Shanghai International Port Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Shanghai International Port Bundle

Don't Miss the Bigger Picture

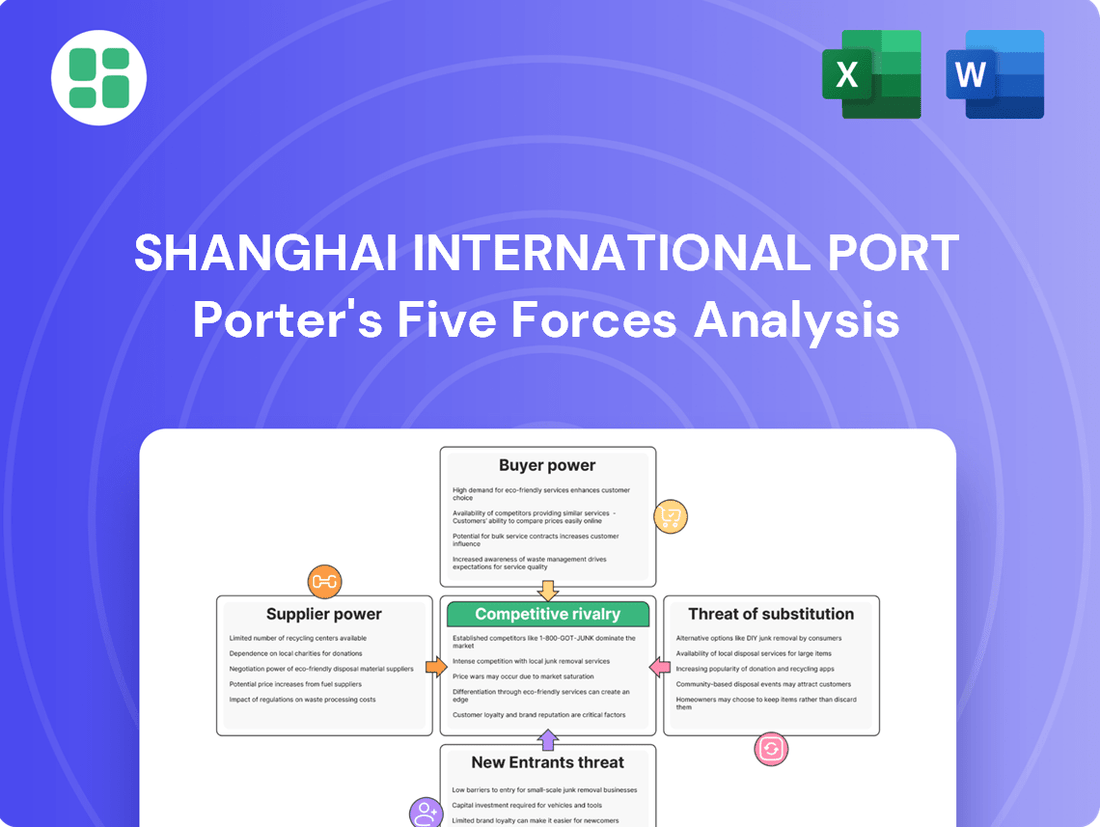

Shanghai International Port operates within a dynamic global maritime landscape, facing intense competition and significant buyer power from shipping lines. Understanding the nuances of supplier relationships and the ever-present threat of new entrants is crucial for sustained success.

The complete report reveals the real forces shaping Shanghai International Port’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Concentration of Key Suppliers

The bargaining power of suppliers for Shanghai International Port (Group) Co., Ltd. (SIPG) is significantly shaped by the concentration of specialized equipment manufacturers. Companies producing essential port machinery like large gantry cranes and advanced automated terminal systems are few globally due to the high capital investment and technical expertise needed.

This limited supplier base grants these specialized manufacturers considerable leverage when negotiating with SIPG. For instance, the development of advanced automated terminals requires highly specific technological solutions, often sourced from a handful of international providers.

However, SIPG's immense purchasing volume and its strategic long-term investment projects, such as the ongoing expansion of the Xiaoyangshan Island automated terminal, can offer some counter-leverage. In 2023, SIPG reported total assets of approximately RMB 200 billion, underscoring its significant market presence and capacity to influence supplier terms through large-scale procurement.

Uniqueness of Inputs

Suppliers of advanced port technology, such as AI, IoT, and automation systems, hold significant bargaining power. Their unique and critical inputs are vital for Shanghai International Port Group (SIPG) to remain efficient and competitive as the globe's busiest container port.

These specialized technologies are not easily replicable, giving suppliers an advantage. SIPG's commitment to smart port development and decarbonization further amplifies the importance of these unique offerings, reinforcing supplier leverage.

Switching Costs for SIPG

Switching costs for Shanghai International Port Group (SIPG) are notably high, especially concerning integrated systems and heavy machinery. When SIPG commits to specific vendors for critical port infrastructure, the expense and complexity of transitioning to a new supplier can be substantial. This includes financial investments for new equipment, potential operational downtime during the switch, and the cost of retraining staff on new technologies, all of which bolster supplier leverage.

Threat of Forward Integration by Suppliers

The threat of forward integration by suppliers for Shanghai International Port Group (SIPG) is generally low. Suppliers of port equipment or technology, such as crane manufacturers or IT solutions providers, typically do not possess the extensive capital, operational expertise, or regulatory licenses needed to run a massive port operation. Their core business remains focused on production and innovation, not the complex logistics and management of a global shipping hub.

For instance, while a company supplying advanced automated terminal systems might have significant technical knowledge, it lacks the established relationships with shipping lines, customs authorities, and the vast workforce required for efficient port management. SIPG’s substantial infrastructure investments and integrated service offerings create a high barrier to entry for such potential entrants.

Consider the capital intensity: building and maintaining a port facility like SIPG involves billions of dollars in infrastructure development and ongoing operational costs. In 2023, SIPG reported total assets exceeding ¥200 billion RMB, a scale far beyond the typical reach of equipment suppliers. This financial chasm effectively deters most suppliers from attempting to enter port operations.

- Low Capitalization of Suppliers: Most equipment and technology suppliers operate with significantly smaller capital bases compared to the multi-billion dollar investments required for port operations.

- Lack of Operational Expertise: Suppliers' core competencies lie in manufacturing or software, not in the intricate, labor-intensive, and highly regulated field of port management.

- Regulatory Hurdles: Operating a major port involves complex licensing, environmental permits, and security clearances that are difficult and time-consuming for external entities to obtain.

- Focus on Core Business: Suppliers are generally more profitable and strategically aligned by focusing on their specialized product or service offerings rather than diversifying into port operations.

Importance of SIPG to Suppliers

Shanghai International Port Group (SIPG) is the world's busiest container port, a title it has held for 15 consecutive years. This immense scale makes SIPG a highly desirable customer for its suppliers, ranging from heavy equipment manufacturers to advanced technology providers and construction firms. The sheer volume of business SIPG represents can significantly diminish the bargaining power of these suppliers.

Consider the implications for port equipment manufacturers. SIPG's ongoing modernization and expansion efforts, such as the development of automated terminals, require substantial investments in new cranes, automated guided vehicles, and other sophisticated machinery. For example, in 2023, SIPG continued its investments in smart port technologies, which necessitates a steady supply of specialized equipment. This consistent, large-scale demand gives SIPG considerable leverage when negotiating prices and terms with these suppliers, as a disruption in this business could severely impact a supplier's revenue.

Furthermore, SIPG's operational efficiency and commitment to technological advancement mean that suppliers must often meet stringent quality and performance standards. Failure to do so can result in lost contracts and a significant blow to a supplier's reputation within the industry. This dynamic reinforces SIPG's position, as suppliers are incentivized to offer competitive pricing and terms to secure and maintain their relationship with such a vital client.

- Massive Customer Base: SIPG's status as the world's busiest container port for 15 years makes it a critical client for numerous industries.

- Volume Leverage: The sheer volume of goods handled by SIPG translates into substantial orders for suppliers, granting SIPG significant negotiating power.

- Investment Dependency: SIPG's continuous investment in modernization and expansion projects creates a reliable, albeit demanding, revenue stream for its suppliers.

- Supplier Competition: The high value of SIPG contracts often attracts intense competition among suppliers, driving down prices and terms in SIPG's favor.

Shanghai Port's Supplier Influence: A Giant's Negotiation Edge

The bargaining power of suppliers for Shanghai International Port Group (SIPG) is moderated by the company's significant purchasing volume and its status as a critical customer. While specialized technology providers have leverage due to unique offerings, SIPG's scale, demonstrated by its total assets exceeding RMB 200 billion in 2023, allows for considerable negotiation power.

SIPG's consistent demand for advanced port machinery and smart technologies, driven by its commitment to modernization, creates a strong incentive for suppliers to offer competitive pricing. The sheer volume of business SIPG represents, as the world's busiest container port for 15 consecutive years, naturally attracts supplier competition, further tilting the balance in SIPG's favor.

Switching costs for critical infrastructure and integrated systems are high for SIPG, which can strengthen supplier positions. However, the threat of forward integration by suppliers is minimal due to the immense capital, operational expertise, and regulatory requirements involved in running a major port.

| Factor | Impact on SIPG | Key Considerations |

| Supplier Concentration | Moderate to High | Few global suppliers for specialized automated port equipment. |

| Switching Costs | High | Significant investment and operational disruption for changing vendors of integrated systems. |

| Forward Integration Threat | Low | Suppliers lack capital, expertise, and regulatory licenses for port operations. |

| SIPG's Purchasing Power | High | World's busiest port status, massive order volumes, and substantial assets (RMB 200 billion in 2023). |

What is included in the product

This Porter's Five Forces analysis for Shanghai International Port dissects the competitive intensity within the global port industry, examining supplier and buyer power, the threat of new entrants and substitutes, and the rivalry among existing players to understand its strategic positioning.

Instantly identify key competitive pressures and potential threats within the Shanghai International Port's ecosystem, enabling proactive strategies to mitigate risks and enhance profitability.

Customers Bargaining Power

Concentration of Customers

Shanghai International Port Group's (SIPG) customers, particularly major global shipping lines and substantial cargo owners, wield considerable bargaining power. This strength stems from their own industry consolidation and the sheer volume of goods they move through SIPG's terminals.

These large clients often manage vast international logistics networks, enabling them to negotiate favorable pricing and service conditions. For instance, a single major shipping alliance could represent a significant portion of a terminal's throughput, giving them leverage in discussions.

In 2024, the top 10 global shipping carriers controlled an estimated 85% of global container capacity, highlighting the concentrated nature of SIPG's customer base and their enhanced ability to influence service agreements and costs.

Switching Costs for Customers

While Shanghai International Port Group (SIPG) operates in a critical global trade hub, customers like shipping lines and cargo owners do encounter switching costs when considering alternative ports. These costs can involve significant logistical adjustments, reconfiguring complex supply chain networks, and the potential for operational delays during the transition. For instance, shifting routes might require renegotiating contracts with trucking companies and adjusting inventory management systems.

However, the competitive landscape in the region offers viable alternatives that temper SIPG's pricing power. Major ports such as Ningbo-Zhoushan, which handled approximately 1.3 billion tons of cargo in 2023, and Singapore, a consistently top-tier global maritime center, present readily available options. This accessibility for customers means they can more easily explore and switch to other ports if SIPG's terms become less favorable, thereby limiting the bargaining power of SIPG.

Customer Information Availability

Customers in the shipping and logistics sector, including those dealing with Shanghai International Port, benefit from a wealth of readily available market information. This includes detailed data on freight rates, port performance metrics, and the services offered by various competitors. For instance, by mid-2024, platforms tracking global shipping costs showed significant volatility, allowing shippers to pinpoint the most cost-effective routes and providers.

The rise of digital platforms and readily accessible industry reports has dramatically increased transparency. This empowers customers to easily compare different service providers, leading to more informed decisions and stronger negotiation positions. In 2024, many logistics software solutions offered real-time rate comparisons, giving customers the leverage to demand better pricing and service levels from ports like Shanghai.

Threat of Backward Integration by Customers

The threat of backward integration by customers for Shanghai International Port Group (SIPG) is generally low. While some major shipping lines, like Maersk or MSC, have made strategic investments in port terminals worldwide, the idea of them fully operating a facility as vast and complex as Shanghai Port is highly improbable.

The sheer scale of investment required is a major hurdle. For instance, building and operating a modern container terminal involves billions of dollars in infrastructure, cranes, and technology. SIPG's own capital expenditures highlight this; in 2023, the company reported significant investments in upgrading its facilities and expanding capacity, demonstrating the substantial financial commitment needed.

Furthermore, the specialized expertise and intricate regulatory landscape surrounding port operations present formidable barriers. Managing a port involves complex logistics, customs procedures, labor relations, and adherence to numerous international and domestic regulations. These factors make it exceptionally difficult for shipping companies, whose core competencies lie in vessel operation and logistics, to successfully manage an entire port infrastructure.

- Low Likelihood of Full Integration: Major shipping lines invest in terminals but rarely operate entire ports like Shanghai's.

- Massive Capital Outlay: Building and running a port requires billions, a significant deterrent for shipping companies.

- Specialized Expertise Needed: Port operations demand unique skills in logistics, customs, and labor management, distinct from shipping.

- Regulatory Complexity: Navigating diverse international and domestic port regulations is a significant barrier to entry for potential integrators.

Price Sensitivity of Customers

Customers in the global shipping industry are highly attuned to pricing, as minimizing their own operational expenses is a constant priority. This price sensitivity directly impacts port service providers like Shanghai International Port. For instance, in 2024, the average cost of shipping a 40-foot container globally saw significant fluctuations, with some routes experiencing a 15% increase compared to the previous year, prompting shippers to actively seek out ports offering more competitive rates.

The inherent competitiveness of the shipping market means that any perceived advantage in port fees can lead to a substantial shift in business. This dynamic is further exacerbated by global economic uncertainties, which compel customers to scrutinize every expenditure. In 2024, reports indicated that major shipping lines were re-evaluating their port calls based on cost-efficiency, directly influencing their bargaining power.

- Price Sensitivity: Customers prioritize cost-effectiveness in port services to optimize their own supply chain expenses.

- Competitive Landscape: The global shipping market's intense competition allows customers to leverage price as a key decision-making factor.

- Economic Uncertainty: Fluctuations in freight rates and broader economic instability in 2024 heightened customer demand for lower port service costs.

Customer Power Shapes Shanghai Port Dynamics

Customer bargaining power at Shanghai International Port is significant due to industry consolidation and the sheer volume of business large clients represent. Their ability to negotiate favorable terms is amplified by readily available market information and the presence of competitive alternatives.

Major shipping lines and cargo owners can easily compare port fees and service levels, a practice intensified by economic pressures in 2024. This transparency, facilitated by digital platforms, empowers customers to demand better pricing and service, limiting SIPG's leverage.

| Factor | Description | Impact on SIPG | 2024 Data/Trend |

|---|---|---|---|

| Customer Concentration | A few large shipping alliances dominate cargo volume. | High bargaining power for major clients. | Top 10 carriers controlled ~85% of global capacity in 2024. |

| Switching Costs | Costs associated with changing ports are moderate for large clients. | Limits SIPG's pricing power. | Logistical adjustments and supply chain reconfigurations are key considerations. |

| Availability of Alternatives | Other major regional ports offer competitive services. | Reduces SIPG's pricing leverage. | Ningbo-Zhoushan handled ~1.3 billion tons in 2023; Singapore remains a key hub. |

| Information Transparency | Easy access to market data and competitor pricing. | Strengthens customer negotiation positions. | Digital platforms in 2024 provided real-time rate comparisons. |

Preview the Actual Deliverable

Shanghai International Port Porter's Five Forces Analysis

This preview displays the complete Shanghai International Port Porter's Five Forces Analysis, offering a thorough examination of competitive forces within the industry. The document you see here is precisely what you will receive immediately after purchase, ensuring no discrepancies or missing information. You can trust that this professionally formatted analysis is ready for your immediate use and strategic planning.

Rivalry Among Competitors

Number and Size of Competitors

The global port industry, especially for container throughput, is intensely competitive. Shanghai International Port Group (SIPG) contends with formidable rivals like Singapore, Ningbo-Zhoushan, and Shenzhen, all major Asian mega-ports. These competitors are actively boosting their capacity and adopting advanced technologies.

While Shanghai consistently ranks as the world's busiest port, its competitors are not standing still. For instance, Ningbo-Zhoushan port saw a significant increase in throughput, handling over 13 million TEUs in the first half of 2024, demonstrating its aggressive expansion and investment in infrastructure.

Industry Growth Rate

The global maritime trade is expected to see continued growth, with projections suggesting an increase in the volume of goods transported by sea. For instance, the UNCTAD Review of Maritime Transport 2024 anticipates that global seaborne trade volume will grow by 2.2% in 2024, following a 1.3% increase in 2023. This expansion presents opportunities, but the growth rate isn't always sufficient to accommodate substantial new capacity, intensifying competition for market share among major ports like Shanghai International Port Porter (SIPG).

Product and Service Differentiation

While core port services like container handling are often seen as similar across operators, Shanghai International Port Group (SIPG) actively pursues differentiation. Its sheer scale, processing over 47 million TEUs in 2023, provides an undeniable advantage, attracting major shipping lines seeking efficient throughput. This scale is further amplified by significant investments in advanced automation, exemplified by the Yangshan Deep Water Port, which enhances speed and reduces operational costs.

SIPG’s strategic positioning within the economically vital Yangtze River Delta, coupled with its development of integrated logistics solutions beyond basic port services, further sets it apart. These services, including warehousing, inland transportation, and value-added processing, create a more comprehensive offering for clients, moving beyond simple cargo transfer to a more holistic supply chain partnership.

Exit Barriers

Exit barriers for Shanghai International Port Porter (SIPG) are exceptionally high. The sheer scale of investment in deep-water terminals, specialized container handling equipment, and extensive logistics networks represents a significant sunk cost. For instance, major port infrastructure projects often run into billions of dollars, making a complete divestment practically unfeasible without substantial financial write-downs.

These substantial capital commitments, coupled with long-term operating concessions and regulatory approvals, create a situation where exiting the market would be financially ruinous. This lack of easy exit intensifies the pressure on existing players like SIPG to remain competitive and manage operations efficiently, as abandoning the market is not a viable option.

- Immense Capital Investment: Ports require massive upfront capital for infrastructure and specialized machinery, creating high sunk costs.

- Long-Term Concessions: Operating agreements often span decades, locking operators into long-term commitments.

- Regulatory Hurdles: Exiting a critical infrastructure sector like port operations involves complex regulatory approvals.

- Specialized Assets: Port equipment and facilities are highly specialized and have limited alternative uses, reducing resale value.

Switching Costs for Customers

While not as substantial as those faced by SIPG's suppliers, switching costs for its customers, primarily shipping lines, do play a role in the competitive landscape. A shipping line might consider changing ports if a rival offers even slightly better pricing or improved transit times.

This necessitates that Shanghai International Port Group (SIPG) consistently focuses on operational efficiency and competitive pricing strategies to maintain its existing clientele.

- Customer Retention Focus: SIPG must actively work to retain its shipping line customers, as even moderate cost savings or efficiency gains elsewhere can incentivize a switch.

- Operational Optimization: Continuous improvement in port operations, such as reducing vessel turnaround times, directly impacts the attractiveness of SIPG to shipping companies.

- Pricing Sensitivity: While not the sole factor, pricing remains a key consideration for shipping lines, meaning SIPG needs to remain competitive in its fee structures.

Shanghai Port: Competing in Asia's High-Stakes Maritime Race

The competitive rivalry for Shanghai International Port Group (SIPG) is fierce, with major Asian ports like Singapore, Ningbo-Zhoushan, and Shenzhen constantly vying for market share. These competitors are not only expanding their capacity but also investing heavily in advanced technologies to enhance efficiency. For instance, Ningbo-Zhoushan port reported handling over 13 million TEUs in the first half of 2024, a clear indicator of its aggressive growth strategy.

SIPG's own impressive throughput of over 47 million TEUs in 2023 highlights its scale advantage, but the global maritime trade growth of 2.2% projected for 2024 means that intense competition for every percentage point of market share will persist. This environment demands continuous operational optimization and competitive pricing from SIPG to retain its crucial shipping line customers.

| Competitor | 2023 Throughput (approx. TEUs) | Key Competitive Actions |

|---|---|---|

| Ningbo-Zhoushan | ~35 million | Capacity expansion, infrastructure investment |

| Singapore | ~39 million | Technological adoption, efficiency improvements |

| Shenzhen | ~30 million | Smart port initiatives, digitalization |

SSubstitutes Threaten

Availability of Alternative Transportation Modes

The threat of direct substitutes for international maritime shipping, particularly for long-haul intercontinental cargo, remains relatively low. While air cargo provides speed, its significantly higher cost and capacity constraints limit its use to high-value, time-sensitive shipments. In 2024, air cargo rates for time-sensitive goods can be more than ten times that of sea freight, making it an impractical substitute for bulk commodities.

Relative Price-Performance of Substitutes

Air freight, while offering speed, carries a significantly higher cost per unit of cargo, making it an impractical substitute for the bulk of goods managed by Shanghai International Port Group (SIPG). For instance, in 2024, the average cost of air cargo per kilogram remained orders of magnitude higher than sea freight, rendering it viable only for extremely high-value or time-sensitive shipments.

Rail transport, though expanding its reach, particularly along Eurasian corridors, presents its own set of limitations as a substitute for maritime shipping. In 2024, while rail freight volumes increased, capacity constraints and slower transit times over very long distances, coupled with less extensive global network connectivity compared to established sea routes, still position it as a secondary option for most international trade handled by SIPG.

Customer Propensity to Substitute

Customer propensity to switch from sea freight to alternatives like air cargo or rail is generally low for bulk and containerized goods. This is primarily due to the superior cost-effectiveness and sheer capacity of ocean shipping for large volumes. For Shanghai International Port Group (SIPG), this translates to a low threat of substitutes impacting its core container handling business.

Impact of Technological Advancements on Substitutes

While technological advancements are indeed shaping alternative logistics, their impact on undermining the dominance of sea freight for Shanghai International Port remains limited. For instance, advancements in air cargo, such as the introduction of larger, more efficient aircraft, and the burgeoning potential of drone delivery for smaller, time-sensitive parcels, offer speed but cannot match the cost-effectiveness and sheer capacity of maritime transport for bulk goods. Similarly, improvements in rail freight, including faster train speeds and enhanced intermodal connectivity, are valuable but still fall short of sea freight’s global reach and volume capabilities.

Ports themselves are actively integrating new technologies to bolster their competitiveness and mitigate the threat of substitutes. Shanghai Port, for example, continues to invest in automation and digitalization. By the end of 2023, Shanghai Port achieved a significant milestone, handling over 49 million TEUs (Twenty-foot Equivalent Units), underscoring its massive scale. This operational efficiency, driven by technological adoption, further solidifies its position against potential shifts to other modes of transport.

- Air Cargo Limitations: Despite advancements like larger cargo planes, air freight remains significantly more expensive per ton-mile than sea freight, making it impractical for the majority of global trade volumes handled by Shanghai Port.

- Rail Freight Capacity: While rail offers improved speed and intermodal integration, its capacity for transcontinental bulk shipments is dwarce compared to the economies of scale provided by container ships.

- Port Technology Adoption: Shanghai Port's ongoing investment in smart port technologies, including automated terminal operations and advanced logistics management systems, enhances its efficiency and cost-competitiveness, thereby reducing the attractiveness of substitutes.

- Volume Disparity: The fundamental difference in the sheer volume and weight of goods transported by sea versus air or rail means that these alternative modes are unlikely to fundamentally erode sea freight's dominance for global trade.

Supply Chain Reconfiguration and Nearshoring

The threat of substitutes for Shanghai International Port's services is influenced by evolving global supply chain strategies. A significant indirect substitute could emerge from the trend of nearshoring and reshoring manufacturing activities. This shift might decrease the reliance on extensive, long-distance maritime transport that Shanghai Port facilitates.

However, China's entrenched position as a global manufacturing powerhouse significantly mitigates this threat. Shanghai Port's strategic importance as a nexus for international trade flows is unlikely to diminish substantially due to these supply chain reconfigurations.

- Nearshoring/Reshoring Impact: While these trends could theoretically reduce demand for long-haul shipping, China's dominant manufacturing role provides a strong counterforce.

- Shanghai's Centrality: As of 2024, China accounts for approximately 30% of global manufacturing output, underscoring Shanghai Port's continued critical function in international trade.

- Trade Volume Resilience: Despite potential shifts, Shanghai Port handled over 47 million TEUs (twenty-foot equivalent units) in 2023, demonstrating its robust and enduring position in global logistics.

Why Shanghai Port's Maritime Services Remain Indispensable

The threat of substitutes for Shanghai International Port's services, particularly for bulk and containerized cargo, remains low. While air cargo offers speed, its prohibitive cost, with rates in 2024 being over ten times that of sea freight for time-sensitive goods, makes it impractical for the vast majority of shipments. Rail transport, though growing, faces capacity and network limitations for intercontinental trade compared to established maritime routes.

Customer loyalty to sea freight is high due to its unparalleled cost-effectiveness and capacity, especially for the high volumes handled by Shanghai Port. For instance, in 2023, Shanghai Port processed over 47 million TEUs, a testament to the enduring demand for its services. Technological advancements in alternative transport modes, like larger cargo planes or faster trains, do not yet rival the scale and economic advantages of maritime shipping for global trade.

The trend of nearshoring and reshoring presents a potential indirect substitute by reducing reliance on long-haul shipping. However, China's dominant manufacturing position, accounting for roughly 30% of global output in 2024, ensures Shanghai Port's continued strategic importance. Investments in automation and digitalization by Shanghai Port further enhance its efficiency, solidifying its competitive edge against any emerging alternatives.

Entrants Threaten

Capital Requirements

The threat of new companies entering the port operating business, particularly at the scale of Shanghai International Port, is exceptionally low. This is primarily due to the immense capital required. Building and modernizing a major international port demands billions of dollars for infrastructure, land acquisition, and state-of-the-art equipment.

For instance, significant investments are continuously made in port expansion and technological upgrades. In 2023, global port infrastructure spending was projected to reach hundreds of billions, highlighting the sheer scale of financial commitment needed. This creates a formidable financial barrier that deters most potential new players.

Economies of Scale and Scope

Shanghai International Port Group (SIPG) enjoys substantial economies of scale, handling over 51 million TEUs in 2024, making it the world's busiest container port. This sheer volume allows SIPG to spread fixed costs over a vast number of units, significantly lowering its per-unit operating expenses. New entrants would find it extremely challenging to match these efficiencies.

The immense scale of operations at SIPG translates into significant cost advantages that are difficult for new players to replicate. Achieving comparable operational efficiencies and the resulting cost leadership would require massive upfront investment in infrastructure and technology, creating a high barrier to entry.

Government Policy and Regulation

The threat of new entrants for Shanghai International Port Porter (SIPG) is significantly mitigated by stringent government policies and regulations within the port industry. Globally, and particularly in China, ports are subject to extensive oversight, often with substantial government ownership or direct control. SIPG's own status as a state-owned enterprise, with a significant stake held by the Shanghai State-owned Asset Supervision and Administration Commission, underscores this reality.

Gaining the necessary permits, securing land, and demonstrating the strategic importance required to establish a new major port facility represents a formidable undertaking. This complex and protracted regulatory process erects high barriers to entry, effectively deterring potential new competitors from entering the market.

Access to Distribution Channels and Locations

New companies entering the port industry would struggle to acquire the necessary prime coastal real estate with deep-water access. Shanghai International Port Group (SIPG) already holds a commanding position, leveraging its strategic location within the economically vital Yangtze River Delta. This existing infrastructure provides a significant barrier to entry for potential competitors seeking to establish similar operational capabilities.

Furthermore, the development of comprehensive land-side distribution networks, including road, rail, and inland waterway connections, is a monumental undertaking. SIPG's established and extensive hinterland connections are critical for efficient cargo evacuation and onward distribution. Building a comparable network would require immense capital investment and time, making it a formidable hurdle for any new entrant aiming to compete effectively.

- Securing Prime Real Estate: New entrants face immense difficulty in obtaining deep-water port locations, a critical asset already secured by SIPG.

- Developing Land-Side Networks: Establishing robust road, rail, and inland waterway connections for cargo handling is a substantial capital and logistical challenge for newcomers.

- SIPG's Existing Advantage: SIPG benefits from its strategic Yangtze River Delta location and pre-existing, well-developed hinterland distribution systems.

Brand Loyalty and Switching Costs

While brand loyalty for a port might not mirror that of consumer goods, Shanghai International Port Group (SIPG) benefits from deep-seated relationships with key players in the global shipping industry. These established ties with major shipping lines, significant cargo owners, and extensive logistics networks act as a formidable barrier. New entrants face the challenge of replicating this trust and operational integration.

The inherent complexities and significant costs associated with switching port operations also deter new competition. Factors like reconfiguring supply chains, retraining staff, and investing in new infrastructure represent substantial hurdles. Customers prioritize the proven reliability and efficiency that SIPG offers, making the perceived risk of engaging with a new, unproven port operator a significant deterrent.

- Established Relationships: SIPG's long-standing partnerships with global shipping giants create a sticky customer base.

- High Switching Costs: The financial and operational burden of changing port providers discourages customers from exploring alternatives.

- Operational Complexity: The intricate nature of port logistics and supply chain integration favors incumbent operators with proven track records.

- Customer Preference for Reliability: Major cargo owners and shipping lines value the consistent performance and efficiency offered by experienced ports like SIPG.

Port Entry: A Fortress of Capital and Scale

The threat of new entrants for Shanghai International Port Group (SIPG) is extremely low, primarily due to the colossal capital investment required to establish and operate a port of this magnitude. SIPG's 2024 throughput of over 51 million TEUs demonstrates its unparalleled economies of scale, a feat nearly impossible for newcomers to replicate due to the immense fixed costs involved in infrastructure, technology, and land acquisition.

| Factor | SIPG's Position | Barrier Strength |

|---|---|---|

| Capital Requirements | Billions in infrastructure, equipment, and land | Very High |

| Economies of Scale | 51+ million TEUs handled in 2024 | Very High |

| Government Regulation & Ownership | State-owned enterprise, extensive permits needed | Very High |

| Real Estate Access | Prime Yangtze River Delta location secured | Very High |

| Hinterland Connectivity | Established road, rail, and waterway networks | Very High |

| Customer Relationships & Switching Costs | Deep ties with shipping lines, high integration costs | High |

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis for Shanghai International Port leverages data from official company disclosures, including annual reports and investor relations materials. We also incorporate insights from reputable maritime industry publications and government economic databases to provide a comprehensive view of the competitive landscape.