Emperor Watch & Jewellery Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Emperor Watch & Jewellery Bundle

From Overview to Strategy Blueprint

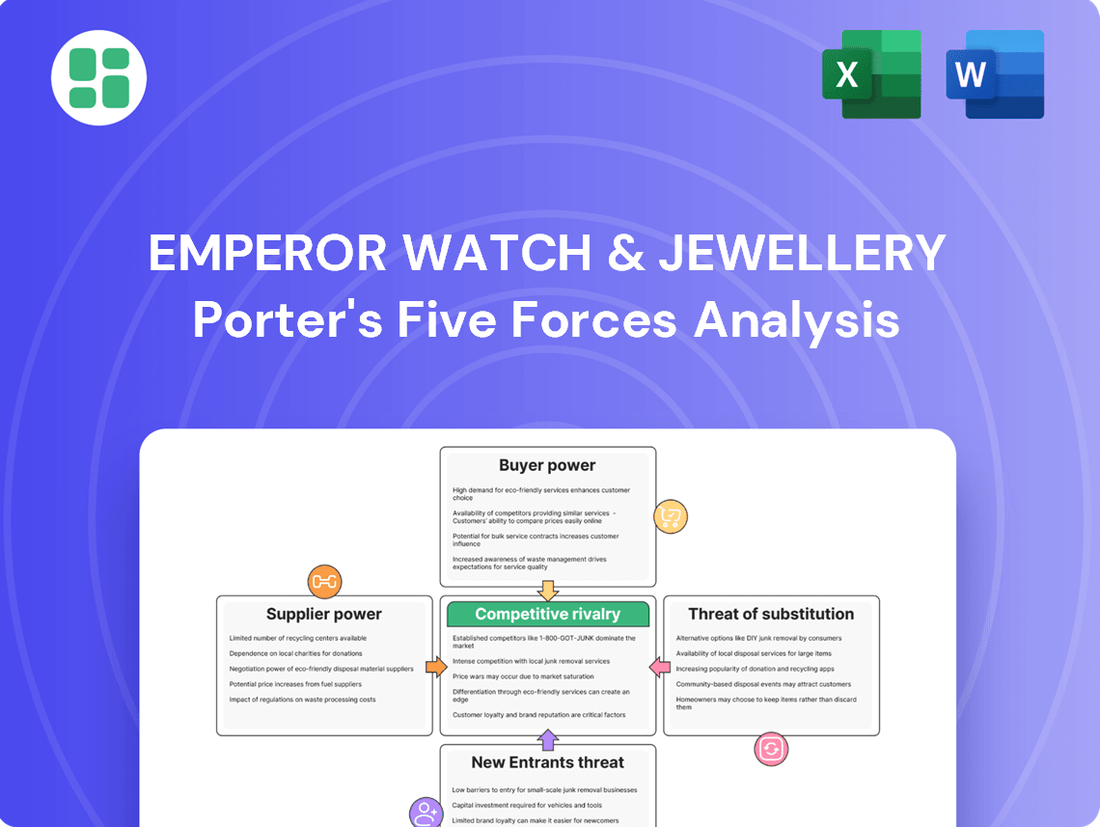

Emperor Watch & Jewellery navigates a competitive landscape shaped by powerful buyers and the constant threat of substitutes. Understanding the intensity of these forces is crucial for sustained success.

The complete report reveals the real forces shaping Emperor Watch & Jewellery’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Supplier Concentration and Uniqueness

Emperor Watch & Jewellery's dependence on a select group of prestigious luxury watch brands, including names like Rolex, Patek Philippe, and Cartier, along with high-end jewelry makers, is a critical factor. These suppliers, due to their strong brand recognition and the inherent desirability of their exclusive products, possess substantial bargaining power. This limited supplier base often means Emperor Watch & Jewellery has less room to negotiate favorable terms, impacting its cost structure and product availability.

Switching Costs for Emperor

Switching costs for Emperor Watch & Jewellery are notably high. This is largely due to the deep-seated relationships and exclusive authorized dealership agreements necessary to stock prestigious watch and jewelry brands. Losing a key brand, for instance, could significantly diminish Emperor's product range and customer draw, as finding immediate, comparable replacements is a considerable challenge.

The process of cultivating new partnerships with other high-end brands is not only time-consuming but also requires substantial capital investment. This barrier reinforces the power of existing suppliers, as Emperor must carefully consider the implications before any action that might jeopardize these crucial alliances.

Threat of Forward Integration by Suppliers

Many luxury watch manufacturers are increasingly establishing their own monobrand boutiques, directly challenging multi-brand retailers such as Emperor Watch & Jewellery. This forward integration by suppliers significantly curtails Emperor's autonomy in distribution and can restrict their access to sought-after, exclusive watch collections or advantageous pricing agreements.

This strategic shift by the brands themselves amplifies their direct market presence, consequently diminishing the leverage and influence previously held by retailers like Emperor. For instance, in 2024, major luxury conglomerates reported a substantial increase in their direct-to-consumer sales channels, often at the expense of traditional wholesale partners.

Importance of Supplier's Product to Emperor's Business

The watches and jewelry sourced from prestigious luxury brands form the absolute bedrock of Emperor Watch & Jewellery's entire operation. These highly desirable items are not merely inventory; they are the very essence of the company's appeal to its discerning clientele.

This critical reliance on iconic brands, such as Rolex or Patek Philippe, inherently grants these suppliers considerable leverage. This power translates directly into their ability to influence pricing structures, dictate supply volumes, and even shape marketing collaborations, all of which directly impact Emperor's profitability and market standing.

- Core Product Dependency: Emperor's value proposition as a premier luxury retailer is inextricably linked to its access to sought-after timepieces and exquisite jewelry from leading global brands.

- Supplier Pricing Power: The exclusivity and demand for these luxury goods allow suppliers to command premium prices, impacting Emperor's cost of goods sold and gross margins.

- Supply Chain Vulnerability: Any disruption in the supply of these core products, whether due to production issues or brand-specific decisions, can significantly affect Emperor's sales and inventory levels.

- Marketing and Brand Alignment: Suppliers often dictate marketing strategies and brand presentation, limiting Emperor's autonomy in its promotional activities and requiring alignment with brand image.

Availability of Substitute Suppliers

The availability of substitute suppliers significantly impacts the bargaining power of suppliers in the watch and jewelry industry, particularly for premium brands like Emperor Watch & Jewellery. While the global market boasts many watch and jewelry manufacturers, the pool of suppliers offering truly exclusive, high-demand luxury components and finished goods that match Emperor's premium positioning is considerably smaller. This scarcity limits Emperor's leverage if a critical supplier attempts to dictate terms or cease operations.

The market for ultra-luxury watches and jewelry continues its strong performance, a trend expected to persist. For instance, the global luxury jewelry market was valued at approximately USD 73.5 billion in 2023 and is projected to grow to USD 113.5 billion by 2030, with a compound annual growth rate (CAGR) of 6.4%. This sustained demand for high-end products reinforces the power of those suppliers who can consistently deliver exceptional quality and unique designs, making it harder for brands like Emperor to find readily available, equally desirable alternatives.

- Limited Luxury Alternatives: The number of suppliers capable of producing materials and components for the ultra-luxury segment, meeting Emperor's stringent quality and design standards, is restricted.

- Supplier Dependence: If a key supplier for rare gemstones or specialized watch movements is lost, finding an immediate, comparable replacement is challenging, granting that supplier increased bargaining power.

- Market Growth Reinforces Power: The robust growth in the ultra-luxury market (e.g., projected CAGR of 6.4% for luxury jewelry through 2030) means that suppliers to this segment are in high demand, enhancing their negotiating position.

- Brand Exclusivity: The very nature of luxury often relies on exclusivity, meaning suppliers who control unique craftsmanship or access to rare materials hold significant sway.

Luxury Suppliers Hold the Reins on Retailer's Fate

Emperor Watch & Jewellery faces significant supplier bargaining power due to its reliance on a limited number of prestigious luxury brands. These suppliers, controlling highly desirable products, can dictate terms, impacting Emperor's costs and product availability.

The exclusivity and high demand for luxury watches and jewelry grant suppliers considerable leverage, allowing them to influence pricing and supply volumes. This is further amplified by the growing trend of brands establishing their own monobrand boutiques, reducing Emperor's distribution autonomy.

Finding comparable luxury alternatives is difficult, as the pool of suppliers meeting Emperor's stringent quality and design standards for the ultra-luxury segment is small. The robust growth in this market, with the global luxury jewelry market projected to reach USD 113.5 billion by 2030, further strengthens supplier negotiating positions.

| Factor | Impact on Emperor Watch & Jewellery | Supplier Leverage |

| Limited Supplier Base | Reduced negotiation power, potential supply disruptions | High |

| High Switching Costs | Difficulty in finding comparable replacements, dependence on existing relationships | High |

| Supplier Forward Integration | Diminished distribution autonomy, potential restricted access to products | High |

| Market Growth (Luxury Segment) | Increased demand for supplier products, enhanced negotiating position | High |

What is included in the product

This analysis of Emperor Watch & Jewellery's competitive environment reveals the intensity of rivalry, the bargaining power of suppliers and buyers, and the threats posed by new entrants and substitutes.

Instantly grasp the competitive landscape of Emperor Watch & Jewellery with a clear, one-sheet summary of all five forces, enabling rapid strategic adjustments.

Customers Bargaining Power

Customer Price Sensitivity

Customer price sensitivity is a growing concern for luxury brands like Emperor Watch & Jewellery. While affluent customers still exist, they are becoming more thoughtful about their purchases. This is particularly evident in markets like China, where consumer sentiment has been somewhat subdued.

This heightened sensitivity means customers are more likely to compare prices across different regions and even consider purchasing overseas if they find a better deal. For instance, reports from late 2023 and early 2024 indicated that luxury goods consumers in China were actively seeking out lower prices, sometimes delaying purchases or exploring alternative purchasing channels. This can significantly increase their bargaining power.

Availability of Customer Choices

The bargaining power of customers for Emperor Watch & Jewellery is significantly influenced by the sheer availability of choices. In 2024, the luxury watch and jewelry market, both new and pre-owned, offers a vast array of brands and retailers. Customers can easily compare prices and offerings from authorized dealers, brand-specific boutiques, and increasingly, reputable online marketplaces. This broad accessibility means consumers have multiple avenues to acquire desired items, directly impacting their leverage in negotiations or their willingness to pay premium prices.

Information Availability and Transparency

The digital age has dramatically shifted the luxury market, with customers now enjoying unparalleled access to product details, pricing, and peer reviews. This surge in information availability, driven by e-commerce, means consumers can easily compare Emperor Watch & Jewellery's offerings against competitors, seeking the most advantageous value.

This transparency erodes the traditional information advantage held by retailers, significantly increasing the bargaining power of customers. For instance, in 2023, online luxury sales reached an estimated $42.5 billion, with a significant portion driven by informed consumers actively comparing options across various platforms.

Luxury as an Investment and Status Symbol

While luxury goods are typically discretionary purchases, high-end watches and jewelry often transcend this classification, being viewed as tangible investments and potent status symbols, especially within Asian markets. This elevated perception can significantly bolster demand for particular, often scarce, items. For instance, the global luxury watch market was valued at approximately $50 billion in 2023, with a projected compound annual growth rate (CAGR) of over 5% through 2028, indicating sustained strong demand for certain pieces.

This strong demand for desirable, limited-edition luxury timepieces and jewelry can paradoxically reduce the bargaining power of individual customers. When a piece is highly coveted and supply is constrained, customers are less likely to negotiate prices downwards, as they recognize the scarcity and potential for future appreciation. In 2024, reports indicated that certain highly sought-after watch models from brands like Rolex and Patek Philippe continued to trade at premiums well above their retail prices on the secondary market, underscoring the limited bargaining power for these specific items.

- Investment Appeal: Luxury watches and jewelry are increasingly seen as alternative investments, similar to art or fine wine, with potential for capital appreciation.

- Status Symbolism: Ownership of prestigious brands and rare items confers social standing and recognition, driving demand irrespective of price sensitivity for some buyers.

- Limited Supply: Many luxury brands intentionally limit production of certain models to maintain exclusivity and desirability, thereby reducing individual customer leverage.

- Secondary Market Premiums: The robust secondary market for certain luxury items, where they often trade at a premium, further demonstrates that customers are willing to pay more, diminishing their bargaining power.

Customer Loyalty and Brand Affinity

Empowerment through enhanced customer relationship management is a key strategy for Emperor Watch & Jewellery to build lasting loyalty. This focus aims to reduce the bargaining power customers might otherwise exert by fostering a strong connection with the retailer itself.

However, the inherent brand affinity customers hold for specific luxury watch and jewelry marques, such as Rolex or Patek Philippe, presents a significant counterpoint. This means that even with excellent service, a customer’s ultimate decision to purchase is often driven by the desirability of the brand, potentially leading them to switch retailers if their preferred brand is unavailable elsewhere.

- Brand Dominance: Customer loyalty is often tied more strongly to the manufacturer's brand than to the retailer.

- Retailer Switching: High brand affinity can lead customers to choose retailers based on brand availability, not necessarily existing relationships.

- Mitigation Challenges: While CRM efforts can help, they may not fully overcome the pull of globally recognized luxury brands.

Customer Power in Luxury: A Dual Reality

While customers have increased bargaining power due to greater price transparency and product availability in 2024, the luxury watch and jewelry market also sees certain highly coveted items trading at premiums. This indicates that for specific, limited-edition pieces, customer bargaining power is significantly reduced, as demonstrated by the continued strong secondary market for brands like Rolex. For instance, in early 2024, certain sought-after models continued to command prices well above retail, reflecting scarcity and investment appeal rather than price sensitivity.

| Factor | Impact on Bargaining Power | Supporting Data (2023-2024) |

|---|---|---|

| Price Sensitivity & Comparison | Increases bargaining power | Luxury consumers in China actively sought lower prices; online luxury sales reached $42.5 billion in 2023, driven by informed buyers. |

| Availability of Choices | Increases bargaining power | Vast array of brands and retailers (authorized dealers, boutiques, online marketplaces) available in 2024. |

| Information Transparency | Increases bargaining power | Easy access to product details, pricing, and reviews online erodes retailer information advantage. |

| Investment Appeal & Status Symbolism | Decreases bargaining power for desirable items | Global luxury watch market valued at ~$50 billion in 2023, with strong demand for specific pieces. |

| Limited Supply & Brand Affinity | Decreases bargaining power for desirable items | Limited production of exclusive models; highly sought-after watches trade at premiums on the secondary market. |

Preview the Actual Deliverable

Emperor Watch & Jewellery Porter's Five Forces Analysis

This preview showcases the complete Emperor Watch & Jewellery Porter's Five Forces Analysis, offering a thorough examination of industry competition, buyer power, supplier leverage, threat of new entrants, and the intensity of substitute products. You are viewing the exact, professionally formatted document that will be instantly available for download upon purchase, ensuring transparency and immediate utility for your strategic planning.

Rivalry Among Competitors

Number and Diversity of Competitors

The luxury watch and jewellery market in Greater China and Southeast Asia is quite crowded. Think of established local powerhouses like Chow Tai Fook, which reported a revenue of HKD 24.2 billion in fiscal year 2024, alongside global luxury groups such as Richemont and LVMH, which also have a significant presence.

Adding to this, many high-end brands operate their own dedicated boutiques, directly engaging with consumers. This rich mix of local, international, and direct-to-consumer competitors creates a fiercely competitive environment where brands constantly vie for market share and customer attention.

Market Growth Rate and Conditions

The luxury market in mainland China saw a significant contraction in 2024, with reports indicating an 18-20% decline. This downturn is particularly challenging for the watch and jewellery sectors.

Looking ahead to 2025, the outlook suggests a flat market, meaning no significant growth is anticipated. This stagnant environment naturally fuels more intense rivalry among businesses vying for market share.

Companies are feeling the pressure as consumer spending increasingly shifts towards international markets, further exacerbating the competitive landscape within China.

Product Differentiation and Brand Loyalty

Emperor Watch & Jewellery differentiates itself through a mix of self-designed jewelry and a substantial offering of European-made watches. For multi-brand retailers like Emperor, product differentiation often hinges on factors beyond the core product itself, such as the quality of customer service, the overall store ambiance, and the breadth and depth of available inventory, as the watches are sourced from external, established brands.

The competitive landscape is significantly shaped by the strong brand equity of the watch manufacturers Emperor carries. Customers often choose Emperor based on their desire for specific, well-recognized watch brands, meaning Emperor's ability to secure and showcase these sought-after labels directly impacts its competitive standing and customer loyalty.

High Fixed Costs and Exit Barriers

Operating a luxury retail network, such as Emperor Watch & Jewellery, is characterized by significant fixed costs. These include the expense of prime retail locations, maintaining a substantial inventory of high-value goods, and employing a skilled sales force. For instance, prime retail rents in Hong Kong, a key market for luxury goods, can easily reach tens of thousands of US dollars per month for a single store.

These substantial fixed costs, coupled with the considerable investment required to establish and maintain a luxury brand image, erect high exit barriers. Companies find it difficult and financially punitive to simply close down operations. This reality forces existing players to intensely compete for market share rather than withdraw, as the cost of exiting is often prohibitive.

The competitive landscape is thus shaped by this dynamic:

- High Fixed Costs: Prime retail leases, extensive inventory, and specialized staff contribute to a high cost structure.

- Brand Investment: Maintaining a luxury image requires ongoing marketing and premium store experiences.

- Exit Barriers: The significant capital tied up in leases, inventory, and brand equity makes exiting the market challenging.

- Intensified Rivalry: Companies are compelled to compete aggressively to recoup their investments and remain viable.

Strategic Objectives of Competitors

Competitors are actively pursuing diverse strategies to thrive in a demanding market. This includes significant investments in digital transformation to reach a wider audience and improve online sales channels. Many are also focusing on enhancing the overall customer experience, both online and in-store, recognizing its importance in brand loyalty.

Furthermore, there's a trend towards consolidating physical retail footprints, optimizing store locations for maximum impact and efficiency. A key differentiator for many is a renewed focus on premiumization, offering exclusive collections and bespoke services to attract discerning clientele. For instance, in 2024, many luxury watch brands saw increased demand for limited-edition pieces, driving up average transaction values.

Emperor Watch & Jewellery's own strategic moves, such as targeted acquisitions and efforts to bolster its jewelry business, directly mirror this heightened competitive intensity. These actions are essential for maintaining market share and capturing new growth opportunities in a dynamic landscape.

- Digital Transformation: Brands are investing heavily in e-commerce platforms and digital marketing.

- Customer Experience Enhancement: Focus on personalized service and omnichannel strategies.

- Footprint Consolidation: Optimizing physical store networks for efficiency and impact.

- Premiumization: Emphasis on high-value products and exclusive offerings.

Luxury Market Showdown: Asia's Intense Watch & Jewellery Battle

The competitive rivalry within the luxury watch and jewellery market, particularly in Greater China and Southeast Asia, is intense. This is driven by the presence of major local players like Chow Tai Fook, which achieved HKD 24.2 billion in revenue in fiscal year 2024, and global giants such as Richemont and LVMH. The market experienced a notable contraction in mainland China in 2024, with an estimated 18-20% decline, and a flat outlook for 2025, intensifying the struggle for market share.

High fixed costs associated with prime retail locations, substantial inventory, and skilled staff, combined with significant brand investment, create high exit barriers. This financial reality compels existing companies to compete fiercely to recoup investments rather than withdraw, leading to a dynamic where brands like Emperor Watch & Jewellery must differentiate through service, ambiance, and brand partnerships to remain viable.

Competitors are actively investing in digital transformation and enhancing customer experiences to capture market share in this challenging environment. Many are also focusing on premiumization, offering exclusive collections and bespoke services, as seen with the increased demand for limited-edition luxury watches in 2024, which boosted average transaction values.

| Company | Market Presence | 2024 Revenue (approx.) | Key Strategy |

|---|---|---|---|

| Chow Tai Fook | Greater China, Southeast Asia | HKD 24.2 billion (FY24) | Extensive retail network, diverse product offerings |

| Richemont | Global | EUR 15.8 billion (FY24) | Portfolio of prestigious watch and jewellery brands |

| LVMH | Global | EUR 86.2 billion (FY24) | Diversified luxury portfolio, strong brand management |

| Emperor Watch & Jewellery | Greater China, Southeast Asia | HKD 2.1 billion (FY24) | Multi-brand retail, self-designed jewellery, European watches |

SSubstitutes Threaten

Alternative Luxury Goods

Consumers with substantial disposable income often consider a range of luxury options beyond just watches and jewelry. For instance, in 2024, the global luxury goods market, encompassing fashion, automotive, and travel, continued its robust growth, indicating that discretionary spending is spread across various premium sectors. This broad competition for consumer attention and expenditure means that a luxury watch purchase might be forgone in favor of a high-end automobile or an exclusive travel experience, directly impacting demand for traditional luxury items.

Emergence of Smartwatches and Wearable Technology

While traditional luxury timepieces from brands like Emperor Watch & Jewellery are prized for their craftsmanship and potential as investments, the rise of smartwatches presents a compelling substitute, particularly for consumers prioritizing functionality. For instance, Apple Watch sales in 2024 are projected to continue their strong trajectory, with estimates suggesting over 50 million units sold globally, offering advanced features like health tracking and seamless connectivity that appeal to a broad demographic.

Furthermore, the luxury smart jewelry market is experiencing notable growth, attracting consumers who desire a blend of cutting-edge technology and sophisticated design. This segment, though niche, directly competes for disposable income that might otherwise be allocated to high-end traditional watches, indicating a shift in consumer preferences towards integrated tech experiences.

Growth of the Pre-Owned and Vintage Market

The pre-owned luxury watch market is experiencing significant growth, presenting a strong substitute for new timepieces. This surge is fueled by consumers seeking investment opportunities and a more sustainable approach to luxury consumption. For instance, the global pre-owned luxury watch market was valued at approximately USD 10.6 billion in 2023 and is projected to reach USD 18.5 billion by 2030, growing at a CAGR of 8.3%.

This expanding secondary market provides consumers with access to sought-after brands and models, often at more accessible price points compared to brand-new offerings. This availability directly impacts the sales potential of new luxury watches, as buyers may opt for pre-owned alternatives to acquire desired pieces or diversify their collections.

Lab-Grown Diamonds and Alternative Materials

Lab-grown diamonds are increasingly becoming a viable substitute for natural diamonds in the fine jewelry sector. Their growing acceptance is fueled by concerns over ethical sourcing and often more accessible pricing, directly impacting the demand for mined diamonds.

The market for lab-grown diamonds has seen significant growth. For instance, in 2023, the global lab-grown diamond market was valued at approximately $13.0 billion, with projections indicating a compound annual growth rate (CAGR) of around 9.5% through 2030. This expansion directly challenges the market share of traditional diamond producers.

- Market Growth: The lab-grown diamond market is expanding rapidly, offering consumers a more affordable and ethically sourced alternative.

- Price Differential: Lab-grown diamonds can be priced 30-50% lower than natural diamonds of comparable quality, making them an attractive substitute.

- Consumer Acceptance: Consumer perception is shifting, with a greater willingness to consider lab-grown diamonds for engagement rings and other fine jewelry.

Non-Luxury Alternatives for Timekeeping or Adornment

The threat of substitutes for Emperor Watch & Jewellery is moderate, particularly for basic timekeeping functions. Consumers increasingly rely on smartphones, with global smartphone penetration reaching over 85% by early 2024, to tell time, diminishing the necessity of a dedicated watch for this purpose alone.

For adornment, the market offers numerous low-cost alternatives. Fast fashion jewelry and costume jewelry brands, which represent a significant portion of the accessories market, provide readily available and inexpensive options for consumers seeking decorative items. The global costume jewelry market was valued at approximately USD 30 billion in 2023 and is projected to grow, indicating a strong substitute presence.

- Ubiquitous Smartphone Timekeeping: Over 85% global smartphone penetration by early 2024 offers a free and convenient alternative for basic timekeeping.

- Affordable Adornment Options: The global costume jewelry market, valued at ~USD 30 billion in 2023, provides low-cost substitutes for decorative purposes.

- Divergence in Value Proposition: While substitutes exist, they do not replicate the luxury segment's emphasis on exclusivity, brand heritage, and superior craftsmanship.

Luxury Market Faces Tech & Pre-Owned Disruptions

The threat of substitutes for Emperor Watch & Jewellery is intensified by the proliferation of smart devices and the growing appeal of the pre-owned luxury market. While smartphones offer basic timekeeping, smartwatches are increasingly sophisticated, with Apple Watch sales projected to exceed 50 million units globally in 2024, providing advanced functionalities that appeal to a broad consumer base. This technological convergence challenges traditional watchmakers by offering integrated convenience and features beyond mere time display.

| Substitute Category | Key Characteristics | Market Data/Projections (2024/Near-term) | Impact on Emperor Watch & Jewellery |

|---|---|---|---|

| Smartwatches | Functionality, connectivity, health tracking | Apple Watch sales > 50 million units (2024 projection) | Addresses basic timekeeping and adds advanced features, diverting some consumer interest. |

| Pre-owned Luxury Watches | Accessibility, investment potential, sustainability | Global pre-owned market valued at ~USD 10.6 billion (2023), projected growth to USD 18.5 billion by 2030 (8.3% CAGR) | Offers a more affordable entry into luxury timepieces, potentially reducing demand for new items. |

| Lab-Grown Diamonds | Ethical sourcing, price advantage, comparable aesthetics | Global market valued at ~$13.0 billion (2023), projected CAGR of ~9.5% through 2030 | Directly competes with natural diamonds, impacting jewelry sales segments. |

Entrants Threaten

High Capital Requirements

Entering the luxury watch and jewelry retail sector, as exemplified by Emperor Watch & Jewellery, demands significant upfront capital. This includes securing prime retail spaces in high-traffic, affluent areas, which can involve substantial leasehold improvements and rental deposits. For instance, prime retail rents in Hong Kong, a key market for luxury goods, can easily run into tens of thousands of dollars per month per square foot.

Furthermore, establishing a credible inventory of high-value timepieces and fine jewelry necessitates a considerable financial outlay. Brands like Rolex or Patek Philippe, often carried by luxury retailers, represent millions in inventory value per store. The cost of acquiring and maintaining such a diverse and high-quality stock, coupled with the need for secure storage and insurance, creates a high financial barrier.

Sophisticated store design and luxurious customer experiences are also critical in the luxury segment. This involves investing in high-end fixtures, lighting, security systems, and potentially even private viewing rooms. These elements, while crucial for brand perception and customer engagement, add considerably to the initial capital expenditure required to compete effectively.

Brand Reputation and Trust

Building a strong brand reputation and cultivating deep customer trust in the luxury watch and jewelry market is a monumental undertaking, often requiring decades, if not centuries, of unwavering commitment to exceptional quality and unparalleled service. Newcomers simply do not possess this deeply ingrained heritage, which is a crucial element for drawing in and holding onto discerning, affluent clientele who value provenance and proven excellence.

Access to Exclusive Supplier Networks

Securing authorized dealership agreements with top-tier luxury watch brands like Rolex and Patek Philippe presents a formidable barrier for new entrants. These coveted partnerships are notoriously difficult to obtain due to extremely limited distribution channels, rigorous vetting processes, and the deeply entrenched relationships these brands have cultivated with their existing, long-standing retailers.

Regulatory and Compliance Hurdles

The luxury jewelry sector, particularly for established players like Emperor Watch & Jewellery, faces significant regulatory and compliance challenges that act as a barrier to new entrants. Operating across Greater China and Southeast Asia means grappling with diverse and often changing rules. These can include varying import duties, complex tax structures, and specific consumer protection laws that differ from one market to another.

New businesses entering this space must invest heavily in understanding and adhering to these multifaceted regulations. For instance, navigating the import duties on precious metals and gemstones, which can range from single digits to over 20% depending on the specific country and material, requires dedicated expertise and resources. Similarly, compliance with differing product safety standards and labeling requirements across these regions adds another layer of complexity.

- Complex Import Duties: Tariffs on luxury goods and raw materials can significantly impact a new entrant's cost structure.

- Varying Taxation Laws: Navigating corporate taxes, VAT, and sales taxes across multiple jurisdictions presents a compliance challenge.

- Consumer Protection Regulations: Adhering to diverse consumer rights, warranty, and product disclosure laws is essential.

- Anti-Money Laundering (AML) and Know Your Customer (KYC): The high value of transactions in the jewelry industry necessitates strict adherence to financial regulations.

Intense Competition from Established Players

The threat of new entrants for Emperor Watch & Jewellery is significantly mitigated by the dominance of established players. These incumbents possess extensive retail networks, boasting strong brand recognition and deeply cultivated customer relationships. For instance, in the luxury watch market, brands like Rolex and Patek Philippe have decades of brand equity, making it incredibly challenging for newcomers to gain traction. Newcomers would face an uphill battle to capture market share from these experienced and resilient competitors, who can leverage their scale and existing customer loyalty to their advantage.

New entrants would need substantial capital to even begin competing. Consider the significant investment required to establish a physical retail presence in prime locations, comparable to the prime locations occupied by established luxury retailers. Furthermore, building brand awareness and trust in a market where heritage and craftsmanship are highly valued demands considerable marketing expenditure and time. In 2024, the global luxury goods market, which includes high-end watches and jewelry, continued to show resilience, with key players reporting robust sales, underscoring the difficulty for new, unproven brands to penetrate this segment.

- Dominant Market Share: Established brands often hold substantial market share, making it difficult for new entrants to gain a foothold.

- High Capital Requirements: Significant investment is needed for retail presence, brand building, and inventory.

- Brand Loyalty and Reputation: Decades of building trust and quality create strong customer loyalty that is hard to replicate.

- Economies of Scale: Existing players benefit from economies of scale in sourcing, manufacturing, and marketing, leading to cost advantages.

Why New Entrants Struggle in Luxury Watch & Jewelry

The threat of new entrants in the luxury watch and jewelry sector, as exemplified by Emperor Watch & Jewellery, is considerably low due to exceptionally high barriers to entry. These include the immense capital required for prime retail locations and substantial, high-value inventory, alongside the challenge of securing authorized dealerships with prestigious brands. Furthermore, building the necessary brand reputation and navigating complex, multi-jurisdictional regulations present formidable obstacles.

| Barrier Type | Description | Impact on New Entrants |

|---|---|---|

| Capital Requirements | Securing prime retail space and high-value inventory necessitates millions in upfront investment. For example, prime Hong Kong retail rents can exceed tens of thousands of dollars per month per square foot. | Very High |

| Brand Reputation & Trust | Decades of commitment to quality and service are needed to build trust with affluent clientele. Newcomers lack this established heritage. | Very High |

| Dealership Agreements | Obtaining authorized partnerships with top brands like Rolex is extremely difficult due to limited distribution and rigorous vetting. | Very High |

| Regulatory Compliance | Navigating diverse import duties, taxes, and consumer laws across Greater China and Southeast Asia demands significant expertise and resources. Import duties on precious materials can range from single digits to over 20%. | High |

Porter's Five Forces Analysis Data Sources

Our Emperor Watch & Jewellery Porter's Five Forces analysis is built upon a foundation of comprehensive data, including industry-specific market research reports from firms like Euromonitor and Statista, alongside publicly available financial statements and annual reports from Emperor Watch & Jewellery and its key competitors.