ATD Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

ATD Bundle

From Overview to Strategy Blueprint

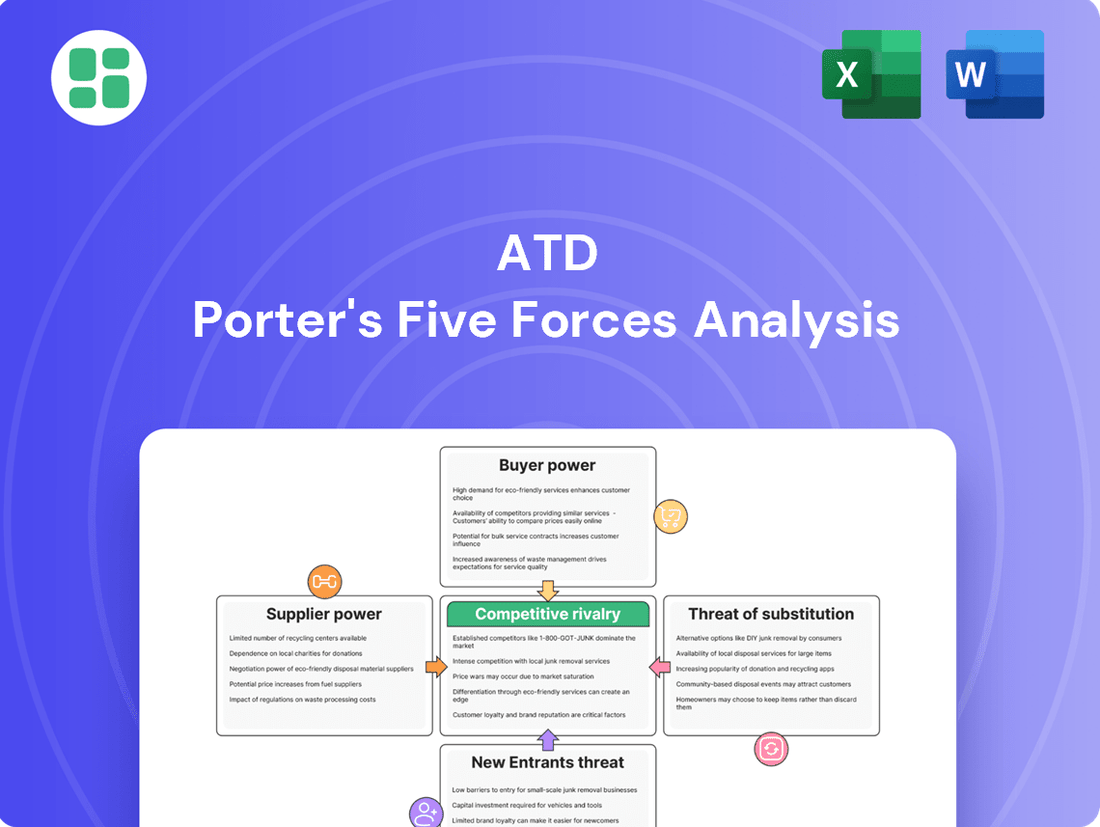

ATD's competitive landscape is shaped by five key forces: the bargaining power of buyers and suppliers, the threat of new entrants and substitutes, and the intensity of rivalry among existing competitors. Understanding these dynamics is crucial for navigating ATD's market effectively.

The complete report reveals the real forces shaping ATD’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Supplier Concentration and Scale

The tire manufacturing sector is highly consolidated, with a handful of global giants holding considerable sway. This concentration means that distributors like ATD have limited choices when it comes to sourcing popular tire brands, as these major players control a significant market share.

These dominant manufacturers leverage their immense scale to dictate terms, including pricing and product availability, to their distributors. For instance, in 2023, the top five global tire manufacturers accounted for approximately 60% of worldwide tire sales, underscoring their market power.

Brand Strength of Manufacturers

Leading tire manufacturers possess significant brand strength, fostering strong consumer recognition and loyalty. This brand equity is crucial for ATD, as its independent retail customers rely on access to these popular brands to satisfy their own clientele and remain competitive in the market. Manufacturers leverage this by knowing ATD needs their products to maintain its market position.

Switching Costs for ATD

Switching primary tire suppliers presents significant hurdles for ATD. These include the costs associated with renegotiating complex contracts, integrating new inventory management systems, and the potential for disruption to established logistics and supply chain operations. These substantial switching costs inherently limit ATD's flexibility in sourcing and bolster the bargaining power of its existing major tire manufacturer partners.

Potential for Forward Integration

The potential for tire manufacturers to integrate forward, moving into direct distribution to retailers or even end consumers, poses a significant bargaining chip. This capability allows them to bypass independent distributors like ATD, giving them leverage in price and term negotiations. For example, a major tire manufacturer could invest in its own logistics network to reach a wider customer base directly, thereby diminishing the reliance on intermediaries.

This threat of forward integration acts as a crucial deterrent, preventing ATD from exerting excessive pressure on suppliers regarding pricing or contractual terms. Manufacturers can point to their own potential to capture more of the value chain as a reason for maintaining certain margins or conditions. In 2024, the logistics and distribution sector continued to see investments in direct-to-consumer models across various industries, underscoring the viability of this strategy.

- Threat of Forward Integration: Tire manufacturers may bypass independent distributors by selling directly to retailers or consumers.

- Leverage in Negotiations: This potential integration gives manufacturers a credible point of leverage in discussions with distributors like ATD.

- Deterrent Effect: The possibility of manufacturers going direct discourages ATD from pushing for unfavorable pricing or terms.

- Industry Trend: Investments in direct-to-consumer distribution models are a growing trend, validating this strategic option.

Importance of ATD's Distribution Network

While suppliers can exert considerable bargaining power, ATD's robust distribution network across North America offers manufacturers a crucial channel to access fragmented independent retail markets. This extensive reach and sophisticated logistics are highly valued by manufacturers seeking efficient product placement.

ATD's ability to move large volumes of product reliably provides a degree of counter-leverage against suppliers. Manufacturers depend on distributors like ATD to ensure their goods reach a broad customer base effectively, creating a mutually beneficial, though often imbalanced, relationship.

- Supplier Leverage: Manufacturers often hold the stronger position due to brand recognition and the essential nature of their products in ATD's inventory.

- ATD's Network Value: ATD's distribution infrastructure is a significant asset, enabling efficient market penetration for its suppliers.

- Market Reach: The network provides access to thousands of independent retailers, a segment difficult for manufacturers to reach directly.

Supplier Power Shapes Tire Distribution Dynamics

The bargaining power of suppliers in the tire industry significantly impacts distributors like ATD. Manufacturers benefit from high industry concentration, strong brand loyalty, and substantial switching costs for distributors, allowing them to dictate terms.

The threat of forward integration, where manufacturers bypass distributors to sell directly, further amplifies supplier leverage. This dynamic limits ATD's ability to push for more favorable pricing or contract conditions.

| Factor | Impact on ATD | Supporting Data (2023/2024) |

|---|---|---|

| Supplier Concentration | Limited sourcing options, increased reliance on major players | Top 5 global tire manufacturers held ~60% market share in 2023 |

| Brand Strength | ATD needs popular brands to satisfy its customers | Brand equity is a key driver of consumer purchasing decisions |

| Switching Costs | High costs to change suppliers limit ATD's flexibility | Costs include contract renegotiation, system integration, and logistics disruption |

| Forward Integration Threat | Manufacturers can bypass ATD, increasing their negotiation power | Direct-to-consumer models saw increased investment in 2024 across industries |

What is included in the product

This analysis examines the five forces impacting ATD's competitive environment, revealing the intensity of rivalry, the power of buyers and suppliers, the threat of new entrants and substitutes, and ultimately, ATD's strategic positioning.

Quickly identify and mitigate competitive threats with a visual breakdown of industry power dynamics.

Customers Bargaining Power

Fragmented Customer Base

ATD's customer base, primarily independent tire retailers, is highly fragmented. This means there are many small, numerous customers, and no single one holds significant sway over ATD.

This widespread distribution of customers significantly dilutes the bargaining power of any individual or small group. ATD's revenue isn't dependent on a few large accounts, making it less vulnerable to price demands or unfavorable terms from any single retailer.

For instance, in 2024, ATD's extensive network likely includes thousands of independent dealers across North America, further solidifying this fragmentation and limiting individual customer leverage.

Volume of Individual Purchases

The bargaining power of ATD's customers is significantly influenced by the volume of their individual purchases. While ATD serves a vast network, many of its customers are independent retailers who, by nature, buy in smaller quantities. This fragmented customer base means that no single small retailer can exert substantial pressure on ATD for price reductions or special terms, as their individual order size is not impactful enough to warrant such concessions.

Switching Costs for Retailers

Independent tire retailers might encounter switching costs when considering alternatives to ATD. These can include the effort and expense of setting up new credit lines, learning and integrating different inventory and ordering systems, and adjusting to new delivery logistics and schedules. For example, a retailer might need to invest in new software or retrain staff on a different platform, which takes time and resources.

These operational adjustments and the time invested in building relationships with ATD can create a degree of stickiness. Retailers who have long-standing partnerships and have optimized their operations around ATD's services may find the prospect of switching less attractive. This inertia, driven by established efficiencies, can somewhat temper their bargaining power.

Furthermore, ATD's loyalty programs or preferred customer benefits can incentivize retailers to stay, reinforcing existing relationships. Trust built over time in ATD's reliability and product availability also contributes to this, making a change less appealing. In 2024, the average small business spent approximately $5,000 to $10,000 on IT system integration when switching major suppliers, a cost that independent tire retailers would need to factor in.

Availability of Alternative Distributors

Retailers can easily source tires from various regional and national distributors, or even directly from some manufacturers, diminishing their reliance on a single supplier like ATD. This access to alternatives significantly boosts their bargaining power.

When retailers have multiple options, they can leverage this to negotiate better pricing and terms with ATD. The credible threat of switching suppliers if ATD's offers aren't competitive keeps ATD focused on maintaining strong value propositions.

The competitive environment created by alternative distributors forces ATD to remain agile and responsive to market demands. For instance, in 2024, the tire distribution market saw continued consolidation, but the rise of specialized online platforms also offered independent retailers new avenues for sourcing, further fragmenting the landscape.

This availability of choice empowers independent retailers by:

- Accessing competitive pricing from multiple sources.

- Negotiating more favorable payment and delivery terms.

- Reducing dependence on any single distributor.

- Diversifying their product offerings by sourcing from various manufacturers.

Price Sensitivity of Retailers

Independent tire retailers are acutely aware of pricing, a direct result of operating in a crowded marketplace where every sale counts towards their bottom line. This constant pursuit of better margins means they actively shop around for the most favorable deals from distributors like ATD.

Their ability to easily compare pricing across various suppliers significantly amplifies their bargaining power. Retailers can quickly identify and switch to distributors offering lower prices, forcing ATD to remain competitive to secure their business. This price sensitivity directly impacts ATD’s pricing strategies and overall profitability.

- Price Sensitivity: Independent tire retailers are highly sensitive to price, often prioritizing the lowest cost to maximize their own profit margins.

- Competitive Landscape: The fragmented nature of the retail tire market intensifies price competition among distributors.

- Information Availability: Retailers have access to widespread pricing information, enabling them to negotiate effectively with suppliers.

- Impact on ATD: ATD faces pressure to offer competitive pricing to retain its customer base of independent retailers.

Independent Tire Retailers: Driving Distribution Terms

The bargaining power of ATD's customers, primarily independent tire retailers, is moderate. While the customer base is fragmented, meaning no single customer dominates, retailers can still exert influence due to market dynamics and their own price sensitivity.

Retailers can easily switch suppliers, as the market offers numerous alternatives, including regional distributors and direct manufacturer access. This ease of substitution significantly empowers them to negotiate better terms. In 2024, the tire distribution sector continued to see new online platforms emerge, providing even more sourcing options for independent dealers.

The average independent tire retailer in 2024 faced tight margins, making them highly price-sensitive and eager to secure the lowest possible wholesale prices. This sensitivity means they actively compare ATD's pricing with competitors, using this information to negotiate.

| Factor | Assessment | Impact on ATD |

|---|---|---|

| Customer Fragmentation | High | Limits individual customer power, but collective action is possible. |

| Switching Costs | Low to Moderate | Retailers can switch with some effort, but established relationships offer some stickiness. |

| Availability of Alternatives | High | Numerous distributors and direct sourcing options increase customer leverage. |

| Price Sensitivity | High | Retailers actively seek lower prices, pressuring ATD on margins. |

Full Version Awaits

ATD Porter's Five Forces Analysis

This preview showcases the complete ATD Porter's Five Forces Analysis, offering a thorough examination of competitive forces within the association's landscape. The document you see here is the exact, professionally formatted analysis you will receive instantly upon purchase, providing actionable insights without any surprises or placeholders.

Rivalry Among Competitors

Number and Size of Competitors

The North American tire distribution landscape is characterized by a substantial number of competitors, ranging from national powerhouses like U.S. AutoForce and National Tire Wholesale (NTW) to a multitude of smaller, regional players. This fragmentation means that no single entity dominates, fostering a highly competitive environment.

This multi-player field intensifies rivalry as each distributor actively competes for the business of independent tire retailers. The presence of these numerous significant players ensures that price, service, and product availability are constant battlegrounds for market share.

Industry Growth Rate

The tire distribution industry generally sees moderate growth, closely mirroring trends in vehicle sales and miles driven. For instance, in 2024, the global automotive market is projected to grow, which in turn supports demand for replacement tires. This mature, slower-growing market environment naturally fuels more intense competition among established players.

When market expansion isn't readily available, companies are compelled to vie more aggressively for existing market share. This dynamic often translates into sharper pricing strategies and a greater emphasis on differentiating through superior customer service or specialized offerings to capture a larger piece of the pie.

Product and Service Differentiation

While the fundamental product, tires, is largely standardized across the industry, distributors like ATD actively differentiate themselves. They achieve this through an extensive brand portfolio, ensuring a wide selection for various customer needs. Furthermore, ATD focuses on superior logistical efficiency, getting the right tires to the right place at the right time, which is a critical differentiator in the fast-paced automotive sector.

Beyond product availability, ATD enhances its competitive standing with valuable services. These include offering training programs for technicians, providing marketing support to help dealers grow their businesses, and delivering exceptional customer service. These business solutions are not just add-ons; they are integral to ATD's strategy to stand out from competitors.

The effectiveness of ATD's differentiation efforts directly impacts the intensity of rivalry. When distributors successfully offer unique value propositions, they can lessen the pressure of price-based competition. Conversely, if offerings become too similar, the market can easily devolve into a battle solely on price, eroding profitability for all players.

High Fixed Costs and Capacity

The beverage distribution industry, including players like Coca-Cola Europacific Partners (CCEP), operates with substantial fixed costs. These are tied to maintaining an extensive network of warehouses, managing large inventories, and operating a significant fleet of delivery trucks. For instance, CCEP's capital expenditures in 2023 alone were €1.3 billion, largely supporting its operational infrastructure.

These high fixed costs necessitate high capacity utilization for profitability. This pressure drives intense competition among distributors, often leading to aggressive pricing strategies, especially when demand falters. Distributors are compelled to fill their capacity, making them susceptible to price wars as they try to secure sales volume.

- Significant Fixed Costs: Beverage distributors invest heavily in warehousing, logistics, and delivery fleets, creating a high barrier to entry and ongoing operational expenses.

- Capacity Utilization Imperative: To cover these fixed costs, distributors must achieve high utilization rates for their assets, pushing them to compete aggressively for market share.

- Price Sensitivity: Periods of lower demand can trigger price wars as distributors fight to maintain sales volume and avoid underutilizing their expensive infrastructure.

Exit Barriers

The tire distribution industry presents significant exit barriers, largely due to specialized assets like extensive warehouse networks and dedicated logistics infrastructure. These capital-intensive requirements make it difficult and costly for companies to divest or repurpose their operations. For instance, the average investment in a large-scale tire distribution center can easily run into millions of dollars, a substantial sum that deters quick exits.

Established relationships with tire manufacturers and a broad customer base further cement these barriers. Severing these long-standing ties can damage reputations and future business prospects, making a clean break challenging. In 2024, many mid-sized distributors reported that over 70% of their business was tied to long-term contracts or preferred supplier agreements, highlighting the difficulty of simply walking away.

Consequently, companies facing financial difficulties often remain in the market, continuing to compete rather than exiting. This persistence prolongs competitive intensity, even during periods of reduced demand or profitability. As a result, the industry often experiences prolonged periods of rivalry, as firms fight to maintain market share rather than incur substantial losses by exiting.

- Specialized Assets: High capital investment in warehouses and logistics infrastructure.

- Established Relationships: Long-term ties with manufacturers and customers create switching costs.

- Prolonged Rivalry: Difficulty exiting means struggling firms remain, intensifying competition.

North American Tire Distribution: A Fiercely Competitive Landscape

The North American tire distribution market is highly competitive, featuring numerous national and regional players vying for market share. This intense rivalry is driven by a mature industry with moderate growth, forcing companies to compete aggressively on price, service, and product availability to capture existing demand.

Differentiation through broad brand portfolios, efficient logistics, and value-added services like technician training and marketing support is crucial for distributors to stand out. Success in these areas can mitigate price-based competition, while a lack of differentiation can lead to profitability erosion.

High fixed costs in areas like warehousing and delivery fleets necessitate high capacity utilization, further fueling competitive pressures. This often results in aggressive pricing, particularly during periods of lower demand, as distributors strive to maintain sales volume and cover their operational expenses.

Significant exit barriers, stemming from specialized assets and established relationships, mean that even struggling companies tend to remain in the market. This persistence prolongs competitive intensity, as firms fight to maintain their position rather than incur substantial losses from exiting.

| Distributor Type | Key Competitors | Differentiation Factors | Competitive Intensity Driver |

|---|---|---|---|

| National | U.S. AutoForce, NTW | Brand Portfolio, Logistics, Value-Added Services | Mature Market Growth |

| Regional/Smaller | Numerous independent players | Niche Offerings, Local Service | Price Competition |

| Industry Characteristic | High Fixed Costs | Capacity Utilization | Price Wars |

SSubstitutes Threaten

Alternative Distribution Models

The rise of direct-to-consumer (D2C) channels by tire manufacturers, coupled with the expansion of online tire retailers, poses a substantial threat of substitution for traditional distributors like ATD. These alternative models provide consumers with new avenues to acquire tires, often circumventing the independent retail networks that ATD relies upon. For instance, in 2024, online tire sales continued to capture a larger market share, with some reports indicating a double-digit percentage growth year-over-year in this segment, directly impacting the volume of business flowing through established distribution channels.

Technological Advancements in Tires

Technological advancements in tire manufacturing present a significant threat of substitution for traditional tire distribution services. Innovations like self-repairing tires or those with significantly extended lifespans, such as Michelin's Uptis prototype, could drastically reduce the frequency of tire replacements. For instance, if a new tire technology allows for a 50% increase in average tire life, the overall demand for tire replacements in the market could decrease by a similar margin over time.

This reduction in replacement cycles directly impacts the volume of business for tire distributors. Less frequent purchases by consumers and fleet operators translate to fewer transactions and potentially lower revenue streams for companies like ATD. The market for tire distribution services is inherently tied to the volume of tires sold, and innovations that decrease this volume pose a direct threat to the existing business model.

Changes in Transportation Patterns

Long-term shifts in how people get around, like a growing preference for ride-sharing services or more reliance on public transit, can directly impact the demand for replacement tires. If fewer people own and drive their own cars, the overall miles driven decrease, leading to a reduced need for new tires.

For instance, by 2024, ride-sharing services like Uber and Lyft have become deeply integrated into urban transportation networks globally, with millions of rides completed daily. This trend, coupled with increased investment in public transportation infrastructure in many cities, signals a potential long-term substitution for individual car ownership and, by extension, a dampening effect on the replacement tire market.

Retreaded or Used Tires

The threat of substitutes for new tires, particularly retreaded and used tires, presents a significant challenge for companies like ATD. For commercial fleets, retreaded tires can offer substantial cost savings compared to new ones. For instance, the retreading process can cost significantly less than manufacturing a new tire, making it an attractive option for budget-conscious businesses. This segment of the market is highly sensitive to price, and the availability of these alternatives directly impacts the demand for new tires.

Used tires also serve as a very low-cost substitute, especially for individual consumers who may not require the performance or longevity of new tires. While ATD's primary business is in new tire distribution, the existence of these lower-priced options can shrink the overall addressable market for new tires. This competitive pressure can limit ATD's ability to command premium pricing, especially in segments where cost is a primary purchasing driver.

The economic conditions in 2024 further amplify this threat. With ongoing inflationary pressures and a focus on cost efficiency across many industries, the appeal of retreaded and used tires is likely to increase. For example, reports from the tire industry in early 2024 indicated a growing interest in sustainable and cost-effective tire solutions, which directly benefits the retreading sector.

- Cost Savings: Retreaded tires can be up to 50% cheaper than new tires, making them a compelling alternative for commercial vehicle operators.

- Market Erosion: The availability of used tires, often sold at a fraction of the new tire price, directly reduces the market share for new tire distributors.

- Price Sensitivity: In price-sensitive segments, the cost advantage of substitutes can force new tire providers to lower their profit margins.

- Sustainability Trends: Growing environmental awareness and the desire for circular economy solutions are boosting the adoption of retreaded tires.

Future Tire Technologies

The development of novel tire technologies, such as airless tires or integrated wheel-tire systems, presents a significant long-term threat. While these are still in early stages, their potential to disrupt the traditional tire replacement market is substantial.

If these advanced systems gain widespread adoption, they could bypass the existing distribution channels for conventional pneumatic tires, fundamentally changing how vehicles are equipped and maintained.

- Emerging Technologies: Airless tires and integrated wheel-tire systems are key examples of potential substitutes.

- Market Disruption: Widespread adoption could eliminate the need for traditional tire replacement and distribution networks.

- Industry Impact: This represents a disruptive force that could redefine the automotive aftermarket and tire manufacturing sectors.

Disruptors Redefine Tire Distribution: Cost, Tech, & Mobility

The threat of substitutes for ATD is multifaceted, encompassing alternative sales channels, innovative tire technologies, evolving transportation habits, and the persistent appeal of retreaded and used tires. These substitutes directly challenge the traditional distribution model by offering cost advantages, reduced replacement frequency, or entirely new ways of vehicle mobility. For instance, the growing popularity of ride-sharing services in urban areas in 2024, with millions of daily rides globally, signifies a shift away from individual car ownership, impacting the overall demand for replacement tires.

The cost-effectiveness of retreaded tires, which can be up to 50% cheaper than new ones, makes them a particularly strong substitute, especially for price-sensitive commercial fleets. Similarly, used tires offer a low-cost alternative for consumers. In 2024, economic pressures and a focus on cost efficiency have likely amplified the demand for these budget-friendly options, further eroding the market share for new tires.

Technological advancements, such as airless tires, also represent a future substitute that could bypass conventional distribution networks. The increasing market share of online tire retailers and the rise of direct-to-consumer models further fragment the market, presenting new avenues for tire acquisition that bypass traditional distributors.

| Substitute Type | Key Characteristic | Impact on ATD | 2024 Relevance |

|---|---|---|---|

| Online Retail/D2C | Convenience, potentially lower prices | Reduced direct sales volume | Continued market share growth |

| Retreaded Tires | Cost savings (up to 50%) | Erosion of new tire demand, particularly in commercial segments | Increased demand due to economic pressures |

| Used Tires | Very low cost | Shrinks addressable market for new tires, limits pricing power | Strong appeal in price-sensitive consumer segments |

| Alternative Mobility | Reduced car usage (ride-sharing, public transit) | Lower overall miles driven, thus less tire wear and replacement demand | Deep integration into urban transport networks |

| Advanced Tire Tech (e.g., Airless) | Extended lifespan, different maintenance needs | Potential long-term disruption of replacement cycles and distribution | Early-stage development, but significant future threat |

Entrants Threaten

High Capital Investment Required

Establishing a national tire distribution network, much like ATD's, necessitates a considerable capital outlay. This includes significant investments in warehousing facilities, maintaining a diverse and robust inventory, operating a dedicated fleet of delivery vehicles, and implementing advanced IT infrastructure for efficient operations. For instance, building a network of regional distribution centers can easily run into tens of millions of dollars, a figure that presents a formidable hurdle for aspiring competitors.

This substantial upfront financial commitment acts as a powerful barrier to entry. Potential new entrants often find it challenging to amass the necessary capital to match the scale and reach of established players like ATD. Consequently, the high capital requirement effectively deters many smaller or less-funded companies from attempting to enter the market, thus protecting ATD from widespread new competition.

Economies of Scale for Existing Players

The threat of new entrants is significantly mitigated by the substantial economies of scale enjoyed by established players like ATD. Their sheer volume in purchasing, optimizing logistics, and streamlining operations creates a cost advantage that is difficult for newcomers to match. For instance, ATD’s extensive distribution network, boasting thousands of locations, allows for bulk purchasing discounts and highly efficient delivery routes, driving down per-unit costs.

New companies entering the market would find it incredibly challenging to achieve comparable cost efficiencies in the short to medium term. This cost disparity would force them to operate at a significant disadvantage, likely requiring them to absorb losses for an extended period to build market share and scale. This financial hurdle acts as a strong deterrent, making entry less appealing.

Established Relationships and Brand Loyalty

ATD's deep-rooted relationships with tire manufacturers and independent retailers create a significant barrier. These established connections are built on years of trust and reliability, making it challenging for new players to gain traction. For instance, in 2024, the tire distribution industry continued to show consolidation, with larger players like ATD leveraging their existing networks to secure favorable terms, further entrenching their market position.

Complex Logistics and Supply Chain Management

The tire industry's intricate logistics and supply chain management present a significant hurdle for potential new entrants. Effectively storing, sorting, and distributing a diverse inventory of tire sizes, brands, and types across expansive territories demands highly sophisticated operational capabilities. Developing these robust supply chain networks requires substantial upfront investment and specialized expertise, acting as a considerable barrier to entry. This complexity extends beyond mere transportation; it encompasses advanced inventory management, warehousing strategies, and last-mile delivery optimization. For example, in 2024, the global tire market, valued at over $250 billion, relies heavily on efficient logistics to meet consumer and industrial demand, underscoring the capital-intensive nature of establishing such infrastructure from scratch.

New players must contend with the sheer scale and complexity involved in managing a wide range of tire SKUs. This includes catering to everything from passenger car tires to heavy-duty industrial and agricultural tires, each with unique storage and handling requirements. Building the necessary warehousing, fleet management, and technological systems to support this can easily run into hundreds of millions of dollars. Furthermore, the need for specialized handling to prevent damage and ensure product integrity adds another layer of operational challenge. The investment in technology for real-time tracking and inventory visibility is also critical, with many leading tire distributors in 2024 leveraging advanced analytics and AI to optimize their supply chains.

- Significant Capital Investment: Establishing a nationwide distribution network for tires requires substantial investment in warehouses, transportation fleets, and inventory, often exceeding hundreds of millions of dollars.

- Operational Expertise: Successfully managing the complexities of tire storage, sorting, and delivery necessitates deep expertise in logistics, supply chain optimization, and inventory management.

- Technological Integration: Modern tire logistics rely on advanced technology for tracking, inventory control, and route optimization, demanding significant IT infrastructure development.

- Geographic Reach: Covering a wide geographic area with a diverse product range means building a complex, multi-regional supply chain, which is a considerable undertaking for any new entrant.

Regulatory Hurdles and Compliance

The tire industry faces significant regulatory hurdles that act as a barrier to new entrants. These include stringent safety standards, such as those mandated by the National Highway Traffic Safety Administration (NHTSA) in the US, which require rigorous testing and certification for tire performance and durability. For instance, NHTSA's Uniform Tire Quality Grading (UTQG) system sets benchmarks for treadwear, traction, and temperature resistance, demanding substantial investment in research and development to meet these specifications.

Environmental regulations also add complexity. The European Union's REACH (Registration, Evaluation, Authorisation and Restriction of Chemicals) regulation impacts the chemical compounds used in tire manufacturing, requiring extensive data submission and potentially limiting the use of certain substances. Compliance with these rules, along with waste management and recycling mandates, increases operational costs and requires specialized expertise. In 2023, for example, the global tire market size was valued at approximately USD 270 billion, with a significant portion of that value attributed to the costs associated with meeting these diverse regulatory requirements.

- Safety Standards: Compliance with NHTSA UTQG ratings and other international safety certifications requires significant upfront investment in product development and testing.

- Environmental Regulations: Adhering to rules like EU REACH and waste disposal directives necessitates specialized knowledge and potentially costly process modifications.

- Transportation and Labeling: Meeting specific transportation regulations and accurate product labeling requirements across different global markets adds further layers of complexity and cost.

Tire Distribution: A Fortress of Capital and Scale

The threat of new entrants into the tire distribution market, particularly for a national player like ATD, is significantly constrained by the immense capital required. Building a robust distribution network, complete with warehouses, a fleet, and sophisticated IT systems, represents a barrier often in the tens or hundreds of millions of dollars. This financial hurdle, combined with the need for operational expertise in managing complex logistics and adhering to stringent regulations, makes it exceptionally difficult for newcomers to compete effectively. For instance, in 2024, the tire industry's ongoing consolidation further solidified the advantages of scale, making it even harder for smaller entities to gain a foothold.

| Barrier Type | Description | Estimated Cost/Impact |

|---|---|---|

| Capital Investment | Establishing nationwide warehousing, fleet, and IT infrastructure. | Hundreds of millions of dollars. |

| Economies of Scale | Lower per-unit costs due to high volume purchasing and optimized logistics. | Significant cost advantage for established players. |

| Supplier Relationships | Long-standing trust and favorable terms with tire manufacturers and retailers. | Difficult for new entrants to replicate in 2024. |

| Regulatory Compliance | Meeting safety (NHTSA) and environmental (REACH) standards. | Requires substantial R&D and process modification costs. |

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis is built upon a foundation of comprehensive data, including company annual reports, industry-specific market research, and government economic indicators, to provide a robust understanding of competitive dynamics.