Banque Cantonale Vaudoise Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Banque Cantonale Vaudoise Bundle

Don't Miss the Bigger Picture

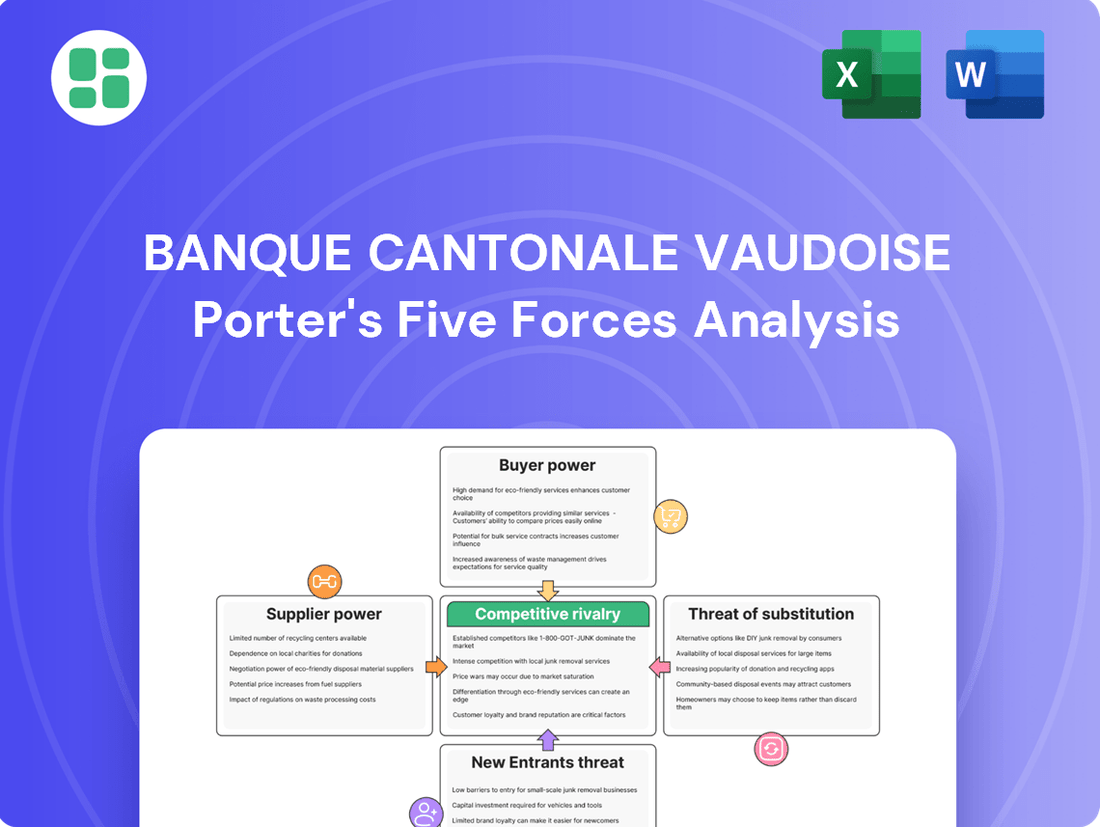

Banque Cantonale Vaudoise navigates a competitive landscape shaped by moderate buyer power and the threat of new entrants, while supplier power and the threat of substitutes present less significant challenges. Understanding these dynamics is crucial for strategic planning.

The complete report reveals the real forces shaping Banque Cantonale Vaudoise’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Technology and Software Providers

Banque Cantonale Vaudoise (BCV) and similar financial institutions depend heavily on technology and software providers for everything from daily operations to advanced digital services. The bargaining power of these suppliers can be significant, particularly for specialized or proprietary systems, due to the high costs and complexities involved in changing vendors. For instance, the integration of new core banking software can cost millions and take years, giving established providers considerable leverage.

The reliance on these providers for critical functions like data security and regulatory compliance means BCV must maintain strong relationships, but also be mindful of potential price increases or service disruptions. While the Swiss fintech scene is growing, offering more options for cloud and specialized solutions, many core systems remain with a few dominant players, keeping their bargaining power elevated in the near to medium term.

Human Capital and Specialized Talent

The banking industry, including institutions like Banque Cantonale Vaudoise (BCV), relies heavily on specialized expertise. Critical areas such as IT, cybersecurity, wealth management, and regulatory compliance demand professionals with advanced skills. The increasing integration of artificial intelligence and digital transformation further amplifies the need for this specialized human capital.

The scarcity of talent in these high-demand fields, particularly in 2024, translates directly into increased bargaining power for employees. This can lead to upward pressure on salaries and intensify the competition among banks to recruit and retain top performers. BCV’s success in attracting and keeping these skilled individuals is therefore a key factor in executing its strategic objectives and maintaining a competitive edge.

Financial Market Data and Analytics Services

For Banque Cantonale Vaudoise (BCV), access to real-time, accurate financial market data and advanced analytics is non-negotiable, underpinning its trading, investment, and risk management functions. Suppliers like Bloomberg and Refinitiv wield moderate power; their services are critical, and switching costs for data integration are substantial. The growing reliance on AI for sophisticated data analysis further solidifies the position of specialized providers in this ecosystem.

Interbank Funding and Capital Markets

Banque Cantonale Vaudoise (BCV), while benefiting from its regional deposit base, also taps into interbank funding and capital markets. The bargaining power of these financial institutions as suppliers of liquidity and capital is significantly shaped by the prevailing interest rate environment and overall market stability. For instance, the Swiss National Bank's (SNB) policy rate cuts, such as the one implemented in March 2024, can reduce funding costs for banks like BCV, thereby lessening the suppliers' leverage.

The ability of BCV to secure funding from other financial institutions is directly tied to market conditions. A stable market with predictable interest rates generally empowers BCV more, as it can negotiate better terms. Conversely, periods of market uncertainty or rising interest rates can increase the bargaining power of suppliers, as they become more selective about where they deploy their capital.

- Interbank Funding Reliance: BCV, like many banks, utilizes interbank markets for short-term liquidity needs, making it susceptible to the pricing power of other banks.

- Capital Markets Access: For longer-term funding, BCV may issue bonds or other debt instruments, where the appetite and pricing from investors (suppliers of capital) influence its costs.

- SNB Policy Impact: The SNB's monetary policy decisions, including the 2024 rate cuts, directly affect the cost of funds in the interbank market, impacting the bargaining power dynamics.

- Market Stability as a Lever: Greater market stability generally reduces the bargaining power of funding suppliers, allowing BCV to negotiate more favorable terms.

Regulatory Compliance and Consulting Services

The complex and evolving Swiss financial regulatory landscape, including new Anti-Money Laundering (AML) frameworks and Basel III standards, creates a significant need for specialized legal and compliance consulting services. These services are essential for banks like Banque Cantonale Vaudoise to navigate stringent requirements and avoid substantial penalties.

Suppliers in this niche, particularly those with profound expertise in Swiss banking law and FINMA (Swiss Financial Market Supervisory Authority) regulations, wield considerable bargaining power. This is due to the critical nature of compliance, where failure can result in severe financial sanctions and reputational damage.

- High Demand for Specialized Expertise: The constant updates to regulations, such as the ongoing implementation of Basel III finalization and evolving AML directives, ensure a sustained demand for highly specialized legal and compliance consultants.

- Cost of Non-Compliance: The financial repercussions of non-compliance are substantial, with fines potentially reaching millions of Swiss Francs, thereby increasing the perceived value and bargaining power of compliant service providers.

- Limited Pool of Qualified Suppliers: The scarcity of consultants with deep, proven experience in Swiss financial regulations means that banks often face limited options, strengthening the negotiating position of these expert suppliers.

Technology Suppliers: High Leverage in Banking

The bargaining power of suppliers for Banque Cantonale Vaudoise (BCV) is a key consideration, particularly concerning technology and specialized services. For instance, core banking software providers often hold significant leverage due to the immense costs and time required for vendor transitions, which can easily run into millions of Swiss Francs and take years to implement.

What is included in the product

This analysis of Banque Cantonale Vaudoise dissects the competitive forces shaping its banking environment, revealing the intensity of rivalry, buyer and supplier power, threat of new entrants, and the impact of substitutes.

Instantly visualize the competitive landscape of the Swiss banking sector with a dynamic Porter's Five Forces model for Banque Cantonale Vaudoise, highlighting key pressures and opportunities.

Customers Bargaining Power

Low Switching Costs for Retail Customers

For basic retail banking services, switching costs for individual customers are relatively low, particularly with the proliferation of digital-first banks and mobile payment solutions in Switzerland. This ease of transition empowers customers, as they can readily compare product offerings and transfer their funds between institutions.

While Banque Cantonale Vaudoise (BCV) enjoys robust regional loyalty within the canton of Vaud, the digital landscape significantly amplifies customer bargaining power. For instance, in 2023, the average number of active bank accounts per capita in Switzerland remained high, indicating a willingness among consumers to engage with multiple financial providers.

The streamlining of digital account opening processes further reduces friction for customers looking to switch banks. This trend, evident across the Swiss banking sector, means that the effort required to move banking relationships is minimal, directly contributing to increased customer leverage.

Price Sensitivity in Standardized Products

Customers for standardized banking products, such as mortgages and savings accounts, often show significant price sensitivity. They actively compare interest rates and fees across various financial institutions, making pricing a key differentiator in these markets. For instance, in 2024, the average mortgage rate in Switzerland hovered around 2.5%, a figure that heavily influences borrower decisions.

While Banque Cantonale Vaudoise (BCV) benefits from a strong regional presence and a dedicated customer base, the highly competitive nature of these standardized products can constrain its pricing power. Without careful consideration, aggressive pricing strategies by competitors could lead to customer attrition, impacting BCV's market share and profitability in these core segments.

Sophistication of Corporate and Institutional Clients

Corporate and institutional clients, such as large corporations and public sector organizations, possess considerable bargaining power. Their sophisticated financial needs and in-house expertise allow them to thoroughly evaluate banking services, compare pricing, and negotiate favorable terms. This sophistication means they can effectively leverage their business volume to secure better deals.

These clients often manage substantial transaction volumes, which makes them attractive to banks. Their ability to spread their banking needs across multiple institutions if unsatisfied with one provider further amplifies their leverage. For instance, a major corporation might consolidate its treasury operations, demanding highly competitive rates and specialized services, thereby influencing the pricing and product offerings of the banks they engage with.

Availability of Diverse Banking Alternatives

The bargaining power of customers for Banque Cantonale Vaudoise (BCV) is significantly influenced by the availability of diverse banking alternatives. Customers can easily switch to major Swiss banks, such as UBS, which now holds a dominant market position after its acquisition of Credit Suisse. Furthermore, other cantonal banks and specialized private banks offer competitive services, increasing customer options.

The burgeoning fintech sector also plays a crucial role, providing innovative digital banking solutions and specialized financial products. This competitive landscape, coupled with increasing customer demand for personalized digital experiences and seamless omnichannel service, allows customers to readily compare offerings and switch to providers that better meet their needs and offer superior value.

- Broad Choice: Customers can choose from large universal banks, other cantonal banks, private banks, and a growing number of fintech companies.

- Competitive Landscape: The Swiss banking market is highly competitive, with numerous players vying for customer loyalty.

- Fintech Disruption: Digital-first fintechs offer specialized services and often lower fees, intensifying pressure on traditional banks.

- Customer Expectations: Evolving demands for digital access, personalized services, and competitive pricing empower customers to seek the best available options.

Demand for Digital and Personalized Services

Customers increasingly expect digital-first banking, demanding seamless online transactions and personalized financial advice. This shift grants them significant bargaining power, as they can easily switch to competitors offering superior digital experiences. For instance, a 2024 report indicated that 75% of banking consumers prefer digital channels for most interactions, highlighting the critical need for banks to adapt.

Banque Cantonale Vaudoise (BCV) recognizes this trend and is actively investing in its digital transformation to meet these evolving customer expectations. Their strategy focuses on enhancing online platforms and mobile applications to provide the convenience and tailored services that modern customers demand.

- Digital Adoption: By mid-2024, over 60% of BCV's customer transactions were conducted through digital channels, demonstrating a strong customer preference for these methods.

- Personalization Efforts: BCV's ongoing digital initiatives aim to leverage data analytics for more personalized product offerings and customer support, directly addressing the demand for tailored services.

- Competitive Landscape: The bank's proactive digital strategy is crucial for retaining customers who have the option to move to fintechs or challenger banks offering highly specialized digital solutions.

Customer Bargaining Power: Rates, Digital, & Diverse Choices

Customers for standardized banking products, such as mortgages and savings accounts, show significant price sensitivity, actively comparing interest rates and fees. For instance, in 2024, the average mortgage rate in Switzerland hovered around 2.5%, a figure that heavily influences borrower decisions. This makes pricing a key differentiator, potentially constraining BCV's pricing power if competitors offer more aggressive terms.

The bargaining power of customers is further amplified by the wide array of banking alternatives available, including major universal banks like UBS, other cantonal banks, private banks, and a growing number of fintech companies. For example, by mid-2024, over 60% of BCV's customer transactions were conducted through digital channels, indicating a strong preference for digital solutions that fintechs often excel at providing.

| Factor | Impact on Customer Bargaining Power | Example/Data Point (2024) |

|---|---|---|

| Switching Costs | Low for retail customers due to digital ease | Digital account opening processes are streamlined |

| Availability of Alternatives | High, increasing customer options | Presence of UBS, cantonal banks, private banks, and fintechs |

| Price Sensitivity | Significant for standardized products | Average mortgage rates around 2.5% |

| Digital Preferences | Growing demand for digital-first banking | Over 60% of BCV transactions via digital channels (mid-2024) |

What You See Is What You Get

Banque Cantonale Vaudoise Porter's Five Forces Analysis

This preview showcases the comprehensive Porter's Five Forces analysis for Banque Cantonale Vaudoise, offering a detailed examination of competitive rivalry, the bargaining power of buyers and suppliers, the threat of new entrants, and the threat of substitute products. The document displayed here is the exact, fully formatted analysis you’ll receive immediately after purchase, providing actionable insights without any placeholders or surprises.

Rivalry Among Competitors

Presence of Major Swiss Banks

The Swiss banking landscape is heavily influenced by major players like UBS, especially after its acquisition of Credit Suisse. These giants operate across all financial services, from wealth management to corporate finance, presenting a formidable competitive force for regional banks such as BCV.

UBS, with its vast resources and global presence, competes directly with BCV even in its core cantonal markets. This intense rivalry means BCV must constantly innovate and differentiate to maintain its market share against these larger, more diversified competitors.

Competition from Other Cantonal and Regional Banks

Banque Cantonale Vaudoise (BCV) contends with significant rivalry from other cantonal and regional banks across Switzerland. These institutions, often operating under similar public law frameworks and possessing a strong regional orientation, directly vie for retail and small to medium-sized enterprise (SME) clients, especially in cantons adjacent to Vaud or within its own territory. This shared characteristic intensifies the battle for local market dominance and customer retention.

Increasing Digitalization and Fintech Innovation

The Swiss banking sector is experiencing a significant surge in digitalization and fintech innovation. Established players like Banque Cantonale Vaudoise are investing heavily in digital transformation, while agile fintech startups are rapidly introducing new solutions. This dynamic environment, fueled by advancements in AI and blockchain, intensifies competitive rivalry.

This increased digitalization allows both new and existing competitors to challenge traditional banking models. Fintechs are particularly adept at offering streamlined digital payment solutions and personalized services, often at more competitive price points. For instance, in 2024, the adoption of digital banking services in Switzerland continued its upward trajectory, with a notable increase in mobile banking transactions and the use of digital wallets, directly impacting how customers interact with financial institutions.

Interest Rate Environment and Margin Pressure

The interest rate environment significantly impacts competitive rivalry among banks. For instance, the Swiss National Bank (SNB) implemented rate cuts in March and June 2024, with further reductions anticipated. This shift from a higher rate regime can compress net interest margins, a primary income source for many financial institutions.

This margin pressure forces banks like Banque Cantonale Vaudoise to intensify their focus on operational efficiency and explore diverse revenue streams beyond traditional lending. The pursuit of profitability in a lower-rate environment naturally heightens competition as banks seek to attract and retain customers and market share.

- SNB Rate Cuts: The SNB cut its policy rate by 25 basis points in March 2024 and again in June 2024, signaling a shift in the interest rate landscape.

- Margin Compression: Lower interest rates directly reduce the spread banks earn on loans and deposits, putting pressure on profitability.

- Focus on Efficiency: Banks are compelled to streamline operations and reduce costs to maintain margins in this environment.

- Revenue Diversification: Fee-based income from wealth management, advisory services, and other non-interest sources becomes increasingly crucial.

Consolidation and Strategic Repositioning

The Swiss private banking landscape has experienced a degree of consolidation, with notable merger and acquisition (M&A) activities shaping the competitive arena. This trend, coupled with broader structural shifts across the financial industry, compels institutions like Banque Cantonale Vaudoise (BCV) to constantly refine their strategies. Banks are actively reassessing their business models, prioritizing technological advancements, and honing in on their core competencies to secure a competitive edge and sustain profitability.

For instance, in 2023, the Swiss banking sector saw several M&A deals, reflecting this ongoing consolidation. These moves are driven by the need to achieve economies of scale, expand market share, and adapt to evolving client demands and regulatory landscapes. Banks that successfully navigate these changes by investing in digital transformation and focusing on specialized services are better positioned for long-term success.

- M&A Activity: The Swiss banking sector has witnessed several significant M&A transactions in recent years, indicating a trend towards consolidation.

- Technological Investment: Banks are increasing their spending on digital transformation initiatives to enhance customer experience and operational efficiency. For example, many Swiss banks reported double-digit percentage increases in IT spending in 2023.

- Focus on Core Strengths: Institutions are strategically repositioning themselves by concentrating on their most profitable business lines and client segments.

- Profitability Pressures: The competitive environment necessitates a continuous focus on cost management and revenue generation to maintain healthy profit margins amidst evolving market conditions.

Swiss Banking: Intense Rivalry and Digital Disruption

The competitive rivalry within the Swiss banking sector is intense, characterized by the dominance of large national players like UBS, which significantly impacts regional banks such as BCV. This rivalry is further amplified by ongoing digitalization and the emergence of agile fintech companies, forcing established institutions to innovate and invest heavily in technology to remain competitive.

The interest rate environment, with recent cuts by the Swiss National Bank in 2024, compresses net interest margins, compelling banks like BCV to prioritize operational efficiency and revenue diversification. Consolidation trends, evidenced by M&A activity in the Swiss banking sector in 2023, also intensify competition as institutions seek scale and market share.

| Competitor | Market Share (Est.) | Key Strengths | BCV Impact |

|---|---|---|---|

| UBS | Significant (Post-Credit Suisse Acquisition) | Global reach, diversified services, strong capital | Direct competition across all segments, pressure on pricing and innovation |

| Other Cantonal/Regional Banks | Varies by canton | Local expertise, strong regional ties | Intense competition for retail and SME clients within Vaud and adjacent cantons |

| Fintech Companies | Growing rapidly | Digital agility, specialized offerings, lower cost structures | Disruption of traditional services, pressure to enhance digital offerings |

SSubstitutes Threaten

Fintech and Neobank Alternatives

The increasing prevalence of fintech and neobanks presents a substantial threat of substitutes for traditional banking institutions like Banque Cantonale Vaudoise. These digital-first entities offer streamlined services such as mobile payments, automated investment advice, and peer-to-peer lending, often at lower costs and with superior user interfaces.

For instance, the global fintech market size was valued at over $2.4 trillion in 2023 and is projected to grow significantly. Neobanks, in particular, have attracted millions of customers, especially younger demographics, by providing convenient, app-based banking experiences that bypass the need for physical branches and traditional account structures.

Direct Investment Platforms and Crowdfunding

The rise of direct investment platforms and crowdfunding presents a significant threat of substitutes for traditional banking services. Customers can now bypass banks for investment and lending, accessing financial markets directly through online brokerages or participating in crowdfunding campaigns. For instance, the global crowdfunding market was projected to reach over $200 billion by 2024, demonstrating a substantial shift in how individuals and businesses access capital, directly challenging banks' traditional roles.

Cryptocurrencies and Digital Assets

The rise of cryptocurrencies and digital assets presents a growing threat of substitution for traditional banking services. As more individuals and institutions explore these alternatives for storing, transferring, and investing value, they bypass conventional financial intermediaries. Switzerland, with its established 'Crypto Valley', is a prime example where this trend is particularly pronounced, indicating a tangible shift in financial behavior.

Non-Bank Wealth Management Firms

Independent wealth management firms and asset management companies present a significant threat of substitution to Banque Cantonale Vaudoise's (BCV) offerings. These entities, operating outside the traditional banking structure, specialize in tailored investment advice and sophisticated portfolio management.

Clients may opt for these specialized firms if they perceive them as providing deeper expertise or a more personalized client experience than a large bank can offer. For instance, in 2024, the independent advisory sector continued to grow, with many firms focusing on niche markets or specific investment strategies that might appeal to BCV's affluent client base.

- Specialized Expertise: Independent firms often cultivate deep knowledge in specific asset classes or investment philosophies, attracting clients seeking this focused approach.

- Personalized Service: A key differentiator is the potential for more direct and individualized attention from senior advisors, a factor highly valued by high-net-worth individuals.

- Fee Structures: Some independent advisors may offer alternative fee arrangements that clients find more transparent or competitive compared to bank-affiliated wealth management services.

- Agility and Innovation: These firms can sometimes be more nimble in adopting new investment technologies or strategies, appealing to clients looking for cutting-edge solutions.

Internal Corporate Finance Solutions

Larger corporations increasingly leverage internal treasury functions for sophisticated financial needs, bypassing traditional banking channels. For instance, in 2024, a significant portion of large enterprises managed their cash and liquidity internally, reducing reliance on external financial institutions for day-to-day operations.

Direct debt issuance in public markets or private placements offers an alternative to bank loans for significant capital raising. In the first half of 2024, corporate bond issuance remained robust, providing companies with substantial funding avenues independent of corporate finance advisory services from banks like BCV.

This trend of internalized financial management and direct access to capital markets acts as a potent substitute for the corporate finance solutions typically offered by banks. It diminishes the necessity for external advisory and execution services for many large-cap companies.

- Internal Treasury Management: Companies increasingly manage their own cash, investments, and risk.

- Direct Debt Issuance: Access to capital markets through bond sales bypasses traditional bank lending.

- Private Placements: Direct negotiation of debt with investors offers an alternative to bank-facilitated deals.

- Reduced Dependence: Sophisticated firms can execute complex financial operations internally, lessening reliance on external corporate finance providers.

Digital Tools Challenge Traditional Wealth Management

The increasing accessibility of do-it-yourself investment platforms and robo-advisors poses a significant threat of substitution for traditional wealth management services. These digital tools democratize investment, offering automated portfolio management and financial planning at a fraction of the cost of human advisors.

For instance, the robo-advisory market globally saw substantial growth, with assets under management projected to surpass $3 trillion by 2025, indicating a clear shift towards automated financial solutions. This trend directly challenges the value proposition of human-centric advisory services offered by institutions like Banque Cantonale Vaudoise.

Furthermore, the proliferation of financial education content and readily available market data empowers individuals to manage their finances more independently. This self-sufficiency reduces the perceived need for traditional banking and advisory relationships for many clients.

| Substitute Type | Key Characteristics | Impact on Traditional Banks | Example Data (2024) |

|---|---|---|---|

| Fintech & Neobanks | Digital-first, lower fees, user-friendly interfaces | Customer attrition, reduced transaction revenue | Global fintech market valued over $2.4 trillion in 2023, projected growth. |

| Direct Investment Platforms | Bypass intermediaries for investing and lending | Loss of brokerage and lending fees | Global crowdfunding market projected over $200 billion by 2024. |

| Cryptocurrencies & Digital Assets | Decentralized value transfer and storage | Disintermediation of payment and store-of-value functions | Switzerland's 'Crypto Valley' demonstrates significant adoption. |

| Independent Wealth Managers | Specialized expertise, personalized service | Competition for high-net-worth clients, potential fee compression | Independent advisory sector continued growth in 2024. |

| DIY Investment & Robo-Advisors | Automated, low-cost portfolio management | Erosion of traditional advisory fees, shift in client expectations | Robo-advisory AUM projected to exceed $3 trillion by 2025. |

Entrants Threaten

High Regulatory and Capital Requirements

Switzerland's banking sector is heavily protected by rigorous regulations. For instance, Basel III standards, fully implemented by January 2025, mandate high capital adequacy ratios, meaning new banks need substantial financial backing to even begin operations. FINMA, the Swiss Financial Market Supervisory Authority, also enforces strict licensing, making it a costly and complex process.

Established Brand Reputation and Customer Trust

Banque Cantonale Vaudoise (BCV) benefits from a deep-rooted history and significant regional trust as a public law institution in the canton of Vaud. This established brand reputation and customer loyalty present a formidable barrier for new entrants aiming to penetrate the Swiss banking sector. In 2024, BCV continued to leverage this trust, reporting a solid financial performance with net income of CHF 274 million for the first half of the year, underscoring the stability associated with its long-standing presence.

Need for Extensive Distribution Networks

The significant capital investment required to build and maintain an extensive branch network, akin to Banque Cantonale Vaudoise's established presence, presents a substantial hurdle for new entrants. This need for physical infrastructure and localized customer service, which BCV excels at, acts as a strong deterrent for traditional banking competitors aiming to enter the market. For instance, establishing a branch can cost hundreds of thousands, if not millions, of Swiss Francs, making it a prohibitive expense for many new players.

Technological Investment and Infrastructure Scale

The banking sector demands massive upfront investment in sophisticated IT systems, cybersecurity, and digital platforms, creating a significant barrier for new entrants. Keeping pace with evolving technologies like artificial intelligence and advanced data analytics requires continuous and substantial capital expenditure, making it difficult for newcomers to compete with established players who have already made these investments.

For instance, in 2024, the global banking sector's spending on IT is projected to reach hundreds of billions of dollars, with a significant portion allocated to digital transformation and cybersecurity. New entrants must not only match this scale but also demonstrate a clear technological advantage to attract customers.

- High Upfront Costs: Building secure and scalable digital banking infrastructure can cost tens to hundreds of millions of dollars.

- Cybersecurity Investment: Banks are investing billions annually in cybersecurity to protect sensitive data, a cost new entrants must absorb.

- Technological Obsolescence: The rapid pace of technological change necessitates ongoing investment to avoid falling behind.

Customer Acquisition Costs and Loyalty

In a mature banking market like Switzerland, where BCV enjoys strong regional loyalty and high recommendation rates, the cost of acquiring new customers is substantial. New entrants must contend with significant customer inertia, often necessitating aggressive pricing strategies or truly groundbreaking products to gain traction.

For instance, the average customer acquisition cost (CAC) in the financial services sector can be quite high, often ranging from several hundred to over a thousand Swiss Francs per customer, depending on the acquisition channel and the value of the customer relationship. BCV's established reputation and deep community ties in Vaud mean that potential new competitors face an uphill battle in convincing customers to switch.

- High Customer Acquisition Costs: Acquiring a new banking customer in Switzerland can cost hundreds to over a thousand Swiss Francs.

- Established Loyalty: BCV benefits from strong regional loyalty and high customer recommendation rates, making it difficult for new entrants to attract customers.

- Barriers to Entry: New banks must overcome customer inertia and invest heavily in marketing or product innovation to compete effectively.

- Competitive Landscape: The presence of established, trusted institutions like BCV creates a significant barrier for new players seeking market share.

Regulatory Walls & Trust Shield BCV from New Entrants

The threat of new entrants for Banque Cantonale Vaudoise (BCV) is significantly mitigated by Switzerland's stringent regulatory environment and the substantial capital required to operate. FINMA's licensing process and Basel III capital requirements, in full effect by early 2025, demand considerable financial resources, making it difficult for newcomers to enter. Furthermore, BCV's established brand, deep regional trust, and extensive physical network in Vaud act as powerful deterrents, as new entrants face high customer acquisition costs and significant inertia to overcome.

| Factor | Impact on New Entrants | BCV Advantage |

|---|---|---|

| Regulatory Hurdles | High (Licensing, Capital Requirements) | Established compliance and financial strength |

| Capital Investment | Very High (IT, Infrastructure) | Existing, depreciated assets and ongoing investment capacity |

| Brand & Trust | Low (Requires building from scratch) | Deep regional loyalty and high recommendation rates |

| Customer Acquisition Cost | High (CHF hundreds to over CHF 1000 per customer) | Leverages existing customer base and community ties |

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis for Banque Cantonale Vaudoise is built upon a foundation of reliable data, including the bank's official annual reports, industry-specific publications from Swiss financial authorities, and macroeconomic data from reputable sources like the Swiss National Bank.