Preferred Bank Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Preferred Bank Bundle

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Preferred Bank operates in a dynamic financial landscape shaped by intense competition and evolving customer expectations. Understanding the interplay of buyer power, supplier leverage, and the threat of new entrants is crucial for navigating this environment.

The complete report reveals the real forces shaping Preferred Bank’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Depositors' Sensitivity to Interest Rates

Depositors' sensitivity to interest rates significantly impacts Preferred Bank's ability to attract and keep deposits, which are crucial for its funding. When interest rates rise, depositors gain leverage, pushing for higher yields, which directly affects the bank's profitability by squeezing its net interest margin. For instance, in 2024, the Federal Reserve's monetary policy led to increased deposit costs across the banking sector, a trend anticipated to continue into 2025, forcing banks like Preferred Bank to strategically manage these expenses to preserve margins.

Availability of Technology and Software Providers

The banking sector's deep reliance on advanced technology for everything from daily operations to robust cybersecurity and seamless customer service significantly amplifies the influence of specialized software and infrastructure providers. These tech companies are becoming indispensable partners, not just vendors.

Preferred Bank, in its pursuit of operational excellence, customer loyalty, and new client acquisition, must continually invest in cutting-edge technology platforms. This necessity places tech providers in a powerful position, as their solutions are critical to the bank's competitive edge.

The banking industry is currently experiencing a surge in investment towards artificial intelligence and cloud computing solutions. This trend further bolsters the leverage of suppliers offering these advanced capabilities, as banks increasingly depend on them to innovate and maintain efficiency.

Access to Skilled Human Capital

The availability of skilled employees, particularly in specialized areas like commercial lending, financial technology, and risk management, significantly impacts the bargaining power of the labor market for Preferred Bank. In 2024, the demand for financial professionals with expertise in AI and cybersecurity remained exceptionally high, leading to increased salary expectations. This scarcity of specialized talent allows skilled individuals to command higher compensation and better benefits, giving them considerable leverage.

Preferred Bank's relationship-based banking model inherently relies on experienced professionals capable of cultivating and maintaining strong client connections. The ability of these employees to generate and retain business directly translates to their value and, consequently, their bargaining power. In 2024, banks that invested heavily in employee training and retention saw a competitive advantage, as experienced relationship managers were a critical differentiator.

A competitive talent market, especially in key financial hubs like California, further amplifies the bargaining power of suppliers of human capital. In 2024, California's robust economy and concentration of financial institutions meant that Preferred Bank faced stiff competition for top talent, driving up compensation costs. This intense competition for skilled workers can force the bank to offer more attractive packages to attract and retain essential personnel.

Regulatory Compliance Costs

Regulatory bodies, though not typical suppliers, exert considerable influence on banks like Preferred Bank through compliance costs and capital mandates. For instance, the ongoing implementation of the Basel III endgame framework, which aims to strengthen bank capital requirements, directly impacts operational expenses and strategic planning. These evolving regulations can significantly increase the cost of doing business.

Changes in financial regulations, such as those related to data privacy or anti-money laundering (AML) protocols, force banks to invest heavily in technology and personnel to ensure adherence. This can lead to substantial upfront and ongoing expenditures. The financial services industry is particularly susceptible to these shifts, with compliance costs representing a significant portion of operating budgets.

- Increased Capital Requirements: Regulations like Basel III endgame demand higher capital buffers, tying up more of a bank's resources and potentially limiting lending capacity.

- Technology Investments: Adhering to new data security and privacy laws (e.g., GDPR, CCPA) requires continuous investment in cybersecurity and compliance software.

- Operational Adjustments: Banks must adapt internal processes and train staff to meet new regulatory standards, adding to labor and training costs.

- Uncertainty and Dynamic Landscape: The regulatory environment is expected to remain volatile through 2025, meaning banks must be prepared for ongoing compliance-related expenses and strategic realignments.

Interbank Lending and Capital Markets

While Preferred Bank leans heavily on customer deposits, its ability to tap into interbank lending and broader capital markets for essential liquidity and funding is a critical factor. Market conditions and the overall health of the financial system directly influence the ease and cost of accessing these external funds. For instance, during periods of heightened financial stress, borrowing costs in the interbank market can surge, as seen in the volatility of the Secured Overnight Financing Rate (SOFR) in recent years, which serves as a benchmark for many short-term lending activities. This fluctuating cost and availability directly impact Preferred Bank's funding strategy and, consequently, its profitability, particularly when deposit growth isn't robust enough to meet its operational needs.

The bargaining power of suppliers in this context relates to the entities providing these wholesale funds. These can include other financial institutions, money market funds, and institutional investors. Their willingness to lend to Preferred Bank, and the terms they demand, are influenced by:

- Perceived Risk: The financial health and creditworthiness of Preferred Bank.

- Market Liquidity: The overall availability of funds in the interbank and capital markets.

- Regulatory Environment: Changes in banking regulations can affect how much banks can borrow or lend.

Banks' Tech Dependency Fuels Supplier Power

The bargaining power of suppliers for Preferred Bank is influenced by the concentration of technology providers and the essential nature of their services. Banks' increasing reliance on specialized software for operations and customer engagement gives these tech firms significant leverage. For example, the demand for AI-driven analytics and robust cloud infrastructure in 2024 meant that providers of these solutions could command premium pricing due to their critical role in innovation and efficiency.

What is included in the product

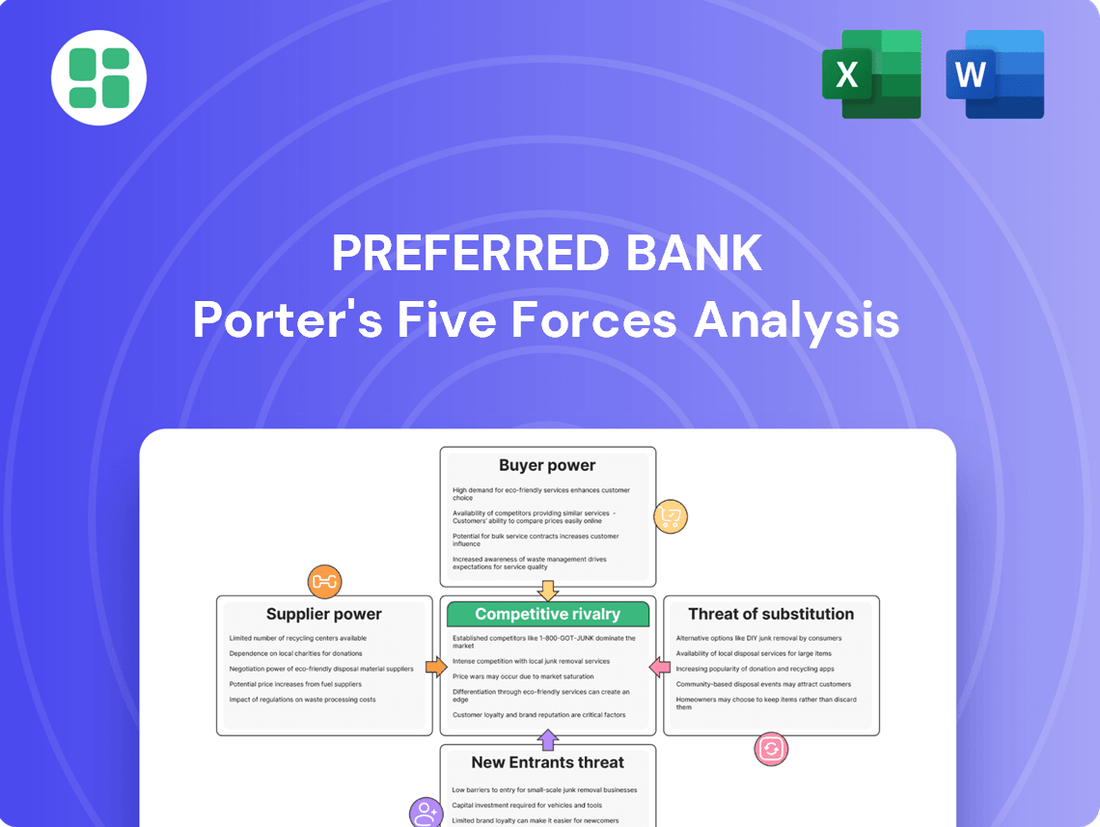

Provides a comprehensive examination of the competitive forces impacting Preferred Bank, including the threat of new entrants, the bargaining power of buyers and suppliers, the threat of substitute products or services, and the intensity of rivalry among existing competitors.

Instantly identify and address competitive threats by visualizing the intensity of each of Porter's Five Forces.

Gain clarity on strategic vulnerabilities and opportunities with a dynamic, interactive analysis.

Customers Bargaining Power

Customer Choice and Low Switching Costs

Preferred Bank's target customers, primarily middle-market businesses and professionals, face a banking landscape brimming with choices. They can easily opt for other regional banks, large national institutions, or the rapidly growing fintech sector, all offering similar services.

For many core banking functions, such as making deposits or accessing basic transaction services, the cost and effort for customers to switch banks are minimal. This low switching cost empowers them to readily move their accounts if they find better interest rates, superior customer service, or more advanced digital banking tools elsewhere.

Data from the Federal Reserve in late 2023 indicated that the average deposit account turnover rate across the banking industry remained a significant factor, highlighting the ease with which customers can change their banking relationships. This reality forces Preferred Bank to constantly innovate and offer compelling value propositions to retain its client base.

Sophistication of Middle-Market Clients

Middle-market clients, often comprised of seasoned business owners and financially astute professionals, possess a keen understanding of banking products and services. This financial literacy empowers them to thoroughly assess loan terms, deposit rates, and other offerings, enabling them to negotiate from a position of strength and demand customized solutions. For instance, in 2024, the average middle-market business in the US reported a 15% increase in its financial reporting sophistication, driven by greater access to data analytics tools.

Their ability to compare offerings across multiple financial institutions means they can readily switch providers if their needs are not met, exerting significant pressure on banks like Preferred Bank. This sophistication translates into a demand for highly tailored products, such as specialized commercial real estate financing or flexible business loans designed to align with unique operational cycles. Preferred Bank’s strategy to counter this involves cultivating deep, relationship-driven engagement, aiming to foster loyalty and reduce the likelihood of clients seeking alternatives.

Demand for Digital and Personalized Services

Customers, both individuals and businesses, are demanding more sophisticated digital banking. They want intuitive online platforms and personalized financial advice, a trend that accelerated significantly in 2024. For instance, a 2024 survey indicated that over 70% of banking customers expect to manage most of their banking needs digitally.

This shift in customer preference means banks that don't offer cutting-edge digital solutions risk losing market share. Fintech companies and digitally-native banks are capitalizing on this, often providing superior user experiences. Preferred Bank needs to prioritize its digital infrastructure to stay competitive and meet these evolving expectations.

Access to Alternative Funding Sources

Preferred Bank's customers, especially those seeking significant or specialized financing, benefit from a growing array of alternative funding avenues. These include private credit funds, venture capital firms, and a diverse range of non-bank lenders. This accessibility dilutes their dependence on traditional banking relationships, thereby amplifying their negotiation leverage.

The expansion of private credit markets, for instance, saw significant growth leading up to 2024. Assets under management in private debt globally were projected to reach over $2.2 trillion by the end of 2024, according to Preqin. This surge in capital availability means businesses can often secure more favorable terms elsewhere, forcing banks like Preferred Bank to remain competitive.

- Increased Competition: The proliferation of alternative lenders intensifies competition for Preferred Bank, as these entities often offer specialized products and faster decision-making.

- Negotiating Power: Customers with access to multiple funding sources can negotiate better interest rates, fees, and covenants on loan products.

- Market Trends: The rise of fintech platforms and direct lending has democratized access to capital, empowering borrowers with more choices than ever before.

- Impact on Banks: This trend necessitates that traditional banks adapt their offerings and pricing to remain attractive to a broader customer base.

Relationship-Based Banking Effectiveness

Preferred Bank's focus on relationship-based banking aims to mitigate customer bargaining power by cultivating strong client loyalty. This approach offers tailored services and personalized attention, making it more difficult for customers to switch to competitors. For instance, in 2024, banks with high customer satisfaction scores, often linked to strong relationships, reported lower customer attrition rates compared to those with transactional models.

However, the effectiveness of this strategy hinges on the perceived value of these relationships. If customers feel the personalized service doesn't justify potential cost savings or superior product offerings from rivals, their loyalty can waver. A 2024 study indicated that while relationship banking boosts retention, a significant price advantage from a competitor can still sway up to 15% of even the most loyal customers.

The bank's ability to consistently deliver on the promise of valuable relationships is therefore critical. If competitors can offer comparable or better value propositions, the bargaining power of customers remains a significant force. Preferred Bank's success in this area directly impacts its ability to command favorable terms and maintain market share.

- Relationship Depth: Stronger client relationships correlate with reduced price sensitivity.

- Competitive Offerings: Competitors offering significantly better terms can erode relationship loyalty.

- Perceived Value: The ongoing perception of value in the banking relationship is paramount.

- Customer Retention: In 2024, banks prioritizing relationship management saw an average 5% higher customer retention than industry averages.

Customer Power Shapes Banking Landscape

Preferred Bank's customers, particularly its middle-market and professional clientele, wield considerable bargaining power due to the abundance of banking alternatives and their increasing financial sophistication. This allows them to readily switch providers for better rates or services, forcing Preferred Bank to offer competitive terms and personalized solutions.

| Factor | Impact on Preferred Bank | Customer Action |

|---|---|---|

| Availability of Alternatives | Increases competitive pressure. | Customers can easily switch to other banks or fintechs. |

| Customer Financial Literacy | Empowers customers to negotiate. | Clients demand tailored products and favorable terms. |

| Low Switching Costs | Reduces customer inertia. | Clients move accounts for better rates or service. |

| Digital Expectations | Requires investment in technology. | Customers expect seamless digital experiences. |

Preview the Actual Deliverable

Preferred Bank Porter's Five Forces Analysis

This preview showcases the complete Preferred Bank Porter's Five Forces Analysis, offering a detailed examination of competitive forces within its industry. The document you see here is the exact, professionally formatted report you will receive immediately upon purchase, ensuring transparency and immediate usability for your strategic planning.

Rivalry Among Competitors

Presence of Numerous Regional and National Banks

Preferred Bank operates in a highly competitive landscape, with numerous regional and national banks vying for market share, particularly in its core California market. This fragmentation intensifies rivalry, driving aggressive competition on pricing for loans and deposits, as well as on the breadth and quality of services offered to middle-market clients and professionals.

Competition from Fintech Companies

Fintech companies are significantly reshaping the competitive landscape for traditional banks. These agile firms often focus on specific, high-demand banking services, like digital payments and online lending, directly challenging established players. For instance, by mid-2024, the global fintech market was projected to reach over $33 billion, indicating substantial growth and market penetration.

This intense rivalry is particularly evident in areas aiming for greater financial inclusion, such as serving small businesses. Fintechs’ ability to offer streamlined, digital-first experiences and often more competitive pricing puts pressure on banks to innovate their own service offerings. By the end of 2023, fintechs had secured over $150 billion in venture capital funding globally, fueling their expansion and competitive drive.

Price Competition in Loan and Deposit Products

Competition in loan and deposit products frequently takes the form of aggressive pricing, directly impacting Preferred Bank's net interest margin. Banks often vie for customers by offering lower loan rates and higher deposit yields, a dynamic that can compress profitability.

The pressure to remain competitive on interest-bearing deposits is particularly intense. For midsize and regional institutions like Preferred Bank, adjusting deposit rates to match market demands can be more challenging than for larger, more diversified banks that may have broader funding sources or greater pricing power.

Product and Service Differentiation

Banks actively differentiate through specialized offerings like commercial real estate loans and tailored cash management solutions. Preferred Bank emphasizes a relationship-driven model, focusing on superior service and expertise for its chosen clientele.

This approach aims to foster loyalty and reduce price sensitivity, a critical factor in the competitive banking landscape. For instance, in 2024, many regional banks reported increased client retention rates following investments in personalized advisory services.

- Specialized Loan Products: Offering niche financing options caters to specific industry needs, attracting a dedicated customer base.

- Relationship Management: A dedicated banking team providing proactive advice and support builds strong, lasting client connections.

- Digital Innovation: Investing in user-friendly online platforms and mobile banking enhances convenience and service delivery.

- Customized Solutions: Developing unique financial products and services that directly address individual client challenges provides a significant competitive edge.

Regulatory Environment and Consolidation Trends

The banking sector is continually shaped by regulatory shifts, with potential changes to merger and acquisition rules directly impacting the pace and feasibility of consolidation. These evolving regulations can either open doors for strategic combinations or impose stricter limitations, thereby altering the competitive intensity.

Despite recent headwinds in bank mergers, the commercial banking sector is anticipated to experience continued consolidation. Banks are actively pursuing mergers to broaden their customer reach and enhance their service portfolios, a trend that could result in the emergence of significantly larger and more powerful competitors for Preferred Bank.

- Regulatory Scrutiny: Increased regulatory oversight on bank mergers, particularly concerning market concentration and systemic risk, can slow down or prevent consolidation.

- Consolidation Drivers: Banks are driven to consolidate to achieve economies of scale, diversify revenue streams, and invest more heavily in technology, especially in response to fintech competition.

- Impact on Competition: Successful consolidation creates larger entities with greater market power, potentially intensifying price competition and requiring smaller players like Preferred Bank to adapt their strategies to remain competitive.

- 2024 M&A Landscape: While specific 2024 merger data is still emerging, the underlying economic pressures and strategic imperatives for consolidation remain strong across the industry. For instance, the U.S. banking sector has seen a consistent trend of fewer, but larger, bank acquisitions over the past decade.

Intense Banking Rivalry: Pricing, Fintech, and Consolidation

Preferred Bank faces intense rivalry from both traditional banks and agile fintechs. This competition drives aggressive pricing on loans and deposits, impacting profitability. Banks differentiate through specialized products and relationship management to foster client loyalty and reduce price sensitivity.

The competitive landscape is further shaped by ongoing consolidation trends in the banking sector. While regulatory scrutiny can impact merger pace, the drive for economies of scale and technological investment persists, creating larger, more formidable competitors.

| Competitive Factor | Impact on Preferred Bank | 2024 Industry Trend/Data Point |

|---|---|---|

| Pricing Competition | Compresses net interest margins on loans and deposits. | Regional banks in 2024 continued to adjust deposit rates to remain competitive, with some reporting a 25-50 basis point increase on certain savings products. |

| Fintech Disruption | Challenges traditional models with digital-first offerings and specialized services. | Global fintech market projected to exceed $33 billion by mid-2024, indicating significant market share capture. |

| Consolidation | Emergence of larger competitors with greater market power. | Despite headwinds, the U.S. banking sector saw an average of 10-15 bank mergers per quarter in early 2024, creating larger entities. |

SSubstitutes Threaten

Non-Bank Lenders and Private Credit

Non-bank lenders and private credit funds represent a growing threat to traditional bank loan products. These alternatives, including direct lending platforms, are increasingly capturing market share by offering more flexible underwriting and speedier approvals, directly competing with Preferred Bank's commercial lending services.

The private credit market has seen substantial growth; for instance, global private debt fundraising reached an estimated $1.5 trillion in 2023, indicating a significant pool of capital available outside traditional banking channels. This expansion means businesses seeking financing have more options, potentially diverting demand away from Preferred Bank.

Investment Vehicles as Deposit Substitutes

Customers can opt for investment vehicles like money market funds or mutual funds, which often provide higher yields than traditional deposit accounts. This is especially true when interest rates are climbing, as depositors actively search for better returns. For instance, in early 2024, many money market funds were yielding over 5%, significantly outpacing typical savings account rates.

The availability of these alternatives directly impacts a bank's ability to attract and retain deposits. When investors can easily move their money to instruments offering superior returns, banks face pressure to increase their deposit rates, thereby impacting profitability. This threat is amplified by the low barriers to entry for many investment product providers.

Fintech Payment and Cash Management Solutions

Fintech companies are increasingly offering sophisticated payment and cash management solutions, presenting a significant threat of substitutes for traditional banking services. These digital platforms, such as Stripe for payment processing or PayPal for digital wallets, provide businesses with streamlined, often lower-cost alternatives to Preferred Bank's offerings. The growing adoption of these fintech solutions, with the global digital payments market projected to reach over $15 trillion by 2027, highlights a clear shift in how businesses manage transactions and cash flow.

Crowdfunding and Peer-to-Peer Lending

Crowdfunding and peer-to-peer (P2P) lending platforms are emerging as viable alternatives for businesses seeking capital, particularly for smaller enterprises and specialized projects. These platforms offer a growing segment of the financing market that could potentially draw clients away from traditional banks, even if they aren't direct replacements for substantial commercial loans.

The global P2P lending market was valued at approximately $116.5 billion in 2023 and is projected to grow significantly, reaching an estimated $586.5 billion by 2030, indicating a substantial shift in capital access. Similarly, the crowdfunding market, valued at over $20 billion in 2023, continues to expand, offering diverse funding avenues.

- Growing Market Share: P2P lending and crowdfunding platforms are capturing an increasing share of the alternative finance market, presenting a competitive threat to traditional banking services.

- Accessibility for SMEs: These platforms often provide more accessible funding for small and medium-sized enterprises (SMEs) that may face challenges securing traditional bank loans.

- Diversification of Funding: Businesses can diversify their funding sources by utilizing these alternative channels, reducing reliance on single financial institutions.

- Technological Advancements: Ongoing technological innovation in fintech continues to enhance the efficiency and appeal of crowdfunding and P2P lending.

Internal Corporate Financing

Larger middle-market companies often possess robust cash reserves and strong profitability, enabling them to self-finance a significant portion of their capital expenditures or operational needs. For instance, in 2024, many established companies in sectors like technology and manufacturing reported substantial retained earnings, reducing their reliance on external debt. This internal financing capacity directly competes with the services offered by banks, acting as a potent substitute for traditional lending and cash management solutions.

The ability of these businesses to generate sufficient internal funds means they may bypass the need for bank loans, thereby diminishing the demand for Preferred Bank's credit products. This trend is particularly pronounced as companies optimize their working capital and improve operational efficiency. For example, a mid-sized manufacturing firm might reinvest its 2024 profits, estimated at $50 million, into new equipment rather than seeking a bank loan, thereby substituting a bank's financing function.

- Internal cash flow generation: Companies can utilize retained earnings and operating cash flow to fund projects, bypassing external financing.

- Efficient working capital management: Optimized inventory, receivables, and payables reduce the need for short-term bank credit.

- Access to capital markets: Larger firms can also tap into bond markets or equity issuance as alternatives to bank loans.

- Stronger creditworthiness: Established businesses often have better credit ratings, making internal financing or alternative capital sources more accessible and cost-effective than bank borrowing.

Financial Alternatives Challenge Traditional Banking Models

The threat of substitutes for Preferred Bank's services is multifaceted, stemming from both direct financial alternatives and evolving customer behaviors. Non-bank lenders and fintech solutions offer increasingly competitive options for businesses and individuals alike, challenging traditional banking models. For instance, the private credit market's substantial growth, with global fundraising reaching an estimated $1.5 trillion in 2023, directly competes for commercial lending business.

Customers also have readily available alternatives for managing their money, such as money market funds that yielded over 5% in early 2024, significantly outpacing typical savings accounts. Fintech platforms are streamlining payments and cash management, with the global digital payments market projected to exceed $15 trillion by 2027. Furthermore, crowdfunding and P2P lending platforms are becoming more accessible, with the P2P market valued at approximately $116.5 billion in 2023, offering alternative capital sources.

| Substitute Category | Key Players/Examples | 2023/2024 Data Point | Impact on Banks | Example of Substitution |

|---|---|---|---|---|

| Non-Bank Lending | Private Credit Funds, Direct Lending Platforms | Global private debt fundraising: ~$1.5 trillion (2023) | Diverts commercial loan demand | Business finances expansion via direct lending instead of bank loan |

| Investment Vehicles | Money Market Funds, Mutual Funds | Money market yields: >5% (Early 2024) | Pressures deposit rates, impacts profitability | Depositor moves funds from savings to MMF for higher yield |

| Fintech Solutions | Stripe, PayPal | Global digital payments market: Projected >$15 trillion by 2027 | Offers streamlined, lower-cost transaction alternatives | Company uses fintech for payroll instead of bank's service |

| Alternative Financing | Crowdfunding, P2P Lending | P2P lending market: ~$116.5 billion (2023) | Provides capital access, especially for SMEs | Startup raises capital via crowdfunding platform |

Entrants Threaten

High Regulatory and Capital Requirements

Entering the banking sector, particularly as a full-service commercial bank, presents substantial regulatory challenges. New entities must secure charters and comply with rigorous capital adequacy standards, such as those outlined in the Basel III endgame reforms. These demanding requirements, which often necessitate billions in initial capital, significantly elevate the cost and complexity of establishing a new bank, thereby limiting the threat of new entrants against established players like Preferred Bank.

Need for Trust and Brand Reputation

The banking sector, particularly for institutions like Preferred Bank, hinges on deep-seated customer trust and a strong brand reputation. Building this takes years, even decades, of consistent service and positive customer interactions. For Preferred Bank, an independent California bank, its established presence and relationship-driven model create a significant barrier for newcomers aiming to quickly win over middle-market businesses.

Established Customer Relationships and Networks

Preferred Bank's established customer relationships and extensive network, particularly its strong presence in California serving middle-market businesses, entrepreneurs, and professionals, present a significant barrier to new entrants. Building similar deep, trust-based connections requires substantial time and investment.

Technological Infrastructure and Investment

The significant capital outlay needed for a bank's technological backbone acts as a considerable barrier to entry. Building and maintaining essential systems like core banking platforms, user-friendly digital interfaces, and robust cybersecurity defenses requires massive upfront funding and continuous investment.

For instance, in 2024, major banks are projected to spend billions on digital transformation and cloud migration. This high cost of entry effectively limits the number of new players who can realistically compete in the full-service commercial banking space.

- Substantial Upfront Investment: Developing advanced core banking systems and secure digital platforms can cost hundreds of millions, if not billions, of dollars.

- Ongoing Expenditure: Continuous upgrades, maintenance, and cybersecurity enhancements represent significant recurring operational costs.

- Talent Acquisition: Attracting and retaining specialized IT talent, crucial for managing complex financial technology, adds another layer of expense.

- Regulatory Compliance: Ensuring technology meets stringent financial regulations often necessitates further investment in specialized systems and compliance personnel.

Niche Entry by Fintechs and Neobanks

While a full-scale assault on established banks like Preferred Bank is tough, the real challenge comes from nimble fintechs and neobanks. These digital natives often focus on specific services, like payments or small business loans, allowing them to operate with much lower costs.

Their specialized offerings can attract customers away from traditional banks, especially in areas where digital convenience is paramount. For instance, the global digital payments market was valued at over $2.5 trillion in 2023 and is projected to grow significantly, indicating a substantial opportunity for fintech disruptors.

- Agile Fintechs: These companies can launch new products and services rapidly, responding to market demands much faster than larger, more regulated institutions.

- Lower Overhead: Digital-only models mean reduced costs associated with physical branches, which can be passed on to customers through more competitive pricing.

- Niche Focus: By concentrating on specific customer segments or service areas, fintechs can offer superior user experiences and tailored solutions that traditional banks may struggle to match.

Banking's High Walls: Capital, Tech, and Trust Block New Entrants

The threat of new entrants in the banking sector is significantly mitigated by high capital requirements and stringent regulatory hurdles. Securing a banking charter and meeting capital adequacy ratios, like the Basel III endgame, demands billions in initial investment, making it exceptionally difficult for new players to challenge established banks like Preferred Bank. Furthermore, the need for substantial technology investment, including core banking platforms and cybersecurity, adds hundreds of millions in upfront and ongoing costs.

| Barrier | Estimated Cost Range (USD) | Impact on New Entrants |

|---|---|---|

| Regulatory Capital Requirements | Billions | Extremely High; limits number of viable entrants |

| Technology Infrastructure (Core Banking, Digital) | Hundreds of Millions to Billions | Very High; requires significant upfront and ongoing investment |

| Brand Reputation & Customer Trust | Years of investment/effort | High; difficult to replicate established relationships |

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis for Preferred Bank is built upon a foundation of comprehensive data, including the bank's annual reports, investor presentations, and regulatory filings. We also leverage industry-specific research from financial analysts and market data providers to capture the competitive landscape.