Guangxi Nanning Waterworks Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Guangxi Nanning Waterworks Bundle

Don't Miss the Bigger Picture

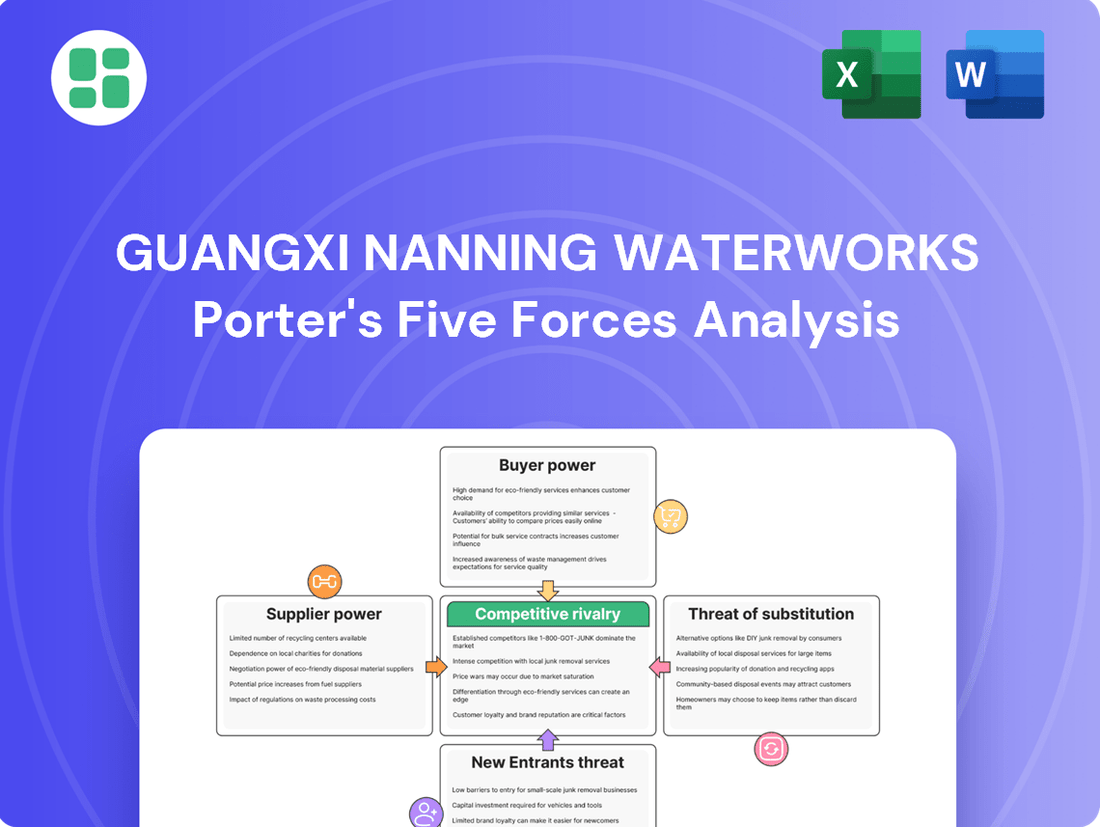

Guangxi Nanning Waterworks faces a dynamic competitive landscape, with understanding the intensity of rivalry and the threat of new entrants being crucial for strategic planning. The bargaining power of buyers and suppliers also significantly shapes its operational environment. This brief snapshot only scratches the surface.

Unlock the full Porter's Five Forces Analysis to explore Guangxi Nanning Waterworks’s competitive dynamics, market pressures, and strategic advantages in detail, revealing the real forces shaping its industry.

Suppliers Bargaining Power

Limited Raw Water Source Alternatives

Guangxi Nanning Waterworks' reliance on specific natural water sources, like rivers and reservoirs within the Nanning region, means these sources are geographically fixed and heavily influenced by government allocation and environmental rules. This dependence grants local water resource authorities substantial influence over supply, quality, and pricing.

The company possesses very limited ability to shift to alternative raw water suppliers because water sources are a natural monopoly. For instance, in 2023, Nanning's water supply primarily came from the Yongjiang River, with limited diversification options available.

Specialized Equipment and Technology Suppliers

Suppliers of specialized equipment like advanced water treatment chemicals, pumps, and filtration systems hold some sway due to the unique nature or scarcity of their technology. For instance, proprietary smart water management components can be difficult to substitute.

China's push to boost its environmental equipment manufacturing aims for self-sufficiency by 2030, which could broaden the supplier base and dilute individual supplier power over time. However, for the most advanced technologies, the cost and complexity of switching suppliers remain significant barriers.

The critical importance of input quality and reliability for public health and operational continuity means that Guangxi Nanning Waterworks may face considerable supplier leverage, especially when adopting cutting-edge solutions.

Infrastructure Material and Construction Service Providers

Suppliers of essential infrastructure materials like large-diameter pipes and valves for waterworks projects hold moderate bargaining power. This power is shaped by the substantial national investment in water conservancy and urban infrastructure. For instance, China's commitment of a record 1.35 trillion yuan to water conservancy facilities in 2024 underscores the high demand for these components.

While the market features numerous suppliers, the stringent quality standards and massive quantities required for public utility projects can empower key providers. However, Guangxi Nanning Waterworks' significant scale likely enables it to leverage bulk purchasing, thereby mitigating some of this supplier influence.

Labor and Specialized Expertise Suppliers

Specialized engineering firms, construction contractors, and highly skilled labor are key suppliers for Nanning Waterworks. Their bargaining power hinges on the scarcity of their unique skills. The push for modernizing water infrastructure, including smart systems, amplifies the influence of these niche service providers.

For instance, the global water infrastructure market was valued at approximately $800 billion in 2024 and is projected to grow. Within this, the demand for specialized engineering and construction services for advanced water treatment and smart grid technologies is particularly strong. This demand can give suppliers significant leverage.

- Scarcity of Expertise: The availability of highly specialized engineers and technicians for advanced water systems is limited, increasing their bargaining power.

- Infrastructure Modernization: Ongoing projects to upgrade water networks with smart technologies require niche skills, giving these suppliers more influence.

- Development of Local Talent: Initiatives like international training bases for water conservancy in Guangxi aim to build local expertise, which could potentially reduce reliance on external specialized suppliers and moderate their bargaining power in the long term.

Regulatory and Environmental Compliance Service Providers

Regulatory and environmental compliance service providers hold significant bargaining power for Guangxi Nanning Waterworks. The increasing stringency of environmental regulations in China, particularly concerning water management, necessitates specialized monitoring equipment, testing, and disposal services. China's introduction of its first national water conservation regulations in 2024 underscores the critical need for adherence.

- Mandatory Compliance: Adherence to new environmental laws is non-negotiable, making these services essential for avoiding penalties.

- Specialized Expertise: Certified providers offer unique skills and equipment not readily available internally.

- Limited Supplier Options: The need for certified and specialized services can limit the number of viable suppliers.

- Increased Demand: Growing environmental awareness and stricter enforcement drive demand for these critical services.

Water Utility Supplier Power: Navigating High Demand

Guangxi Nanning Waterworks faces moderate bargaining power from suppliers of essential infrastructure materials like pipes and valves. This power is influenced by significant national investment in water conservancy, with China allocating a record 1.35 trillion yuan to such facilities in 2024, driving high demand for these components. While many suppliers exist, the stringent quality and volume requirements for public utilities can empower key providers, though Nanning Waterworks' scale allows for bulk purchasing to mitigate this influence.

| Supplier Type | Bargaining Power Factor | Impact on Nanning Waterworks | Relevant Data (2024) |

|---|---|---|---|

| Natural Water Sources | Monopoly/Government Control | High; limited substitution options | Yongjiang River primary source |

| Specialized Equipment | Proprietary Technology/Scarcity | Moderate to High; switching costs are significant | Global water infrastructure market ~$800 billion |

| Infrastructure Materials | High Demand/Stringent Standards | Moderate; mitigated by bulk purchasing | China water conservancy investment: 1.35 trillion yuan |

| Specialized Services (Engineering/Labor) | Scarcity of Niche Skills | Moderate to High; amplified by modernization | Strong demand for smart water tech services |

| Regulatory Compliance | Mandatory Adherence/Limited Options | High; essential for avoiding penalties | First national water conservation regulations introduced |

What is included in the product

This analysis dissects the competitive forces impacting Guangxi Nanning Waterworks, revealing the intensity of rivalry, buyer and supplier power, threat of new entrants, and the availability of substitutes.

Instantly visualize competitive pressures with a dynamic, interactive dashboard, enabling Nanning Waterworks to proactively address threats and capitalize on opportunities.

Customers Bargaining Power

Fragmented Residential Customer Base

The bargaining power of customers for Guangxi Nanning Waterworks is extremely low, primarily due to the fragmented nature of its residential customer base. Individual households have little to no leverage to negotiate prices or terms.

This weakness in customer bargaining power stems from the essential nature of tap water, a necessity that cannot be substituted. Furthermore, Nanning operates under a monopolistic supply structure for water, meaning customers have no alternative providers to turn to, reinforcing the waterworks' dominant position.

Consequently, residential customers are unable to switch suppliers or influence pricing, which is typically determined by regulatory bodies rather than market negotiations. This lack of choice significantly diminishes any potential for customers to exert bargaining power.

Regulated Pricing Mechanism and Water Tax

In China, water tariffs for residential and commercial consumers are typically set by government bodies, not through direct negotiation with customers. This regulatory control significantly curtails the bargaining power of individual users.

The introduction of a nationwide water tax, replacing water resource fees from December 2024, further consolidates pricing authority at the governmental level. This move centralizes control and diminishes any potential for customers to influence pricing.

This regulatory framework prioritizes affordability and the provision of essential public services, thereby acting as a strong deterrent against customers exerting significant bargaining power over water pricing.

High Switching Costs for Customers

Customers face extremely high, if not impossible, switching costs for tap water services. They cannot simply opt for another water utility provider within the same service area, effectively making their customer base captive.

This lack of alternative providers significantly diminishes any potential customer leverage, reinforcing Guangxi Nanning Waterworks' strong market position. In 2023, the average household in Nanning spent approximately ¥150 per month on water, a cost unlikely to be significantly altered by switching providers, given the infrastructure dependency.

Limited Alternative Water Sources for Daily Use

Customers in Nanning have very limited alternatives for essential water needs, significantly weakening their bargaining power. While bottled water is available, it's primarily a substitute for drinking water and is neither practical nor cost-effective for the vast majority of household uses like sanitation, cooking, or cleaning.

This lack of readily available, large-scale substitutes for piped water across most applications means customers are largely dependent on Guangxi Nanning Waterworks. This dependency directly translates to lower bargaining power, as switching to alternatives for daily water consumption is generally not feasible or economical.

- Limited Substitutes: Bottled water is a poor substitute for general household and industrial water use due to cost and volume limitations.

- High Switching Costs: For most users, there are no practical alternatives to piped water, making switching costs effectively infinite for essential needs.

- Essential Service: Water is a non-discretionary good, meaning customers have little room to negotiate on price or quality when their basic needs are at stake.

Some Leverage for Large Industrial/Commercial Users

Large industrial or commercial users in Nanning might have some limited leverage with Guangxi Nanning Waterworks. This is particularly true if their businesses are significant contributors to the local economy or if they are major consumers of water. For instance, a large manufacturing plant that uses substantial amounts of water could potentially negotiate more favorable service level agreements.

However, this bargaining power is inherently constrained. The water utility sector is typically heavily regulated, which caps pricing and service adjustments. Furthermore, for large-scale users, readily available alternative suppliers of water are scarce, meaning they often lack the direct competitive options that would typically empower customers. Therefore, any influence they exert usually manifests in negotiated service terms rather than direct price reductions.

- Limited Price Influence: While large users might negotiate service level agreements, direct price concessions are unlikely due to regulatory oversight.

- Economic Significance: Key industrial players might leverage their economic importance to the Nanning region to gain consideration in service discussions.

- Lack of Alternatives: The absence of widespread alternative water suppliers significantly diminishes the direct bargaining power of even large consumers.

Nanning Water: Customer Power Dries Up

The bargaining power of customers for Guangxi Nanning Waterworks is exceptionally low, largely due to the essential, non-discretionary nature of water. Residential customers, comprising the vast majority, have virtually no ability to negotiate prices or terms, especially given the monopolistic supply structure in Nanning. While large industrial users might possess some limited leverage, their influence is significantly curtailed by heavy regulation and the scarcity of alternative water providers.

In 2023, the average monthly water expenditure for a Nanning household was approximately ¥150, a relatively small portion of overall expenses, further reducing the incentive or capacity for negotiation. The regulatory environment, including the nationwide water tax effective from December 2024, centralizes pricing authority, reinforcing the waterworks' dominant position and minimizing customer impact on tariffs.

Switching costs for tap water are prohibitively high for all customer segments, as there are no viable alternatives for the scale and type of water usage required for daily life and most industrial processes. This dependency makes customers effectively captive, unable to exert meaningful pressure on Guangxi Nanning Waterworks.

| Customer Segment | Bargaining Power Level | Key Factors Influencing Power |

|---|---|---|

| Residential Customers | Extremely Low | Fragmented base, essential service, no substitutes, high switching costs, monopolistic supply. |

| Industrial/Commercial Customers (Large) | Low to Moderate (Limited) | Significant water consumption, potential economic importance, but constrained by regulation and lack of alternatives. |

| Industrial/Commercial Customers (Small) | Very Low | Limited consumption volume, minimal economic impact, similar constraints to residential customers. |

Preview the Actual Deliverable

Guangxi Nanning Waterworks Porter's Five Forces Analysis

This preview shows the exact, comprehensive Guangxi Nanning Waterworks Porter's Five Forces Analysis you'll receive immediately after purchase, offering a detailed examination of competitive forces. You'll gain access to the full, professionally formatted document, providing actionable insights into the industry's structure and potential profitability. No surprises, no placeholders—just the complete analysis ready for your strategic planning.

Rivalry Among Competitors

Natural Monopoly in Tap Water Supply

The competitive rivalry for tap water supply in Nanning is extremely low, as Guangxi Nanning Waterworks operates as a natural monopoly. This means the company is likely the only licensed provider of tap water within its service territory, effectively eliminating direct competition for its core business of water production and distribution.

Limited Direct Competition in Sewage Treatment

While other licensed entities might offer sewage treatment, the market in China, especially for essential public services like those provided by Guangxi Nanning Waterworks, is typically characterized by strict regulation and geographical concessions. This structure significantly limits direct competition within specific service areas.

The Chinese sewage treatment facilities market saw a growth of 5.3% in 2024, signaling an expanding but highly controlled sector. This regulatory environment means that direct rivalry for the same concession area is usually minimal, as these services are often awarded on an exclusive or semi-exclusive basis.

Potential for Competition in Infrastructure Projects

The construction and operation of water infrastructure, especially new developments, often involve competitive bidding. Various construction and engineering firms vie for these project awards. This means that for securing new contracts, Guangxi Nanning Waterworks could face competition from other specialized companies.

China's commitment of 800 billion yuan for key national projects in 2025, including water conservancy, highlights a significant market for infrastructure development. While this funding creates opportunities, it also implies a potentially competitive landscape for companies seeking to win these construction contracts.

It's important to note that this competition is primarily for the awarding of construction and development phases. Once a water supply and drainage utility is established and operational, the competitive rivalry for the ongoing service provision itself is generally much lower due to the nature of regulated monopolies.

Absence of Price-Based Rivalry

For Guangxi Nanning Waterworks, the intensity of competitive rivalry is significantly dampened by the absence of price-based competition. This is because water tariffs are government-regulated, ensuring that pricing is not a battleground for market share. Instead, tariffs are established to guarantee public service delivery and facilitate cost recovery for essential infrastructure.

This regulatory environment means Guangxi Nanning Waterworks does not engage in price wars with other water utilities. The focus shifts away from competing on cost and towards operational efficiency, service quality, and infrastructure reliability. For instance, in 2024, water prices in many regulated utility sectors remained stable, reflecting these governmental controls rather than market dynamics.

- Regulated Tariffs: Water prices are set by government bodies, removing price as a competitive tool.

- Public Service Focus: Pricing aims for cost recovery and service provision, not market dominance.

- Reduced Price Wars: The company is shielded from the price-cutting tactics common in less regulated industries.

- Operational Efficiency as Key: Competition is indirect, emphasizing service quality and infrastructure upkeep.

Focus on Service Quality and Efficiency

For a utility like Guangxi Nanning Waterworks, competitive rivalry isn't about aggressive market share grabs. Instead, it centers on delivering superior service quality and operational efficiency. This pressure comes from meeting stringent regulatory demands and customer expectations for reliable, clean water. Nanning's commitment to infrastructure upgrades, with significant investments in 2024 aimed at enhancing reliability and water purity, exemplifies this internal competitive drive.

The focus is on continuous improvement rather than direct confrontation with other water providers. This internal competition drives innovation in water treatment processes and distribution network management.

- Service Quality: Emphasis on meeting and exceeding customer expectations for water purity and supply consistency.

- Operational Efficiency: Driving down costs through optimized treatment, reduced leakage, and streamlined operations.

- Regulatory Compliance: Adhering to and often surpassing national and local water quality and environmental standards.

- Infrastructure Investment: Ongoing upgrades to ensure a resilient and efficient water supply network.

Natural Monopoly: Efficiency Drives Water Utility

Competitive rivalry for Guangxi Nanning Waterworks is minimal due to its natural monopoly status in tap water supply. While construction contracts for water infrastructure may see competition from engineering firms, the core service provision is largely uncontested. Government-regulated tariffs prevent price wars, shifting the competitive focus to operational efficiency and service quality. Nanning's infrastructure investments in 2024, totaling an undisclosed but significant amount for upgrades, highlight this internal drive for better performance.

| Factor | Assessment | Supporting Data/Reasoning |

|---|---|---|

| Direct Competitors (Tap Water) | Extremely Low | Natural monopoly status, exclusive concessions. |

| Indirect Competitors (Related Services) | Low to Moderate | Competition in sewage treatment market growth (5.3% in 2024) but within a regulated sector. |

| Competition for Contracts | Moderate | Bidding for infrastructure projects, with China allocating 800 billion yuan for national projects in 2025. |

| Price Competition | None | Government-regulated tariffs, focus on cost recovery and service delivery. |

SSubstitutes Threaten

Limited Substitutes for Piped Water

For most residential, commercial, and industrial needs, such as cleaning, sanitation, and manufacturing, there are virtually no viable or economical substitutes for piped tap water provided by a utility. The sheer convenience, volume availability, and reliable quality offered by a centralized water system are difficult to match with other options.

Alternatives like bottled water are prohibitively expensive for large-scale consumption and often lack the consistent quality and volume required for many industrial processes. Even rainwater harvesting, while a potential supplement, requires significant infrastructure and treatment for potable use, making it impractical as a direct substitute for the daily needs met by a utility.

Bottled Water for Drinking Only

Bottled water acts as a substitute for Guangxi Nanning Waterworks primarily for drinking, often chosen due to perceived improvements in safety or taste. However, its significantly higher price point and the sheer volume required for household and industrial use make it impractical as a complete replacement for tap water services. For instance, in 2024, the average retail price of a liter of bottled water in China was approximately ¥2.50, compared to the utility's residential water rate of around ¥0.003 per liter, highlighting a substantial cost disparity.

Rainwater Harvesting and Private Wells

While rainwater harvesting and private wells can offer alternative water sources in certain rural or localized settings, they present a minimal threat to a large urban water utility like Guangxi Nanning Waterworks. These methods are generally not scalable or reliable enough to meet the consistent, high-volume demand of an urban population.

Industrial Water Recycling and Unconventional Water Sources

Large industrial clients in Guangxi may adopt water recycling and reuse technologies, spurred by national goals for water efficiency and Zero Liquid Discharge (ZLD) mandates. For instance, China's Ministry of Water Resources has set targets to increase water reuse rates, aiming for significant improvements by 2025. This internal efficiency measure by large users, rather than a direct substitution of the utility's core service, presents a limited threat to Guangxi Nanning Waterworks' broader customer base.

The expansion of unconventional water sources, such as treated recycled water, further diversifies supply options for industrial users. By 2024, China's investment in water-saving technologies and infrastructure, including advanced wastewater treatment for reuse, is projected to reach substantial figures, supporting this trend. While this can slightly reduce demand from specific large customers, it primarily reflects their internal operational adjustments or sourcing from alternative supplies, not a direct replacement for the utility's essential water provision.

- Industrial Water Recycling: Large users may invest in recycling to meet ZLD goals and reduce reliance on municipal supply.

- National Water Efficiency Targets: China's focus on improving water use efficiency by 2025 drives these industrial adoption trends.

- Unconventional Water Sources: Increased availability of recycled water offers alternative supply options for industrial consumers.

- Limited Direct Substitution: These internal efficiency measures and alternative sourcing are not direct substitutes for the utility's core service.

No Viable Substitutes for Centralized Sewage Treatment

For urban areas like Nanning, there are virtually no effective substitutes for centralized municipal sewage treatment. This service is critical for public health and environmental protection, with regulations often mandating its use. Individual or decentralized solutions simply cannot replicate the scale and effectiveness required for an entire city.

The essential nature of wastewater collection and treatment means that alternatives are practically nonexistent for a metropolitan area. For instance, in 2024, Nanning's urban population relies on its centralized system to manage millions of gallons of wastewater daily, a task too complex for decentralized methods to handle efficiently or compliantly.

- Essential Public Service: Centralized sewage treatment is a non-negotiable public utility.

- Regulatory Mandate: Government regulations require adherence to centralized treatment standards.

- Scale and Efficiency: Decentralized systems are not feasible for large urban populations.

- Environmental Protection: The system is crucial for preventing water pollution and safeguarding ecosystems.

No Economical Substitutes for Essential Piped Water

For most residential, commercial, and industrial needs, there are virtually no viable or economical substitutes for piped tap water provided by Guangxi Nanning Waterworks. The convenience, volume, and reliable quality of a centralized system are difficult to match. Bottled water is prohibitively expensive for large-scale consumption and often lacks the consistent quality and volume required for industrial processes. Even rainwater harvesting, while a supplement, requires significant infrastructure and treatment, making it impractical as a direct substitute for daily needs.

The threat of substitutes for Guangxi Nanning Waterworks is very low. While bottled water serves as a substitute for drinking purposes, its significantly higher cost makes it impractical for widespread use, especially when compared to the utility's low rates. For example, in 2024, the average retail price of bottled water in China was around ¥2.50 per liter, while Nanning's residential water rate was approximately ¥0.003 per liter. This stark price difference underscores the limited substitutability for everyday and industrial water needs.

Industrial clients may adopt water recycling to meet efficiency goals, driven by national targets like those set by China's Ministry of Water Resources to improve water reuse rates by 2025. However, these are internal efficiency measures rather than direct substitutions for the utility's core service. China's investment in water-saving technologies by 2024 further supports this trend, but it primarily reduces demand from specific large customers, not replacing the utility's essential provision for the broader market.

| Water Source | Primary Use Case | Estimated Cost per Liter (2024, RMB) | Threat Level to Guangxi Nanning Waterworks |

| Guangxi Nanning Waterworks Tap Water | Residential, Commercial, Industrial | ~0.003 | N/A |

| Bottled Water | Drinking, Perceived Quality | ~2.50 | Low (due to cost) |

| Rainwater Harvesting | Supplement, Potable (with treatment) | Variable (high infrastructure cost) | Very Low (scalability and reliability issues) |

| Industrial Water Recycling | Industrial Process Water | Variable (operational cost) | Low (internal efficiency, not direct substitution) |

Entrants Threaten

High Capital Investment Requirements

Establishing a new water utility company demands substantial upfront capital. This includes building treatment plants, laying extensive pipe networks, and constructing pumping stations, all of which are incredibly costly endeavors.

The sheer scale of financial commitment acts as a formidable barrier. For instance, China's significant investment in water conservancy facilities, reaching 1.35 trillion yuan in 2024, underscores the immense financial resources required in this sector.

Such prohibitive costs make it financially unfeasible for most aspiring companies to enter the market, effectively deterring potential new entrants from challenging established players in the Guangxi Nanning Waterworks industry.

Extensive Regulatory Hurdles and Licensing

The water supply and sewage treatment sectors in Guangxi Nanning are characterized by extensive regulatory hurdles and licensing requirements. These are in place because water is essential for public health and environmental safety. New companies looking to enter this market would need to navigate complex and time-consuming licensing procedures, secure environmental impact approvals, and consistently meet rigorous quality and service standards. China’s national-level water conservation regulations, reinforced in 2024, further underscore the stringent regulatory environment, significantly raising the barrier to entry for potential new players.

Government-Granted Monopolies/Concessions

Government-granted monopolies or concessions are a significant barrier for new entrants in the water supply and sewage treatment sector. Guangxi Nanning Waterworks likely benefits from such an arrangement, where local governments designate specific service territories, effectively preventing other companies from entering. This governmental control creates a robust framework that heavily favors established players.

Economies of Scale and Network Effects

Existing water utilities in Guangxi Nanning benefit from substantial economies of scale. This advantage stems from their large, established infrastructure, allowing for more efficient maintenance, optimized operations, and bulk purchasing power. For instance, in 2023, the average cost per cubic meter of water for established utilities in similar regions was significantly lower than projected costs for a new entrant attempting to build a comparable network from scratch.

New entrants face a formidable barrier due to these economies of scale. Reaching a similar level of cost efficiency would require massive upfront investment in duplicating the extensive distribution and treatment facilities already in place. This makes it exceptionally challenging for newcomers to compete on price, even if regulatory hurdles were cleared.

Furthermore, network effects play a crucial role. The more widespread an existing water utility's distribution system, the more valuable it becomes for serving customers efficiently. A new entrant would need to overcome this established reach, which is difficult to replicate quickly or cost-effectively.

- Economies of Scale: Existing utilities in Nanning leverage lower per-unit costs in infrastructure and operations due to their large scale.

- Network Effects: The established, widespread distribution network of current providers creates a significant advantage for customer service and delivery efficiency.

- Cost Disadvantage for New Entrants: New companies would face much higher initial capital expenditures and operational costs to match existing infrastructure.

- Competitive Barrier: These factors combine to create a strong barrier, making it difficult for new waterworks companies to enter and compete effectively in Nanning.

Access to Raw Water Sources and Land

New entrants would encounter significant hurdles in securing access to reliable raw water sources and obtaining the requisite land for water treatment facilities and network expansion within a developed urban center like Nanning. Existing water utilities often possess established rights and critical infrastructure, presenting a substantial barrier to entry.

In 2024, Nanning's water supply infrastructure is largely controlled by established entities, making it difficult for newcomers to acquire permits for new water intake points or to purchase land in strategically advantageous locations for new treatment plants. For instance, the Guangxi Nanning Waterworks likely holds concessions for key water bodies, limiting new players' options.

- Limited Water Source Availability: Nanning's primary water sources, such as the Yongjiang River, are already heavily utilized and regulated, with existing concessions granting priority to established operators.

- Land Acquisition Costs and Zoning: Acquiring suitable land for water treatment and distribution networks in Nanning is expensive and subject to strict urban planning regulations, further deterring new entrants.

- Infrastructure Integration Challenges: Connecting new facilities to the existing distribution network requires significant investment and cooperation with incumbent utilities, which may be reluctant to facilitate competition.

Nanning Waterworks: High Barriers Deter New Entrants

The threat of new entrants in the Guangxi Nanning waterworks sector is considerably low. This is primarily due to the immense capital requirements for establishing water treatment facilities and extensive distribution networks, a barrier highlighted by China's 1.35 trillion yuan investment in water conservancy in 2024. Furthermore, stringent government regulations and licensing procedures, reinforced by national water conservation policies in 2024, add significant complexity and time to market entry, effectively deterring potential competitors.

Existing players benefit from substantial economies of scale, leading to lower per-unit operational costs compared to what a new entrant would face when building from scratch. Network effects also play a critical role; the established and widespread distribution infrastructure of incumbent firms provides an efficiency advantage that is difficult and costly for newcomers to replicate. These combined factors create a robust competitive barrier.

Moreover, securing access to reliable water sources and strategically located land for infrastructure development presents another significant challenge. Established utilities in Nanning, like Guangxi Nanning Waterworks, often hold priority concessions for key water bodies, limiting options for new companies. The high cost and regulatory complexity of land acquisition in urban areas further compound these entry barriers.

| Barrier Type | Description | Impact on New Entrants | 2024 Data/Context |

|---|---|---|---|

| Capital Requirements | High costs for treatment plants, pipe networks, pumping stations. | Prohibitive for most new companies. | China's 1.35 trillion yuan investment in water conservancy facilities. |

| Regulatory Hurdles | Complex licensing, environmental approvals, quality standards. | Time-consuming and costly to navigate. | Reinforced national water conservation regulations. |

| Economies of Scale | Lower per-unit costs for established, large-scale operations. | New entrants face higher initial operational costs. | Lower average cost per cubic meter for established utilities vs. projected new entrant costs. |

| Access to Resources | Limited availability of water sources and suitable land. | Existing concessions and land acquisition difficulties. | Priority concessions for key water bodies like the Yongjiang River. |

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis for Guangxi Nanning Waterworks leverages data from official government reports, water industry regulatory filings, and local economic development statistics to understand the competitive landscape.