Bank of Jiujiang Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Bank of Jiujiang Bundle

Don't Miss the Bigger Picture

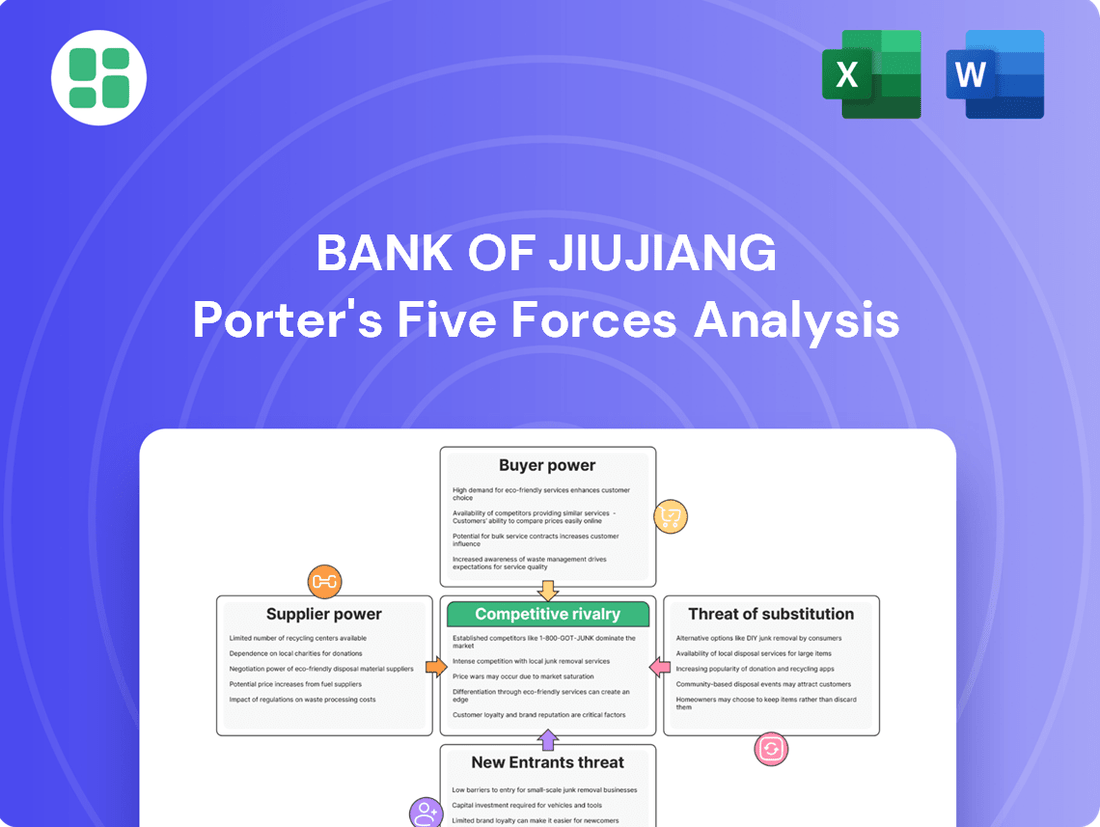

The Bank of Jiujiang operates within a dynamic financial landscape, where understanding the interplay of industry forces is paramount. Our analysis highlights moderate buyer power due to product differentiation and the threat of substitutes, while also delving into the intensity of rivalry and the influence of suppliers and new entrants.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Bank of Jiujiang’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Regulatory and Central Bank Policies

The People's Bank of China (PBOC) and the National Financial Regulatory Administration (NFRA) wield considerable influence over banks like Bank of Jiujiang through monetary policy, interest rate adjustments, and capital adequacy mandates. These policy decisions directly affect a bank's funding costs and the availability of essential interbank liquidity, thereby impacting their operational flexibility and profitability.

Interbank Market Funding

Bank of Jiujiang's dependence on the interbank market for short-term funding positions these financial institutions as powerful suppliers. The cost and availability of these funds are directly influenced by market liquidity and the monetary policy stance of the People's Bank of China.

In 2024, interbank lending rates, such as the Shanghai Interbank Offered Rate (SHIBOR), have shown fluctuations reflecting broader economic pressures and regulatory adjustments. For instance, a tightening of monetary policy could increase borrowing costs for Bank of Jiujiang, thereby enhancing the bargaining power of interbank market participants.

Technology and IT Service Providers

The accelerating digital transformation within China's banking sector grants significant leverage to technology and IT service providers. As institutions like Bank of Jiujiang pour resources into areas such as artificial intelligence and cloud infrastructure, their reliance on these specialized vendors for innovation and smooth operations grows, thereby increasing supplier power.

In 2023, Chinese banks collectively invested over 150 billion yuan in IT modernization, a trend expected to continue. This substantial investment underscores the critical role of tech providers, who are essential for banks to maintain a competitive edge and enhance their digital service offerings.

Skilled Human Capital

The banking sector, including regional players like Bank of Jiujiang, relies heavily on specialized talent. Professionals in finance, risk management, and the rapidly evolving field of financial technology are in high demand. This demand directly impacts the bargaining power of suppliers, which in this case, are the skilled individuals themselves.

For a regional bank, attracting and retaining top-tier talent can be particularly challenging. Larger national and international banks often offer more competitive compensation packages and broader career advancement opportunities. This disparity can give skilled professionals significant leverage when negotiating salaries and benefits.

- High Demand for Fintech Expertise: As banks increasingly adopt digital solutions, the need for professionals skilled in areas like data analytics, cybersecurity, and AI has surged.

- Specialized Financial Skills: Expertise in complex financial modeling, regulatory compliance, and sophisticated risk assessment remains crucial and commands premium compensation.

- Talent Scarcity in Regional Markets: Smaller banks may face greater difficulty in competing for limited pools of highly qualified candidates compared to larger institutions.

- Impact on Operational Costs: The cost of acquiring and retaining such human capital directly influences a bank's operating expenses and profitability.

Deposit Funding Costs

For banks like Bank of Jiujiang, customer deposits represent a critical source of funding, essentially acting as the 'supply' side of their operations. In China's competitive financial landscape, particularly with prevailing low-interest rates, banks are compelled to offer attractive deposit rates to attract and retain these funds. This dynamic directly influences their cost of capital and, consequently, their profitability.

The intense competition for savings among Chinese banks puts upward pressure on deposit rates. This means that while customers are often viewed as buyers, their role as depositors makes them powerful suppliers of funds. Banks must balance offering competitive rates to secure liquidity with maintaining healthy net interest margins. For instance, in late 2023 and early 2024, many Chinese banks adjusted their deposit rates to remain competitive, reflecting this ongoing supply-side pressure.

- Deposit Dependence: Banks rely heavily on customer deposits as their primary funding source.

- Competitive Deposit Rates: Low-interest rate environments and market competition force banks to offer higher deposit rates to attract funds.

- Margin Pressure: Increased deposit costs directly squeeze a bank's net interest margin, impacting overall profitability.

- Customer as Supplier: In this context, depositors are powerful suppliers, influencing the cost of a bank's core raw material – money.

Bank's Supplier Power: Funding, Tech, Talent Drive Costs

The bargaining power of suppliers for Bank of Jiujiang is influenced by several key factors, including the interbank market, technology providers, and skilled human capital. Fluctuations in interbank lending rates, such as SHIBOR, directly impact the cost of funding. Furthermore, the increasing reliance on specialized IT services and the high demand for fintech expertise empower these suppliers, driving up costs for banks investing in digital transformation.

In 2023, Chinese banks' IT spending exceeded 150 billion yuan, highlighting the significant leverage held by technology vendors. This trend is expected to continue, as banks like Bank of Jiujiang prioritize digital upgrades to remain competitive.

The scarcity of specialized talent in financial technology and risk management also grants considerable bargaining power to skilled professionals. Regional banks often face challenges in attracting and retaining this talent compared to larger national institutions, leading to higher labor costs.

| Supplier Type | Key Influence | 2024 Trend/Impact |

|---|---|---|

| Interbank Market Participants | Cost and availability of short-term funding | SHIBOR fluctuations reflect monetary policy, impacting borrowing costs. |

| Technology & IT Service Providers | Digital transformation, AI, cloud infrastructure | Increased reliance due to significant IT investment by banks. |

| Skilled Human Capital (Fintech, Risk) | Talent acquisition and retention | High demand and scarcity in regional markets drive up labor costs. |

What is included in the product

This analysis of Bank of Jiujiang reveals the intensity of rivalry, the bargaining power of customers and suppliers, the threat of new entrants and substitutes, all crucial for understanding its competitive environment.

A clear, one-sheet summary of all five forces—perfect for quick decision-making regarding the Bank of Jiujiang's competitive landscape.

Instantly understand strategic pressure with a powerful spider/radar chart, highlighting the Bank of Jiujiang's competitive positioning.

Customers Bargaining Power

Low Switching Costs for Retail Customers

For retail customers, the bargaining power is notably high due to low switching costs. The proliferation of digital banking platforms and mobile payment solutions has made it remarkably simple for individuals to move their accounts between financial institutions for core services like deposits, transactions, and even certain loan products. This ease of transition directly erodes customer loyalty, empowering them to readily pursue more favorable interest rates or superior service offerings from competitors.

Interest Rate Sensitivity of Corporate Clients

Corporate clients, especially larger enterprises, wield significant bargaining power due to their sensitivity to interest rates. They can leverage their substantial business volume to negotiate more favorable loan terms with financial institutions like Bank of Jiujiang. This means the bank must remain competitive in its lending rates to secure and retain these valuable clients.

Availability of Alternative Financial Channels

The bargaining power of customers for Bank of Jiujiang is significantly influenced by the increasing availability of alternative financial channels. Customers now have a wider array of options beyond traditional banking, including direct investment platforms and wealth management services from non-bank entities.

In 2024, the fintech sector continued its rapid expansion, with digital lending platforms and robo-advisors attracting substantial customer interest. For instance, the global fintech market was projected to reach over $2.4 trillion by 2024, indicating a strong customer shift towards these alternatives.

This proliferation of choices empowers customers to seek better rates, more personalized services, and innovative products, thereby increasing their leverage when dealing with established banks like Bank of Jiujiang.

Digital Empowerment and Information Access

Customers today are significantly more informed, thanks to the proliferation of online resources. Financial literacy has surged, with individuals readily accessing detailed product information and comparing offerings across various institutions. This digital empowerment directly translates to increased bargaining power.

The availability of financial comparison websites and readily accessible online reviews means customers can easily identify the best rates and terms. For instance, in 2024, data indicates a substantial portion of consumers actively use comparison tools before selecting banking products, forcing institutions like the Bank of Jiujiang to offer competitive pricing and superior service to retain business.

- Increased Online Research: A significant percentage of banking customers in 2024 reported using online comparison tools to evaluate financial products.

- Demand for Transparency: Customers expect clear and easily understandable information about fees, interest rates, and service charges.

- Focus on Value: The ease of switching and comparing services means customers are less loyal to a single institution and prioritize the best overall value proposition.

Regulatory Protection for Consumers

Chinese regulators are increasingly prioritizing consumer protection within the financial industry. Measures addressing mobile payment security and enhancing complaint resolution mechanisms are examples of this trend. This heightened regulatory scrutiny can indirectly bolster the bargaining power of individual customers by ensuring they receive fair treatment and have avenues for recourse.

The People's Bank of China (PBOC) has been active in this space. For instance, in 2023, the PBOC continued to refine regulations around fintech, including those impacting consumer data privacy and the transparency of financial product offerings. These efforts aim to create a more level playing field where customers have greater confidence and ability to negotiate terms or seek redress.

- Enhanced Complaint Resolution: Stricter rules on how financial institutions handle customer grievances provide a stronger foundation for consumers to assert their rights.

- Data Privacy Safeguards: Regulations protecting personal financial data limit how banks can leverage customer information, potentially reducing information asymmetry.

- Fairer Pricing and Terms: Increased oversight on product disclosures and fees can empower customers to compare offerings and demand more favorable terms.

Customer Power Reshapes Banking Dynamics

Customers, both individual and corporate, hold considerable sway over Bank of Jiujiang due to increased market transparency and the ease with which they can switch providers. The digital transformation of banking means customers can readily compare rates, fees, and services online, often utilizing comparison websites. This accessibility, coupled with a growing demand for personalized financial solutions and a greater awareness of alternative financial providers, significantly amplifies their bargaining power.

| Factor | Impact on Bargaining Power | 2024 Data/Trend |

|---|---|---|

| Switching Costs (Retail) | High | Digital banking and mobile payments offer near-zero switching costs for core retail services. |

| Interest Rate Sensitivity (Corporate) | High | Large corporate clients can negotiate favorable terms due to their significant transaction volumes. |

| Availability of Alternatives | High | Fintech platforms and non-bank financial services provide competitive options, increasing customer leverage. |

| Customer Information Access | High | Online resources and comparison tools empower customers to make informed decisions and demand better value. |

Same Document Delivered

Bank of Jiujiang Porter's Five Forces Analysis

This preview showcases the Bank of Jiujiang's Porter's Five Forces analysis, providing a comprehensive examination of competitive forces within its industry. The document you see here is the exact, fully formatted report you will receive instantly upon purchase, ensuring no discrepancies or missing information. You're looking at the actual document, ready for immediate download and use, offering a complete and professionally written strategic overview.

Rivalry Among Competitors

Intense Competition from Larger Banks

Bank of Jiujiang contends with formidable rivals in the form of major state-owned and national joint-stock banks. These larger institutions leverage their vast branch networks, substantial capital reserves, and comprehensive product suites to capture market share. For instance, as of the first quarter of 2024, the total assets of China's five largest state-owned commercial banks exceeded 110 trillion RMB, dwarfing regional players.

This intense rivalry means that Bank of Jiujiang must constantly innovate and offer compelling value propositions to attract and retain customers. The sheer scale and resources of these larger competitors allow them to offer more aggressive pricing on loans and deposits, creating a challenging environment for smaller regional banks to compete solely on price.

Narrowing Net Interest Margins

The Chinese banking sector, including regional players like Bank of Jiujiang, faces significant pressure on net interest margins. This is largely driven by a low-interest rate environment and intense competition for both deposits and loans. For instance, in 2023, the People's Bank of China maintained its benchmark lending rates, contributing to this margin compression across the industry.

This narrowing of net interest margins escalates competitive rivalry. Banks are compelled to fight more aggressively for market share and profitability in a landscape where the spread between lending income and funding costs is shrinking. This dynamic forces banks to seek efficiency and differentiation to maintain their financial health.

Digital Transformation Race

The Chinese banking sector is in a fierce digital transformation race, compelling institutions like the Bank of Jiujiang to invest significantly in technologies such as AI and cloud computing. This drive aims to boost operational efficiency and customer engagement, creating a dynamic competitive landscape where innovation is paramount.

In 2023, Chinese banks collectively poured billions into digital initiatives, with major state-owned banks leading the charge. This intense competition means that lagging in technological adoption can quickly lead to a loss of market share, forcing even regional players like the Bank of Jiujiang to allocate substantial capital to stay relevant and competitive.

Regional and Local Market Competition

Within Jiangxi Province, Bank of Jiujiang navigates a competitive landscape populated by other city commercial banks and rural commercial banks. These institutions are also deeply entrenched in the local economy, targeting similar customer bases and community needs. For instance, as of early 2024, China boasted over 4,000 rural commercial banks, many of which operate at a regional level, presenting a significant number of direct competitors to Bank of Jiujiang's core markets.

While Bank of Jiujiang's specialized local focus offers a degree of advantage, it does not insulate it from intense competition. The bank must actively vie for market share against a multitude of regional players, each vying for deposits, loans, and fee-based services within the province. This dynamic means that customer loyalty can be fluid, and the bank needs to continuously innovate and offer compelling value propositions to retain and attract business.

- Intense Local Competition: Bank of Jiujiang faces significant rivalry from numerous city commercial banks and rural commercial banks operating within Jiangxi Province.

- Shared Focus: These competitors also concentrate on serving the local economy and communities, creating direct overlap in customer segments and service offerings.

- Market Share Battles: The bank actively competes for market share against these regional players, necessitating strong product development and customer relationship management.

Regulatory Driven Consolidation

The Chinese government's initiative to consolidate smaller and regional banks, a move aimed at bolstering financial stability and mitigating systemic risks, is actively reshaping the competitive arena for institutions like the Bank of Jiujiang. This regulatory push is leading to fewer, yet demonstrably stronger, banking entities emerging from the mergers.

This trend implies that Bank of Jiujiang is navigating an increasingly dynamic competitive environment. As consolidation progresses, the bank might find itself contending with larger, more resource-rich regional competitors that possess enhanced market power and a broader operational footprint.

- Regulatory Mandate for Consolidation: China's banking regulator, the China Banking and Insurance Regulatory Commission (CBIRC), has been actively encouraging mergers and acquisitions among smaller banks.

- Systemic Risk Mitigation: The primary driver for this consolidation is to reduce the number of undercapitalized and poorly managed institutions that could pose a threat to the broader financial system.

- Emergence of Stronger Competitors: Successful consolidations result in banks with larger asset bases, improved capital adequacy ratios, and enhanced risk management capabilities, thereby intensifying competition.

- Evolving Landscape: For Bank of Jiujiang, this means adapting to a future where it may face formidable regional banking groups that have benefited from these regulatory-driven consolidations.

Regional Banks: Battling Giants for Market Share and Margins

Bank of Jiujiang faces intense rivalry from larger state-owned and national joint-stock banks that possess significant advantages in scale, capital, and product offerings, as evidenced by the first quarter of 2024 data showing the top five state-owned banks holding over 110 trillion RMB in assets. This disparity forces regional players to innovate and differentiate to attract customers, as larger competitors can offer more aggressive pricing, squeezing net interest margins across the industry, a trend exacerbated by the People's Bank of China's stable benchmark lending rates in 2023.

| Competitor Type | Key Advantages | Impact on Bank of Jiujiang | 2023/2024 Data Point |

|---|---|---|---|

| Large State-Owned & National Joint-Stock Banks | Vast branch networks, substantial capital reserves, comprehensive product suites, aggressive pricing capabilities | Pressure on market share and net interest margins, necessitates innovation and differentiation | Total assets of top 5 state-owned banks exceeded 110 trillion RMB (Q1 2024) |

| Other City & Rural Commercial Banks (Jiangxi Province) | Deep local economic entrenchment, targeting similar customer bases and community needs | Direct competition for deposits, loans, and fee-based services within core markets, fluid customer loyalty | Over 4,000 rural commercial banks in China (early 2024) |

| Consolidated Regional Banks | Enhanced market power, broader operational footprint, improved capital adequacy, advanced risk management | Emergence of stronger, more resource-rich competitors, requiring adaptation to a more concentrated competitive landscape | Ongoing regulatory push for mergers and acquisitions among smaller banks |

SSubstitutes Threaten

Fintech and Digital Payment Platforms

The rise of fintech and digital payment platforms like Alipay and WeChat Pay presents a significant threat of substitution for traditional banks. These platforms offer highly convenient alternatives for daily transactions, directly impacting banks' market share. For instance, in 2023, mobile payments in China continued their upward trajectory, with billions of transactions processed daily, highlighting the widespread adoption and preference for these digital solutions over traditional banking channels.

Online Lending and Wealth Management Platforms

Non-bank online platforms present a significant threat of substitution for Bank of Jiujiang. These platforms, like Ant Group's MYbank or Tencent's WeBank in China, offer streamlined access to personal loans, small business financing, and investment products, often bypassing traditional banking infrastructure. For instance, in 2023, China's fintech lending market continued its robust growth, with digital channels facilitating a substantial portion of consumer credit, directly challenging Bank of Jiujiang's traditional loan origination.

Direct Capital Market Financing

For larger corporate clients, direct capital market financing, such as issuing bonds or equity, presents a significant substitute for traditional bank loans. As China's capital markets continue to develop and deepen, companies are increasingly able to access funds directly, potentially bypassing commercial banks. In 2024, China's onshore bond market saw robust activity, with corporate bond issuance reaching trillions of yuan, indicating a strong alternative for corporate funding.

Insurance and Fund Products as Savings Alternatives

Customers are increasingly looking beyond traditional bank deposits for their savings and investment needs. This is particularly true for those aiming for higher returns or specific financial objectives. For instance, in 2024, the global mutual fund industry continued its robust growth, managing trillions of dollars in assets, indicating a strong preference for diversified investment vehicles.

Insurance products, especially those with investment components like universal life or variable annuities, present a significant substitute. These often offer tax advantages and potential for capital appreciation that traditional savings accounts do not. As of early 2025, the life insurance sector in major economies saw continued inflows, demonstrating consumer confidence in these alternative savings avenues.

The availability and marketing of these non-bank financial products directly challenge the deposit-gathering capabilities of banks like Bank of Jiujiang. As customers become more financially savvy, they are more likely to compare offerings and shift funds to where they perceive greater value or better alignment with their long-term financial strategies.

- Growing Mutual Fund Assets: Global mutual fund assets surpassed $60 trillion in 2024, highlighting a significant shift of savings towards investment products.

- Insurance Product Appeal: Investment-linked insurance policies offer tax-efficient growth and protection, attracting a segment of savers seeking dual benefits.

- Customer Sophistication: Increased financial literacy empowers customers to seek alternatives offering potentially higher yields than standard bank deposits.

- Competition for Deposits: The rise of these substitutes intensifies competition for customer deposits, potentially impacting banks' funding costs and strategies.

Central Bank Digital Currency (Digital Yuan)

The emergence of Central Bank Digital Currencies (CBDCs), such as China's Digital Yuan (e-CNY), presents a significant threat of substitutes for traditional banking services. While not a direct replacement for all banking functions, the e-CNY's potential to facilitate direct peer-to-peer transactions and streamline payment processes could reduce reliance on commercial banks for retail settlements. By mid-2024, pilot programs for the e-CNY had expanded significantly, involving millions of users and a growing number of transaction scenarios, indicating a tangible shift in payment behaviors.

The e-CNY's design aims to coexist with, rather than replace, the existing financial infrastructure. However, its increasing adoption could reshape the competitive dynamics within the retail payment sector. This could lead to a gradual erosion of transaction-based revenue streams for commercial banks if consumers increasingly opt for the direct and potentially lower-cost digital currency for everyday purchases. For instance, by the end of 2023, the e-CNY had been used in over 264 million transactions, totaling over 1.8 trillion yuan, demonstrating its growing penetration.

The threat of substitutes is amplified by the potential for the e-CNY to offer enhanced efficiency and lower transaction costs compared to existing payment rails. This could incentivize a shift in consumer preference, particularly for smaller, frequent transactions.

- Reduced reliance on commercial bank payment systems for retail transactions.

- Potential for lower transaction fees offered by the e-CNY.

- Increased competition in the digital payment landscape.

- Shifting consumer preferences towards direct digital currency usage.

The Substitute Threat: How Digital Finance Reshapes Traditional Banking

The threat of substitutes for Bank of Jiujiang is multifaceted, encompassing digital payment platforms, non-bank online lenders, direct capital market access, alternative investment vehicles like mutual funds and insurance, and the burgeoning Central Bank Digital Currency (CBDC) landscape.

These substitutes offer convenience, potentially higher returns, and specialized financial services that can divert customers and revenue away from traditional banking. For instance, China's digital payment market saw continued exponential growth in 2024, with mobile transactions dominating daily commerce, directly challenging banks' transaction fee income.

Furthermore, the increasing sophistication of financial products and the growing comfort of consumers with digital channels mean that banks must constantly innovate to retain market share. In 2024, global mutual fund assets exceeded $60 trillion, illustrating a significant migration of savings towards non-bank managed investment products.

| Substitute Category | Key Players/Examples | Impact on Bank of Jiujiang | 2024/2025 Data Point |

|---|---|---|---|

| Digital Payment Platforms | Alipay, WeChat Pay | Reduced transaction revenue, customer loyalty erosion | Billions of daily mobile transactions in China |

| Fintech Lenders | MYbank, WeBank | Loss of loan origination market share | Robust growth in China's fintech lending market |

| Capital Markets | Bond issuance, Equity offerings | Reduced demand for corporate loans | Trillions of yuan in Chinese corporate bond issuance in 2024 |

| Investment Products | Mutual Funds, Insurance | Deposit outflows, reduced interest income | Global mutual fund assets surpassed $60 trillion in 2024 |

| Central Bank Digital Currencies | Digital Yuan (e-CNY) | Potential disintermediation of retail payments | Over 264 million e-CNY transactions by end of 2023 |

Entrants Threaten

High Capital Requirements and Regulatory Hurdles

The threat of new entrants for Bank of Jiujiang is significantly mitigated by the high capital requirements and formidable regulatory hurdles inherent in China's banking sector. Obtaining a banking license is an arduous process, demanding substantial financial backing and adherence to strict operational standards. For instance, in 2024, the minimum registered capital for a rural commercial bank in China remained a considerable barrier, often in the hundreds of millions of RMB, effectively pricing out many potential new players.

Established Brand Reputation and Customer Trust

Established banks like Bank of Jiujiang have cultivated strong brand reputations and deep customer trust over many years. This is a formidable barrier for any new entrant aiming to gain market share.

Newcomers must overcome the significant hurdle of building credibility and attracting a loyal customer base, especially within a market where local relationships are paramount. For instance, in 2023, Bank of Jiujiang reported a customer deposit base of over ¥150 billion, reflecting this established trust.

Economies of Scale and Scope

Incumbent banks like Bank of Jiujiang enjoy significant cost advantages due to economies of scale. For instance, in 2023, major Chinese banks reported operating costs per asset that were substantially lower than smaller regional players, reflecting their ability to spread fixed costs over a larger asset base.

New entrants would face immense difficulty in matching these efficiencies, particularly in areas like advanced technology infrastructure and widespread marketing campaigns. Building a comparable operational scale and customer reach from scratch would require massive upfront investment, creating a substantial barrier to entry.

Access to Funding and Interbank Networks

New banks entering the market would struggle to establish robust funding streams. Securing stable customer deposits and gaining access to the interbank lending market, vital for liquidity, presents significant hurdles.

Established institutions like Bank of Jiujiang benefit from long-standing customer relationships and preferential access to interbank networks, creating a substantial barrier for newcomers.

- Funding Challenges: New entrants face difficulties in attracting deposits and securing wholesale funding compared to incumbent banks with established reputations and customer bases.

- Interbank Access: Access to the interbank market, crucial for short-term liquidity management and lending, is often granted based on creditworthiness and existing relationships, favoring established players.

- Cost of Funds: New banks may incur higher costs for funding due to perceived higher risk, impacting their profitability and competitiveness against established banks.

Data and Technology Infrastructure Investment

The significant capital required for developing and maintaining advanced data and technology infrastructure presents a substantial hurdle for new entrants. Building a secure, reliable, and competitive digital banking platform necessitates massive investments in cutting-edge technology, sophisticated data analytics capabilities, and robust cybersecurity measures. For instance, as of early 2024, major banks are investing billions in digital transformation, with many allocating over $10 billion annually to technology upgrades and cybersecurity alone. This immense financial commitment, coupled with the ongoing need for continuous innovation and adaptation to evolving technological landscapes, creates a formidable barrier to entry.

Potential new players face the challenge of matching the existing infrastructure and expertise of established institutions. This includes not only the initial outlay for hardware, software, and specialized talent but also the ongoing operational costs and the need to stay ahead of rapid technological advancements. Without this foundational investment, new entrants would struggle to offer the seamless digital experience, data-driven insights, and security assurances that customers expect from modern financial services. The sheer scale of these investments effectively deters many aspiring competitors from entering the market.

- High Capital Outlay: Building a modern digital banking infrastructure requires billions in investment for hardware, software, and cloud services.

- Data Analytics & AI: Significant spending is needed for advanced analytics platforms and artificial intelligence to process vast amounts of customer data.

- Cybersecurity Investment: Financial institutions are increasingly prioritizing cybersecurity, with global spending projected to reach hundreds of billions in the coming years to protect against sophisticated threats.

- Talent Acquisition: Attracting and retaining specialized IT and data science talent commands high salaries, adding to the operational cost burden for new entrants.

China's Banking: High Entry Barriers Protect Incumbents

The threat of new entrants for Bank of Jiujiang is low due to substantial capital requirements and stringent regulatory oversight in China's banking sector. For instance, in 2024, minimum capital for rural commercial banks remained in the hundreds of millions of RMB, a significant barrier. Established brand loyalty and deep customer trust, exemplified by Bank of Jiujiang's ¥150 billion deposit base in 2023, further deter newcomers.

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis for Bank of Jiujiang leverages data from official company filings, including annual reports and prospectuses, alongside industry-specific research from financial data providers and banking sector regulatory bodies.