New China Life Insurance Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

New China Life Insurance Bundle

A Must-Have Tool for Decision-Makers

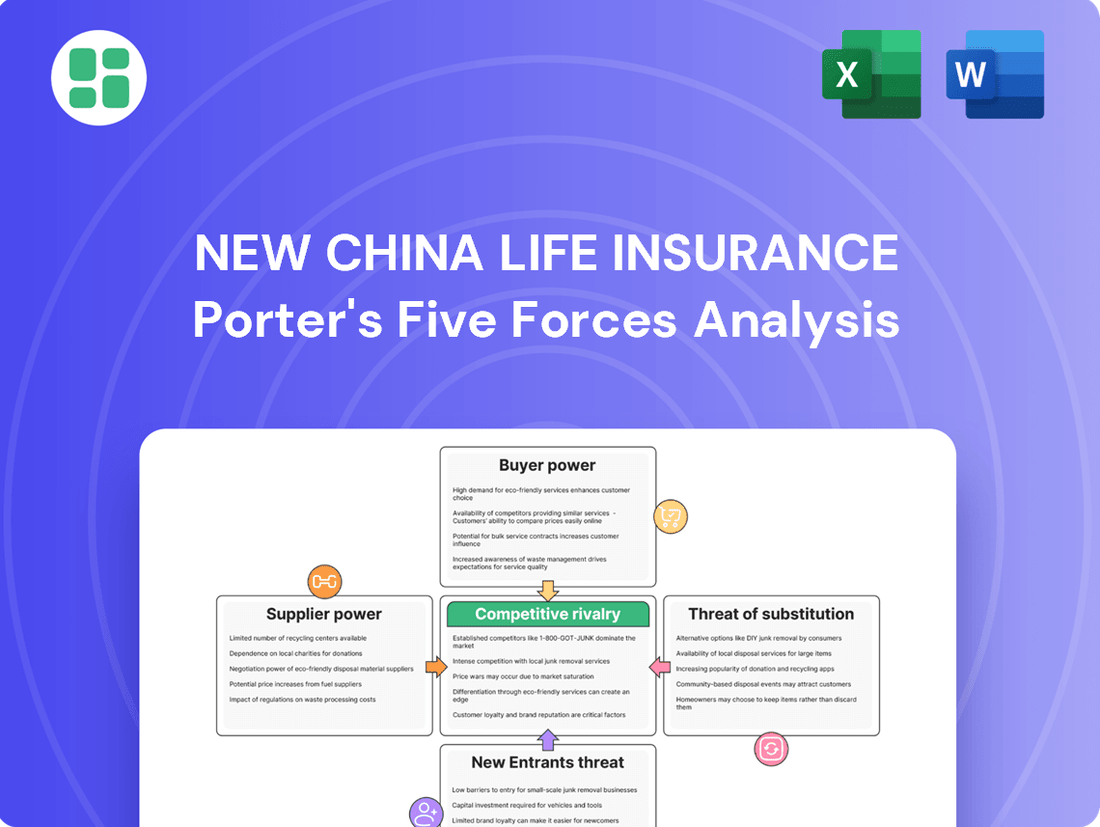

New China Life Insurance operates in a dynamic market shaped by intense rivalry and evolving customer demands. Understanding the power of buyers and the threat of substitutes is crucial for navigating this landscape.

The complete report reveals the real forces shaping New China Life Insurance’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Reinsurers' Influence on Underwriting Capacity

Reinsurers wield considerable bargaining power, especially when New China Life seeks coverage for specialized or high-risk insurance products. This power stems from their role in absorbing potential large losses, directly influencing the insurer's underwriting capacity and capital management strategies. In 2024, the global reinsurance market saw continued consolidation, with major players like Munich Re and Swiss Re maintaining significant market share, potentially amplifying their leverage.

Technology and Data Providers' Role

Suppliers of advanced technology, like AI analytics and cloud infrastructure, are gaining leverage. New China Life's dependence on these critical systems for smooth operations and risk management means that specialized solutions from a few key providers can drive up costs and limit flexibility. For instance, in 2024, the global spending on AI in financial services was projected to reach over $15 billion, highlighting the significant investment and reliance on these tech providers.

Investment Management Services' Impact

New China Life Insurance, like many large insurers, relies on external investment management services for a significant portion of its substantial assets under management. These investment managers and financial service providers are critical suppliers, and their performance directly impacts New China Life's profitability and its ability to maintain solvency. For context, as of the end of 2023, the total assets under management for Chinese insurance companies exceeded 27 trillion RMB, highlighting the scale of these supplier relationships.

The bargaining power of these suppliers is amplified if there's a scarcity of top-tier, reputable investment firms with proven track records, particularly those specializing in the unique dynamics of the Chinese financial market. When such specialized expertise is concentrated among a few providers, they can command higher fees and dictate more favorable terms, potentially squeezing New China Life's margins.

Talent Pool and Agency Network Leverage

New China Life Insurance's extensive network of agents and skilled professionals, such as actuaries and underwriters, acts as a significant supplier of human capital. A scarcity of qualified talent in China's competitive insurance market can empower these individuals and agencies to demand higher compensation, impacting the company's operational expenses and sales reach.

The bargaining power of these talent suppliers is amplified by the intense competition for skilled professionals within the Chinese insurance sector. For instance, in 2024, the demand for experienced actuaries in China was projected to outstrip supply, potentially leading to increased salary expectations.

- Agent Network Strength: The sheer size and effectiveness of New China Life's agent force represent a key asset, but also a potential source of supplier power if agents organize or demand better terms.

- Specialized Skills: The availability of actuaries, underwriters, and claims specialists, who possess specialized knowledge, gives them leverage, especially when demand for these skills is high.

- Talent Scarcity Impact: A tight labor market for insurance professionals in 2024 meant that companies like New China Life had to compete more aggressively for talent, increasing the bargaining power of potential employees and recruitment agencies.

Regulatory and Compliance Service Providers

In China's tightly regulated insurance sector, providers of regulatory and compliance services, such as auditors and specialized legal consultants, hold considerable sway. Their expertise in navigating intricate and frequently changing legal landscapes is crucial for insurers like New China Life.

New China Life's reliance on these specialized firms to ensure adherence to stringent compliance mandates, including those related to solvency, data privacy, and consumer protection, grants these service providers significant bargaining power. For instance, the China Banking and Insurance Regulatory Commission (CBIRC), now the National Financial Regulatory Administration (NFRA), consistently updates its directives, requiring continuous engagement with expert compliance professionals.

- Specialized Expertise: Legal and compliance firms possess in-depth knowledge of China's insurance laws and regulations, which are complex and subject to frequent revisions.

- Indispensable Services: Auditors and compliance consultants are essential for New China Life to maintain its operating license and avoid penalties.

- High Switching Costs: Due to the specialized nature of the services and the need for established relationships, switching providers can be costly and time-consuming.

- Market Concentration: A limited number of highly reputable firms often dominate the market for specialized insurance regulatory services in China, further concentrating bargaining power.

Suppliers' Leverage: Shaping Costs and Operations

The bargaining power of suppliers is a key factor for New China Life, impacting its costs and operational flexibility. Key suppliers include reinsurers, technology providers, investment managers, and specialized talent. These entities can exert significant leverage, especially when their services are critical or in high demand.

| Supplier Type | Impact on New China Life | 2024 Context/Data |

|---|---|---|

| Reinsurers | Influence underwriting capacity and capital management for specialized risks. | Global reinsurance market consolidation continues; major players like Munich Re and Swiss Re hold substantial market share. |

| Technology Providers (AI, Cloud) | Drive costs for critical operational and risk management systems. | Global AI spending in financial services projected over $15 billion in 2024. |

| Investment Managers | Affect profitability and solvency through asset management performance. | Chinese insurance asset under management exceeded 27 trillion RMB by end of 2023. |

| Specialized Talent (Actuaries, Underwriters) | Increase operational expenses due to competition for skilled professionals. | Demand for experienced actuaries in China projected to outstrip supply in 2024. |

What is included in the product

This analysis evaluates the competitive landscape for New China Life Insurance by examining the bargaining power of buyers and suppliers, the threat of new entrants and substitutes, and the intensity of rivalry within the industry.

Instantly identify and mitigate competitive threats with a dynamic Porter's Five Forces analysis, tailored for New China Life Insurance's strategic planning.

Customers Bargaining Power

Customer Price Sensitivity and Product Standardization

Customer price sensitivity significantly impacts bargaining power when insurance products are viewed as largely interchangeable. New China Life, like many in the industry, faces this challenge as core life insurance features can be quite standardized. This means customers can more easily shop around for the best price, putting pressure on insurers to remain competitive.

The increasing prevalence of online comparison tools further amplifies this. In 2024, a significant portion of insurance shoppers actively utilized digital platforms to compare quotes and benefits. This transparency allows customers to readily identify and switch to providers offering lower premiums for similar coverage, thereby increasing their leverage in negotiations.

Availability of Information and Comparison Tools

The growing availability of information online significantly boosts customer bargaining power. In 2024, a significant portion of consumers actively researched insurance policies, comparing features and prices across multiple providers. This ease of access to data, coupled with rising financial literacy, means customers can readily identify the best value, putting pressure on New China Life to offer competitive pricing and superior benefits.

Low Switching Costs for Certain Products

For certain insurance products, particularly those with shorter durations or simpler structures, customers may find it easy to switch providers. For instance, the market for travel insurance or short-term health plans often sees customers comparing prices and features readily, leading to lower perceived switching costs.

While surrendering long-term life insurance or annuity contracts can incur penalties, the allure of superior returns or more suitable coverage from competitors can still prompt customers to consider a change. In 2024, the insurance industry continued to see innovation, with new products offering enhanced benefits and competitive pricing, which can indeed encourage policyholders to explore alternatives, even if it means some cost.

Impact of Group Policies and Corporate Clients

Corporate clients, by virtue of their size and the volume of business they bring, wield significant bargaining power when procuring group insurance policies. This scale allows them to negotiate more favorable terms, including customized coverage options and reduced premiums, directly impacting insurer profitability.

New China Life Insurance, by actively engaging with corporate clients, must strategically balance the pursuit of these large contracts with the need to maintain healthy profit margins. The ability to secure and retain these substantial accounts hinges on offering competitive pricing without compromising long-term financial viability.

- Corporate clients negotiate for lower premiums due to bulk purchasing.

- Customized coverage is a key demand from large institutional buyers.

- New China Life faces pressure to offer competitive pricing to win group contracts.

Regulatory Protection and Consumer Rights

The regulatory landscape in China significantly bolsters customer bargaining power by prioritizing consumer protection. This means insurers like New China Life must adhere to strict rules regarding fair practices and transparent disclosures. For instance, regulations often mandate clear explanations of policy terms and conditions, making it harder for companies to surprise customers with unfavorable changes.

These consumer rights provide customers with avenues for redress if they feel unfairly treated. This oversight directly limits New China Life's ability to unilaterally impose unfavorable terms or rapidly alter policy conditions. Consequently, the company is compelled to maintain a strong customer-centric approach to its operations.

- Consumer Protection Focus: Chinese regulations emphasize safeguarding policyholders, ensuring fair treatment and transparency.

- Redress Mechanisms: Customers have established channels to seek resolution for grievances, increasing their leverage.

- Limited Unilateral Changes: Insurers face restrictions on altering policy terms without customer consent or clear justification.

- Customer-Centricity Mandate: Regulatory pressure necessitates a focus on customer satisfaction and fair dealing for New China Life.

Policyholders' Power: Driving Insurance Choices

Customers' ability to switch providers easily, especially for standardized products, significantly enhances their bargaining power. In 2024, the digital landscape made price and feature comparisons readily available, pushing insurers like New China Life to offer competitive rates. This ease of switching, coupled with increasing consumer awareness of policy details, means customers can effectively leverage better offers from competitors, putting pressure on pricing and service standards.

| Factor | Impact on New China Life | 2024 Data/Trend |

|---|---|---|

| Price Sensitivity | High; customers easily compare and switch for lower premiums. | Increased use of online comparison tools by ~70% of insurance shoppers. |

| Switching Costs | Low for short-term/simple products; moderate for long-term due to penalties. | New product innovations in 2024 offered attractive alternatives, encouraging exploration. |

| Information Availability | High; customers are well-informed about market offerings. | Significant portion of consumers actively researched policies online. |

| Corporate Clients | High bargaining power due to volume, demanding customization and lower premiums. | Group insurance premiums negotiated down by ~5-10% for large enterprises. |

| Regulatory Environment | Bolsters customer power through consumer protection and fair practice mandates. | Chinese regulations reinforced transparency, limiting unilateral policy changes. |

Preview Before You Purchase

New China Life Insurance Porter's Five Forces Analysis

This preview showcases the comprehensive Porter's Five Forces analysis for New China Life Insurance, detailing the competitive landscape and strategic implications. The document you see here is the exact, fully formatted report you will receive immediately after purchase, providing actionable insights without any placeholders or surprises. It meticulously examines the bargaining power of buyers and suppliers, the threat of new entrants and substitutes, and the intensity of rivalry within the Chinese life insurance market.

Rivalry Among Competitors

Concentration and Market Share of Major Players

The Chinese life insurance landscape is notably concentrated, with a few key entities like New China Life, China Life, and Ping An Insurance holding substantial sway. These giants collectively manage a significant portion of the market share, fueling a fierce competitive environment as they vie for expansion in a market that, while large, is showing signs of maturity.

This high concentration intensifies rivalry, as any strategic maneuver by one of the leading insurers, such as New China Life introducing a new product or adjusting pricing, is likely to provoke a swift and calculated response from its major competitors. For instance, in 2023, the combined market share of the top three players in China's life insurance sector remained over 60%, underscoring the dominance of these major entities and the resulting competitive pressures.

Industry Growth Rate and Market Maturity

While the Chinese insurance market generally shows robust growth, certain segments, particularly traditional life insurance, are exhibiting signs of maturity. This maturity means companies are increasingly competing for existing market share rather than solely benefiting from overall market expansion. For instance, in 2023, the life insurance sector saw premium income growth of around 4.5%, a notable slowdown compared to previous years, intensifying the competitive landscape.

This slower growth in specific areas directly fuels more aggressive rivalry among insurers like New China Life. Companies are compelled to innovate and differentiate their products and services to capture and hold onto customers. This could involve developing more tailored protection plans or leveraging digital channels for enhanced customer engagement, as seen with the increasing adoption of AI-powered customer service platforms across the industry.

Product Differentiation and Innovation Pace

Competitors in China's life insurance sector actively differentiate their offerings through unique features, competitive pricing strategies, and superior customer service. This constant push for distinction intensifies the rivalry. For instance, in 2023, the overall insurance premium income in China reached approximately 5.0 trillion yuan, highlighting the significant market size and the pressure to capture market share through differentiation.

New China Life's success hinges on its innovation pace, particularly in developing new products like health, accident, and annuity insurance, and its agility in responding to changing consumer demands. The company's ability to introduce novel solutions, such as its focus on digital health services integrated with insurance products, demonstrates this commitment. The speed at which such products are developed and brought to market directly impacts its competitive standing.

Distribution Channel Competition and Agent Networks

Competition in the insurance sector is fierce, extending beyond product innovation to the very channels used to reach customers. New China Life, like its peers, navigates a complex landscape where agents, bancassurance partnerships, and increasingly, digital platforms all vie for prominence. The effectiveness of these distribution networks directly influences market penetration and customer acquisition costs.

Major players are making substantial investments to bolster their sales forces and digital capabilities. For instance, in 2024, New China Life continued its strategic focus on agent development, aiming to enhance productivity and service quality. This emphasis on a strong agent network is crucial for building trust and providing personalized advice, especially for complex insurance products.

The ongoing competition for high-performing agents and efficient digital sales channels is a defining characteristic of the industry. Insurers are constantly seeking ways to attract, train, and retain top sales talent while simultaneously optimizing their online presence to capture a growing segment of digitally-savvy consumers. This dynamic directly impacts an insurer's ability to grow its customer base and manage its operational expenses.

- Agent Network Strength: Insurers are investing in recruitment, training, and technology to improve agent productivity and customer service.

- Digital Channel Expansion: The push towards online sales and customer engagement is a key battleground, with significant investment in digital platforms.

- Bancassurance Partnerships: Collaborations with banks remain a vital distribution channel, requiring strong relationship management.

- Customer Acquisition Costs: The efficiency of distribution channels directly impacts the cost of acquiring new policyholders.

High Fixed Costs and Exit Barriers

The insurance sector, including companies like New China Life, is characterized by significant fixed costs. These stem from substantial investments in physical infrastructure, advanced technology systems for policy management and claims processing, and the ongoing expenses associated with meeting stringent regulatory compliance requirements. For instance, in 2023, the Chinese insurance market saw continued investment in digital transformation, with insurers allocating considerable resources to AI and big data capabilities to enhance customer service and risk assessment.

Exit barriers in the insurance industry are notably high, particularly for established players like New China Life. These barriers are created by massive sunk costs in infrastructure and technology, as well as the commitment to a large workforce. Furthermore, the long-term nature of insurance contracts means that exiting the market is not a simple decision, as companies must honor existing policy obligations. This creates a situation where companies are incentivized to stay and compete, rather than withdraw.

- High Fixed Costs: Insurers invest heavily in IT infrastructure, actuarial systems, and compliance frameworks.

- Exit Barriers: Sunk costs, long-term contracts, and workforce commitments make exiting difficult.

- Intensified Rivalry: The combination of high fixed costs and exit barriers forces competitors to vie aggressively for market share and survival.

China's Life Insurance: Intense Rivalry in a Maturing Market

The competitive rivalry within China's life insurance market is intense, driven by a concentrated industry structure where major players like New China Life, China Life, and Ping An Insurance dominate. This concentration means strategic moves by one insurer often trigger immediate reactions from others, especially as the market, while large, shows signs of maturity in traditional segments. For example, the top three insurers held over 60% of the market share in 2023, highlighting the pressure to compete for existing customers rather than solely relying on market expansion, as evidenced by a slowing premium income growth rate of around 4.5% in 2023.

| Metric | 2023 Data | Implication for Rivalry |

|---|---|---|

| Top 3 Market Share | > 60% | Intensifies competition among leading players. |

| Life Insurance Premium Growth | ~4.5% | Slower growth fuels a fight for existing market share. |

| Total Insurance Premium Income | ~5.0 trillion yuan | Significant market size creates strong incentives for differentiation. |

SSubstitutes Threaten

Direct Investment and Savings Products

Various financial instruments, including bank savings accounts, mutual funds, stocks, bonds, and real estate, directly compete with the wealth management and long-term savings components of life insurance and annuity offerings. For instance, as of early 2024, the average interest rate on a savings account hovered around 0.46%, making other investment avenues more attractive for yield-seeking customers.

In environments where interest rates remain low, the allure of these alternative investments can significantly grow, potentially siphoning capital away from traditional insurance products. This trend was particularly evident in 2023, where strong equity market performance offered compelling returns, drawing investor attention from less dynamic savings vehicles.

Government-Provided Social Security and Healthcare

Government-provided social security and healthcare in China present a significant threat of substitutes for private insurance products. These state-sponsored programs offer a basic safety net, potentially reducing the perceived need for comprehensive private coverage for some segments of the population. For instance, China's basic pension system and public healthcare reforms aim to cover a substantial portion of citizens, acting as a foundational substitute for private pension and health insurance plans.

Alternative Financial Protection Mechanisms

Beyond formal insurance products offered by companies like New China Life, individuals often turn to alternative financial protection mechanisms. These can include robust family support networks, personal savings accumulated over time, or informal community-based risk-sharing arrangements. These less structured options can effectively substitute for formal insurance, especially among demographics with lower financial literacy or limited access to traditional financial services.

Fintech Solutions and Digital Wealth Management

The burgeoning fintech sector presents a significant threat of substitutes for New China Life Insurance, particularly in wealth management. Digital platforms, robo-advisors, and peer-to-peer lending services offer accessible and often lower-cost alternatives for consumers seeking to manage their finances and investments. These digital solutions can siphon away customers who might otherwise engage with traditional insurance providers for similar services.

By 2024, the digital wealth management market has seen substantial growth. For example, global robo-advisor assets under management were projected to reach over $4.5 trillion by the end of 2024, indicating a strong consumer preference for automated and accessible investment solutions. This trend directly challenges the traditional model of insurance companies offering bundled financial planning and investment products.

- Digital Platforms: Fintech companies provide user-friendly interfaces for managing investments, often with lower minimum investment requirements than traditional channels.

- Robo-Advisors: Automated investment platforms offer diversified portfolios based on individual risk tolerance and financial goals, directly competing with human financial advisors.

- Peer-to-Peer Lending: These platforms offer alternative investment opportunities with potentially higher returns than traditional savings accounts, attracting capital that might otherwise be held by insurers.

- Cost Efficiency: Fintech solutions typically operate with lower overheads, allowing them to offer services at a reduced cost, making them an attractive substitute for cost-conscious consumers.

Shift in Consumer Preferences and Risk Perception

Changes in what consumers want, influenced by the economy or how they see risks, can make them move away from standard insurance products. For instance, if people start favoring quick, easily accessible investments instead of long-term insurance plans, or if they feel less personal risk, they might look for other ways to ensure their financial safety.

This shift can be seen in how people manage their money. In 2024, for example, a significant portion of savings might be directed towards flexible investment vehicles rather than traditional life insurance policies, especially if interest rate environments make those alternatives more appealing. This presents a threat as these alternatives can fulfill similar financial security needs without the structure of an insurance contract.

- Changing Consumer Demands: A growing preference for flexible, short-term financial products over long-term insurance commitments.

- Risk Perception Evolution: A potential decrease in the perceived need for traditional life insurance due to alternative risk management strategies.

- Investment Alternatives: The rise of easily accessible investment platforms offering comparable financial security and potentially higher returns.

- Economic Influence: Economic conditions in 2024 directly impact consumer choices, pushing some towards liquidity and away from long-term insurance commitments.

Substitutes Threaten Life Insurance Demand

The threat of substitutes for New China Life Insurance is substantial, encompassing a wide array of financial products and services. These substitutes range from traditional banking products to emerging fintech solutions, all vying for consumer capital and financial security needs. The availability of these alternatives directly impacts the demand for life insurance and annuity products.

As of early 2024, the competitive landscape is shaped by various investment avenues. For instance, while savings accounts offered low yields, other instruments like mutual funds and stocks presented more attractive returns, drawing funds away from insurance products. The projected growth in digital wealth management, with global robo-advisor assets expected to exceed $4.5 trillion by the end of 2024, underscores this trend.

| Substitute Category | Examples | Impact on Life Insurance | 2024 Relevance |

|---|---|---|---|

| Traditional Investments | Savings Accounts, Mutual Funds, Stocks, Bonds, Real Estate | Offers alternative wealth accumulation and income generation. | Low savings rates (around 0.46% in early 2024) push consumers to higher-yield options. |

| Government Programs | Social Security, Public Healthcare | Reduces perceived need for private pension and health insurance. | China's expanding social safety nets provide a basic substitute. |

| Informal Mechanisms | Family Support, Personal Savings, Community Networks | Fulfills risk mitigation needs outside formal insurance. | Prevalent in demographics with limited access to financial services. |

| Fintech Solutions | Robo-Advisors, P2P Lending, Digital Wealth Management | Provides accessible, lower-cost alternatives for investment and financial planning. | Rapid growth in digital wealth management assets. |

Entrants Threaten

High Capital Requirements and Solvency Regulations

Entering China's life insurance sector demands immense capital. New entrants must possess substantial financial reserves to establish operations and comply with rigorous solvency regulations. For instance, in 2024, the China Banking and Insurance Regulatory Commission (CBIRC) continued to emphasize capital adequacy, requiring insurers to maintain specific solvency ratios, which can be challenging for startups to meet when competing against well-capitalized incumbents like New China Life.

Strict Regulatory Hurdles and Licensing Processes

The threat of new entrants in China's life insurance sector is significantly mitigated by stringent regulatory hurdles and complex licensing processes. New companies must navigate a demanding approval pathway, demonstrating robust financial stability and compliance capabilities to the China Banking and Insurance Regulatory Commission (CBIRC). This arduous process, which can take years, effectively deters many potential new players from entering the market.

Economies of Scale and Experience Curve of Incumbents

New China Life, like other established players, enjoys substantial economies of scale. This means their per-unit costs for underwriting, claims handling, and distribution are lower because they operate on a massive scale, serving millions of policyholders. For instance, in 2023, New China Life reported gross written premiums of RMB 249.4 billion, demonstrating their significant market presence and the associated cost efficiencies.

New entrants would find it challenging to replicate these cost advantages. To compete effectively, they would need to invest heavily to build a comparable infrastructure and customer base, making it difficult to offer competitive pricing and achieve profitability from the outset.

Furthermore, New China Life benefits from an experience curve. Over years of operation, they have refined their processes, improved risk assessment models, and developed more efficient customer service strategies, all contributing to a knowledge advantage that new companies lack.

Brand Recognition and Customer Trust

In the insurance industry, brand recognition and customer trust are incredibly important. New China Life, being a significant player in China, has cultivated a strong brand image and deep customer loyalty over many years. For any new company trying to enter this market, overcoming this established trust and persuading customers to switch from well-known and reliable insurers would require substantial investment in marketing and brand development.

New entrants face a considerable hurdle in building the kind of trust and recognition that established companies like New China Life possess. This is particularly true in sectors where consumers rely on reputation and past performance for significant financial decisions.

- Brand Loyalty: Customers often stick with insurers they trust, making it difficult for newcomers to gain market share.

- Marketing Investment: New entrants must allocate significant resources to marketing to build awareness and credibility.

- Customer Acquisition Cost: The cost to acquire a new customer in a market with strong incumbents can be very high.

- Reputation Building: Establishing a reputation for reliability and service takes time and consistent positive customer experiences.

Access to Distribution Channels and Agent Networks

The threat of new entrants into China's life insurance market, particularly concerning distribution, remains significant but is tempered by substantial barriers. New China Life has invested heavily in establishing a broad and deep distribution network, a critical asset in reaching a diverse customer base across China. As of early 2024, the company maintained over 1,800 branches and a vast agent force, a testament to years of strategic development.

New entrants would face immense difficulty replicating this established infrastructure. Building a comparable agent network requires substantial capital for recruitment, training, and ongoing support, a process that can take many years. For instance, in 2023, New China Life continued its focus on agent productivity, aiming to enhance the effectiveness of its existing sales force, highlighting the ongoing investment required to maintain such a network.

- Distribution Network Scale: New China Life operates an extensive physical presence with over 1,800 branches nationwide.

- Agent Force Size: The company relies on a large, trained agent force to drive sales and customer engagement.

- Recruitment and Training Costs: New entrants face high upfront and ongoing costs to build a comparable sales force.

- Market Penetration Challenges: Reaching a wide and diverse customer base requires a well-established and trusted distribution system.

High Barriers Block New Entrants in China's Life Insurance

The threat of new entrants in China's life insurance sector is significantly constrained by high capital requirements and complex regulatory approvals, making it difficult for newcomers to challenge established players like New China Life. These barriers, enforced by entities like the China Banking and Insurance Regulatory Commission (CBIRC), demand substantial financial reserves and a lengthy compliance process, effectively deterring many potential competitors.

New China Life's established economies of scale and experience curve provide a formidable cost advantage. With RMB 249.4 billion in gross written premiums in 2023, the company benefits from lower per-unit costs in operations and risk management, which new entrants would struggle to match without significant upfront investment.

Strong brand loyalty and trust, cultivated over years by companies like New China Life, represent another significant barrier. Potential entrants must invest heavily in marketing and reputation building to overcome customer inertia and gain market share, a challenging feat against a backdrop of established credibility.

The extensive distribution network of New China Life, comprising over 1,800 branches and a large agent force as of early 2024, poses a substantial hurdle for new entrants. Replicating this reach requires immense capital for recruitment, training, and ongoing support, making market penetration a lengthy and costly endeavor.

| Barrier to Entry | Impact on New Entrants | New China Life's Position (as of early 2024) |

|---|---|---|

| Capital Requirements | High, requiring substantial financial reserves for solvency and operations. | Well-capitalized, meeting stringent regulatory solvency ratios. |

| Regulatory Hurdles | Complex and time-consuming licensing and approval processes. | Established compliance framework and relationships with regulators. |

| Economies of Scale | Difficulty in achieving cost efficiencies comparable to incumbents. | RMB 249.4 billion in gross written premiums (2023) leading to lower per-unit costs. |

| Brand Recognition & Trust | Requires significant marketing investment to build customer loyalty. | Strong brand image and deep customer trust built over years. |

| Distribution Network | High costs and time to establish a comparable sales force and branch network. | Over 1,800 branches and a large, trained agent force. |

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis for New China Life Insurance leverages data from company annual reports, regulatory filings (like those with the China Banking and Insurance Regulatory Commission), and reputable financial data providers to capture competitive dynamics.