EPL Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

EPL Bundle

Don't Miss the Bigger Picture

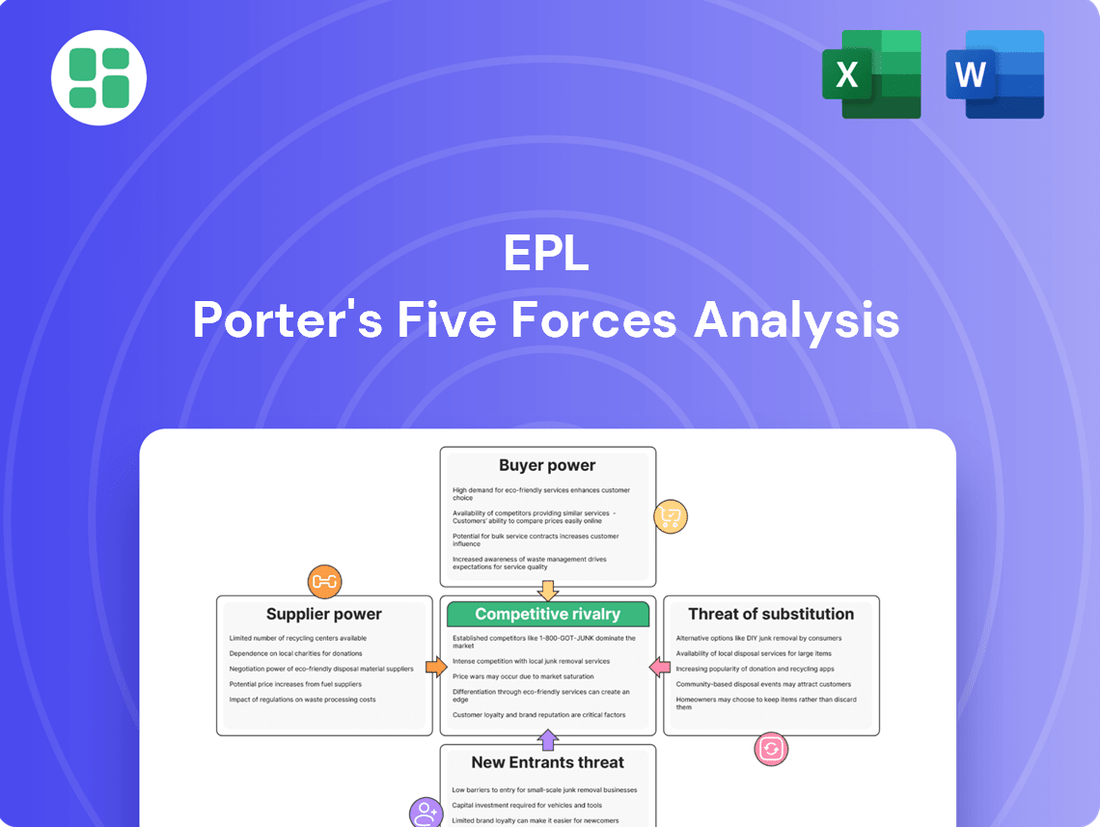

Porter's Five Forces reveals the intense competition within the EPL, highlighting significant threats from new entrants and the constant pressure from powerful buyers. Understanding these dynamics is crucial for any stakeholder looking to navigate this complex market.

The complete report reveals the real forces shaping EPL’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Raw Material Dependency

EPL's reliance on polymer resins, laminates, and inks as core components for its laminated plastic tubes places significant weight on supplier bargaining power. These materials are not only fundamental to production but also directly influence the cost of goods sold.

The market for these raw materials is often volatile, with prices susceptible to shifts in global oil markets and the ever-present risk of supply chain disruptions. For instance, a surge in crude oil prices in early 2024 directly translated to higher resin costs for many manufacturers. Furthermore, the availability and pricing of specialized barrier materials, such as EVOH or aluminum foil, are crucial for achieving the desired performance characteristics of the final product, adding another layer of supplier influence.

EPL's strategic move to incorporate recycled resins for sustainability also brings its own set of market dynamics. The pricing of these recycled materials, while offering environmental benefits, is still subject to supply and demand fluctuations, meaning suppliers of these also hold considerable sway.

Limited Number of Specialized Suppliers

For specialized packaging components, particularly those meeting stringent pharmaceutical or sensitive FMCG product requirements, the pool of qualified suppliers can be quite small. This scarcity inherently grants these niche suppliers greater negotiating power regarding pricing and contract terms.

When switching costs are substantial for a company like EPL, perhaps due to intricate technical specifications or necessary certifications, this supplier leverage intensifies. EPL's strategic pivot towards sustainable packaging, such as tubes made from 100% recyclable materials, further anchors its reliance on suppliers proficient in advanced recycled content and bio-based plastics, potentially concentrating power among a select few.

Supplier Concentration and Scale

While the market for basic polymers might feature numerous suppliers, the bargaining power shifts significantly when considering specialized materials like advanced laminates or unique machinery crucial for tube manufacturing. These niche segments often exhibit higher supplier concentration, giving dominant players more leverage. For instance, in 2024, the global advanced materials market, which includes specialized polymers, saw key players controlling substantial market share, allowing them to dictate terms.

Large, globally integrated chemical companies that produce polymers can wield considerable bargaining power. Their sheer scale of operations, economies of scale in production, and control over proprietary technologies or raw material access enable them to influence pricing and supply availability. This was evident in 2024 as major chemical producers continued to benefit from optimized global supply chains, impacting raw material costs for downstream manufacturers.

EPL's extensive global manufacturing footprint is a strategic advantage in managing supplier relationships. By sourcing materials from diverse geographic regions, EPL can mitigate the risks associated with localized supplier power or disruptions. This diversification helps ensure a more stable and cost-effective supply chain, even when dealing with concentrated suppliers in specific product categories.

Switching Costs for EPL

Switching suppliers for critical raw materials or specialized machinery presents significant hurdles for EPL. These can include the costs associated with re-qualifying new vendors, rigorous testing of new materials, potential adjustments to production lines, and the time and resources needed to establish new supplier relationships. These factors create a tangible barrier to switching, which in turn amplifies the bargaining power of EPL's existing suppliers.

EPL is actively working to mitigate these switching costs. Their strategies include exploring and implementing raw material substitutions where feasible and consolidating their supplier base. These initiatives are designed to reduce dependence on any single supplier and to gain more leverage in negotiations by streamlining procurement processes and potentially achieving economies of scale.

- High Re-qualification Costs: For specialized components, the process of testing and approving a new supplier can take months and cost hundreds of thousands of dollars, potentially impacting production schedules.

- Production Line Adjustments: A change in a key raw material might necessitate recalibrating machinery, adding further expense and downtime for EPL.

- Supplier Consolidation Benefits: By reducing the number of suppliers, EPL can negotiate better terms and build stronger, more collaborative partnerships, thereby reducing the impact of individual supplier power.

Forward Integration Threat from Suppliers

The threat of suppliers integrating forward into manufacturing basic packaging components, while generally low for intricate items like laminated tubes, remains a potential concern. For instance, a major chemical supplier with extensive R&D could theoretically develop capabilities to produce specialized caps or seals, thereby entering the packaging component market.

This forward integration threat is particularly relevant if suppliers possess proprietary technologies or unique materials. Such dependencies can significantly amplify supplier bargaining power. For example, in 2024, the specialty chemicals sector saw significant consolidation, with a few key players dominating the supply of advanced barrier resins crucial for high-performance packaging, potentially giving them leverage over downstream manufacturers.

- Forward Integration Threat: Suppliers moving into component manufacturing.

- Impact on Laminated Tubes: Generally low, but a latent consideration for basic components.

- Supplier Leverage: Increased by proprietary technologies and material dependencies.

- 2024 Trend: Consolidation in specialty chemicals amplified supplier power in critical material supply chains.

Specialized Materials Drive Significant Supplier Bargaining Power

The bargaining power of suppliers for EPL is significant, primarily due to the specialized nature of raw materials like polymer resins, laminates, and inks. These essential components are subject to price volatility, as seen with crude oil price surges in early 2024 impacting resin costs. Furthermore, the limited availability of specialized barrier materials and the high costs associated with switching suppliers, including re-qualification and production line adjustments, grant suppliers considerable leverage.

The concentration of suppliers in niche markets, such as advanced barrier resins, further empowers them. For instance, major chemical producers in 2024 benefited from optimized global supply chains, influencing raw material costs for manufacturers like EPL. While EPL diversifies its sourcing geographically, the inherent dependencies on specialized materials and the substantial switching costs remain key drivers of supplier bargaining power.

| Factor | Impact on EPL | 2024 Data/Trend |

|---|---|---|

| Material Specialization | High reliance on specific resins, laminates, and inks. | Specialty chemicals sector saw consolidation, increasing power of key players. |

| Price Volatility | Susceptible to fluctuations in oil markets and raw material costs. | Crude oil price surges in early 2024 directly increased resin costs. |

| Switching Costs | Significant expenses for re-qualification, testing, and production line adjustments. | Re-qualification can cost hundreds of thousands of dollars and impact production schedules. |

| Supplier Concentration | Limited qualified suppliers for specialized or high-performance materials. | Dominant players in advanced materials and barrier resins dictate terms. |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to the English Premier League's unique ecosystem.

Instantly assess competitive intensity with a visual breakdown of each force, simplifying complex market dynamics.

Customers Bargaining Power

Large, Consolidated FMCG and Pharma Clients

EPL's customer base includes major Fast-Moving Consumer Goods (FMCG) and pharmaceutical giants, many of which are multinational corporations. These large clients leverage their significant purchasing volumes to negotiate favorable terms.

With substantial order sizes and established procurement departments, these customers can effectively demand competitive pricing, flexible payment schedules, and stringent quality assurances from suppliers like EPL.

For instance, in 2024, the global FMCG market was valued at over $10 trillion, with large players like Procter & Gamble and Nestlé commanding immense buying power, directly impacting their suppliers' pricing strategies.

Price Sensitivity and Cost Pressure

Customers, especially in the fast-moving consumer goods (FMCG) sector, exhibit significant price sensitivity. This is driven by the fierce competition they face within their own industries, directly impacting packaging suppliers like EPL. For instance, in 2024, the average FMCG company experienced a 3% increase in input costs, pushing them to seek cost reductions from their suppliers.

This price sensitivity creates continuous pressure on EPL to maintain low costs and offer competitive pricing strategies. Even in sectors like pharmaceuticals, where quality and regulatory compliance are paramount, there's a persistent demand for cost efficiencies. In 2023, pharmaceutical companies reported an average of 5% of their overall budget dedicated to packaging, highlighting the importance of cost management in this area.

Product Standardization and Switching Costs

While EPL provides tailored packaging solutions, the core laminated plastic tubes possess a degree of standardization. This means large customers, particularly those in less regulated sectors, can more readily compare and switch between suppliers if pricing or terms become unfavorable. For instance, in the cosmetics industry, where aesthetic appeal is key but regulatory hurdles are lower, switching suppliers might be less complex.

However, the equation shifts significantly for sectors with stringent requirements. The substantial investment in research and development, coupled with rigorous certification processes, particularly for pharmaceutical packaging, erects considerable barriers to switching. For a pharmaceutical company, re-validating a new tube supplier can cost hundreds of thousands of dollars and take months, effectively locking them in with existing providers like EPL and mitigating customer bargaining power.

Customer Demand for Sustainability

Customer demand for sustainability is a growing force, particularly in sectors like FMCG and pharmaceuticals. These industries are increasingly seeking packaging suppliers that offer eco-friendly and recyclable options. This trend empowers customers, giving them leverage to choose partners like EPL that can demonstrate robust sustainability practices, such as providing tubes made from 100% post-consumer recycled (PCR) content.

EPL's commitment to sustainable innovation directly addresses this customer need. For instance, in 2024, the global market for sustainable packaging was valued at over $250 billion, with a significant portion driven by consumer preference for environmentally responsible products. Companies actively seeking PCR content in their packaging can exert greater bargaining power, favoring suppliers who meet these stringent criteria.

- Growing Demand: Consumer and business pressure for sustainable products is a key driver.

- Supplier Differentiation: Companies like EPL offering 100% recyclable or PCR content gain an advantage.

- Market Value: The sustainable packaging market exceeded $250 billion in 2024, highlighting its economic significance.

- Customer Leverage: Prioritizing suppliers with strong sustainability credentials enhances customer bargaining power.

Backward Integration Threat from Customers

While large FMCG and pharmaceutical firms might theoretically consider backward integration into packaging production, the highly specialized nature of laminated tube manufacturing makes this a rare occurrence. Their primary focus remains on core product development and marketing, not the intricacies of specialized packaging processes.

However, these powerful buyers wield significant leverage by dictating precise product specifications and actively soliciting bids from multiple packaging suppliers. This competitive tendering process effectively drives down prices and forces manufacturers to operate with tighter margins, demonstrating a strong form of customer bargaining power.

For instance, in 2024, major consumer goods companies continued to consolidate their supplier bases, often demanding price reductions of 3-5% on existing contracts. This trend is driven by increased global competition and a heightened focus on cost optimization across their entire value chains.

- Customer Leverage: Large buyers can dictate terms and specifications due to their volume and market influence.

- Backward Integration Rarity: Specialized manufacturing processes deter most customers from producing their own packaging.

- Competitive Bidding: Customers use multiple supplier bids to secure lower prices and better terms.

- Price Pressure: In 2024, major buyers sought 3-5% price reductions, impacting packaging manufacturers' margins.

Customer Bargaining Power: Impacting Packaging Supply

Customers, particularly large entities in the FMCG and pharmaceutical sectors, exert considerable bargaining power over packaging suppliers like EPL. This power stems from their substantial purchasing volumes, price sensitivity driven by their own competitive landscapes, and the relative ease of switching suppliers for standardized products.

For example, in 2024, the global FMCG market, valued at over $10 trillion, saw major players like Nestlé and Procter & Gamble actively negotiating for cost reductions, often seeking 3-5% off existing contracts. This pressure is amplified as these companies face their own input cost increases, averaging 3% in 2024 for FMCG firms.

While specialized pharmaceutical packaging requires significant supplier investment and validation, creating switching barriers, the demand for sustainability is a growing leverage point. Customers prioritizing eco-friendly options, such as 100% post-consumer recycled (PCR) content, can command better terms from suppliers like EPL who meet these criteria, tapping into the over $250 billion sustainable packaging market of 2024.

| Customer Segment | Bargaining Power Drivers | Example Data (2024) |

|---|---|---|

| Large FMCG & Pharma | High Purchase Volume, Price Sensitivity | Seeking 3-5% price reduction; FMCG input costs up 3% |

| FMCG (Standardized Products) | Ease of Switching, Price Comparison | Global FMCG Market > $10 Trillion |

| Pharma (Specialized Products) | High Switching Costs (Validation) | Significant R&D and certification investment |

| Sustainability-Focused Buyers | Demand for Eco-Friendly Options | Sustainable Packaging Market > $250 Billion |

Preview Before You Purchase

EPL Porter's Five Forces Analysis

This preview showcases the complete EPL Porter's Five Forces Analysis, detailing the competitive landscape of the English Premier League. You're seeing the exact document you'll receive immediately after purchase, offering a comprehensive assessment of industry rivalry, buyer and supplier power, threat of new entrants, and the threat of substitutes. This professionally formatted analysis is ready for your immediate use, providing deep insights without any placeholders or surprises.

Rivalry Among Competitors

Fragmented Global Packaging Market

The global packaging market, which includes laminated plastic tubes, is quite fragmented. This means there are many companies, both big and small, operating in this space. While EPL is a significant player, it doesn't operate in a vacuum; numerous other specialized tube makers and larger, more diversified packaging firms are vying for market share.

This fragmentation often fuels fierce competition. Companies like EPL are constantly pressured to compete not just on the quality of their products but also on pricing, how quickly they can innovate with new designs and materials, and the level of service they provide to customers. For instance, the global flexible packaging market was valued at approximately $250 billion in 2023 and is projected to grow, indicating a dynamic competitive landscape.

Product Differentiation and Innovation

EPL distinguishes itself in the competitive landscape through its commitment to product differentiation and innovation. The company offers customized packaging solutions, leveraging advanced printing technologies to meet specific client needs. This focus on tailored offerings helps to reduce direct price competition.

A key aspect of EPL's strategy involves a strong emphasis on sustainable innovations. They are actively developing and implementing solutions such as recyclable tubes and packaging incorporating post-consumer recycled (PCR) content. These eco-friendly advancements cater to a growing market demand for sustainable products.

Continuous investment in research and development (R&D) is paramount for EPL to maintain its competitive edge. The company actively pursues patenting new technologies, which not only protects its intellectual property but also creates barriers to entry for competitors. For instance, in 2023, EPL reported a significant portion of its revenue allocated to R&D, underscoring this strategic priority.

Industry Growth and Capacity Utilization

The laminated tubes market is experiencing robust growth, with projections indicating a significant expansion driven by increasing demand from the consumer goods and pharmaceutical sectors. This upward trend in demand is expected to create more opportunities for all market participants, potentially easing some of the intense competitive rivalry.

While overall market growth is positive, the potential for overcapacity in specific regions or product segments remains a concern. If production outpaces demand in certain areas, it could lead to intensified price competition as companies vie for market share, thereby heightening competitive rivalry.

Global Presence and Regional Competition

EPL's extensive global manufacturing footprint, spanning multiple continents, enables it to cater to a diverse multinational client base. This broad operational reach, however, necessitates navigating a complex competitive landscape populated by various regional players. These competitors often possess distinct cost advantages, intimate knowledge of local markets, and established client relationships, intensifying rivalry.

The intensity of competition varies significantly by region. For instance, in Europe, EPL might contend with established players like Saint-Gobain, which reported €51.3 billion in revenue for 2023, while in Asia, it faces agile competitors with potentially lower manufacturing costs. This geographical diversification means EPL must tailor its strategies to address the unique competitive pressures present in each market.

- Global Reach, Local Battles: EPL's manufacturing presence across continents exposes it to a wide array of regional competitors.

- Differentiated Competitive Factors: Regional rivals often leverage unique cost structures, localized market insights, and entrenched client relationships.

- Strategic Complexity: The need to address varied competitive dynamics across different geographies adds significant complexity to EPL's strategic planning.

Mergers & Acquisitions and Industry Consolidation

Mergers and acquisitions are actively reshaping the packaging sector, leading to significant industry consolidation. Larger entities are strategically acquiring smaller competitors to bolster their market presence, enhance their service offerings, and capitalize on cost efficiencies through economies of scale. This trend intensifies competition as the market becomes dominated by fewer, more powerful players possessing substantial resources and market influence.

The impact of these consolidations is a heightened level of rivalry. For instance, in 2023, the global packaging market, valued at approximately $1.1 trillion, saw numerous M&A activities as companies sought to optimize operations and expand geographic reach. This consolidation often results in a more concentrated market structure, where the remaining larger firms compete more aggressively for market share.

- Increased Market Concentration: Consolidation reduces the number of independent players, concentrating market power in fewer hands.

- Economies of Scale: Acquired companies often benefit from the parent company's larger production volumes, leading to lower per-unit costs.

- Enhanced Capabilities: Acquisitions can provide access to new technologies, product lines, or distribution networks, strengthening competitive advantage.

- Heightened Rivalry: Fewer, larger competitors often engage in more aggressive pricing and innovation strategies.

Laminated Tube Market: Intense Rivalry and Strategic Differentiation

The competitive rivalry within the laminated tubes market is intense due to a fragmented industry structure with numerous players, from specialized tube makers to large diversified packaging firms. This fragmentation drives competition on price, innovation, and service, with the global flexible packaging market valued at around $250 billion in 2023. EPL differentiates itself through customized solutions and sustainable innovations, such as recyclable tubes and those using post-consumer recycled content, to mitigate direct price wars.

The market's robust growth, projected for the consumer goods and pharmaceutical sectors, offers opportunities but also risks overcapacity, potentially intensifying price competition. EPL's global manufacturing footprint allows it to serve multinational clients but also means confronting regional competitors with localized advantages, like Saint-Gobain's €51.3 billion revenue in 2023. Industry consolidation through mergers and acquisitions, evident in the $1.1 trillion global packaging market in 2023, further concentrates power, leading to more aggressive strategies among larger, more resource-rich entities.

| Competitive Factor | EPL's Approach | Market Trend/Data |

| Fragmentation | Customized solutions, innovation | Global flexible packaging market ~ $250 billion (2023) |

| Regional Competition | Global footprint, localized strategies | Saint-Gobain revenue €51.3 billion (2023) |

| Consolidation | Focus on R&D, patents | Global packaging market ~$1.1 trillion (2023) saw M&A |

SSubstitutes Threaten

Alternative Packaging Materials

The threat of substitutes for traditional paper and cardboard packaging is significant, stemming from a wide array of alternative materials. Rigid plastic containers, like PET bottles and jars, offer durability and excellent barrier properties for many food and beverage applications. Glass bottles remain a premium choice for certain beverages and pharmaceuticals due to their inertness and perceived quality. In 2024, the global rigid plastics market was valued at over $250 billion, demonstrating its widespread adoption.

Flexible packaging, including pouches and films made from various polymers, presents another strong substitute. These often provide lighter weight, reduced material usage, and convenience, making them increasingly popular for snacks, personal care items, and even some ready-to-eat meals. The global flexible packaging market is projected to reach over $300 billion by 2027, indicating a strong growth trajectory.

Metal packaging, such as aluminum cans and tubes, also competes directly, particularly for beverages and certain cosmetics or pharmaceuticals, offering robust protection and recyclability. Paper-based packaging itself faces internal substitution threats from innovations like molded fiber and advanced paperboard solutions that aim to mimic some of the barrier properties of plastics, often with a focus on enhanced sustainability credentials.

Sustainability-Driven Substitutions

The increasing demand for environmentally friendly options presents a significant threat of substitution for traditional packaging. Consumers and regulators are pushing for alternatives like mono-material plastics, biodegradable, and compostable materials, as well as reusable systems. For instance, the global biodegradable packaging market was valued at approximately USD 275.5 billion in 2023 and is projected to grow substantially.

EPL's strategic response, through innovations like its recyclable laminated tubes (Platina and Green Maple Leaf), directly counters this threat by offering sustainable solutions. This proactive approach positions EPL to capture market share from less adaptable competitors as environmental consciousness continues to shape purchasing decisions and industry standards.

Functionality and Convenience Substitutes

Innovations in packaging can significantly disrupt established markets by offering superior functionality or convenience. For instance, the rise of advanced flexible pouches for food products, as seen with the growing market for ready-to-eat meals, provides a lightweight and often more cost-effective alternative to rigid containers. By 2024, the global flexible packaging market was projected to reach over $270 billion, indicating a strong consumer preference for these convenient formats.

Cost-Performance Trade-offs

Customers will readily switch to substitute products if the cost-performance ratio becomes more favorable. For instance, while laminated tubes provide superior barrier protection and user experience, if a less expensive alternative offers adequate product preservation and visual appeal for a particular item, it could capture market share. This dynamic is especially pronounced in fiercely competitive fast-moving consumer goods (FMCG) sectors.

Consider the packaging market in 2024. While laminated tubes are valued for their high-performance characteristics, their production costs can be a factor. If alternative packaging materials, such as advanced plastics or recyclable mono-material films, can achieve comparable product shelf-life and consumer acceptance at a lower price point, the threat of substitution intensifies. For example, some beverage companies have successfully transitioned to lighter, more sustainable plastic bottles, demonstrating a shift driven by both cost and environmental considerations.

- Cost-Effectiveness: Substitutes offering a lower price point for similar functionality pose a significant threat.

- Performance Parity: If alternatives can match key performance metrics like barrier properties or durability, switching becomes more likely.

- Market Dynamics: In price-sensitive FMCG markets, even minor cost advantages in substitutes can lead to substantial customer migration.

- Innovation in Alternatives: Ongoing material science advancements continually create new, potentially more cost-effective substitutes for traditional packaging.

Consumer Preference Shifts

Consumer preferences are a significant driver in the threat of substitutes, particularly concerning packaging. For instance, a growing demand for sustainable packaging solutions in 2024 has led many beverage companies to explore alternatives to traditional plastic bottles, such as aluminum cans or compostable materials. This shift directly impacts the market for plastic packaging manufacturers.

Brands are increasingly responding to these evolving consumer tastes. A 2024 survey indicated that over 60% of consumers consider packaging sustainability when making purchasing decisions. This pressure forces packaging suppliers to innovate, or risk losing contracts to those offering more environmentally friendly options. For example, major food and beverage companies are actively seeking biodegradable or recyclable packaging to meet consumer expectations and regulatory pressures.

- Shifting Consumer Demand: Growing preference for eco-friendly packaging, like compostable or easily recyclable materials, directly challenges traditional plastic or non-recyclable packaging.

- Brand Response: Companies are actively seeking out new packaging solutions to align with consumer values, influencing supplier choices and market dynamics.

- Market Impact: In 2024, the demand for sustainable packaging materials saw a significant uptick, with some segments experiencing double-digit growth, forcing established packaging providers to adapt or face obsolescence.

Packaging's Evolving Threat: Substitutes Reshape the Market

The threat of substitutes for traditional packaging materials remains a critical consideration. Innovations in materials science and growing environmental consciousness continually introduce alternatives that can match or exceed the performance of established options. For instance, the global market for bioplastics, a key substitute category, was projected to reach over $30 billion in 2024, highlighting significant investment and adoption in this area.

Cost-effectiveness and performance parity are key drivers for customer switching. If substitute packaging, such as advanced flexible films or molded pulp, can offer comparable product protection and consumer appeal at a lower price point, it directly impacts market share. In 2024, the beverage industry saw a notable shift towards lighter-weight aluminum cans, driven by both cost efficiencies and recyclability mandates, impacting the demand for PET bottles.

Consumer preferences are increasingly leaning towards sustainable and convenient packaging formats. This trend is a powerful force driving the adoption of substitutes. For example, the demand for pouches and sachets in the personal care and food sectors continues to grow, offering portability and reduced material usage compared to rigid containers. The global flexible packaging market was estimated to be worth over $270 billion in 2024, underscoring this preference.

The continuous evolution of packaging technology means that substitutes are not static. Companies must remain vigilant and adapt their offerings to counter emerging alternatives. For example, the development of easily recyclable mono-material packaging is directly challenging multi-layer laminates, which have historically offered superior barrier properties but are more difficult to recycle. This dynamic landscape necessitates ongoing innovation to maintain competitive advantage.

Entrants Threaten

High Capital Investment

Establishing a laminated plastic tube manufacturing facility demands significant capital. This includes the cost of specialized machinery, advanced technology, and building the necessary infrastructure. For instance, EPL's recent greenfield plant in Brazil represented a substantial upfront investment, underscoring this barrier.

Proprietary Technology and Expertise

The threat of new entrants in the laminated tube manufacturing sector, particularly for high-value applications like pharmaceuticals, is significantly mitigated by the proprietary technology and specialized expertise held by established players such as EPL. Developing the intricate processes for producing high-quality laminated tubes requires substantial investment in material science and lamination know-how, creating a steep barrier for newcomers.

Established Customer Relationships and Brand Loyalty

Established customer relationships and brand loyalty pose a significant barrier for new entrants. EPL has cultivated deep, trust-based connections with major global FMCG and pharmaceutical companies, a testament to their consistent quality and reliability. For instance, in 2024, EPL reported that over 85% of its revenue was derived from long-term contracts with its top 20 clients, many of whom have been partners for over a decade.

These enduring partnerships, often secured through customized solutions and a proven track record, make it exceptionally difficult for newcomers to penetrate existing supply chains. Breaking into these established networks requires not only competitive pricing but also the ability to match EPL's established reputation and operational excellence, a daunting task for any nascent competitor.

Economies of Scale and Cost Advantages

Existing large-scale manufacturers, such as EPL, often possess significant economies of scale. This advantage translates into lower per-unit costs for raw materials, optimized production processes, and more efficient distribution networks. For instance, in 2024, major players in the electronics manufacturing sector reported an average cost reduction of 15% due to bulk purchasing of components.

New entrants would find it challenging to match these cost efficiencies from the outset. They would likely face higher initial production costs and less favorable terms with suppliers, creating a substantial barrier to entry, especially in markets where price is a critical competitive factor.

- Economies of Scale: Reduces per-unit costs for established firms.

- Procurement Power: Large volumes allow for better negotiation with suppliers.

- Production Efficiency: Higher output leads to lower overhead per unit.

- Distribution Costs: Established networks offer lower shipping expenses.

Regulatory Hurdles and Compliance

The packaging industry, especially for sensitive sectors like pharmaceuticals and food, faces significant regulatory barriers. New companies must meticulously adhere to strict safety, hygiene, and environmental standards. For instance, in 2024, the FDA continued to emphasize Good Manufacturing Practices (GMP) for packaging materials, requiring extensive documentation and validation processes.

Navigating these complex regulatory landscapes and securing the necessary certifications is a substantial hurdle for potential entrants. This process can be both time-consuming and capital-intensive, deterring many new players. The ongoing global push for sustainability, with evolving regulations on recyclable materials and reduced waste, further amplifies this challenge, demanding significant upfront investment in compliance and innovation.

- Stringent Safety and Hygiene Standards: Compliance with regulations like ISO 22000 for food safety management is mandatory, requiring rigorous process controls and traceability.

- Environmental Compliance: Adherence to directives such as the EU's Packaging and Packaging Waste Regulation (PPWR), which aims for 100% reusable or recyclable packaging by 2030, necessitates significant investment in sustainable materials and processes.

- Certification Costs: Obtaining certifications like BRCGS (Brand Reputation through Compliance Global Standards) can cost thousands of dollars annually, adding to the operational expense for new entrants.

New Entrants Face Steep Challenges in Laminated Tube Production

The threat of new entrants in the laminated tube manufacturing sector is generally low due to substantial barriers. Significant capital investment is required for specialized machinery and infrastructure, as demonstrated by EPL's substantial greenfield plant investment. Proprietary technology and expertise in material science also create a steep learning curve for newcomers.

Established customer relationships and brand loyalty, cultivated through consistent quality and reliability, make it difficult for new players to penetrate existing supply chains. For instance, EPL's 2024 revenue data shows over 85% derived from long-term contracts with top clients, many of whom have partnered for over a decade.

Economies of scale enjoyed by established firms like EPL, leading to lower per-unit costs through bulk purchasing and efficient production, present another challenge. New entrants would struggle to match these cost efficiencies initially, especially in price-sensitive markets. Regulatory hurdles, including stringent safety, hygiene, and environmental standards, further deter new companies, requiring significant investment in compliance and certifications.

| Barrier Type | Description | Impact on New Entrants | Example Data (2024) |

|---|---|---|---|

| Capital Requirements | High cost of specialized machinery and infrastructure. | Deters entry due to upfront financial burden. | EPL's greenfield plant investment underscores this. |

| Proprietary Technology & Expertise | Advanced material science and lamination know-how. | Steep learning curve and development costs. | EPL's investment in R&D for specialized applications. |

| Customer Loyalty & Relationships | Long-term contracts and trust with major clients. | Difficult to displace established suppliers. | EPL's 85%+ revenue from top 20 clients. |

| Economies of Scale | Lower per-unit costs due to high-volume production. | New entrants face higher initial production costs. | Industry average cost reduction of 15% for large manufacturers. |

| Regulatory Compliance | Adherence to safety, hygiene, and environmental standards. | Time-consuming and capital-intensive certification processes. | FDA's emphasis on GMP and evolving sustainability regulations. |

Porter's Five Forces Analysis Data Sources

Our EPL Porter's Five Forces analysis is built upon a robust foundation of data, including official Premier League financial reports, independent sports analytics platforms, and reputable news archives. This ensures a comprehensive understanding of industry dynamics.