PSC Insurance Group PESTLE Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

PSC Insurance Group Bundle

Your Shortcut to Market Insight Starts Here

Navigate the complex external landscape affecting PSC Insurance Group with our detailed PESTLE analysis. Understand how political shifts, economic volatility, and evolving social trends are shaping opportunities and risks for the company. Equip yourself with actionable intelligence to refine your own strategic approach.

Gain a competitive edge by delving into our comprehensive PESTLE analysis of PSC Insurance Group. Uncover critical insights into technological advancements, environmental considerations, and legal frameworks impacting the insurance sector. Download the full report to unlock strategic foresight and make informed decisions.

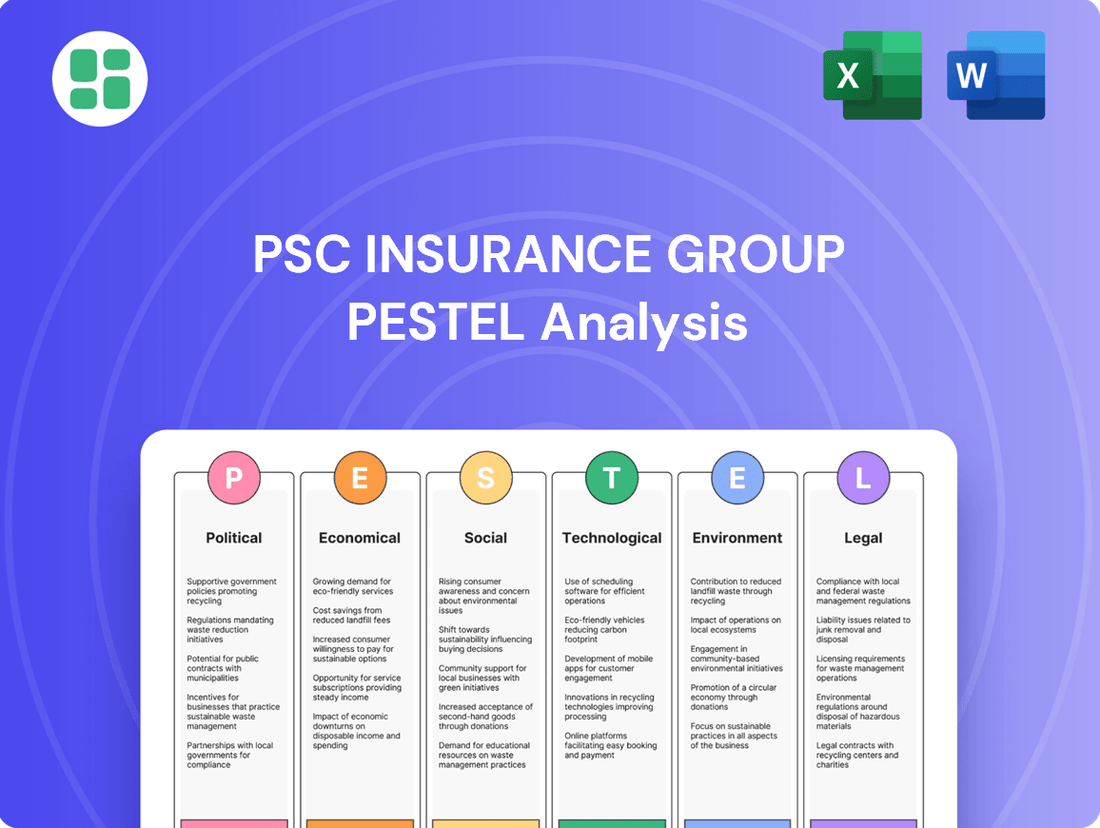

Political factors

Regulatory Stability and Change

Australia's generally stable political environment offers a degree of predictability for financial services, including insurance. This stability is crucial for long-term planning and investment within PSC Insurance Group.

However, potential shifts in government policy, such as proposed reforms to consumer protection in financial advice, could necessitate adjustments for PSC Insurance Group. For instance, the Australian Securities and Investments Commission (ASIC) has been actively reviewing conduct in the financial advice sector throughout 2024, potentially leading to increased compliance costs.

The government's approach to market competition and consolidation within the insurance industry also presents a key political factor. Decisions regarding mergers and acquisitions, or the fostering of new market entrants, could significantly influence PSC Insurance Group's strategic options and competitive landscape.

Government Policy on Financial Services

Government policies significantly shape the landscape for insurance brokers and financial planners. For instance, changes in superannuation contribution caps or tax treatments on investment earnings directly impact the advice PSC Insurance Group can offer and the products available to clients. The Australian government's focus on financial advice reform, including the Quality of Advice reforms aimed at making advice more accessible and affordable, presents both opportunities for PSC to expand its client base and challenges in adapting to new regulatory frameworks.

International Trade Relations

PSC Insurance Group, being an Australian company, is indirectly influenced by international trade relations through the activities of its diverse client base. Shifts in global trade agreements, such as potential renegotiations of existing pacts or the emergence of new bilateral trade deals impacting key Australian export markets, could alter the financial health and operational scope of PSC's clients. For instance, a slowdown in trade with a major partner could reduce expansion plans for businesses PSC insures, thereby affecting demand for certain insurance products.

Geopolitical tensions also play a significant role. For example, ongoing trade disputes between major economic blocs could disrupt supply chains for industries PSC serves, leading to increased operational risks for its clients. This might necessitate adjustments in coverage, such as political risk insurance or business interruption policies, to address these evolving client needs. The Australian government's trade policies and its engagement in international forums directly shape the broader economic landscape within which PSC operates.

Consumer Protection Initiatives

Consumer protection is a significant political factor for PSC Insurance Group. The Australian government, through bodies like the Australian Securities and Investments Commission (ASIC), consistently updates consumer protection laws. For example, ASIC's focus on financial advice reforms and product suitability, as seen in ongoing reviews and enforcement actions in 2024, directly impacts how PSC operates. These changes can influence everything from product development and disclosure wording to how client relationships are managed, demanding continuous adaptation to maintain compliance and protect its reputation.

PSC Insurance Group must navigate a landscape where regulatory scrutiny is high. In 2024, ASIC continued its work on enhancing consumer outcomes in financial services, including insurance broking. This means PSC needs to ensure its broking and advisory services meet stringent standards regarding transparency, fairness, and client best interests. Failure to comply can lead to penalties and reputational damage, making adherence a critical operational imperative.

- Regulatory Scrutiny: ASIC's ongoing focus on consumer protection in financial services, particularly in 2024, necessitates robust compliance frameworks for PSC Insurance Group.

- Evolving Standards: Changes in consumer protection laws can affect product design, disclosure requirements, and client engagement, requiring PSC to remain agile.

- Reputational Risk: Adherence to these regulations is crucial for maintaining PSC's standing in the market and avoiding legal repercussions.

- Compliance Costs: Implementing and maintaining compliance with new consumer protection initiatives can incur significant operational costs for the group.

Industry Support and Subsidies

Government programs offering support or subsidies to specific industries or regions, particularly those impacted by natural disasters, can significantly shape the demand for and the very nature of insurance products. For example, in Australia, following the severe bushfires of 2019-2020, there were discussions and some initiatives around government-backed insurance schemes for high-risk areas, though widespread implementation for general insurance remained limited. PSC Insurance Group, being an Australian-based insurer, would need to remain agile in developing and marketing products that align with any emerging government incentives or support packages for businesses or individuals recovering from or preparing for such events.

These subsidy programs can create new market opportunities. Imagine a region receiving government funding for flood resilience upgrades; PSC could offer specialized insurance products covering these enhanced infrastructure projects or the residual risks. Such initiatives directly influence the risk pool by potentially reducing certain perils or by bringing new, insured entities into the market. For instance, if a government program subsidizes the uptake of renewable energy infrastructure, PSC might see increased demand for specialized coverage for solar farms or wind turbines, which often come with unique risk profiles. The Australian government's commitment to supporting regional development and disaster recovery, as seen in funding allocations for infrastructure post-2022 floods, demonstrates this dynamic. For 2024-2025, continued focus on climate resilience could translate into more targeted support schemes, influencing insurance demand.

- Government support for disaster-affected regions can boost demand for specialized insurance.

- Agility in product development is key to capitalizing on subsidy-driven market shifts.

- New government schemes can alter the risk pool for insurers like PSC.

- Examples include potential support for renewable energy infrastructure or flood resilience projects.

Australian Policy & Global Trade: Insurance Sector Impacts

Australia's stable political climate provides a predictable operating environment for PSC Insurance Group, fostering long-term strategic planning. However, evolving government policies, particularly regarding consumer protection in financial services, require constant adaptation. For instance, the Australian Securities and Investments Commission's (ASIC) ongoing focus on financial advice reforms throughout 2024 could increase compliance burdens.

Government decisions on market competition and consolidation within the insurance sector directly influence PSC's strategic options. Furthermore, shifts in tax laws or superannuation regulations, such as the Australian government's Quality of Advice reforms aimed at improving advice accessibility, present both opportunities for client growth and challenges in regulatory compliance.

Geopolitical stability and international trade relations indirectly impact PSC through its client base's financial health. Disruptions from global trade disputes or changes in trade agreements can affect client expansion plans, thus influencing demand for insurance products. PSC must remain attuned to how government trade policies shape the broader economic landscape.

What is included in the product

This PESTLE analysis delves into the external macro-environmental forces impacting PSC Insurance Group, examining Political, Economic, Social, Technological, Environmental, and Legal factors to uncover strategic opportunities and potential threats.

A clear, actionable PESTLE analysis of PSC Insurance Group, designed to simplify complex external factors into manageable insights for strategic decision-making.

This PESTLE analysis for PSC Insurance Group acts as a pain point reliever by providing a structured framework to anticipate and navigate external market dynamics, thereby reducing uncertainty and improving strategic planning.

Economic factors

Economic Growth and Stability

Australia's economic health is a significant driver for PSC Insurance Group. In 2024, the Australian economy was projected to grow by 2.0% according to the Reserve Bank of Australia, indicating a moderate but stable environment. This growth generally supports demand for insurance and financial services as businesses expand and individuals have more disposable income.

Stronger economic periods often correlate with increased demand for PSC's offerings. For instance, robust business activity in 2024 would likely boost the need for commercial insurance lines, while rising household incomes could fuel demand for personal insurance and wealth management solutions. This trend is supported by data showing a correlation between GDP growth and insurance premium volumes.

Conversely, economic slowdowns present challenges. A projected slowdown in global growth for 2025 could translate to reduced spending on insurance and financial products in Australia. Furthermore, economic downturns can sometimes lead to an increase in claims, particularly in areas like business interruption or credit insurance, impacting profitability.

Interest Rate Fluctuations

Interest rate fluctuations directly impact PSC Insurance Group's financial performance. For instance, as of early 2024, central banks in major economies like the US and UK maintained higher interest rates compared to the preceding years. This environment generally boosts PSC's investment income derived from premiums held in reserve, as these funds can be invested at more favorable yields. However, higher rates also increase the cost of capital for any potential acquisitions or operational financing.

Conversely, a scenario of falling interest rates, a trend that began to emerge in some regions towards the end of 2024 and into early 2025, can put pressure on PSC's profit margins. This is because the returns on their investment portfolios may decrease. Furthermore, shifts in interest rates can influence the affordability of insurance products for customers, as businesses and individuals may face higher borrowing costs, potentially impacting their ability to purchase new policies or renew existing ones.

Inflationary Pressures

Inflation significantly impacts PSC Insurance Group by increasing the cost of settling claims, especially in property and casualty insurance where the expense of replacing damaged goods or rebuilding structures escalates. For instance, rising material costs in construction, a direct consequence of inflation, directly translate to higher payouts for property damage claims.

Beyond claims, inflationary pressures also drive up PSC's internal operational costs, from employee salaries to office supplies and technology. This necessitates careful management of the company's expense ratios to maintain financial health.

To counter these effects, PSC must strategically adjust its premium pricing and refine its underwriting processes. For example, if inflation leads to a 5% increase in repair costs, PSC would need to factor a similar or greater increase into its premiums to preserve its profit margins and ensure it can adequately cover its policyholders' future claims, a crucial balancing act in the 2024-2025 financial landscape.

Consumer and Business Confidence

Consumer confidence plays a crucial role in the insurance sector. For instance, the ANZ-Roy Morgan Consumer Confidence Index in Australia hovered around 77.5 in early 2024, indicating a cautious but gradually improving sentiment. When consumers feel secure about their financial future, they are more likely to invest in insurance products, seeing them as essential rather than discretionary spending.

Business confidence also directly impacts PSC Insurance Group. In the UK, the CBI's Industrial Trends Survey for Q1 2024 showed that business optimism remained subdued, with firms reporting slower order books. This cautious outlook can translate into businesses re-evaluating their insurance needs, potentially leading to a reduction in coverage or a delay in purchasing new policies. Conversely, a surge in business confidence would likely drive demand for more robust insurance solutions to protect expanding operations.

- Consumer Confidence: In Australia, the ANZ-Roy Morgan Consumer Confidence Index was around 77.5 in early 2024, reflecting a moderate level of consumer optimism that supports insurance spending.

- Business Sentiment: The UK's CBI Industrial Trends Survey in Q1 2024 indicated that business optimism was subdued, potentially impacting demand for comprehensive business insurance.

- Investment Correlation: Higher confidence levels generally correlate with increased willingness from both individuals and businesses to invest in insurance and financial planning services.

- Risk Appetite: Elevated confidence encourages greater risk-taking and expansion, which in turn heightens the need for adequate insurance coverage to mitigate potential losses.

Global Economic Trends

Global economic trends significantly shape the operating environment for PSC Insurance Group, particularly given its diverse clientele engaged in international activities. For instance, the International Monetary Fund (IMF) projected global growth to be 3.2% in 2024, a figure that influences the economic health and risk appetites of businesses PSC insures.

Disruptions in global supply chains, a persistent issue since 2020, can directly affect the insurance needs of companies involved in manufacturing and logistics. These disruptions can lead to increased business interruption claims and necessitate adjustments in coverage for clients. In 2024, while some supply chain pressures eased, geopolitical tensions continued to pose risks, impacting shipping costs and delivery times.

Furthermore, international financial market volatility, such as currency exchange rate fluctuations or interest rate changes set by major central banks like the US Federal Reserve or the European Central Bank, can indirectly impact PSC's clients. These financial shifts can affect the profitability and investment portfolios of businesses, thereby altering their insurance requirements and their capacity to pay premiums. For example, a strong US dollar in late 2024 could make it more expensive for Australian clients to purchase goods or services from the US, impacting their financial stability.

- Global Growth Impact: A projected 3.2% global growth in 2024 by the IMF provides a baseline for economic activity, influencing client demand for insurance and their overall risk exposure.

- Supply Chain Volatility: Ongoing supply chain disruptions in 2024, exacerbated by geopolitical factors, increase the likelihood of business interruption claims for PSC's clients in trade and manufacturing.

- Financial Market Fluctuations: Currency exchange rate shifts and interest rate adjustments by global central banks in 2024 can affect the financial health of PSC's international clients, altering their insurance needs.

Economic Factors Influence Insurance Group's Performance

Economic factors significantly influence PSC Insurance Group's performance. Australia's projected GDP growth of 2.0% in 2024, as per the Reserve Bank of Australia, generally supports demand for insurance. However, a global growth slowdown projected for 2025 could temper this demand.

Interest rate shifts are critical; higher rates in early 2024 boosted PSC's investment income, but falling rates towards late 2024 and into early 2025 may reduce investment returns and impact customer affordability.

Inflation directly increases claims costs, particularly for property and casualty insurance due to rising material expenses, and also escalates PSC's operational costs, necessitating strategic premium adjustments.

Consumer and business confidence levels are key indicators; Australia's ANZ-Roy Morgan Consumer Confidence Index around 77.5 in early 2024 suggested cautious optimism, while subdued business optimism in the UK's Q1 2024 CBI survey indicated potential impacts on commercial insurance demand.

| Economic Factor | 2024 Data/Projection | Impact on PSC Insurance Group |

| Australian GDP Growth | Projected 2.0% (RBA) | Supports demand for insurance services. |

| Global GDP Growth | Projected 3.2% (IMF) | Influences client economic health and risk appetite. |

| Interest Rates (Major Economies) | Generally higher in early 2024, with some easing late 2024/early 2025 | Boosts investment income when high, pressures margins when falling. |

| Inflation | Rising material costs impacting claims and operations | Increases claims settlement costs and operational expenses. |

| Consumer Confidence (Australia) | ANZ-Roy Morgan Index ~77.5 (early 2024) | Moderate optimism supports insurance spending. |

| Business Sentiment (UK) | Subdued optimism (Q1 2024 CBI Survey) | Potentially dampens demand for business insurance. |

Preview Before You Purchase

PSC Insurance Group PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This comprehensive PESTLE analysis of PSC Insurance Group delves into the Political, Economic, Social, Technological, Legal, and Environmental factors impacting the company. Understand the strategic implications and potential challenges for PSC Insurance Group with this detailed report.

Sociological factors

Demographic Shifts

Australia's demographic landscape is undergoing significant shifts, notably an aging population. By 2025, projections indicate a continued increase in the proportion of Australians aged 65 and over. This trend directly impacts PSC Insurance Group, creating a growing demand for products like aged care insurance and tailored retirement income solutions. Simultaneously, evolving household structures, including single-parent families and blended families, necessitate adaptable insurance coverage and financial planning services that reflect these diverse needs.

Changing Consumer Preferences

Modern consumers, particularly those in the 25-40 age bracket, are increasingly prioritizing transparency, seamless digital experiences, and personalized interactions when choosing financial services. For instance, a 2024 survey indicated that 78% of consumers expect financial institutions to offer personalized product recommendations, a significant jump from previous years.

PSC Insurance Group needs to actively adapt by bolstering its digital platforms, introducing more adaptable insurance products, and delivering customized advisory services to align with these evolving expectations. The company's investment in its mobile app, which saw a 20% increase in user engagement in late 2024, reflects a strategic move in this direction.

Failing to cater to these shifting consumer preferences risks not only customer churn but also a weakening of PSC's competitive standing in the market. In 2024, insurance companies that lagged in digital transformation reported an average 5% higher customer attrition rate compared to industry leaders.

Risk Perception and Awareness

Societal awareness of risks like cyber threats, climate change, and health crises directly impacts the demand for insurance. For instance, a 2024 report indicated a 30% increase in cyber insurance inquiries following major data breaches. This heightened perception allows PSC Insurance Group to tailor offerings, potentially boosting revenue.

PSC can leverage this increased risk awareness by actively educating its client base and developing specialized insurance products. By positioning itself as a proactive partner in managing these evolving concerns, the company can strengthen client relationships and capture market share. This strategy aligns with the growing consumer desire for comprehensive protection against modern perils.

Workforce Evolution

The modern workforce is rapidly changing, with a significant rise in flexible work arrangements, the gig economy, and remote employment. This evolution directly influences the types of insurance individuals and businesses require. For instance, the increasing number of independent contractors and freelancers highlights a need for specialized personal liability coverage and tailored business interruption policies for those operating from home.

PSC Insurance Group must remain agile in its product development to cater to these shifting employment landscapes. By understanding the unique risks associated with non-traditional work structures, PSC can offer more relevant and competitive insurance solutions. This adaptability is crucial for maintaining market share and meeting customer demands in 2024 and beyond.

Consider these key impacts:

- Rise of Gig Work: In 2024, an estimated 60 million Americans participated in the gig economy, a figure projected to grow. This necessitates insurance products that cover income volatility and liability for independent service providers.

- Remote Work Prevalence: Post-pandemic, remote work continues to be a significant trend. This impacts commercial insurance by potentially altering risks related to cybersecurity and property damage for home-based offices, and personal insurance by changing commuting risks.

- Demand for Flexibility: Employees increasingly value flexibility, pushing companies to adopt hybrid or fully remote models. Insurers need to offer flexible policy options that can adapt to fluctuating employee locations and work arrangements.

Ethical and Social Responsibility

Societal expectations for ethical conduct and corporate social responsibility are increasingly shaping consumer decisions and influencing talent acquisition. In 2024, a significant portion of consumers, estimated to be over 60%, reported actively seeking out brands that demonstrate strong ethical stances. PSC Insurance Group's dedication to Environmental, Social, and Governance (ESG) principles, coupled with its commitment to fair claims processing and active community involvement, directly addresses this trend. This focus can significantly bolster its brand image, making it more attractive to clients and potential employees who prioritize socially conscious businesses.

Transparency regarding these ethical commitments is paramount. For instance, PSC's reporting on its ESG performance, such as its progress in reducing its carbon footprint or its diversity and inclusion initiatives, directly impacts its public perception. By clearly communicating these efforts, PSC can build trust and differentiate itself in a competitive market. This is particularly relevant as studies in 2025 indicate that over 70% of millennials and Gen Z consider a company's social impact when making purchasing or employment decisions.

- Growing Consumer Demand: Over 60% of consumers in 2024 indicated a preference for ethically aligned brands.

- Talent Attraction: A majority of younger professionals prioritize employers with strong ESG commitments.

- Brand Reputation Enhancement: PSC's ESG initiatives and community engagement boost its appeal.

- Transparency as a Key Differentiator: Clear communication of ethical practices builds trust and market advantage.

Societal Shifts Drive Insurance Innovation & Digital Engagement

Societal shifts, including an aging demographic and evolving family structures, directly influence PSC Insurance Group's product development and service offerings. For example, the increasing demand for retirement solutions and adaptable coverage for diverse households highlights a need for specialized financial planning. Furthermore, a growing emphasis on digital engagement and personalized experiences, with 78% of consumers expecting tailored recommendations in 2024, necessitates robust online platforms and customer-centric strategies.

Technological factors

Digital Transformation and Automation

The insurance sector's digital transformation is accelerating, with a significant push towards automation. This trend is driven by the need for greater efficiency and cost reduction. For instance, in 2024, many insurance firms reported that investments in AI and automation technologies were key to improving claims processing times and customer service interactions, with some seeing up to a 30% reduction in manual processing errors.

PSC Insurance Group can capitalize on this by integrating Robotic Process Automation (RPA) for repetitive tasks like data entry and policy administration. Furthermore, developing robust digital portals for clients to manage their policies, submit claims, and access information offers a substantial opportunity to enhance customer satisfaction and operational streamlining. This digital shift is crucial for remaining competitive in the evolving insurance landscape.

Data Analytics and AI/ML

Advanced data analytics and AI/ML are transforming how PSC Insurance Group assesses risk and manages operations. By leveraging these technologies, PSC can gain a more granular understanding of client risk profiles, leading to more accurate underwriting and pricing. For instance, in 2024, insurers utilizing AI for fraud detection reported an average reduction in fraudulent claims by up to 15%, directly boosting profitability.

The predictive capabilities of AI and ML allow PSC to anticipate claim likelihoods with greater precision, enabling proactive risk mitigation strategies. This also facilitates the personalization of insurance products, tailoring coverage to individual client needs and improving customer satisfaction. Machine learning models are proving invaluable, with some firms seeing a 10% improvement in claims processing efficiency through AI-driven automation.

Cybersecurity and Data Protection

Cybersecurity is a critical technological factor for PSC Insurance Group, given its handling of sensitive client financial information. In 2024, the global cost of cybercrime was projected to reach $10.5 trillion annually, highlighting the immense risk financial institutions face. PSC's investment in advanced security protocols and data encryption is therefore essential not only to safeguard against sophisticated cyberattacks but also to ensure compliance with evolving data protection regulations like GDPR and similar frameworks, which carry substantial penalties for breaches.

Insurtech Innovations

The rise of Insurtech startups is fundamentally reshaping the insurance landscape. These agile companies are introducing novel business models, such as peer-to-peer insurance platforms and usage-based policies that tailor premiums to individual behavior. For PSC Insurance Group, staying abreast of these innovations is crucial for maintaining a competitive edge. This could involve strategic partnerships or even acquisitions of promising Insurtech firms to integrate advanced technologies and foster greater market relevance.

The Insurtech sector saw significant investment activity leading up to July 2025. For instance, global Insurtech funding reached approximately $15 billion in 2023, with a notable portion directed towards startups focused on AI-driven underwriting and personalized customer experiences. PSC's strategic response to these trends could include:

- Exploring partnerships with Insurtechs specializing in AI for claims processing to improve efficiency.

- Evaluating the integration of telematics data for usage-based insurance products, mirroring successful models in the automotive sector.

- Investing in digital platforms that enhance customer engagement and streamline policy management.

- Monitoring regulatory changes that may impact the adoption of new Insurtech technologies.

Enhanced Customer Engagement Platforms

PSC Insurance Group's technological advancements are significantly boosting customer engagement. By utilizing online platforms, mobile apps, and robust CRM systems, the company can now offer more personalized interactions and efficient service. This digital push allows clients real-time access to their policy details, fostering greater satisfaction and loyalty in the increasingly competitive insurance landscape.

The adoption of these enhanced customer engagement platforms is crucial for maintaining a competitive edge. For instance, many insurance providers reported a substantial increase in digital channel usage during 2024, with mobile app interactions often growing by over 20% year-over-year. This trend highlights the growing expectation for seamless, digital-first customer experiences.

- Personalized Communication: Tailoring messages and offers based on individual customer data.

- Efficient Service Delivery: Streamlining claims processing and policy inquiries through digital channels.

- Real-time Information Access: Empowering customers with instant access to their policy documents and updates.

- Enhanced Customer Satisfaction: Building stronger relationships through responsive and accessible digital support.

Tech Transforms Insurance: Efficiency, Engagement & Risk Management

Technological advancements are fundamentally reshaping the insurance sector, driving efficiency and customer engagement for PSC Insurance Group. Automation, particularly through AI and RPA, is streamlining operations like claims processing, with firms reporting up to a 30% reduction in manual errors in 2024. Advanced data analytics and AI are enhancing risk assessment and fraud detection, with insurers seeing up to a 15% reduction in fraudulent claims.

The increasing prevalence of Insurtech startups, which attracted around $15 billion in global funding in 2023, necessitates PSC's strategic engagement through partnerships or acquisitions. Cybersecurity remains paramount, especially with the global cost of cybercrime projected to reach $10.5 trillion annually in 2024, requiring robust security measures to protect sensitive data and ensure regulatory compliance.

Digital platforms and mobile apps are significantly improving customer engagement, with many insurers experiencing over a 20% year-over-year growth in mobile app interactions in 2024, enabling personalized communication and real-time information access.

Legal factors

Insurance Laws and Regulations

PSC Insurance Group navigates a dense regulatory landscape, adhering to stringent rules on licensing, policy clarity, and claims processing. For instance, in Australia, the Insurance Contracts Act 1984, with ongoing reforms, dictates many aspects of product design and consumer interaction. Failure to comply can result in significant fines and the loss of operating licenses, underscoring the critical nature of regulatory adherence for PSC.

Financial Services Licensing and Conduct

As an Australian Financial Services Licence (AFSL) holder, PSC Insurance Group operates under the strict oversight of the Australian Securities and Investments Commission (ASIC). This necessitates adherence to key conduct obligations, including the best interests duty, ensuring clients' needs are prioritized. For instance, ASIC's enforcement actions in 2023 highlighted the importance of robust compliance frameworks, with significant penalties levied against entities failing to meet these standards.

PSC must also comply with responsible lending practices where applicable, and demonstrate fair dealing with all clients. Maintaining up-to-date compliance training for staff and implementing strong internal controls are critical to meeting these regulatory expectations and mitigating the risk of misconduct allegations. In 2024, ASIC continued its focus on consumer protection, reinforcing the need for financial services firms to demonstrate a commitment to ethical conduct and transparent dealings.

Data Privacy and Security Laws

PSC Insurance Group operates under Australia's Privacy Act 1988 and other data protection regulations, which govern the collection, storage, and use of personal information. These laws mandate strict handling of sensitive financial and customer data, directly influencing PSC's technology infrastructure and data governance frameworks.

The increasing global emphasis on data breaches and enhanced consumer rights, particularly evident in regulatory actions throughout 2024 and anticipated in 2025, necessitates robust compliance measures. For PSC, this means ensuring all data handling practices align with evolving legal requirements to mitigate risks and maintain customer trust.

Anti-Money Laundering (AML) and Counter-Terrorism Financing (CTF)

PSC Insurance Group, operating within the financial services sector, is subject to rigorous Anti-Money Laundering (AML) and Counter-Terrorism Financing (CTF) regulations. These laws mandate that PSC implement robust measures to prevent the use of its services for illegal financial activities. This includes thorough Know Your Customer (KYC) procedures for client onboarding, the diligent reporting of any suspicious transactions, and continuous monitoring of financial flows.

Failure to adhere to these AML/CTF obligations can result in substantial financial penalties and significant damage to PSC's reputation. For instance, in 2023, financial institutions globally faced billions in AML-related fines. To mitigate these risks, PSC must maintain and regularly update comprehensive internal policies and provide ongoing training to its staff on these critical compliance matters.

- Client Due Diligence: PSC must verify the identity of all clients and understand the nature of their business to prevent illicit activities.

- Transaction Monitoring: Continuous oversight of transactions is required to detect and report any unusual or suspicious patterns.

- Regulatory Reporting: Timely submission of Suspicious Activity Reports (SARs) to relevant authorities is a core requirement.

- Staff Training: Regular and effective training programs are essential to ensure all employees understand their AML/CTF responsibilities.

Consumer Protection and Dispute Resolution

Consumer protection laws are a significant legal factor for PSC Insurance Group. These regulations, designed to safeguard individuals engaging with financial services, directly influence PSC's operational procedures. For instance, the Australian Financial Complaints Authority (AFCA) provides a structured avenue for dispute resolution, impacting how PSC handles client grievances and aims for fair, timely outcomes. This focus on client trust and regulatory compliance shapes PSC's approach to product development and the clarity of its disclosures.

Ensuring adherence to these consumer protection frameworks is paramount. In the 2023-2024 financial year, AFCA reported receiving over 100,000 complaints across various financial sectors, highlighting the volume and importance of these mechanisms. PSC's commitment to robust internal complaint handling and transparent communication is therefore essential not only for maintaining client loyalty but also for mitigating potential regulatory scrutiny and associated costs.

- Consumer Protection Laws: Statutes mandating fair treatment and transparency in financial dealings.

- Dispute Resolution: Mechanisms like AFCA offer avenues for addressing client complaints.

- Client Trust: Fair and timely dispute resolution is key to maintaining customer confidence.

- Regulatory Compliance: Adherence to consumer protection laws helps avoid penalties and reputational damage.

Navigating Australian Insurance Regulatory Compliance 2023-2025

PSC Insurance Group operates within a complex web of legal and regulatory frameworks, particularly in Australia. These laws govern everything from how policies are designed and sold to how claims are processed and customer data is handled. For example, the Insurance Contracts Act 1984 in Australia sets many of the rules PSC must follow. Adherence is crucial, as non-compliance can lead to substantial fines and even the loss of their operating licenses, making legal compliance a core operational imperative for PSC in 2024 and beyond.

The Australian Securities and Investments Commission (ASIC) maintains rigorous oversight of PSC as an Australian Financial Services Licence (AFSL) holder. This includes enforcing conduct obligations like the best interests duty, ensuring clients' needs are paramount. ASIC's enforcement actions in 2023, which saw significant penalties for compliance failures, underscore the critical need for PSC to maintain robust internal controls and up-to-date compliance training for its staff. This focus on consumer protection and ethical conduct is expected to continue through 2025.

Furthermore, PSC must comply with Australia's Privacy Act 1988 and other data protection laws, which dictate how sensitive customer information is collected, stored, and used. The increasing global trend of stringent data breach regulations, evident in regulatory actions throughout 2024 and projected for 2025, means PSC must ensure its data governance aligns with these evolving legal standards to protect customer trust and avoid penalties.

Anti-Money Laundering (AML) and Counter-Terrorism Financing (CTF) regulations are also key legal considerations for PSC. These laws require thorough Know Your Customer (KYC) procedures, transaction monitoring, and the reporting of suspicious activities. Global AML fines in 2023 alone amounted to billions, highlighting the severe financial and reputational risks associated with non-compliance, making ongoing staff training and policy updates essential for PSC.

| Legal Area | Key Legislation/Body | Impact on PSC | Regulatory Focus (2023-2025) | Example Penalty Type |

|---|---|---|---|---|

| Insurance Regulation | Insurance Contracts Act 1984 (AUS) | Policy design, claims processing, consumer interaction | Ongoing reforms, product clarity | Fines, license suspension |

| Financial Services Conduct | ASIC (AUS) | Best interests duty, fair dealing, client needs | Consumer protection, enforcement actions | Significant financial penalties |

| Data Protection | Privacy Act 1988 (AUS) | Data collection, storage, usage, privacy | Data breach mitigation, enhanced consumer rights | Reputational damage, fines |

| Financial Crime Prevention | AML/CTF Laws (AUS) | KYC, transaction monitoring, SARs | Preventing illicit financial activities | Billions in global fines |

Environmental factors

Climate Change Impact on Claims

Climate change is significantly increasing the frequency and intensity of extreme weather events, directly affecting PSC Insurance Group's profitability, especially in property and casualty insurance. For instance, in 2024, Australia experienced a notable rise in severe weather, with insured losses from natural catastrophes estimated to be in the billions, impacting claims costs for insurers like PSC.

Events such as widespread flooding and severe storms result in higher claims payouts, which in turn can influence how PSC assesses and prices insurance policies in affected areas. This trend also raises concerns about the long-term availability and affordability of coverage in regions prone to these escalating climate-related risks.

To counter these impacts, PSC is compelled to continuously refine its risk assessment methodologies and adjust its pricing strategies. This adaptation is crucial for maintaining underwriting profitability and ensuring the sustainability of its insurance products in the face of a changing climate.

ESG Reporting and Compliance

The increasing demand for Environmental, Social, and Governance (ESG) reporting is significantly impacting financial services. PSC Insurance Group, like its peers, is navigating a landscape where regulators and stakeholders expect greater transparency on sustainability. For instance, by the end of 2024, many jurisdictions are implementing stricter climate-related disclosure requirements, pushing companies to quantify their environmental footprint and transition plans.

This evolving regulatory environment means PSC will likely need to report on climate risks, such as the physical impact of extreme weather on its assets or the transition risks associated with a low-carbon economy. Such disclosures are becoming standard practice, with major stock exchanges and financial bodies, like the Task Force on Climate-related Financial Disclosures (TCFD), setting benchmarks that companies are increasingly adopting or being mandated to follow.

Consequently, PSC's approach to corporate governance, its investment strategies, and its overall transparency with investors and clients will be shaped by these ESG reporting mandates. This shift influences how PSC manages its operations and communicates its commitment to sustainability, directly impacting investor confidence and its long-term financial resilience.

Natural Disaster Resilience

PSC Insurance Group plays a key role in helping clients navigate environmental risks by offering advice on natural disaster resilience. This can include suggesting ways to reduce risk or providing specific insurance for events like floods and storms, which saw significant insured losses globally in 2024, with preliminary estimates suggesting billions in damages.

The company's own preparedness for environmental events is also vital. Ensuring their operations can continue without interruption during natural disasters is crucial for maintaining service delivery to their policyholders, especially as climate change continues to influence the frequency and intensity of extreme weather events.

Sustainability in Investment Practices

Sustainability is increasingly shaping investment decisions, influencing how PSC Insurance Group approaches wealth management and underwriting. The global shift towards Environmental, Social, and Governance (ESG) investing means that capital allocation is being scrutinized for its environmental impact, potentially altering asset choices for both PSC and its clients. For example, by the end of 2023, global sustainable investment assets reached an estimated $150 trillion, demonstrating a significant market demand for environmentally conscious options.

This trend directly impacts PSC's underwriting capital and wealth management services, as clients and regulators alike expect a commitment to sustainable practices. PSC may see a greater demand for investment products that align with environmental goals, such as renewable energy or green bonds. In 2024, the Responsible Investment market is projected to grow by 15-20% annually, indicating a strong and sustained interest in this area.

- Growing ESG Demand: Investors are actively seeking investments that demonstrate positive environmental impact, influencing asset selection.

- Regulatory Influence: Environmental regulations and reporting requirements are becoming more stringent, pushing financial institutions towards sustainable operations.

- Climate Risk Management: PSC must consider the physical and transitional risks associated with climate change when underwriting policies and managing investments.

- Reputational Impact: A strong sustainability stance can enhance PSC's brand reputation and attract environmentally conscious clients and talent.

Regulatory Focus on Climate Risk

Regulators are intensifying their focus on climate risk, with bodies like APRA (Australian Prudential Regulation Authority) actively scrutinizing how financial institutions manage and disclose these evolving threats. This means PSC Insurance Group must showcase strong systems for identifying, assessing, and mitigating climate-related financial risks throughout its broking, underwriting, and financial planning divisions to align with growing regulatory demands. For instance, APRA's Prudential Practice Guide APG 210 outlines expectations for climate risk governance and risk management, which PSC would need to address.

PSC's proactive approach to these regulatory shifts is crucial. Demonstrating a clear understanding and implementation of climate risk management frameworks will be key to maintaining compliance and investor confidence. This includes transparent reporting on how climate change impacts their business operations and the financial products they offer. The increasing emphasis on Environmental, Social, and Governance (ESG) factors by investors further underscores the importance of this regulatory alignment.

- APRA's Climate Risk Expectations: APRA's ongoing work on climate risk, including potential future prudential standards, necessitates a robust response from entities like PSC.

- Disclosure Requirements: PSC must ensure its disclosures align with evolving international and domestic reporting frameworks, such as those recommended by the Task Force on Climate-related Financial Disclosures (TCFD).

- Operational Resilience: The group needs to assess and manage the physical and transitional risks associated with climate change across its diverse business lines.

- Investor Demand for ESG: Growing investor interest in ESG performance means that strong climate risk management is becoming a competitive advantage.

PSC Insurance Navigates Climate & ESG Pressures

The escalating frequency of extreme weather events, such as the severe storms and floods impacting Australia in 2024, directly increases insurance claims and operational costs for PSC Insurance Group. This necessitates continuous adaptation in risk assessment and pricing to maintain profitability amidst growing climate volatility.

PSC faces increasing pressure from regulators and investors to enhance transparency regarding its environmental impact and climate risk management strategies. By the close of 2024, stricter climate-related disclosure mandates are being implemented globally, pushing companies like PSC to quantify their environmental footprint and transition plans.

The global surge in ESG investing, with sustainable investment assets reaching an estimated $150 trillion by the end of 2023, is reshaping how PSC approaches its investment and underwriting decisions. This trend highlights a significant market demand for environmentally conscious financial products and services, influencing PSC's capital allocation and service offerings.

PESTLE Analysis Data Sources

Our PESTLE analysis for PSC Insurance Group draws on a comprehensive mix of data, including official government publications, reputable financial news outlets, and industry-specific market research reports. This ensures a robust understanding of the political, economic, social, technological, legal, and environmental factors impacting the insurance sector.