CAR Group Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

CAR Group Bundle

From Overview to Strategy Blueprint

Understanding the competitive landscape for CAR Group is crucial for any strategic decision. Our initial look reveals moderate bargaining power from buyers and suppliers, with a notable threat from substitute products impacting the industry.

The complete report reveals the real forces shaping CAR Group’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Supplier Power 1

The primary suppliers for CAR Group are car dealerships and private sellers who list vehicles on its platforms. These content providers hold moderate bargaining power. CAR Group's strong market dominance, particularly in Australia, offers dealers significant reach to potential buyers, which is a key value proposition.

While CAR Group's platform offers substantial exposure, the fragmented nature of the dealer market means that individual dealerships typically don't represent a large enough portion of total listings to exert significant leverage. This lack of concentration among suppliers limits their ability to dictate terms.

Supplier Power 2

CAR Group's reliance on technology and data providers means these entities act as significant suppliers. The effectiveness of CAR Group's valuation tools, advertising capabilities, and platform operations hinges on robust technological infrastructure and advanced data analytics.

The bargaining power of these specialized tech and data firms can range from moderate to high. This is especially true when they offer niche or proprietary solutions that are essential for CAR Group to improve its services and maintain its competitive advantage in the market.

For instance, the cost of cloud computing services, a critical component for data storage and processing, saw a notable increase in 2024. Major cloud providers, such as Amazon Web Services (AWS), Microsoft Azure, and Google Cloud, have considerable leverage due to the specialized nature of their infrastructure and the significant investment required to switch providers.

Supplier Power 3

Advertising technology and digital marketing service providers represent a key supplier group for CAR Group. These companies are crucial for optimizing advertising solutions offered to dealers and private sellers, as well as for CAR Group's internal marketing initiatives. The influence these suppliers wield can fluctuate based on how standardized their offerings are; specialized or deeply integrated services tend to hold greater leverage.

Supplier Power 4

Payment processing and financial service providers are crucial for CAR Group's platforms, enabling transactions and offering financing. These partners are essential for the smooth operation of the marketplace, directly impacting customer experience and sales conversion rates.

The bargaining power of these suppliers is considerable. For instance, in 2024, CAR Group continued its significant partnership with Santander in Brazil, a key player in providing financial services. Such strong alliances highlight the suppliers' integral role in facilitating transactions and offering vital finance options to CAR Group's customer base.

- Financial institutions are critical enablers of transactions on CAR Group's digital platforms.

- Partnerships with entities like Santander in Brazil underscore the importance of these financial service providers.

- The ability of these suppliers to offer competitive financing solutions directly influences customer purchasing decisions and CAR Group's sales volume.

- In 2024, the continued reliance on established financial partners demonstrated their significant leverage in the automotive e-commerce ecosystem.

Supplier Power 5

The automotive industry's accelerating digital transformation, marked by AI-driven platforms and virtual showrooms, significantly impacts supplier power. Suppliers offering cutting-edge AI, AR/VR capabilities, or robust digital integration solutions are increasingly influential as CAR Group prioritizes enhanced customer experiences and operational streamlining.

CAR Group's strategic investments in digital technologies, such as its reported spending of over $1 billion in 2024 on software development and AI integration, underscore the growing importance of tech-savvy suppliers. Suppliers demonstrating expertise in these areas can command higher prices and more favorable terms, as their contributions are critical to CAR Group's competitive edge.

- Digital Integration Expertise: Suppliers adept at integrating complex digital systems, from AI-powered diagnostics to seamless online sales platforms, hold considerable sway.

- AI and Advanced Technology Providers: Companies specializing in AI algorithms for vehicle performance, predictive maintenance, or personalized customer journeys are in high demand.

- Data Security and Management Solutions: With the proliferation of connected vehicles, suppliers offering secure data management and cybersecurity solutions gain leverage.

- Virtual Showroom and AR/VR Technology: Suppliers providing innovative virtual showroom experiences and augmented reality applications for car customization are vital for CAR Group's evolving sales strategies.

Supplier Leverage: Navigating CAR Group's Critical Partnerships

CAR Group faces moderate bargaining power from its primary suppliers, car dealerships and private sellers, due to its dominant market position which offers them significant buyer reach. However, the fragmented nature of these sellers limits their collective ability to dictate terms.

Tech and data providers, crucial for CAR Group's platform functionality, possess moderate to high bargaining power, especially those offering specialized or proprietary solutions. For instance, the cost of essential cloud computing services, a critical component for data processing, saw increases in 2024 from major providers like AWS and Azure, reflecting their leverage.

Financial institutions and advertising technology firms also exert considerable influence. CAR Group's 2024 partnership with Santander in Brazil highlights the integral role of financial partners in facilitating transactions and offering vital financing options, directly impacting sales volume.

Suppliers of advanced digital technologies, including AI and AR/VR capabilities, are gaining significant leverage as CAR Group invests heavily in digital transformation. CAR Group's reported over $1 billion investment in 2024 for software development and AI integration underscores the critical importance of these tech-savvy suppliers, allowing them to command higher prices and more favorable terms.

| Supplier Type | Bargaining Power | Key Factors | 2024 Data/Examples |

| Car Dealerships/Private Sellers | Moderate | Market reach, fragmented seller base | CAR Group's Australian dominance provides significant exposure. |

| Tech & Data Providers | Moderate to High | Niche/proprietary solutions, essential infrastructure | Increased cloud computing costs from providers like AWS, Azure in 2024. |

| Financial Service Providers | Considerable | Transaction facilitation, financing options | Continued partnership with Santander in Brazil for financing solutions. |

| Digital Technology Providers (AI, AR/VR) | High | Cutting-edge capabilities, digital integration expertise | CAR Group's >$1 billion investment in AI and software development in 2024. |

What is included in the product

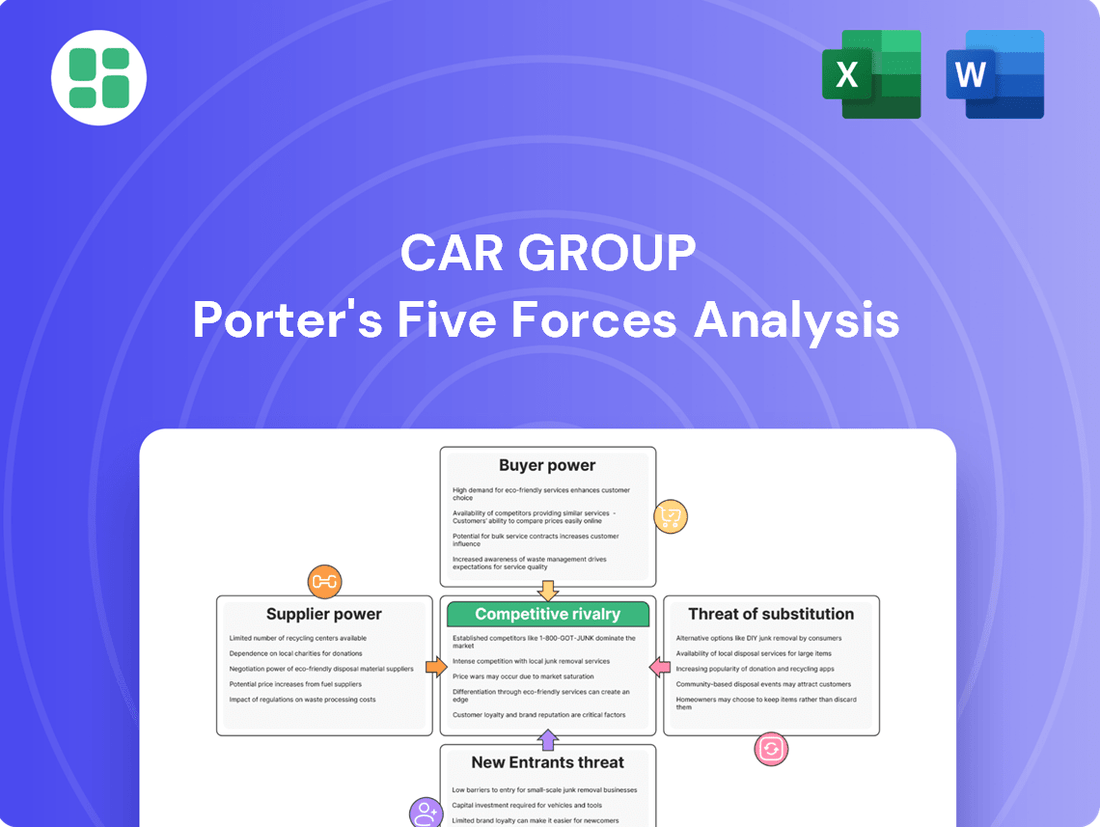

This analysis unpacks the competitive forces impacting CAR Group, revealing the intensity of rivalry, buyer and supplier power, threat of new entrants, and the availability of substitutes.

Quickly identify and mitigate competitive threats with a visual breakdown of industry power dynamics.

Customers Bargaining Power

Buyer Power 1

The bargaining power of individual car buyers on CAR Group's platforms is typically low. While consumers benefit from a broad selection and convenient search tools, their ability to negotiate directly with CAR Group regarding platform usage fees is minimal. The aggregated value of the marketplace, offering a centralized and efficient car-shopping experience, generally outweighs an individual buyer's leverage.

Buyer Power 2

Car dealerships and professional sellers, as key customers for CAR Group, wield moderate bargaining power. Their reliance on CAR Group's platform for market access is significant, particularly in a crowded automotive sales environment. In 2024, the automotive market continued to see intense competition, pushing dealerships to seek favorable terms from lead generation and advertising partners.

These professional sellers contribute a substantial portion of CAR Group's overall revenue, giving them leverage to negotiate pricing, service packages, and lead quality. The growing interest in direct-to-consumer sales models and alternative online marketplaces could further embolden dealerships to demand better value or explore other avenues if CAR Group's offerings become less competitive.

Buyer Power 3

Advertisers, especially major automotive manufacturers and large dealership networks, wield moderate bargaining power over CAR Group. These advertisers rely on CAR Group's digital platforms to connect with a vast audience of potential car buyers, utilizing its data analytics for precise targeting. However, their significant marketing expenditures give them leverage to negotiate favorable advertising rates and demand customized solutions.

While CAR Group offers valuable reach, advertisers are not entirely dependent, as numerous alternative advertising channels exist, from social media to traditional media. In 2024, the automotive advertising market saw continued shifts towards digital, with online channels accounting for a significant portion of ad spend, providing advertisers with options and increasing their ability to negotiate with platform providers like CAR Group.

Buyer Power 4

The bargaining power of customers for CAR Group is increasing due to the digital transformation of car buying. Customers now have access to online financing options and digital paperwork, providing them with greater transparency and information. This empowers them to negotiate more effectively with sellers, directly impacting the value CAR Group must offer to its dealership clients.

This shift means CAR Group must continuously adapt its value proposition to ensure dealerships remain competitive and attractive to these informed buyers. For instance, by mid-2024, platforms offering transparent pricing and financing comparisons saw significant user engagement, indicating a strong customer preference for readily available information.

- Increased Information Access: Digital platforms provide customers with detailed vehicle information, pricing, and financing comparisons, reducing information asymmetry.

- Online Financing and Paperwork: The ease of securing financing and completing documentation online gives buyers more control and reduces reliance on traditional dealership processes.

- Negotiating Leverage: Greater transparency and access to market data empower customers to negotiate prices more assertively, putting pressure on sellers.

- Impact on CAR Group's Value Proposition: CAR Group must ensure its services help dealerships maintain a competitive edge in an environment where buyers are increasingly well-informed and empowered.

Buyer Power 5

The bargaining power of customers in the used car market, particularly concerning platforms like CAR Group, is influenced by current market conditions. In 2024, the used car market has seen some stabilization after significant price surges in previous years. For instance, while average used car prices in the US saw a notable increase from 2020 to 2022, by mid-2024, data suggests a more moderate trend, with some segments experiencing slight declines or plateauing. This environment can shift buyer leverage.

Despite fluctuations, customers still rely on digital platforms for information and purchasing convenience. CAR Group's role in aggregating inventory and providing comparison tools remains crucial. Even when prices are high and supply is constrained, buyers need efficient ways to locate vehicles and assess value. This reliance on the platform itself can be a counter-balance to their direct bargaining power with individual sellers.

- Shifting Market Dynamics: Used car prices in 2024 have shown a cooling trend compared to the peak inflation of 2021-2022, potentially giving buyers slightly more room to negotiate.

- Information Asymmetry Reduction: Platforms like CAR Group empower buyers by providing access to vast amounts of data, including pricing history and vehicle condition reports, which enhances their ability to negotiate effectively.

- Inventory Scarcity Impact: While market conditions in 2024 are improving, localized or segment-specific inventory shortages can still limit buyer options, thereby reducing their immediate bargaining power.

- Platform Reliance: Buyers continue to depend on CAR Group's user-friendly interface and comprehensive listings to navigate the market, which indirectly strengthens the platform's position.

Customer Bargaining Power in the 2024 Automotive Market

The bargaining power of customers for CAR Group is a dynamic factor, influenced by market conditions and the increasing digital sophistication of car buyers. While individual buyers have limited direct leverage on the platform itself, their collective demand for transparency and convenience significantly shapes the automotive retail landscape. This trend is evident as of mid-2024, with a notable increase in user engagement on platforms offering clear pricing and financing comparisons, underscoring a strong buyer preference for readily accessible information.

Dealerships and professional sellers, representing a key customer segment for CAR Group, possess moderate bargaining power. Their reliance on the platform for lead generation and market access, especially within the competitive 2024 automotive sales environment, allows them to negotiate terms. Major advertisers, such as automotive manufacturers, also wield considerable influence due to their substantial marketing investments and the availability of alternative advertising channels, enabling them to negotiate favorable rates and demand tailored solutions.

| Customer Segment | Bargaining Power Level | Key Influencing Factors | 2024 Market Context |

|---|---|---|---|

| Individual Car Buyers | Low | Limited direct negotiation with platform; benefit from aggregated selection. | Increased demand for transparency and digital tools. |

| Car Dealerships/Professional Sellers | Moderate | Reliance on platform for leads; significant revenue contribution. | Intense market competition; seeking favorable terms from lead generation partners. |

| Major Advertisers (Manufacturers, Large Networks) | Moderate | Significant ad spend; leverage from alternative advertising channels. | Shift towards digital advertising; demand for precise targeting and customized solutions. |

Same Document Delivered

CAR Group Porter's Five Forces Analysis

This preview shows the exact CAR Group Porter's Five Forces Analysis you'll receive immediately after purchase, offering a comprehensive examination of industry competition and profitability. You'll gain detailed insights into the bargaining power of buyers and suppliers, the threat of new entrants and substitutes, and the intensity of rivalry within the automotive retail sector. This professionally formatted document is ready for your strategic planning needs.

Rivalry Among Competitors

Competitive Rivalry 1

Competitive rivalry within the online automotive marketplace is intense, fueled by both seasoned industry giants and the relentless digital evolution of the automotive sector. CAR Group navigates this landscape, encountering a diverse array of local and international rivals. Its substantial market share in key regions like Australia, Brazil, South Korea, and the United States underscores its leadership, though this position is constantly tested.

Competitive Rivalry 2

Competitive rivalry within the online automotive classifieds sector is intense, with CAR Group facing pressure from various fronts. Key competitors include other large online classifieds portals that may expand their automotive offerings, specialized automotive marketplaces focusing solely on vehicles, and even general e-commerce giants like Amazon or eBay that are increasingly exploring vehicle sales and related services.

While CAR Group holds a dominant position in its core Australian market, its international ventures encounter competition from established regional players and global platforms. For example, in markets where CAR Group operates internationally, it must contend with local classifieds sites that have deep-rooted customer loyalty and understanding of regional nuances, as well as global classifieds networks that leverage scale and brand recognition.

Competitive Rivalry 3

The automotive industry is seeing a significant shift with manufacturers like Tesla and BYD increasingly adopting direct-to-consumer (D2C) sales models. This trend, alongside the growth of digital-first dealerships such as Carvana and Vroom, fundamentally alters the competitive landscape. These new approaches offer consumers alternative, often more streamlined, buying experiences that can bypass traditional channels.

This intensification of rivalry pressures established platforms like CAR Group. By directly engaging with buyers and sellers, these D2C and digital models reduce reliance on third-party marketplaces for vehicle discovery and transactions. Consequently, CAR Group must constantly innovate and clearly articulate its unique value proposition to both consumers seeking to buy and dealers or private sellers looking to list their vehicles.

For instance, Carvana reported a revenue of $3.9 billion in 2023, demonstrating the scale of these digital-first operations. This growth highlights the need for platforms like CAR Group to adapt and enhance their offerings, perhaps by integrating more advanced digital tools or providing superior market insights to remain competitive in this evolving automotive retail environment.

Competitive Rivalry 4

Technological innovation is rapidly reshaping the automotive retail landscape, making it a fierce battleground for CAR Group. Competitors are pouring resources into advancements like artificial intelligence, augmented and virtual reality, and sophisticated data analytics to gain an edge. For instance, in 2024, several automotive retailers launched AI-powered virtual assistants to handle customer inquiries, aiming to improve response times and personalize interactions. This push for technological superiority means CAR Group must continuously invest in and develop cutting-edge features to remain competitive and meet evolving customer expectations.

The drive towards enhanced customer experiences, including virtual showrooms and seamless online transactions, is a significant factor in competitive rivalry. Many rivals are focusing on creating immersive digital environments where customers can explore vehicles remotely and complete purchases with minimal friction. By mid-2024, reports indicated that a significant percentage of car buyers were utilizing online tools for research and even initiating purchases, underscoring the importance of these digital capabilities. CAR Group’s ability to offer a superior, integrated online-to-offline experience will be crucial in attracting and retaining customers.

- Technological Investment: Competitors are increasing R&D spending on AI and AR/VR. For example, a major competitor announced a $500 million investment in AI for customer service by the end of 2024.

- Personalized Experiences: The focus is on tailoring offers and interactions. Data analytics are being used to predict customer needs, with some firms reporting a 15% increase in conversion rates from personalized campaigns in early 2024.

- Virtual Showrooms: Companies are developing advanced virtual showroom technologies. One competitor saw a 30% rise in online engagement after launching its interactive VR showroom in Q1 2024.

- Online Transaction Streamlining: Efforts are concentrated on making online car buying easier. A recent industry survey found that 40% of potential buyers prioritize a smooth online purchasing process when choosing a dealership.

Competitive Rivalry 5

The automotive industry is experiencing intensified competitive rivalry, significantly impacting CAR Group. The global expansion of automotive companies, particularly Chinese electric vehicle (EV) manufacturers, is a major driver. These new entrants are aggressively entering diverse geographical markets, often with competitive pricing and innovative technology, directly challenging established players like CAR Group.

CAR Group must actively defend its market share in this increasingly crowded landscape. This necessitates a proactive approach to its own global expansion strategies, including strategic acquisitions and international growth initiatives. The digital presence of these competitors also means CAR Group needs to bolster its online offerings and customer engagement to remain competitive.

- Intensified Global Competition: Chinese EV manufacturers like BYD and SAIC Motor are expanding rapidly worldwide. BYD, for instance, reported a significant increase in its global sales in 2023, surpassing 3 million vehicles, a substantial portion of which were new energy vehicles.

- Digital Marketplaces: The rise of online car sales platforms and digital customer interaction models means that competition extends beyond traditional dealerships to the digital realm, requiring CAR Group to invest heavily in its online presence and e-commerce capabilities.

- Acquisition Strategies: To counter this, CAR Group may need to pursue strategic acquisitions to gain market access, acquire new technologies, or consolidate its position in key regions, mirroring the consolidation trends seen across the automotive sector.

Automotive Competition: D2C, Global EVs, Tech Drive Market Shifts

Competitive rivalry is escalating due to the rise of direct-to-consumer (D2C) models from manufacturers and digital-first dealerships like Carvana, which reported $3.9 billion in revenue in 2023. These players bypass traditional marketplaces, forcing CAR Group to innovate and highlight its unique value proposition. Furthermore, aggressive global expansion by new entrants, particularly Chinese EV manufacturers such as BYD, which sold over 3 million vehicles in 2023, intensifies competition, necessitating CAR Group's strategic market defense and digital enhancement.

| Competitor Type | Key Trend/Action | Impact on CAR Group | Example Data/Fact |

|---|---|---|---|

| D2C Manufacturers & Digital Dealerships | Direct sales, streamlined digital experience | Reduced reliance on marketplaces, need for differentiated value | Carvana revenue: $3.9 billion (2023) |

| Global Automakers (esp. Chinese EVs) | Aggressive international market entry, competitive pricing | Market share erosion, need for global strategy enhancement | BYD global sales: >3 million vehicles (2023) |

| Tech-focused Competitors | Investment in AI, AR/VR, personalized experiences | Pressure to invest in technology for customer engagement | Competitor AI investment: $500 million (by end of 2024) |

SSubstitutes Threaten

1

The threat of substitutes for CAR Group's online marketplace services remains a significant consideration, generally assessed as moderate to high. While CAR Group offers a streamlined digital experience, traditional physical car dealerships continue to represent a viable alternative for many consumers. These brick-and-mortar establishments cater to buyers who value the hands-on experience of test driving vehicles and the immediate gratification of taking possession of a car. In 2024, despite the digital shift, a substantial portion of car sales still occurred through traditional dealerships, indicating their persistent appeal.

2

Direct-to-consumer (D2C) sales models are a growing threat. Major automotive manufacturers are increasingly selling new and used vehicles directly to buyers through their own online platforms. This bypasses traditional third-party marketplaces, potentially impacting CAR Group's listing volumes and advertising revenue.

3

General online classifieds and social media platforms present a significant threat of substitutes for CAR Group. Websites like Gumtree in Australia, and the ubiquitous Facebook Marketplace, offer private sellers a low-cost or even free avenue to list vehicles. While these platforms may not possess the specialized automotive features or the extensive buyer reach of CAR Group's dedicated sites, they cater effectively to budget-conscious individuals looking to offload a car without incurring listing fees.

4

The rise of new mobility solutions presents a significant threat of substitutes for traditional car ownership, and by extension, for automotive marketplaces. Services like car-sharing, ride-hailing, and vehicle subscription models are gaining traction, particularly in urban areas. These alternatives directly address the need for transportation without the commitment of purchasing a vehicle. For instance, the global ride-hailing market was valued at approximately $150 billion in 2023 and is projected to grow substantially, indicating a shift in consumer preferences. This trend could gradually reduce the demand for new and used car sales, impacting transaction volumes on platforms like those operated by CAR Group.

While these new mobility options do not directly replace the act of owning a car, they fulfill the underlying need for mobility. This indirect competition can erode the market share for vehicle ownership over the long term. As more consumers opt for flexible, pay-as-you-go transportation, the perceived necessity of owning a personal vehicle diminishes. This could lead to a contraction in the overall pool of potential buyers for cars, affecting the revenue streams of automotive marketplaces that rely on transaction volume and advertising from dealerships.

The impact of these substitutes is likely to be more pronounced among younger demographics and in densely populated urban environments where the cost and inconvenience of car ownership are higher. Data from 2024 surveys indicate a growing preference for mobility-as-a-service among Gen Z and Millennials. This evolving consumer behavior necessitates that automotive marketplaces adapt by potentially integrating or partnering with these new mobility providers to remain relevant.

Key aspects of the threat of substitutes include:

- Reduced Demand for Vehicle Ownership: Mobility services offer convenient alternatives to personal car ownership, potentially decreasing the overall number of car purchases.

- Shifting Consumer Preferences: Younger generations, in particular, are increasingly embracing subscription and sharing models over traditional ownership.

- Impact on Transaction Volume: A decline in vehicle sales directly translates to fewer transactions on automotive marketplaces, affecting revenue.

- Long-Term Market Erosion: While not an immediate threat to car sales, the sustained growth of these services poses a long-term risk to the traditional automotive retail model.

5

Peer-to-peer selling apps and platforms represent a growing threat of substitutes for CAR Group. These platforms, such as Facebook Marketplace or specialized local selling apps, allow individuals to directly connect and conduct private sales without relying on a traditional marketplace intermediary. This disintermediation can bypass CAR Group's platform fees and services, particularly for sellers who prioritize simplicity and cost savings over the structured environment CAR Group provides.

The ease of use and accessibility of these peer-to-peer channels are key drivers of their threat. For instance, in 2024, the used car market saw a significant portion of transactions occur through informal channels, with estimates suggesting up to 30% of private used car sales bypassed traditional dealerships or online marketplaces. This trend is fueled by the desire for direct negotiation and potentially lower prices, directly challenging CAR Group's value proposition.

CAR Group faces this threat through several avenues:

- Direct Sales Channels: Platforms enabling direct buyer-seller interaction without a marketplace intermediary.

- Reduced Transaction Costs: These alternatives often have lower or no fees compared to established platforms.

- Niche Market Appeal: They cater to segments of the market seeking simplicity and direct negotiation, potentially fragmenting CAR Group's user base.

Diverse Substitutes Challenge the Automotive Marketplace

The threat of substitutes for CAR Group is multifaceted, encompassing traditional dealerships, direct-to-consumer sales, general online classifieds, and new mobility solutions. Traditional dealerships, while facing digital disruption, still appeal to buyers valuing in-person experiences, with a significant portion of 2024 car sales occurring through these channels. Direct-to-consumer models by manufacturers bypass marketplaces, impacting listing volumes. General online platforms like Facebook Marketplace offer low-cost alternatives for private sellers, capturing a segment prioritizing cost savings over specialized features.

New mobility services such as car-sharing and ride-hailing are evolving substitutes for car ownership itself. The global ride-hailing market, valued at around $150 billion in 2023, highlights a growing preference for transportation-as-a-service, particularly among younger demographics in urban areas. This trend, evident in 2024 surveys showing increased adoption by Gen Z and Millennials, could gradually reduce the overall demand for vehicle purchases, indirectly affecting automotive marketplaces.

Peer-to-peer selling platforms also pose a threat by enabling direct buyer-seller transactions, bypassing intermediary fees. In 2024, an estimated 30% of private used car sales occurred through informal channels, underscoring the appeal of simplicity and direct negotiation for a segment of the market.

| Substitute Type | Key Features | Impact on CAR Group | 2024 Data/Trend |

|---|---|---|---|

| Traditional Dealerships | Hands-on experience, immediate possession | Persistent customer base, potential for reduced online traffic | Significant portion of 2024 sales |

| Direct-to-Consumer (D2C) | Manufacturer-controlled sales | Reduced inventory on marketplaces, lower listing volumes | Growing trend among major automakers |

| General Online Classifieds/Social Media | Low/no cost, broad reach | Fragmented market, loss of private seller listings | High usage for informal sales |

| New Mobility Services | Transportation-as-a-service, reduced ownership need | Long-term erosion of car ownership demand | $150B ride-hailing market (2023), increasing Gen Z/Millennial adoption |

| Peer-to-Peer Selling | Direct buyer-seller interaction, cost savings | Disintermediation, loss of transaction fees | Estimated 30% of private used car sales (2024) |

Entrants Threaten

1

The threat of new entrants in the online automotive marketplace sector, where CAR Group operates, is currently moderate. While setting up a basic listing site may not demand vast capital, creating a truly competitive platform akin to CAR Group necessitates substantial investment. This includes robust technology infrastructure, significant marketing to build brand awareness, and the crucial task of attracting a critical mass of both vehicle sellers and potential buyers.

2

The threat of new entrants for CAR Group is relatively low, primarily due to the powerful network effects at play. CAR Group benefits from a robust two-sided market: a vast number of car buyers are attracted by the extensive inventory of sellers, and conversely, numerous sellers are drawn to the platform due to its large buyer audience. This creates a virtuous cycle that is difficult for newcomers to replicate.

New entrants face a significant hurdle in achieving the critical mass of both buyers and sellers that CAR Group already commands. Users naturally gravitate towards platforms offering the most comprehensive selection of vehicles and the widest reach of potential buyers, making it challenging for new platforms to gain traction and compete effectively. For instance, in 2024, the automotive classifieds market continues to be dominated by established players, with CAR Group holding a substantial market share.

3

The threat of new entrants for CAR Group is generally considered moderate. CAR Group's established brand loyalty and deep-seated trust, built over decades (dating back to 1997 as carsales.com Ltd), present a significant hurdle for newcomers. Achieving a comparable level of credibility with both consumers and dealerships requires substantial time and investment.

New entrants would need to overcome CAR Group's extensive network and data advantages. For instance, in 2024, CAR Group continued to dominate online automotive classifieds in Australia, a market where network effects are crucial for buyer and seller engagement. Building a comparable user base and inventory from scratch is a considerable challenge.

4

The threat of new entrants for CAR Group is moderate, largely due to the significant barriers created by its proprietary data and advanced analytics. CAR Group's extensive datasets on vehicle valuations, market trends, and consumer behavior are a crucial competitive advantage. Building a comparable data repository and analytical infrastructure would require substantial investment and time for any new player. For instance, as of early 2024, the automotive data analytics market is projected to grow significantly, indicating high interest but also the need for deep data integration capabilities.

New entrants would face considerable challenges in replicating CAR Group's established position.

- Proprietary Data: CAR Group's access to unique and comprehensive vehicle data is a key differentiator.

- Advanced Analytics: Sophisticated analytical tools and algorithms are necessary to derive actionable insights from this data.

- Time and Resource Investment: New entrants would need years and significant capital to build comparable data sets and analytical capabilities.

- Market Trust: CAR Group has cultivated trust and recognition within the industry, which is difficult for newcomers to achieve quickly.

5

The threat of new entrants for CAR Group, particularly in international markets, is significantly mitigated by substantial regulatory hurdles and compliance requirements. Navigating diverse legal frameworks, consumer protection laws, and data privacy regulations across multiple countries presents a complex and costly challenge. This complexity favors established players who already possess the necessary legal and operational infrastructure.

For instance, in 2024, the automotive industry globally saw increased scrutiny on data handling and cybersecurity, with new regulations like the EU's AI Act impacting how autonomous driving features are developed and deployed. For a new entrant, understanding and implementing compliance for these evolving standards across different jurisdictions, such as the GDPR in Europe or similar mandates in Asia and North America, requires significant investment in legal expertise and technological adaptation. This creates a high barrier to entry, protecting incumbent companies like CAR Group.

- Regulatory Complexity: CAR Group benefits from established expertise in navigating international automotive regulations.

- Compliance Costs: New entrants face substantial upfront costs for legal and compliance infrastructure.

- Data Privacy: Evolving data protection laws globally add another layer of complexity for potential market entrants.

- Established Infrastructure: Existing players have the advantage of pre-existing operational and legal frameworks.

CAR Group's Defenses: High Barriers for New Entrants

The threat of new entrants for CAR Group is generally moderate, tempered by significant capital requirements and the need to build extensive networks. While initial setup costs for a basic platform might be manageable, establishing a competitive presence akin to CAR Group requires substantial investment in technology, marketing, and crucially, acquiring a critical mass of both buyers and sellers. This is particularly true in 2024, where the online automotive marketplace is characterized by strong network effects, making it difficult for newcomers to gain traction against established players like CAR Group.

CAR Group's established brand, deep-seated trust, and significant data advantages further deter new entrants. Building comparable credibility with consumers and dealerships takes considerable time and investment, a hurdle that newcomers in 2024 must overcome. Moreover, CAR Group's proprietary data and advanced analytics, which provide insights into vehicle valuations and market trends, represent a substantial barrier. For instance, the automotive data analytics market is experiencing robust growth in 2024, highlighting the value and complexity of these capabilities.

International expansion for CAR Group also faces mitigated threats from new entrants due to complex regulatory and compliance landscapes. Navigating diverse legal frameworks, consumer protection laws, and data privacy regulations across multiple countries requires significant investment in legal expertise and technological adaptation, favoring established entities. The ongoing global focus on data handling and cybersecurity in 2024, with evolving regulations, further elevates these entry barriers.

Porter's Five Forces Analysis Data Sources

Our CAR Group Porter's Five Forces analysis is built upon a foundation of robust data, including company annual reports, industry-specific market research, and regulatory filings. This ensures a comprehensive understanding of competitive dynamics.