Gentrack Group Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Gentrack Group Bundle

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Gentrack Group operates within a dynamic software and services sector, where the threat of new entrants can be significant due to lower initial capital requirements. Understanding the bargaining power of buyers and suppliers is crucial for their pricing strategies and operational efficiency. The intensity of rivalry among existing players, including established competitors and emerging disruptors, directly impacts market share and profitability.

The full analysis reveals the strength and intensity of each market force affecting Gentrack Group, complete with visuals and summaries for fast, clear interpretation.

Suppliers Bargaining Power

Concentration of Key Technology Providers

The software industry, especially for large-scale enterprise solutions, leans heavily on a few dominant cloud service providers such as AWS, Microsoft Azure, and Google Cloud. These companies together hold a massive portion of the market, giving them considerable leverage. Any rise in the cost of their fundamental infrastructure services directly affects Gentrack's operating expenses.

Gentrack's reliance on AWS and Salesforce for its g2.0 solution highlights its dependence on these crucial technology suppliers. For instance, in 2023, AWS reported revenue of $90.77 billion, underscoring its significant market presence and pricing influence.

Availability of Specialized Talent

Gentrack's need for specialized talent in areas like cloud-native development and data analytics directly impacts supplier power. The scarcity of professionals skilled in complex utility and airport software, including adherence to industry regulations, means these individuals and firms can command higher rates. This is a significant factor given Gentrack's workforce, which includes approximately 690 utility professionals and over 90 in its Veovo airport division.

Switching Costs for Core Components

Gentrack's reliance on key partners like Salesforce and AWS for its core platform components presents a significant challenge regarding supplier bargaining power. The substantial investments in time, resources, and the inherent risk of operational disruption associated with migrating from one major cloud provider or critical software vendor to another create high switching costs. This integration lock-in diminishes Gentrack's leverage in negotiations, potentially leading to less favorable pricing or contract terms from these entrenched suppliers.

Proprietary Technologies and Intellectual Property

Suppliers who possess unique technologies or intellectual property vital for Gentrack's software offerings, like specialized algorithms or crucial database components, wield significant bargaining power. This is particularly true if Gentrack's innovation, such as its g2.0 platform leveraging low-code and composable architecture, relies heavily on these proprietary elements, thereby amplifying the influence of their intellectual property holders.

For instance, in 2024, the global software market saw continued demand for specialized intellectual property, with acquisitions of companies holding unique technology often commanding significant premiums, reflecting the value placed on such proprietary assets by software providers like Gentrack.

- Proprietary Algorithms: Suppliers with unique, patented algorithms for data processing or customer management in the utilities sector can command higher prices.

- Niche Integrations: Companies providing essential integrations with legacy systems or specialized third-party services that Gentrack requires have increased leverage.

- Data Security Innovations: Suppliers offering advanced, proprietary data security solutions critical for Gentrack's cloud-based platforms can exert greater influence.

Hardware Sourcing for Non-Recurring Revenue

Gentrack Group's non-recurring revenue stream, which includes hardware sales, generated $6.8 million in fiscal year 2024. The bargaining power of the suppliers providing this hardware is a key consideration for Gentrack.

This supplier power directly impacts Gentrack's profitability on hardware-centric projects. Factors such as the availability of alternative suppliers and the demand for specific hardware components can significantly sway the negotiation leverage.

- Hardware Sourcing Impact: Gentrack's $6.8 million in FY24 non-recurring revenue from hardware highlights supplier influence.

- Margin Pressure: High supplier bargaining power can compress margins on these hardware sales.

- Supply Chain Vulnerability: Limited supplier options or high demand for specific components increase supplier leverage.

Supplier Dominance: Impacting Operational Costs and Leverage

Gentrack's reliance on a concentrated group of cloud service providers like AWS and Salesforce, which reported substantial revenues in 2023 ($90.77 billion for AWS), grants these suppliers significant pricing leverage. This dependence, coupled with high switching costs and integration lock-in, limits Gentrack's negotiation power, potentially impacting operating expenses and contract terms.

The scarcity of specialized talent in utility and airport software development, where Gentrack employs around 690 utility professionals and over 90 in its Veovo airport division, empowers skilled individuals and firms. Suppliers possessing unique technologies or intellectual property crucial for Gentrack's platforms, like its g2.0 solution, can also command higher prices, as evidenced by the premiums paid for unique technology in the 2024 global software market.

Gentrack's non-recurring hardware revenue of $6.8 million in fiscal year 2024 underscores the bargaining power of hardware suppliers. Limited sourcing options or high demand for specific components can compress margins on these sales and create supply chain vulnerabilities.

| Factor | Impact on Gentrack | Supporting Data/Context |

|---|---|---|

| Cloud Provider Dominance | Increased operating costs, limited negotiation leverage | AWS 2023 Revenue: $90.77 billion |

| Specialized Talent Scarcity | Higher labor costs, supplier pricing power | Gentrack workforce: ~690 utility, >90 Veovo professionals |

| Proprietary Technology Reliance | Amplified supplier influence, potential for higher licensing fees | 2024 global software market premiums for unique IP |

| Hardware Sourcing | Margin pressure on non-recurring revenue | Gentrack FY24 non-recurring revenue: $6.8 million |

What is included in the product

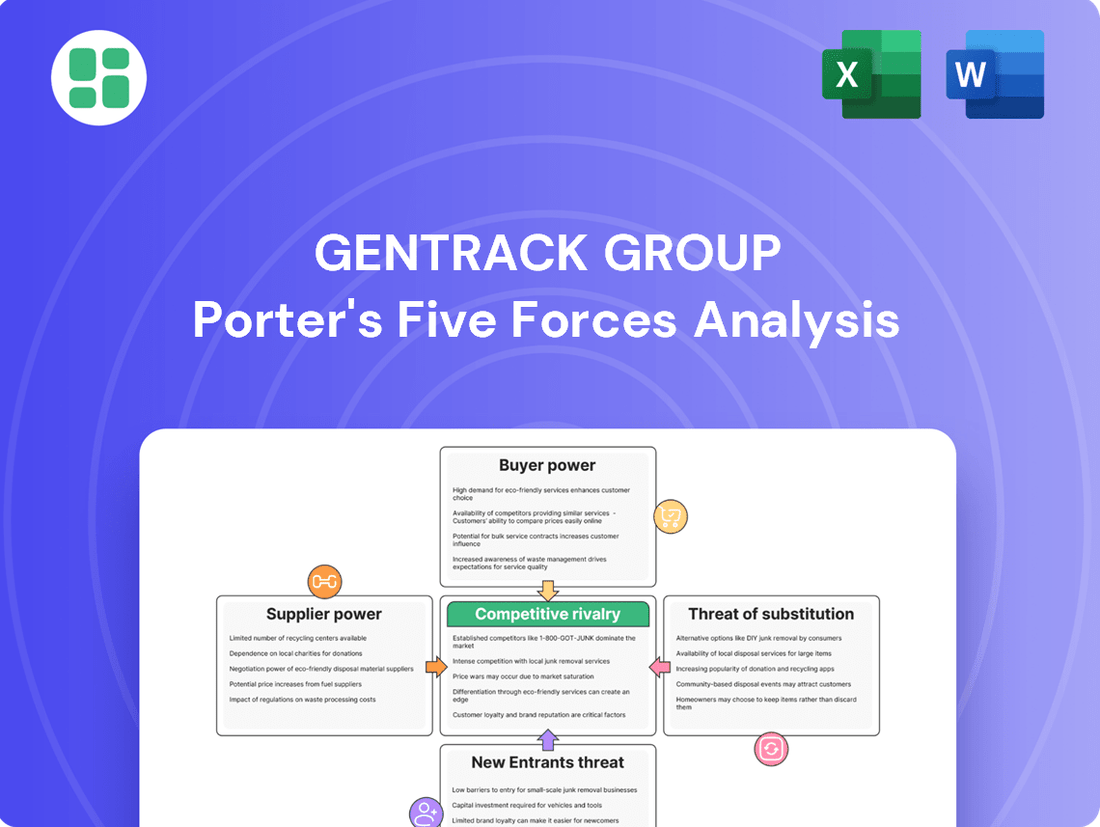

This analysis meticulously examines the competitive forces impacting Gentrack Group, including the threat of new entrants, the bargaining power of buyers and suppliers, the threat of substitutes, and the intensity of rivalry within the utility billing and CRM software market.

Gentrack Group's Porter's Five Forces analysis provides a clear, one-sheet summary of all five forces—perfect for quick decision-making by alleviating the pain of information overload.

Customers Bargaining Power

High Switching Costs for Customers

Gentrack's customer base, largely composed of utilities and airports, experiences exceptionally high costs when considering a change in their core operational software. These systems, often involving intricate billing, customer information, and operational management, represent a significant investment.

The process of migrating such complex software is not a simple undertaking; it demands substantial financial outlay, presents considerable data migration hurdles, and carries the risk of operational disruption. These factors collectively diminish a customer's ability to switch providers once Gentrack's solutions are deeply embedded within their infrastructure, thereby reducing their bargaining power.

Criticality of Software to Operations

Gentrack's software is absolutely vital for utilities and airports, handling everything from billing to managing customer information and daily operations. This means that when these businesses choose a software provider, they're looking for rock-solid reliability and excellent support. Because these systems are so critical, customers tend to be less focused on just the price and more on ensuring their operations run smoothly with a trusted partner like Gentrack.

Customer Size and Industry Consolidation

Gentrack's customer base includes major utility companies and over 140 airports globally, with significant FY24 wins like Manchester Airports Group and Saudi Arabian airports. While individual large clients possess substantial purchasing power, the highly specialized nature of Gentrack's software and the substantial costs associated with integrating new systems often mitigate their collective ability to exert significant downward pressure on pricing or demand unfavorable terms.

Regulatory and Compliance Drivers

Utilities, especially in the energy and water sectors, operate under stringent regulatory frameworks. Gentrack's software is designed to help these companies navigate and adhere to these complex compliance demands, a critical function that significantly influences their operational continuity.

Gentrack's ability to enable clients to avoid substantial regulatory penalties, such as avoiding fines that could amount to millions for non-compliance, underscores the tangible value its solutions provide. This direct financial benefit makes Gentrack's offerings highly sticky, as switching costs become considerable when considering the risk of non-compliance.

The regulatory environment effectively reduces customer bargaining power by making Gentrack an essential partner for compliance. For example, in 2024, regulatory changes in the UK regarding data reporting for energy suppliers mandated new software capabilities, a space where Gentrack's solutions are well-positioned.

- Regulatory Compliance as a Value Driver: Gentrack's software directly addresses the need for utilities to meet complex regulatory and compliance requirements, a non-negotiable aspect of their operations.

- Mitigation of Financial Penalties: The software's capability to help clients avoid significant fines from regulators demonstrates a clear return on investment, reducing the incentive for customers to seek alternative, potentially non-compliant solutions.

- Indispensable Partnership: By embedding itself as a critical component for regulatory adherence, Gentrack fosters a partnership that diminishes customer bargaining power, as switching would introduce significant compliance risks and associated costs.

- Market Responsiveness to Regulatory Shifts: Gentrack's ability to adapt its software to evolving regulations, such as those impacting smart metering data in Australia in 2024, solidifies its position as a vital, hard-to-replace supplier.

Long-term Contractual Relationships

Gentrack's business model thrives on long-term contractual relationships, often spanning several years. These agreements are built on recurring revenue from software licenses, essential maintenance, and ongoing support services. This sticky nature of their offerings means that once a customer is integrated, switching costs become significant, thereby reducing customer bargaining power over time.

For example, in the fiscal year ending September 30, 2023, Gentrack reported that approximately 80% of its revenue was recurring. This high proportion of recurring revenue demonstrates the deep integration and ongoing reliance customers have on Gentrack's platforms, making it less likely for them to exert significant downward price pressure or demand unfavorable terms after the initial contract period.

- Recurring Revenue Dominance: Gentrack's high percentage of recurring revenue, around 80% as of FY23, anchors customers into long-term engagements.

- Embedded Software: The deep integration of Gentrack's software into client operations creates high switching costs.

- Upsell and Upgrade Potential: Opportunities for additional services and platform upgrades further solidify customer dependence.

- Diminishing Bargaining Power: While initial negotiations can be competitive, customer leverage typically wanes as the contract progresses due to these embedded factors.

Gentrack's Customer Power: Locked In by High Switching Costs

Gentrack's customer bargaining power is notably low due to the significant switching costs involved in replacing their mission-critical software. The deep integration into utility and airport operations, coupled with substantial financial and operational risks associated with migration, makes customers hesitant to change providers. For instance, Gentrack's FY23 results showed approximately 80% of revenue was recurring, indicating strong customer retention and reliance.

| Factor | Impact on Bargaining Power | Gentrack Specifics |

|---|---|---|

| Switching Costs | Lowers customer power | High financial and operational costs for migration; deep system integration. |

| Customer Loyalty/Retention | Lowers customer power | 80% recurring revenue (FY23) signifies strong ongoing relationships and reliance. |

| Regulatory Dependency | Lowers customer power | Software is crucial for compliance, avoiding substantial fines; e.g., UK data reporting mandates in 2024. |

| Specialized Nature of Software | Lowers customer power | Solutions are tailored for utilities and airports, with few direct, equally capable alternatives. |

Preview Before You Purchase

Gentrack Group Porter's Five Forces Analysis

This preview shows the exact Gentrack Group Porter's Five Forces Analysis you'll receive immediately after purchase, offering a comprehensive breakdown of competitive forces impacting the company. You'll gain insights into the bargaining power of buyers and suppliers, the threat of new entrants and substitutes, and the intensity of rivalry within the industry. This detailed analysis is ready for your immediate use, providing valuable strategic intelligence without any surprises.

Rivalry Among Competitors

Presence of Established Legacy Players

The utility and airport software sectors are characterized by the enduring presence of major legacy players such as Oracle and SAP. These established companies have historically commanded substantial market share, leveraging their long-standing relationships and extensive enterprise resource planning (ERP) suites to retain clients.

While Gentrack Group champions cloud-native, Software as a Service (SaaS) solutions, these incumbents remain formidable competitors. For large enterprises, particularly those already deeply integrated with comprehensive ERP systems, the appeal of migrating to a new, albeit modern, platform can be outweighed by the perceived risk and complexity of switching from familiar, albeit older, technologies.

Emergence of Agile Cloud-Native Competitors

Gentrack is experiencing heightened competition from nimble, cloud-native rivals such as Kraken. This new wave of competitors is leveraging modern technology stacks to offer more flexible and potentially cost-effective solutions. For instance, Kraken has successfully secured contracts in Gentrack's key Australian and New Zealand markets, even winning business from significant clients like Red Energy and Meridian.

Differentiation Through Innovation and Ecosystems

Gentrack is actively differentiating itself through its innovative g2.0 platform, a collaborative effort with major tech players like Salesforce and AWS. This composable technology allows for swift introduction of new customer propositions and a more efficient cost-to-serve model.

The company’s ability to foster innovation and integrate with expanding ecosystems, such as smart energy technologies exemplified by its partnership with Amber, is a critical factor in securing a competitive edge. This approach allows Gentrack to offer more comprehensive solutions than rivals.

High Stakes and Binary Nature of Contracts

The competitive rivalry within the utility and airport software sector is fierce, largely due to the significant financial implications of securing major contracts. These agreements are often substantial and mission-critical, creating a binary outcome for bidders: a win translates to a major revenue boost, while a loss can be a considerable setback. This high-stakes environment intensifies competition as companies vie for these lucrative opportunities.

The intensity of this rivalry was underscored in early 2024 when Gentrack Group experienced notable contract losses to competitor Kraken. These defeats sent ripples through the financial analyst community, serving as a stark reminder of the cutthroat nature of bidding for these high-value deals. Such outcomes highlight the crucial importance of every contract win in this specialized software market.

- High Contract Value: Utility and airport software contracts are typically multi-million dollar deals, making each win or loss highly impactful.

- Binary Outcomes: The nature of these bids means companies either win a significant contract or lose it entirely, with little room for partial success.

- Intense Competition: Recent contract losses for Gentrack Group to Kraken in early 2024 illustrate the aggressive competition for these critical software solutions.

- Market Sensitivity: The market reacts strongly to these contract wins and losses, as they directly influence revenue forecasts and company valuations.

Global Expansion and Regional Competition

Gentrack's global expansion strategy inherently intensifies its competitive rivalry. As the company pushes into new countries and deepens its presence in existing ones across both utilities and airports, it encounters a complex web of competitors. These range from established regional specialists with deep local market knowledge to other global software providers vying for the same contracts.

The success of Gentrack hinges on its ability to tailor its solutions to the unique regulatory environments and market demands of each region. This adaptability is crucial because competition isn't uniform; it varies significantly based on local market maturity and the presence of strong domestic players. For instance, in mature European utility markets, competition might be more focused on advanced feature sets and integration capabilities, whereas in emerging markets, the emphasis could be on cost-effectiveness and rapid deployment.

- Global Reach, Local Battles: Gentrack's presence in over 20 countries means it faces a diverse competitive landscape, from large multinational software firms to niche regional providers.

- Adaptability is Key: Success requires tailoring solutions to varied regulatory frameworks and market needs, a challenge highlighted by the differing demands in sectors like UK utilities versus Australian airports.

- Market Penetration Drives Rivalry: As Gentrack aims to grow its customer base and expand service offerings within existing territories, it directly confronts rivals seeking similar market share gains.

- 2024 Market Dynamics: The ongoing digital transformation across utilities and airports in 2024 means companies like Gentrack are competing not only on software but also on their ability to offer integrated digital solutions and data analytics.

Gentrack's Software Showdown: Battling Oracle, SAP, and Kraken

The competitive rivalry in the utility and airport software sectors is intense, driven by the high stakes of securing major, mission-critical contracts. Gentrack Group faces strong competition from both established legacy players like Oracle and SAP, and agile cloud-native rivals such as Kraken, which has notably secured contracts from Red Energy and Meridian in 2024.

| Competitor | Key Strengths | Gentrack's Position |

|---|---|---|

| Oracle | Established ERP suites, large enterprise relationships | Faces integration challenges for existing Oracle clients |

| SAP | Extensive ERP capabilities, global presence | Similar challenges to Oracle for deeply integrated clients |

| Kraken | Cloud-native, flexible solutions | Directly competing for contracts; has won business from Gentrack's clients |

SSubstitutes Threaten

In-house Development by Large Organizations

Large utilities and airport operators, possessing substantial IT departments and unique operational needs, may explore developing proprietary software solutions as an alternative to purchasing from specialized vendors like Gentrack. This in-house approach aims to tailor systems precisely to their workflows.

However, the immense undertaking of creating, managing, and continuously updating complex software, particularly for critical infrastructure, presents considerable challenges. The sheer cost, time investment, and the need for ongoing expertise often render these internal projects less practical and more resource-intensive than leveraging established, specialized providers.

Manual Processes or Outdated Systems

While modern utilities and airports are unlikely to revert to purely manual operations, the threat of substitutes can manifest as the continued reliance on severely outdated legacy systems. These systems often struggle with the real-time data demands and complex integrations required by today's operational environments. For instance, a utility still relying on paper-based meter readings or a legacy billing system that cannot integrate with smart grid technology faces significant inefficiencies and potential compliance issues.

Generic Enterprise Resource Planning (ERP) Solutions

Generic Enterprise Resource Planning (ERP) solutions from giants like Oracle and SAP present a potential substitute threat. While these broad-based systems might offer enough functionality for some utility or airport operations, they typically lack the deep industry-specific specialization that Gentrack provides. For instance, Gentrack's tailored approach to complex data sets and smart meter management offers a more refined solution compared to a one-size-fits-all ERP.

Delaying Software Upgrades or Modernization

Customers delaying software upgrades presents a subtle yet significant threat of substitution for Gentrack Group. This often stems from budget constraints, where organizations might postpone investments in new versions or modernizations. For instance, in 2024, many companies across various sectors tightened their IT spending, leading to extended lifecycles for existing software solutions rather than immediate upgrades.

The perceived high costs associated with switching, including implementation, training, and data migration, also encourage customers to stick with their current Gentrack systems. This inertia means Gentrack misses out on revenue from new licenses and enhanced service contracts. In the utilities sector, a key market for Gentrack, the complexity of integrating new billing or customer management systems can be a deterrent, pushing decisions to upgrade further down the line.

Furthermore, a lack of a compelling business case or a clear return on investment for modernization can lead customers to delay adoption. If existing systems, even if older, continue to meet basic operational needs, the impetus for change diminishes. This can be seen in how some legacy systems, though less efficient, are maintained to avoid the disruption and cost of a full overhaul, effectively acting as a substitute for Gentrack's latest offerings.

- Delayed Upgrades: Customers postponing modernization due to budget limitations in 2024.

- High Switching Costs: The financial and operational burden of migrating from existing Gentrack solutions.

- Lack of Compelling ROI: Businesses delaying upgrades if current systems meet essential needs.

- Extended System Lifecycles: Older software versions being maintained, acting as a substitute for new purchases.

Leveraging New Technologies Independently

Customers' ability to switch to alternative solutions poses a threat, especially as new technologies emerge. For instance, a utility company might consider integrating advanced AI or IoT solutions directly from specialized vendors, potentially bypassing a comprehensive platform provider like Gentrack. This could fragment the market and reduce reliance on a single, integrated system.

However, Gentrack is actively mitigating this threat by ensuring its g2.0 platform is designed to readily incorporate these emerging innovations. Their strategy involves acting as the central hub for these technologies, rather than being replaced by them. A prime example is their partnership with Amber, which allows for the integration of smart energy technologies directly into their offering.

- Threat of Substitutes: Customers may opt for standalone AI or IoT solutions, bypassing integrated platforms.

- Gentrack's Response: g2.0 platform is built to integrate new technologies, acting as an enabler rather than a bottleneck.

- Example: Partnership with Amber for smart energy tech integration showcases this strategy.

- Market Position: Gentrack aims to be the preferred integrated solution, reducing the appeal of fragmented technological adoption.

Facing Substitutes: In-house Development and Legacy Systems

The threat of substitutes for Gentrack Group stems from alternative ways customers can meet their needs, such as developing in-house solutions or relying on older, less integrated systems. While building proprietary software is challenging and costly, the continued use of outdated legacy systems presents a more immediate concern, hindering efficiency and compliance. Generic ERP solutions also offer a substitute, though they typically lack Gentrack's specialized industry focus.

Entrants Threaten

High Capital and R&D Investment

Entering the utility and airport software sectors demands significant upfront capital for research and development. New entrants must create sophisticated, reliable, and scalable software, a costly endeavor. Gentrack's own substantial R&D investments in its g2.0 platform underscore this barrier; newcomers would need to replicate this without the benefit of an established customer base.

Specialized Domain Expertise and Regulatory Knowledge

Gentrack Group's software solutions for utilities and airports necessitate profound industry-specific knowledge. This includes navigating intricate billing regulations, adhering to strict operational protocols, and meeting various compliance standards. New companies entering this market would need substantial investment in time and resources to cultivate such specialized domain expertise, presenting a considerable hurdle.

Difficulty in Building Trust and Reputation

New entrants face significant challenges in establishing trust and reputation within the utilities and airports sectors, which demand exceptionally reliable and secure software solutions. Building the necessary credibility to win contracts with these critical infrastructure providers is a protracted endeavor, often taking decades, presenting a formidable barrier for newcomers lacking a demonstrated history of success.

High Switching Costs for Customers as a Barrier

Gentrack Group benefits from high switching costs for its utility and energy clients. Existing customers are entrenched in their current software, making a move to a new provider a significant undertaking. This inertia creates a substantial barrier for potential new entrants aiming to disrupt the market.

These high switching costs are often tied to the complexity of migrating vast amounts of customer data, integrating with existing IT infrastructure, and the extensive training required for staff. For instance, a utility company might have decades of billing history and customer interaction data that needs to be meticulously transferred and validated. This process can be both time-consuming and expensive, often running into hundreds of thousands or even millions of dollars.

- High Capital Investment: New entrants need to invest heavily in developing robust, feature-rich software that can compete with established players like Gentrack.

- Customer Inertia: The significant costs and operational disruptions associated with migrating from existing, deeply integrated systems discourage utilities from switching providers.

- Proven Track Record: Established companies like Gentrack have a history of reliability and support, which is crucial for critical infrastructure software where downtime is unacceptable.

- Regulatory Compliance: New entrants must demonstrate compliance with stringent industry regulations, a hurdle that established providers have already cleared.

Network Effects and Ecosystem Integration

Gentrack Group benefits significantly from its deeply integrated ecosystem, which includes key partnerships with technology giants like Amazon Web Services (AWS) and Salesforce. These alliances, alongside strategic investments such as its stake in Amber, bolster Gentrack's product suite and market position. For instance, in 2024, Gentrack continued to leverage these partnerships to enhance its cloud-native utility management solutions, offering greater scalability and advanced data analytics to its clients.

The threat of new entrants is considerably reduced due to the substantial investment and time required to replicate Gentrack's established network effects and ecosystem integration. New players would need to forge comparable strategic alliances or develop exceptionally disruptive, self-contained technologies to gain traction. This barrier is amplified by the complexity of integrating with existing utility infrastructure and data systems, a hurdle Gentrack has already overcome.

- Established Ecosystem: Gentrack's partnerships with AWS and Salesforce provide a robust foundation for its offerings, enhancing scalability and data management capabilities.

- Strategic Investments: Investments like the one in Amber further strengthen Gentrack's product portfolio and market reach, creating a more comprehensive solution for clients.

- High Entry Barriers: New entrants face significant challenges in building comparable ecosystems or offering truly disruptive standalone products that can compete with Gentrack's integrated approach.

- Cost and Complexity: The cost and complexity of replicating Gentrack's established network and integrating with utility infrastructure present a formidable barrier to market entry.

Fortified Software Markets: High Barriers Deter New Competitors

The threat of new entrants into Gentrack Group's core markets of utility and airport software is significantly mitigated by high capital requirements and the need for specialized industry knowledge. Developing sophisticated, compliant, and reliable software demands substantial upfront investment in R&D, as evidenced by Gentrack's own significant expenditures on platforms like g2.0. New companies must also acquire deep expertise in complex billing, operational protocols, and regulatory frameworks, which takes considerable time and resources.

Building trust and a proven track record in critical infrastructure sectors is another major barrier, often taking decades to achieve. Gentrack's established reputation for reliability and support provides a competitive advantage that newcomers struggle to match. Furthermore, high customer switching costs, driven by the complexity and expense of data migration and system integration, create significant inertia for existing clients, making it difficult for new entrants to gain market share.

| Barrier to Entry | Description | Impact on New Entrants |

|---|---|---|

| Capital Investment | High R&D costs for sophisticated software. | Requires substantial funding to match established players. |

| Industry Expertise | Need for deep knowledge of regulations, operations, and billing. | Time-consuming and resource-intensive to acquire. |

| Reputation & Trust | Critical for infrastructure software; takes years to build. | New entrants lack the proven reliability sought by clients. |

| Switching Costs | High costs and complexity for clients to change providers. | Discourages utilities from adopting new software solutions. |

| Ecosystem Integration | Gentrack's partnerships (e.g., AWS, Salesforce) create network effects. | Difficult for new entrants to replicate the integrated value proposition. |

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis for Gentrack Group is built upon a foundation of comprehensive data, drawing from Gentrack's annual reports, investor presentations, and official company disclosures. We supplement this with industry-specific market research reports, regulatory filings from relevant authorities, and insights from financial news outlets to provide a robust competitive landscape assessment.