Credit Agricole Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Credit Agricole Bundle

A Must-Have Tool for Decision-Makers

Credit Agricole operates within a dynamic banking landscape, facing intense competition and evolving customer expectations. Understanding the interplay of buyer power, supplier leverage, and the threat of new entrants is crucial for its strategic positioning. The threat of substitutes, alongside the intensity of rivalry among existing players, further shapes its competitive environment.

The complete report reveals the real forces shaping Credit Agricole’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Specialized Technology and Software Providers

Crédit Agricole's dependence on specialized technology and software providers is a significant factor in supplier bargaining power. The bank utilizes advanced IT systems for core banking operations, robust cybersecurity measures, and sophisticated data analytics, all of which are critical for its functioning and strategic goals. Suppliers offering highly specialized or proprietary technology can command considerable leverage due to the substantial costs and operational disruptions associated with switching providers, especially as financial technology becomes more intricate.

Financial Market Data and Analytics Providers

Financial market data and analytics providers hold significant bargaining power over Crédit Agricole. Access to real-time financial data, market intelligence, and advanced analytics is fundamental for Crédit Agricole's investment banking, asset management, and risk management operations. Companies like Bloomberg and Refinitiv are key suppliers, offering comprehensive datasets that are critical for informed decision-making.

The power of these data providers is amplified by the proprietary nature of their information and the sheer scale of their data infrastructure, which is incredibly challenging and costly for any single institution to replicate internally. For instance, Bloomberg's terminal, a ubiquitous tool in finance, provides access to a vast array of data and analytics, making it a near-essential service for many financial professionals. Their ability to aggregate, clean, and deliver such extensive data creates a strong dependency for their clients.

Payment Network Operators

Payment network operators like Visa and Mastercard hold considerable sway over Crédit Agricole. These networks are essential for processing retail and corporate transactions, and their ubiquity means banks have few alternatives. In 2023, Visa reported processing over 250 billion transactions globally, highlighting the sheer scale and indispensability of these payment rails.

Human Capital and Expert Consultants

The banking sector, especially in corporate and investment banking, relies heavily on specialized expertise. Finding and keeping top talent in areas like AI, cybersecurity, and regulatory compliance is a significant challenge. This scarcity gives suppliers of high-caliber human capital, such as specialized recruitment firms and consulting groups, considerable bargaining power.

For instance, in 2024, the demand for AI specialists in finance outstripped supply, leading to salary increases of up to 25% for experienced professionals in this field, according to industry reports. Similarly, the need for cybersecurity experts saw a surge in demand, with consulting fees for specialized projects often exceeding $1,000 per hour. This elevates the bargaining power of these human capital suppliers.

- Scarcity of Specialized Skills: Niche areas like AI and cybersecurity in banking face a significant talent gap.

- High Demand for Expertise: Banks actively compete for a limited pool of highly skilled professionals and consultants.

- Supplier Power: Recruitment agencies and consulting firms specializing in these areas leverage the demand to command higher fees.

- Impact on Costs: This dynamic directly influences Credit Agricole's operational costs related to talent acquisition and project outsourcing.

Regulatory Compliance and Legal Services

The bargaining power of suppliers in the financial sector, particularly concerning regulatory compliance and legal services, is significant for institutions like Crédit Agricole. Given the intricate web of national and international financial regulations, specialized legal and compliance expertise is not merely beneficial but essential for operational integrity.

These specialized service providers, including law firms and compliance tech vendors, hold considerable sway due to their unique knowledge base. For instance, the European Union's General Data Protection Regulation (GDPR) or the ongoing evolution of anti-money laundering (AML) directives necessitate sophisticated legal interpretation and technological solutions, often only available from these niche suppliers.

The power of these suppliers stems from the critical need for Crédit Agricole to adhere strictly to these regulations. Failure to comply can result in substantial fines, reputational damage, and even operational restrictions. In 2023, fines for regulatory breaches in the financial sector globally amounted to billions of dollars, underscoring the high stakes involved.

- High Switching Costs: Specialized legal and compliance systems are deeply integrated, making it costly and time-consuming to switch providers.

- Essential Expertise: The complexity of financial regulations means few firms possess the necessary depth of knowledge.

- Risk of Non-Compliance: The severe penalties for regulatory failures empower suppliers whose services mitigate these risks.

- Concentration of Providers: In certain niche areas of financial regulation, the number of highly qualified providers can be limited.

Crédit Agricole: High Supplier Power Drives Costs and Operational Risks

Crédit Agricole faces significant supplier bargaining power from providers of specialized technology, essential financial data, and critical payment networks. The high costs and operational risks associated with switching these providers, coupled with the scarcity of niche expertise in areas like AI and cybersecurity, empower these suppliers. For instance, the demand for AI specialists in finance in 2024 led to salary increases of up to 25%, highlighting the leverage these human capital suppliers possess. Similarly, regulatory compliance services are dominated by firms with unique knowledge, where non-compliance can incur billions in global fines, as seen in 2023, amplifying supplier leverage.

| Supplier Category | Key Providers/Examples | Bargaining Power Drivers | Impact on Crédit Agricole | Relevant Data Point (2023-2024) |

|---|---|---|---|---|

| Technology & Software | Specialized IT system providers, Cybersecurity firms | Proprietary technology, High switching costs, Operational integration | Increased IT expenditure, Potential for vendor lock-in | N/A (Specific vendor data not public) |

| Financial Data & Analytics | Bloomberg, Refinitiv | Scale of data infrastructure, Proprietary information, Essential for operations | Significant subscription costs, Dependency on data accuracy | Bloomberg Terminal fees can exceed $25,000 annually per user. |

| Payment Networks | Visa, Mastercard | Ubiquity, Network effects, Few viable alternatives | Transaction fees, Reliance on network availability | Visa processed over 250 billion transactions globally in 2023. |

| Human Capital (Specialized) | Niche recruitment firms, Consulting groups (AI, Cybersecurity) | Scarcity of skills, High demand, Specialized expertise | Higher recruitment and consulting costs, Talent acquisition challenges | AI specialist salaries increased up to 25% in 2024; consulting fees can exceed $1,000/hour. |

| Regulatory Compliance & Legal | Specialized law firms, Compliance tech vendors | Unique knowledge, High stakes of non-compliance, Regulatory complexity | Increased compliance costs, Reliance on external expertise | Global financial sector fines for regulatory breaches reached billions in 2023. |

What is included in the product

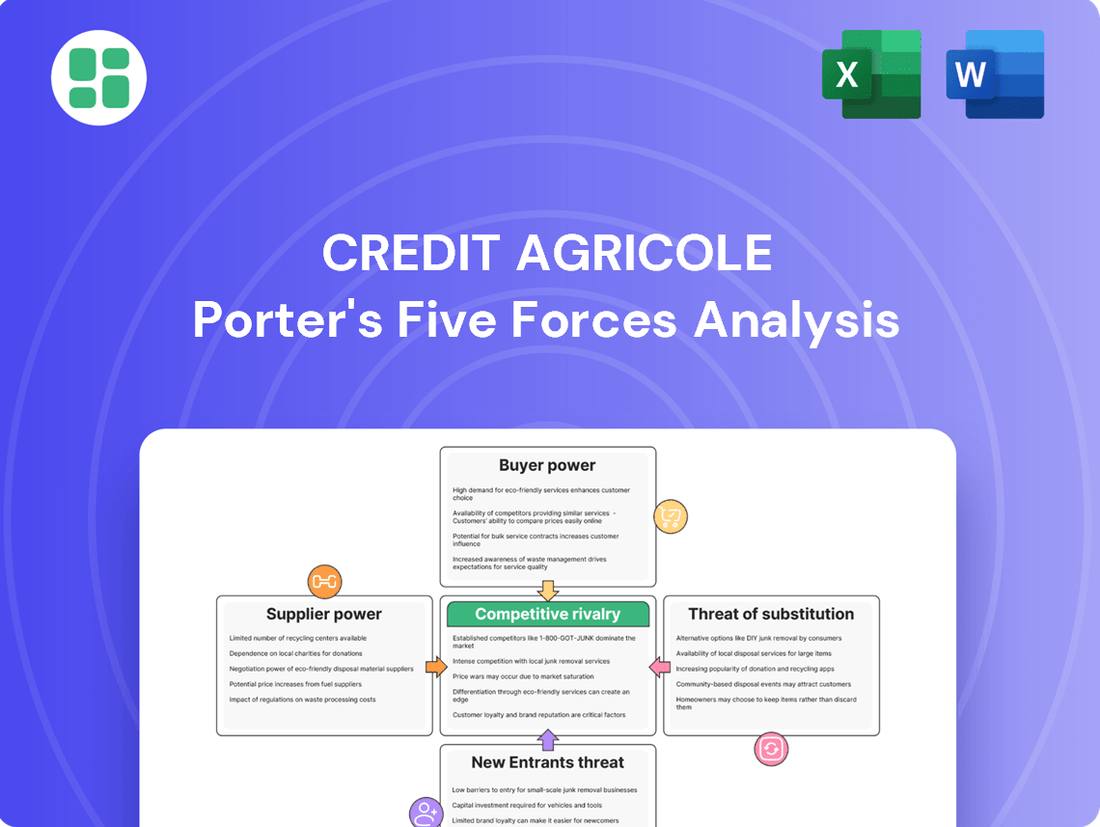

This Porter's Five Forces analysis is tailored to Credit Agricole, dissecting the competitive intensity, buyer and supplier power, threat of new entrants, and the availability of substitutes within its operating environment.

Instantly assess competitive pressures from rivals, suppliers, and new entrants to proactively mitigate risks and capitalize on opportunities.

Customers Bargaining Power

Retail Banking Customers

Individual retail banking customers typically wield moderate bargaining power. The sheer number of competing banks, coupled with the rise of digital-only banks and fintech solutions, provides ample choice. For instance, in 2024, the UK banking sector saw continued growth in challenger banks, offering customers more competitive rates and lower fees, thereby amplifying their ability to negotiate or switch.

While switching costs for simple checking or savings accounts are often low, they escalate for more intricate products. Moving mortgages, investment portfolios, or bundled services involves significant administrative effort and potential disruption, which can deter customers from switching, even if better deals are available elsewhere. This inertia, however, is being chipped away by increasingly user-friendly digital onboarding processes.

Digitalization has been a game-changer, significantly enhancing customer power. In 2024, comparison websites and mobile banking apps made it easier than ever for consumers to scrutinize interest rates, fees, and service quality across different institutions. This transparency allows customers to exert greater influence, pushing banks to offer more attractive terms to retain their business.

Small and Medium-sized Enterprises (SMEs)

Small and Medium-sized Enterprises (SMEs) often wield considerable bargaining power with financial institutions like Credit Agricole. This is especially true for SMEs that engage in substantial transaction volumes or require highly specialized financing solutions. For instance, in 2024, SMEs represented a significant portion of the business lending market, with many banks actively seeking to expand their SME portfolios.

These businesses are adept at comparing offerings, actively seeking out more favorable interest rates, adaptable loan repayment schedules, and customized business banking services. Their ability to negotiate effectively is directly tied to their financial health and credit standing. Furthermore, the competitive landscape among banks eager to capture this vital growth segment amplifies the SMEs' leverage.

Large Corporate and Institutional Clients

Large corporate and institutional clients, including major public sector entities, wield considerable bargaining power with banks like Crédit Agricole. This is primarily due to the sheer volume of business they generate across lending, investment banking, and asset management. For instance, in 2024, large corporations often represent billions in assets under management or significant loan portfolios, making their business highly sought after.

These sophisticated clients frequently initiate competitive bidding processes, pushing banks to offer not only aggressive pricing but also highly tailored financial solutions and dedicated relationship management. Their capacity to spread their business across multiple banking partners further amplifies their leverage, allowing them to negotiate more favorable terms and services.

Digital-Savvy Customers

Digital-savvy customers, increasingly prevalent in 2024, wield significant bargaining power against financial institutions like Crédit Agricole. Their comfort with online platforms and digital-only services frees them from traditional banking limitations.

These customers actively seek out challenger banks and fintech firms offering better digital experiences, lower fees, or specialized services. This competitive pressure compels established players to invest heavily in digital innovation. For instance, by the end of 2023, the global digital banking market was valued at over $20 trillion, indicating a substantial shift in customer preference.

- Increased Price Sensitivity: Digital customers can easily compare fees and rates across multiple providers, forcing banks to remain competitive.

- Demand for Seamless Experience: Customers expect intuitive, user-friendly digital interfaces, pushing banks to enhance their online and mobile offerings.

- Openness to New Entrants: The rise of fintech and neobanks means customers are less loyal to traditional institutions if a better digital alternative exists.

Cooperative Members and Shareholders

As a cooperative financial institution, Crédit Agricole's structure grants its cooperative members and shareholders a distinct collective bargaining power. These stakeholders can directly influence strategic decisions through their voting rights and active participation in the bank's governance. This internal power dynamic significantly shapes the bank's operations, compelling Crédit Agricole to align its services and values with the interests of its member-owners.

This cooperative model means that customer loyalty isn't solely driven by product offerings but also by shared ownership and governance. For instance, in 2023, Crédit Agricole reported a significant portion of its capital held by cooperative groups, underscoring the influence of these members. This structure can lead to more stable customer relationships compared to traditional banks, as members have a vested interest in the bank's long-term success and ethical conduct.

- Member Influence: Cooperative members can vote on key strategic initiatives, directly impacting the bank's direction.

- Alignment of Interests: The bank must prioritize member satisfaction and financial well-being, fostering a strong sense of partnership.

- Governance Impact: Crédit Agricole's governance structure, with representatives from cooperative groups, ensures member voices are heard in decision-making processes.

- Reduced Price Sensitivity: Members may exhibit lower price sensitivity due to their ownership stake and the cooperative's focus on shared value.

Customer Influence in Banking: Digital Demands & Segmented Strength

Individual retail banking customers, while numerous, generally possess moderate bargaining power. The expanding digital banking landscape, with numerous fintech alternatives available in 2024, offers consumers greater choice and the ability to seek better rates and lower fees. However, switching costs for complex financial products like mortgages or investment portfolios can still deter customers, even with improved digital onboarding processes.

SMEs and large corporate clients exhibit higher bargaining power due to their significant transaction volumes and specialized financial needs. In 2024, banks actively competed for SME business, recognizing their growth potential. These clients can leverage their financial standing and the competitive market to negotiate more favorable terms, including pricing and tailored solutions.

Digital-savvy customers in 2024 have amplified their influence by easily comparing offerings across various providers, pushing banks to enhance their digital platforms and customer experiences. The global digital banking market's substantial growth underscores this trend, forcing traditional institutions to innovate to retain business.

Crédit Agricole's cooperative structure grants its members significant collective bargaining power. These stakeholders influence strategic decisions through voting rights, fostering a strong alignment of interests and potentially reducing price sensitivity due to their ownership stake. This model encourages loyalty beyond product offerings, as members have a vested interest in the bank's long-term success.

| Customer Segment | Bargaining Power Level | Key Drivers of Power |

|---|---|---|

| Individual Retail Customers | Moderate | Digital alternatives, ease of comparison, but higher switching costs for complex products. |

| Small and Medium-sized Enterprises (SMEs) | Considerable | Transaction volumes, specialized needs, active bank competition for their business. |

| Large Corporate & Institutional Clients | High | Massive business volumes, competitive bidding, ability to diversify banking relationships. |

| Digital-Savvy Customers | Significant | Ease of comparison, demand for seamless digital experience, openness to new entrants. |

| Cooperative Members/Shareholders | High (Internal) | Voting rights, governance influence, alignment of interests, vested ownership stake. |

Full Version Awaits

Credit Agricole Porter's Five Forces Analysis

This preview showcases the comprehensive Credit Agricole Porter's Five Forces Analysis, detailing the competitive landscape and strategic implications for the bank. The document you see here is the exact, fully formatted analysis you'll receive immediately after purchase, providing actionable insights without any placeholders or surprises.

Rivalry Among Competitors

Intense Competition from Traditional French and European Banks

Crédit Agricole operates in a fiercely competitive landscape, facing significant rivalry from established French banking giants such as BNP Paribas and Société Générale. These domestic players, along with other major European banks, offer a broad spectrum of financial services, directly challenging Crédit Agricole for customers across retail, corporate, and investment banking. For instance, in 2023, BNP Paribas reported a net income of €11.0 billion, demonstrating its substantial market presence and competitive strength.

Growing Pressure from Neobanks and Fintechs

The competitive landscape for traditional banks like Credit Agricole is increasingly shaped by the rise of neobanks and fintech firms. Digital-only entities such as N26 and Revolut are rapidly gaining traction, particularly among younger, tech-savvy consumers, by offering streamlined digital experiences and often lower fee structures. These agile competitors are chipping away at market share in key areas like payments and consumer lending.

Competition in Specialized Financial Services

Crédit Agricole faces significant competition beyond traditional banking. In wealth management, asset management, and insurance, specialized firms like Amundi (a Crédit Agricole subsidiary itself, but also a competitor in the broader market) and major insurance players such as AXA and Allianz vie for customer assets and premiums. For instance, Amundi managed €1.6 trillion in assets as of the end of 2023, highlighting the scale of competition in this segment.

These specialized entities often possess deep domain expertise and highly focused product suites, leading to fierce rivalry within specific financial service lines. This intense competition, particularly in areas like investment banking and capital markets where firms like JPMorgan Chase and Goldman Sachs are dominant, compels Crédit Agricole to constantly innovate and differentiate its offerings across its broad financial services portfolio to maintain market share and profitability.

Regulatory Environment and Market Concentration

The banking sector is heavily regulated, and with a mature market, competition is intense. Established institutions fight for limited growth, and regulatory shifts can significantly alter competitive landscapes. For instance, in 2024, the European Banking Authority continued to emphasize stringent capital requirements, impacting how banks like Crédit Agricole can deploy resources and potentially creating advantages for those with stronger capital buffers.

Market concentration among major European banks means that strategic actions by one entity, such as a significant acquisition or a new digital offering, often provoke swift and strong responses from competitors. This dynamic is evident as major banks, including Crédit Agricole, invest heavily in digital transformation to capture market share, leading to a ripple effect across the industry.

- Regulatory Scrutiny: Banks face ongoing compliance burdens, with evolving rules on capital adequacy (e.g., Basel IV implementation in 2024-2025) directly influencing strategic flexibility and competitive positioning.

- Market Maturity: In developed markets like France, growth is often incremental, intensifying rivalry for existing customer bases and fee-generating services.

- Strategic Interdependence: A move by a competitor, such as BNP Paribas announcing a new fintech partnership in early 2024, immediately prompts other major banks to assess and potentially counter with their own strategic alliances or product innovations.

Innovation and Digital Transformation Race

The banking sector is experiencing intense rivalry driven by a relentless pursuit of innovation and digital transformation. Banks like Crédit Agricole are in a constant race to enhance their digital platforms, deliver personalized customer experiences, and streamline operations. This necessitates significant and ongoing investment in cutting-edge technologies such as artificial intelligence and advanced data analytics to stay ahead of both established competitors and nimble fintech startups.

In 2024, the focus on digital channels remains paramount. For instance, many major European banks reported substantial increases in mobile banking adoption, with some seeing over 70% of customer transactions conducted digitally. Crédit Agricole’s commitment to this area is evident in its ongoing digital transformation initiatives, aimed at improving customer engagement and operational efficiency. Failure to keep pace with these technological advancements risks market share erosion.

- Digital Investment: Banks are allocating significant portions of their IT budgets to digital transformation, with many European institutions projecting digital spending to exceed 20% of their IT budgets in 2024.

- Fintech Competition: The rise of agile fintechs, often unburdened by legacy systems, presents a direct challenge, forcing traditional banks to accelerate their own digital capabilities to match or surpass new entrants.

- Customer Experience: Superior digital platforms and personalized services are becoming key differentiators, directly impacting customer acquisition and retention rates in a highly competitive market.

- AI and Data Analytics: The strategic use of AI and data analytics is crucial for understanding customer behavior, offering tailored financial products, and optimizing risk management, thereby enhancing competitive positioning.

Banking Sector: Intense Rivalry & Digital Innovation Reshaping Competition

Competitive rivalry within the banking sector is intense, with established players like Crédit Agricole facing strong competition from domestic and international banks, as well as agile fintech firms. This rivalry is fueled by a mature market, the need for constant digital innovation, and strategic responses to competitors' moves. For example, in 2023, European banks collectively invested billions in technology to enhance digital offerings and customer experience.

| Competitor Type | Key Competitors | 2023 Net Income (Approx.) | Competitive Focus |

|---|---|---|---|

| Traditional Banks | BNP Paribas, Société Générale | BNP Paribas: €11.0 billion | Retail, Corporate, Investment Banking, Digital Services |

| Fintech/Neobanks | N26, Revolut | N/A (Private Companies) | Digital-first experience, lower fees, specific niches |

| Asset Management | Amundi, BlackRock | Amundi: €1.3 billion | Asset growth, investment performance, specialized funds |

SSubstitutes Threaten

Fintech Solutions for Payments and Lending

The rise of fintech alternatives presents a substantial threat to Crédit Agricole's core payment and lending businesses. Platforms like Klarna and Afterpay offer buy-now-pay-later services, directly competing with traditional credit products. In 2023, the global buy-now-pay-later market was valued at over $130 billion, demonstrating significant customer adoption of these substitute payment methods.

Direct Investment and Robo-Advisory Platforms

Direct investment platforms and robo-advisors present a significant threat of substitution for Crédit Agricole's traditional wealth management services. These digital alternatives empower individuals to manage their portfolios directly or utilize algorithm-based advice, often at a fraction of the cost associated with human advisors. This accessibility and cost-effectiveness can lure away assets that might otherwise be managed by the bank.

The growing adoption of these platforms is evident. For instance, the global robo-advisory market was valued at approximately $2.7 billion in 2023 and is projected to reach over $13.7 billion by 2030, demonstrating a compound annual growth rate of over 25%. This rapid expansion indicates a clear shift in consumer preference towards more automated and lower-cost investment solutions, directly challenging the established models of banks like Crédit Agricole.

Crowdfunding and Alternative Financing

Crowdfunding platforms offer a significant substitute for traditional bank lending, allowing businesses and individuals to raise capital directly from a large pool of investors. This trend is particularly impactful for startups and small to medium-sized enterprises (SMEs) that may face hurdles in securing loans from institutions like Crédit Agricole. For instance, the global crowdfunding market was projected to reach over $20 billion in 2024, demonstrating its growing capacity to channel funds outside conventional banking channels.

Blockchain and Decentralized Finance (DeFi)

The burgeoning blockchain and Decentralized Finance (DeFi) ecosystem presents a nascent but evolving threat of substitution for traditional banking services. These platforms offer alternative avenues for lending, borrowing, and asset management, aiming to bypass intermediaries and potentially reduce costs. While the DeFi market experienced significant growth, with total value locked (TVL) reaching over $170 billion in early 2024 before seeing fluctuations, its long-term impact hinges on achieving broader adoption and navigating regulatory landscapes.

Key aspects of this threat include:

- Disintermediation: DeFi protocols directly connect lenders and borrowers, removing the need for traditional banks as financial intermediaries.

- Cost Efficiency: By cutting out overheads associated with traditional banking, DeFi aims to offer lower transaction fees and higher yields.

- Innovation in Services: DeFi is rapidly developing new financial products, such as yield farming and decentralized exchanges, which could attract customers seeking novel investment opportunities.

- Accessibility: DeFi platforms are often accessible globally with just an internet connection, potentially appealing to underserved markets.

Insurance Products from Non-Bank Entities

The threat of substitutes for Crédit Agricole's insurance products, particularly those offered through its bancassurance model, is significant. Many specialized insurance companies, online comparison platforms, and even non-traditional players are entering the market, offering a wide array of life, health, and property insurance options. For instance, the global insurtech market is projected to reach over $100 billion by 2025, indicating a substantial shift towards digital and specialized insurance providers.

Customers now have unprecedented ease in comparing and purchasing policies directly from these entities, often at competitive prices. This disintermediation bypasses the traditional bundled offerings of banks. In 2024, online insurance sales channels continued to grow, with a notable increase in consumer preference for digital-first insurance providers, especially among younger demographics.

- Increased competition from specialized insurers: Companies focusing solely on insurance can offer more tailored products and potentially lower costs.

- Rise of online aggregators and comparison sites: These platforms empower consumers to easily find and switch to alternative insurance providers.

- Entry of non-financial companies: Retailers and tech firms are increasingly offering insurance products, leveraging their customer bases and brand loyalty.

- Customer preference for digital channels: A growing segment of consumers prefers the convenience and transparency of online insurance purchases.

Traditional Finance Faces Digital Substitution Threats

The threat of substitutes for Crédit Agricole's traditional banking services is multifaceted, encompassing fintech innovations, direct investment platforms, crowdfunding, and the burgeoning DeFi space. These alternatives often offer greater convenience, lower costs, and specialized services, directly challenging the bank's established market share. For instance, the global robo-advisory market is expected to exceed $13.7 billion by 2030, highlighting a significant shift towards automated wealth management solutions.

Moreover, the insurance sector also faces substantial substitution threats from specialized providers and online platforms. The insurtech market's projected growth to over $100 billion by 2025 underscores the increasing consumer preference for digital-first, tailored insurance offerings. This trend, coupled with the rise of online aggregators, empowers customers to bypass traditional bancassurance models.

| Substitute Area | Example Substitutes | Market Data (2023/2024 Estimates) | Impact on Crédit Agricole |

|---|---|---|---|

| Payments & Lending | Buy-Now-Pay-Later (Klarna, Afterpay) | BNPL market > $130 billion (2023) | Direct competition with credit products |

| Wealth Management | Robo-advisors, Direct Investment Platforms | Robo-advisory market ~$2.7 billion (2023) | Attracts assets from traditional advisory |

| Capital Raising | Crowdfunding Platforms | Crowdfunding market > $20 billion (2024 projection) | Alternative for SMEs and startups |

| Financial Services | DeFi Protocols | DeFi TVL > $170 billion (early 2024) | Disintermediation, cost efficiency |

| Insurance | Specialized Insurers, Online Aggregators | Insurtech market > $100 billion (2025 projection) | Bypasses bancassurance, price competition |

Entrants Threaten

High Regulatory and Capital Barriers

The banking sector, including major players like Crédit Agricole, faces a significant threat from new entrants due to exceptionally high regulatory and capital barriers. Navigating complex licensing, stringent capital adequacy rules such as Basel III/IV, and continuous compliance demands substantial investment, time, and specialized expertise. For instance, as of early 2024, the average capital requirement for a Tier 1 bank can run into billions of euros, making it exceedingly difficult for new, undercapitalized entities to compete with established institutions.

Need for Trust and Brand Recognition

The financial services sector, particularly banking, demands a profound level of trust. Building this trust and establishing strong brand recognition is a lengthy, often multi-decade, endeavor. Consumers are naturally cautious with their finances, making them hesitant to switch to unfamiliar providers.

Crédit Agricole, with its deep roots and extensive history, has cultivated significant brand loyalty and public confidence over many years. This established reputation acts as a formidable barrier for newcomers.

New entrants, especially digital-only banks or fintech firms, face a substantial hurdle in bridging this trust gap. They must invest heavily in marketing and customer service to even begin to compete with the ingrained credibility of established players like Crédit Agricole. For instance, in 2024, traditional banks continued to leverage their long-standing customer relationships, which often translate into higher retention rates compared to newer, less established digital platforms.

Economies of Scale and Scope

Established financial institutions, such as Crédit Agricole, leverage significant economies of scale. This translates into lower per-unit costs for technology, risk management, and operations, enabling them to offer competitive pricing and a broad product portfolio efficiently. For instance, in 2023, major European banks reported substantial investments in digital transformation, a cost barrier for smaller, newer players.

New entrants face a steep climb to match these efficiencies. Replicating the extensive infrastructure and sophisticated risk models of incumbents requires immense capital. This makes it challenging for them to compete on cost, especially when offering a full spectrum of services from retail to corporate banking, where scale is paramount for profitability.

Technological Investment and Infrastructure

The threat of new entrants into the banking sector is significantly mitigated by the immense technological investment and infrastructure required. While emerging fintechs can utilize cloud solutions and agile methodologies, establishing a comprehensive, secure, and scalable technological backbone akin to established institutions like Crédit Agricole demands substantial and ongoing capital outlay. For instance, in 2023, global IT spending in the banking sector was projected to reach hundreds of billions of dollars, reflecting the sheer scale of investment needed for core banking systems, cybersecurity, and data management.

Replicating the sophisticated IT capabilities necessary for a full-service bank, including seamless integration of diverse financial products, robust cybersecurity defenses, and the meticulous management of vast customer data, presents a formidable barrier. New entrants would face enormous costs and complexity in building these systems from the ground up, making it difficult to compete on par with incumbents who have decades of investment and refinement in their technological infrastructure. This high cost of entry, particularly in cutting-edge areas like AI-driven fraud detection and personalized digital banking experiences, acts as a significant deterrent.

- Massive Capital Outlay: Building secure, scalable, and integrated banking technology infrastructure requires billions in investment, a significant hurdle for new entrants.

- Cybersecurity Demands: Protecting sensitive financial data necessitates advanced and continuously updated cybersecurity measures, adding substantial operational costs.

- Integration Complexity: Seamlessly integrating diverse financial products and services into a unified platform is technically challenging and expensive to develop from scratch.

- Data Management: Handling and analyzing vast quantities of customer data for compliance and service enhancement requires sophisticated and costly data infrastructure.

Niche Market Entry by Fintechs and Challenger Banks

The threat of new entrants for Crédit Agricole, while generally moderated by significant capital requirements and regulatory hurdles, is notably present through agile fintechs and challenger banks. These entities often target lucrative niches within the financial services landscape, leveraging digital-first strategies to bypass the overhead associated with traditional branch networks.

These new players can offer highly specialized services, such as streamlined digital payment solutions or instant loan origination, which appeal to specific customer segments. For instance, by focusing on a single, highly convenient digital offering, they can attract users who might otherwise be served by larger institutions. This approach allows them to gain traction without needing to replicate the full-service model of incumbents like Crédit Agricole.

While these fintechs may not immediately challenge Crédit Agricole across its entire product suite, their ability to capture profitable segments poses a persistent threat. Their lower operating costs and ability to innovate rapidly allow them to compete effectively on price and user experience within their chosen niches. For example, in 2024, the digital banking sector saw continued growth, with neobanks in Europe attracting millions of new customers, demonstrating the impact of these specialized entrants.

- Fintechs bypass traditional barriers like extensive branch networks.

- Challenger banks focus on specific, profitable niches within financial services.

- Digital-only models reduce operational costs and increase agility.

- These entrants can erode market share in lucrative segments, impacting overall profitability.

Banking's Fortified Walls: Entry Barriers Protect Incumbents

The threat of new entrants for Crédit Agricole is significantly lowered by the immense capital requirements and stringent regulatory landscape inherent in banking. Building a full-service bank requires billions in capital, extensive licensing, and adherence to complex rules like Basel III/IV, making it incredibly difficult for newcomers. For example, in 2024, capital adequacy ratios for major banks remained high, demanding substantial financial backing.

Established players like Crédit Agricole benefit from strong brand recognition and deep customer loyalty, cultivated over decades. This trust is a major barrier for new entrants, who must invest heavily in marketing and customer acquisition to even begin to compete. In 2023, traditional banks continued to see higher customer retention rates than many newer digital platforms.

Economies of scale enjoyed by incumbents, such as Crédit Agricole, allow for lower operating costs in technology, risk management, and product development. Replicating this efficiency requires massive investment, posing a significant challenge for smaller, newer firms trying to compete on price and service breadth.

While traditional barriers are high, agile fintechs and challenger banks pose a more nuanced threat by targeting specific, profitable niches with digital-first offerings. These specialized entrants can bypass traditional infrastructure costs and rapidly attract customers in areas like digital payments or streamlined lending, as seen with the continued growth of neobanks in Europe during 2024.

| Barrier Type | Description | Impact on New Entrants | Example (2024/2025 Data) |

|---|---|---|---|

| Capital Requirements | High minimum capital reserves mandated by regulators. | Significant financial hurdle, limiting the number of potential entrants. | Tier 1 capital requirements for major banks often in the tens of billions of Euros. |

| Regulatory Hurdles | Complex licensing, compliance, and reporting obligations. | Increases time-to-market and operational costs, requiring specialized legal and compliance expertise. | Ongoing adjustments to Basel IV framework continue to shape capital management strategies. |

| Brand Reputation & Trust | Established customer relationships and perceived reliability. | Difficult and time-consuming for new players to build equivalent trust. | Traditional banks maintained higher customer loyalty compared to emerging digital-only banks. |

| Economies of Scale | Lower per-unit costs due to large operational volume. | New entrants struggle to match pricing and service breadth of incumbents. | Large banks' investments in IT infrastructure and risk modeling create significant cost advantages. |

| Technological Infrastructure | Sophisticated IT systems for core banking, security, and data management. | Massive upfront and ongoing investment required to build and maintain competitive technology. | Global IT spending in banking sector projected to exceed $600 billion annually in 2024. |

Porter's Five Forces Analysis Data Sources

Our Credit Agricole Porter's Five Forces analysis is built upon a foundation of robust data, drawing from Credit Agricole's annual reports, investor presentations, and regulatory filings. We supplement this with insights from reputable financial news outlets, industry-specific research reports, and macroeconomic data providers to ensure a comprehensive understanding of the competitive landscape.