First Commonwealth Bank Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

First Commonwealth Bank Bundle

From Overview to Strategy Blueprint

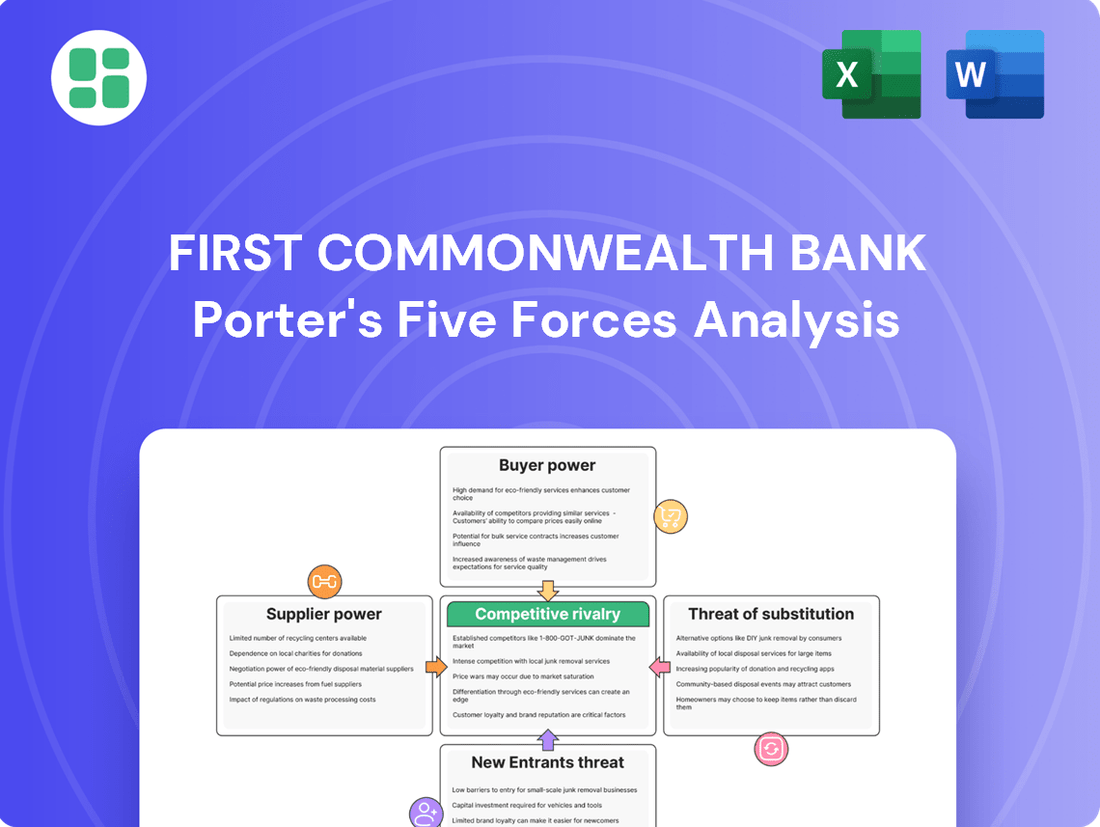

First Commonwealth Bank operates within a dynamic financial landscape, where understanding the competitive forces at play is crucial for success. Our analysis delves into the intensity of rivalry among existing competitors, the bargaining power of their customers, and the influence of their suppliers.

The complete report reveals the real forces shaping First Commonwealth Bank’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Supplier Concentration

Supplier concentration within the banking sector is a significant factor influencing the bargaining power of suppliers. Banks heavily depend on a limited number of specialized technology providers for critical functions like core processing, cybersecurity, and digital banking platforms.

This concentration means that a few key suppliers hold substantial sway. For instance, in 2024, the market for core banking systems is dominated by a handful of major players, making it difficult for banks to find alternative solutions quickly.

The high switching costs associated with these integrated systems further empower these suppliers. Banks face considerable expense and operational disruption when attempting to change providers, reinforcing the suppliers' leverage in negotiations.

Importance of Inputs

For First Commonwealth Bank, the importance of inputs like advanced financial software and data analytics tools cannot be overstated. These are the engines that drive operational efficiency and ensure compliance with ever-evolving financial regulations.

The providers of these critical services, such as specialized fintech firms and data vendors, often hold significant sway. Their ability to offer unique, indispensable solutions means they can command higher prices or more favorable terms, directly impacting the bank's cost structure and profitability.

In 2024, the financial services sector saw continued investment in technology, with many banks allocating substantial budgets to digital transformation and data infrastructure. This reliance on specialized external providers for these key inputs amplifies their bargaining power within the industry.

Switching Costs for the Bank

For First Commonwealth Bank, the bargaining power of suppliers is significantly influenced by the high switching costs associated with its core banking software and IT infrastructure. Changing these systems involves substantial financial outlays, potential operational disruptions, and the necessity for extensive employee retraining, making it difficult to switch providers readily. For instance, in 2024, the average cost for a mid-sized bank to migrate its core banking system was estimated to be in the tens of millions of dollars, with implementation timelines often extending over 18-24 months. This inertia inherently strengthens the leverage of existing IT vendors.

Availability of Substitutes for Suppliers

The availability of substitutes for suppliers significantly impacts First Commonwealth Bank's bargaining power. While many providers offer generic IT services, the market for highly specialized banking software and regulatory compliance solutions is much more concentrated. This scarcity of alternatives for critical banking functions means First Commonwealth Bank has a limited pool of suppliers to choose from.

This limited choice directly translates to increased supplier bargaining power. For instance, in 2024, the average cost of core banking software implementation for regional banks saw an increase of approximately 7-10% due to the specialized nature of the technology and the limited number of vendors capable of providing robust, compliant solutions. Consequently, First Commonwealth Bank faces higher costs and potentially less favorable contract terms when procuring these essential services.

- Limited Substitutes for Specialized Software: Core banking systems and advanced cybersecurity platforms often have few direct competitors, giving suppliers leverage.

- High Switching Costs: Migrating to a new specialized software provider can be complex and expensive, further entrenching existing supplier relationships.

- Impact on Profitability: Increased costs from powerful suppliers can directly reduce First Commonwealth Bank's profit margins.

Human Capital Expertise

The bargaining power of suppliers for First Commonwealth Bank is significantly influenced by the availability of human capital expertise. Access to highly skilled professionals in critical areas such as cybersecurity, artificial intelligence, and wealth management represents a key supplier dynamic. A scarcity of these specialized talents in the broader market can directly impact the bank's operational costs by increasing the expense associated with recruiting and retaining top-tier employees.

This talent shortage can translate into higher salary demands and more competitive benefits packages, ultimately driving up the bank's overall operating expenses. For instance, in 2024, the demand for cybersecurity professionals continued to outstrip supply, with average salaries for experienced professionals in this field seeing significant year-over-year increases across the financial services sector.

- Talent Scarcity Impact: Shortages in specialized fields like AI and cybersecurity increase recruitment and retention costs.

- Salary Pressures: Limited supply of skilled professionals leads to upward pressure on compensation, raising operating expenses.

- Competitive Landscape: Banks like First Commonwealth must compete for a finite pool of talent, potentially driving up labor costs.

- Strategic Importance: Expertise in areas like wealth management is crucial for growth, making talent acquisition a key supplier consideration.

Supplier Power: The Bank's Costly Challenge

The bargaining power of suppliers for First Commonwealth Bank is substantial due to the concentrated nature of specialized technology providers and the high costs associated with switching these critical systems. This leverage allows suppliers to command higher prices, impacting the bank's profitability.

In 2024, the market for core banking systems remained dominated by a few key players, with migration costs for mid-sized banks estimated in the tens of millions of dollars and implementation timelines often exceeding 18 months. This limited choice and high switching inertia significantly strengthen supplier leverage.

| Supplier Characteristic | Impact on First Commonwealth Bank | 2024 Data/Example |

|---|---|---|

| Supplier Concentration (Core Banking) | Limited choice, increased leverage for suppliers | Market dominated by a few major vendors |

| Switching Costs (IT Infrastructure) | High financial outlay, operational disruption, retraining needs | Estimated $10M+ for mid-sized bank migration; 18-24 month implementation |

| Scarcity of Specialized Software | Limited alternatives for critical banking functions | 7-10% cost increase for specialized software implementation in 2024 |

| Talent Scarcity (AI, Cybersecurity) | Increased recruitment and retention costs | Significant year-over-year salary increases for experienced professionals |

What is included in the product

This Porter's Five Forces analysis for First Commonwealth Bank delves into the competitive intensity within the banking sector, examining the bargaining power of customers and suppliers, the threat of new entrants and substitutes, and the overall rivalry among existing players.

Instantly visualize competitive intensity across all five forces, enabling First Commonwealth Bank to proactively address potential threats and capitalize on opportunities.

Customers Bargaining Power

Customer Switching Costs

For many everyday banking needs, like checking and savings accounts, customers can switch to another bank with minimal hassle. The rise of online banking and mobile apps means opening a new account can often be done in minutes, with very low direct financial or procedural barriers. This low switching cost for basic services puts pressure on First Commonwealth Bank to remain competitive on fees and service quality.

However, the picture changes for more involved financial relationships. When customers have commercial loans, mortgages, or utilize comprehensive wealth management services, the costs to switch become significantly higher. These costs can include early repayment penalties, the time and effort to re-establish credit lines, or the complexity of transferring investment portfolios. In 2024, for instance, the average time to close on a new mortgage can be 30-60 days, a significant undertaking that discourages frequent switching for such products.

Customer Information Availability

Customers today have unprecedented access to information about banking products. Online comparison tools and direct bank websites allow consumers to easily research interest rates, fees, and service features from numerous financial institutions. This readily available data significantly enhances their ability to shop around and secure the most favorable terms, directly boosting their bargaining power.

Customer Segmentation

First Commonwealth Bank caters to a broad spectrum of clients, from individual consumers to large institutional investors. For retail customers, the ability to switch banks is generally straightforward, giving them significant bargaining power, especially when seeking better rates or lower fees. In 2024, the average checking account fee across U.S. banks was around $10 per month, a figure individual customers can readily compare and negotiate or avoid by switching.

Price Sensitivity of Customers

Customers in the banking sector often show significant price sensitivity, especially when it comes to interest rates on loans and the yields offered on deposits. This means that First Commonwealth Bank must remain highly competitive on its pricing to draw in and keep its customer base, which directly influences its bottom line.

For instance, in 2024, the average interest rate for a 30-year fixed-rate mortgage hovered around 6.6%, a figure that heavily influences borrower decisions. Similarly, deposit account yields can be a deciding factor for customers choosing where to park their savings.

- High Price Sensitivity: Customers frequently compare rates for loans and savings accounts, making pricing a critical differentiator.

- Impact on Profitability: Competitive pricing pressures can squeeze net interest margins for banks like First Commonwealth.

- Customer Retention: Offering attractive rates is key to preventing customers from switching to competitors.

Product Differentiation

Product differentiation is a key factor in mitigating the bargaining power of customers for First Commonwealth Bank. Many core banking products, such as checking accounts and basic savings, are viewed as commodities. This makes it challenging for any bank, including First Commonwealth, to stand out based on features alone.

Consequently, differentiation efforts for First Commonwealth Bank must focus on areas beyond just product specifications. Superior service quality, seamless digital banking experiences, convenient branch networks, and fostering strong, personalized relationships are crucial. These elements can significantly influence customer loyalty and reduce their inclination to switch to competitors, thereby lessening their bargaining power.

In 2024, customer retention remains a paramount concern for financial institutions. For instance, a study by Bain & Company indicated that a 5% increase in customer retention can boost profits by 25% to 95%. This underscores the importance of First Commonwealth Bank’s strategies in service and relationship building to counter the commoditized nature of its offerings and maintain a stable customer base.

- Service Quality: Investing in customer service training and efficient issue resolution directly impacts customer satisfaction.

- Digital Convenience: Enhancing mobile banking apps and online platforms makes transactions easier, fostering loyalty.

- Branch Accessibility: A well-distributed branch network offers physical touchpoints that some customers still value.

- Relationship Banking: Personalized advice and tailored financial solutions build deeper connections, reducing price sensitivity.

Customer Power: Navigating Banking's Competitive Landscape

The bargaining power of customers for First Commonwealth Bank is significant, particularly for basic banking services where switching costs are low. Customers can easily compare rates and fees across institutions, making price sensitivity a key factor. In 2024, the average checking account fee of around $10 per month highlights how easily customers can assess and avoid such costs by moving to a competitor, directly impacting the bank's revenue streams.

For more complex products like mortgages or wealth management, switching becomes more involved, increasing customer stickiness. However, the ease of information access through online tools empowers customers to find better deals, even for these services. For example, the average 30-year fixed mortgage rate in 2024, around 6.6%, means customers actively seek the best terms, putting pressure on First Commonwealth to remain competitive.

To counter this, First Commonwealth Bank focuses on product differentiation through superior service, digital convenience, and relationship banking. A 5% increase in customer retention can boost profits by 25% to 95%, according to Bain & Company, underscoring the value of these strategies in mitigating customer bargaining power.

| Factor | Impact on First Commonwealth Bank | Mitigation Strategy |

|---|---|---|

| Low Switching Costs (Basic Services) | High customer price sensitivity, easy to switch for better rates/lower fees. | Competitive pricing, loyalty programs. |

| High Switching Costs (Complex Services) | Reduced customer inclination to switch for mortgages, wealth management. | Enhanced value-added services, personalized advice. |

| Information Accessibility | Customers easily compare offerings, increasing bargaining power. | Transparent fee structures, clear communication of value proposition. |

| Price Sensitivity | Direct impact on net interest margins and deposit growth. | Strategic rate setting, focus on non-price customer benefits. |

What You See Is What You Get

First Commonwealth Bank Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. It details the competitive landscape for First Commonwealth Bank, analyzing the intensity of rivalry among existing firms, the bargaining power of suppliers and buyers, the threat of new entrants, and the availability of substitute products and services. This comprehensive Porter's Five Forces analysis provides actionable insights into the strategic positioning and potential challenges facing First Commonwealth Bank.

Rivalry Among Competitors

Number and Diversity of Competitors

First Commonwealth Bank faces a competitive environment featuring a broad array of players, from national banking giants to smaller community banks and credit unions. This diversity means rivalry is multifaceted, with each competitor type vying for distinct customer bases, particularly within its core Pennsylvania and Ohio markets.

Market Growth Rate

The banking market in Pennsylvania and Ohio, where First Commonwealth Bank primarily operates, is quite mature. This maturity means growth is generally slower compared to newer markets. In 2024, the U.S. banking industry saw a modest net interest margin expansion, but for established regional banks, the challenge remains attracting new business in a saturated environment.

Product Commoditization

Many of First Commonwealth Bank's core offerings, like basic checking and savings accounts, are highly commoditized. This means there's little to distinguish them from competitors' products, forcing banks to compete primarily on price and fees.

This intense competition on price and fees, driven by product commoditization, can significantly pressure profit margins. For instance, in 2024, the average checking account had a monthly maintenance fee of around $10, with many banks waiving it for minimum balances or direct deposit, highlighting the pressure to offer low-cost or no-cost basic services.

High Fixed Costs and Exit Barriers

First Commonwealth Bank operates in a sector with substantial fixed costs. These include investments in technology, maintaining a physical branch presence, and adhering to stringent regulatory requirements. For instance, in 2024, the financial services industry continued to see significant capital allocation towards digital transformation and cybersecurity, estimated to be in the billions globally.

The banking industry also faces high exit barriers. These are not just financial but also social and economic. Shutting down branches or ceasing operations can have considerable local economic impacts and affect customer relationships built over years. This discourages banks from leaving the market, leading them to compete intensely for market share rather than exiting.

- High Capital Investment: Banks must invest heavily in IT systems, compliance software, and physical infrastructure.

- Regulatory Hurdles: Strict regulations necessitate ongoing compliance spending, making it costly to exit.

- Customer Loyalty and Brand Reputation: The cost and effort to build customer trust mean banks are reluctant to abandon their customer base.

- Geographic Presence: Maintaining a network of branches, even with reduced foot traffic, represents a significant fixed cost that is difficult to divest quickly.

Technological Advancements and Digitalization

Technological advancements and the growing preference for digital banking are intensifying competition. Banks like First Commonwealth must constantly upgrade their digital offerings to keep pace. For instance, in 2024, the global digital banking market was projected to reach over $25 trillion, highlighting the significant investment required.

This rapid evolution means that institutions slow to adopt new technologies, such as AI-driven customer service or enhanced mobile app functionalities, risk falling behind. The pressure to innovate is continuous, forcing strategic decisions about resource allocation towards digital transformation.

- Digital Transformation Investment: Banks are channeling billions into upgrading digital platforms.

- Customer Expectations: Consumers increasingly demand seamless, intuitive online and mobile banking experiences.

- Fintech Competition: Agile fintech companies are often at the forefront of digital innovation, challenging traditional banks.

- Data Analytics: Leveraging data analytics to personalize services is becoming a key differentiator in the digital space.

Financial Institutions Face Intense Rivalry and Digital Disruption

The competitive rivalry for First Commonwealth Bank is intense due to the presence of numerous financial institutions, ranging from national banks to local credit unions, all vying for market share in its core Pennsylvania and Ohio regions. This rivalry is amplified by the commoditized nature of many banking products, forcing competition on price and fees, which can compress profit margins. For example, in 2024, many regional banks focused on retaining customers through competitive pricing on loans and deposits amidst a challenging economic climate.

High fixed costs associated with technology, compliance, and physical infrastructure, coupled with significant exit barriers, mean that banks remain in the market, intensifying competition. The ongoing digital transformation in the banking sector, with billions invested globally in 2024 for upgrades and fintech integration, further fuels this rivalry as institutions strive to meet evolving customer expectations for seamless online and mobile experiences.

| Competitor Type | Key Differentiator | Impact on Rivalry |

|---|---|---|

| National Banks | Brand recognition, broader product suite | Price pressure, economies of scale |

| Community Banks | Local relationships, personalized service | Niche market competition, customer retention focus |

| Credit Unions | Member-focused, often lower fees | Direct competition on cost for certain customer segments |

| Fintech Companies | Digital innovation, agility | Disruption of traditional services, pressure to modernize |

SSubstitutes Threaten

Rise of Fintech Companies

The rise of fintech companies presents a significant threat of substitutes for traditional banks like First Commonwealth. These nimble digital players offer specialized solutions that directly compete with core banking services. For instance, mobile payment apps are increasingly replacing traditional methods for everyday transactions, and peer-to-peer lending platforms offer alternative financing options, often with more streamlined processes and potentially lower interest rates for borrowers.

These fintech alternatives frequently compete on convenience and cost. Many users find mobile banking and payment solutions far more accessible and user-friendly than traditional branch visits or even online banking portals. Furthermore, the operational efficiencies of digital-first companies often translate into lower fees for consumers, making them an attractive substitute for services like money transfers, wealth management, and even small business loans. By mid-2024, the global fintech market was valued at over $2.5 trillion, demonstrating the substantial scale of this competitive landscape.

Non-Bank Lending Platforms

Non-bank lending platforms, such as online lenders and crowdfunding sites, present a significant threat of substitution for traditional banks like First Commonwealth. These platforms offer alternative avenues for businesses and individuals seeking capital, thereby diminishing reliance on commercial banks for loans. For instance, in 2023, the US online lending market was valued at over $140 billion, demonstrating substantial growth and a clear alternative for borrowers.

Alternative Investment Vehicles

Customers seeking to grow their savings and manage their wealth have a wide array of alternatives to traditional bank deposits. These include money market funds, mutual funds, brokerage accounts, and direct investments in stocks and bonds. For instance, as of early 2024, many money market funds were offering yields exceeding 5%, a significantly higher return than typical savings accounts, thus presenting a strong substitute for bank deposits.

Credit Unions and Community Development Financial Institutions (CDFIs)

Credit unions present a significant threat of substitution for First Commonwealth Bank. As member-owned, non-profit entities, they frequently provide more favorable interest rates and reduced fees compared to traditional commercial banks, appealing strongly to both individual consumers and small businesses. For instance, in 2023, credit unions reported an average interest rate on savings accounts that was 0.15% higher than that of commercial banks, according to data from the National Credit Union Administration.

Community Development Financial Institutions (CDFIs) also serve as viable alternatives, particularly for customers in underserved areas. These organizations focus on providing specialized financial services and fostering economic growth within specific communities, offering a distinct value proposition that can draw customers away from larger, more conventional financial institutions. The number of CDFIs in the U.S. grew by 10% in 2023, reaching over 1,400 certified institutions, highlighting their expanding reach and influence.

- Competitive Rates: Credit unions often boast higher savings rates and lower loan rates than commercial banks.

- Lower Fees: Many credit unions offer fewer or lower fees on checking accounts and other services.

- Community Focus: CDFIs specifically target and serve communities that may be overlooked by traditional banks.

- Member Benefits: As non-profits, credit unions can reinvest profits back into member services, potentially offering better terms.

Digital Payment and Wallet Solutions

The rise of digital payment and wallet solutions presents a significant threat of substitutes for First Commonwealth Bank. Platforms like PayPal, Apple Pay, and various fintech apps offer convenient alternatives for everyday transactions, bypassing traditional banking infrastructure.

This trend directly impacts banks by siphoning off fee income traditionally generated from debit and credit card processing. For instance, in 2023, the global digital payments market was valued at over $9 trillion, demonstrating a substantial shift away from legacy systems.

- Convenience: Digital wallets offer seamless, often one-tap payment experiences.

- Accessibility: Many digital solutions are readily available on smartphones, a device nearly ubiquitous in 2024.

- Fee Structures: Some digital payment providers may offer lower transaction fees or different revenue models compared to traditional banks.

- Innovation: The rapid pace of innovation in the fintech sector continually introduces new and improved payment alternatives.

Financial Alternatives: The Growing Threat to Conventional Banking

The threat of substitutes for First Commonwealth Bank is substantial, stemming from a diverse range of financial service providers and technological advancements. Fintech companies, credit unions, and non-bank lenders offer compelling alternatives that directly challenge traditional banking models by providing specialized services, competitive rates, and enhanced convenience. The growing adoption of digital payment solutions further erodes reliance on conventional banking channels for everyday transactions.

| Substitute Type | Key Offering | Competitive Advantage | Market Data Point (2023/2024) |

|---|---|---|---|

| Fintech Companies | Digital payments, P2P lending, specialized lending | Convenience, lower fees, streamlined processes | Global fintech market valued over $2.5 trillion (mid-2024) |

| Credit Unions | Banking services, loans | Favorable interest rates, lower fees, member focus | Higher savings rates than commercial banks (2023) |

| Non-Bank Lenders | Online loans, crowdfunding | Alternative capital access, potentially faster approvals | US online lending market valued over $140 billion (2023) |

| Digital Wallets/Payments | Mobile transactions | Seamless user experience, widespread smartphone adoption | Global digital payments market valued over $9 trillion (2023) |

Entrants Threaten

High Capital Requirements

Establishing a new bank, like First Commonwealth Bank, demands significant capital. In 2024, regulatory bodies often require new banks to hold substantial reserves, sometimes in the tens of millions of dollars, to ensure stability and protect depositors. This hefty financial barrier inherently limits the pool of potential new entrants, as only well-funded organizations can realistically consider entering the market.

Stringent Regulatory Environment

The banking sector, including institutions like First Commonwealth Bank, is characterized by a stringent regulatory environment. Federal and state authorities impose complex licensing requirements, demanding significant capital and operational adherence. For instance, the Dodd-Frank Act, enacted in 2010 and continually updated, introduced extensive regulations aimed at financial stability, creating a high hurdle for any new player seeking to enter the market.

Economies of Scale and Experience

Existing financial institutions, such as First Commonwealth Bank, leverage significant economies of scale. This allows them to spread operational costs, technology investments, and marketing expenses over a larger customer base, leading to lower per-unit costs. For instance, in 2023, large banks often reported significantly lower efficiency ratios compared to smaller, regional players.

New entrants face a substantial hurdle in replicating these cost advantages. Building a comparable infrastructure and achieving similar operational efficiencies takes considerable time and capital investment, making it difficult to compete on price from the outset. This barrier is particularly pronounced in areas like digital banking platforms and regulatory compliance, where upfront costs are high.

Brand Loyalty and Trust

Brand loyalty and trust are significant barriers for new entrants in the banking sector. Customers often feel secure with established institutions for managing their savings and investments, making it difficult for newcomers to gain traction. Building this level of trust requires years of consistent, reliable service.

For instance, as of late 2024, major banks continue to report high customer retention rates, often exceeding 90% for core deposit accounts. This deep-seated loyalty means new banks must offer compelling incentives or a truly differentiated service to even begin chipping away at the market share of incumbents like First Commonwealth Bank.

- High Customer Retention: Established banks benefit from long-standing customer relationships, often seeing retention rates above 90% for primary accounts.

- Trust as a Barrier: The perceived security and reliability of established financial institutions deter customers from switching to newer, unproven entities.

- Time and Effort: Cultivating brand loyalty and trust is a lengthy process, demanding substantial investment in customer service and consistent performance.

- Differentiated Offerings: New entrants must present unique value propositions to overcome the inertia of customer loyalty.

Difficulty in Building Distribution Networks

Building an effective distribution network for a bank like First Commonwealth is a significant hurdle for potential new entrants. This involves not just physical branches and ATMs, but also sophisticated and secure digital banking platforms. The sheer capital outlay and the time needed to establish this infrastructure from scratch are substantial deterrents.

Even for digital-native challengers, overcoming the distribution challenge requires immense marketing investment. While they avoid the costs of physical real estate, they must spend heavily to gain brand recognition and cultivate customer trust in a crowded market. For instance, in 2024, the average customer acquisition cost for digital banks continued to be a major factor impacting profitability.

- Capital Investment: New entrants need to invest heavily in both physical (branches, ATMs) and digital infrastructure to compete with established players.

- Time to Market: Developing a comprehensive and trusted distribution network takes years, creating a significant time lag for newcomers.

- Marketing and Brand Building: Digital banks, while saving on physical costs, face high customer acquisition costs due to the need for extensive marketing to build awareness and trust.

- Regulatory Compliance: Establishing a compliant and secure distribution network involves navigating complex regulatory landscapes, adding to the cost and time.

New Entrants Face Formidable Banking Barriers

The threat of new entrants for First Commonwealth Bank is generally low, primarily due to the substantial capital requirements and complex regulatory landscape governing the banking industry. For example, in 2024, establishing a new bank often necessitates initial capital exceeding $10 million, with many requiring upwards of $50 million to meet regulatory reserves and operational needs.

Furthermore, established players like First Commonwealth benefit from significant economies of scale, which translate into lower per-unit costs for services. Newcomers struggle to match these efficiencies, as replicating extensive branch networks and sophisticated digital platforms demands considerable time and investment. In 2023, the average efficiency ratio for large, established banks was often around 50-60%, a benchmark difficult for new entrants to achieve quickly.

Customer loyalty and trust also act as formidable barriers. As of late 2024, major banks consistently report customer retention rates above 90% for core banking products. New entrants must offer compelling incentives or highly differentiated services to attract customers away from trusted, incumbent institutions, a process that is both time-consuming and costly.

| Barrier Type | Description | Impact on New Entrants | Example Data (2023-2024) |

|---|---|---|---|

| Capital Requirements | High initial investment needed to meet regulatory standards and operational setup. | Significantly limits the number of potential new entrants. | Minimum capital for new national banks often in the tens of millions USD. |

| Regulatory Hurdles | Complex licensing, compliance, and ongoing oversight from financial authorities. | Increases time-to-market and operational costs for new players. | Dodd-Frank Act and subsequent regulations impose extensive compliance burdens. |

| Economies of Scale | Established banks spread fixed costs over a larger customer base, leading to lower unit costs. | New entrants face higher per-unit operating costs, impacting price competitiveness. | Large banks often have efficiency ratios below 60%, while startups struggle to reach this. |

| Brand Loyalty & Trust | Customers' preference for established, reliable financial institutions. | Makes customer acquisition difficult and expensive for new banks. | Incumbent banks frequently maintain customer retention rates above 90%. |

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis for First Commonwealth Bank leverages data from their annual reports, investor relations website, and financial statements. We also incorporate insights from industry publications, market research reports, and competitor announcements to provide a comprehensive view of the competitive landscape.