CrossFirst Bankshares Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

CrossFirst Bankshares Bundle

Don't Miss the Bigger Picture

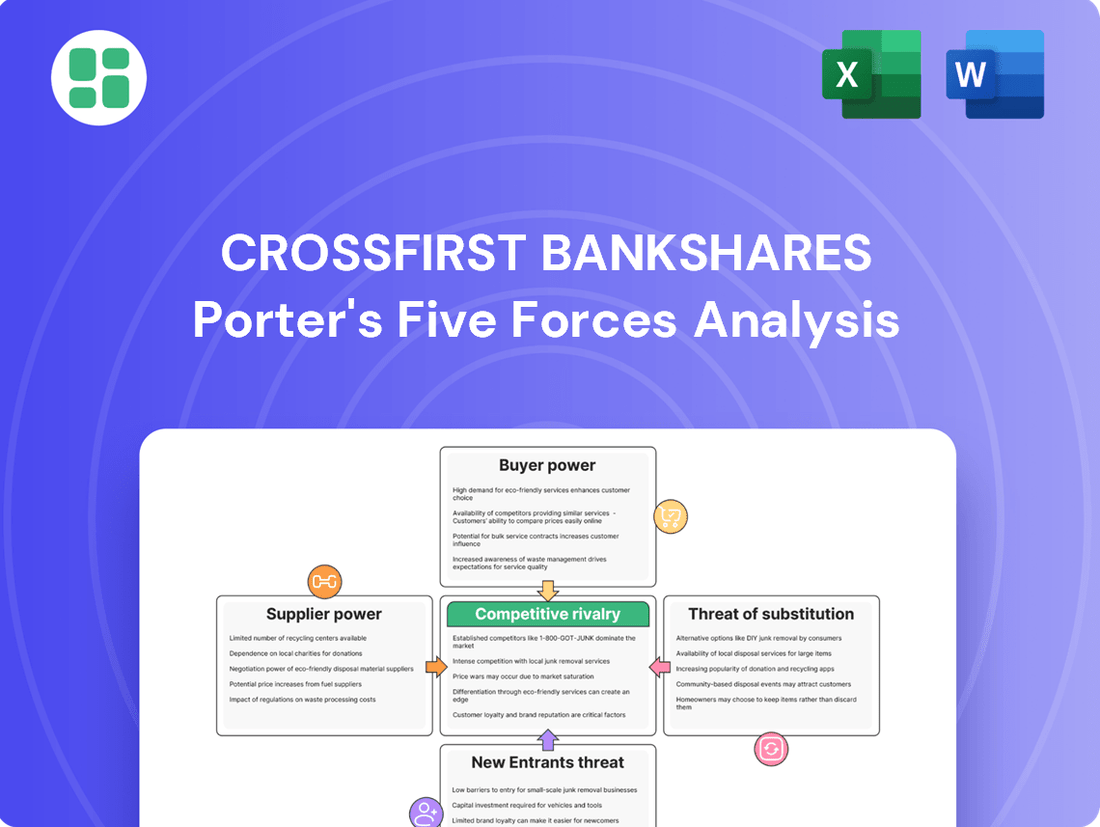

CrossFirst Bankshares faces moderate competitive rivalry, with a limited number of large, established banks and a growing number of community banks vying for market share. The threat of new entrants is relatively low due to significant capital requirements and regulatory hurdles. Buyer power is moderate, as customers can switch banks, but loyalty and specialized services can mitigate this.

The complete report reveals the real forces shaping CrossFirst Bankshares’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Concentration of Key Suppliers

The banking sector, including institutions like CrossFirst Bankshares, often depends on a relatively small number of specialized technology providers for critical functions such as core banking software, robust cybersecurity, and the underlying digital infrastructure. This concentration means these suppliers hold significant sway.

For a regional bank such as CrossFirst, this can translate into a disadvantage during negotiations. Unlike larger, national banks that might have greater purchasing power or the ability to develop in-house solutions, CrossFirst may face less favorable pricing or more rigid contract terms from these essential tech vendors. For instance, in 2024, the average cost for core banking system implementation and ongoing support can range from hundreds of thousands to millions of dollars, and a concentrated supplier market can inflate these figures.

Availability of Capital (Depositors)

Depositors are essentially the suppliers of capital for banks like CrossFirst Bankshares. While most individual savers don't wield much influence, large corporate clients and wealthy individuals who deposit substantial sums can exert considerable bargaining power. This is because the sheer volume of funds they control gives them leverage to demand better terms.

The competition for these crucial deposits can be fierce, especially for regional banks. In 2024, for instance, banks were actively competing for deposits, leading to upward pressure on the interest rates they offered. This dynamic means that CrossFirst, like its peers, might face higher costs to attract and retain these vital capital sources, particularly as interest rates fluctuate.

Talent Pool Scarcity

The scarcity of skilled financial professionals, especially in niche areas like wealth management, commercial lending, and financial technology, can significantly amplify the bargaining power of employees. For regional banks such as CrossFirst Bankshares, this often translates into increased competition for top talent.

Larger, more established financial institutions or nimble fintech companies can often offer more attractive compensation packages and career advancement opportunities, making it difficult for regional players to attract and retain the best individuals. This talent gap can consequently drive up labor costs and impact operational efficiency for CrossFirst.

Regulatory and Compliance Burdens

While not direct suppliers in the traditional sense, regulatory bodies significantly influence the banking sector. For CrossFirst Bankshares, compliance with evolving rules, such as those concerning cybersecurity and capital adequacy, adds substantial operational costs. These increasing demands effectively raise the "price" of operating within the financial industry, impacting profitability and strategic flexibility.

The banking industry in 2024 continued to grapple with a dynamic regulatory landscape. For instance, the Federal Reserve's ongoing adjustments to capital requirements, influenced by broader economic conditions and global financial stability concerns, directly affect how banks like CrossFirst Bankshares must manage their balance sheets. These requirements often necessitate holding more capital, which can reduce lending capacity and increase the cost of capital.

- Increased Compliance Costs: Banks face mounting expenses related to adhering to new and updated regulations, including investments in technology and personnel for compliance.

- Operational Adjustments: Evolving rules often require significant changes to internal processes and risk management frameworks, adding complexity and cost.

- Capital Requirements: Stricter capital adequacy ratios, such as those reinforced by Basel III Endgame proposals, mean banks must hold more capital against their assets, impacting return on equity.

Switching Costs for Banks

Banks face significant hurdles when considering a change in their core technology providers or major service vendors. These challenges include complex integration processes, the intricate task of migrating vast amounts of data, and the necessity for extensive staff training. These factors collectively create high switching costs.

The elevated switching costs directly bolster the bargaining power of incumbent suppliers. This means that for a bank like CrossFirst, it becomes considerably more difficult and expensive to transition away from an existing vendor, even when faced with less favorable contract terms or pricing. This situation can limit a bank's flexibility in vendor management.

- High Integration Complexity: Core banking systems often involve numerous interconnected modules, making seamless integration with new vendors a substantial undertaking.

- Data Migration Risks: Transferring sensitive customer and transactional data requires meticulous planning and execution to prevent loss or corruption, a process that can take months.

- Training and Adoption Costs: Employees need to be retrained on new platforms, incurring significant time and resource expenditures.

Bank Suppliers: Who Holds the Power?

The bargaining power of suppliers for banks like CrossFirst Bankshares is influenced by several factors, including the concentration of specialized technology providers and the cost of switching vendors. Additionally, the availability and cost of essential inputs like capital (deposits) and skilled labor play a crucial role in shaping supplier leverage.

For CrossFirst, the reliance on a few key technology vendors for core banking systems and cybersecurity means these suppliers can dictate terms, especially given the high costs and complexity associated with switching providers. This was evident in 2024, where specialized IT services for financial institutions saw continued demand, potentially increasing vendor pricing power.

Depositors, particularly large corporate clients, represent a significant supplier of capital. Their ability to move substantial funds can force banks to offer competitive interest rates, a dynamic that intensified in 2024 as banks vied for stable funding sources amidst economic uncertainty.

| Factor | Impact on CrossFirst Bankshares | 2024 Trend/Data Point |

|---|---|---|

| Technology Vendors | High bargaining power due to specialized services and high switching costs. | Continued strong demand for cloud-based core banking solutions and advanced cybersecurity. |

| Depositors (Large Clients) | Moderate to high bargaining power, influencing deposit rates. | Increased competition for large deposits, with some institutions offering tiered rates based on balance size. |

| Skilled Labor | Moderate bargaining power, driving up talent acquisition costs. | Shortage of experienced professionals in areas like digital banking and compliance. |

What is included in the product

This analysis of CrossFirst Bankshares examines the intensity of rivalry, the bargaining power of customers and suppliers, the threat of new entrants, and the availability of substitutes within the banking sector.

Instantly identify and address competitive threats with a dynamic Porter's Five Forces analysis, allowing CrossFirst Bankshares to proactively mitigate market pressures.

Customers Bargaining Power

Customer Segmentation and Volume

CrossFirst Bankshares caters to a broad range of clients, from everyday individuals to substantial businesses and high-net-worth individuals. The bargaining power of customers is heavily influenced by their size and the volume of business they bring to the bank.

While individual retail customers typically have minimal leverage due to the relatively small scale of their transactions, larger commercial clients and private banking customers represent a significant source of revenue. These key accounts can negotiate for better interest rates, reduced service charges, or customized banking solutions, directly affecting CrossFirst Bankshares' margins on these relationships.

Low Switching Costs for Retail Customers

While many customers perceive switching banks as a hassle, this barrier is diminishing. In fact, a significant portion of consumers, nearly 20%, are expected to switch financial institutions in 2025, with younger demographics leading this trend.

The rise of digital banking makes opening and managing accounts incredibly simple. This ease of access empowers individual customers to readily move to competitors offering more attractive interest rates or a better digital experience, thereby increasing their bargaining power.

Access to Information and Digital Tools

Customers today possess an unprecedented ability to access information about banking products, interest rates, and fees. Online comparison tools and financial aggregators have democratized this data, making it readily available. This transparency significantly bolsters customer bargaining power.

For banks like CrossFirst Bankshares, this means a constant need to remain competitive. They must offer attractive pricing and high-quality service to both win new clients and keep existing ones. In 2024, the average consumer spent over 50 hours researching financial products online before making a decision.

Demand for Personalized and Digital Services

Customers, particularly younger demographics, are increasingly demanding intuitive digital banking experiences and tailored financial products. For instance, a 2024 report indicated that over 70% of Gen Z and Millennial consumers prefer mobile banking for everyday transactions. This shift empowers customers, as they can readily switch to financial institutions offering superior digital capabilities and personalized services, thereby amplifying their bargaining power.

Banks that lag in technological innovation face a significant risk of customer attrition. As of early 2025, data suggests that a substantial portion of customers are willing to switch banks for better digital tools and personalized offers. This heightened customer mobility directly translates to increased bargaining power, forcing financial institutions to compete more aggressively on service quality and digital convenience.

- Digital Preference: Over 70% of Gen Z and Millennials favor mobile banking.

- Customer Mobility: A significant percentage of customers will switch banks for better digital offerings.

- Personalization Demand: Customers expect tailored financial solutions, increasing their leverage.

Impact of Merger on Customer Relationships

The merger of CrossFirst Bankshares with First Busey Corporation, finalized in March 2025, creates a significantly larger financial institution. This consolidation aims to provide customers with a wider array of services and an expanded geographic footprint. However, a key challenge for the combined entity will be to preserve the high-touch, personalized service that was a hallmark of CrossFirst Bank. If this personalized approach is diluted, customers may feel empowered to seek out smaller, more niche financial providers offering tailored experiences.

The increased scale from the merger could potentially lead to less individualized attention for customers. For instance, if customer service interactions shift towards more standardized, less personal channels, it could weaken existing relationships. This shift might prompt customers, particularly those valuing direct relationships with their bankers, to explore alternatives that better cater to their specific needs and preferences.

- Increased Scale: The merger combines the strengths of two entities, potentially offering a broader product suite.

- Personalization Challenge: Maintaining the personalized service CrossFirst was known for is crucial post-merger.

- Customer Retention Risk: Dilution of personalized service could drive customers to competitors offering more tailored experiences.

- Market Dynamics: The banking sector in 2025 continues to see a demand for both digital convenience and human connection.

Digital Convenience Fuels Customer Bargaining Power

The bargaining power of CrossFirst Bankshares' customers is amplified by the increasing ease of switching financial institutions and the readily available information on banking products. This trend is particularly pronounced among younger demographics who prioritize digital convenience.

In 2025, an estimated 20% of consumers are expected to switch banks, with digital banking adoption being a key driver. For instance, over 70% of Gen Z and Millennials prefer mobile banking for their transactions, a preference that empowers them to seek out institutions offering superior digital experiences.

| Customer Segment | Bargaining Power Factors | Impact on CrossFirst Bankshares |

|---|---|---|

| Retail Customers | Low individual transaction volume, but collective switching behavior | Price sensitivity, demand for competitive rates and fees |

| Commercial Clients | High transaction volume, potential for customized solutions | Ability to negotiate better terms, impacting net interest margins |

| High-Net-Worth Individuals | Significant assets under management, demand for personalized service | Leverage for premium services, tailored investment advice, and preferential rates |

Preview Before You Purchase

CrossFirst Bankshares Porter's Five Forces Analysis

This preview showcases the comprehensive Porter's Five Forces analysis for CrossFirst Bankshares, detailing the competitive landscape including threats of new entrants, bargaining power of buyers and suppliers, and the intensity of rivalry. The document displayed here is the part of the full version you’ll get—ready for download and use the moment you buy, providing actionable insights into CrossFirst Bankshares' strategic positioning. You can trust that the analysis you see is the exact, professionally crafted document you will receive immediately after purchase, with no alterations or missing sections.

Rivalry Among Competitors

Industry Concentration and Regional Focus

CrossFirst Bankshares operates within a highly competitive regional banking landscape. Intense rivalry stems from large national institutions, other regional banks, and numerous community banks, all vying for market share.

Despite strong recent performance, the banking sector remains fragmented. This fragmentation fuels a fierce competition for essential deposits and robust loan growth opportunities, a key driver of profitability.

For instance, as of the first quarter of 2024, the U.S. banking industry saw an average net interest margin of 3.32%, highlighting the pressure on banks to attract deposits and lend profitably amidst this rivalry.

M&A Activity and Consolidation

Merger and acquisition (M&A) activity in the banking sector has significantly escalated, with deal values tripling in 2024 and projections indicating further acceleration into 2025. This trend is reshaping the competitive landscape, as consolidation efforts aim to achieve greater scale and operational efficiencies.

CrossFirst Bankshares' own merger with First Busey Corporation, finalized in March 2025, exemplifies this industry-wide consolidation. Such strategic combinations intensify competitive pressures on remaining independent regional banks and newly formed entities to successfully integrate operations and achieve anticipated synergies.

Digital Transformation and Technology Investment

Competitive rivalry in banking is intensifying due to technology. Larger institutions are pouring billions into digital platforms, creating a significant hurdle for regional players like CrossFirst Bankshares. For instance, JP Morgan Chase announced a $15 billion technology investment for 2024 alone, aiming to enhance its digital offerings and customer experience.

To stay competitive, CrossFirst must consistently upgrade its technological infrastructure. Failing to do so means risking customer attrition to more digitally advanced banks and nimble fintech startups that are rapidly capturing market share. This necessitates ongoing investment in areas like AI-driven customer service, seamless mobile banking, and robust cybersecurity measures.

Product and Service Differentiation

CrossFirst Bank emphasizes relationship-driven banking, commercial lending, and wealth management to stand out. This approach aims to build strong client connections, a key differentiator in a crowded market.

However, many financial institutions offer similar comprehensive service portfolios. This makes achieving genuine product differentiation difficult, with success often hinging on the quality of client relationships and the overall service experience.

- Relationship Focus: CrossFirst Bank's strategy centers on personalized service and deep client engagement.

- Service Overlap: Competitors frequently offer comparable banking and financial solutions.

- Differentiation Challenge: True product differentiation is tough, making service and relationships paramount.

Interest Rate Environment and Deposit Competition

The interest rate environment is a crucial factor for banks like CrossFirst Bankshares. When rates are rising, as they have been in recent periods, banks must pay more to attract and keep deposits, which directly impacts their net interest income. This dynamic intensifies competition among regional banks, forcing them to offer more attractive rates to secure essential funding.

In 2024, the Federal Reserve's monetary policy continued to influence deposit pricing. For instance, while the Fed held rates steady for much of the year, the lingering effects of prior hikes meant that deposit costs remained elevated. This pressure on margins is a direct consequence of banks needing to compete fiercely for customer deposits, which are the lifeblood of their lending operations.

- Deposit Rate Competition: Banks are actively competing on deposit rates to attract and retain customer funds.

- Impact on Net Interest Income: Fluctuations in interest rates directly affect a bank's profitability by altering the cost of its funding.

- Regional Bank Challenges: Regional banks, in particular, face significant pressure to offer competitive deposit rates to maintain their funding base amidst broader market conditions.

Banking Battleground: Tech, M&A, and Rates Drive Fierce Competition

The competitive rivalry for CrossFirst Bankshares is fierce, driven by a fragmented market of national, regional, and community banks, all battling for deposits and loans. This intense competition is further amplified by significant merger and acquisition activity, with deal values in the banking sector tripling in 2024, creating larger, more formidable competitors.

Technological advancements are a major battleground, with large institutions investing billions, like JP Morgan Chase's $15 billion tech investment in 2024, to enhance digital offerings. CrossFirst must also invest heavily in technology to avoid losing customers to digitally advanced banks and fintechs.

While CrossFirst focuses on relationship banking and personalized service, many competitors offer similar products, making differentiation challenging and service quality the key differentiator.

The current interest rate environment, with elevated deposit costs influenced by Federal Reserve policy throughout 2024, forces banks to compete aggressively on deposit rates, directly impacting net interest margins and profitability.

| Competitor Type | Key Competitive Factor | 2024 Impact/Example |

| National Banks | Scale, Technology Investment | JP Morgan Chase: $15B tech investment |

| Regional Banks | Consolidation, Synergies | Banking M&A deal values tripled in 2024 |

| Community Banks | Local Relationships, Niche Markets | Fragmented market fuels competition |

| Fintech Startups | Digital Agility, Innovation | Capturing market share through advanced platforms |

SSubstitutes Threaten

Fintech Companies and Digital Payment Platforms

Fintech companies and digital payment platforms present a significant threat of substitutes for traditional banks like CrossFirst Bankshares. These innovators offer specialized services such as peer-to-peer lending, streamlined digital payments, and convenient online-only banking, directly challenging established bank products.

The appeal of fintech often lies in their ability to provide lower fees, enhanced user experience, and tailored niche services, drawing customers who might otherwise use conventional banking channels. For instance, the global digital payments market was valued at over $2 trillion in 2023 and is projected to grow substantially, indicating a clear shift in consumer preference towards these digital alternatives.

Alternative Lending and Funding Sources

The threat of substitutes for traditional bank lending is growing, as businesses and individuals can increasingly turn to alternative sources for capital. Platforms like crowdfunding and private equity, along with a surge in non-bank lenders, offer competitive alternatives to traditional loans. This diversification directly challenges the core business model of banks like CrossFirst Bankshares.

Embedded Finance Solutions

The increasing prevalence of embedded finance presents a significant threat of substitutes for traditional banks like CrossFirst Bankshares. Non-financial companies, such as large e-commerce platforms and software providers, are increasingly embedding financial services directly into their customer journeys. This means consumers can access payment processing, lending, or even insurance without needing to engage with a traditional financial institution.

This shift bypasses the need for direct banking relationships, potentially eroding a bank's customer base and traditional revenue streams. For instance, by 2024, projections suggest the embedded finance market could reach trillions of dollars globally, indicating a substantial portion of financial transactions may occur outside of conventional banking channels.

Credit Unions and Community Banks

Credit unions and community banks present a significant threat of substitution for CrossFirst Bankshares. These institutions, while traditional, often compete by offering attractive rates and a more personalized, community-centric approach that resonates with specific local customer bases. Their member-owned or non-profit status can sometimes translate into more favorable terms for their clientele.

For instance, in 2024, credit unions continued to gain market share in certain regions, with total assets for US credit unions reaching approximately $2.1 trillion by the end of the first quarter. This growth indicates their ability to attract and retain customers, potentially drawing them away from larger, publicly traded banks like CrossFirst.

- Competitive Rates: Credit unions and community banks can often offer slightly higher deposit rates and lower loan rates due to their operational structures.

- Personalized Service: A strong emphasis on local relationships and tailored financial advice can be a key differentiator.

- Community Focus: Deep ties within local communities foster loyalty and trust, acting as a barrier for external competitors.

- Member-Owned Advantage: For credit unions, profits are often returned to members in the form of better rates or lower fees.

Cryptocurrency and Digital Assets

The increasing adoption of cryptocurrencies and digital assets, especially among younger consumers, presents a developing threat of substitution for traditional banking functions. As these digital ecosystems mature, they offer alternatives for payments and wealth storage. For instance, reports from 2024 indicate a continued rise in cryptocurrency ownership, with a significant portion of users under 40. This trend suggests a potential shift in how financial transactions and asset management are approached.

This evolving landscape challenges incumbent financial institutions by offering decentralized and potentially more accessible alternatives. While still in its early stages for widespread mainstream use, the underlying technology and growing user base cannot be ignored. By 2025, projections suggest further integration of digital assets into everyday financial activities, necessitating a strategic response from traditional banks.

Key aspects of this threat include:

- Growing Consumer Adoption: Younger demographics are increasingly comfortable with and utilizing digital assets for transactions and savings.

- Development of Ecosystems: The infrastructure supporting cryptocurrencies and digital assets is expanding, offering more robust services.

- Potential for Disintermediation: Digital assets can bypass traditional financial intermediaries, offering direct peer-to-peer transactions.

Traditional Banking Faces Trillion-Dollar Substitutes

The threat of substitutes for traditional banking services is multifaceted, encompassing fintech innovations, alternative lending platforms, embedded finance, credit unions, and the burgeoning digital asset space. These substitutes often appeal to customers through lower costs, enhanced convenience, specialized features, or a more personalized approach.

The increasing integration of financial services into non-financial platforms, known as embedded finance, represents a significant substitution threat. By 2024, this market was projected to reach trillions of dollars globally, indicating a substantial portion of financial transactions could occur outside traditional banking channels, bypassing direct bank relationships.

Cryptocurrencies and digital assets are also emerging as substitutes, particularly for younger demographics, offering alternatives for payments and wealth storage. By 2025, further integration of digital assets into everyday financial activities is anticipated, challenging incumbent institutions with decentralized and accessible options.

| Substitute Category | Key Offerings | Customer Appeal | Market Trend/Data (2023-2024) |

|---|---|---|---|

| Fintech & Digital Payments | P2P lending, digital payments, online-only banking | Lower fees, enhanced UX, niche services | Global digital payments market >$2 trillion (2023) |

| Alternative Lending | Crowdfunding, private equity, non-bank lenders | Access to capital, competitive terms | Growing market share challenging traditional loans |

| Embedded Finance | Financial services within e-commerce/software platforms | Seamless integration, convenience | Projected trillions globally by 2024 |

| Credit Unions & Community Banks | Attractive rates, personalized service | Community focus, member-owned benefits | US credit union assets ~$2.1 trillion (Q1 2024) |

| Cryptocurrencies & Digital Assets | Digital payments, asset storage | Decentralization, accessibility | Continued rise in ownership, especially among <40 demographic |

Entrants Threaten

High Capital Requirements and Regulatory Hurdles

The banking sector presents formidable barriers to entry, primarily due to exceptionally high capital requirements. For instance, in 2024, regulatory bodies like the Federal Reserve mandate significant capital reserves for banks to ensure stability and absorb potential losses. This means a new bank would need hundreds of millions, if not billions, of dollars just to meet initial capitalization standards, a sum few new players can readily access.

Beyond capital, the regulatory landscape is a significant deterrent. Obtaining banking licenses involves rigorous scrutiny and adherence to complex compliance frameworks, including anti-money laundering (AML) and know-your-customer (KYC) regulations. These ongoing compliance costs and the sheer complexity of navigating these rules, which are constantly evolving, make it incredibly challenging for new entrants to compete with established institutions like CrossFirst Bankshares.

Brand Recognition and Trust

Established financial institutions like CrossFirst Bankshares have cultivated significant brand recognition and customer trust over many years. This deep-seated trust is a formidable barrier for newcomers in the banking sector, where reliability and reputation are paramount. For instance, in 2024, the banking industry continued to see a strong preference for established brands, with customer retention rates for major banks remaining robust, often exceeding 90% for those with long-standing relationships.

Economies of Scale and Scope

Existing banks, particularly following consolidation such as CrossFirst Bankshares' merger with First Busey, leverage significant economies of scale. This allows them to spread costs across a larger operational base for technology, marketing, and back-office functions, leading to lower per-unit costs. For instance, in 2023, the banking industry saw continued consolidation, with numerous mergers and acquisitions aimed at achieving greater efficiency and market share.

New entrants face a considerable hurdle in replicating these cost advantages. Without an established customer base or the substantial initial capital required to build comparable infrastructure, new banks find it challenging to compete on price or offer the same breadth of services as incumbents. This barrier is particularly high in a sector where customer loyalty and trust are paramount, and where regulatory compliance demands significant ongoing investment.

Customer Loyalty and Switching Costs

Customer inertia and the perceived hassle of switching banks create some degree of loyalty to existing institutions. For instance, in 2023, the average customer tenure at a primary bank in the US remained significant, with many individuals holding their accounts for over a decade, reflecting this inertia.

New entrants must offer compelling incentives, superior technology, or unique value propositions to overcome these switching costs and attract customers from incumbents. For example, digital-only banks often provide higher interest rates and lower fees, which can be a strong draw for customers looking to optimize their banking experience.

- Customer Inertia: Many customers remain with their current bank due to habit and the perceived effort involved in changing.

- Switching Costs: While not always direct financial penalties, the time and effort to transfer direct deposits, automatic payments, and update account information act as a barrier.

- Competitive Response: New banks must offer a clear advantage, such as innovative mobile banking features or more attractive interest rates, to entice customers to move.

Fintech as a Disruptive Entry Model

Fintech companies represent a significant threat of new entrants, often bypassing the high barriers to entry faced by traditional banks. By focusing on specific services like payments or lending, these digital-first firms can operate with a lighter regulatory load, allowing for quicker market penetration. For instance, in 2024, the global fintech market was projected to reach over $33 trillion, highlighting the scale of this emerging competition.

These agile fintechs can cherry-pick profitable market segments, creating disruption for established institutions like CrossFirst Bankshares. While traditional banks are responding by acquiring or partnering with fintechs, this trend underscores the evolving competitive landscape and the continuous pressure from innovative new players.

- Fintechs target specific banking services, reducing initial regulatory hurdles.

- The global fintech market's substantial growth, projected to exceed $33 trillion in 2024, indicates a robust influx of new competitors.

- Traditional banks are increasingly engaging with fintechs through acquisitions and partnerships to mitigate this threat.

Fintech's Impact on Banking's High Entry Barriers

The threat of new entrants for CrossFirst Bankshares is generally low due to significant barriers. High capital requirements, stringent regulatory approvals, and the need for established trust make it difficult for new banks to emerge and compete effectively.

However, the rise of fintech companies presents a more dynamic challenge. These digital-first entities can bypass some traditional hurdles by focusing on niche services, as seen in the projected over $33 trillion global fintech market in 2024, indicating a growing competitive force.

Established brand loyalty and customer inertia further solidify the position of incumbents like CrossFirst Bankshares, as customers often remain with familiar institutions, making it hard for newcomers to gain traction.

Economies of scale enjoyed by existing banks, amplified by industry consolidation, create cost advantages that new entrants struggle to match without substantial initial investment and customer acquisition.

| Barrier Type | Impact on New Entrants | Example for 2024/2023 |

|---|---|---|

| Capital Requirements | Very High | Millions to billions needed for initial capitalization. |

| Regulation & Compliance | High | Complex licensing, AML/KYC rules require significant resources. |

| Brand Loyalty & Trust | High | Customer tenure often exceeds a decade; preference for established brands. |

| Economies of Scale | High | Consolidation in 2023 created larger, more cost-efficient institutions. |

| Fintech Disruption | Moderate to High | Targeting specific services with lighter regulation; global market >$33T in 2024. |

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis for CrossFirst Bankshares is built upon a foundation of verified data, including their annual reports and SEC filings. We also incorporate insights from industry publications and market research reports to understand competitive dynamics.