally conscious consumers.

- Consumer preference shift: Growing demand for plant-based alternatives and wild-caught seafood due to health and environmental perceptions.

- Market growth of substitutes: The global plant-based food market exceeded $30 billion in 2023, highlighting the increasing appeal of alternatives.

- Mowi's mitigation strategy: Emphasis on sustainability certifications like ASC and GlobalG.A.P. to build consumer trust and differentiate products.

- Focus on transparency: Mowi's efforts to reduce its carbon footprint and promote responsible aquaculture practices address consumer concerns directly.

Protein Substitutes: Understanding Market Dynamics

The threat of substitutes for Mowi is shaped by various protein sources, both from the sea and land. While other seafood options like shrimp and cod are readily available, with global shrimp production around 5.4 million metric tons in 2022, the more significant substitution threat comes from non-seafood proteins. Chicken, in particular, remains a strong competitor. For instance, in 2023, US retail prices for boneless, skinless chicken breast averaged about $4.00 per pound, making it a considerably more economical choice than salmon for many consumers.

Emerging alternatives, such as plant-based seafood and cultivated fish, are also gaining traction. The global plant-based seafood market was valued at over $2 billion in 2024, signaling growing consumer interest and technological advancements in this area. Mowi counters these threats by highlighting its sustainability practices, backed by certifications like ASC and GlobalG.A.P., to appeal to health- and environmentally-conscious consumers.

| Substitute Category | Example | 2023/2024 Data Point | Impact on Mowi |

|---|---|---|---|

| Other Seafood | Shrimp | Global production ~5.4 million metric tons (2022) | Readily available, price-sensitive competition. |

| Non-Seafood Protein | Chicken | US retail price ~$4.00/lb (2023) | Significant price advantage, especially during economic downturns. |

| Alternative Proteins | Plant-based Seafood | Global market value >$2 billion (2024) | Growing niche market driven by innovation and consumer trends. |

Entrants Threaten

High Capital Intensity

The salmon farming industry, especially for large, integrated players like Mowi, demands significant initial investment. This includes setting up hatcheries, marine farms, processing facilities, and feed production. For instance, establishing a new, large-scale salmon farming operation can easily run into hundreds of millions of dollars.

This substantial capital requirement acts as a formidable barrier, deterring many potential new entrants who may lack the necessary financial resources or access to significant funding. It makes it incredibly difficult for smaller companies or new ventures to compete with established giants.

Strict Regulatory Environment and Licensing

The aquaculture industry, particularly in major producing nations like Norway and Canada, operates under a stringent regulatory framework. This includes rigorous licensing procedures, comprehensive environmental standards, and limitations on biomass, effectively raising the barrier to entry for newcomers. For instance, new regulations introduced in 2024 concerning land-based farming applications further increase the complexity and financial investment required for potential market participants.

Biological and Environmental Risks

New entrants into the aquaculture sector, particularly salmon farming like Mowi, confront substantial biological risks. These include the ever-present threat of disease outbreaks, such as piscine orthoreovirus (PRV), and the persistent challenge of sea lice infestations, which can significantly impact fish health and growth rates. For example, in 2023, the Norwegian salmon farming industry reported substantial losses due to disease, impacting production volumes and increasing operational costs.

Furthermore, the intensifying effects of climate change present a growing barrier. Rising water temperatures can stress salmon, making them more susceptible to pathogens and altering the prevalence of harmful algal blooms. These environmental shifts demand sophisticated monitoring and adaptive management strategies, requiring considerable upfront investment and ongoing scientific expertise that can deter potential new entrants.

Established Integrated Value Chains

Mowi's established integrated value chains present a significant barrier to new entrants. This end-to-end control, encompassing everything from feed production to processing and global distribution, allows for substantial economies of scale and cost efficiencies. For instance, Mowi's feed division, Ewos, is a major player, providing a cost advantage and quality control that new, less integrated companies would struggle to match. This deep integration creates a formidable hurdle for any aspiring competitor aiming to enter the salmon farming market.

The complexity and capital investment required to replicate Mowi's integrated model are immense. New entrants would need to invest heavily in feed mills, hatcheries, farming operations, processing plants, and a global logistics network. This creates a high barrier to entry, protecting Mowi's market position.

Key aspects of Mowi's integrated value chain as a barrier include:

- Economies of Scale: Mowi's large-scale operations across the entire value chain drive down per-unit costs, making it difficult for smaller, new entrants to compete on price.

- Cost Control: Internalizing key functions like feed production (e.g., Ewos) provides better cost management and predictability compared to relying on external suppliers. In 2023, Mowi reported total revenue of EUR 5.2 billion, reflecting the scale of its operations.

- Operational Efficiency: Seamless integration allows for optimized logistics, reduced waste, and improved quality control from farm to fork, enhancing overall efficiency.

- Market Access: Mowi's established global distribution network and brand recognition provide immediate access to key markets, a significant advantage over newcomers.

Brand Recognition and Distribution Networks

Mowi’s significant investment in building its MOWI brand and establishing a vast global distribution network presents a formidable barrier to new entrants. This extensive reach, cultivated over years, makes it incredibly difficult for newcomers to achieve comparable market penetration and customer loyalty. For instance, Mowi’s 2023 annual report highlighted its presence in over 100 countries, a testament to its established distribution infrastructure.

New companies would face substantial hurdles in replicating Mowi's market access and the ingrained brand recognition that fosters customer preference. The sheer cost and time required to build a comparable global supply chain and marketing presence are prohibitive. Consider that in 2024, the global seafood market continues to be dominated by a few large, integrated players like Mowi, further solidifying their competitive advantage.

- Brand Recognition: Mowi’s MOWI brand enjoys widespread recognition, built through consistent marketing and product quality, making it a trusted name for consumers worldwide.

- Distribution Networks: Mowi operates an extensive and efficient global distribution system, ensuring product availability and timely delivery across diverse markets.

- Cost and Time Investment: Establishing a similar level of brand awareness and distribution reach would require immense capital outlay and a significant time commitment, deterring most potential new entrants.

- Market Access: Existing players like Mowi have secured strong relationships with retailers and food service providers, granting them preferential market access that is hard for newcomers to obtain.

Entry Barriers Fortify Salmon Farming Giants

The threat of new entrants into the salmon farming industry, particularly for established players like Mowi, is significantly mitigated by several high barriers. These include the immense capital required to establish operations, stringent regulatory environments, and the inherent biological and climate-related risks involved. For instance, Mowi's 2023 revenue of EUR 5.2 billion underscores the scale of investment needed to compete. Furthermore, the complexity of replicating Mowi's integrated value chain, from feed production to global distribution, presents a substantial hurdle.

| Barrier Type | Description | Impact on New Entrants | Example Data (Mowi) |

|---|---|---|---|

| Capital Requirements | High upfront investment for facilities, technology, and licenses. | Deters smaller firms and new ventures due to financial risk. | Establishment costs can reach hundreds of millions of dollars. |

| Regulatory Environment | Strict licensing, environmental standards, and biomass limits. | Increases complexity, cost, and time to market. | New land-based farming regulations in 2024 add further complexity. |

| Integrated Value Chain | Control over feed, farming, processing, and distribution. | Creates economies of scale, cost efficiencies, and quality control. | Mowi's feed division, Ewos, provides a significant cost advantage. |

| Brand and Distribution | Established global brand recognition and extensive distribution networks. | Difficult for newcomers to achieve comparable market penetration and customer loyalty. | Mowi operates in over 100 countries, a testament to its network. |

Porter's Five Forces Analysis Data Sources

Our Mowi Porter's Five Forces analysis leverages a comprehensive dataset including Mowi's annual reports, industry-specific market research from firms like SeafoodSource and IntraFish, and broader economic indicators from sources such as the World Bank.