Sun Pharma Industries Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Sun Pharma Industries Bundle

Don't Miss the Bigger Picture

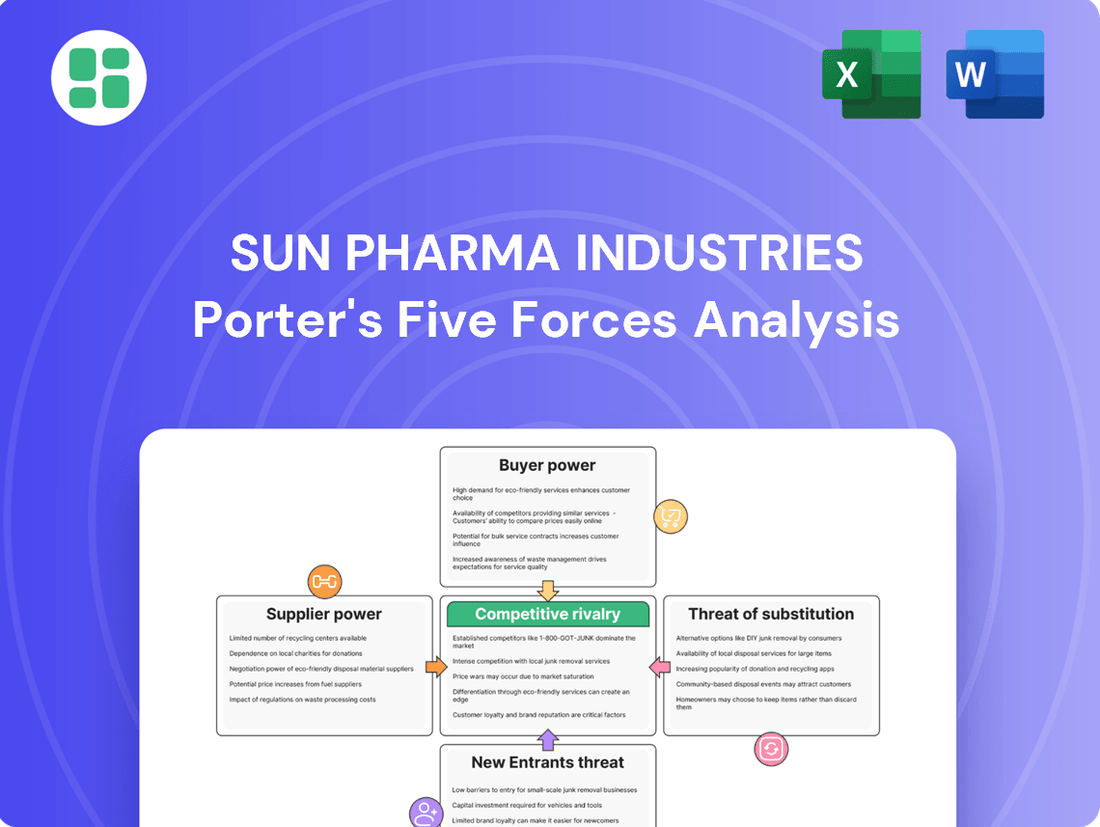

Sun Pharma Industries navigates a complex pharmaceutical landscape where intense rivalry and the threat of substitutes significantly shape its market. Understanding the bargaining power of both suppliers and buyers is crucial for maintaining profitability in this dynamic sector.

The complete report reveals the real forces shaping Sun Pharma Industries’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Specialized API and Raw Material Suppliers

Sun Pharma's reliance on a global supply chain for Active Pharmaceutical Ingredients (APIs) and specialized raw materials means the bargaining power of these suppliers can be significant. When suppliers offer patented or highly specialized components, Sun Pharma faces limited alternatives, potentially driving up input costs.

For instance, in 2024, the pharmaceutical industry continued to grapple with supply chain vulnerabilities, with some API manufacturers commanding higher prices due to their unique production capabilities or intellectual property. This concentration of specialized suppliers can directly impact Sun Pharma's cost of goods sold.

Compliance and Quality Standards

Suppliers of pharmaceutical raw materials face rigorous quality and regulatory demands, including adherence to Good Manufacturing Practices (GMP). This requirement naturally narrows the field of qualified suppliers, giving those who meet these high standards greater influence. For Sun Pharma, this means a reduced pool of potential suppliers, which can amplify the bargaining power of those remaining, potentially affecting supply chain costs and flexibility.

Concentration of Niche Suppliers

In specialized segments of the pharmaceutical market, such as for certain complex active pharmaceutical ingredients (APIs) or unique drug delivery systems, Sun Pharma might encounter a limited pool of qualified suppliers. For instance, if a particular niche therapeutic area relies on a highly specific molecule for which only a handful of manufacturers globally possess the advanced synthesis capabilities, these suppliers gain considerable leverage. This concentration means Sun Pharma has fewer alternatives, potentially leading to higher input costs and less favorable contract terms.

Switching Costs for APIs

Switching API suppliers presents substantial hurdles for Sun Pharma Industries. The process demands considerable investment in time and resources, encompassing rigorous re-validation of the new API, securing necessary regulatory approvals, and managing the inherent risk of production disruptions during the transition. These factors significantly elevate switching costs.

The high switching costs directly bolster the bargaining power of existing API suppliers. Sun Pharma faces a situation where changing suppliers, even in response to price hikes, becomes a complex and costly endeavor, limiting its leverage in negotiations.

- High Re-validation Costs: Each new API requires extensive testing and validation, which can cost hundreds of thousands of dollars.

- Regulatory Hurdles: Obtaining approvals from bodies like the FDA or EMA for a new API source can take 12-18 months, impacting time-to-market.

- Production Interruption Risk: A poorly managed API switch can lead to stock-outs and delayed drug manufacturing, affecting revenue.

Proprietary Technology and Patents

Suppliers who possess proprietary technology or patents for critical chemical processes or unique drug intermediates wield significant bargaining power over Sun Pharma. This dependence restricts Sun Pharma's ability to negotiate favorable terms and can potentially delay crucial product development cycles.

- Proprietary Technology: Suppliers with exclusive rights to advanced manufacturing techniques or novel synthesis routes for active pharmaceutical ingredients (APIs) can command higher prices.

- Patent Protection: Patents on key intermediates or specialized chemicals grant suppliers a temporary monopoly, giving them considerable leverage in pricing and supply agreements. For instance, if a supplier holds a patent for a crucial component in a blockbuster drug, Sun Pharma would have limited alternatives.

- Dependency and Negotiation Leverage: Sun Pharma's reliance on these specialized inputs directly impacts its negotiation leverage, potentially leading to increased costs and longer lead times, which can affect market competitiveness.

Supplier Power: The High Cost of Pharma Raw Materials

Sun Pharma's suppliers of specialized raw materials and Active Pharmaceutical Ingredients (APIs) can exert significant bargaining power, especially when they offer patented or unique components. This limited availability of alternatives means Sun Pharma may face higher input costs. For example, in 2024, the pharmaceutical sector continued to see some API manufacturers leverage their specialized production capabilities and intellectual property to command premium pricing, directly impacting the cost of goods sold for companies like Sun Pharma.

The rigorous quality and regulatory standards, such as Good Manufacturing Practices (GMP), required for pharmaceutical raw materials naturally limit the pool of qualified suppliers. This scarcity grants greater influence to those who meet these stringent demands, reducing Sun Pharma's options and potentially increasing supply chain costs and decreasing flexibility.

Switching API suppliers is a complex and costly process for Sun Pharma, involving extensive re-validation, regulatory approvals that can take 12-18 months, and the risk of production disruptions. These high switching costs significantly strengthen the bargaining power of existing suppliers, making it difficult for Sun Pharma to negotiate favorable terms even when facing price increases.

Suppliers holding patents for critical chemical processes or unique drug intermediates possess substantial leverage over Sun Pharma, potentially impacting development timelines and pricing. For instance, a patent on a key component for a widely used drug grants a temporary monopoly, giving the supplier considerable negotiation power.

| Factor | Impact on Sun Pharma | Example (2024 Context) |

| Supplier Specialization & IP | Limited alternatives, higher input costs | API manufacturers with unique synthesis capabilities commanding premium prices. |

| Regulatory Compliance | Reduced pool of qualified suppliers, increased leverage for compliant suppliers | GMP adherence narrows supplier options, amplifying power of those meeting standards. |

| High Switching Costs | Reduced negotiation leverage for Sun Pharma | Costly re-validation and regulatory approvals for new API sources deter supplier changes. |

| Proprietary Technology/Patents | Dependency, increased costs, potential delays | Patented intermediates grant suppliers monopoly power, affecting pricing and lead times. |

What is included in the product

This analysis unpacks the competitive forces shaping Sun Pharma Industries, detailing the intensity of rivalry, buyer and supplier power, threat of new entrants, and the impact of substitutes on its market position.

Sun Pharma's Porter's Five Forces analysis provides a clear, actionable framework to navigate competitive pressures, helping to alleviate the pain of strategic uncertainty.

Customers Bargaining Power

Large Institutional Buyers and Government Tenders

Large institutional buyers, including major hospital networks and government healthcare initiatives, wield considerable influence over Sun Pharma. These entities procure pharmaceuticals in massive volumes, granting them significant leverage to negotiate lower prices and more favorable contract terms. For instance, government tenders, often awarded through competitive bidding processes, can exert downward pressure on pricing for essential medicines.

Availability of Generics and Biosimilars

The increasing availability of generic and biosimilar versions of Sun Pharma's drugs directly amplifies customer bargaining power. This competitive landscape allows patients and healthcare providers to readily access more affordable alternatives, pressuring Sun Pharma to keep its pricing competitive, particularly for established, off-patent medications.

Price Sensitivity in Developing Markets

In developing markets where Sun Pharma has a significant footprint, customers and healthcare systems exhibit a pronounced price sensitivity. This is largely due to constrained healthcare budgets, a common characteristic of these economies.

This heightened price sensitivity directly translates into increased bargaining power for buyers. They can more effectively negotiate for lower prices on pharmaceuticals, which can put pressure on Sun Pharma's profit margins in these crucial growth regions.

For instance, in India, a key market for Sun Pharma, out-of-pocket healthcare expenditure remains substantial for many, driving demand for more affordable medication options. This dynamic underscores the importance of price competitiveness for Sun Pharma in these emerging economies.

Information Asymmetry and Formulary Inclusion

Customers, especially Pharmacy Benefit Managers (PBMs) and healthcare providers, wield significant bargaining power due to their access to comprehensive data on drug effectiveness, cost, and available substitutes. This informational edge allows them to negotiate favorable terms and influence which medications are placed on preferred drug lists, directly impacting Sun Pharma's market penetration.

The ability of these powerful customers to dictate formulary inclusion is a critical lever. For instance, in 2024, PBMs continued to consolidate their influence, managing prescription benefits for a substantial portion of the insured population in the United States. Sun Pharma's success is heavily reliant on securing favorable formulary placement, as exclusion can severely limit patient access and, consequently, sales volume.

- Information Advantage: PBMs and healthcare systems possess detailed data on drug performance and pricing, enabling informed negotiation.

- Formulary Control: Inclusion on preferred drug lists is crucial for market access; exclusion significantly hampers sales.

- Market Access Dependence: Sun Pharma's revenue is directly tied to its ability to gain and maintain formulary acceptance.

Patient Choice and Physician Influence

While patients ultimately decide which medications to use, their choices are significantly shaped by their physicians and the coverage provided by their insurance plans. This physician-driven influence can moderate the direct bargaining power of the end consumer for companies like Sun Pharma.

However, the landscape is evolving. Growing patient awareness and the increasing prominence of patient advocacy groups are starting to exert indirect pressure. These groups can influence pricing and access, particularly for expensive specialty medications, impacting companies that rely on these segments.

- Physician Influence: Doctors often recommend specific treatments based on efficacy and their own experience, acting as a key intermediary in patient purchasing decisions.

- Insurance Coverage: Payer formularies and co-pay structures heavily dictate patient choice, limiting direct consumer bargaining power.

- Patient Advocacy: In 2024, patient advocacy groups continued to gain traction, pushing for greater transparency and affordability in drug pricing, especially for chronic and rare diseases.

- Specialty Drug Impact: For high-cost specialty drugs, which represent a growing portion of the pharmaceutical market, patient advocacy can be a more potent force in negotiating access and price.

Customer Power: Driving Pharma Pricing and Market Access

Sun Pharma faces significant customer bargaining power, particularly from large institutional buyers like hospital networks and government healthcare programs that negotiate bulk discounts. The rise of generic and biosimilar alternatives further empowers customers by offering more affordable options, forcing Sun Pharma to remain competitive on pricing. In price-sensitive emerging markets, this pressure is even more pronounced due to limited healthcare budgets.

Pharmacy Benefit Managers (PBMs) in the US, managing benefits for a large portion of the insured population in 2024, wield considerable influence through their control over drug formularies. Securing a spot on these preferred drug lists is critical for Sun Pharma's market access and sales volume, as exclusion can severely limit patient access. While physicians and insurance coverage significantly shape patient choices, patient advocacy groups are increasingly impacting pricing and access for specialty medications.

| Customer Segment | Bargaining Power Driver | Impact on Sun Pharma |

|---|---|---|

| Institutional Buyers (Hospitals, Governments) | Volume purchasing, competitive bidding | Downward price pressure, contract negotiations |

| PBMs & Payers | Formulary control, data access | Market access dependence, pricing strategy |

| Patients (Indirectly) | Price sensitivity, advocacy groups | Demand for affordability, indirect pricing influence |

Full Version Awaits

Sun Pharma Industries Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. Our comprehensive Porter's Five Forces analysis for Sun Pharma Industries delves into the intense competitive rivalry within the pharmaceutical sector, highlighting the significant threat of new entrants due to high R&D costs and regulatory hurdles. It further examines the bargaining power of buyers, primarily healthcare providers and governments, and the substantial threat of substitutes, such as generic drugs and alternative therapies, impacting pricing strategies.

Rivalry Among Competitors

Global and Domestic Competitor Landscape

Sun Pharma navigates a fiercely competitive environment, contending with global giants like Pfizer and Roche, as well as a robust base of domestic Indian pharmaceutical companies. This intense rivalry, evident in the crowded generic drug market and the ongoing pursuit of new drug approvals, directly impacts pricing power and the ability to capture market share.

Product Differentiation and R&D Investment

Competitive rivalry in the pharmaceutical sector, exemplified by Sun Pharma, is intensely fueled by ongoing investments in research and development (R&D). This continuous innovation is crucial for introducing novel and enhanced medications to the market, directly impacting market share and profitability.

To stand out, companies like Sun Pharma need to differentiate their offerings through factors such as proven clinical efficacy, unique drug formulations, and advanced delivery systems. This differentiation is key to securing a competitive advantage and supporting premium pricing strategies in a crowded marketplace.

For instance, Sun Pharma's commitment to R&D is evident in its significant spending. In the fiscal year 2023-24, the company allocated approximately 6.7% of its revenue to R&D, a substantial investment aimed at developing a robust pipeline of differentiated products to combat intense competition from both global giants and emerging players.

Price Competition in Generic Segments

The generic pharmaceutical market, a cornerstone of Sun Pharma's operations, is a battleground of intense price competition. This fierce rivalry stems from the relative ease with which off-patent drugs can be replicated, leading to a commoditized market. Companies are compelled to continually lower prices to defend their market share against a multitude of generic manufacturers, a dynamic that significantly pressures profit margins.

Market Share Battles in Key Therapeutic Areas

Sun Pharma's significant presence across diverse therapeutic areas like dermatology, cardiology, and neurology inherently places it in direct competition with numerous players within each specialized segment. This intense rivalry is fueled by aggressive strategies focused on capturing market share.

Companies actively engage in robust marketing campaigns, optimize sales force efficiency, and forge strategic alliances to gain a competitive edge. For instance, in the dermatology segment, Sun Pharma competes with companies like AbbVie and Pfizer, both of which have strong product portfolios and significant market penetration. This constant jostling for position intensifies the overall competitive landscape.

- Dermatology: Sun Pharma faces intense competition from global giants and specialized dermatological firms.

- Cardiology: The cardiology market is highly competitive, with numerous established players vying for market share.

- Neurology: Sun Pharma's neurology segment sees rivalry from companies with strong R&D pipelines and established treatments.

- Aggressive Market Share Pursuit: Companies utilize marketing, sales force effectiveness, and partnerships to outmaneuver rivals.

Mergers, Acquisitions, and Strategic Alliances

The pharmaceutical sector is characterized by dynamic consolidation. In 2024, we've seen significant M&A activity as companies aim to bolster their market standing and innovation pipelines. For instance, the global pharmaceutical M&A market saw substantial deal values throughout 2023, with expectations for continued robust activity into 2024 as firms look to acquire novel therapies and expand geographic reach. Sun Pharma must actively monitor these trends to identify opportunities and mitigate threats from competitors leveraging these strategic moves.

These strategic maneuvers, including mergers, acquisitions, and alliances, directly influence competitive rivalry by altering market concentration and R&D capabilities. Companies like Sun Pharma engage in these to gain economies of scale, diversify their drug portfolios, and secure intellectual property. For example, a major acquisition by a rival could significantly shift market share in key therapeutic areas, necessitating a swift strategic response from Sun Pharma.

- Market Consolidation: Frequent M&A activity intensifies competition as larger entities emerge with greater resources and market influence.

- Portfolio Expansion: Acquisitions allow companies to quickly broaden their product offerings, potentially encroaching on Sun Pharma's existing market segments.

- Access to Innovation: Strategic alliances and acquisitions are crucial for gaining access to cutting-edge research and development, a key differentiator in the pharma industry.

- Competitive Landscape Shifts: These corporate actions continuously reshape the competitive environment, demanding agility and strategic foresight from Sun Pharma.

Intense Pharma Rivalry: Innovation and Price Strategies

Sun Pharma faces intense rivalry from both global pharmaceutical giants and a significant number of domestic Indian players. This competition is particularly fierce in the generics market, where price wars are common, and in specialized therapeutic areas where innovation and market penetration are key. The company's R&D spending, around 6.7% of revenue in FY23-24, highlights the necessity of continuous innovation to maintain a competitive edge against rivals actively pursuing market share through aggressive marketing and strategic partnerships.

| Key Competitors | Therapeutic Areas of Overlap | Competitive Strategy Examples |

| Pfizer, Roche | Multiple (e.g., Oncology, Cardiology) | New drug development, aggressive marketing |

| Domestic Indian Pharma Companies | Generics, various therapeutic areas | Price competition, rapid market entry |

| AbbVie | Dermatology | Strong product portfolios, market penetration |

SSubstitutes Threaten

Alternative Therapies and Lifestyle Changes

The primary threat of substitutes for pharmaceutical products like those offered by Sun Pharma comes from non-pharmacological interventions. These include lifestyle modifications, dietary changes, physical therapy, or even surgical procedures.

For certain conditions, these alternatives can significantly reduce or even eliminate the need for medication. For instance, a growing awareness of preventive healthcare means more individuals are exploring diet and exercise to manage conditions like diabetes or hypertension, potentially impacting Sun Pharma's sales in these therapeutic areas.

The global wellness market, valued at over $5.6 trillion in 2023, highlights the increasing consumer interest in these substitute approaches. This trend suggests a growing potential for lifestyle changes to displace demand for certain pharmaceutical treatments.

Generic and Biosimilar Alternatives

Generic and biosimilar alternatives pose a significant threat to Sun Pharma's branded and off-patent products. These lower-cost options provide comparable therapeutic benefits, forcing Sun Pharma to either continuously innovate or engage in aggressive price competition once patent protection lapses. For instance, the global generics market is projected to reach $330 billion by 2024, highlighting the intense pressure from these substitutes.

Preventive Healthcare and Wellness Trends

The growing emphasis on preventive healthcare and wellness, a trend gaining significant traction globally, poses a potential threat of substitution for some of Sun Pharma's offerings. As individuals increasingly prioritize early diagnosis and proactive health management, the demand for certain treatments for acute or chronic conditions could diminish over time. For instance, a surge in preventative measures against cardiovascular diseases, supported by lifestyle changes and early screening, might lessen reliance on specific cardiovascular medications.

Novel Drug Delivery Systems and Technologies

Advances in novel drug delivery systems and technologies present a significant threat of substitutes for Sun Pharma. Emerging areas like gene therapies and personalized medicine offer alternative treatment modalities that could bypass traditional pharmaceutical formulations. For instance, the global gene therapy market was valued at approximately USD 10.7 billion in 2023 and is projected to grow substantially, indicating a shift in treatment paradigms.

These innovative approaches can address unmet medical needs or offer superior efficacy and patient convenience compared to existing drugs. Sun Pharma's substantial investment in research and development, which stood at INR 2,238 crore (approximately USD 269 million) in FY24, is crucial to staying competitive and developing its own advanced delivery systems or integrating these new technologies. Failure to adapt could lead to market share erosion as patients and healthcare providers adopt more cutting-edge solutions.

The threat is amplified by the potential for these new technologies to disrupt established markets for chronic diseases where Sun Pharma has a strong presence. Consider the growing pipeline of cell and gene therapies for conditions like sickle cell disease, which could eventually substitute for lifelong treatments involving conventional drugs.

- Emerging Technologies: Gene therapies, cell therapies, and personalized medicine offer alternative treatment pathways.

- Market Disruption: These novel systems can bypass traditional drug formulations, impacting established markets.

- R&D Investment: Sun Pharma's R&D spending of INR 2,238 crore (approx. USD 269 million) in FY24 is vital for counteracting this threat.

- Competitive Landscape: The increasing pipeline of advanced therapies necessitates continuous innovation to maintain market relevance.

Over-the-Counter (OTC) Solutions and Supplements

The threat of substitutes for Sun Pharma's products is significant, particularly from over-the-counter (OTC) solutions and supplements. For many common ailments, consumers can readily access non-prescription alternatives like pain relievers, vitamins, or herbal remedies. This is especially true in therapeutic areas where Sun Pharma might have prescription offerings that also have widely available OTC counterparts or perceived natural alternatives.

In 2024, the global dietary supplements market was valued at over $170 billion, indicating a strong consumer preference for self-care and alternative health solutions. This trend directly impacts pharmaceutical companies like Sun Pharma, as consumers may choose these more accessible options over prescription medications for conditions ranging from mild pain to vitamin deficiencies.

- Consumer preference for self-treatment drives demand for OTC products.

- The global dietary supplements market exceeded $170 billion in 2024.

- OTC alternatives can reduce reliance on prescription drugs for certain conditions.

- Herbal remedies and supplements pose a direct substitute threat in specific therapeutic areas.

Pharma's Challenge: Battling Diverse Product Substitutes

The threat of substitutes for Sun Pharma's products is multifaceted, encompassing both non-pharmacological interventions and alternative pharmaceutical approaches. Lifestyle changes, preventive healthcare, and the burgeoning wellness market, valued at over $5.6 trillion in 2023, represent significant substitutes for certain medications. Additionally, the global generics and biosimil market, projected to reach $330 billion by 2024, poses a direct threat by offering lower-cost alternatives to branded drugs.

| Substitute Category | Impact on Sun Pharma | Supporting Data/Trend |

| Non-Pharmacological Interventions (Lifestyle, Diet, Therapy) | Reduces demand for certain chronic disease medications. | Global wellness market > $5.6 trillion (2023). |

| Generic and Biosimilar Drugs | Erodes market share and pricing power of off-patent branded drugs. | Global generics market projected to reach $330 billion (2024). |

| Over-the-Counter (OTC) & Supplements | Offers accessible alternatives for common ailments, impacting prescription drug sales. | Global dietary supplements market > $170 billion (2024). |

| Novel Drug Delivery & Advanced Therapies (Gene, Cell, Personalized Medicine) | Disrupts traditional pharmaceutical markets, requiring continuous innovation. | Global gene therapy market ~ $10.7 billion (2023); Sun Pharma R&D: INR 2,238 crore (FY24). |

Entrants Threaten

High Research and Development Costs

Developing innovative pharmaceutical products demands substantial investment in research and development. This includes rigorous preclinical testing and extensive clinical trials, a process that can easily span over a decade and incur costs in the billions of dollars.

For instance, bringing a new drug to market often requires an average investment exceeding $2.6 billion, according to some industry estimates. These exorbitant upfront capital requirements create a formidable barrier, significantly deterring potential new entrants from entering the highly competitive pharmaceutical sector.

Stringent Regulatory Approval Processes

The pharmaceutical industry, including companies like Sun Pharma, faces significant hurdles due to stringent regulatory approval processes. Agencies such as the U.S. Food and Drug Administration (FDA), the European Medicines Agency (EMA), and India's Central Drugs Standard Control Organisation (CDSCO) demand extensive clinical trials and data before granting market authorization.

These lengthy, complex, and costly approval pathways act as a substantial barrier to entry. For instance, the average cost to bring a new drug to market has been estimated to be in the billions of dollars, with development timelines often exceeding a decade. This financial and temporal commitment deters many potential new entrants who may not possess the necessary capital, scientific expertise, or regulatory navigation capabilities.

Intellectual Property and Patent Protection

Sun Pharma, like other major pharmaceutical players, benefits significantly from intellectual property and patent protection. These patents grant exclusive rights to market innovative drugs for a specific duration, creating a substantial barrier for potential new entrants. For instance, in 2023, Sun Pharma had a robust pipeline of new drug applications, many of which are expected to be protected by patents, solidifying its market position.

Established Distribution Channels and Brand Recognition

New entrants into the pharmaceutical market, particularly in areas where Sun Pharma operates, face significant hurdles in establishing their presence. Building out the necessary distribution channels to reach pharmacies, hospitals, and clinics requires substantial investment and time. Furthermore, securing formulary access, which dictates which drugs are covered by insurance plans, is a complex and often lengthy process. Sun Pharma, with its established network, has a distinct advantage here.

Brand recognition and trust among healthcare professionals and patients are critical differentiators. Sun Pharma has cultivated decades of experience and a reputation for quality and efficacy, making physicians more inclined to prescribe their products. For a new company, overcoming this ingrained trust and achieving comparable brand awareness is a formidable challenge, often necessitating extensive marketing and clinical data to gain traction.

Consider these points regarding established distribution and brand recognition:

- Distribution Network Strength: Sun Pharma's extensive global distribution network, reaching over 100 countries, represents a significant barrier to entry for new players who must replicate this infrastructure.

- Physician Relationships: Long-standing relationships with doctors and healthcare providers, built on consistent product delivery and clinical support, give established firms like Sun Pharma a competitive edge.

- Brand Loyalty: Physician and patient loyalty to established brands, often driven by positive past experiences and perceived reliability, makes it difficult for new entrants to gain market share quickly.

- Formulary Access: Securing a place on hospital and insurance formularies is a crucial step, and incumbent companies often have existing agreements and leverage that new entrants struggle to match.

Economies of Scale in Manufacturing and Marketing

The threat of new entrants for Sun Pharma Industries is significantly moderated by the substantial economies of scale enjoyed by established players in manufacturing and marketing. Large pharmaceutical giants, including Sun Pharma, leverage their massive production volumes to secure lower per-unit costs in manufacturing and raw material procurement. For instance, in 2023, Sun Pharma's revenue reached approximately INR 44,662 crore (around $5.3 billion), allowing for significant purchasing power and operational efficiencies that are difficult for newcomers to replicate.

Furthermore, the marketing and distribution networks of incumbent firms are vast and deeply entrenched. New entrants would face immense challenges in building comparable sales forces and brand recognition to compete effectively. This scale advantage translates directly into a cost barrier; new companies would likely incur much higher per-unit costs, hindering their ability to offer competitive pricing and achieve market penetration against established giants like Sun Pharma.

- Economies of Scale in Manufacturing: Large players benefit from bulk purchasing of raw materials and optimized production processes, reducing per-unit manufacturing costs.

- Marketing and Distribution Efficiencies: Established companies have widespread sales forces and established distribution channels, creating high entry barriers for new entrants.

- Cost Disadvantage for Newcomers: Without comparable scale, new entrants face higher operational costs, impacting their pricing strategies and market competitiveness.

Pharma's Impenetrable Barriers: Capital, Patents, and Scale

The threat of new entrants for Sun Pharma is considerably low due to the immense capital required for research, development, and navigating complex regulatory approvals, often costing billions of dollars and taking over a decade. For example, the average cost to bring a new drug to market has been estimated to exceed $2.6 billion. This financial and temporal commitment, coupled with stringent requirements from bodies like the FDA and EMA, deters many potential competitors.

Intellectual property rights, such as patents, also create a significant barrier, granting exclusive marketing rights for new drugs. Sun Pharma's robust patent portfolio, evidenced by its new drug applications in 2023, further solidifies this protection. Furthermore, established players like Sun Pharma benefit from economies of scale in manufacturing and marketing, leading to lower per-unit costs and efficient distribution networks that newcomers struggle to match. In 2023, Sun Pharma's revenue of approximately INR 44,662 crore (around $5.3 billion) highlights its significant purchasing power and operational efficiencies.

| Barrier Type | Description | Impact on New Entrants | Sun Pharma's Advantage |

|---|---|---|---|

| Capital Requirements | High R&D and clinical trial costs (>$2.6 billion per drug) | Deters new entrants due to financial risk | Established financial resources and investment capacity |

| Regulatory Hurdles | Lengthy and complex FDA/EMA approval processes | Requires extensive expertise and time to navigate | Proven track record and in-house regulatory affairs teams |

| Intellectual Property | Patent protection for innovative drugs | Restricts market entry for generic or similar products | Strong patent portfolio and ongoing innovation pipeline |

| Economies of Scale | Lower manufacturing and marketing costs for large players | New entrants face higher per-unit costs | Efficient large-scale production and established distribution networks (INR 44,662 crore revenue in 2023) |

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis for Sun Pharma Industries is built upon a foundation of comprehensive data, including annual reports, investor presentations, and regulatory filings from the company itself.

We supplement this with insights from reputable industry research firms, market intelligence reports, and pharmaceutical sector-specific publications to capture a holistic view of the competitive landscape.