Halkbank Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Halkbank Bundle

A Must-Have Tool for Decision-Makers

Halkbank faces significant competitive pressures, particularly from the threat of new entrants and the bargaining power of buyers in the Turkish banking sector. Understanding these forces is crucial for navigating the market effectively.

The complete report reveals the real forces shaping Halkbank’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Concentration of Key Technology Providers

The banking sector's dependence on a limited number of providers for essential technologies like core banking systems, cybersecurity solutions, and digital platforms significantly amplifies supplier bargaining power. For Halkbank, this concentration means that if a few key technology vendors dominate the market, they can dictate terms, as switching to an alternative system is often prohibitively expensive and complex, involving substantial migration costs and potential operational disruptions.

Availability of Funding Sources

Halkbank's ability to provide loans and investment products hinges on its access to various funding sources like deposits, interbank markets, and international finance. The power of these capital suppliers is shaped by global interest rates, market liquidity, and Halkbank's own credit standing, which directly affects its borrowing costs.

For instance, in 2023, Halkbank's total deposits stood at approximately TRY 1.16 trillion, forming a crucial base of its funding. However, reliance on interbank markets or international bonds means being exposed to the prevailing global financial conditions and investor sentiment, which can fluctuate significantly.

As a state-owned entity, Halkbank benefits from government backing, which can provide a stable and potentially lower-cost funding avenue compared to purely market-driven sources. This government support can buffer against volatility in private capital markets, influencing the bank's overall cost of capital.

Skilled Labor Market Dynamics

The availability of highly skilled professionals in areas like IT, finance, risk management, and digital banking is crucial for Halkbank's operations. A tight labor market, where specialized talent is scarce, significantly empowers employees and recruitment agencies.

This scarcity translates into higher wage demands and increased operational costs for Halkbank. For instance, in 2024, the demand for cybersecurity experts in the Turkish banking sector outpaced supply, leading to average salary increases of up to 15% for these roles, directly impacting recruitment budgets.

Regulatory and Compliance Bodies

Regulatory and compliance bodies, like the Central Bank of the Republic of Turkey (CBRT) and the Banking Regulation and Supervision Agency (BDDK), wield significant influence over Halkbank, akin to powerful suppliers. These entities set the operational rules, capital requirements, and compliance standards that Halkbank must adhere to. Failure to comply can result in severe penalties, meaning Halkbank has little room to negotiate these 'inputs'.

Halkbank’s compliance with these mandates requires substantial investment in technology, processes, and personnel. For instance, Turkish banks are required to maintain a minimum capital adequacy ratio of 12% under Basel III guidelines, a non-negotiable operational cost dictated by regulators. This effectively grants these bodies considerable power over the bank’s strategic and financial planning.

- Regulatory Mandates: CBRT and BDDK set capital requirements and operational standards.

- Compliance Costs: Significant investment is needed to meet these regulatory dictates.

- Non-Negotiable Inputs: Halkbank must adhere to rules like the 12% minimum capital adequacy ratio.

- Supplier Power: Regulators act as powerful suppliers, dictating crucial operational parameters.

Payment Network Providers

Payment network providers hold considerable bargaining power over Halkbank. These networks, often functioning as oligopolies, dictate terms and fees for essential transaction services, directly influencing Halkbank's operational costs and its ability to offer competitive services. For instance, SWIFT's dominance in international messaging means banks have limited alternatives, granting SWIFT significant leverage.

The increasing demand for digital payment solutions in Turkey further strengthens the position of these providers. The rapid adoption of systems like FAST, which saw a substantial increase in transaction volume in 2023, highlights the growing reliance on these networks. This trend means banks like Halkbank must often accept the terms set by network operators to remain competitive and serve their customers effectively.

- Network Dominance: Global and national payment networks often operate with limited competition, allowing them to set terms and fees that banks must adhere to.

- Fee Structures: Providers can influence transaction costs for Halkbank through their pricing models for services like cross-border payments and domestic transfers.

- Service Access: Access to these networks is crucial for Halkbank's operations, giving providers leverage in negotiations over service availability and quality.

- Growing Digital Demand: The increasing use of electronic payment systems, such as Turkey's FAST, enhances the bargaining power of the underlying network providers.

Suppliers' Grip on Halkbank: Costs and Control

Suppliers of critical technology and specialized talent exert significant influence over Halkbank. The concentration in core banking systems and the scarcity of IT and finance professionals allow these suppliers to command higher prices and dictate terms, directly impacting Halkbank's operational costs and recruitment strategies. For instance, in 2024, the demand for cybersecurity experts in Turkey's banking sector led to salary increases of up to 15% for these roles.

Regulatory bodies like the CBRT and BDDK act as powerful suppliers, setting non-negotiable operational parameters such as capital adequacy ratios. Halkbank must invest heavily to comply with these mandates, limiting its flexibility. Similarly, payment network providers, often operating as oligopolies, dictate fees for essential transaction services, with Turkey's FAST system experiencing substantial transaction volume growth in 2023, reinforcing provider leverage.

| Supplier Type | Halkbank's Dependence | Supplier Bargaining Power Factors | Impact on Halkbank | 2024 Data/Trend |

|---|---|---|---|---|

| Technology Vendors | Core banking, cybersecurity, digital platforms | Market concentration, high switching costs | Dictated terms, increased IT costs | High demand for cybersecurity experts |

| Skilled Labor | IT, finance, risk management, digital banking | Scarcity of specialized talent | Higher wage demands, increased recruitment costs | Up to 15% salary increase for cybersecurity roles |

| Regulators (CBRT, BDDK) | Operational rules, capital requirements | Mandatory compliance, penalties for non-compliance | Limited negotiation, significant compliance investment | 12% minimum capital adequacy ratio (Basel III) |

| Payment Networks | Transaction processing, cross-border payments | Oligopolistic nature, essential service access | Fee structures, service terms influence costs | Increased transaction volume in FAST system (2023) |

What is included in the product

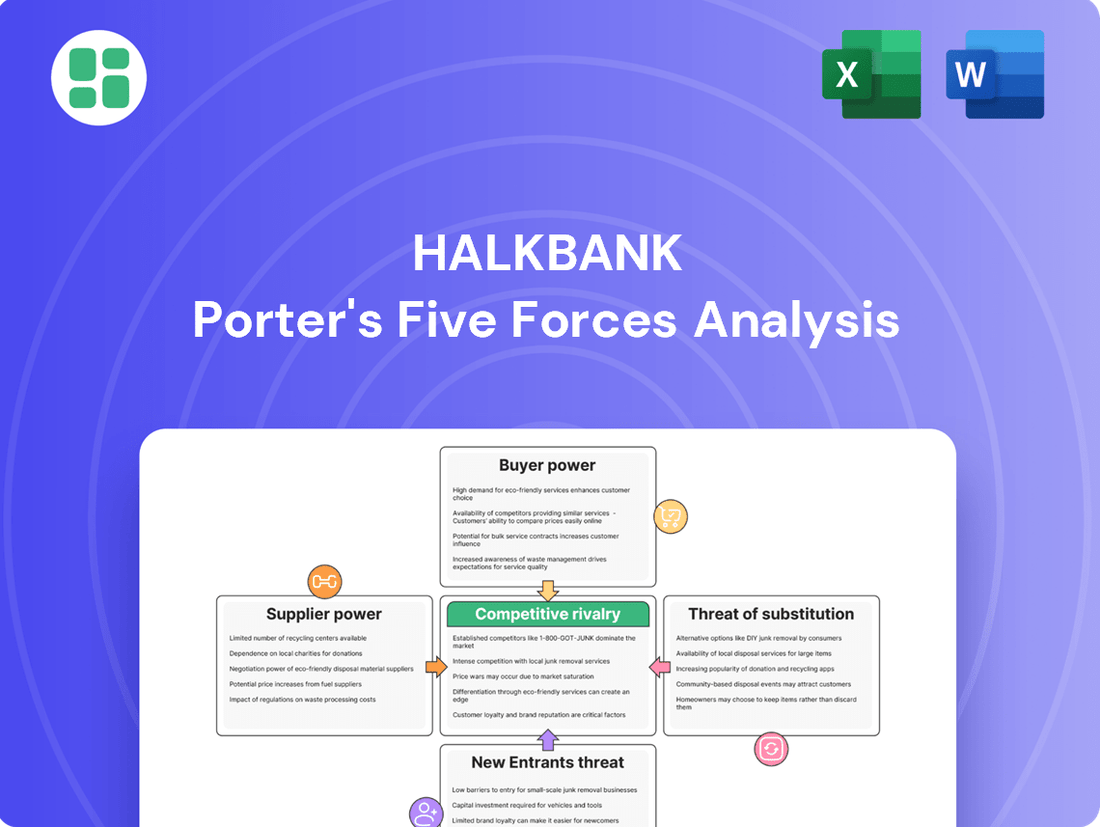

This analysis unpacks the competitive forces impacting Halkbank, examining the threat of new entrants, the bargaining power of buyers and suppliers, the intensity of rivalry, and the threat of substitutes.

Effortlessly identify and mitigate competitive threats by visualizing Halkbank's market position against key industry players.

Customers Bargaining Power

High Availability of Alternatives

The Turkish banking landscape offers a wealth of options, significantly boosting customer bargaining power. With 63 banks operating as of March 2024, including 33 deposit banks, customers can readily compare offerings. This means Halkbank faces intense competition not only from other state-owned entities like Ziraat Bank and VakıfBank but also from a broad spectrum of private and international banks.

Customers have the freedom to switch to institutions providing superior interest rates, enhanced service quality, or more user-friendly digital banking experiences. This ease of switching directly empowers them to negotiate better terms or seek alternatives, putting pressure on Halkbank to remain competitive and customer-centric.

Low Switching Costs for Retail Customers

Retail customers in Türkiye face minimal costs when switching banks for everyday services like savings accounts or personal loans. This low barrier to entry is amplified by the country's robust digital banking infrastructure, with over 90 million active online banking users as of 2024, making account transfers and new setups remarkably simple.

The sheer volume of digitally engaged customers means Halkbank must consistently offer competitive rates and superior service to retain its retail base. If other institutions present more attractive deals or a smoother digital experience, customers can readily shift their business, directly impacting Halkbank's market share and profitability in the retail segment.

Information Transparency and Access

Customers today have unprecedented access to information, making it easier than ever to compare Halkbank's interest rates, fees, and product features against those of its competitors. This heightened transparency erodes the informational advantage banks historically held, empowering customers to negotiate for better terms. For instance, by mid-2024, a significant portion of banking customers in Turkey actively utilized online comparison tools, demonstrating a clear trend towards informed decision-making.

Concentration of Large Corporate Clients

The concentration of large corporate clients significantly influences Halkbank's bargaining power of customers. While individual retail customers have minimal leverage due to low switching costs, major corporate and Small and Medium-sized Enterprise (SME) clients often possess greater negotiating power. This is because their banking requirements are typically more intricate, fostering deeper, long-term relationships that can involve multiple banking partners.

If a few substantial clients account for a significant percentage of Halkbank's overall business, their individual bargaining power is amplified. This allows them to negotiate more favorable interest rates, fees, and bespoke banking solutions. Halkbank's strategic focus includes providing crucial financial support to SMEs, a sector often characterized by the presence of these larger, more influential players.

- Client Concentration: A few large corporate clients can disproportionately impact revenue, giving them significant leverage.

- Negotiating Power: These clients can demand better terms due to the potential loss of substantial business.

- Customized Services: Their complex needs often require tailored solutions, further strengthening their position.

- SME Mandate: Halkbank's commitment to SMEs means engaging with businesses that can grow into these large client categories.

State-Owned Bank Mandate and Customer Perception

As a state-owned entity, Halkbank's mandate often includes supporting public policy and economic stabilization in Turkey, which can influence its pricing strategies and service offerings. This can mean that certain customer segments might not see the same level of aggressive price competition as they would with purely private banks. However, customers still retain significant power by seeking better terms or alternative providers, especially for standard banking products.

Customers might expect a degree of social benefit or stability from a state-backed institution like Halkbank. While this can foster loyalty, it doesn't negate their ability to shop around for the best commercial deals, especially in a competitive market. For instance, while Halkbank plays a crucial role in supporting SMEs and public sector initiatives, individual customers can still leverage competitive offerings from other financial institutions.

- State Mandate: Halkbank's role in supporting Turkish economic policy can lead to a perception of less aggressive pricing in certain areas.

- Customer Expectations: While customers may value stability from a state bank, they still actively seek favorable commercial terms.

- Competitive Landscape: The Turkish banking sector is competitive, giving customers options to compare rates and services across various institutions.

Customer Power Shapes Turkey's Banking Landscape

The bargaining power of customers in Turkey's banking sector is substantial, driven by a highly competitive market with 63 banks as of March 2024. This abundance of choice, from state-owned giants to international players, empowers customers to easily switch for better rates or services. The low cost of switching for retail customers, coupled with a robust digital banking infrastructure serving over 90 million online users in 2024, further amplifies their leverage. Consequently, Halkbank must remain competitive on pricing and service quality to retain its customer base.

| Factor | Impact on Halkbank | Supporting Data (2024) |

|---|---|---|

| Market Competition | High customer bargaining power | 63 banks operating in Turkey |

| Switching Costs (Retail) | Low, increasing customer power | Minimal costs for basic banking services |

| Digital Adoption | Facilitates easy switching | >90 million online banking users |

| Information Availability | Empowers informed decisions | Widespread use of online comparison tools |

What You See Is What You Get

Halkbank Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. The comprehensive Halkbank Porter's Five Forces Analysis details the competitive landscape, including the bargaining power of buyers and suppliers, the threat of new entrants and substitutes, and the intensity of rivalry within the banking sector.

Rivalry Among Competitors

Large Number of Competitors in Turkey

The Turkish banking sector is highly competitive, with a significant number of domestic and international players vying for market share. This crowded environment includes large state-owned banks like Ziraat Bank and VakıfBank, prominent private institutions such as İşbank and Garanti BBVA, and a variety of smaller, specialized banks.

This intense rivalry means Halkbank faces constant pressure across all its service areas, from individual customer accounts to large corporate financing. As of the close of 2024, the Turkish banking landscape comprised 61 distinct state, private, and foreign-owned financial institutions, underscoring the breadth of competition.

Product and Service Homogenization

Many standard banking products, like checking accounts, personal loans, and basic payment services, are very similar across different financial institutions. This lack of unique features means Halkbank often has to compete mainly on price, offering lower interest rates or fees to attract customers.

This intense price competition directly impacts profitability. For instance, the banking sector's net interest margins (NIMs) have faced downward pressure. In 2024, global NIMs continued to reflect this trend, with many banks reporting narrower spreads between what they earn on loans and what they pay on deposits, making it harder to generate substantial profits from core lending activities.

High Exit Barriers

The banking sector, including Halkbank, faces intense rivalry due to substantial exit barriers. These include massive investments in physical branches and IT systems, significant employee numbers, and strict regulatory requirements that make leaving the market difficult and costly. As of the end of 2024, the Turkish banking sector alone employed over 208,000 individuals across more than 10,950 branches.

These high exit barriers mean that even banks experiencing financial difficulties are unlikely to cease operations. This persistence ensures that competition remains fierce for Halkbank, as weaker players continue to vie for market share, particularly during challenging economic periods, thereby sustaining a high level of competitive rivalry.

Aggressive Digital Transformation and Innovation

Turkish banks are locked in an aggressive digital transformation, pouring resources into mobile banking, fintech solutions, and online platforms. This intense focus on digital innovation is a direct response to customer demand and the need to stay competitive. Halkbank, like its peers, must constantly upgrade its digital offerings to attract and retain customers in this rapidly evolving landscape.

The drive for digital supremacy creates a dynamic and fiercely competitive environment. Competitors are not just traditional banks but also emerging fintech players, all vying for market share through superior digital experiences and innovative financial products. This necessitates continuous investment and a proactive approach to technological advancement for Halkbank.

The significance of this digital shift is underscored by its economic impact. In 2023, mobile and internet banking transactions represented a substantial portion of Turkey's Gross National Product (GNP), highlighting how central digital finance has become to the national economy. This trend is expected to continue growing, making digital capabilities a critical determinant of success for banks like Halkbank.

- Digital Investment: Turkish banks are prioritizing digital channels and innovative financial technologies.

- Customer Acquisition: Digital transformation efforts are crucial for attracting and retaining customers.

- Competitive Pressure: Halkbank faces intense rivalry from agile competitors in the digital space.

- Economic Impact: Mobile and internet banking transactions significantly contribute to Turkey's GNP.

Impact of Economic Conditions and Regulatory Environment

The Turkish economy's inherent volatility and a continuously shifting regulatory framework are major drivers of competitive rivalry for Halkbank. During times of elevated inflation or economic instability, banks often intensify their efforts to attract deposits and secure lending to reliable customers, thereby heightening competition. Furthermore, the introduction of new regulations can fundamentally reshape the competitive landscape, influencing Halkbank's strategic standing against its peers.

The Turkish banking sector is poised for growth, with projections indicating positive impacts from anticipated economic improvements. Analysts are forecasting a cautious easing of monetary policy by the Central Bank of the Republic of Turkey (CBRT) throughout 2025. This economic climate is expected to foster a more favorable environment for competition, potentially benefiting institutions like Halkbank.

- Economic Volatility: High inflation and economic uncertainty in Turkey intensify competition for deposits and creditworthy borrowers.

- Regulatory Evolution: New regulations can significantly alter the competitive dynamics and strategic positioning of banks like Halkbank.

- Growth Projections: The Turkish banking sector anticipates benefits from general economic improvements and a cautious easing cycle by the CBRT in 2025.

Turkish Banking: Fierce Rivalry & Digital Shift

Halkbank operates within a highly competitive Turkish banking sector, characterized by a substantial number of domestic and international institutions. This intense rivalry is further fueled by the commoditization of many banking products, forcing competition to pivot towards price and digital innovation. The sector's significant exit barriers, including substantial infrastructure investments and large workforces, ensure that even struggling banks remain active participants, perpetuating fierce competition.

| Metric | Halkbank & Peers (2024 Data) | Industry Trend |

|---|---|---|

| Number of Banks in Turkey | 61 | High, indicating intense rivalry |

| Banking Sector Employment (Turkey) | > 208,000 | High, contributing to exit barriers |

| Digital Transaction Share (Turkey) | Significant portion of GNP | Increasing, driving digital competition |

| Net Interest Margins (Global) | Facing downward pressure | Intensifies price competition |

SSubstitutes Threaten

Emergence of Fintech and Digital Payment Platforms

The rise of fintech and digital payment platforms presents a substantial threat of substitutes for Halkbank. These companies, offering services like digital wallets and online payments, provide convenient and often faster alternatives to traditional banking. As of January 31, 2024, Turkey boasted 691 active fintech companies, with the payments sector leading the charge, indicating a growing competitive landscape that can disintermediate Halkbank from customer transactions.

Direct Capital Market Access

Large corporations are increasingly bypassing traditional bank loans by accessing capital directly through bond markets, equity offerings, or private placements. This trend, evident globally and within Turkey, directly substitutes Halkbank's traditional lending services, particularly for significant financing needs. For example, in 2024, Turkish corporate bond issuance saw a notable increase, indicating a growing preference for direct market access over bank financing for many large entities.

Alternative Lending and Crowdfunding Platforms

Alternative lending and crowdfunding platforms represent a significant threat to traditional banks like Halkbank. These platforms, especially those catering to small and medium-sized enterprises (SMEs) and individuals, offer accessible funding options that bypass conventional banking channels. For instance, the fintech sector in Turkey, including its financing components, has experienced substantial growth, indicating a rising preference for these alternative methods.

Non-Bank Financial Institutions and Insurance Companies

Non-bank financial institutions and insurance companies are increasingly encroaching on traditional banking services, offering alternatives for investment products, wealth management, and lending. This trend presents a significant threat of substitution for Halkbank, as these entities can fulfill specific customer needs, forcing the bank to continually innovate and strengthen its value proposition to remain competitive. For instance, the global fintech market was valued at approximately $2.4 trillion in 2023 and is projected to grow substantially, indicating the growing influence of these substitute providers.

These competitors, including fintech firms, offer a diverse array of services that directly substitute for Halkbank's offerings. Fintechs, in particular, are rapidly expanding into areas like asset management and insurance, providing customers with convenient, often digital-first alternatives. By 2024, it's estimated that over 70% of consumers will use at least one fintech service, highlighting the widespread adoption and competitive pressure these substitutes exert.

- Growing Fintech Adoption: Over 70% of consumers are expected to use fintech services by 2024, directly competing with traditional banking offerings.

- Diversification of Financial Services: Non-bank institutions and insurers now provide investment, wealth management, and lending, acting as direct substitutes.

- Market Value of Fintech: The global fintech market reached an estimated $2.4 trillion in 2023, underscoring the scale of this competitive landscape.

Internal Corporate Treasury Management

Large corporations are increasingly developing robust internal treasury departments. These in-house teams can manage cash, investments, and even provide internal financing, effectively substituting many traditional banking services. For example, by 2024, many multinational corporations are expected to have dedicated treasury units capable of optimizing liquidity and managing foreign exchange exposures internally, reducing their need for external cash management solutions.

This trend directly impacts banks like Halkbank, as it diminishes the demand for their corporate banking offerings. When clients can efficiently handle their own cash pooling, intercompany lending, and short-term investment needs, the bank's revenue streams from these services are naturally reduced. This necessitates banks to innovate and offer more sophisticated, value-added services to retain these clients.

- In-house Cash Management: Corporations can manage pooled cash, reducing reliance on bank-provided sweeping services.

- Internal Financing: Sophisticated treasuries can facilitate intercompany loans, bypassing bank credit facilities for short-term needs.

- Investment Management: Large corporate treasuries may manage their own short-term investment portfolios, opting out of bank-managed funds.

- Reduced Demand: This internal capability directly substitutes services previously offered by banks, impacting revenue.

Fintech & Corporate Finance: The Growing Threat of Substitutes to Banking

The threat of substitutes for Halkbank is significant, primarily driven by the burgeoning fintech sector and evolving corporate finance strategies. Fintech companies offer digital wallets, online payments, and alternative lending, directly competing with traditional banking services. Furthermore, large corporations are increasingly accessing capital markets directly and developing in-house treasury functions, reducing their reliance on banks for financing and cash management.

| Substitute Area | Example | Impact on Halkbank | 2024 Data/Trend |

|---|---|---|---|

| Digital Payments & Wallets | Fintech payment platforms | Disintermediation of transactions | Over 70% consumer fintech adoption expected by 2024 |

| Corporate Financing | Bond markets, equity offerings | Reduced demand for corporate loans | Increased Turkish corporate bond issuance in 2024 |

| Alternative Lending | Crowdfunding platforms | Competition for SME and individual financing | Substantial growth in Turkey's fintech financing sector |

| Cash Management | In-house corporate treasury functions | Lower revenue from corporate cash pooling and investment services | Multinational corporations strengthening internal treasury units by 2024 |

Entrants Threaten

High Regulatory Barriers to Entry

The banking sector, particularly in Turkey, faces substantial regulatory hurdles that significantly deter new entrants. Obtaining the necessary licenses, meeting stringent capital adequacy requirements like the 12% minimum mandated by Basel III principles integrated into Turkish regulations, and complying with extensive anti-money laundering and consumer protection laws demand considerable resources and expertise. These high barriers effectively dampen the threat of new traditional banks challenging established players like Halkbank.

Substantial Capital Requirements

Establishing a new bank, like Halkbank, demands enormous capital. This includes significant investments in physical branches, advanced technology systems, and crucially, meeting stringent regulatory capital requirements. For instance, in 2023, the Banking Regulation and Supervision Agency (BDDK) in Turkey maintained robust capital adequacy ratios for banks, generally exceeding international Basel III norms, which translates into substantial upfront capital needs for any new player.

These substantial financial barriers effectively deter many potential new entrants. Only a select few organizations possess the sheer volume of resources required to launch and compete effectively against well-established institutions like Halkbank, which already benefit from economies of scale and deep market penetration.

Brand Loyalty and Customer Trust

Existing banks, particularly state-backed institutions like Halkbank, possess a significant advantage due to their long-standing brand recognition and deeply ingrained customer trust. Newcomers must invest heavily and strategically to cultivate similar levels of credibility, a challenging hurdle to overcome when trying to attract a substantial customer base rapidly.

Halkbank, with its 86-year history, has cemented a strong and reliable presence within the Turkish economic landscape. This longevity translates into a powerful incumbent advantage, making it difficult for new entrants to quickly erode Halkbank's established customer loyalty and market position.

Economies of Scale and Distribution Networks

Established banks like Halkbank enjoy significant advantages due to their sheer size. This means they can spread costs across a larger volume of business, making their operations, technology investments, and marketing efforts more efficient and cost-effective. For instance, Halkbank's extensive network, boasting over 1,000 branches, represents a substantial barrier to entry for any new player aiming to achieve comparable physical reach and customer accessibility.

Furthermore, the established distribution networks, encompassing both physical branches and robust digital platforms, are difficult and expensive for newcomers to replicate. These networks have been built and refined over many years, fostering deep customer relationships and brand loyalty. A new entrant would face immense challenges in building a comparable infrastructure and customer base, requiring substantial capital outlay and considerable time to even approach Halkbank's established market presence.

- Economies of Scale: Halkbank leverages its size to reduce per-unit costs in operations, technology, and marketing.

- Distribution Network: Over 1,000 branches and established digital infrastructure create significant reach.

- Capital Requirements: New entrants need massive investment to match Halkbank's scale and network.

Emergence of Digital-Only Banks and Niche Fintechs

The threat of new entrants for Halkbank is evolving, with digital-only banks and niche fintechs posing a significant challenge. While establishing a full-service traditional bank remains capital-intensive and heavily regulated, these new players operate with leaner structures and advanced technology. They can effectively target specific, profitable market segments, such as payments or consumer loans, thereby eroding Halkbank's market share in those areas. The growth in this sector is notable; by the close of 2024, Turkey had 89 licensed payment and electronic money institutions, indicating a fertile ground for new, digitally-focused financial services.

- Digital-only banks (neobanks) offer lower overheads and agile technology.

- Niche fintechs focus on specific segments like payments or consumer lending.

- These entrants can bypass traditional barriers to entry.

- Turkey's regulatory landscape saw 89 licensed payment and electronic money institutions by the end of 2024.

Turkey's Banking Sector: New Entrants and Digital Disruption

The threat of new entrants for Halkbank remains moderate, primarily due to substantial regulatory and capital barriers in the Turkish banking sector. However, the rise of digital-only banks and specialized fintech companies presents a growing challenge, as these entities can operate with lower overheads and target specific market segments effectively. By the end of 2024, Turkey's financial landscape featured 89 licensed payment and electronic money institutions, highlighting the dynamic nature of this competitive environment.

| Factor | Impact on Halkbank | Notes |

| Regulatory Hurdles | High | Stringent licensing, capital adequacy (e.g., Basel III integration), and compliance requirements deter traditional new banks. |

| Capital Requirements | High | Significant upfront investment needed for branches, technology, and regulatory capital, estimated in the hundreds of millions of USD for a full-service bank. |

| Brand Recognition & Trust | High Advantage | Halkbank's 86-year history fosters customer loyalty, requiring substantial marketing and time for newcomers to build equivalent credibility. |

| Economies of Scale & Network | High Advantage | Halkbank's over 1,000 branches and established digital platforms offer cost efficiencies and market reach difficult for new entrants to match. |

| Digital-Only Banks & Fintechs | Emerging Threat | Lower overheads, agile technology, and focused strategies allow them to capture specific market segments, impacting Halkbank's market share in areas like payments and consumer loans. |

Porter's Five Forces Analysis Data Sources

Our Halkbank Porter's Five Forces analysis is built upon a foundation of verified data, including Halkbank's official annual reports, regulatory filings from the Turkish Banking Regulation and Supervision Agency (BDDK), and reputable industry publications that track the Turkish banking sector. We also incorporate macroeconomic data from sources like the Central Bank of the Republic of Turkey and international financial institutions to contextualize the competitive landscape.