Bank Central Asia Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Bank Central Asia Bundle

A Must-Have Tool for Decision-Makers

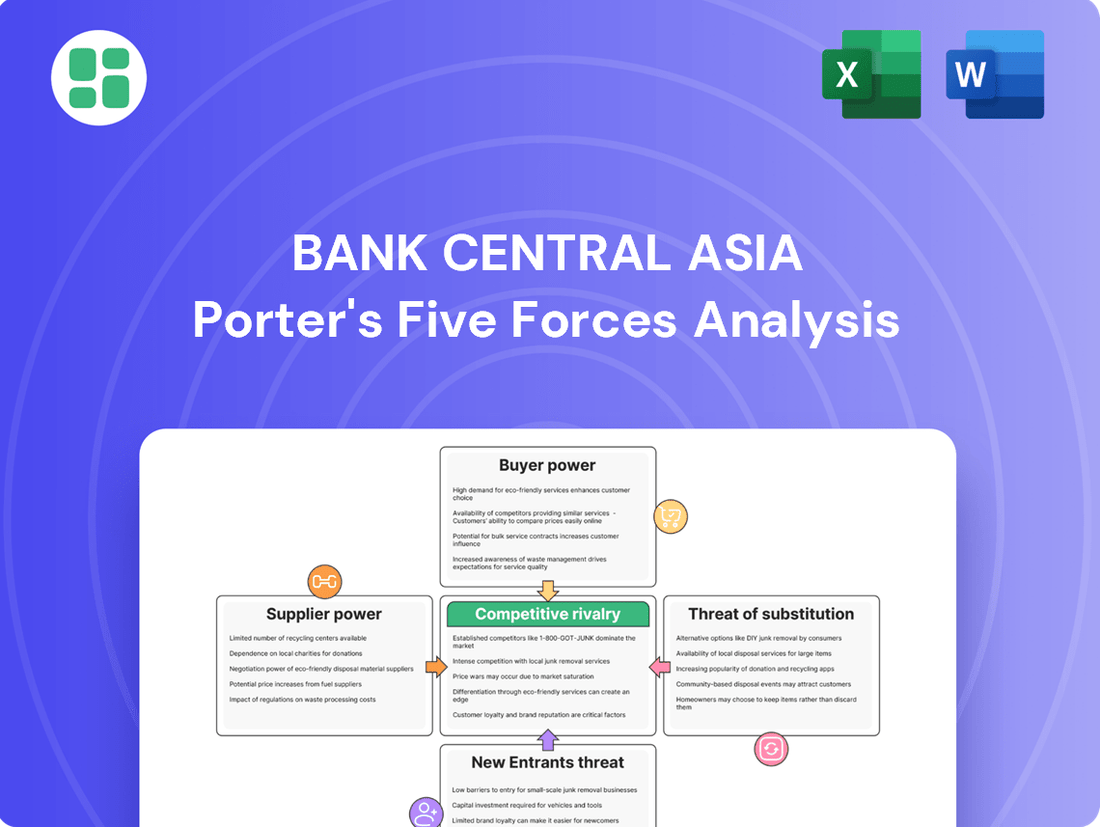

Bank Central Asia navigates a dynamic financial landscape, facing intense competition and evolving customer expectations. Understanding the interplay of industry rivalry, buyer power, and the threat of new entrants is crucial for sustained success.

The complete report reveals the real forces shaping Bank Central Asia’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Concentrated Funding Sources

Concentrated funding sources significantly amplify supplier bargaining power in the Indonesian banking sector. Tight liquidity means banks are highly dependent on a limited pool of depositors, especially for stable, low-cost current and savings accounts (CASA). This reliance gives these depositors more leverage in demanding better terms.

The Indonesian banking industry's high loan-to-deposit ratio (LDR) underscores this dependence; for instance, in early 2024, many Indonesian banks operated with LDRs exceeding 90%, indicating a strong need for deposit funding. Furthermore, the central bank’s monetary policy, including its management of interest rates and the Rupiah, directly influences the cost of these essential funds, effectively positioning the central bank as a powerful supplier.

Increasing Reliance on Technology Providers

Bank Central Asia's increasing reliance on technology providers for digital transformation, including software and cybersecurity, strengthens the bargaining power of these suppliers. As Indonesian banks, including BCA, push for advanced digital services, they require specialized tech solutions, fostering a market where key providers can exert more influence. This dependency highlights the need for strategic partnerships to ensure continued innovation and competitive digital offerings.

Skilled Human Capital Demand

The banking sector's swift move towards digitalization has significantly amplified the demand for specialized talent. This is particularly true in fields such as data analytics, cybersecurity, and the development of digital banking platforms. For instance, in 2024, the global demand for cybersecurity professionals was projected to outpace supply by a considerable margin, impacting recruitment costs across industries, including banking.

This heightened need for digitally adept professionals grants them substantial bargaining power. Banks like Bank Central Asia (BCA) face increased costs for attracting and retaining individuals possessing these in-demand skills. The industry-wide emphasis on digital transformation directly fuels this trend, making skilled human capital a critical factor in competitive advantage.

Interbank Market Dynamics

The interbank lending market is a crucial source of short-term funds for banks, including Bank Central Asia (BCA). When system-wide liquidity is scarce, banks holding excess funds gain significant leverage, driving up borrowing costs for those in need. This directly impacts BCA's treasury management and its overall cost of funding.

In 2024, interbank rates, such as the Jakarta Interbank Offered Rate (JIBOR), reflect the prevailing liquidity conditions. For instance, if JIBOR experiences an upward trend due to tighter liquidity, it signifies increased bargaining power for suppliers of funds in this market, potentially raising BCA's operational expenses.

- Interbank Market as Supplier: Banks with surplus liquidity act as key suppliers in the interbank market, providing essential short-term funding.

- Liquidity Impact on Power: Tight liquidity conditions amplify the bargaining power of these surplus-holding banks, leading to higher borrowing costs.

- BCA's Exposure: BCA's treasury operations and funding costs are directly influenced by these interbank market dynamics.

- 2024 Data Indicator: Trends in interbank rates like JIBOR in 2024 would provide concrete evidence of supplier power shifts.

Regulatory Compliance and Service Providers

Suppliers of regulatory compliance, auditing, and legal services wield considerable influence over Bank Central Asia (BCA). This is largely due to Indonesia's intricate and constantly shifting financial regulations. For instance, the Financial Services Authority (OJK) frequently introduces new rules, such as those impacting financial reporting standards and the adoption of technological innovations. Banks like BCA must strictly adhere to these mandates, making specialized compliance services essential for navigating these requirements. Failing to comply can result in significant financial penalties, underscoring the critical role these service providers play in ensuring BCA's operational integrity.

The bargaining power of these suppliers is further amplified by the specialized knowledge and certifications they possess. For example, in 2024, the OJK continued to emphasize robust cybersecurity measures and data privacy, requiring banks to engage with IT security consultants and legal experts with deep understanding in these niche areas. The cost and complexity of obtaining and maintaining these expertise internally often makes outsourcing to specialized firms a more practical and cost-effective solution for BCA, thereby increasing supplier leverage.

- High demand for specialized compliance expertise: Banks require services for adhering to OJK regulations on financial reporting, risk management, and digital banking.

- Risk of penalties for non-compliance: Significant fines and reputational damage incentivize banks to engage with reputable compliance service providers.

- Limited number of qualified providers: The specialized nature of regulatory compliance creates a concentrated market for these services.

- Increasing regulatory complexity: New regulations, such as those related to data protection and anti-money laundering, further enhance supplier power.

Tech Suppliers Hold Sway Over Bank Digital Future

Suppliers of essential banking technology, particularly those providing core banking systems and advanced digital platforms, hold significant bargaining power over Bank Central Asia (BCA). The increasing reliance on sophisticated IT infrastructure for competitive advantage means banks are heavily dependent on these specialized vendors. This dependency is amplified by the high switching costs associated with changing core systems, giving established tech providers considerable leverage.

In 2024, the demand for cloud-based solutions and AI-driven analytics in banking continued to surge, creating a concentrated market for providers offering these cutting-edge technologies. For instance, global IT spending by banks was projected to grow, with a significant portion allocated to digital transformation initiatives, highlighting the critical role of these technology suppliers.

The bargaining power of these technology suppliers is further solidified by the need for ongoing support, maintenance, and upgrades to ensure system security and operational efficiency. BCA's commitment to digital innovation necessitates strong partnerships with these vendors, who can dictate terms due to their specialized knowledge and the critical nature of their services.

| Supplier Type | Bargaining Power Driver | Impact on BCA | 2024 Trend Example |

|---|---|---|---|

| Core Banking System Providers | High switching costs, specialized expertise | Increased dependency, potential for higher licensing/support fees | Continued demand for modernizing legacy systems |

| Digital Platform Vendors (e.g., AI, Cloud) | Rapid technological advancement, limited top-tier providers | Leverage in negotiating service level agreements and pricing | Growth in cloud adoption for banking services |

| Cybersecurity Solution Providers | Increasing cyber threats, regulatory mandates | Essential for compliance and risk management, influencing vendor selection and costs | Heightened focus on data protection and threat intelligence |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored exclusively to Bank Central Asia's operational environment.

Instantly visualize the competitive landscape for Bank Central Asia, highlighting key pressures from rivals and new entrants to inform strategic responses.

Customers Bargaining Power

High Customer Loyalty and Sticky CASA Deposits

Bank Central Asia (BCA) enjoys robust customer loyalty, evidenced by its strong current and savings account (CASA) ratio. This high proportion of low-cost deposits signifies that customers are less likely to move their funds, a testament to their deep-rooted relationship with the bank and its efficient transaction banking services. For instance, as of the first quarter of 2024, BCA's CASA ratio stood at an impressive 77.8%, a key indicator of its stable funding base and a significant advantage in managing funding costs.

BCA further solidifies customer loyalty through its premium banking segments, Solitaire and Prioritas. These offerings provide high-net-worth individuals with tailored services and exclusive benefits, creating a "sticky" customer base. This personalized approach makes these affluent clients less susceptible to competitive offers, thereby reducing the bargaining power of this customer segment.

Increased Digital Options and Lower Switching Costs

The surge in digital banking platforms and fintech innovations across Indonesia has significantly boosted customer bargaining power. With more convenient and cost-effective alternatives readily available, customers face fewer hurdles when considering switching providers. This increased accessibility to services from neobanks and e-wallets, in addition to established players like Bank Central Asia (BCA), intensifies competition.

For instance, the number of digital banks operating in Indonesia has grown substantially, offering specialized services that cater to diverse customer needs. In 2024, digital transactions through mobile banking and internet banking channels continued to see robust growth, reflecting a clear shift in consumer preference towards digital channels. This trend allows customers to easily compare offerings and move their funds, putting pressure on traditional banks to maintain competitive pricing and service quality.

Greater Information Transparency

Digital platforms and financial comparison tools have significantly boosted customer knowledge about banking products. For instance, in 2024, a significant portion of consumers actively used online resources to compare loan rates and account fees before making decisions.

This increased transparency empowers customers by making it easier to identify and switch to institutions offering superior value. As a result, banks like Bank Central Asia face pressure to remain competitive on pricing and service quality to retain their customer base.

Price Sensitivity in Mass Market Segments

In mass-market segments, especially for straightforward banking products like loans and basic accounts, customers often prioritize price. This means banks, including Bank Central Asia (BCA), face significant pressure to offer competitive rates to attract and keep clients. For instance, in 2023, the average interest rate for a personal loan in Indonesia hovered around 10-12%, a key benchmark for price-sensitive consumers.

- High Price Sensitivity: Mass-market customers are more likely to switch providers based on minor price differences for standard banking services.

- Competitive Pricing: BCA needs to balance its premium brand image with competitive pricing, particularly in product categories with less perceived differentiation.

- Impact on Market Share: Intense price competition can directly affect a bank's ability to gain or maintain market share in these high-volume segments.

- BCA's Brand Advantage: Despite price sensitivity, BCA's strong brand reputation and service quality provide a buffer, allowing it to retain a loyal customer base even when not always offering the absolute lowest price.

Influence of Tech-Savvy Generations

The growing influence of tech-savvy generations, particularly Gen Z and Millennials, is a significant factor in the bargaining power of customers for banks like Bank Central Asia (BCA). These demographics expect digital-first, seamless, and flexible banking experiences, pushing banks to prioritize innovation in their online and mobile platforms. For instance, in 2024, a significant portion of banking transactions are conducted digitally, with mobile banking apps becoming the primary channel for many users.

This shift means customers have considerable sway over how products are developed and services are delivered. Their preference for integrated digital services and mobile-first solutions compels banks to continuously upgrade their offerings to remain competitive. A report from early 2024 indicated that over 70% of Gen Z consumers prefer digital channels for their banking needs, directly impacting how BCA must design its services to attract and retain this crucial demographic.

- Digital Adoption: Gen Z and digitally native customers prioritize mobile and online banking, demanding intuitive and secure digital experiences.

- Service Expectations: These customer segments expect seamless integration of financial services and flexible access, influencing bank product roadmaps.

- Innovation Pressure: Banks must constantly innovate their digital offerings to meet the evolving demands of tech-savvy customers, increasing customer bargaining power.

- Market Trends: By 2024, a substantial percentage of banking transactions are digital, underscoring the power of customers who prefer and utilize these channels.

Customer Power: Digital Demands & Price Pressure in Banking

The bargaining power of customers for Bank Central Asia (BCA) is influenced by several factors, including price sensitivity in mass-market segments and the increasing demand for digital services from younger demographics. While BCA's strong brand and premium offerings create loyalty in certain segments, the broader market benefits from greater transparency and more readily available alternatives.

| Factor | Impact on BCA | Example/Data (2023-2024) |

|---|---|---|

| Digitalization & Fintech | Increases customer ability to switch providers easily. | Digital transactions grew significantly in 2024, with many consumers comparing rates online. |

| Price Sensitivity (Mass Market) | Pressures BCA to offer competitive rates on standard products. | Personal loan rates in Indonesia averaged 10-12% in 2023, a key benchmark. |

| Tech-Savvy Generations (Gen Z/Millennials) | Drives demand for innovative, seamless digital banking experiences. | Over 70% of Gen Z preferred digital channels for banking in early 2024. |

| Brand Loyalty (Premium Segments) | Mitigates bargaining power for high-net-worth individuals. | Solitaire and Prioritas segments benefit from tailored services, reducing switching likelihood. |

Full Version Awaits

Bank Central Asia Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. It delves into Bank Central Asia's competitive landscape through Porter's Five Forces, analyzing the bargaining power of buyers and suppliers, the threat of new entrants and substitutes, and the intensity of rivalry within the Indonesian banking sector. This comprehensive assessment provides actionable insights into the strategic positioning and future outlook of Bank Central Asia.

Rivalry Among Competitors

Dominance of Major Banks

The Indonesian banking landscape is dominated by a few major players, creating fierce competition. For instance, as of the first quarter of 2024, state-owned giants like Bank Mandiri, BRI, and BNI, along with private leader BCA, collectively managed trillions of Indonesian Rupiah in assets, underscoring their significant market control.

This concentration means intense rivalry for both customer deposits and loan opportunities. These large banks often leverage their extensive branch networks and brand recognition to attract and retain customers, pushing smaller institutions to innovate or focus on niche markets.

Intensifying Competition for Deposits and Lending

Despite predictions of a less aggressive lending environment in 2025 due to elevated funding expenses, the banking industry is grappling with a pervasive liquidity squeeze. This scarcity of funds is heating up the competition for stable, low-cost deposits, a critical resource for banks.

Banks are increasingly cautious about extending credit, with many becoming more discerning about loan applications. This heightened selectivity stems from growing concerns about potential increases in non-performing loans (NPLs) within specific market segments. For instance, in 2024, Indonesian banks saw their NPL ratios hover around 2.4%, a slight increase from the previous year, prompting a focus on asset quality.

This shift in lending strategy suggests a potential recalibration of competitive forces. Instead of solely pursuing loan volume, banks may find themselves vying for market share based on superior asset quality and operational efficiency, aiming to manage risk effectively amidst economic uncertainties.

Rapid Digitalization and Fintech Integration

Traditional banks like Bank Central Asia (BCA) are in an intense competition to digitize their offerings and incorporate fintech. This is driven by the need to keep pace with nimble digital-only banks and innovative fintech startups. For instance, in 2024, many established banks, including BCA, continued to heavily invest in upgrading their mobile banking apps and expanding their digital payment ecosystems to attract and retain customers in this rapidly evolving landscape.

Product and Service Differentiation

Banks are increasingly differentiating their offerings to capture market share. BCA, for example, highlights its robust transaction banking capabilities and tailored services for its affluent customer base, alongside a strong push in digital advancements. This focus on unique value propositions helps in customer retention and acquisition.

The competitive landscape compels banks to move beyond standard financial products. BCA's strategy emphasizes providing a complete range of interconnected financial solutions, which serves as a significant differentiator in the crowded banking sector. This integrated approach aims to foster deeper customer relationships.

- BCA's Digital Focus: In 2024, BCA reported a substantial increase in digital transactions, reflecting its success in product differentiation through technology.

- Personalized Banking: The bank's premium segment continues to grow, demonstrating the effectiveness of personalized services in attracting and retaining high-value clients.

- Integrated Solutions: BCA's ability to offer a seamless experience across various financial products, from savings to investments and loans, is a key factor in its competitive edge.

Regulatory Environment and Market Stability

The Indonesian Financial Services Authority (OJK) is a key player, setting rules that impact competition. In 2024, the OJK continued its focus on digital banking regulations, aiming to boost financial inclusion while ensuring stability. These regulations can act as a hurdle for new entrants, but they also foster a more structured and fair competitive environment for established players like Bank Central Asia (BCA).

BCA's strategies are significantly influenced by the OJK's directives, which promote healthy competition and digital innovation. For instance, the OJK's push for increased digital transactions in 2024, with a target of 90% of all transactions being digital by year-end, directly shapes how banks like BCA invest in technology and customer service. This regulatory framework ensures that while competition exists, it's within a managed and stable market.

- OJK's role in financial stability: The OJK actively monitors and regulates the banking sector to prevent systemic risks, a crucial aspect of market stability in Indonesia.

- Digital transformation push: Regulations encourage banks to adopt digital technologies, impacting operational costs and customer engagement strategies.

- Barriers to entry: While promoting competition, regulatory compliance can create significant barriers for new banks seeking to enter the market.

- Level playing field: OJK regulations aim to ensure fair competition, preventing monopolistic practices and promoting innovation among all financial institutions.

Indonesia's Banking Battle: Digital Dominance and Deposit Scarcity

Competitive rivalry in Indonesia's banking sector is intense, driven by a few dominant state-owned banks and private leaders like BCA, which collectively held trillions in assets by Q1 2024. This concentration fuels aggressive competition for deposits and loans, pushing banks to innovate and differentiate their offerings. The scarcity of funds in 2025 further intensifies this rivalry, particularly for low-cost deposits, as banks become more selective in lending due to concerns about rising non-performing loans, which stood at approximately 2.4% in 2024.

Banks are actively digitizing to compete with fintech, with BCA heavily investing in its mobile banking and payment systems in 2024. This digital push, alongside personalized banking for premium clients and integrated financial solutions, serves as key differentiators. For instance, BCA saw a substantial increase in digital transactions in 2024, underscoring the success of its technology-driven product differentiation.

| Bank | Asset Size (IDR Trillions, Q1 2024 est.) | Digital Transaction Growth (2024 est.) | NPL Ratio (2024 est.) |

|---|---|---|---|

| Bank Mandiri | 1,300+ | Significant increase | ~2.3% |

| BRI | 1,200+ | Significant increase | ~2.5% |

| BNI | 1,100+ | Significant increase | ~2.4% |

| BCA | 1,000+ | Substantial increase | ~1.2% |

SSubstitutes Threaten

Proliferation of Fintech Solutions

The most significant threat of substitutes for Bank Central Asia (BCA) stems from the rapidly expanding fintech sector in Indonesia. These innovative companies provide a diverse range of financial services that can directly compete with traditional banking functions, often at a lower cost or with greater convenience.

Digital payment platforms like GoPay and OVO have gained immense traction, allowing consumers to conduct transactions without relying on bank accounts or traditional payment networks. Furthermore, peer-to-peer (P2P) lending platforms and buy now pay later (BNPL) services offer alternative avenues for credit and financing, bypassing bank loan processes entirely.

In 2023, the digital payment market in Indonesia saw substantial growth, with transaction volumes soaring. For instance, GoPay reported a significant increase in its user base and transaction frequency, reflecting a growing preference for digital wallets. Similarly, BNPL services have become increasingly popular, with several fintech players reporting millions of transactions, indicating a clear shift in consumer behavior away from traditional credit facilities.

Robo-advisors also present a substitute for wealth management services, offering automated investment advice and portfolio management that can be more accessible and affordable than traditional advisory services. This proliferation of fintech solutions directly challenges BCA's market share by offering specialized, user-friendly alternatives for various financial needs.

Rise of E-Wallets and Digital Payments

The rise of e-wallets and digital payment platforms presents a significant threat of substitutes for traditional banking services. These platforms, like GoPay and OVO in Indonesia, have experienced substantial user growth, with GoPay alone reporting over 170 million transactions in Q1 2024. This shift directly challenges banks' revenue from transaction fees and interest income on deposited funds, as consumers increasingly opt for the convenience and speed of digital wallets for everyday purchases.

Direct Capital Market Investments

Customers, especially those with substantial savings, might opt for direct investments in capital market instruments like government bonds (SBN) over conventional bank deposits, particularly when bond yields present a more appealing return. This trend directly siphons funds away from bank deposit bases, consequently affecting a bank's liquidity and its overall funding structure.

Emergence of Digital-Only Banks

The rise of digital-only banks, or neobanks, presents a significant threat of substitutes for traditional banks like Bank Central Asia (BCA). These new players offer entirely online banking experiences, often with lower fees and more intuitive digital interfaces, which are particularly appealing to younger, tech-savvy demographics such as Gen Z.

These neobanks directly challenge the established branch-based models of incumbent banks. For instance, by early 2024, several neobanks in Southeast Asia had already captured millions of users, demonstrating their ability to attract customers seeking convenience and cost-effectiveness. This competitive pressure forces traditional banks to accelerate their own digital transformation efforts to remain relevant.

- Neobanks Offer Lower Fees: Many digital-only banks operate with significantly reduced overhead compared to traditional banks, allowing them to pass these savings onto customers through lower transaction fees or even fee-free services.

- Enhanced User Experience: Neobanks prioritize user-friendly mobile apps and online platforms, providing a seamless and intuitive banking experience that appeals to digitally native consumers.

- Targeting Underserved Segments: Some neobanks focus on specific market segments, such as small businesses or freelancers, offering tailored financial products and services that traditional banks may not adequately address.

- Agility and Innovation: Their lean structures enable neobanks to adapt quickly to market changes and introduce innovative features and services at a faster pace than larger, more established institutions.

Alternative Lending and Crowdfunding Platforms

Alternative lending and crowdfunding platforms present a significant threat of substitutes to traditional bank loans for Bank Central Asia (BCA). These platforms, such as peer-to-peer (P2P) lending and crowdfunding initiatives, offer accessible financing for individuals and small to medium-sized enterprises (MSMEs) often overlooked by conventional banks.

These alternatives can provide faster approval processes and potentially more favorable interest rates compared to traditional bank offerings. For instance, the Indonesian P2P lending market experienced substantial growth, with outstanding loan portfolios reaching trillions of Rupiah in recent years, indicating a clear shift in financing preferences for certain segments.

- Increased Accessibility: P2P lending and crowdfunding bypass stringent bank requirements, opening doors for underserved borrowers.

- Competitive Rates: These platforms can sometimes offer lower interest rates due to reduced overhead compared to traditional banks.

- Market Growth: The digital lending sector, including P2P, has seen rapid expansion, capturing a notable share of the credit market.

- Speed and Convenience: Online platforms often provide quicker application and disbursement times, appealing to borrowers seeking immediate funds.

Fintech and Alternative Investments: The Growing Threat to Traditional Banking

The threat of substitutes for Bank Central Asia (BCA) is substantial, primarily driven by the burgeoning fintech landscape and alternative investment avenues. Digital payment platforms and neobanks offer convenience and lower costs, directly challenging traditional banking services. For instance, by Q1 2024, GoPay facilitated over 170 million transactions, showcasing a significant shift in consumer preference for digital wallets over conventional banking for daily transactions.

Customers are increasingly exploring alternatives to bank deposits for wealth accumulation. Government bonds (SBN) and other capital market instruments can offer more attractive yields than traditional savings accounts, directly impacting bank deposit bases. In 2023, the Indonesian capital market saw significant retail investor participation, with many channeling funds into SBN offerings that provided competitive returns.

Alternative lending platforms, such as peer-to-peer (P2P) lending, provide accessible financing options that bypass traditional bank loan processes. The Indonesian P2P lending market's outstanding loan portfolio reached trillions of Rupiah in recent years, highlighting its growing role in credit provision, particularly for SMEs and individuals who may find traditional bank loans less accessible.

| Substitute Type | Key Characteristics | Impact on BCA | 2023/2024 Data Point |

|---|---|---|---|

| Digital Payment Platforms (e.g., GoPay, OVO) | Convenience, speed, lower transaction fees | Reduces transaction fee revenue, shifts customer loyalty | GoPay processed over 170 million transactions in Q1 2024 |

| Neobanks | Lower fees, enhanced digital experience, targeted segments | Attracts tech-savvy customers, pressures fee structures | Several Southeast Asian neobanks reached millions of users by early 2024 |

| Capital Market Instruments (e.g., SBN) | Potentially higher yields, direct investment | Drains deposit base, impacts liquidity | Significant retail participation in Indonesian SBN offerings in 2023 |

| P2P Lending & Crowdfunding | Faster approval, accessible financing for underserved | Captures loan market share, reduces demand for bank loans | Indonesian P2P lending market portfolio in trillions of Rupiah in recent years |

Entrants Threaten

High Regulatory and Capital Barriers

Indonesia's banking sector is characterized by substantial regulatory and capital barriers, significantly deterring new entrants. The Otoritas Jasa Keuangan (OJK) and Bank Indonesia impose stringent licensing and capital requirements, ensuring financial stability and consumer protection. For instance, in 2024, the minimum paid-up capital for commercial banks was set at IDR 3 trillion (approximately USD 190 million), a considerable hurdle for aspiring institutions.

While regulators are encouraging digital banking innovation, traditional new entrants still face rigorous scrutiny. These requirements, designed to safeguard the financial system, mean that establishing a new bank in Indonesia is a complex and capital-intensive undertaking, effectively limiting the threat of new competitors.

Established Brand Loyalty and Trust

Established brand loyalty and trust represent a significant barrier to new entrants in the banking sector. Incumbent institutions like Bank Central Asia (BCA) have cultivated decades of strong brand recognition and customer confidence, making it difficult for newcomers to gain traction quickly. For instance, as of early 2024, BCA consistently ranks among the most trusted banking brands in Indonesia, a testament to its long-standing commitment to service and reliability.

Economies of Scale and Distribution Networks

Existing large banks like Bank Central Asia (BCA) leverage substantial economies of scale, meaning their per-unit costs decrease as their output increases. This is evident in their massive investments in technology infrastructure and extensive distribution networks, encompassing thousands of branches and ATMs, alongside sophisticated digital platforms. For instance, in 2023, BCA reported a net profit of IDR 40.9 trillion, underscoring its operational efficiency and market dominance.

New entrants face a formidable barrier in replicating this scale. Establishing a comparable operational footprint and achieving similar cost efficiencies would necessitate massive capital outlays, making it difficult for newcomers to compete on price or service breadth against incumbents who have already amortized these costs over decades.

Digital-First Bank Entry and Regulatory Sandbox

The Indonesian financial landscape is evolving, with the Otoritas Jasa Keuangan (OJK) actively promoting a digital banking roadmap. This initiative, coupled with the establishment of a regulatory sandbox, significantly lowers the initial hurdles for new entrants. Neobanks and fintech firms can now test their innovative models with potentially less stringent capital and operational requirements compared to established traditional banks.

This regulatory environment directly addresses the threat of new entrants by fostering innovation. For instance, in 2024, several digital banks and fintech platforms continued to gain traction, leveraging technology to offer streamlined services and attract customers. While these digital-first players still face rigorous oversight as they grow and scale their operations, their initial entry is facilitated, posing a competitive challenge to incumbents like Bank Central Asia.

- Digital Banking Roadmap: OJK's strategic plan to encourage digital transformation in the banking sector.

- Regulatory Sandbox: A controlled environment for testing new financial products and services.

- Neobank and Fintech Entry: Facilitated entry for technology-driven financial service providers.

- Market Traction: Digital players leverage technology to attract and retain customers, challenging traditional models.

Talent Acquisition and Technology Investment

New entrants face significant challenges in attracting skilled personnel and making substantial investments in cutting-edge technology. In 2024, the demand for talent in areas like AI, data analytics, and cybersecurity remained exceptionally high, driving up recruitment costs for financial institutions. Aspiring banks must also allocate considerable capital towards developing and maintaining sophisticated digital platforms, a process that is both resource-intensive and complex.

The financial sector's rapid digital transformation necessitates continuous investment in technologies such as AI for fraud detection and customer service, blockchain for secure transactions, and robust cybersecurity measures to protect sensitive data. For instance, global spending on AI in banking was projected to reach tens of billions of dollars in 2024, highlighting the scale of investment required. This technological arms race creates a substantial barrier to entry, as new players must match or exceed the existing digital capabilities of established institutions to remain competitive.

- Talent War: Banks are competing fiercely for top talent in AI, cybersecurity, and data science, driving up salary expectations and recruitment expenses.

- Tech Investment: Developing and maintaining advanced digital platforms requires significant upfront and ongoing capital expenditure, estimated to be in the billions for comprehensive solutions.

- Digital Infrastructure: Building secure, user-friendly, and scalable digital banking solutions is a complex and costly undertaking, posing a considerable hurdle for new entrants.

- Regulatory Compliance: New entrants must also navigate stringent regulatory requirements for digital operations, adding another layer of complexity and cost.

New Entrants Challenge Indonesian Banking Giants

While regulatory and capital requirements present significant barriers, the Indonesian government's push for digital banking innovation, exemplified by the OJK's digital banking roadmap and regulatory sandbox initiatives, has lowered initial entry hurdles for fintechs and neobanks. This has led to increased traction for digital-first players in 2024, creating a more dynamic competitive landscape.

These new digital entrants leverage technology to offer streamlined services, challenging traditional models and forcing incumbents like Bank Central Asia to adapt. Although they still face rigorous oversight as they scale, their facilitated entry directly addresses the threat of new entrants, making the sector more competitive than in previous years.

However, established brand loyalty and trust remain potent defenses for incumbents. BCA, for instance, consistently ranks as a highly trusted brand in Indonesia as of early 2024, a result of decades of reliable service. This deep-seated customer confidence makes it challenging for newcomers to rapidly gain market share, despite technological advancements.

The threat of new entrants in Indonesia's banking sector is moderate, influenced by a dual dynamic of high regulatory and capital barriers for traditional banks, counterbalanced by government initiatives fostering digital banking innovation. This creates a complex environment where established players like Bank Central Asia benefit from strong brand loyalty and economies of scale, while new digital-focused entities find a pathway to enter and compete.

| Factor | Impact on New Entrants | Example/Data (2024) |

|---|---|---|

| Regulatory & Capital Barriers | High (Traditional Banks) | Minimum paid-up capital for commercial banks: IDR 3 trillion (approx. USD 190 million) |

| Digital Banking Initiatives | Moderate (Fintech/Neobanks) | OJK's Digital Banking Roadmap and Regulatory Sandbox |

| Brand Loyalty & Trust | High Barrier | BCA consistently ranked among Indonesia's most trusted banking brands |

| Economies of Scale | High Barrier | BCA's 2023 net profit: IDR 40.9 trillion, indicating significant operational efficiency |

| Talent & Technology Investment | High Barrier | High demand for AI/cybersecurity talent; global AI in banking spending in tens of billions of dollars |

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis for Bank Central Asia leverages data from official company filings, investor relations reports, and reputable financial news outlets. We also incorporate insights from industry-specific research and macroeconomic indicators to provide a comprehensive view of the competitive landscape.