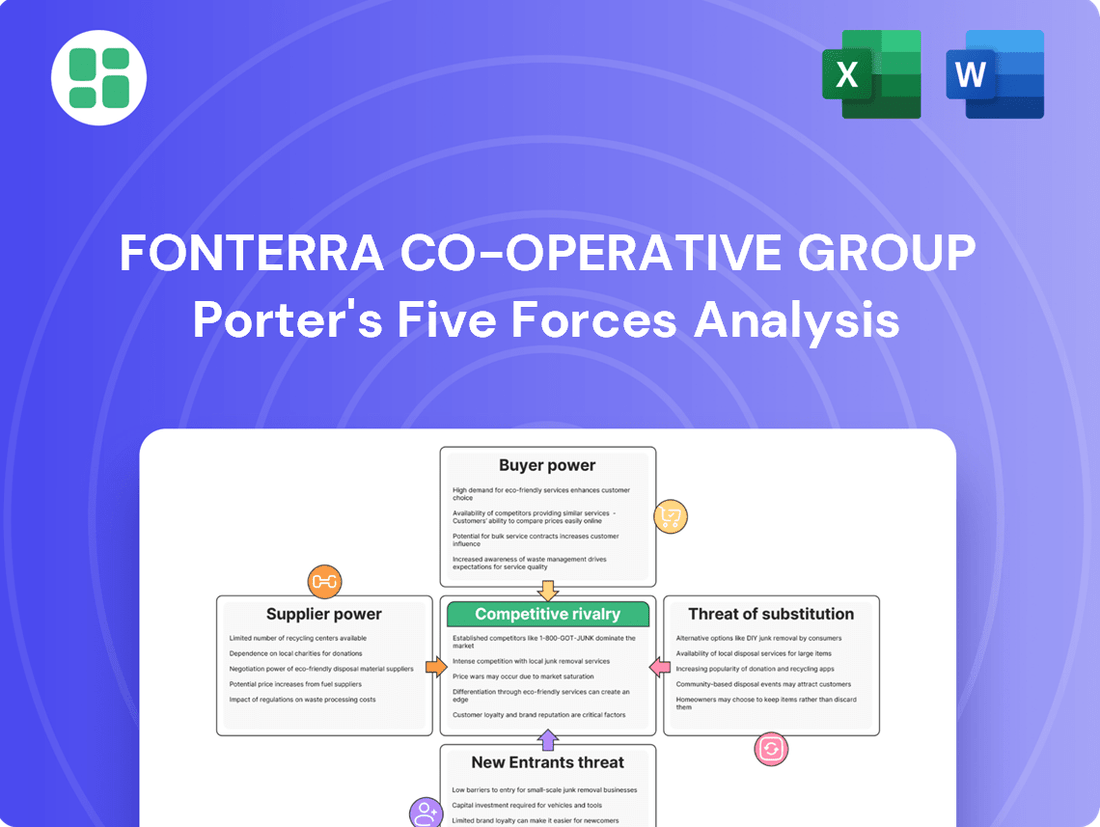

Fonterra Co-operative Group Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Fonterra Co-operative Group Bundle

Go Beyond the Preview—Access the Full Strategic Report

Fonterra Co-operative Group faces significant competitive pressures, with the bargaining power of buyers and the threat of substitutes being particularly noteworthy forces. Understanding the intensity of these dynamics is crucial for strategic planning.

The complete report reveals the real forces shaping Fonterra Co-operative Group’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Collective Ownership and Aligned Interests

Fonterra's co-operative model, with roughly 9,000 New Zealand farmer-owners as its core milk suppliers, fundamentally alters the traditional supplier bargaining power dynamic. This structure creates a powerful alignment of interests, as farmers are directly invested in the co-operative's success and stability.

The farmers' direct stake in Fonterra's profitability and consistent milk price payouts fosters a strong, collaborative relationship. This contrasts sharply with the often adversarial relationships seen between independent suppliers and corporations, significantly mitigating supplier leverage.

High Switching Costs for Farmers

For New Zealand dairy farmers, the decision to switch milk processors away from Fonterra is fraught with significant logistical and financial challenges. Fonterra's extensive, established network for milk collection and processing across New Zealand presents a formidable barrier to entry for potential competitors, leaving farmers with few readily available alternatives.

These high switching costs effectively curtail the bargaining power of individual farmers. The substantial investment required to change processors, coupled with the limited viable options, means farmers are less likely to threaten to divert their milk supply, thereby strengthening Fonterra's position as a buyer.

Farmgate Milk Price Influence

The bargaining power of suppliers, particularly dairy farmers, is a significant factor for Fonterra. While farmers are owners, the Fonterra board, representing farmer shareholders, sets the Farmgate Milk Price. This price is a critical determinant of farmer profitability and directly influences their willingness to supply milk to the co-operative.

For the 2024/25 season, Fonterra's forecast Farmgate Milk Price range was NZ$7.50 to NZ$8.50 per kilogram of milk solids (kg/MS). The 2025/26 season forecasts also indicated a strong milk price environment. These favorable prices enhance farmer satisfaction and loyalty, thereby strengthening their position as suppliers.

Dependence on Fonterra's Market Access

Fonterra's extensive global reach, serving over 100 countries, is a significant factor in its farmer-owners' bargaining power. This unparalleled market access is a critical asset that individual farmers or smaller entities would struggle to establish independently.

The co-operative's robust distribution network effectively channels dairy products to international markets, a service that is difficult for any single supplier to match. This reliance on Fonterra for global market penetration inherently limits the bargaining power of individual suppliers outside the co-operative structure.

- Global Market Access: Fonterra's presence in over 100 countries provides a crucial advantage.

- Distribution Network: The co-operative's established logistics are hard to replicate.

- Reduced Supplier Leverage: Dependence on Fonterra for market access diminishes individual supplier bargaining power.

Farmer Engagement and Support Programs

Fonterra's commitment to its farmer-owners is evident in its robust engagement and support programs. In the 2023 financial year, Fonterra invested NZ$100 million in initiatives aimed at enhancing on-farm productivity and sustainability, directly benefiting its supplier base.

- Farmer Support: Fonterra offers financial incentives and technical assistance for on-farm efficiency improvements.

- Sustainability Focus: Programs encourage and fund sustainable farming practices, aligning with co-operative goals.

- Relationship Strengthening: These initiatives foster deeper integration and loyalty among farmer-owners.

- Productivity Gains: Support aims to boost farm output, ensuring a stable and high-quality milk supply.

Co-op Structure: Weakening Supplier Power

Fonterra's co-operative structure significantly mitigates supplier bargaining power. With approximately 9,000 farmer-owners, Fonterra benefits from aligned interests and high switching costs for farmers, as Fonterra's extensive infrastructure is difficult to replicate. The co-operative's global market access, serving over 100 countries, further solidifies this position, making individual farmer reliance on Fonterra for market penetration a key factor.

Fonterra's investment in farmer support, such as NZ$100 million in on-farm productivity and sustainability initiatives during the 2023 financial year, strengthens the supplier relationship. This focus on farmer prosperity, coupled with favorable forecast Farmgate Milk Prices for the 2024/25 season (NZ$7.50 to NZ$8.50 per kg/MS), enhances loyalty and reduces the likelihood of farmers leveraging their position.

| Metric | Value | Year | Impact on Supplier Bargaining Power |

|---|---|---|---|

| Number of Farmer-Owners | ~9,000 | 2024 | Lowers individual power due to collective ownership |

| Global Market Reach | 100+ countries | 2024 | Reduces farmer leverage by providing essential market access |

| On-Farm Investment | NZ$100 million | FY2023 | Increases farmer loyalty and reduces incentive to seek alternatives |

| Forecast Farmgate Milk Price | NZ$7.50 - NZ$8.50 / kg/MS | 2024/25 | Favorable pricing enhances farmer satisfaction and reduces bargaining leverage |

What is included in the product

This analysis delves into the competitive forces impacting Fonterra Co-operative Group, examining the bargaining power of buyers and suppliers, the threat of new entrants and substitutes, and the intensity of rivalry within the global dairy industry.

Easily identify and mitigate competitive threats by visualizing the intensity of each of Porter's Five Forces for Fonterra, enabling proactive strategic adjustments.

Customers Bargaining Power

Diverse Global Customer Base

Fonterra's bargaining power of customers is significantly mitigated by its exceptionally diverse global customer base, spanning over 100 countries. This broad reach includes dairy ingredient buyers for manufacturing, the foodservice sector, and end-consumer brands, meaning no single customer or small cluster holds substantial sway over Fonterra's operations.

In 2024, Fonterra's strategy continues to emphasize higher-value channels, further fragmenting its customer base and reducing the potential for concentrated customer power. This approach allows Fonterra to optimize returns by catering to segments less sensitive to price alone.

Availability of Alternative Dairy Suppliers

The bargaining power of customers is significantly influenced by the availability of alternative dairy suppliers. For Fonterra, particularly in bulk dairy ingredient sales, customers can source products from major dairy-producing regions globally, including the European Union and the United States. This broad access to alternatives means buyers can readily compare pricing and quality across different suppliers, effectively putting pressure on Fonterra's pricing strategies.

Price Sensitivity in Commodity Markets

For commodity dairy ingredients, customers are often highly price-sensitive, consistently seeking the most cost-effective supply. This inherent price sensitivity means that Fonterra must remain competitive on cost for these products, limiting its ability to command premium prices in these segments. In 2024, the global dairy commodity market experienced significant price volatility, with key ingredients like skim milk powder fluctuating based on supply and demand dynamics, reinforcing this customer pressure.

Value Proposition of Specialised Products

Fonterra's specialized products, particularly in foodservice and consumer markets, command a degree of customer loyalty due to their emphasis on quality, innovation, and established brand recognition. This focus allows Fonterra to reduce the impact of customer price sensitivity, as many buyers are willing to pay more for superior ingredients or trusted names.

For instance, Fonterra's foodservice offerings often include functional ingredients designed for specific culinary applications, and their consumer brands are built on decades of trust. This differentiation means that for certain product categories, the bargaining power of customers is somewhat diminished because the unique value proposition outweighs a simple price comparison.

- Fonterra's foodservice channel leverages specialized ingredients, boosting its value proposition.

- Consumer brands benefit from Fonterra's reputation, reducing price sensitivity.

- In fiscal year 2023, Fonterra reported strong performance in its Foodservice segment, indicating customer willingness to pay for specialized dairy solutions.

Strong Customer Relationships and Service

Fonterra actively cultivates enduring customer relationships by offering comprehensive technical and innovation support. This dedication to service and collaborative partnerships, evidenced by industry accolades, fosters significant customer loyalty. Consequently, customers are less inclined to switch providers based solely on minor price variations, thereby mitigating the bargaining power of customers.

- Customer Retention: Fonterra's emphasis on service strengthens loyalty, making price the sole driver for switching less impactful.

- Innovation Support: Providing technical and innovation assistance creates value beyond the product itself, deepening customer ties.

- Partnership Approach: Treating customers as partners rather than just buyers fosters a sense of mutual benefit and reduces price sensitivity.

Customer Fragmentation: Weakening Buyer Influence

Fonterra's diverse global customer base, spanning over 100 countries and encompassing ingredient buyers, foodservice, and consumer brands, significantly dilutes individual customer bargaining power. This fragmentation means no single entity can exert substantial influence over Fonterra's pricing or terms. In 2024, Fonterra's continued focus on higher-value segments further reduces the potential for concentrated customer power, as these channels are less driven by price alone.

| Customer Segment | Impact on Bargaining Power | Fonterra's Strategy |

|---|---|---|

| Global Ingredient Buyers | Moderate to High (Price Sensitivity, Alternatives Available) | Focus on cost competitiveness, leveraging economies of scale. |

| Foodservice Sector | Moderate (Value Proposition, Brand Recognition) | Emphasis on specialized ingredients, innovation, and technical support. |

| Consumer Brands | Low to Moderate (Brand Loyalty, Quality Perception) | Leveraging established brand trust and product differentiation. |

Same Document Delivered

Fonterra Co-operative Group Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase, detailing Fonterra's competitive landscape through Porter's Five Forces. You'll gain a comprehensive understanding of the threats from new entrants and substitute products, as well as the bargaining power of buyers and suppliers. This analysis also thoroughly assesses the intensity of rivalry within the dairy industry, providing actionable insights for strategic decision-making.

Rivalry Among Competitors

Intense Global Dairy Market Competition

The global dairy market is a fiercely contested arena, with giants like Lactalis, Nestlé, and Danone constantly vying for market share alongside a multitude of regional and local players. This intense rivalry spans across all product segments, from essential dairy ingredients to finished consumer goods, meaning Fonterra faces a diverse set of competitors depending on the specific market it operates in.

Competition for New Zealand Milk Supply

While Fonterra remains the dominant force in New Zealand's dairy sector, it contends with a growing number of smaller, independent dairy processors actively vying for raw milk supply. This competition, though often localized, puts pressure on Fonterra's ability to secure its entire milk pool.

This internal rivalry has contributed to a noticeable, albeit slight, erosion of Fonterra's market share within New Zealand. For instance, in the 2023-2024 season, Fonterra's share of the total New Zealand milk supply saw a marginal dip compared to previous years, reflecting the increased competition from these agile, independent players.

Product and Channel Diversification

Fonterra actively diversifies its product portfolio and sales channels to reduce direct competition. By prioritizing higher-margin segments such as foodservice and specialized ingredients, the co-operative aims to sidestep intense rivalry in more commoditized areas of the dairy market.

This strategic shift is evident in Fonterra's focus on value-added products. For instance, in the fiscal year ending July 31, 2023, Fonterra's Ingredients segment, which includes specialized ingredients, reported strong performance, contributing to overall revenue growth and demonstrating the success of this diversification strategy in a competitive landscape.

Innovation and Sustainability as Competitive Differentiators

Fonterra faces intense competition where rivals are increasingly setting themselves apart through novel product development, robust sustainability initiatives, and sophisticated supply chain management. This dynamic forces Fonterra to continually adapt.

To stay ahead, Fonterra is channeling significant investment into digital transformation projects and actively pursuing decarbonization strategies. Furthermore, the co-operative is focused on creating premium, value-added dairy products that cater to evolving consumer demands and offer a distinct advantage in the marketplace.

- Product Innovation: Fonterra's investment in R&D aims to create specialized, high-margin dairy ingredients and consumer products.

- Sustainability Leadership: The co-operative is committed to reducing its environmental footprint, a key differentiator for increasingly eco-conscious consumers and business partners.

- Digital Supply Chain: Enhancing traceability and efficiency through digital solutions provides a competitive edge in managing a complex global network.

- Value-Added Solutions: Shifting focus from commodity milk to specialized ingredients and finished goods allows for greater margin capture and differentiation.

Market Share and Scale

Fonterra's competitive rivalry is intense, yet its global scale offers a distinct advantage. Despite a slight decrease in its New Zealand market share, the co-operative continues to dominate as the world's largest dairy exporter. This colossal scale translates into significant economies of scale across processing, logistics, and its extensive global distribution network. For the fiscal year ending July 31, 2023, Fonterra reported revenue of NZ$22.1 billion, underscoring its vast operational footprint.

This immense scale provides Fonterra with a substantial cost advantage, making it challenging for smaller competitors to replicate its efficiency and reach. The ability to process vast quantities of milk and distribute products worldwide at a lower per-unit cost grants Fonterra considerable market power. For instance, in 2023, Fonterra handled approximately 15 billion litres of milk, a volume that dwarfs most rivals.

- Global Dominance: Fonterra remains the largest dairy exporter worldwide, a position built on decades of expansion and market penetration.

- Economies of Scale: Significant cost efficiencies are realized in processing, logistics, and global distribution due to its sheer size.

- Market Power: This scale allows Fonterra to wield considerable influence in global dairy markets, often setting benchmarks for pricing and supply.

- Rivalry Challenge: Smaller dairy players find it difficult to compete on cost and reach, as they lack Fonterra's established infrastructure and volume.

Global Dairy Rivalry: Navigating Competition

Fonterra faces a highly competitive global dairy market, with major players like Lactalis and Nestlé constantly vying for market share. While Fonterra's scale provides significant cost advantages, smaller domestic competitors in New Zealand are chipping away at its milk supply. This intense rivalry necessitates continuous innovation and strategic diversification by Fonterra to maintain its market position.

Fonterra's competitive landscape is characterized by rivals differentiating through product innovation, sustainability efforts, and advanced supply chain management. The co-operative is actively investing in digital transformation and decarbonization to strengthen its competitive edge. For the fiscal year ending July 31, 2023, Fonterra reported revenue of NZ$22.1 billion, highlighting its substantial global presence amidst this rivalry.

Fonterra's global dominance as the largest dairy exporter, handling around 15 billion litres of milk in 2023, grants it considerable economies of scale. This allows for cost efficiencies in processing and distribution that smaller competitors struggle to match. The co-operative's strategy of focusing on value-added products and specialized ingredients aims to mitigate direct competition in more commoditized dairy sectors.

| Key Competitors | Market Focus | 2023 Revenue (Approx.) |

| Lactalis | Global Dairy Products, Cheese, Milk | €28 Billion (2023) |

| Nestlé | Global Food & Beverage, Dairy Products | CHF 91.0 Billion (2023) |

| Danone | Global Food & Beverage, Dairy Products | €27.2 Billion (2023) |

| Fonterra | Global Dairy Ingredients & Consumer Products | NZ$22.1 Billion (FY23) |

SSubstitutes Threaten

Rising Popularity of Plant-Based Alternatives

The growing appeal of plant-based options like oat, almond, and soy milk presents a notable threat to Fonterra's traditional dairy products. Consumers are increasingly choosing these alternatives for perceived health benefits, ethical considerations, and environmental impact.

This shift directly impacts milk consumption, offering a viable substitute that can erode market share for conventional dairy. For instance, the global plant-based milk market was valued at approximately $20.1 billion in 2023 and is projected to reach $47.5 billion by 2030, indicating a substantial and growing competitive landscape.

Improving Quality and Variety of Substitutes

The threat of substitutes for Fonterra is intensifying as plant-based alternatives rapidly improve. These alternatives are not only matching dairy in taste and texture but also enhancing their nutritional content, making them a more compelling choice for consumers. For instance, the global plant-based dairy market was valued at approximately USD 20.5 billion in 2023 and is projected to grow significantly, demonstrating a clear shift in consumer preference and a stronger competitive threat.

Health and Dietary Trends

The rise of health and dietary trends presents a significant threat of substitutes for Fonterra. Growing consumer awareness around lactose intolerance, dairy allergies, and the perceived health advantages of plant-based eating is driving a noticeable shift away from traditional dairy products. This trend is further amplified by the increasing popularity of vegan and flexitarian lifestyles, which actively encourage the adoption of dairy alternatives.

Environmental and Ethical Considerations

Growing concerns over the environmental footprint of traditional dairy farming, including significant greenhouse gas emissions and substantial water consumption, are pushing consumers towards plant-based alternatives. For instance, dairy farming accounts for roughly 3% of global anthropogenic greenhouse gas emissions, according to the UN's Food and Agriculture Organization.

These environmental and ethical considerations directly impact purchasing behavior, especially for a growing segment of consumers who prioritize sustainability and animal welfare. This trend is evident in the expanding market for dairy-free products.

- Environmental Impact: Dairy farming contributes to methane emissions and land/water use, prompting shifts to lower-impact alternatives.

- Animal Welfare: Ethical concerns regarding animal treatment in conventional dairy operations encourage consumers to seek plant-based options.

- Consumer Preferences: A rising number of consumers, particularly younger demographics, are actively choosing products aligned with their environmental and ethical values.

- Market Growth: The global plant-based milk market, a key substitute for traditional dairy, was valued at over USD 14 billion in 2023 and is projected to grow significantly.

Fonterra's Focus on Dairy's Unique Value

Fonterra acknowledges the increasing presence of substitute products, such as plant-based alternatives. However, their strategic approach centers on reinforcing the inherent value of New Zealand dairy, highlighting its distinct nutritional profile and broad applications.

The co-operative's primary objective is to elevate its dairy offerings through differentiation, rather than engaging in direct competition with the burgeoning plant-based sector. This strategy leverages the established trust and quality associated with Fonterra's dairy products.

In 2024, Fonterra continued to invest in research and development to underscore the superior nutritional content of dairy, particularly its protein and calcium levels, which are often cited as key advantages over many plant-based options. For instance, a typical glass of milk provides a significant portion of the daily recommended intake for several essential nutrients.

- Nutritional Superiority: Dairy milk remains a rich source of complete protein, essential vitamins like B12 and D, and minerals such as calcium, often exceeding the nutritional density of many plant-based alternatives.

- Versatility in Culinary Applications: Dairy products are integral to a vast array of culinary traditions and food manufacturing processes, offering functional properties like emulsification and texture that are difficult to replicate.

- Brand Trust and Heritage: Fonterra benefits from decades of established brand recognition and consumer trust in the quality and safety of its dairy products, a significant barrier for newer substitute categories.

- Focus on Value-Added Products: The company is increasingly focusing on developing specialized dairy ingredients and consumer products that offer enhanced nutritional benefits or unique functional properties, thereby commanding premium pricing.

Dairy Faces $20.1 Billion Plant-Based Market Challenge

The threat of substitutes for Fonterra is significant, primarily driven by the growing popularity of plant-based alternatives like oat, almond, and soy milk. These substitutes are appealing due to perceived health benefits, ethical considerations, and environmental impact. The global plant-based milk market was valued at approximately $20.1 billion in 2023, highlighting a substantial and expanding competitive landscape that directly challenges traditional dairy consumption.

| Substitute Category | Market Value (USD Billion) - 2023 (Approx.) | Projected Growth (CAGR) | Key Drivers |

|---|---|---|---|

| Plant-Based Milk | 20.1 | 10-15% (2024-2030) | Health, Ethics, Environment |

| Dairy-Free Yogurts & Cheeses | 5.5 | 8-12% (2024-2030) | Dietary Needs, Lifestyle Trends |

Entrants Threaten

High Capital Investment Requirement

Entering the global dairy processing and distribution arena, especially at a scale that could rival Fonterra, demands a staggering amount of capital. We're talking about billions of dollars needed for state-of-the-art processing facilities, extensive cold chain logistics, and sophisticated distribution networks. For instance, establishing a new, fully integrated dairy processing plant can easily cost hundreds of millions of dollars, making it a significant hurdle for newcomers.

Difficult Access to Raw Milk Supply

The threat of new entrants in the dairy industry, particularly concerning raw milk supply, is significantly low for Fonterra. In New Zealand, Fonterra's cooperative structure and its extensive network for milk collection create substantial barriers. Farmers are deeply embedded within this system, making it difficult for new players to establish reliable access to the primary input.

Securing a consistent and adequate volume of raw milk is a major hurdle for any potential competitor. Fonterra's established relationships and the logistical infrastructure it commands mean that new entrants would face considerable challenges in replicating this essential supply chain. For instance, in the 2023 financial year, Fonterra collected approximately 21.7 billion litres of milk, underscoring its scale and market dominance which new entrants must contend with.

Economies of Scale and Cost Advantages

Fonterra Co-operative Group benefits from substantial economies of scale in its integrated operations, from sourcing milk to its extensive global distribution network. These efficiencies allow Fonterra to achieve cost advantages that make it difficult for smaller, new entrants to compete on price and profitability.

Established Brands and Distribution Networks

Fonterra's established brands and extensive distribution networks represent a significant barrier to entry for new competitors. Building this level of global reach, spanning over 100 countries, requires immense investment in time, capital, and specialized market knowledge. New entrants would struggle to replicate Fonterra's deep market penetration and brand loyalty, which have been cultivated over decades.

Consider these points regarding Fonterra's competitive advantages:

- Brand Equity: Fonterra's portfolio of well-recognized brands, such as Anchor and Mainland, have strong consumer trust and loyalty, making it difficult for new brands to gain traction.

- Distribution Dominance: The co-operative's established relationships with retailers and its sophisticated logistics infrastructure across numerous international markets provide a substantial hurdle for any new player attempting to access consumers efficiently.

- Market Penetration: Fonterra's deep roots in key dairy markets, often built over many years, mean they have a significant share and understanding of consumer preferences and purchasing habits that newcomers would find challenging to match.

Stringent Regulatory and Food Safety Standards

The dairy industry is heavily regulated, with stringent food safety, quality, and environmental standards worldwide. For example, the US Food and Drug Administration (FDA) mandates strict pasteurization requirements and pathogen testing. Navigating these complex and often differing international regulations significantly increases compliance costs for any new player.

These high compliance hurdles act as a substantial barrier to entry. New companies must invest heavily in meeting these standards, which can be prohibitive. In 2024, the global food safety testing market, a key component of regulatory compliance, was valued at approximately $21.5 billion, indicating the significant financial commitment required.

- High Compliance Costs: New entrants must invest in systems and processes to meet global food safety and quality regulations.

- Regulatory Complexity: Navigating diverse and evolving international regulatory frameworks presents a significant challenge.

- Investment in Infrastructure: Meeting standards often requires substantial upfront investment in specialized facilities and technology.

- Market Access Hurdles: Non-compliance can result in denied market access, further deterring potential new entrants.

Dairy Market Entry: A Formidable Challenge

The threat of new entrants for Fonterra is generally low due to immense capital requirements for facilities and logistics, estimated in the hundreds of millions for a single plant. Fonterra's established milk supply network and cooperative structure create significant barriers, making it difficult for newcomers to secure raw milk. Furthermore, its strong brand equity and extensive global distribution channels, reaching over 100 countries, demand decades of investment and market knowledge to replicate.

Regulatory compliance, including stringent food safety standards like those from the FDA, adds substantial costs, estimated to be a significant portion of the $21.5 billion global food safety testing market in 2024. These combined factors create formidable challenges for any potential new competitor aiming to enter Fonterra's operational space.

| Barrier Type | Description | Impact on New Entrants | Fonterra's Advantage |

|---|---|---|---|

| Capital Intensity | High cost of processing plants and logistics | Prohibitive upfront investment | Economies of scale, established infrastructure |

| Raw Material Access | Securing reliable milk supply | Difficulty replicating Fonterra's network | Dominant milk collection infrastructure |

| Brand & Distribution | Building brand loyalty and global reach | Challenging to match market penetration | Decades of brand building and distribution networks |

| Regulatory Compliance | Meeting global food safety standards | Significant investment and complexity | Established compliance systems and expertise |

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis for Fonterra Co-operative Group is built upon a robust foundation of data, including Fonterra's annual reports, investor presentations, and publicly available financial statements. We also incorporate insights from industry-specific market research reports, agricultural economic databases, and global dairy trade publications to provide a comprehensive view of the competitive landscape.