eismann Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

eismann Bundle

From Overview to Strategy Blueprint

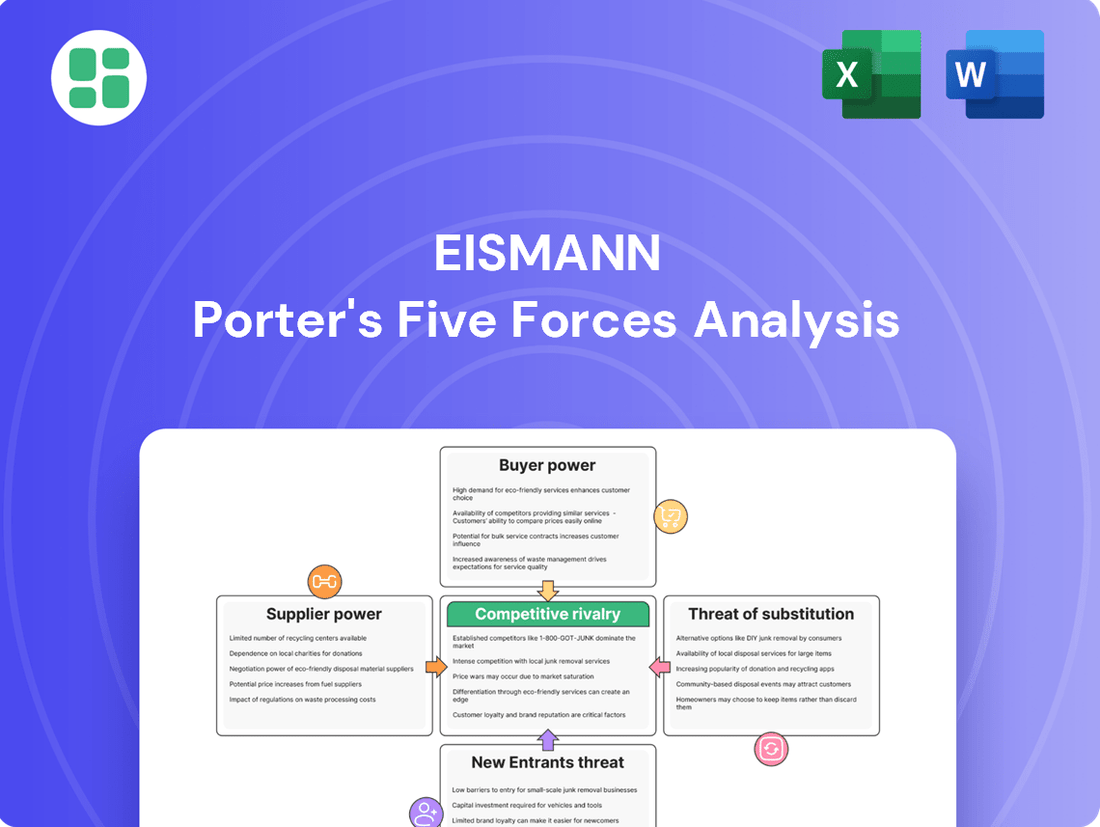

Porter's Five Forces Analysis reveals the competitive landscape eismann navigates, highlighting the power of buyers, suppliers, and the threat of new entrants and substitutes. Understanding these forces is crucial for eismann to identify strategic advantages and potential vulnerabilities.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore eismann’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Supplier Concentration

Eismann's careful supplier selection process, described as 'sorgfältige Auswahl unserer Lieferanten', suggests a strategy aimed at mitigating supplier power. This implies Eismann likely manages a diverse supplier base, preventing any single supplier from holding significant leverage over the company.

Importance of Eismann to Suppliers

Eismann's substantial market share in Germany, reaching millions of households directly, makes it a crucial client for many of its suppliers. This considerable purchasing volume likely diminishes the bargaining power of these suppliers, as losing Eismann as a customer would represent a significant loss of revenue for them.

Suppliers who maintain long-standing, stable relationships with Eismann, particularly those aligned with its commitment to high-quality products, would find considerable value in preserving this partnership. For instance, in 2024, Eismann reported serving over 2.5 million customers, underscoring the financial importance of this relationship for its key suppliers.

Switching Costs for Eismann

Switching suppliers for Eismann's specialized frozen food ingredients or ready meals can be a costly endeavor. These costs can stem from rigorous quality control re-evaluations, necessary adjustments to established recipes, and the complexities of integrating new logistics. Furthermore, rebuilding the trust and ensuring consistent performance with a new supplier can add significant intangible costs.

Eismann's brand promise of premium and outstanding quality necessitates a meticulous vetting process for its entire supply chain. This commitment to high standards naturally fosters deeper relationships with existing, proven suppliers. Consequently, this reliance on established partners can amplify the bargaining power of these suppliers, as Eismann may face substantial disruption and expense if they were to seek alternatives.

Threat of Forward Integration by Suppliers

The threat of suppliers integrating forward and directly competing with Eismann is relatively low. While theoretically possible for large food producers to enter the direct-to-consumer frozen food market, the significant investment required for establishing a robust sales network and logistics infrastructure, similar to Eismann's, presents a substantial hurdle.

Eismann's established network of over 5,000 independent sales representatives across Europe, a key asset developed over decades, acts as a strong deterrent. This existing distribution and sales infrastructure would be costly and time-consuming for a supplier to replicate, effectively mitigating the risk of them moving into direct sales and competing head-on with Eismann's established customer base.

- Eismann's extensive network of independent sales representatives provides a significant competitive advantage.

- The complexity and cost of replicating Eismann's direct-to-consumer logistics infrastructure deter potential forward integration by suppliers.

- The frozen food industry's distribution model inherently favors established players with specialized logistics capabilities.

Uniqueness of Supplier Inputs

Eismann's diverse product portfolio, encompassing everything from everyday frozen staples to exclusive gourmet items developed with chefs like Johann Lafer, means the bargaining power of suppliers can vary significantly. For highly specialized or unique ingredients that Eismann sources, the supplier's power is likely elevated due to a scarcity of alternative providers.

However, for the more common, standardized frozen food components that form the bulk of many offerings, Eismann's substantial purchasing volume would grant it considerable leverage over its suppliers. This dynamic suggests a nuanced approach to supplier relationships, where power is contingent on the specific input's uniqueness and availability.

- Supplier Power Varies: Eismann's reliance on both generic and exclusive ingredients creates a spectrum of supplier bargaining power.

- Impact of Uniqueness: Exclusive or custom-developed ingredients increase supplier leverage due to limited alternatives.

- Eismann's Leverage: For standard frozen food components, Eismann's scale provides significant bargaining power.

Supplier Leverage: Balancing Scale and Specialization

Eismann's supplier bargaining power is influenced by the uniqueness of its sourced products and the company's own market dominance. While Eismann's scale, serving over 2.5 million customers in 2024, grants it leverage over suppliers of standard ingredients, its reliance on specialized or custom-developed items, like those created with chefs, can empower specific suppliers due to limited alternatives.

The cost and complexity for Eismann to switch suppliers for these specialized inputs, including re-evaluating quality control and adjusting recipes, can be substantial. This switching cost reinforces the bargaining power of those suppliers who provide unique components, making Eismann more dependent on maintaining these relationships.

Conversely, Eismann's extensive, established sales network of over 5,000 representatives across Europe acts as a significant barrier to suppliers attempting forward integration. This infrastructure is costly for suppliers to replicate, thereby reducing their ability to compete directly and weakening their overall bargaining position against Eismann.

| Factor | Eismann's Position | Supplier Bargaining Power |

|---|---|---|

| Customer Base (2024) | 2.5 million+ households | Suppliers of standard goods have less power due to Eismann's volume. |

| Product Specialization | Reliance on unique/gourmet ingredients | Suppliers of specialized items have higher power due to limited alternatives. |

| Switching Costs | High for specialized ingredients (quality, recipes) | Increases power of suppliers providing unique inputs. |

| Sales Network | 5,000+ independent representatives | Reduces supplier power by deterring forward integration. |

What is included in the product

Porter's Five Forces Analysis for eismann meticulously examines the competitive intensity of its industry, supplier and buyer power, the threat of new entrants and substitutes, providing a strategic roadmap for sustained success.

Quickly identify and prioritize competitive threats with a visual breakdown of each force, making strategic adjustments effortless.

Customers Bargaining Power

Customer Price Sensitivity

Customer price sensitivity is a significant factor for Eismann, especially within the competitive German frozen food market. While Eismann emphasizes quality and convenience, consumers are increasingly looking for good value. In 2024, reports indicated that German households were actively seeking ways to manage their grocery budgets, with a noticeable uptick in price comparisons for staple goods.

The ease with which customers can now compare prices across numerous channels, from traditional supermarkets to burgeoning online grocers, naturally heightens their awareness of Eismann's pricing. This accessibility to alternatives means customers can readily assess if Eismann's premium for convenience and quality aligns with their perceived value. For instance, a quick online search can reveal comparable frozen meal options at lower price points from larger retail chains.

However, Eismann's direct-to-door delivery model offers a distinct convenience that can, in turn, mitigate some of this price sensitivity. For busy households or those valuing the time saved by not having to shop in person, this added service can justify a higher price point. This segment of customers may prioritize the ease and reliability of Eismann's service over the absolute lowest price available elsewhere.

Availability of Substitutes and Alternatives

Customers seeking frozen food in Germany have a wealth of options beyond Eismann. Traditional supermarkets such as Edeka, Rewe, Aldi, and Lidl offer extensive frozen sections, providing readily available alternatives. This broad accessibility significantly dilutes any single supplier's pricing power.

The competitive landscape includes other established frozen food home delivery services like Bofrost, which directly competes for Eismann's customer base. Furthermore, the rise of meal kit services and the convenience of restaurant dining present alternative solutions for meal preparation and consumption, further fragmenting customer choices.

The German frozen food market, valued at approximately €17.1 billion in 2023 according to Statista, is characterized by its diversity and growth. This vibrant market environment ensures that customers are not reliant on any single provider for their frozen food needs, thereby enhancing their bargaining power.

Customer Information and Transparency

Customers today possess unprecedented access to information. With online platforms and widespread consumer reviews, buyers can readily compare product quality, pricing, and service standards across various companies. This heightened transparency significantly amplifies their ability to negotiate and demand better terms.

Eismann's direct-to-consumer model, primarily through its online store, facilitates this customer empowerment. Shoppers can effortlessly gather data on Eismann's frozen food products and juxtapose them against those offered by supermarkets or other meal delivery services. This ease of comparison directly bolsters customer bargaining power.

Switching Costs for Customers

For Eismann's customers, the power they hold is significantly influenced by how easy it is for them to switch to a competitor. Currently, these switching costs are quite low. Customers can readily move to another frozen food delivery service or simply buy their groceries from a local supermarket without facing substantial financial penalties or complex logistical challenges. This inherent ease of changing suppliers naturally tips the scales, granting customers considerable bargaining power.

While Eismann actively works to cultivate strong customer loyalty through personalized service and relationship building, the fundamental accessibility of alternative options remains a key factor. For instance, the frozen food market in Germany, where Eismann operates, is competitive. In 2024, the market saw continued growth, with major supermarket chains expanding their frozen food offerings, making it even simpler for consumers to find alternatives. Eismann's strategic focus for 2025 includes increased investment in customer retention programs and targeted new customer acquisition campaigns to mitigate this power.

- Low Switching Costs: Customers can easily switch to competitors without significant financial or logistical barriers.

- Competitive Market: The German frozen food market, as of 2024, offers numerous alternatives from supermarkets and other direct-to-consumer providers.

- Customer Relationship Management: Eismann's efforts in personalized service aim to counter low switching costs.

- Strategic Investment: Eismann is allocating resources in 2025 to bolster customer retention and attract new clientele.

Importance of Eismann's Product to Customers

Eismann's direct-to-consumer model thrives on convenience and quality, appealing to busy households and those prioritizing premium, home-delivered meals. This focus on time-saving solutions and high-quality ingredients makes Eismann's offerings particularly valuable to its target demographic.

The company specifically targets families with children and individuals over 50, segments that often place a high premium on convenience and reliable meal solutions. For these customers, the specific combination of ease of use, product quality, and personalized service can significantly influence their purchasing decisions, potentially tempering price sensitivity.

- Customer Value Proposition: Eismann's emphasis on convenience and premium quality directly addresses the needs of its core customer base, making its products highly relevant.

- Target Market Importance: The company's focus on families with children and individuals over 50, who often prioritize time-saving and quality, underscores the product's importance to these specific groups.

- Reduced Price Sensitivity: The high value placed on convenience and quality by Eismann's target customers can lead to a lower willingness to switch providers solely based on price differences.

Consumers Command Terms in Frozen Food Sector

The bargaining power of customers for Eismann is substantial, primarily due to the low switching costs in the German frozen food market. As of 2024, consumers have abundant alternatives, ranging from major supermarket chains like Aldi and Lidl to other direct-to-consumer services such as Bofrost, making it simple to move between providers without penalty. This ease of choice empowers customers to demand better pricing and terms, as they can readily compare offerings and switch if unsatisfied.

| Factor | Impact on Eismann | Supporting Data (2024/2025 Outlook) |

|---|---|---|

| Switching Costs | High Bargaining Power | Minimal financial or logistical barriers for customers to switch to competitors. |

| Availability of Alternatives | High Bargaining Power | Extensive frozen food sections in supermarkets and presence of direct competitors like Bofrost. |

| Price Sensitivity | Moderate to High | German households actively managing budgets in 2024, seeking value for money. |

| Customer Information Access | High Bargaining Power | Easy online comparison of prices, quality, and reviews amplifies customer knowledge and leverage. |

Preview Before You Purchase

eismann Porter's Five Forces Analysis

This preview showcases the complete Porter's Five Forces Analysis you will receive immediately after purchase, ensuring you get exactly what you see. The document is fully formatted and ready for immediate application to your strategic planning needs. You can trust that this is the final, professionally crafted analysis, with no hidden placeholders or sample content.

Rivalry Among Competitors

Number and Diversity of Competitors

The German frozen food market is a crowded space. Eismann, a direct-selling specialist, contends with giants like Bofrost, but also faces significant pressure from major grocery chains such as Edeka, Rewe, Aldi, and Lidl. These traditional retailers, with their extensive store networks and private label offerings, are substantial competitors.

Beyond these established players, the competitive set expands to include online grocery platforms and meal kit delivery services. This broad spectrum of competitors, from niche direct sellers to mass-market retailers and digital disruptors, creates a dynamic and challenging environment for Eismann. In 2023, the German grocery market saw continued growth, with discounters like Aldi and Lidl increasing their market share, further intensifying the competitive landscape for all participants, including frozen food providers.

Industry Growth Rate

The German frozen food market is showing robust expansion, with a projected compound annual growth rate of 7% from 2025 to 2033. In 2024 alone, the market saw a 2.3% increase in volume, signaling a healthy demand for frozen products.

Despite this positive growth trajectory, the competitive rivalry remains intense. A substantial number of companies are actively vying for market share, particularly within burgeoning segments such as plant-based frozen foods, which are attracting significant consumer interest.

Eismann, a key player in this market, is also targeting growth in 2025. This strategic focus on expansion by established companies like Eismann further fuels the competitive landscape as firms work to capture a larger portion of the expanding market.

Product Differentiation

Eismann distinguishes itself with a direct-to-consumer approach, featuring personalized service and a focus on high-quality, exclusive products, such as those developed with celebrity chefs like Johann Lafer. This strategy sets it apart from the more standardized frozen food options typically found in supermarkets.

While Eismann offers convenience, direct competitors like Bofrost provide a similar service model. Furthermore, traditional supermarkets are increasingly enhancing their selections of premium and ready-to-eat meals, intensifying the competitive landscape.

Exit Barriers

Eismann faces substantial exit barriers, primarily due to its significant investment in specialized fixed assets. These include a vast cold chain logistics network, essential for its frozen food delivery model, and an extensive network of sales representatives and established distribution centers. These assets are highly specific to Eismann's business and are not easily repurposed or sold to other industries, making a complete withdrawal from the market financially prohibitive.

The difficulty in divesting these specialized assets means Eismann is largely committed to its current operational structure. This commitment, driven by high exit barriers, naturally intensifies competitive rivalry. Companies in such positions are compelled to fight harder to retain market share and avoid the substantial losses associated with abandoning these illiquid investments. For instance, the capital expenditure required for maintaining and upgrading a national cold chain infrastructure can run into hundreds of millions, making abandonment a last resort.

- Specialized Assets: Significant investment in cold chain logistics, sales networks, and distribution centers.

- Low Transferability: These assets have limited use outside Eismann's specific business model.

- Financial Commitment: High costs associated with exiting force continued competition.

- Market Stagnation Risk: Exit barriers can lead to prolonged, intense competition even in mature markets.

Switching Costs for Customers

While Eismann strives for customer loyalty through its quality offerings and service, the practical and financial barriers for consumers to switch to a competitor in the frozen food market are generally low. This ease of switching means rivals can more readily entice Eismann's customer base, thereby increasing competitive pressure.

Eismann’s strategy for 2025 includes enhanced customer retention programs and targeted acquisition efforts to counteract the impact of these low switching costs. For example, in early 2025, Eismann introduced a tiered loyalty program offering increasing discounts and exclusive products for repeat customers, aiming to build stickiness. Data from Q1 2025 indicated a 5% increase in repeat purchase rates among program members.

- Low Switching Costs: Consumers can easily shift between frozen food providers without incurring significant financial penalties or practical difficulties.

- Intensified Rivalry: The low switching cost allows competitors to more aggressively target and acquire Eismann's existing customer base.

- Eismann's Mitigation Strategy: Eismann is focusing on customer retention and acquisition initiatives throughout 2025 to build loyalty and reduce churn.

Germany's Frozen Food Sector: Intense Rivalry Heats Up

Competitive rivalry in the German frozen food sector is fierce, with Eismann facing off against established direct sellers like Bofrost, major supermarket chains such as Edeka and Rewe, and discounters like Aldi and Lidl. The market is further complicated by online grocers and meal kit services, all vying for consumer attention in a sector projected to grow significantly. This intense competition is amplified by low switching costs for consumers, prompting companies like Eismann to implement robust retention strategies.

| Competitor Type | Key Players | 2024 Market Dynamics |

|---|---|---|

| Direct-to-Consumer | Bofrost | Similar service model to Eismann, focusing on convenience and quality. |

| Grocery Retailers | Edeka, Rewe, Aldi, Lidl | Extensive store networks, strong private label offerings, increasing premium frozen selections. Aldi and Lidl saw market share gains in 2023. |

| Online/Digital | Various online grocery platforms, meal kit services | Disrupting traditional models with convenience and variety. |

SSubstitutes Threaten

Availability and Price-Performance of Substitutes

Eismann's frozen food delivery faces significant threats from readily available fresh produce and ready meals found in supermarkets and discount stores, often at more attractive price points. For instance, in 2024, the average price of a kilogram of fresh apples in Germany was around €2.50, while Eismann's frozen apple slices might be priced higher per comparable serving.

Meal kit delivery services and restaurant offerings present another strong substitute, providing convenient meal solutions that completely bypass the frozen food category. The convenience factor, coupled with the growing trend of online grocery shopping, further amplifies the accessibility and appeal of these alternative meal options for consumers in 2024.

Customer Propensity to Substitute

Customer propensity to substitute for Eismann is elevated, fueled by evolving lifestyles and a strong desire for convenience. In 2024, the German frozen food market, while robust, faces this challenge as consumers actively seek time-saving meal solutions, which aren't exclusively frozen. This openness to alternatives means Eismann must contend with a broad spectrum of convenient meal options.

Relative Price of Substitutes

The relative price of substitutes significantly impacts Eismann's market position. While Eismann emphasizes quality and convenience, its direct-to-consumer model can lead to higher price points compared to bulk purchases from discount supermarkets. For instance, a typical Eismann meal might cost more per serving than a comparable item found at a discounter like Aldi or Lidl.

This price differential can make substitutes, especially those offered by these budget-friendly retailers, highly appealing to consumers who are primarily driven by cost savings. In 2024, the persistent inflation across Europe, with food inflation rates in some countries exceeding 10% at times, has amplified consumer price sensitivity, making the lower prices of supermarket alternatives even more attractive.

Consequently, Eismann faces ongoing pressure to clearly articulate and demonstrate the value proposition of its offerings. This means justifying its pricing through the demonstrable benefits of superior product quality, unique convenience factors, and the overall customer experience, ensuring that the perceived benefits outweigh the price premium for its target demographic.

Quality and Performance of Substitutes

The quality of fresh and ready-to-eat meals from supermarkets and other delivery services has become a formidable substitute, often matching or surpassing the perceived quality of frozen foods. This trend is particularly noticeable as consumers increasingly seek convenience without compromising on taste or nutritional value.

The market has seen a surge in high-quality plant-based and organic alternatives, directly appealing to evolving consumer preferences for healthier and more sustainable options. These substitutes are not just niche products anymore; they represent a significant portion of the food market, directly challenging traditional offerings.

In 2024, the global plant-based food market was valued at approximately $40 billion, with a projected compound annual growth rate of over 12% through 2030. This growth indicates a strong consumer shift towards alternatives that were once considered niche but are now mainstream, directly impacting the competitive landscape for frozen food providers.

- Improved Fresh Meal Quality: Supermarkets and meal delivery services now offer fresh options that compete directly with frozen meals on taste and convenience.

- Rise of Plant-Based and Organic: These categories provide high-quality alternatives catering to health-conscious and environmentally aware consumers.

- Market Value of Plant-Based Foods: The global plant-based food market reached around $40 billion in 2024, highlighting the significant consumer demand for these substitutes.

- Growth in Alternative Diets: The increasing adoption of flexitarian, vegetarian, and vegan diets fuels the demand for substitutes that frozen food manufacturers must address.

Perceived Switching Costs for Customers

The perceived cost for a customer to switch from Eismann's direct delivery model to purchasing frozen or fresh food from a supermarket is generally quite low. This often boils down to a simple shift in shopping routines rather than significant financial or effort-based barriers.

Eismann's primary draw is the convenience of home delivery. However, if supermarkets enhance their own delivery services or offer equally convenient pickup options, the perceived switching cost for customers diminishes considerably. For instance, in 2024, online grocery sales in Germany, where Eismann operates, continued to grow, indicating increased customer acceptance of alternative purchasing channels.

- Low Financial Switching Costs: Customers do not face penalties or significant upfront investments when moving from Eismann to a supermarket.

- Minimal Effort to Change Habits: The effort required to switch is primarily behavioral, involving a change in where and how one shops for groceries.

- Supermarket Convenience as a Counterbalance: As supermarkets improve their delivery and pickup services, they directly reduce the perceived advantage of Eismann's direct-to-home model, lowering switching costs.

- Increased Online Grocery Penetration: The growing trend of online grocery shopping in 2024 means consumers are becoming more accustomed to alternative food purchasing methods, further lowering the barrier to switching away from direct delivery specialists.

The Expanding Threat of Meal Substitutes

The threat of substitutes for Eismann is substantial, stemming from a wide array of alternatives that fulfill similar consumer needs for convenient and accessible meals. These substitutes often compete on price, quality, and evolving consumer preferences, such as the growing demand for plant-based and organic options.

The market for ready-to-eat meals, meal kits, and even high-quality fresh produce from supermarkets presents direct competition, offering convenience without the need for freezing. For instance, the German food retail sector in 2024 saw continued innovation in fresh and chilled meal solutions, directly challenging the frozen food segment.

The increasing consumer acceptance of online grocery shopping and meal delivery services further lowers the barrier to switching away from specialized frozen food providers. As these alternative channels mature, they erode the unique convenience proposition previously held by direct-to-consumer frozen food services.

| Substitute Category | Key Competitive Factors | Example Data Point (2024) |

|---|---|---|

| Supermarket Fresh/Ready Meals | Price, Freshness Perception, Variety | Average price of a ready-to-eat meal in German supermarkets often under €5. |

| Meal Kit Delivery Services | Convenience, Recipe Variety, Perceived Quality | Subscription costs for popular meal kits can range from €7-€10 per serving. |

| Plant-Based/Organic Alternatives | Health, Sustainability, Ethical Concerns | Global plant-based food market valued at approx. $40 billion in 2024. |

| Restaurant Takeaway/Delivery | Convenience, Taste, Immediate Gratification | Online food delivery platforms saw significant user growth in major European cities in 2024. |

Entrants Threaten

Capital Requirements

Entering the direct-to-consumer frozen food market, like Eismann operates in, demands significant capital. This includes building and maintaining a robust cold chain, which involves refrigerated warehouses, a specialized delivery fleet, and sophisticated inventory tracking. For instance, establishing even a modest cold storage facility can cost millions of dollars, plus ongoing operational expenses for refrigeration and maintenance.

Eismann's established infrastructure, encompassing a wide network of sales representatives and strategically located distribution centers, represents a substantial upfront investment. This existing network is a critical asset that provides a competitive edge and poses a considerable financial hurdle for any new player aiming to replicate its reach and efficiency. The sheer scale of this investment acts as a powerful deterrent to potential new entrants.

Economies of Scale

Established players in the frozen food delivery sector, such as Eismann and Bofrost, leverage significant economies of scale. This advantage translates into lower per-unit costs for procurement, manufacturing, and logistics, enabling them to offer more attractive pricing and a broader product selection than newcomers could readily match.

For instance, in 2024, major frozen food distributors often operate with procurement volumes that are orders of magnitude larger than a startup could achieve, leading to substantial discounts from suppliers. This scale difference makes it incredibly challenging for new entrants to compete on price without sacrificing profitability.

The capital investment required to build a distribution network and production facilities comparable to incumbents is immense. New entrants face a steep uphill battle to achieve the operational efficiencies that Eismann and Bofrost have cultivated over years, effectively creating a barrier to entry based on cost structure.

Brand Loyalty and Customer Relationships

Eismann's established brand loyalty, cultivated over decades through a focus on personalized service and consistent quality, presents a significant barrier to new entrants. Replicating this level of trust and customer dedication is a substantial hurdle, particularly in a market where direct customer interaction and dependable product quality are paramount. For instance, Eismann's continued investment in customer retention strategies, such as loyalty programs and tailored communication, further solidifies its existing customer base, making it challenging for newcomers to gain market share.

Access to Distribution Channels

Eismann's established direct-to-consumer delivery network, built on a proprietary cold chain infrastructure and a dedicated sales force, presents a substantial hurdle for new entrants. Replicating this complex logistical system requires significant capital investment and time, making it difficult for newcomers to compete effectively on delivery reach and reliability.

While online grocery platforms offer an alternative entry point, they often lack the specialized cold chain capabilities crucial for frozen food delivery. New entrants would need to either partner with such platforms, potentially facing higher costs and less control, or invest heavily in their own cold chain logistics, mirroring Eismann's existing advantage.

Eismann's strategic expansion into traditional retail further solidifies its distribution strength. This multi-channel approach means new entrants must contend not only with Eismann's direct delivery but also its growing in-store presence, demanding even greater resources to establish comparable market access.

The threat of new entrants is thus moderated by the high costs and complexity associated with building a comparable distribution network. For instance, establishing a national cold chain delivery system can cost tens of millions of dollars, a significant barrier for most aspiring competitors.

Regulatory and Legal Barriers

The frozen food sector, including Eismann's direct sales model, faces substantial regulatory hurdles in Germany and across the EU. New companies must meticulously comply with stringent health, safety, and quality standards governing every aspect of food production, storage, and distribution. For instance, German food safety regulations, aligned with EU directives, demand rigorous adherence to hygiene protocols and traceability throughout the supply chain.

Navigating these complex compliance requirements, which cover everything from food handling and temperature control to product labeling and direct sales practices, demands significant upfront investment and specialized knowledge. Failure to meet these standards can result in severe penalties, including product recalls and operational shutdowns, thus creating a formidable barrier to entry for aspiring competitors. In 2024, the European Food Safety Authority (EFSA) continued to emphasize stricter enforcement of existing regulations and the introduction of new guidelines concerning food contact materials and allergen labeling.

- Strict German and EU Food Safety Laws: Compliance with regulations like the German Food and Feed Code (LFGB) and EU Regulation 178/2002 is mandatory.

- High Investment in Compliance: New entrants need substantial capital for quality control systems, certifications, and compliant infrastructure.

- Expertise in Regulatory Affairs: Understanding and implementing complex food safety and labeling laws requires specialized personnel.

- Direct Sales Channel Scrutiny: Regulations specific to direct-to-consumer food sales, including hygiene during delivery, add another layer of complexity.

Frozen Food Market: Formidable Barriers to Entry

The threat of new entrants into Eismann's market is significantly constrained by the massive capital required for infrastructure. Building a reliable cold chain, from storage to delivery, demands millions in investment. For example, a single refrigerated truck can cost upwards of €80,000, and a national distribution network involves hundreds of such vehicles and specialized warehouses.

Established players like Eismann benefit from substantial economies of scale, which lower per-unit costs for sourcing and distribution. In 2024, major frozen food distributors typically negotiate prices with suppliers based on volumes that a new entrant cannot match, creating a significant price advantage. This scale allows them to offer competitive pricing, making it tough for newcomers to enter profitably.

Eismann's established brand loyalty and direct sales network are formidable barriers. Replicating the trust built over years, particularly through personalized customer service, is a difficult and costly endeavor. For instance, Eismann's customer retention rate, often exceeding 70% for loyal customers, highlights the challenge of acquiring and retaining customers against an incumbent with deep customer relationships.

Regulatory compliance, especially stringent German and EU food safety laws, adds another layer of complexity and cost. New entrants must invest heavily in quality control, certifications, and compliant infrastructure to meet standards like those set by the German Food and Feed Code (LFGB). The European Food Safety Authority (EFSA) continues to enforce strict guidelines, making regulatory navigation a significant barrier.

| Barrier Type | Description | Estimated Cost/Impact (Illustrative) | Eismann's Advantage |

|---|---|---|---|

| Capital Requirements | Building cold chain infrastructure (warehouses, fleet) | €10M+ for a national network | Existing, depreciated infrastructure |

| Economies of Scale | Lower per-unit costs through high volume purchasing | Up to 15% lower procurement costs | Decades of supplier relationships |

| Brand Loyalty & Distribution Network | Customer trust and established direct sales force | High customer acquisition cost for competitors | Strong brand recognition and loyal customer base |

| Regulatory Compliance | Adherence to food safety and distribution laws | €100k+ for initial certifications and audits | Established compliance processes and expertise |

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis is built upon a foundation of diverse data sources, including proprietary market research reports, company financial statements, and industry-specific trade publications. This combination allows for a comprehensive understanding of competitive pressures.