Antero Midstream Partners Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Antero Midstream Partners Bundle

Don't Miss the Bigger Picture

Antero Midstream Partners operates within a sector characterized by significant capital investment and regulatory oversight, influencing the intensity of rivalry and the threat of new entrants. Understanding the bargaining power of both suppliers and buyers is crucial for navigating this complex landscape.

The complete report reveals the real forces shaping Antero Midstream Partners’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

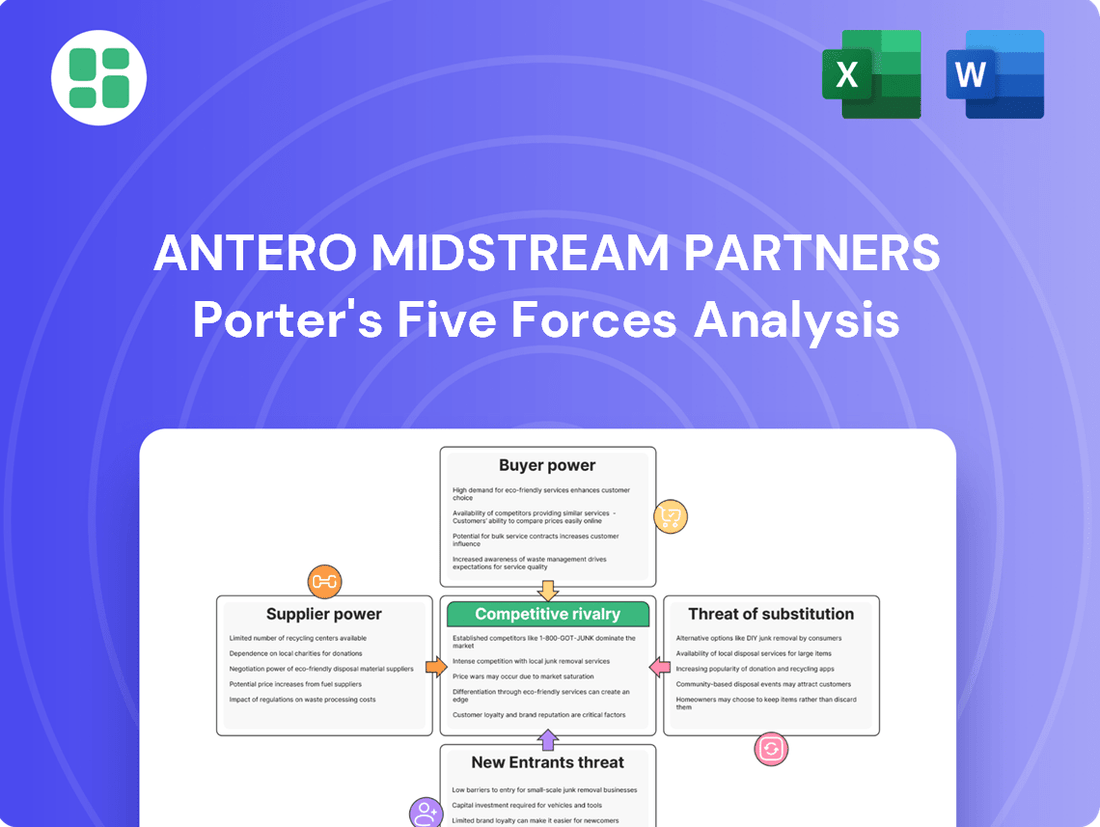

Suppliers Bargaining Power

Supplier Concentration and Uniqueness

The bargaining power of suppliers for Antero Midstream Partners leans towards moderate to high, especially when it comes to specialized equipment and services crucial for their operations. Suppliers who offer unique or proprietary technology for natural gas compression, processing, or water treatment infrastructure naturally hold more sway in negotiations.

The degree to which alternative suppliers exist for these critical components significantly impacts this leverage. For instance, in 2024, a shortage of specialized compression units, driven by increased demand across the energy sector, could elevate the bargaining power of the few manufacturers capable of producing them.

Switching Costs for Antero Midstream

Switching costs for Antero Midstream can be substantial if its midstream infrastructure, like pipelines and processing facilities, is deeply integrated with specific supplier technologies or requires proprietary parts for maintenance. This integration can make it difficult and costly to switch to alternative suppliers for critical components or services.

Antero Midstream's reliance on long-term contracts with key suppliers for essential materials, such as specialized steel for pipelines or advanced compressor station equipment, can also bolster supplier bargaining power. For example, in 2023, Antero Midstream reported capital expenditures of approximately $600 million, a significant portion of which would involve procurement from these specialized suppliers.

Availability of Substitutes for Supplier Inputs

While Antero Midstream Partners likely sources many standard materials from a broad supplier base, the availability of substitutes for specialized inputs significantly impacts supplier bargaining power. For instance, while generic steel for pipelines might have numerous suppliers, advanced drilling fluids or highly specialized compression equipment could have a more concentrated supplier market, increasing their leverage.

Importance of Antero Midstream to Suppliers

Antero Midstream's substantial scale and the ongoing need for midstream infrastructure development and maintenance position it as a crucial customer for numerous suppliers. This significant demand can indeed temper the bargaining power of these suppliers, particularly those whose revenue streams are heavily reliant on Antero's operations. When suppliers depend significantly on Antero, it can lead to more competitive pricing as they vie for the company's consistent business.

For example, Antero Midstream's capital expenditures in 2023 were approximately $600 million, a substantial portion of which was allocated to infrastructure projects. This consistent investment cycle means suppliers of materials like steel pipe, specialized equipment, and construction services benefit from a predictable revenue stream. This predictability can reduce their need to exert strong pricing power, as Antero's consistent demand provides a stable market.

- Scale of Operations: Antero Midstream's extensive network of pipelines and processing facilities requires a continuous supply of goods and services, making it a key client for many in the sector.

- Consistent Demand: The company's ongoing development and maintenance needs create a reliable demand for suppliers, potentially increasing Antero's leverage in price negotiations.

- Supplier Dependence: Suppliers heavily reliant on Antero's contracts may find their bargaining power diminished due to the risk of losing a major customer.

- Competitive Landscape: The presence of multiple capable suppliers vying for Antero's business further contributes to a more favorable pricing environment for the company.

Threat of Forward Integration by Suppliers

The threat of suppliers integrating forward into midstream operations for Antero Midstream Partners (AM) is typically low. This is largely because the capital required to build and operate pipelines and processing facilities is substantial, and the regulatory environment is complex. For instance, constructing a new natural gas pipeline can easily cost hundreds of millions, if not billions, of dollars, creating a significant barrier to entry for most suppliers.

However, there's a potential for certain suppliers, particularly large industrial equipment manufacturers, to pose a limited threat. These companies could develop and offer more comprehensive, integrated solutions. Imagine a scenario where a major pipe manufacturer also offers pre-fabricated processing modules, potentially reducing Antero's direct control over the selection and integration of specific operational components.

While this forward integration by suppliers isn't a dominant force, it's a factor Antero Midstream must monitor. The sheer scale of investment needed for midstream infrastructure means that traditional suppliers are unlikely to become direct competitors. Yet, shifts in manufacturing capabilities and service offerings could subtly alter the competitive landscape.

- High Capital Intensity: Building midstream infrastructure like pipelines requires billions in investment, deterring most suppliers from forward integration.

- Regulatory Hurdles: Navigating environmental permits and operational regulations for midstream assets is a significant barrier for potential integrating suppliers.

- Potential for Integrated Solutions: Large equipment manufacturers might offer combined product and service packages, indirectly impacting Antero's operational control.

Antero Midstream: Supplier Power, Specialized Needs, and Strategic Procurement

The bargaining power of suppliers for Antero Midstream Partners is generally moderate, influenced by the availability of specialized equipment and services. While Antero's significant scale and consistent demand can provide leverage, the specialized nature of some midstream components means suppliers of these critical items can command higher prices. For example, in 2023, Antero Midstream's capital expenditures of approximately $600 million highlight its substantial procurement needs, which can influence supplier pricing strategies.

The existence of alternative suppliers for essential materials and services plays a crucial role in determining supplier leverage. If Antero Midstream relies on a limited number of providers for highly specialized technology, such as advanced compressor units or proprietary processing equipment, these suppliers gain considerable bargaining power. Conversely, for more commoditized inputs like standard steel for pipelines, a wider supplier base generally limits individual supplier influence.

Switching costs also impact supplier power; if Antero's infrastructure is deeply integrated with specific supplier technologies, the expense and complexity of changing providers can make suppliers more indispensable. However, Antero's consistent capital investment, exemplified by its 2023 spending, suggests a steady demand that can foster more competitive supplier relationships, especially where multiple capable vendors exist.

The threat of suppliers integrating forward into midstream operations for Antero Midstream is low due to the immense capital and regulatory hurdles. Building and operating pipelines or processing facilities requires billions in investment and complex permitting, deterring most suppliers. While some large equipment manufacturers might offer more integrated solutions, this is a limited concern compared to the high barriers to direct entry.

| Factor | Impact on Antero Midstream | 2023/2024 Data/Context |

|---|---|---|

| Specialized Equipment Availability | Moderate to High Supplier Power | Shortages of specialized compression units in 2024 could increase supplier leverage. |

| Switching Costs | Moderate to High Supplier Power | Deep integration of proprietary technologies can make switching difficult and costly. |

| Supplier Dependence on Antero | Low to Moderate Supplier Power | Antero's significant scale and consistent demand can temper supplier pricing power. |

| Forward Integration Threat | Low | High capital intensity and regulatory complexity deter suppliers from direct midstream operations. |

What is included in the product

This analysis reveals Antero Midstream Partners' competitive environment, highlighting the bargaining power of its customers and suppliers, the threat of new entrants and substitutes, and the intensity of rivalry within the midstream sector.

Antero Midstream Partners' Porter's Five Forces analysis provides a clear, actionable framework to navigate competitive pressures, offering a strategic roadmap for sustainable growth.

This analysis helps Antero Midstream identify and mitigate threats from rivals, new entrants, and substitute products, ultimately strengthening its market position.

Customers Bargaining Power

Customer Concentration

Antero Midstream Partners faces significant bargaining power from its customers, largely due to customer concentration. A prime example is Antero Resources, a major producer and a substantial shareholder in Antero Midstream. This close relationship means a significant portion of Antero Midstream's revenue is directly linked to Antero Resources' operational success and contractual agreements.

In 2024, Antero Resources' role as the primary customer for Antero Midstream's gathering and processing services underscores this dynamic. The long-term nature of their contracts, often structured to align with Antero Resources' production volumes, grants Antero Resources considerable leverage in negotiations. This concentration inherently limits Antero Midstream's ability to diversify its revenue streams away from its largest client, intensifying the impact of any pricing or contract term disputes.

Volume of Purchases by Customers

Antero Resources' significant production volumes, particularly in natural gas and NGLs from the Appalachian Basin, create substantial demand for Antero Midstream's infrastructure. In 2023, Antero Resources continued to be a primary customer, underscoring the impact of this volume on Antero Midstream's operations.

These large volumes, often secured through long-term agreements, grant Antero Resources considerable leverage. This customer's commitment ensures consistent revenue for Antero Midstream but also emphasizes the customer's significant bargaining power.

Switching Costs for Customers

For Antero Resources, the costs associated with switching midstream providers are substantial. This is primarily due to the highly integrated nature of their operations, which rely on dedicated infrastructure and long-term contracts. These factors create significant barriers to entry for alternative providers and lock in Antero Resources, thereby reducing their leverage.

Customer's Ability to Backward Integrate

The bargaining power of customers, specifically their ability to backward integrate, is a key consideration for Antero Midstream Partners. While Antero Resources, the upstream producer, could theoretically develop its own midstream assets, this path is extremely capital-intensive and moves away from its core business of exploration and production.

The existing, deeply intertwined contractual relationship and Antero Resources' significant ownership stake in Antero Midstream significantly diminish the incentive and practicality of pursuing backward integration. This shared interest and established infrastructure make such a move economically unappealing.

- High Capital Requirements: Building midstream infrastructure requires billions in investment, a substantial hurdle for an upstream producer.

- Core Competency Mismatch: Antero Resources' expertise lies in drilling and extraction, not pipeline construction and operation.

- Existing Synergies: The current partnership structure already provides Antero Resources with the midstream services it needs efficiently.

Price Sensitivity of Customers

While Antero Midstream Partners' revenue streams are primarily secured through long-term contracts, the underlying profitability of its main customer, Antero Resources, is directly tied to volatile commodity prices. In 2024, the average spot price for natural gas hovered around $2.50 per MMBtu, significantly impacting Antero Resources' margins.

This price sensitivity can translate into customer bargaining power. If Antero Resources faces periods of sustained low natural gas and NGL prices, it might seek to renegotiate service fees with Antero Midstream, provided its contracts allow for such adjustments. However, the prevalence of long-term, fixed-fee agreements in the midstream sector generally mitigates this pressure to a considerable extent.

- Price Sensitivity Impact: Antero Resources' profitability is directly linked to natural gas and NGL prices, influencing its capacity to absorb midstream service fees.

- Contractual Safeguards: Long-term, fixed-fee contracts between Antero Midstream and Antero Resources significantly limit the customer's ability to exert downward pressure on fees.

- Market Conditions in 2024: The average natural gas spot price in 2024, around $2.50/MMBtu, highlights the economic environment Antero Resources operates within and its potential impact on fee negotiations.

Customer Leverage Shapes Midstream Negotiations

Antero Midstream Partners' customer bargaining power is significantly influenced by its concentrated customer base, with Antero Resources being the dominant client. This relationship, solidified by substantial ownership and long-term contracts, grants Antero Resources considerable leverage in negotiating terms and pricing for gathering and processing services.

The sheer volume of production Antero Resources brings to Antero Midstream, particularly from the Appalachian Basin, creates a strong dependency. For instance, in 2023, Antero Resources remained a primary customer, highlighting the critical role its production plays in Antero Midstream's revenue generation and operational capacity.

While Antero Resources' profitability is tied to volatile commodity prices, as seen with natural gas spot prices around $2.50/MMBtu in 2024, the structure of their long-term, fixed-fee contracts generally shields Antero Midstream from direct price-based renegotiations, thereby limiting customer bargaining power on fees.

| Customer | Key Services Provided | Contractual Terms | Impact on Bargaining Power |

|---|---|---|---|

| Antero Resources | Gathering and Processing | Long-term, Fixed-fee | High due to concentration and volume |

| Antero Resources | NGL Fractionation | Long-term, Fixed-fee | High due to concentration and volume |

Preview the Actual Deliverable

Antero Midstream Partners Porter's Five Forces Analysis

This preview showcases a comprehensive Porter's Five Forces analysis for Antero Midstream Partners, detailing the competitive landscape within the midstream energy sector. You'll gain insights into the bargaining power of suppliers and buyers, the threat of new entrants, the intensity of rivalry among existing players, and the threat of substitute products or services. The document displayed here is the part of the full version you’ll get—ready for download and use the moment you buy.

Rivalry Among Competitors

Number and Size of Competitors

The midstream sector in the Appalachian Basin, Antero Midstream's primary operational area, is characterized by the presence of several well-established competitors. While Antero Midstream benefits from its strong relationship with Antero Resources, other significant midstream companies also maintain operations in this lucrative region.

This competitive landscape means Antero Midstream isn't the sole provider of essential midstream services. Companies like Enterprise Products Partners, Energy Transfer, and Boardwalk Pipeline Partners are also active players in the Appalachian Basin, each with their own extensive infrastructure networks and customer relationships.

The presence of these larger, diversified midstream entities, alongside more specialized regional operators, intensifies competition for securing contracts and market share. This dynamic environment necessitates continuous investment in infrastructure and operational efficiency to maintain a competitive edge.

Industry Growth Rate

The U.S. midstream sector, especially for natural gas, is seeing a healthy growth spurt. This is largely thanks to the rising demand for liquefied natural gas (LNG) exports and the energy needs of power generation, including the burgeoning data center industry. For example, U.S. LNG exports reached record highs in 2023, underscoring this demand.

This expanding market can actually ease competitive rivalry, as there’s more pie for everyone to share. However, in key regions like Appalachia, existing capacity limitations for natural gas pipelines might actually heat up competition. Companies will likely vie more intensely for the chance to build out new infrastructure to meet this growing demand.

Product and Service Differentiation

While some midstream services like gathering and processing can feel like commodities, Antero Midstream distinguishes itself through a highly integrated system. This integration, coupled with a focus on capital efficiency, allows them to manage costs effectively. Furthermore, their long-term dedications with Antero Resources, their primary customer, create a stable revenue stream and reduce the impact of market fluctuations.

Exit Barriers for Competitors

Antero Midstream Partners operates within a sector characterized by substantial exit barriers. The immense capital outlay required for constructing and maintaining extensive pipeline networks and processing facilities makes it incredibly difficult and expensive for competitors to leave the market. This high fixed cost structure is a significant deterrent.

These high exit barriers mean that even when market conditions are unfavorable, competitors are often compelled to remain operational. This persistence ensures that competitive pressure remains a constant factor for Antero Midstream, as rivals are unlikely to simply cease operations and reduce capacity. For instance, the midstream sector saw significant investment in infrastructure expansion leading up to 2023, creating a large installed base of assets that are not easily decommissioned.

- Significant Capital Investment: The construction of long-haul pipelines and sophisticated processing plants represents billions of dollars in sunk costs, making divestiture or abandonment economically unfeasible for many players.

- Long-Term Contracts: Many midstream companies, including Antero Midstream, operate under long-term, fee-based contracts with producers. These agreements provide revenue stability but also lock competitors into ongoing operational commitments.

- Specialized Infrastructure: The highly specialized nature of midstream assets, designed for specific types of hydrocarbons and geographic locations, limits their utility and resale value outside their intended purpose, further increasing exit costs.

Strategic Commitments and M&A Activity

Antero Midstream Partners, like many in the midstream sector, is navigating a landscape shaped by a strong emphasis on financial discipline and debt reduction. This focus influences their strategic decisions, including how they approach growth opportunities and potential mergers and acquisitions. The goal is often to strengthen their financial footing while selectively pursuing expansion.

The midstream industry continues to see merger and acquisition (M&A) activity, with a particular trend towards bolt-on acquisitions. These smaller, strategic purchases can help companies consolidate their market position and expand their network reach. For instance, in 2024, Antero Midstream itself completed a significant transaction, acquiring the remaining stake in its joint venture, effectively consolidating its operations and demonstrating a commitment to strategic growth within its existing footprint.

- Focus on Financial Discipline: Midstream companies are prioritizing deleveraging and improving cash flow generation.

- Strategic Growth Initiatives: Companies are evaluating growth opportunities, including organic projects and targeted acquisitions.

- M&A Activity: Bolt-on acquisitions are a key strategy for market consolidation and network expansion.

- Competitive Landscape Impact: M&A can intensify or reduce rivalry depending on the nature and scale of the transactions.

Midstream Market Dynamics: Rivalry, Investment, and Strategic Growth

Competitive rivalry within Antero Midstream's operational sphere is moderate but impactful, driven by established players and the capital-intensive nature of the midstream sector. While Antero's integrated model and long-term contracts with Antero Resources provide a stable foundation, the presence of large, diversified competitors like Enterprise Products Partners and Energy Transfer in the Appalachian Basin necessitates ongoing investment and efficiency to secure market share.

The substantial capital required for midstream infrastructure, coupled with long-term contractual commitments, creates high exit barriers, ensuring that competitors remain in the market even during downturns. This persistence maintains a consistent level of rivalry, as companies are incentivized to operate and compete for new projects and contracts, especially given the growing demand for natural gas driven by LNG exports and data centers.

Antero Midstream's strategic focus on financial discipline and bolt-on acquisitions, such as its 2024 acquisition of the remaining stake in a joint venture, aims to consolidate its position and enhance competitiveness. This strategic maneuvering within the M&A landscape can either intensify or alleviate rivalry depending on the scale and impact of these transactions on market capacity and participant numbers.

| Competitor | Primary Operational Area | Key Strengths |

|---|---|---|

| Antero Midstream Partners | Appalachian Basin | Integrated system, long-term dedications with Antero Resources, capital efficiency |

| Enterprise Products Partners | Appalachian Basin and broader U.S. | Extensive infrastructure network, diversified services, strong market presence |

| Energy Transfer | Appalachian Basin and broader U.S. | Large-scale pipeline network, significant NGL processing capacity |

| Boardwalk Pipeline Partners | Appalachian Basin and other regions | Natural gas transportation, diverse customer base |

SSubstitutes Threaten

Alternative Transportation Methods for Hydrocarbons

While pipelines are the undisputed champions for transporting large volumes of natural gas and NGLs over long distances, offering superior cost-efficiency, alternative methods like rail and trucking do exist. These alternatives are typically employed for smaller, more localized movements or when pipeline access is unavailable.

However, for Antero Midstream Partners, whose business model is built on the efficient, high-capacity movement of hydrocarbons, these alternatives present a significant threat. Rail and trucking are substantially more expensive per unit and less efficient for the scale Antero operates, making them poor substitutes for its core pipeline infrastructure.

Shift to Renewable Energy Sources

The long-term global transition towards renewable energy sources like solar and wind power presents a potential threat to Antero Midstream Partners by potentially reducing the overall demand for natural gas. This shift could consequently impact the need for the midstream infrastructure that transports and processes natural gas.

Despite this, natural gas is projected to maintain its importance in the energy landscape, particularly for ensuring grid stability and serving as a bridge fuel during the energy transition. The increasing demand for Liquefied Natural Gas (LNG) exports, coupled with the burgeoning need for power from data centers, offers a counterbalancing factor that supports continued demand for natural gas services.

Technological Advancements in Energy Storage

Technological advancements in energy storage, such as improved battery technology and hydrogen fuel cells, pose a potential threat by offering alternatives to natural gas for peak power generation. For instance, by the end of 2024, grid-scale battery storage capacity in the U.S. is projected to reach over 30 GW, a significant increase that could displace some natural gas peaker plants.

While these innovations could reduce Antero Midstream's reliance on natural gas for certain applications, they are not yet a complete substitute for baseload power or large-scale grid support. The current cost and scalability limitations of these emerging technologies mean that natural gas will likely remain a crucial component of the energy mix for the foreseeable future.

Demand-Side Management and Energy Efficiency

Increased energy efficiency in homes and industries, coupled with demand-side management initiatives, presents a potential headwind for natural gas demand growth. For instance, the U.S. Energy Information Administration (EIA) projects that energy efficiency improvements will continue to temper electricity demand growth, which can indirectly impact natural gas consumption in power generation.

While these trends could temper growth, the immediate impact on Antero Midstream Partners is currently mitigated by robust demand from other sectors. In 2024, industrial demand for natural gas remained strong, driven by manufacturing and chemical production. Furthermore, the expansion of liquefied natural gas (LNG) export capacity continues to be a significant driver of demand, with U.S. LNG exports reaching record levels in recent periods.

- Energy Efficiency Gains: Technological advancements and policy support for energy efficiency can reduce overall energy consumption per unit of output.

- Demand-Side Management: Programs encouraging consumers to shift energy use away from peak hours can flatten demand curves, potentially reducing the need for peak natural gas supply.

- Industrial Consumption: The manufacturing and petrochemical sectors are key consumers of natural gas, and their continued expansion supports demand.

- LNG Exports: Global demand for U.S. LNG provides a significant outlet for natural gas production, offsetting some domestic demand moderation.

Regulatory and Policy Shifts Favoring Alternatives

Government policies and regulations can significantly influence the threat of substitutes. For instance, initiatives promoting renewable energy sources or imposing stricter environmental standards on fossil fuels might make alternatives more appealing. This could impact demand for Antero Midstream's services if, for example, policies heavily favored electric vehicles over natural gas vehicles.

However, recent trends in 2024 indicate a more supportive regulatory landscape for natural gas infrastructure. The U.S. Department of Energy, for example, has continued to emphasize the role of natural gas as a transition fuel. This has bolstered domestic demand and supported the expansion of export facilities, thereby mitigating the immediate threat from substitutes in key markets.

- Favorable U.S. policies for natural gas exports.

- Continued emphasis on natural gas as a transition fuel.

- Growth in domestic natural gas demand.

Natural Gas: Enduring Demand Despite Emerging Substitutes

While rail and trucking serve as alternatives for transporting natural gas, they are significantly less cost-effective and efficient for the large-scale operations Antero Midstream engages in. Emerging technologies like advanced battery storage, projected to exceed 30 GW of U.S. capacity by the end of 2024, offer potential substitutes for natural gas in peak power generation, though they are not yet viable for baseload needs.

Despite these evolving alternatives, the demand for natural gas remains robust, bolstered by its role as a transition fuel and strong global demand for U.S. LNG exports. Government policies in 2024 have largely supported natural gas infrastructure, reinforcing its position and mitigating the immediate threat from substitutes.

| Substitute Type | Antero Midstream Relevance | Threat Level (2024) | Key Factors |

|---|---|---|---|

| Rail/Trucking | Low for large-scale transport | Low | Higher cost, lower efficiency vs. pipelines |

| Renewable Energy | Potential long-term demand reduction | Medium | Grid stability needs, energy transition role |

| Battery Storage | Displacement of peak gas generation | Medium | Projected 30+ GW U.S. capacity by end-2024 |

| Energy Efficiency | Tempering demand growth | Low to Medium | EIA projections show continued efficiency gains |

Entrants Threaten

Capital Intensity

The midstream energy sector demands massive upfront investment, with figures for new pipeline construction easily reaching hundreds of millions or even billions of dollars. For instance, a major natural gas pipeline project can cost upwards of $1 billion. This immense capital requirement acts as a formidable barrier, meaning only well-established companies with significant financial backing can realistically consider entering the market.

Regulatory Hurdles and Permitting Process

The path for new midstream companies is significantly obstructed by regulatory complexities and the lengthy permitting process. Obtaining the necessary approvals and navigating stringent environmental regulations for new projects can be a protracted and demanding undertaking. For instance, the Mountain Valley Pipeline project has experienced considerable delays due to these very challenges, underscoring the substantial barrier to entry this creates.

Economies of Scale and Existing Infrastructure

Antero Midstream Partners, like many established midstream companies, benefits significantly from the formidable barriers to entry created by economies of scale and existing infrastructure. Companies already operating in key regions, such as the prolific Appalachian Basin, have already made substantial capital investments in pipelines, processing facilities, and storage. For instance, Antero Midstream's extensive network is a result of years of development and strategic acquisitions. This existing infrastructure allows them to operate more efficiently and at a lower cost per unit of throughput compared to a new entrant who would need to replicate these assets from scratch.

The sheer capital required to build out a comparable network of pipelines, compressor stations, and processing plants is a major deterrent for new companies. In 2024, the cost of constructing new midstream infrastructure, including long-haul pipelines and complex processing facilities, continues to be in the billions of dollars, making it an extremely capital-intensive undertaking. This high upfront cost, coupled with the time and regulatory hurdles involved in obtaining permits and rights-of-way, creates a significant disadvantage for potential new entrants looking to compete with established players like Antero Midstream on price or service offerings.

Access to Customers and Dedicated Acreage

New entrants into the midstream sector face a significant hurdle in accessing customers, particularly large, reliable sources of hydrocarbons. Antero Midstream Partners benefits from its long-term, dedicated contracts with Antero Resources, which guarantees a steady flow of product through its infrastructure. This established relationship provides a predictable revenue stream and operational efficiency that is difficult for newcomers to replicate.

The dedication of prime acreage is another major barrier. Most of the highly prospective areas for oil and gas production are already under contract with existing midstream operators like Antero Midstream. For a new entrant to gain traction, they would need to secure similar long-term acreage dedications, which are scarce and highly sought after. For instance, Antero Resources has dedicated a substantial portion of its proved developed producing reserves to Antero Midstream, ensuring volume commitments that are vital for new infrastructure projects to be economically viable.

- Dedicated Acreage: Antero Resources has dedicated a significant percentage of its proved developed producing reserves to Antero Midstream.

- Customer Lock-in: Long-term contracts with major producers like Antero Resources create a strong customer lock-in effect.

- Barrier to Entry: New entrants would struggle to secure comparable acreage dedications and long-term customer agreements in prime operating regions.

- Volume Guarantees: The consistent volume of hydrocarbons secured through these contracts is essential for the profitability of midstream assets.

Brand Loyalty and Reputation

While brand loyalty isn't a direct consumer concern for midstream infrastructure, Antero Midstream Partners benefits from established trust and a proven track record with producers. New entrants face a significant hurdle in demonstrating comparable operational reliability and safety standards, which are paramount for securing long-term contracts for critical transportation and processing services.

For instance, in 2024, the midstream sector continued to emphasize ESG (Environmental, Social, and Governance) performance as a key differentiator. Companies with a strong history of responsible operations, like Antero Midstream, are better positioned to attract and retain producer relationships. A new entrant would need substantial capital investment not just in physical assets but also in building a reputation for dependability and regulatory compliance to compete effectively.

- Established Trust: Antero Midstream's existing relationships with upstream producers are built on years of reliable service and operational expertise.

- Operational Reliability: New entrants must prove their capacity to safely and efficiently manage complex midstream infrastructure, a significant barrier to entry.

- Producer Relationships: Securing contracts with producers in 2024, as in previous years, hinges on demonstrating a commitment to consistent performance and risk mitigation.

Midstream Entry Barriers: A Fortress of Capital and Regulation

The threat of new entrants for Antero Midstream Partners is significantly low due to the substantial capital required to build new infrastructure, often running into billions of dollars for major pipeline projects. Furthermore, the intricate web of regulatory approvals and lengthy permitting processes, exemplified by projects like the Mountain Valley Pipeline, presents a formidable and time-consuming challenge for any newcomer.

Established players like Antero Midstream benefit from existing infrastructure and economies of scale, making it difficult for new companies to compete on cost. Securing dedicated acreage and long-term contracts with producers, such as Antero Resources' dedication of proved developed producing reserves, is crucial for viability, and these prime opportunities are already largely secured by incumbents.

| Barrier Type | Description | Impact on New Entrants |

| Capital Requirements | Construction of pipelines and processing facilities can cost hundreds of millions to over a billion dollars. | Prohibitive for most potential new entrants. |

| Regulatory Hurdles | Complex permitting and environmental compliance can cause significant project delays. | Increases cost and time-to-market, deterring new players. |

| Existing Infrastructure | Antero Midstream's extensive network offers operational efficiencies and cost advantages. | New entrants must invest heavily to replicate or compete with existing capacity. |

| Customer Contracts | Long-term dedications from producers like Antero Resources ensure volume and revenue stability. | Difficult for new entrants to secure similar guaranteed volumes. |

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis for Antero Midstream Partners is built upon a foundation of verified data, including Antero's SEC filings, annual reports, and investor presentations. We also incorporate industry-specific data from reputable sources like EIA reports and energy sector market research firms.