BAC Holding International Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

BAC Holding International Bundle

A Must-Have Tool for Decision-Makers

BAC Holding International navigates a competitive landscape shaped by significant buyer power and the constant threat of substitutes. Understanding these forces is crucial for any strategic decision.

The full analysis reveals the strength and intensity of each market force affecting BAC Holding International, complete with visuals and summaries for fast, clear interpretation.

Suppliers Bargaining Power

Dependency on Technology Vendors

BAC Holding International's reliance on specialized technology vendors for banking software, IT infrastructure, and cybersecurity solutions grants these suppliers considerable bargaining power. This is particularly true when their products are proprietary or involve substantial costs for BAC Holding to switch to a different provider. For instance, a significant portion of the global banking IT market is dominated by a few key players, meaning BAC Holding might not have numerous equally capable alternatives readily available.

Access to Wholesale Funding

BAC Holding International's reliance on wholesale funding markets means that suppliers of capital, like major banks and institutional investors, hold significant sway. These suppliers can dictate terms and interest rates, particularly when market confidence wavers or credit conditions tighten, directly impacting BAC's cost of doing business.

Human Capital and Specialized Talent

The availability of skilled professionals in digital banking, data analytics, and risk management significantly influences the bargaining power of human capital. A scarcity of these specialized talents in Central America, where BAC Holding International operates, would empower employees and recruitment agencies, potentially driving up salary demands and affecting operational efficiency.

Regulatory Compliance Service Providers

Regulatory compliance service providers hold significant bargaining power over BAC Holding International, especially within Central America's intricate and frequently changing financial regulatory environment. These specialized firms possess critical knowledge and expertise necessary for navigating complex local and international financial laws, making BAC Holding International’s reliance on them a key factor in their influence.

For instance, the increasing focus on anti-money laundering (AML) and know-your-customer (KYC) regulations globally has led to a surge in demand for compliance services. In 2024, financial institutions worldwide were expected to spend an estimated $50 billion on compliance technology and services, highlighting the essential nature of these providers.

- High Switching Costs: Changing compliance providers can be costly and time-consuming due to the need to re-familiarize new consultants with BAC Holding International's specific operations and regulatory history.

- Concentrated Market: The market for highly specialized financial regulatory expertise in Central America may be relatively concentrated, giving fewer providers more leverage.

- Essential Service: Non-compliance can result in severe penalties, including hefty fines and reputational damage, making these services indispensable for BAC Holding International.

Payment Network Providers

Payment network providers like Visa and Mastercard hold significant sway in the financial industry. Their established infrastructure and near-universal acceptance make them critical partners for any entity facilitating card transactions, including BAC Holding International. This dominance allows them to dictate terms, including interchange fees and network access, which directly influence BAC's operational costs and the services it can offer its customers.

- Interchange Fees: These fees, paid by the merchant's bank to the cardholder's bank, are a primary revenue stream for payment networks. In 2024, interchange fees continue to be a major cost factor for businesses and a key determinant of profitability for financial institutions.

- Network Dominance: Visa and Mastercard process trillions of dollars in transactions annually, solidifying their market power. For instance, Visa reported over $14.1 trillion in total payment volume in fiscal year 2023, highlighting their essential role.

- Contractual Leverage: The terms of service and pricing agreements with these networks are often long-term and can be difficult to renegotiate, giving the providers substantial bargaining power over BAC Holding International.

Supplier Bargaining Power: Key Influences on BAC Holding International

The bargaining power of suppliers for BAC Holding International is a significant factor, particularly concerning technology and capital. Specialized IT vendors and wholesale funding providers can exert considerable influence due to high switching costs and market concentration.

Human capital and regulatory compliance service providers also hold substantial power, especially given the scarcity of specialized talent and the complexity of financial regulations in Central America. For instance, global spending on compliance technology and services was projected to reach $50 billion in 2024.

Payment network providers like Visa and Mastercard wield significant influence through their network dominance and contractual terms, impacting BAC Holding International's operational costs. Visa alone processed over $14.1 trillion in total payment volume in fiscal year 2023.

| Supplier Type | Key Factors Influencing Bargaining Power | Impact on BAC Holding International | Illustrative Data (2023-2024) |

|---|---|---|---|

| Technology Vendors | Proprietary solutions, high switching costs, market concentration | Increased IT costs, potential for vendor lock-in | Global IT spending by financial services expected to grow |

| Wholesale Funding Providers | Market confidence, credit conditions, access to capital | Higher borrowing costs, limited access to funds | Interest rate trends in major economies |

| Human Capital (Specialized Talent) | Scarcity of skills, demand for expertise | Higher salary demands, recruitment challenges | Growth in demand for FinTech and data analytics professionals |

| Regulatory Compliance Services | Complex regulations, specialized knowledge, penalties for non-compliance | Increased compliance costs, reliance on expert advice | Estimated $50 billion global spend on compliance tech/services in 2024 |

| Payment Networks (Visa, Mastercard) | Network dominance, interchange fees, contractual terms | Transaction costs, influence on service offerings | Visa's $14.1 trillion payment volume (FY2023) |

What is included in the product

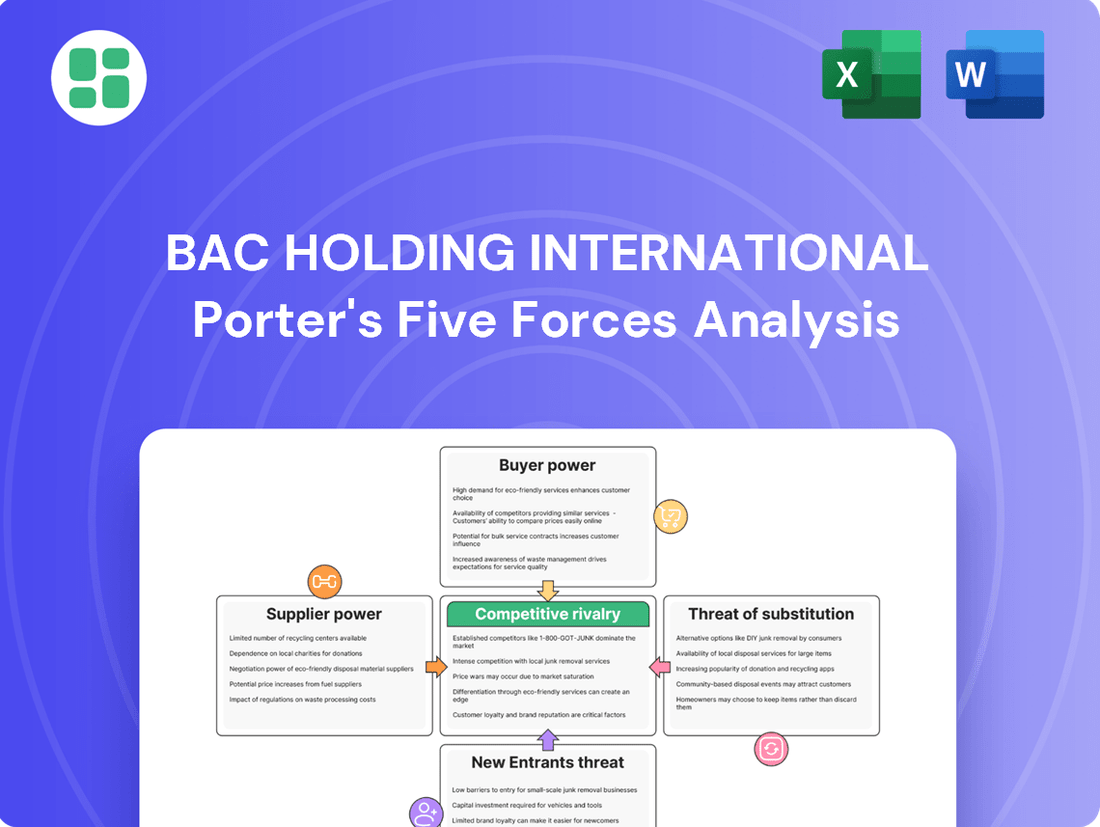

BAC Holding International's Porter's Five Forces analysis reveals the intense competitive rivalry, moderate buyer and supplier power, and significant barriers to entry within its operating environment.

Instantly identify and mitigate competitive threats by visualizing the impact of each Porter's Five Forces on BAC Holding International.

Customers Bargaining Power

Diverse Customer Segments

BAC Holding International's customer base is quite varied, encompassing individual retail clients, small and medium-sized enterprises (SMEs), and large corporate entities. This diversity means the bargaining power isn't uniform across the board.

For instance, large corporations and high-net-worth individuals often wield significant influence. Their substantial business volumes allow them to negotiate more favorable terms, potentially impacting BAC Holding International's fee structures and service agreements. This is a common dynamic in financial services where client size directly correlates with negotiation leverage.

Availability of Alternative Financial Services

The bargaining power of customers for BAC Holding International is significantly amplified by the increasing availability of alternative financial services. Customers can readily switch to other traditional banks or explore innovative fintech solutions, especially in Central America where digital adoption is on the rise. This ease of switching empowers customers by giving them more choices.

Emerging neobanks and accessible mobile payment platforms in regions like Central America directly enhance customer choice, putting more pressure on established institutions like BAC Holding International. For instance, by mid-2024, several fintech startups in the region reported significant user growth, with some neobanks seeing a 30% year-over-year increase in active accounts, directly impacting customer retention strategies for traditional banks.

Price Sensitivity and Transparency

Customers today have more power than ever to compare banking products, thanks to readily available digital tools. This transparency means they can easily see who offers the best rates on savings accounts or the lowest fees on loans. For instance, in 2024, many online comparison sites highlighted significant differences in interest rates offered by various banks for similar savings products, pushing institutions to be more competitive.

Digital Sophistication and Financial Literacy

As customers increasingly embrace digital tools and enhance their financial understanding, their bargaining power naturally grows. This heightened digital sophistication allows them to effortlessly compare product features, pricing, and terms across various providers, making informed decisions and readily switching if a better deal arises. For instance, studies in 2024 indicated that over 70% of consumers actively use online comparison tools before making financial service decisions.

BAC Holding International's own push towards digitalization further amplifies this trend. Customers now expect intuitive, seamless digital interactions, and any perceived inefficiency or difficulty in navigating BAC's digital platforms can quickly lead to customer dissatisfaction and potential defection. This means that maintaining a user-friendly and robust digital experience is paramount to retaining customers in today's competitive landscape.

- Digital Savvy Customers: A 2024 survey revealed that 65% of banking customers prefer digital channels for most transactions, indicating a strong reliance on technology.

- Informed Decision-Making: With access to vast online information, customers can easily research and compare financial products, increasing their ability to negotiate better terms.

- Expectation of Seamlessness: Customers expect digital platforms to be intuitive and efficient; a poor user experience can directly impact loyalty and drive them to competitors.

- Switching Behavior: The ease of switching providers, facilitated by digital onboarding processes, empowers customers to act on better offers more readily.

Regulatory Protections for Consumers

Consumer protection regulations across Central American nations, covering aspects like fee transparency, data privacy, and complaint resolution, significantly bolster the bargaining power of customers. These rules often mandate fair practices and establish channels for customers to seek redress, thereby curbing the unilateral authority of financial institutions.

- Consumer Protection Laws: Many Central American countries have implemented consumer protection laws that regulate banking practices, including disclosure of fees and interest rates.

- Data Privacy: Regulations regarding data privacy empower customers by giving them more control over their personal financial information, limiting how banks can use it.

- Dispute Resolution Mechanisms: The availability of accessible and fair dispute resolution processes provides customers with leverage when dealing with banks, as they have recourse if unsatisfied.

- Impact on Bargaining Power: These regulatory frameworks collectively enhance customer bargaining power by ensuring greater transparency, fairness, and avenues for complaint, reducing the information asymmetry between banks and their clients.

Customers' Power: Digital Tools & Alternatives Reshape Banking

The bargaining power of customers for BAC Holding International is substantial, driven by heightened digital savviness and increased access to alternative financial solutions. Customers can easily compare offerings, with over 70% of consumers in 2024 using online comparison tools for financial decisions. This empowers them to negotiate better terms and readily switch providers if unsatisfied, especially with the rise of fintech and neobanks in Central America, which saw some neobanks grow active accounts by 30% year-over-year in mid-2024.

| Factor | Impact on BAC Holding International | Supporting Data (2024) |

|---|---|---|

| Digital Sophistication | Increased ability to compare and negotiate | 70% of consumers use online comparison tools |

| Availability of Alternatives | Pressure to offer competitive terms | 30% YoY growth in active accounts for some neobanks |

| Consumer Protection | Limits unilateral authority of the bank | Mandated fee transparency and data privacy regulations |

Preview the Actual Deliverable

BAC Holding International Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. The comprehensive Porter's Five Forces analysis for BAC Holding International meticulously details the competitive landscape, offering insights into the bargaining power of buyers and suppliers, the threat of new entrants and substitutes, and the intensity of rivalry within the industry. This professionally formatted analysis is ready for your immediate use and strategic decision-making.

Rivalry Among Competitors

Number and Size of Competitors

The Central American banking landscape is a dynamic arena, characterized by the presence of both substantial regional financial institutions and numerous smaller, locally focused banks. This mix creates a highly competitive environment where market share is fiercely contested.

BAC Holding International, a prominent financial group operating within this region, encounters significant rivalry. Its competitors include well-established domestic banks with deep roots in their respective countries, as well as international banks that bring global expertise and capital to the Central American market.

Market Growth and Saturation

While Central America continues to address its unbanked and underbanked populations, offering avenues for growth, the more established retail and corporate banking sectors are likely experiencing a slowdown. This maturity intensifies rivalry, as existing financial institutions vie more aggressively for market share. For instance, in 2024, several major banks in the region reported single-digit percentage increases in net interest income, a sign of a more competitive lending environment.

Product and Service Differentiation

Competitive rivalry in the banking sector is significantly influenced by how effectively institutions can differentiate their products and services. This differentiation can manifest in various ways, from cutting-edge digital banking platforms to highly specialized loan products or exceptionally personalized customer service. For instance, banks that invest heavily in user-friendly mobile apps and seamless online account management often attract a younger, tech-savvy demographic.

BAC Holding International, for its part, is strategically positioning itself by emphasizing its 'Net Positive' approach and a strong commitment to digital innovation. This strategy is designed to cultivate unique value propositions that set it apart from competitors. By focusing on these areas, BAC aims to build a distinct brand identity and attract customers seeking more than just traditional banking services, potentially leading to increased customer loyalty and market share.

Switching Costs for Customers

Switching costs for customers in banking can be a significant factor in competitive rivalry. Traditionally, moving accounts, direct debits, and credit histories presented a hurdle, making customers less likely to switch. However, the financial landscape is evolving rapidly.

The proliferation of digital banking platforms and the push for open finance initiatives are actively working to lower these barriers. For instance, many neobanks offer seamless account switching services, significantly reducing the effort required from customers. This trend suggests that while historical switching costs were high, they are diminishing, potentially intensifying competition.

Banks are actively trying to counteract this by building integrated ecosystems that lock customers in. This involves offering a suite of services, from checking accounts and loans to investment platforms and budgeting tools, all within a single digital interface. The goal is to make the overall value proposition so compelling that the perceived cost of leaving outweighs the benefits of switching.

- Traditional Switching Costs: Moving direct debits, payment schedules, and credit history historically created inertia for customers.

- Digital Disruption: Open finance and user-friendly digital banking apps are actively reducing the effort and time involved in switching providers.

- Ecosystem Lock-in: Banks are fostering loyalty by integrating multiple financial services, aiming to increase the perceived cost of leaving.

- Competitive Intensity: As switching costs decrease, the threat of customers moving to competitors, especially digital-first banks, rises.

Intensity of Digital Transformation

The competitive rivalry within BAC Holding International's operating regions, particularly Central America, is significantly intensified by the rapid pace of digital transformation. Banks are channeling substantial investments into technology to roll out advanced mobile banking, seamless digital payment solutions, and improved online customer experiences. This technological arms race means that institutions unable to keep up with these innovations risk losing their competitive standing.

This digital shift is not just about offering new services; it's a fundamental change in how financial institutions operate and interact with customers. For instance, in 2024, the digital banking sector in Latin America saw continued growth, with mobile banking adoption rates climbing steadily. Banks that fail to invest in these areas, such as enhancing their digital platforms or integrating new fintech solutions, will find it increasingly difficult to attract and retain customers, thereby fueling the rivalry among those that do.

- Digital Investment: Banks are allocating significant capital towards upgrading their technological infrastructure and developing innovative digital products.

- Fintech Integration: The adoption of fintech solutions is accelerating, forcing traditional banks to compete with agile, tech-focused disruptors.

- Customer Expectations: Consumers increasingly demand convenient, accessible, and personalized digital banking services, putting pressure on all players to deliver.

- Market Share Erosion: Institutions lagging in digital capabilities face the risk of losing market share to more digitally adept competitors.

Central America's Banking Sector: A Digital Battleground

The competitive rivalry for BAC Holding International in Central America is intense, driven by a mix of established local banks, international players, and increasingly, agile fintech companies. This dynamic landscape means that differentiation through digital innovation and customer service is paramount for survival and growth.

The banking sector's maturity in many Central American markets, coupled with a focus on capturing the unbanked, forces institutions to compete fiercely for existing customers. For example, in 2024, many regional banks saw modest single-digit growth in net interest income, reflecting a competitive lending environment where margins are tighter.

Decreasing customer switching costs, facilitated by digital platforms and open finance initiatives, further amplifies this rivalry. Banks are responding by building integrated financial ecosystems to foster loyalty, making it harder for customers to leave.

| Competitor Type | Key Characteristics | Impact on Rivalry |

|---|---|---|

| Established Domestic Banks | Deep local market knowledge, existing customer base | Strong brand loyalty, significant market share |

| International Banks | Global expertise, access to larger capital pools | Introduce advanced products, increase competitive pressure |

| Fintech Companies | Agile digital platforms, innovative solutions | Disrupt traditional models, attract tech-savvy customers |

| Digital-first Banks | Lower overheads, seamless user experience | Challenge incumbents on cost and convenience |

SSubstitutes Threaten

Fintech Companies and Digital Wallets

Fintech companies and digital wallets are a growing threat to traditional banks. These platforms offer convenient and often cheaper alternatives for transactions, payments, and even lending. For instance, by the end of 2023, global digital payment transaction value was projected to reach over $11 trillion, demonstrating a significant shift away from traditional methods.

Digital wallets, like Apple Pay and Google Pay, are increasingly integrated into daily life, allowing consumers to make purchases without needing physical cards or visiting bank branches. This convenience directly substitutes a core service offered by BAC Holding International, potentially eroding customer loyalty and transaction volume.

Non-Bank Lending and Alternative Financing

Customers, particularly small and medium-sized enterprises (SMEs), are increasingly exploring financing options beyond traditional banks. Non-bank lenders, peer-to-peer lending platforms, and crowdfunding sites are becoming more prevalent, offering alternatives to conventional bank loans. For instance, the alternative lending market in the US alone was projected to reach over $200 billion in 2024, highlighting a significant shift in customer behavior.

Cryptocurrencies and Blockchain Solutions

While still in its early stages for everyday use, the burgeoning world of cryptocurrencies and blockchain technology presents a potential alternative to traditional financial systems. These decentralized solutions could eventually disrupt services like cross-border payments and remittances, offering a new avenue for value transfer.

Internal Corporate Finance Departments

Large corporations can develop robust internal finance departments, effectively acting as a substitute for many external corporate banking and treasury services. This self-sufficiency allows them to manage cash, debt, and investments without relying on third-party providers like BAC. For instance, a significant portion of large enterprises now possess sophisticated treasury management systems, enabling them to handle foreign exchange hedging and liquidity management internally.

The trend toward in-house financial operations has been steadily growing. In 2024, a survey indicated that over 60% of Fortune 500 companies have dedicated treasury departments capable of performing complex financial functions. This internal capability directly challenges the revenue streams of financial institutions by offering a comparable, and often more customized, alternative for core financial management tasks.

- Internal Treasury Management: Corporations can manage their own cash, liquidity, and foreign exchange exposures.

- Self-Financing Capabilities: Large entities may opt to fund operations and growth through retained earnings or direct debt issuance, bypassing traditional bank lending for certain needs.

- Technological Advancements: Sophisticated treasury management systems (TMS) empower internal teams to perform functions previously outsourced to banks.

- Cost Efficiency: For high-volume transactions, maintaining an internal department can sometimes prove more cost-effective than paying bank fees.

Informal Financial Systems

Informal financial systems, particularly prevalent in Central America, pose a significant threat of substitution for formal banking services offered by entities like BAC Holding International. These informal networks, including community savings groups and local lending circles, often cater to populations underserved by traditional institutions, providing accessible credit and savings mechanisms.

In 2024, it's estimated that a substantial portion of economic activity in some Central American nations occurs within the informal sector, highlighting the reach of these alternative financial channels. For instance, in countries like El Salvador, informal credit markets are crucial for small businesses and individuals who may not meet the stringent requirements of formal banks. This reliance on informal systems can limit the customer base and market share for formal financial institutions.

The threat is amplified by:

- Accessibility: Informal lenders often require less documentation and have more flexible repayment terms than traditional banks.

- Cost: While interest rates can be high, the overall transaction costs and time investment might be lower for users of informal finance.

- Community Trust: These systems are often built on personal relationships and community trust, which can be a powerful draw for participants.

Financial Substitutes: Reshaping the Banking Landscape

The threat of substitutes for BAC Holding International is significant, driven by evolving financial technologies and customer preferences. Digital payment platforms and fintech solutions offer convenient and often lower-cost alternatives for core banking services, impacting transaction volumes and customer loyalty.

Alternative lending channels, including peer-to-peer platforms and non-bank lenders, are increasingly capturing market share from traditional bank loans, especially among SMEs. By the end of 2023, the global digital payment transaction value was projected to exceed $11 trillion, underscoring the shift away from conventional banking methods.

Furthermore, large corporations are increasingly building internal treasury capabilities, substituting the need for many external banking services. This trend, with over 60% of Fortune 500 companies having dedicated treasury departments in 2024, directly challenges traditional revenue streams.

| Substitute Category | Key Characteristics | Impact on BAC | 2024 Market Insight |

|---|---|---|---|

| Fintech & Digital Wallets | Convenience, lower fees, mobile integration | Reduced transaction volume, potential customer attrition | Global digital payment value projected over $11 trillion (end of 2023) |

| Alternative Lending | Faster approvals, flexible terms, niche financing | Loss of loan origination and interest income | US alternative lending market projected over $200 billion (2024) |

| Internal Corporate Treasury | Cost efficiency, customization, direct control | Reduced demand for corporate banking services (cash management, FX) | Over 60% of Fortune 500 companies have dedicated treasury departments (2024) |

Entrants Threaten

Regulatory Barriers and Capital Requirements

The financial sector in Central America is heavily regulated, presenting a significant challenge for new companies looking to enter. These regulations include strict licensing procedures and substantial capital requirements, which can easily run into millions of dollars, effectively deterring many potential entrants.

For instance, in 2024, the minimum capital requirement for a new commercial bank in Guatemala was reported to be around $10 million USD, a considerable sum that acts as a powerful barrier. Navigating these complex compliance obligations adds further cost and time, making it difficult for smaller or less capitalized firms to compete.

Brand Loyalty and Trust

Established financial institutions like BAC Holding International possess significant brand loyalty and customer trust, cultivated over decades of reliable service. This deep-seated trust makes it difficult for new entrants to attract customers away from their preferred, familiar providers.

For instance, in 2024, customer retention rates for major banks in developed markets often exceed 90%, underscoring the challenge new players face in acquiring market share. Building a comparable level of confidence and recognition requires substantial investment and time.

Economies of Scale and Network Effects

Existing banks, like those within BAC Holding International's portfolio, often leverage significant economies of scale. This allows them to spread costs across a vast customer base, leading to lower per-unit operational expenses in areas such as technology infrastructure and marketing campaigns. For instance, major global banks in 2024 consistently reported billions in IT spending, a cost prohibitive for many startups.

The established presence of these institutions creates powerful network effects. A wide-reaching branch network and extensive ATM access provide convenience and accessibility that new entrants struggle to match. In 2024, the average number of branches for a large incumbent bank often numbered in the thousands, a stark contrast to the digital-first approach of many neobanks which, while growing, still face challenges in physical accessibility for certain customer segments.

Access to Talent and Technology Infrastructure

The financial services industry, particularly for entities like BAC Holding International, faces a significant barrier to entry concerning the acquisition of top-tier talent and the establishment of advanced technology infrastructure. New players must compete for skilled financial professionals, including analysts, traders, and compliance officers, often requiring substantial compensation packages and attractive benefits. In 2024, the demand for specialized fintech talent remained exceptionally high, with average salaries for AI and machine learning engineers in finance exceeding $150,000 annually in major financial hubs.

Furthermore, the capital expenditure required for robust, secure, and compliant technology is immense. This includes investments in trading platforms, cybersecurity measures, data analytics tools, and cloud computing. For instance, a new entrant aiming to offer competitive digital banking services might need to allocate upwards of $50 million to $100 million in the initial phase for technology development and implementation alone, a cost that deters many potential competitors, especially those not backed by substantial capital.

- Talent Acquisition Costs: High demand for specialized financial and tech talent drives up recruitment and retention expenses.

- Technology Infrastructure Investment: Significant upfront and ongoing costs for secure, scalable, and compliant IT systems.

- Regulatory Compliance Burden: New entrants must invest heavily in systems and personnel to meet stringent financial regulations.

- Economies of Scale in Tech: Established firms benefit from existing infrastructure, making it harder for new entrants to compete on cost.

Disruptive Fintech Startups

Disruptive fintech startups present a significant threat to established players like BAC Holding International. While regulatory hurdles can be a barrier, these agile companies often leverage innovative business models and enjoy lower operational costs. For instance, in 2024, fintech funding continued to flow into areas like digital payments and embedded finance, with venture capital investments reaching billions globally, enabling these startups to enter specific market niches with less initial capital.

These digital-first entrants can quickly gain traction by focusing on user experience and specialized services, potentially siphoning off profitable segments of the market. Their ability to operate with leaner structures allows them to offer competitive pricing or more tailored solutions. Consider the growth in Buy Now, Pay Later (BNPL) services, which saw significant adoption in 2024, demonstrating how new entrants can rapidly capture market share in traditional lending areas.

- Agile Business Models: Fintech startups can rapidly adapt and innovate, often outpacing larger, more established institutions.

- Lower Overhead: Digital-native operations reduce the need for extensive physical infrastructure, lowering cost bases.

- Niche Market Disruption: Entry into specific, high-demand areas like payments or micro-lending allows for focused customer acquisition and rapid growth.

- Capital Efficiency: Lower capital requirements for entry into certain fintech segments enable a broader range of new players to emerge.

Central American Banking: High Hurdles & Fintech's Rise

The threat of new entrants for BAC Holding International is moderate, primarily due to high capital requirements and stringent regulatory frameworks in Central America's financial sector. These barriers, including substantial licensing fees and minimum capital reserves, effectively deter many smaller players. For instance, in 2024, the minimum capital for a new bank in El Salvador was approximately $5 million USD, a significant hurdle.

Established brand loyalty and trust are also considerable deterrents; in 2024, customer retention rates for major banks often surpassed 90%, making it difficult for newcomers to attract a substantial customer base. Furthermore, existing institutions benefit from significant economies of scale, particularly in technology and marketing, which new entrants find difficult to match. For example, major banks in 2024 reported billions in annual IT spending, a cost prohibitive for startups.

However, disruptive fintech startups pose a growing challenge. Their agile business models, lower overhead, and focus on niche markets, such as digital payments, allow them to enter specific segments rapidly. Global fintech funding in 2024 reached hundreds of billions, enabling these companies to challenge incumbents, even with regulatory complexities.

| Barrier to Entry | Description | 2024 Data/Example |

|---|---|---|

| Capital Requirements | Substantial minimum capital needed to operate. | El Salvador: ~$5 million USD (new bank) |

| Regulatory Hurdles | Complex licensing, compliance, and reporting. | Extensive compliance systems and personnel costs. |

| Brand Loyalty & Trust | Established customer relationships are hard to break. | Customer retention rates >90% for major banks. |

| Economies of Scale | Lower per-unit costs due to large operational size. | Billions in annual IT spending by major banks. |

| Fintech Disruption | Agile startups entering niche markets. | Global fintech funding in the hundreds of billions. |

Porter's Five Forces Analysis Data Sources

Our BAC Holding International Porter's Five Forces analysis is built upon a foundation of comprehensive data, including official company filings, industry-specific market research reports, and reputable financial news outlets.