Stock Yards Bank & Trust Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Stock Yards Bank & Trust Bundle

Go Beyond the Preview—Access the Full Strategic Report

Stock Yards Bank & Trust operates within a dynamic financial landscape, facing pressures from new entrants and the bargaining power of its customers. Understanding these forces is crucial for strategic planning.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Stock Yards Bank & Trust’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Technology and Software Providers

Stock Yards Bank & Trust depends on technology and software suppliers for its digital services, core banking systems, and security measures. The bargaining power of these specialized providers can be substantial, particularly for unique or deeply integrated software, as the cost and complexity of switching are high, involving data migration and potential operational downtime. For instance, the average cost for a mid-sized bank to switch core banking systems can range from millions to tens of millions of dollars.

The growing adoption of artificial intelligence and automation across the financial sector by 2025 is expected to amplify the influence of leading technology providers offering these advanced solutions. This trend means banks like Stock Yards Bank & Trust may face increased negotiation leverage from suppliers who control critical AI-driven platforms, impacting efficiency and competitive positioning.

Financial Data and Information Services

Suppliers of critical financial data, credit reports, and regulatory information exert a degree of bargaining power over Stock Yards Bank & Trust. The bank relies heavily on these external sources for accurate and timely data essential for robust risk assessment, informed investment strategies, and maintaining regulatory compliance.

The leverage held by these data providers can stem from the concentrated nature of certain data markets or the unique, proprietary status of their information. For instance, specialized financial data terminals often have few direct competitors, allowing them to command higher prices. However, the general availability of multiple vendors offering similar data services typically moderates this supplier power, preventing any single provider from gaining excessive control.

In 2024, the financial data services market continued to see significant investment. Companies like Bloomberg and Refinitiv (now part of LSEG) remain dominant players, with Bloomberg reporting over $10 billion in annual revenue. The increasing demand for real-time analytics and ESG data further solidifies the importance of these suppliers, though the competitive landscape does offer some recourse for financial institutions like Stock Yards Bank & Trust.

Human Capital (Skilled Employees)

The availability of skilled talent in financial technology, cybersecurity, wealth management, and relationship banking is a key supplier consideration. A scarcity of these professionals can drive up recruitment expenses and salaries, thereby amplifying their bargaining power.

Stock Yards Bank & Trust's designation as a 'Best Bank to Work For' in 2024 indicates a strategic approach to managing this supplier power by cultivating a supportive workplace culture.

Capital Markets and Funding Sources

For a bank like Stock Yards Bank & Trust, the bargaining power of suppliers translates to the cost and availability of its primary inputs: capital. While not traditional suppliers, entities providing funding, such as depositors and wholesale funding markets, wield significant influence. The broader economic climate, interest rate movements, and overall investor sentiment directly impact how much it costs the bank to acquire these essential funds.

In 2024, the banking sector experienced a notable increase in deposit costs. This trend is projected to continue into 2025, putting pressure on banks' net interest margins. For instance, the average cost of deposits for U.S. commercial banks saw a substantial rise throughout 2023 and into early 2024, driven by Federal Reserve rate hikes and increased competition for customer balances.

- Depositor Bargaining Power: Individual and institutional depositors can demand higher interest rates, especially during periods of rising inflation or when alternative investment opportunities offer more attractive yields.

- Wholesale Funding Markets: Banks relying on borrowing from other financial institutions or capital markets face fluctuating rates and availability, influenced by market liquidity and credit conditions.

- Investor Confidence: A bank's perceived financial health and market reputation directly affect its ability to attract capital, influencing the terms offered by investors and lenders.

- Regulatory Environment: Capital requirements and liquidity rules imposed by regulators can indirectly affect the cost and accessibility of funding.

Regulatory Bodies

Regulatory bodies like the OCC, FDIC, and Federal Reserve are crucial 'suppliers' for banks, providing operating licenses and compliance guidelines. Their mandates directly shape how institutions like Stock Yards Bank & Trust manage risk and conduct business. For instance, evolving regulations around cybersecurity and data privacy, which saw increased emphasis in 2024 and are projected to continue in 2025, necessitate significant investment in technology and compliance, thereby influencing operational expenses and strategic planning.

These governmental agencies wield considerable power by setting the rules of engagement for the banking sector. Their pronouncements can require substantial adjustments to a bank's business model, technology infrastructure, and risk management protocols. For example, in 2024, the banking industry faced ongoing discussions and potential new requirements related to capital adequacy and liquidity, directly impacting how banks allocate resources and manage their balance sheets.

The bargaining power of these regulatory bodies is evident in their ability to impose fines, revoke charters, or mandate specific operational changes. In 2024, the financial sector saw continued focus on consumer protection regulations, which require banks to invest in compliance training and robust internal controls, directly affecting profitability and operational flexibility.

Key aspects of regulatory influence include:

- Licensing and Charter Authority: Regulators grant and can revoke the fundamental right to operate.

- Compliance Frameworks: Rules dictate operational procedures, risk management, and capital requirements.

- Enforcement Actions: Penalties for non-compliance can be severe, impacting financial health.

- Evolving Mandates: New focuses, such as climate risk disclosure and AI governance in 2024-2025, force strategic adaptation and cost increases.

Supplier Power: Navigating Banking's Critical Dependencies

Stock Yards Bank & Trust faces significant supplier power from technology providers, especially for core banking systems and specialized software, due to high switching costs. For example, migrating a core banking system can cost millions. The increasing reliance on AI by 2025 further concentrates power with leading tech firms.

Data suppliers also hold sway, as accurate financial and regulatory data is crucial. While competition exists, concentrated markets for unique data, like those dominated by terminals such as Bloomberg (over $10 billion annual revenue in 2024), can limit negotiation leverage for banks.

The bank's ability to attract and retain skilled financial talent in 2024 influences recruitment costs, with a scarcity of professionals increasing bargaining power. Stock Yards Bank & Trust's recognition as a 'Best Bank to Work For' in 2024 highlights its strategy in managing this human capital supplier dynamic.

Capital providers, including depositors and wholesale funding markets, exert considerable bargaining power, directly impacting the bank's cost of funds. In 2024, deposit costs rose significantly, a trend expected to continue into 2025, squeezing net interest margins.

| Supplier Type | Key Considerations | 2024/2025 Impact | Example Data |

|---|---|---|---|

| Technology Providers | Core banking systems, AI solutions, cybersecurity | High switching costs, increasing AI influence | Core system migration: millions of dollars |

| Data Suppliers | Financial data, credit reports, regulatory information | Concentration in niche markets, demand for real-time analytics | Bloomberg revenue: >$10 billion (2024) |

| Human Capital | Skilled financial professionals, tech talent | Scarcity drives up recruitment costs | 'Best Bank to Work For' status (2024) influences talent acquisition |

| Capital Providers | Depositors, wholesale funding markets | Rising deposit costs pressure margins | Increased average deposit costs for U.S. banks (2023-2024) |

What is included in the product

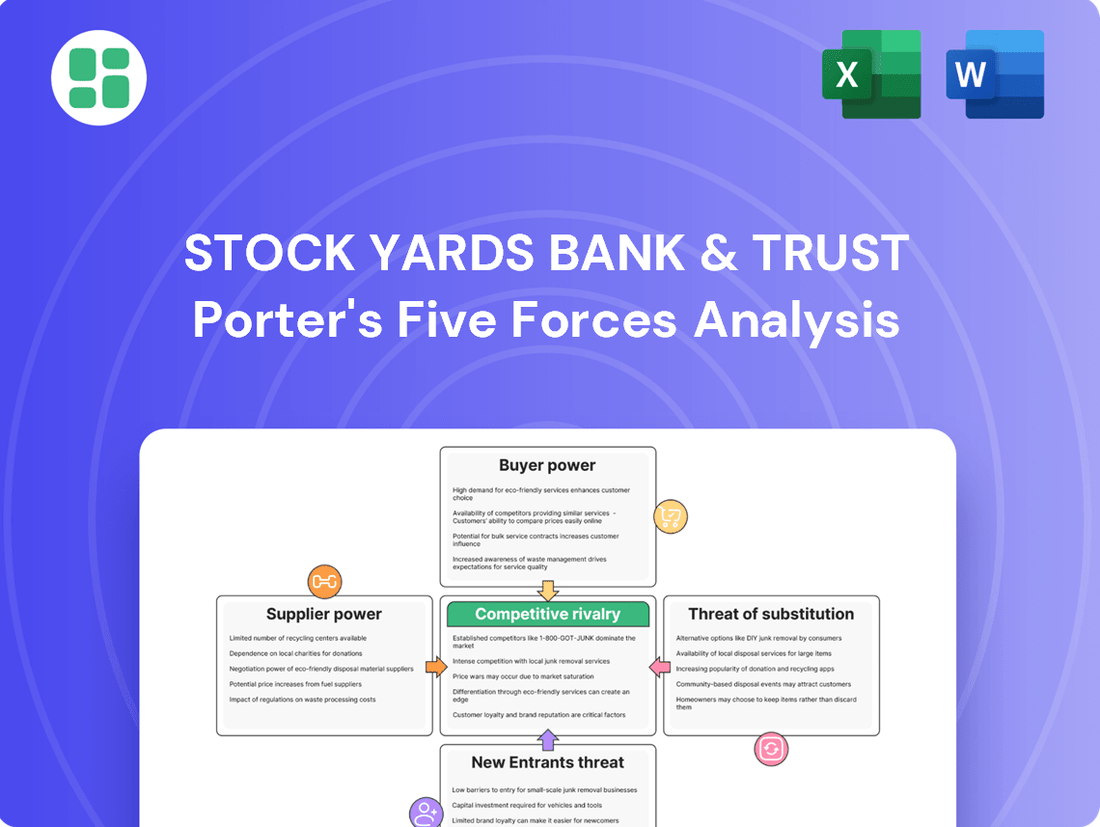

This analysis unpacks the competitive forces impacting Stock Yards Bank & Trust, detailing threats from new entrants, the bargaining power of buyers and suppliers, the intensity of rivalry, and the threat of substitutes.

Stock Yards Bank & Trust's Porter's Five Forces analysis offers a clear, one-sheet summary of all five forces—perfect for quick decision-making.

The intuitive design allows for easy customization of pressure levels based on new data or evolving market trends.

Customers Bargaining Power

Diverse Customer Base

Stock Yards Bank & Trust's diverse customer base, encompassing individuals, small businesses, and various organizations, generally dilutes the collective bargaining power of its clientele. This broad spectrum of service needs, from personal banking to complex trust and investment management, means no single customer segment holds significant sway over the bank's pricing or service terms.

While the overall customer base is fragmented, certain high-net-worth individuals within wealth management may exert more individual influence. However, for the majority, the lack of concentration limits their ability to demand concessions, thereby reducing their bargaining power in the overall competitive landscape.

Low Switching Costs for Basic Services

For fundamental banking needs such as checking and savings accounts, customers often face minimal costs when switching providers. This is particularly true given the growth of digital banking platforms and neobanks, which streamline the account opening and transfer processes. In 2024, the ease of digital onboarding means a customer can open a new account and transfer funds in a matter of minutes, significantly reducing the friction associated with changing banks.

High Switching Costs for Complex Services

For complex financial services like commercial loans and wealth management, customers face substantial hurdles when considering a switch. These include the time and effort to re-establish trust with a new provider, integrate new financial systems, and the potential loss of accumulated personalized advice and relationship history. For instance, a business reliant on a long-standing commercial lending relationship might find it difficult and costly to transfer loan portfolios, renegotiate terms, and retrain staff on new banking platforms.

Availability of Information and Digital Tools

Customers today have unprecedented access to information and digital tools. This allows them to easily compare financial products and services from various institutions. For instance, in 2024, numerous financial comparison websites and apps provide real-time data on interest rates, fees, and product features for everything from savings accounts to mortgages. This transparency significantly shifts power towards the consumer.

This enhanced ability to compare empowers customers to actively seek the best terms available. When a bank like Stock Yards Bank & Trust offers standard loan products or deposit rates, customers can readily identify if competitors are providing more favorable conditions. This forces financial institutions to remain competitive on pricing and service to retain their customer base.

- Increased Transparency: Digital platforms allow for easy comparison of financial products.

- Informed Decision-Making: Customers can readily access data on rates, fees, and features.

- Competitive Pressure: Banks must offer competitive terms to attract and retain customers.

- Focus on Value: The availability of information drives customers to seek the best overall value.

Demand for Digital and Personalized Experiences

Customers increasingly expect digital convenience and tailored advice. This demand for seamless online interactions and personalized financial guidance, available around the clock, significantly boosts their leverage. For instance, a 2024 survey indicated that over 70% of banking customers prefer digital channels for routine transactions.

Banks that lag in adopting advanced digital tools and AI for personalization face the risk of becoming obsolete. This pressure compels established institutions like Stock Yards Bank & Trust to prioritize innovation. In 2023, digital banking adoption continued its upward trend, with mobile banking users growing by approximately 10% year-over-year.

- Digital Expectations: Customers demand intuitive apps and online platforms.

- Personalization is Key: AI-driven insights and tailored product offerings are crucial.

- 24/7 Accessibility: Continuous access to banking services is a growing expectation.

- Competitive Landscape: Fintechs and neobanks often lead in digital experience, increasing customer options and bargaining power.

Customer Power: Navigating Banking Services in 2024

The bargaining power of customers for Stock Yards Bank & Trust is generally moderate, influenced by the type of service. For basic banking products, switching costs are low, amplified by digital tools in 2024 that allow for quick account transfers. However, for more complex services like commercial loans or wealth management, the effort and relationship capital involved in switching significantly increase costs for customers, thereby reducing their leverage.

Customers' ability to compare offerings has intensified due to readily available online information and comparison tools. This transparency in 2024, showing interest rates and fees across institutions, compels banks to remain competitive. The increasing demand for digital convenience and personalized services also empowers customers, as banks must innovate to meet these expectations, particularly with the rise of fintech competitors.

| Service Type | Switching Costs | Customer Bargaining Power | 2024 Trend Impact |

|---|---|---|---|

| Basic Banking (Checking/Savings) | Low | Moderate to High | Increased by digital onboarding |

| Loans (Personal/Mortgage) | Moderate | Moderate | Information transparency aids comparison |

| Commercial Loans | High | Low to Moderate | Relationship dependency limits switching |

| Wealth Management | High | Low to Moderate | Personalized advice creates stickiness |

What You See Is What You Get

Stock Yards Bank & Trust Porter's Five Forces Analysis

This preview showcases the complete Stock Yards Bank & Trust Porter's Five Forces Analysis, offering a thorough examination of competitive forces within its industry. The document you see here is precisely what you'll receive immediately after purchase, ensuring no surprises and full readiness for your strategic planning.

Rivalry Among Competitors

Fragmented Regional Market

Stock Yards Bank & Trust navigates a fragmented competitive landscape across Kentucky, Indiana, and Ohio. This regional market features a diverse array of financial institutions, from major national players and substantial super-regional banks to a multitude of smaller community banks.

Despite its growth to approximately $8 billion in assets, Stock Yards Bank faces significant rivalry. This competition stems from both the sheer number of smaller, agile community banks and the extensive resources and broader reach of larger national and super-regional competitors.

Presence of Large National Banks

Large national banks, including Bank of America and Chase, are increasingly encroaching on Stock Yards Bank & Trust's service areas, both physically and digitally. These giants leverage their vast resources and established brand recognition to offer a comprehensive suite of financial products, from mortgages to investment services. For instance, Bank of America reported over $1.1 trillion in deposits as of Q1 2024, demonstrating their significant market power.

Competition from Other Regional and Community Banks

Stock Yards Bank & Trust navigates a competitive landscape populated by robust regional players such as Republic Bank & Trust and German American Bank, both of which demonstrate strong performance within the same operational states. These institutions, much like Stock Yards, often leverage their established presence and local market understanding to attract and retain customers.

Furthermore, the persistent competition from numerous community banks cannot be overlooked. These smaller institutions frequently differentiate themselves through highly personalized customer service and deep-rooted local relationships, areas where Stock Yards Bank & Trust also excels, creating a direct overlap in competitive strategy and customer appeal.

Product and Service Differentiation

Competitive rivalry at Stock Yards Bank & Trust is significantly shaped by its focus on product and service differentiation. The bank actively distinguishes itself through personalized customer relationships, a robust suite of wealth management services, and tailored business banking solutions. This strategic emphasis aims to create a unique value proposition in a crowded market.

Stock Yards Bank & Trust's commitment to differentiation is further underscored by external recognition. For instance, its designation as a 'Best-in-State Bank' and a 'Best Bank to Work For' highlights successful execution in both customer service quality and fostering a strong organizational culture, key elements in standing out from competitors.

- Differentiation Focus: Emphasis on personal relationships, comprehensive wealth management, and business services.

- Service Quality Recognition: Named a 'Best-in-State Bank', indicating superior customer experience.

- Employer Brand: Recognized as a 'Best Bank to Work For', suggesting a strong internal culture that can translate to better client service.

Industry Consolidation and Mergers

The banking sector has been a hotbed for mergers and acquisitions. For instance, in 2023, the US saw a significant number of bank mergers, with notable deals like First Citizens BancShares acquiring Silicon Valley Bank for $16.5 billion. This trend continues into 2024, as banks seek to expand their reach and service offerings.

These consolidations lead to fewer, but larger, banking institutions. Think of it like this: a smaller bank might merge with another, creating a much bigger player. This new, larger entity can often compete more aggressively on price and offer a broader range of financial products, from mortgages to investment banking.

- Increased Scale: Mergers allow banks to operate more efficiently, spreading fixed costs over a larger asset base.

- Geographic Diversification: Acquiring banks in new regions helps reduce reliance on any single market.

- Enhanced Service Offerings: Consolidated banks can combine expertise and technology to provide a more comprehensive suite of services.

- Formidable Competition: Larger banks can leverage their size to offer more competitive rates and attract a wider customer base.

Navigating Fierce Banking Competition

Stock Yards Bank & Trust faces intense rivalry from national banks like Chase and Bank of America, which boast substantial assets, exceeding $1.1 trillion for Bank of America as of Q1 2024. Regional competitors such as Republic Bank & Trust and German American Bank also present significant competition, often leveraging local market knowledge. The market is further fragmented by numerous community banks that compete on personalized service and local relationships.

| Competitor Type | Key Strengths | Impact on Stock Yards Bank & Trust |

|---|---|---|

| National Banks (e.g., Chase, Bank of America) | Vast resources, broad product offerings, strong brand recognition | Pressure on pricing, market share erosion, digital competition |

| Super-Regional Banks (e.g., Republic Bank & Trust) | Established regional presence, local market understanding | Direct competition for similar customer segments |

| Community Banks | Personalized service, deep local relationships | Competition for customers valuing tailored experiences |

SSubstitutes Threaten

Fintech Companies and Digital-Only Banks

Fintech companies and digital-only banks are increasingly offering attractive alternatives to traditional banking services. These agile players often provide streamlined digital experiences, competitive interest rates, and lower fees, directly challenging established institutions. For instance, by mid-2024, neobanks in the US reported an average customer acquisition cost significantly lower than traditional banks, highlighting their cost-effectiveness.

These digital disruptors are particularly appealing to younger demographics and those seeking convenient, mobile-first financial solutions. Their ability to innovate rapidly and adapt to changing consumer preferences means they can quickly carve out market share. By the end of 2023, the global fintech market size was valued at over $2.4 trillion, demonstrating the substantial impact these companies are already having.

Credit Unions

Credit unions present a notable threat of substitutes for Stock Yards Bank & Trust, particularly in personal and small business banking. As not-for-profit entities, they frequently provide more attractive interest rates on savings and loans, alongside reduced fees. For instance, in 2024, the average credit union interest rate on savings accounts often hovered around 4.00-4.50%, compared to typical commercial bank rates closer to 0.50-1.00% for standard accounts. This cost advantage, coupled with their community-focused, member-centric approach, makes them a compelling alternative for customers seeking personalized service and better value.

Online Lenders and Alternative Financing

Online lenders and alternative financing platforms present a significant threat of substitutes for Stock Yards Bank & Trust. These fintech companies, including those offering peer-to-peer lending and digital loan marketplaces, provide consumers and businesses with avenues for credit that bypass traditional banking channels. For instance, the online lending market in the US saw substantial growth, with originations projected to reach hundreds of billions of dollars annually by 2024, offering competitive rates and faster approvals, especially for those who might not fit traditional bank criteria.

Investment Management Firms and Robo-Advisors

The threat of substitutes for Stock Yards Bank's wealth management services comes from dedicated investment management firms and the burgeoning robo-advisor sector. Robo-advisors, like Betterment and Wealthfront, offer automated, low-cost investment advice, directly competing for clients who might otherwise use a traditional wealth manager. These platforms leverage algorithms to create and manage diversified portfolios, often at a fraction of the cost of human advisors.

The appeal of robo-advisors is significant, especially for younger or less affluent investors. For instance, by early 2024, the assets under management for the top robo-advisors had surpassed $200 billion, indicating their growing market share. This trend suggests that a substantial portion of potential clients may opt for these digital solutions due to their accessibility and cost-effectiveness, thereby posing a direct substitute threat.

- Robo-advisor market growth: Assets under management in the robo-advisor industry are projected to reach over $3 trillion by 2027, highlighting a significant and growing substitute.

- Cost advantage: Robo-advisors typically charge annual management fees in the range of 0.25% to 0.50%, considerably lower than the 1% or more often charged by traditional wealth managers.

- Accessibility: Many robo-advisor platforms have low or no minimum investment requirements, making them accessible to a wider demographic than traditional wealth management services.

Embedded Finance and Non-Financial Companies

The increasing integration of financial services into non-financial platforms, known as embedded finance, presents a significant threat of substitutes for traditional banks like Stock Yards Bank & Trust. Consumers can now access payments, lending, and insurance directly within their everyday digital experiences, such as e-commerce checkouts or ride-sharing apps.

This trend bypasses the need for customers to interact with traditional banking interfaces, potentially diminishing customer loyalty and transaction volume. For instance, by 2024, it's projected that the embedded finance market will reach over $7 trillion globally, according to various market research reports, highlighting the substantial shift in how financial services are consumed.

- Embedded Payments: E-commerce platforms offer seamless payment solutions, reducing reliance on bank-issued cards or direct transfers.

- Embedded Lending: Buy-Now-Pay-Later (BNPL) services integrated into retail checkouts provide instant credit, substituting traditional loan applications.

- Embedded Insurance: Travel booking sites offering travel insurance at the point of sale are a prime example of this substitution.

Substitutes Surge: Redefining Financial Services

The threat of substitutes for Stock Yards Bank & Trust is substantial, driven by a rapidly evolving financial landscape. Digital-only banks and fintech companies offer streamlined, cost-effective alternatives, particularly appealing to younger demographics. Credit unions, with their member-centric approach and often better rates, also pose a direct challenge, especially in personal and small business sectors. Online lenders and embedded finance solutions further fragment the market, providing convenient credit and financial services directly within consumer experiences, reducing the need for traditional banking interactions.

| Substitute Type | Key Features | Impact on Traditional Banks | 2024 Data/Projections |

|---|---|---|---|

| Fintech/Neobanks | Digital-first, lower fees, competitive rates, agile innovation | Customer acquisition, transaction volume, fee income | US neobanks: lower customer acquisition costs; Global fintech market: >$2.4 trillion (end 2023) |

| Credit Unions | Not-for-profit, better rates, community focus | Personal and small business banking market share | Savings account rates: 4.00-4.50% (credit unions) vs. 0.50-1.00% (traditional banks) |

| Online Lenders | Faster approvals, alternative credit criteria, competitive rates | Loan origination market share | US online lending market: projected hundreds of billions in annual originations by 2024 |

| Robo-Advisors | Automated, low-cost investment management | Wealth management client base, advisory fees | Assets under management: >$200 billion (top robo-advisors early 2024); Fees: 0.25%-0.50% |

| Embedded Finance | Financial services integrated into non-financial platforms | Customer interaction, transaction volume, brand loyalty | Global embedded finance market: projected >$7 trillion by 2024 |

Entrants Threaten

High Regulatory Barriers

The banking sector, including institutions like Stock Yards Bank & Trust, faces significant hurdles for new players due to stringent regulatory requirements. Obtaining the necessary charters, licenses, and adhering to capital adequacy ratios, such as those mandated by Basel III, demands substantial upfront investment and expertise. For instance, in 2024, the average capital required to charter a new national bank remained exceptionally high, discouraging many potential entrants.

Significant Capital Requirements

Establishing a new bank, particularly one with a physical presence like Stock Yards Bank & Trust, demands immense capital for branches, technology, and maintaining sufficient liquidity. These significant upfront costs act as a formidable barrier, discouraging many potential competitors from entering the market.

Brand Loyalty and Trust

Established financial institutions like Stock Yards Bank & Trust, boasting over 100 years of operation and a deep commitment to customer relationships, cultivate significant brand loyalty and trust. This deeply ingrained customer allegiance, built over decades, acts as a formidable barrier.

For new entrants, replicating this level of trust and recognition is a monumental task, requiring substantial investment in marketing, service quality, and community engagement to even begin competing. For instance, in 2023, customer retention rates for established banks often exceeded 90%, a figure new competitors struggle to approach initially.

Technological Infrastructure and Expertise

Building a robust and secure technological infrastructure for banking, encompassing core systems, digital platforms, and advanced cybersecurity measures, presents a significant barrier for potential new entrants. This complexity and the substantial investment required in cutting-edge technology are crucial for any new player aiming to compete effectively in the financial services landscape.

For instance, in 2024, the global cybersecurity market was projected to reach hundreds of billions of dollars, highlighting the immense cost associated with securing financial operations. New entrants must not only replicate existing technological capabilities but also innovate to offer superior digital experiences and security protocols, demanding substantial capital outlay and specialized expertise.

- High Capital Investment: New entrants need to invest heavily in core banking systems, digital payment gateways, and customer relationship management (CRM) platforms.

- Cybersecurity Demands: Significant resources are required for robust cybersecurity infrastructure to protect sensitive customer data and prevent financial fraud.

- Technological Expertise: Attracting and retaining skilled IT professionals with expertise in areas like cloud computing, AI, and blockchain is a prerequisite for technological parity.

Difficulty in Achieving Economies of Scale

New entrants into the banking sector often face significant hurdles in achieving the economies of scale that incumbent institutions like Stock Yards Bank & Trust have cultivated over time. This disparity can hinder their ability to compete effectively on price or to efficiently manage the substantial fixed costs inherent in banking, especially concerning lending and deposit-gathering activities.

For instance, a new bank might find it difficult to spread the costs of regulatory compliance, technology infrastructure, and branch networks across a large enough customer base to match the per-unit cost advantages of an established player.

- Economies of Scale Barrier: Established banks benefit from lower per-unit costs due to higher asset volumes, making it harder for new entrants to match pricing.

- High Fixed Costs: Banking operations, including technology and compliance, require significant upfront investment that new entrants must absorb with a smaller initial customer base.

- Competitive Pricing Pressure: The inability to achieve scale can force new entrants to price services higher, deterring customers who are accustomed to the competitive rates offered by larger, established banks.

Banking Entry Barriers: A Fortress for Incumbents

The threat of new entrants for Stock Yards Bank & Trust is generally low, primarily due to the immense capital requirements and strict regulatory landscape that new banks must navigate. Obtaining necessary charters and licenses, coupled with the need for substantial upfront investment in technology and physical infrastructure, creates significant barriers.

For example, in 2024, the cost to establish a new bank with a physical presence and robust digital capabilities easily runs into tens of millions of dollars, a figure that deters many potential competitors. Furthermore, established brand loyalty and the trust built over decades by institutions like Stock Yards Bank & Trust are difficult and costly for newcomers to replicate.

New entrants also struggle to achieve the economies of scale that established players enjoy, impacting their ability to compete on pricing. This makes it challenging for them to offer competitive rates on loans and deposits, further limiting their market penetration against incumbents with lower operational costs per customer.

| Barrier Type | Description | Impact on New Entrants | Example Data (2024 Estimates) |

|---|---|---|---|

| Regulatory Hurdles | Strict licensing, capital adequacy (e.g., Basel III compliance) | High upfront costs, lengthy approval processes | Minimum capital requirements for national bank charter often exceed $10 million. |

| Capital Investment | Technology, physical branches, liquidity | Significant upfront expenditure, high fixed costs | Establishing a modern banking IT infrastructure can cost upwards of $20 million. |

| Brand Loyalty & Trust | Decades of customer relationships, reputation | Difficult to replicate, requires substantial marketing | Customer retention rates for established banks often above 90%. |

| Economies of Scale | Lower per-unit costs with higher asset volume | Inability to match pricing, higher operational costs | Large banks can achieve significantly lower cost-to-asset ratios than startups. |

Porter's Five Forces Analysis Data Sources

Our Stock Yards Bank & Trust Porter's Five Forces analysis is built upon a robust foundation of data, including SEC filings, annual reports, and industry-specific market research from reputable firms like IBISWorld and S&P Global Market Intelligence.