GE HealthCare Technologies Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

GE HealthCare Technologies Bundle

A Must-Have Tool for Decision-Makers

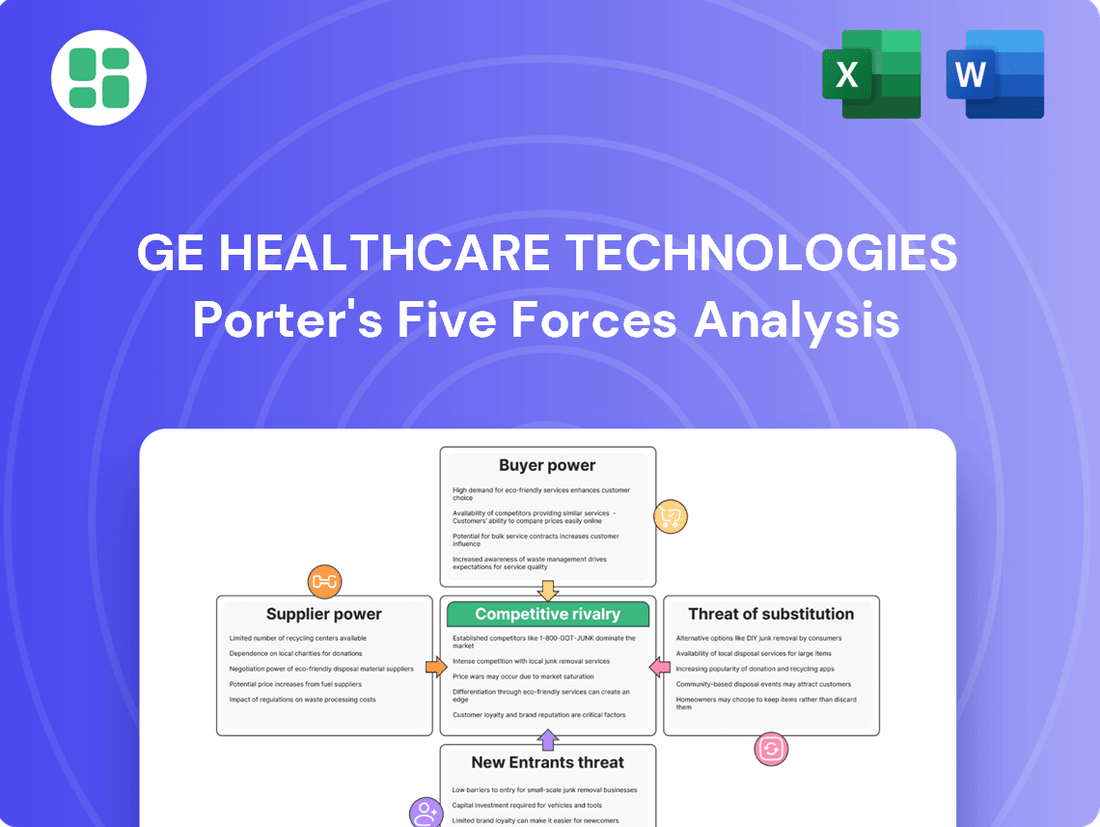

GE HealthCare Technologies operates in a dynamic market shaped by intense competition, significant buyer power from large healthcare systems, and the constant threat of new entrants with innovative technologies. Understanding these forces is crucial for strategic planning and identifying growth opportunities.

The complete report reveals the real forces shaping GE HealthCare Technologies’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Concentration of Suppliers

GE HealthCare Technologies faces a moderate bargaining power of suppliers, largely influenced by the concentration of suppliers for specialized medical components and raw materials. For instance, the advanced materials needed for their AI-enabled diagnostic tools and complex imaging equipment are often sourced from a select group of manufacturers. This concentration means these suppliers can potentially dictate terms, especially when the components are highly proprietary or require specialized manufacturing processes.

The unique nature of many inputs, particularly those critical for GE HealthCare's cutting-edge solutions, limits readily available alternatives. This scarcity of substitutes naturally bolsters the leverage of existing suppliers. While GE HealthCare's substantial global footprint enables some diversification of its supplier base, reducing absolute dependence on any single entity, the inherent specialization of certain inputs remains a key factor in supplier power.

The impact of geopolitical factors, such as trade tensions and tariffs, has become increasingly apparent in managing supplier relationships. For example, the U.S.-China trade dynamics in 2024 have prompted GE HealthCare to actively reconfigure its global supply chain. This strategic realignment aims to mitigate tariff impacts and foster local-for-local manufacturing initiatives, demonstrating a proactive strategy to control and reduce supplier leverage by building a more resilient and geographically diverse supply network.

Switching Costs for GE HealthCare

Switching suppliers for highly specialized components or critical pharmaceutical ingredients can involve substantial costs and time for GE HealthCare. This includes re-qualification, regulatory approvals, and integration with existing manufacturing processes, which strengthens supplier bargaining power. For example, changing a supplier for a unique imaging sensor or a diagnostic agent might require extensive testing to ensure product efficacy and compliance, making the transition complex and expensive.

Uniqueness of Supplier Offerings

When suppliers offer unique technology, patented materials, or highly specialized services that are essential for GE HealthCare's groundbreaking products, their bargaining power significantly increases. For instance, a provider of a one-of-a-kind contrast agent for pharmaceutical diagnostics or a specialized AI chip crucial for advanced imaging systems can demand higher prices due to the distinctiveness of their contributions.

Threat of Forward Integration by Suppliers

The threat of suppliers integrating forward into GE HealthCare's market, while theoretically possible, is significantly mitigated in the medical technology sector. This would mean a supplier creating their own finished medical devices or diagnostic equipment, directly challenging GE HealthCare's established product lines.

However, the substantial capital investment, complex regulatory approvals, and the need for extensive market penetration make this a formidable undertaking for most suppliers. For instance, bringing a new medical device to market can cost hundreds of millions of dollars and take many years to navigate FDA or EMA approvals. GE HealthCare's 2023 revenue of $19.2 billion underscores the scale of the market they operate in, a scale that is difficult for component suppliers to replicate independently.

- High Barriers to Entry: The medical device industry demands immense R&D spending, clinical trials, and navigating stringent regulatory pathways, making forward integration by suppliers exceptionally challenging.

- Capital Requirements: Launching competing products requires significant capital, far beyond the scope of most component manufacturers. GE HealthCare's substantial market capitalization provides a strong competitive moat.

- Regulatory Hurdles: Gaining approval for medical devices is a lengthy and costly process, often taking years and millions of dollars, which deters most suppliers from attempting direct market entry.

- Established Market Presence: GE HealthCare possesses strong brand recognition and established distribution channels, creating a significant hurdle for any supplier attempting to enter the market with new, competing products.

Importance of GE HealthCare to Suppliers

GE HealthCare Technologies, as a global leader in healthcare technology, wields considerable purchasing power due to its substantial order volumes. This makes it a critical client for many of its suppliers, potentially giving GE HealthCare leverage in negotiations. For instance, in 2023, GE HealthCare reported revenue of $18.3 billion, indicating the scale of its operations and its impact on the supply chain.

However, the bargaining power dynamic can shift depending on the supplier's specialization. For suppliers offering highly specialized components or unique technologies essential to GE HealthCare's product lines, their niche position can grant them significant influence. This is particularly true if alternative suppliers are scarce or if switching costs are high for GE HealthCare.

- Significant Customer: GE HealthCare's substantial purchasing volumes make it a key client for many suppliers, potentially granting it negotiation leverage.

- Niche Supplier Power: Suppliers with unique or highly specialized offerings may retain significant bargaining power, even with large customers like GE HealthCare.

- 2023 Revenue Context: GE HealthCare's $18.3 billion in revenue underscores its market presence and the importance of its supplier relationships.

GE HealthCare: Supplier Power and Specialized Component Challenges

GE HealthCare Technologies faces a moderate supplier bargaining power, primarily due to the specialized nature of critical components and the limited number of qualified manufacturers. For instance, the advanced materials for their AI-powered diagnostic tools are often sourced from a select few, giving these suppliers leverage.

The scarcity of readily available alternatives for unique inputs, especially those vital for GE HealthCare's innovative products, naturally strengthens supplier influence. While GE HealthCare's global scale allows for some supplier diversification, the specialized requirements for certain materials remain a key factor.

Switching suppliers for highly specialized components or critical pharmaceutical ingredients involves significant costs for GE HealthCare, including re-qualification and regulatory approvals, which bolsters supplier power. For example, changing a supplier for a unique imaging sensor requires extensive testing to ensure product efficacy and compliance.

| Factor | Impact on GE HealthCare | Example/Data Point |

| Supplier Concentration | Moderate to High | Specialized components for AI diagnostics sourced from a select group of manufacturers. |

| Uniqueness of Inputs | High | Proprietary materials for advanced imaging equipment limit alternatives. |

| Switching Costs | High | Re-qualification and regulatory approvals for new suppliers of critical components are time-consuming and expensive. |

| GE HealthCare Purchasing Power | Moderate | While GE HealthCare's 2023 revenue was $18.3 billion, niche suppliers of essential technologies can still command leverage. |

What is included in the product

This analysis explores the competitive forces impacting GE HealthCare Technologies, including the threat of new entrants, bargaining power of buyers and suppliers, threat of substitutes, and the intensity of rivalry.

GE HealthCare Technologies' Porter's Five Forces analysis provides a clear, one-sheet summary of all five forces—perfect for quick decision-making regarding competitive pressures.

Customers Bargaining Power

Customer Concentration and Size

GE HealthCare's customer base is largely concentrated among major healthcare systems, hospitals, and clinics. These entities often operate as consolidated groups and procure medical equipment and solutions in substantial quantities, giving them considerable leverage.

The significant purchasing power of large integrated delivery networks (IDNs), such as Ascension and OSF HealthCare, with whom GE HealthCare maintains strategic partnerships, is a key factor. Their sheer scale allows them to exert influence over market dynamics and negotiate favorable terms.

Consequently, these substantial customers can effectively demand preferential pricing, bespoke product configurations, and comprehensive support services, directly impacting GE HealthCare's profitability and market strategy.

Switching Costs for Customers

Switching costs for hospitals and healthcare providers are significant when moving between GE HealthCare's medical imaging systems or patient monitoring platforms. These costs encompass not only the outright replacement of expensive equipment but also the crucial investments in retraining clinical staff and ensuring seamless integration with current IT and electronic health record systems. For instance, a major hospital system might face millions in costs to transition from one MRI vendor to another, impacting workflow and patient care during the changeover.

Customer Price Sensitivity

Healthcare providers are increasingly feeling the pinch from rising costs, including inflation and higher labor expenses, coupled with reimbursement pressures. This environment makes them very sensitive to the prices of medical technology, pushing them to seek the best value. For instance, in 2024, many hospital systems reported operating margins in the low single digits, amplifying their focus on cost containment.

Value analysis committees (VACs) are a key mechanism through which this price sensitivity is expressed. These hospital committees meticulously evaluate the cost of medical devices against their proven clinical and financial benefits. This rigorous scrutiny forces companies like GE HealthCare to clearly articulate the return on investment and cost-effectiveness of their offerings, often requiring detailed data to justify pricing.

Availability of Substitute Products/Services for Customers

The bargaining power of customers is significantly influenced by the availability of substitute products and services. For GE HealthCare, this means customers in medical imaging, ultrasound, and patient monitoring have numerous alternatives from established competitors. Companies like Siemens Healthineers, Philips Healthcare, and Canon Medical Systems offer similar core functionalities, directly impacting GE HealthCare's pricing flexibility and market share.

This competitive environment, where multiple vendors provide comparable solutions, even with differing features or AI integration, empowers customers. They can readily switch between providers if GE HealthCare's offerings are perceived as less competitive on price, performance, or innovation. For instance, in the diagnostic imaging market, the ability to choose between different MRI or CT scanner manufacturers based on specific clinical needs and budget constraints is a key driver of customer power.

- Increased Customer Choice: GE HealthCare faces competition from major players like Siemens Healthineers, Philips Healthcare, and Canon Medical Systems across its key product segments.

- Impact of Substitutes: The presence of numerous vendors offering similar core technologies in medical imaging, ultrasound, and patient monitoring amplifies customer bargaining power.

- Innovation Imperative: This competitive landscape compels GE HealthCare to continually innovate and deliver superior value propositions to retain its customer base.

- Market Dynamics: In 2024, the healthcare technology market continues to see robust competition, with customers actively comparing features, pricing, and service agreements from various suppliers.

Customer Information and Transparency

Customers in the healthcare sector are becoming significantly more informed. With readily available data on product specifications, pricing structures, and competitor offerings, they are better equipped to negotiate favorable terms. This heightened transparency directly impacts GE HealthCare's pricing power.

For instance, in 2024, the increasing availability of comparative data on medical equipment performance and total cost of ownership allows hospital systems to benchmark GE HealthCare's solutions against rivals more effectively. This empowers them to demand competitive pricing and service level agreements.

- Informed Decision-Making: Patients and providers access vast amounts of information, leading to more discerning purchasing choices.

- Price Sensitivity: Greater transparency fuels price sensitivity, pushing providers to seek the most cost-effective solutions.

- Negotiation Leverage: Knowledge of market alternatives and competitor pricing grants customers significant bargaining leverage.

- Demand for Value: Customers increasingly demand not just product quality but also demonstrable value and transparent pricing models.

Healthcare Buyers Command Equipment Pricing

GE HealthCare's customers, primarily large hospital systems and integrated delivery networks, possess significant bargaining power due to their substantial purchasing volume and the availability of numerous comparable alternatives from competitors like Siemens Healthineers and Philips Healthcare. This power is amplified by increasing price sensitivity in the healthcare sector, where providers, facing tight operating margins in 2024, scrutinize costs rigorously through value analysis committees. Consequently, customers can effectively demand preferential pricing and customized solutions, impacting GE HealthCare's profitability and strategic pricing decisions.

| Customer Segment | Bargaining Power Factor | Impact on GE HealthCare |

|---|---|---|

| Large Hospital Systems (e.g., Ascension) | High Volume Purchasing | Leverage for price negotiation, demand for volume discounts |

| Integrated Delivery Networks (IDNs) | Consolidated Procurement | Increased negotiation leverage, ability to dictate terms |

| Healthcare Providers (General) | Price Sensitivity (e.g., low single-digit operating margins in 2024) | Pressure on pricing, demand for cost-effectiveness and value |

| Customers Seeking Alternatives | Availability of Substitutes (Siemens, Philips, Canon) | Reduced pricing flexibility, need for competitive differentiation |

Preview Before You Purchase

GE HealthCare Technologies Porter's Five Forces Analysis

The document you see is your deliverable. It’s ready for immediate use—no customization or setup required. This comprehensive Porter's Five Forces analysis for GE HealthCare Technologies delves into the competitive landscape, detailing the bargaining power of buyers and suppliers, the threat of new entrants and substitutes, and the intensity of existing rivalry within the healthcare technology sector. You are previewing the final version—precisely the same document that will be available to you instantly after buying.

Rivalry Among Competitors

Number and Diversity of Competitors

GE HealthCare operates in a market with a concentrated yet highly competitive field of rivals. The medical technology, pharmaceutical diagnostics, and digital solutions sectors are dominated by a few large, global companies.

Key competitors like Siemens Healthineers, Philips Healthcare, and Canon Medical Systems offer comparable product portfolios to GE HealthCare. This similarity means these players are in constant competition for market share, driving innovation and pricing strategies.

For instance, in 2023, Siemens Healthineers reported revenue of approximately €21.7 billion, underscoring its significant presence and competitive capacity against GE HealthCare's reported revenue of $18.3 billion for the same year.

Industry Growth Rate

The MedTech sector is poised for strong expansion, with AI-driven diagnostics and digital health leading the charge. However, more established areas like medical imaging are likely to see slower, more measured growth.

This differential growth rate fuels intense competition. While burgeoning markets attract new entrants and innovation, mature segments see companies battling fiercely for existing market share. The AI in diagnostics market, for example, is a prime area of focus, with significant projected growth attracting considerable competitive attention.

Product Differentiation and Innovation

GE HealthCare's competitive rivalry is intense, largely due to the critical role of product differentiation and continuous innovation. The healthcare technology sector thrives on advancements in areas such as artificial intelligence, digital solutions, and sophisticated diagnostic equipment. This necessitates substantial investment in research and development to stay ahead.

In 2024, GE HealthCare allocated over $1.3 billion to R&D, fueling the development of differentiating technologies like its AI-powered Air Recon DL for faster MRI scans and advanced digital X-ray systems. This commitment to innovation is mirrored by its competitors, who also pour significant resources into R&D to introduce novel technologies and secure a competitive edge.

High Fixed Costs and Exit Barriers

GE HealthCare Technologies operates in an industry with substantial fixed costs. These include significant investments in research and development, advanced manufacturing facilities, and broad sales and service infrastructures. For instance, in 2023, GE HealthCare reported R&D expenses of $1.4 billion, highlighting the ongoing commitment to innovation required in the sector.

These high fixed costs act as considerable barriers to exiting the market. Companies often find it more economically viable to continue operating and competing, even in downturns, to recover their substantial capital outlays rather than abandoning their investments. This persistence fuels intense competition among existing players.

Furthermore, the medical technology landscape necessitates continuous innovation and strict adherence to regulatory standards, such as those set by the FDA. These ongoing requirements contribute to elevated fixed costs, reinforcing the difficulty of exiting and encouraging sustained competitive rivalry.

- High R&D Investment: GE HealthCare's 2023 R&D spending was $1.4 billion, a critical factor in maintaining competitiveness.

- Capital-Intensive Operations: Significant upfront costs for manufacturing and service networks create high barriers to entry and exit.

- Regulatory Compliance Costs: Meeting stringent industry regulations adds to the fixed cost structure, influencing competitive dynamics.

- Exit Barriers: The need to recoup substantial investments makes exiting the market challenging, leading to prolonged competition.

Strategic Alliances and Acquisitions

Strategic alliances and acquisitions are key tools for companies like GE HealthCare to bolster their market presence and innovate. By teaming up or buying other entities, they can broaden their product ranges and tap into new technologies or customer bases. For instance, GE HealthCare's alliance with Ascension and OSF HealthCare aims to deliver more complete care solutions, while its partnership with FPT focuses on advancing AI in healthcare.

- Market Consolidation: These moves can lead to a more consolidated market, where larger players with integrated offerings become more dominant.

- Innovation Acceleration: Collaborations, like GE HealthCare's work with FPT on AI, speed up the adoption of cutting-edge technologies, potentially giving partners a significant edge.

- Competitive Advantage: By forming alliances and acquiring complementary businesses, companies can create more robust and appealing solutions, thereby intensifying competition for those who don't participate in such strategic moves.

Healthcare Tech: The Battle for Market Share

Competitive rivalry in the healthcare technology sector is fierce, driven by a few dominant global players like GE HealthCare, Siemens Healthineers, and Philips Healthcare. These companies offer similar products, leading to intense competition for market share and a constant push for innovation and favorable pricing. For example, in 2023, Siemens Healthineers achieved revenues of approximately €21.7 billion, directly competing with GE HealthCare's $18.3 billion revenue for the same period.

High fixed costs associated with research and development, advanced manufacturing, and extensive service networks act as significant barriers to market entry and exit. GE HealthCare's 2023 R&D spending of $1.4 billion illustrates the substantial investment required to stay competitive. These costs encourage existing players to remain in the market, intensifying ongoing rivalry.

The dynamic nature of the MedTech industry, with rapid advancements in AI-driven diagnostics and digital health, further fuels competition. Companies are compelled to invest heavily in R&D to differentiate their offerings, as seen with GE HealthCare's over $1.3 billion R&D allocation in 2024 for technologies like AI-powered MRI scans. This creates a challenging environment where continuous innovation is paramount.

Strategic alliances and acquisitions are crucial for companies like GE HealthCare to enhance their market position and accelerate innovation. These moves, such as GE HealthCare's alliances with Ascension and FPT, can lead to market consolidation and provide a competitive edge, intensifying pressure on rivals who do not engage in similar strategic partnerships.

| Key Competitor | 2023 Revenue (Approx.) | Key Focus Areas |

|---|---|---|

| GE HealthCare Technologies | $18.3 billion | Medical Imaging, Digital Solutions, Pharmaceutical Diagnostics |

| Siemens Healthineers | €21.7 billion (approx. $23.6 billion) | Medical Imaging, Diagnostics, Digital Health Services |

| Philips Healthcare | €17.8 billion (approx. $19.4 billion) | Diagnostic Imaging, Patient Monitoring, Connected Care |

| Canon Medical Systems | Not publicly disclosed separately, part of Canon Inc. | Medical Imaging, Healthcare IT |

SSubstitutes Threaten

Alternative Diagnostic Methods

The threat of substitutes for GE HealthCare's diagnostic offerings is growing as alternative methods emerge to achieve similar health insights. For instance, advancements in liquid biopsies, which analyze biomarkers in blood or other bodily fluids, present a potential substitute for some tissue-based diagnostics. In 2024, the global liquid biopsy market was estimated to be worth billions, showcasing its increasing adoption.

Furthermore, the rise of non-invasive monitoring systems, like continuous glucose monitors that reduce the need for traditional blood draws, also poses a substitute threat. As preventive care and personalized medicine gain traction, there's a greater demand for accessible and less invasive diagnostic approaches, potentially diverting demand from some of GE HealthCare's established imaging and lab-based solutions.

Shift to Less Invasive Procedures

The increasing prevalence of less invasive medical procedures presents a significant threat of substitution for GE HealthCare. As surgical techniques advance, the need for certain traditional diagnostic and monitoring equipment may diminish. For instance, the rise of robotic-assisted surgery, which often requires less extensive pre-operative imaging, could reduce demand for some of GE HealthCare's established product lines.

Digital Health and Telemedicine Solutions

The rise of digital health and telemedicine presents a significant threat of substitutes for GE HealthCare. These solutions can decentralize care, lessening the need for traditional, hospital-centric equipment. For instance, the global telemedicine market was valued at approximately $117.4 billion in 2023 and is projected to grow substantially, indicating a shift in how healthcare is accessed and delivered.

AI-powered virtual assistants and wearable devices are increasingly capable of providing continuous patient monitoring and remote consultations. This can directly substitute for certain in-person diagnostic procedures that rely on GE HealthCare's imaging and monitoring technologies. The adoption of remote patient monitoring systems, for example, surged during and after the pandemic, with a significant portion of healthcare providers reporting increased usage for chronic disease management.

Preventive Health and Wellness Trends

The growing societal emphasis on preventive health and wellness presents a subtle but significant threat of substitution for GE HealthCare. This shift prioritizes lifestyle modifications and early disease detection over reactive, late-stage treatments.

While preventive measures still necessitate diagnostic equipment, the overall demand for certain high-end therapeutic devices could be indirectly affected by a reduced need for extensive interventions. For instance, a successful focus on managing chronic conditions through lifestyle changes might lessen the reliance on advanced surgical equipment or long-term care technologies.

However, GE HealthCare's strategic alignment with early detection and precision medicine partially mitigates this threat. The company's investments in advanced imaging, AI-powered diagnostics, and personalized treatment planning directly support the preventive health movement.

- Preventive Healthcare Growth: The global preventive healthcare market was valued at approximately $1.3 trillion in 2023 and is projected to grow significantly, indicating a strong societal trend.

- Shift in Treatment Modalities: A move towards less invasive procedures and early intervention could reduce the market share for certain traditional, more complex medical devices.

- GE HealthCare's Mitigation Strategy: GE HealthCare's focus on diagnostic solutions and digital health platforms positions it to capitalize on, rather than be undermined by, the preventive health trend.

Evolution of AI and Software-only Diagnostics

The increasing sophistication of AI and machine learning in diagnostics, especially in image analysis and predictive analytics, could spawn software-only solutions that replicate functions traditionally reliant on specialized hardware. For instance, advancements in deep learning for radiology interpretation are enabling software to identify anomalies with accuracy comparable to human experts, potentially reducing the need for certain imaging hardware.

While GE HealthCare strategically embeds AI within its advanced medical devices, the emergence of standalone AI-driven diagnostic software poses a potential long-term substitute threat. These solutions can operate on readily available computing platforms, offering a cost-effective alternative if they achieve high accuracy and become widely adopted as independent tools, bypassing the need for proprietary hardware integration.

By mid-2024, the global AI in healthcare market was projected to reach substantial figures, with diagnostic AI a significant component. For example, some reports estimated the AI in medical diagnostics market alone to be worth tens of billions of dollars, indicating a robust and growing sector where software-only solutions could gain traction.

- AI-powered diagnostic software can reduce reliance on specialized imaging hardware.

- Standalone AI solutions offer a potentially more cost-effective alternative.

- The global AI in healthcare market, including diagnostics, is experiencing rapid growth.

- GE HealthCare's strategy involves integrating AI, but independent software presents a competitive challenge.

Diagnostic Substitutes: A Growing Threat

The threat of substitutes for GE HealthCare's diagnostic offerings is significant, driven by advancements in alternative health insights and monitoring methods. Liquid biopsies, for example, offer a less invasive substitute for some traditional tissue diagnostics, with the global market valued in the billions in 2024. Similarly, non-invasive systems like continuous glucose monitors reduce the need for conventional blood draws, aligning with the growing demand for accessible, preventive care.

The rise of digital health and telemedicine further amplifies this threat, decentralizing care and potentially lessening reliance on hospital-centric equipment. The global telemedicine market, valued at approximately $117.4 billion in 2023, highlights a significant shift in healthcare delivery. AI-powered virtual assistants and wearables also offer continuous monitoring and remote consultations, substituting for certain in-person diagnostic procedures.

The increasing sophistication of AI and machine learning in diagnostics, particularly in image analysis, could lead to software-only solutions that replicate functions traditionally requiring specialized hardware. For instance, deep learning for radiology interpretation is achieving accuracy comparable to human experts, potentially reducing the need for certain imaging hardware. By mid-2024, the global AI in healthcare market, with diagnostics as a key component, was projected to reach tens of billions of dollars, indicating a robust sector where software-only solutions can gain traction.

| Substitute Type | Description | Market Trend/Data Point (2023-2024) | Impact on GE HealthCare |

|---|---|---|---|

| Liquid Biopsies | Analysis of biomarkers in bodily fluids | Global market valued in billions (2024 estimate) | Potential reduction in demand for some tissue-based diagnostics |

| Non-invasive Monitoring | Continuous patient monitoring systems | Growing adoption for chronic disease management | May reduce reliance on traditional lab-based diagnostics |

| Digital Health/Telemedicine | Remote consultations and decentralized care | Global market valued at $117.4 billion (2023) | Decreased need for hospital-centric diagnostic equipment |

| AI-Powered Software | Standalone diagnostic interpretation software | AI in medical diagnostics market worth tens of billions (mid-2024 projection) | Potential bypass of proprietary hardware integration |

Entrants Threaten

High Capital Investment Requirements

The medical technology and pharmaceutical diagnostics sectors demand immense capital for research and development, state-of-the-art manufacturing, and establishing robust global distribution. For instance, developing a new advanced imaging system can easily cost hundreds of millions of dollars, a significant hurdle for any newcomer.

Extensive Regulatory Hurdles and Compliance

The medical device and pharmaceutical diagnostics industries, where GE HealthCare Technologies operates, are subject to stringent oversight from agencies like the U.S. Food and Drug Administration (FDA) and similar global bodies. New companies must navigate costly and time-consuming pre-market approval pathways, ongoing post-market surveillance, and intricate compliance mandates, often spanning several years. This demanding regulatory environment significantly deters potential new competitors.

Brand Recognition and Established Relationships

GE HealthCare's extensive history, spanning over 125 years, has cultivated formidable brand recognition. This, coupled with a global installed base of roughly 5 million units, signifies deep trust and reliance from healthcare institutions. Newcomers face a significant hurdle in replicating this established reputation and the critical distribution networks that GE HealthCare already commands.

Proprietary Technology and Intellectual Property

GE HealthCare's substantial patent portfolio and proprietary technologies in areas like medical imaging and pharmaceutical diagnostics create a significant hurdle for potential new entrants. For instance, the company holds numerous patents covering its advanced ultrasound technology, making it difficult for newcomers to replicate its capabilities without extensive legal and financial resources. This deep well of intellectual property, often a result of decades of research and development, acts as a powerful deterrent, requiring new companies to either invest heavily in their own R&D or navigate complex licensing agreements.

The sheer scale of investment needed to develop comparable intellectual property or circumvent existing patents is a major barrier. Newcomers would need to commit substantial capital to research and development, a process that is both time-consuming and inherently risky. GE HealthCare's ongoing investments, such as its focus on AI-enabled medical devices, further elevate this barrier by continuously pushing the technological frontier.

- Patented Technologies: GE HealthCare possesses a vast library of patents covering its core product lines, including MRI, CT scanners, and diagnostic ultrasound equipment.

- R&D Investment: The company consistently invests billions in research and development annually, a figure that new entrants would struggle to match to achieve comparable innovation. In 2023, GE HealthCare reported $2.8 billion in R&D expenses.

- AI Integration: The integration of artificial intelligence into its devices, such as AI-powered image reconstruction, presents a sophisticated technological barrier that requires specialized expertise to overcome.

- Market Dominance: Existing market share and established customer relationships built on these proprietary technologies also make it challenging for new entrants to gain traction.

Economies of Scale and Experience Curve

GE HealthCare Technologies benefits significantly from established economies of scale. In 2023, the company reported revenues of $18.3 billion, demonstrating its substantial market presence which allows for cost advantages in manufacturing, supply chain management, and research and development. This scale makes it challenging for new entrants to match GE HealthCare's per-unit production costs.

The experience curve also presents a formidable barrier. Years of operational refinement have equipped GE HealthCare with deep-seated efficiencies and proprietary knowledge in areas like medical imaging and diagnostics. This accumulated expertise translates into smoother production processes and a better understanding of market needs, creating a steep learning curve for any new competitor aiming to achieve similar cost-effectiveness and product quality.

- Economies of Scale: GE HealthCare's $18.3 billion revenue in 2023 enables lower per-unit costs in production and procurement.

- Experience Curve: Decades of operational refinement lead to superior efficiency and market understanding, a difficult advantage for newcomers to replicate.

- R&D Investment: Significant and ongoing investment in research and development, a hallmark of established players, further solidifies their competitive edge.

Healthcare Tech: High Barriers to Entry

The threat of new entrants for GE HealthCare Technologies is considerably low due to substantial capital requirements for R&D and manufacturing, alongside rigorous regulatory hurdles. Established brand loyalty, extensive patent portfolios, and significant economies of scale further solidify GE HealthCare's position, making it extremely difficult for newcomers to compete effectively.

| Barrier Type | Description | Impact on New Entrants | GE HealthCare's Advantage |

|---|---|---|---|

| Capital Requirements | High costs for R&D, manufacturing, and distribution. | Significant financial barrier. | Established infrastructure and funding capacity. |

| Regulatory Hurdles | Strict FDA and global agency approvals, compliance. | Lengthy and costly market entry process. | Expertise in navigating complex regulatory landscapes. |

| Brand & Reputation | Over 125 years of history, global installed base. | Difficulty in building trust and market acceptance. | Deep customer relationships and brand recognition. |

| Intellectual Property | Extensive patents, proprietary technologies. | Requires significant investment to replicate or circumvent. | Technological leadership and competitive moat. |

| Economies of Scale | $18.3 billion revenue in 2023, efficient operations. | Inability to match cost advantages. | Lower per-unit costs and supply chain efficiencies. |

Porter's Five Forces Analysis Data Sources

Our GE HealthCare Technologies Porter's Five Forces analysis is built upon a foundation of verified data, including the company's annual reports, SEC filings, and industry-specific market research from reputable firms like Gartner and IDC.