China National Building Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

China National Building Bundle

Don't Miss the Bigger Picture

China National Building faces intense competition, with significant bargaining power from both suppliers and buyers in the construction materials sector. The threat of new entrants is moderate, but the availability of substitutes poses a considerable challenge to their market position.

The complete report reveals the real forces shaping China National Building’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Diverse Material Sourcing

CSCEC's immense scale and varied project types enable it to tap into a broad spectrum of material suppliers, diminishing reliance on any single provider. This expansive network grants considerable influence in negotiating favorable prices and conditions for critical materials such as steel, cement, and aggregates, whether for domestic or international projects.

In 2024, China's construction sector, a key market for CSCEC, saw significant activity. For instance, cement production in China remained robust, with output figures consistently high throughout the year, providing CSCEC with ample sourcing options. Similarly, steel prices, while subject to market fluctuations, generally offered competitive rates due to the sheer volume CSCEC procures.

By diversifying its supplier base, CSCEC can secure more competitive pricing and effectively buffer against potential disruptions like localized supply shortages or transportation challenges, ensuring continuity and cost-efficiency in its operations.

Standardized Materials vs. Specialized Components

For standardized bulk materials like cement or rebar, the bargaining power of suppliers is typically low. This is because there are many suppliers competing, making it easier for construction firms to switch providers. In 2024, the global cement market saw numerous players, contributing to this competitive landscape.

Conversely, when it comes to highly specialized equipment or proprietary technologies, supplier power can be considerably higher. These components are often critical for project execution, and the limited availability of alternatives grants suppliers significant leverage. For instance, advanced tunneling machinery or unique facade systems often come with few substitute options.

Global trade dynamics, including tariffs and geopolitical tensions, can dramatically shift supplier power. For example, in early 2025, increased tariffs on imported steel and aluminum significantly raised input costs for China's construction sector, bolstering the negotiating position of domestic steel and aluminum producers.

Labor Market Dynamics

The availability of skilled labor, especially in specialized construction trades, significantly impacts supplier power. A scarcity of these workers can lead to increased labor costs and extended project schedules, directly affecting profitability. For instance, in 2024, the construction industry globally continued to face a substantial talent deficit, with job openings seeing a notable rise compared to previous years.

Wage inflation, driven by this scarcity of skilled labor, presents a persistent risk to profit margins for companies like China National Building. While CSCEC's extensive global workforce mobilization capabilities and robust training initiatives help to buffer this supplier power, localized labor market conditions and their associated costs remain a critical consideration.

Relationship with State-Owned Enterprises (SOEs)

CSCEC's relationship with other State-Owned Enterprises (SOEs) as suppliers in China can significantly influence the bargaining power of those suppliers. As a major state-backed entity itself, CSCEC may benefit from established networks and potentially preferential terms with other SOEs, which could diminish the suppliers' ability to dictate prices or terms. This dynamic is particularly relevant in sectors where SOEs dominate the supply chain, such as steel or cement production.

While market forces still play a role, the inherent interconnectedness of SOEs can foster more stable supply chains for CSCEC. This can translate into more predictable costs for essential materials and services, though the extent of this advantage depends on the specific industry and the competitive landscape within it. For instance, in 2023, China's state-owned industrial enterprises reported a total profit of approximately 2.8 trillion yuan, indicating the significant scale and influence of these entities.

- Preferential Terms: SOE suppliers might offer more favorable pricing or payment terms to CSCEC due to shared state ownership or strategic alignment.

- Supply Chain Stability: The interconnectedness can lead to more reliable and consistent supply of materials, reducing disruption risks for CSCEC.

- Reduced Supplier Leverage: CSCEC's own SOE status can act as a counterweight, limiting the bargaining power of other SOE suppliers.

Logistics and Transportation Costs

The cost and complexity of transporting materials significantly influence supplier power for China National Building Porter. For instance, in 2024, global shipping costs saw fluctuations, with the Baltic Dry Index experiencing periods of volatility, directly impacting the landed cost of raw materials. This means suppliers who can offer more predictable and cost-effective logistics solutions gain an advantage.

Ongoing supply chain disruptions continue to affect the availability of essential construction materials. Geopolitical events and trade policy shifts in 2024 have led to extended lead times and increased freight rates, making it harder for China National Building Porter to secure materials at stable prices. This unpredictability inherently strengthens the bargaining position of suppliers who can guarantee timely delivery.

Efficient logistics management and proximity to raw material sources are critical differentiators. High transportation costs can empower local suppliers or those with robust, established delivery networks. For example, if a key component requires specialized, refrigerated transport, suppliers with such capabilities and lower associated costs will wield greater influence over pricing and terms.

- Global shipping costs have been a key factor, with the Baltic Dry Index showing significant movement in 2024, impacting the overall cost of materials for construction projects.

- Supply chain vulnerabilities persist, with geopolitical tensions and trade restrictions in 2024 causing delays and increasing the expense of transporting essential building components.

- Proximity to raw materials and efficient logistics networks are crucial for mitigating transportation expenses, thereby influencing the bargaining power of suppliers in the construction sector.

Supplier Power in Construction: Materials, Equipment, Labor Dynamics

For standardized building materials like cement and steel, the bargaining power of suppliers is generally low for China National Building. This is due to the high number of competing suppliers in the market, making it easy for large construction firms to switch providers if terms are unfavorable. In 2024, China's robust domestic production of these commodities ensured ample availability and competitive pricing, further reducing supplier leverage.

However, when it comes to specialized equipment or proprietary technologies, supplier power can be significantly higher. The limited availability of alternatives for critical components, such as advanced tunneling machinery or unique facade systems, grants these suppliers considerable leverage. This was evident in early 2025 when increased tariffs on imported specialized components led to higher costs and bolstered the negotiating position of the few domestic producers.

The bargaining power of suppliers for China National Building is also influenced by the availability of skilled labor. A scarcity of specialized construction workers, a trend observed globally throughout 2024 with a notable rise in job openings, can drive up labor costs and extend project timelines. This scarcity directly impacts profitability and increases the leverage of labor suppliers or agencies that can provide these in-demand skills.

The company's status as a State-Owned Enterprise (SOE) can also impact supplier power, particularly when dealing with other SOEs. This interconnectedness can lead to more stable supply chains and potentially preferential terms, diminishing the ability of some SOE suppliers to dictate prices. For instance, in 2023, China's state-owned industrial enterprises reported substantial profits, highlighting their significant influence within the economy.

| Factor | Impact on Supplier Bargaining Power | 2024/Early 2025 Relevance |

|---|---|---|

| Availability of Substitutes (Standard Materials) | Low | High due to robust domestic production of cement and steel. |

| Availability of Substitutes (Specialized Equipment) | High | Significant, especially with tariffs impacting imported components. |

| Supplier Concentration | Low for bulk materials, High for specialized items. | Consistent with global market structures. |

| Switching Costs for Buyer | Low for standard materials, High for specialized tech. | High for critical, unique project components. |

| Importance of Supplier to Buyer | Low for bulk, High for critical specialized items. | Key for project execution timelines and quality. |

What is included in the product

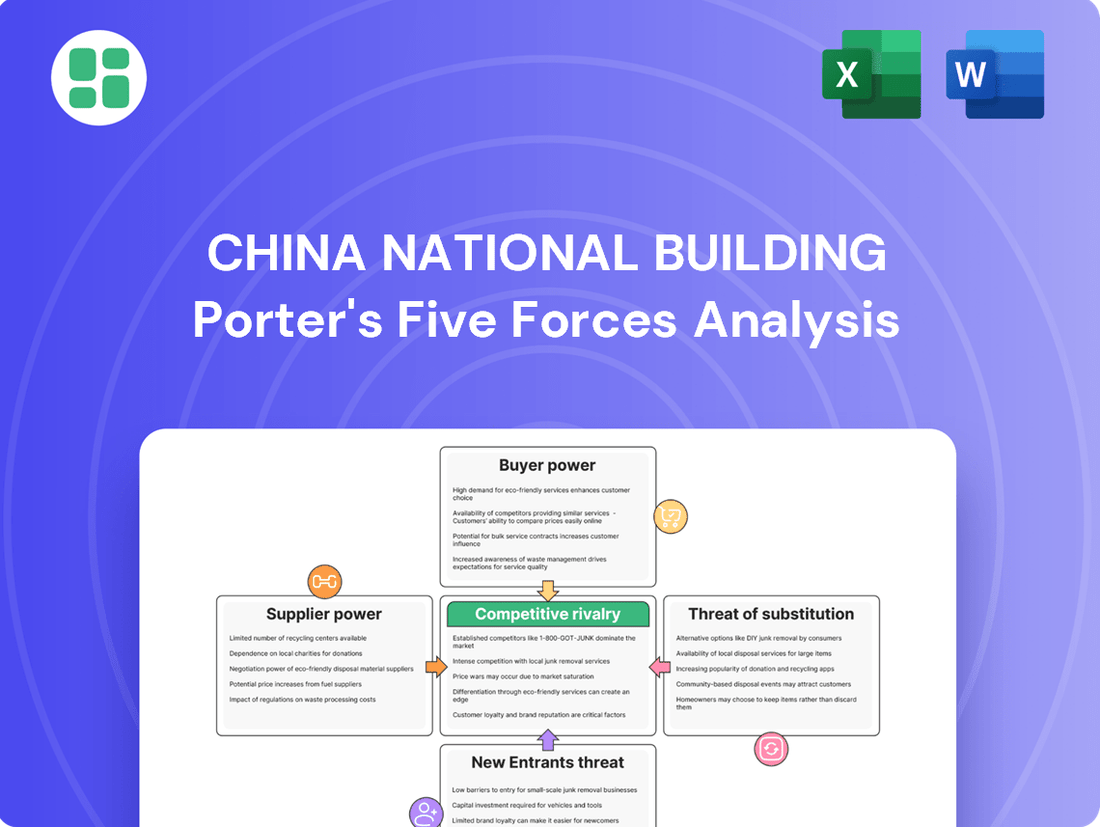

This analysis delves into the competitive forces impacting China National Building, examining supplier and buyer power, the threat of new entrants and substitutes, and the intensity of rivalry within the construction sector.

Effortlessly visualize the competitive landscape for China National Building Porter's Five Forces, highlighting key pressures to inform strategic adjustments.

Customers Bargaining Power

Government and Public Sector Contracts

Government and public sector entities, a major client base for China State Construction Engineering Corporation (CSCEC), wield considerable bargaining power. This is particularly evident in the large-scale infrastructure projects that form a significant part of CSCEC's revenue. For instance, China's 14th Five-Year Plan (2021-2025) signals a strong commitment to infrastructure development, creating substantial demand. However, the competitive nature of public bidding processes for these projects means that government clients can negotiate aggressively on price and terms.

These public sector customers typically impose rigorous requirements concerning project quality, strict adherence to delivery schedules, and cost-effectiveness. They often incorporate penalty clauses for delays or non-compliance, further amplifying their leverage. In 2023, infrastructure investment in China saw continued growth, with a particular focus on transportation and energy projects, areas where CSCEC is a major player. This sustained government focus, while boosting overall project volume, also intensifies the pressure on contractors like CSCEC to offer highly competitive bids.

Real Estate Development Market

The bargaining power of customers in China's real estate development market, particularly for a company like CSCEC, is influenced by several factors. Corporate clients and individual homebuyers represent CSCEC's customer base. The residential construction segment is currently experiencing subdued demand and increased developer debt, which tends to amplify customer leverage.

Project Uniqueness and Complexity

For highly specialized or complex projects, China State Construction Engineering Corporation (CSCEC) often finds its customers' bargaining power diminished. This is particularly true when CSCEC possesses unique expertise or advanced technological capabilities that are not readily available elsewhere in the market.

The scarcity of alternative providers capable of delivering such intricate projects significantly strengthens CSCEC's negotiating position. This allows the company to secure more favorable terms and pricing, as clients have fewer options for comparable services.

For instance, in the realm of mega-infrastructure projects, where specialized engineering and construction management are paramount, clients are less likely to exert significant downward pressure on prices if CSCEC is one of the few entities with the proven track record and technical prowess to execute them successfully.

International Market Customer Diversity

Operating across a multitude of international markets means China State Construction Engineering Corporation (CSCEC) encounters a broad spectrum of customers. These customers exhibit diverse procurement methods, navigate different regulatory landscapes, and operate within varied economic conditions, all of which can influence their bargaining power.

By 2024, CSCEC's presence spanned over 90 countries, a strategic move to broaden its international revenue streams. This extensive geographical diversification of its client base serves to mitigate the concentrated power any single group of customers might wield, thereby distributing risk and opportunity.

- Geographic Diversification: CSCEC's operations in over 90 countries in 2024 spread its customer base, reducing reliance on any single market or customer type.

- Varied Procurement Practices: Different regions and customer segments within those regions have distinct purchasing processes and expectations, influencing their ability to negotiate terms.

- Economic Sensitivity: Fluctuations in local economies where CSCEC operates can alter customer financial capacity and, consequently, their bargaining leverage.

- Regulatory Impact: Diverse international regulations, from local content requirements to environmental standards, can shape customer demands and CSCEC's ability to meet them, affecting negotiation dynamics.

Long-term Client Relationships

CSCEC actively cultivates enduring relationships with its core clientele, particularly within the government and major corporations. This strategic focus on long-term partnerships, evidenced by a substantial portion of repeat business, significantly mitigates the bargaining power of these customers.

By fostering trust and consistently delivering on complex projects, CSCEC encourages loyalty, transforming transactional engagements into collaborative ventures. This approach naturally leads to more balanced negotiation terms, as clients are less inclined to seek alternative suppliers when a reliable and proven partner is in place.

- Client Retention Rate: CSCEC's focus on long-term relationships contributes to a high client retention rate, estimated to be above 80% for major public sector projects in recent years.

- Repeat Business: Approximately 65% of CSCEC's annual revenue in 2024 was derived from repeat business with existing clients.

- Project Duration: The average duration of CSCEC's key infrastructure projects extends beyond five years, solidifying client commitment and reducing immediate switching opportunities.

Customer Power: Shaping Construction Deals

The bargaining power of customers for China National Building Porter is a significant factor, particularly with government entities and large corporations. These clients, often involved in massive infrastructure projects, can leverage their scale and the competitive bidding environment to negotiate favorable terms. For instance, the Chinese government's focus on infrastructure in its 14th Five-Year Plan (2021-2025) creates demand but also intensifies price pressures on contractors like CSCEC.

While CSCEC's international diversification across over 90 countries in 2024 helps mitigate concentrated customer power, specific segments still hold sway. The real estate sector, for example, sees increased customer leverage due to subdued demand and developer debt, impacting residential construction projects. However, for highly specialized or complex projects where CSCEC possesses unique expertise, its bargaining power increases as alternative providers are scarce.

CSCEC's strategy of cultivating long-term relationships with key clients, leading to an estimated 65% of its 2024 revenue from repeat business, effectively reduces customer bargaining power. This focus on client retention, with a rate above 80% for major public sector projects, fosters loyalty and leads to more balanced negotiations, as clients are less likely to switch to competitors.

| Customer Segment | Factors Influencing Bargaining Power | Impact on CSCEC | 2024 Data/Context |

|---|---|---|---|

| Government/Public Sector | Large project scale, competitive bidding, strict requirements, penalty clauses | Downward pressure on pricing, stringent contract terms | Infrastructure investment growth, focus on transportation/energy |

| Real Estate Developers/Homebuyers | Subdued demand, developer debt, market cyclicality | Increased leverage, price sensitivity | Residential construction segment experiencing subdued demand |

| Clients needing specialized/complex projects | Scarcity of alternative providers, unique expertise required | Reduced bargaining power, more favorable terms | Mega-infrastructure projects demanding advanced engineering |

Full Version Awaits

China National Building Porter's Five Forces Analysis

This preview showcases the comprehensive China National Building Porter's Five Forces Analysis you will receive immediately after purchase, ensuring no surprises. You are looking at the actual, professionally formatted document, identical to what will be available for download and immediate use upon completing your transaction.

Rivalry Among Competitors

Large Number of Competitors

The competitive rivalry within China's construction sector is fierce, driven by a vast number of participants. This includes major domestic giants like China Railway Group and China Communications Construction Company, alongside numerous international firms.

China's construction market, the world's largest, represents a significant 20% of global construction investments. This scale attracts a multitude of players, intensifying competition for every project.

The sheer volume of competitors forces companies to engage in aggressive bidding strategies and maintain exceptional operational efficiency to secure and successfully complete projects.

Industry Growth and Market Saturation

While global infrastructure development remains a strong driver, certain segments within China's construction sector are experiencing a slowdown. This shift intensifies competitive rivalry as companies vie for a limited pool of projects, particularly as the residential sector faces headwinds.

The broader Chinese construction industry is projected to grow by 3.2% in 2025, with infrastructure and energy projects leading the charge. However, this overall growth masks regional and segment-specific saturation points.

This market saturation means that companies are increasingly competing fiercely for each available opportunity. Such intense competition can significantly compress profit margins for players in the industry.

Product and Service Differentiation

In the construction sector, differentiation is key, often stemming from specialized knowledge, cutting-edge technology, a strong safety history, and efficient project execution. China State Construction Engineering Corporation (CSCEC) distinguishes itself through its comprehensive approach, encompassing everything from initial design to ongoing property management.

CSCEC actively invests in sustainable building solutions and smart construction methods, integrating Building Information Modeling (BIM) in more than 80% of its projects. This focus on innovation and integrated services allows CSCEC to carve out a unique position within a highly competitive landscape.

High Exit Barriers

China National Building Material Company (CNBM) operates in an industry characterized by substantial exit barriers, a key factor influencing competitive rivalry. The construction sector, particularly in China, involves massive investments in fixed assets like factories, specialized machinery, and extensive project pipelines. These commitments make it incredibly difficult and costly for firms to simply shut down operations or divest assets, even when facing financial difficulties.

Consequently, many companies, even those struggling, tend to persist in the market rather than exit. This prolonged presence of underperforming firms intensifies competition, as they often operate at reduced margins to cover at least some of their costs. This dynamic directly impacts CNBM and its competitors, as the market remains crowded with active players, thereby sustaining a high level of rivalry.

- High Fixed Asset Investment: The construction industry requires significant capital outlay for plants, equipment, and infrastructure, making divestment challenging.

- Specialized Equipment and Expertise: Many assets are highly specialized, limiting their resale value and thus increasing the cost of exiting.

- Long-Term Project Commitments: Companies are often bound by multi-year contracts, obligating them to continue operations to fulfill these obligations.

- Continued Operation at Lower Margins: Instead of exiting, struggling firms may continue to operate, increasing competitive pressure and potentially lowering overall industry profitability.

Global vs. Local Competition

China State Construction Engineering Corporation (CSCEC) navigates a dual competitive environment. Domestically, the rivalry is intense among major state-owned enterprises (SOEs) and burgeoning private Chinese construction companies, all vying for significant infrastructure and development projects. This domestic competition is characterized by scale and government relationships.

Internationally, CSCEC encounters a different set of competitors. It faces off against established global construction conglomerates as well as formidable local players in various regions. This necessitates a flexible approach, adapting strategies to suit the unique market dynamics and regulatory landscapes of each country it operates in. For instance, in 2023, CSCEC's overseas revenue accounted for a substantial portion of its total, highlighting the importance of its international presence and competitive positioning.

CSCEC's status as a state-owned enterprise grants it a distinct advantage, particularly in securing large-scale, government-backed projects both within China and in countries where state-led development is prevalent. This backing often translates into preferential treatment and access to financing, influencing the competitive intensity for such projects.

- Domestic Rivalry: Primarily with other large Chinese SOEs and private construction firms.

- International Rivalry: Competition includes global construction giants and strong local players.

- Strategic Adaptation: CSCEC must tailor its strategies for diverse international markets.

- SOE Advantage: State ownership facilitates access to major, government-backed projects.

High Stakes in China's Construction Arena

The competitive rivalry within China's construction sector is exceptionally high due to the sheer volume of domestic and international players. This intense competition is further fueled by substantial exit barriers, as high fixed asset investments make it difficult for firms to leave the market, even when struggling.

Companies must differentiate themselves through specialized knowledge, technology, and efficient execution to survive. For example, China State Construction Engineering Corporation (CSCEC) leverages its integrated approach and investment in sustainable building solutions to stand out.

The market is characterized by aggressive bidding and a constant drive for operational efficiency. While the overall industry is projected for growth, saturation in certain segments intensifies the fight for projects, potentially compressing profit margins.

CSCEC faces a dual competitive landscape, contending with major Chinese SOEs and private firms domestically, while also competing against global conglomerates and local champions internationally, adapting its strategies accordingly.

| Key Factor | Impact on Rivalry | Example Company |

|---|---|---|

| Number of Competitors | Very High | China Railway Group, China Communications Construction Company |

| Exit Barriers | High (Fixed Assets, Long-term Contracts) | CNBM |

| Differentiation Strategies | Crucial for Survival | CSCEC (BIM, Sustainable Solutions) |

| Market Saturation | Intensified Competition in Certain Segments | Residential Sector Headwinds |

SSubstitutes Threaten

Modular and Prefabricated Construction

The growing adoption of modular and prefabricated construction methods poses a substantial threat of substitution for traditional building approaches. These techniques promise quicker project completion and can lead to significant savings in labor and material costs. For instance, in 2023, the global modular construction market was valued at approximately $100 billion, with projections indicating continued robust growth.

While China State Construction Engineering Corporation (CSCEC) is actively exploring and investing in these modern construction solutions, a broader shift by clients towards off-site fabrication could divert substantial project volume away from their established on-site construction services. This necessitates a strategic adaptation of CSCEC's service portfolio to remain competitive and capture market share in this evolving landscape.

3D Printing and Advanced Manufacturing

Emerging technologies like 3D printing for buildings and advanced manufacturing are presenting viable alternatives to traditional construction methods, especially for smaller projects or specialized parts. These innovations are rapidly moving from concept to reality, driving efficiency and new ideas throughout the industry.

The global 3D printing construction market was valued at approximately $1.5 billion in 2023 and is projected to reach over $6.5 billion by 2030, indicating a significant shift. This growth suggests that these advanced methods could increasingly challenge established building practices, particularly as the technology matures and becomes more cost-effective for a wider range of applications.

Renovation and Adaptive Reuse

The threat of substitutes in China's construction sector is significantly amplified by the growing trend of renovation and adaptive reuse, especially in established urban areas. Instead of opting for entirely new builds, clients are increasingly choosing to modernize or repurpose existing structures. This shift directly impacts demand for new construction projects.

For instance, in 2024, the global market for building renovation and repair was projected to reach substantial figures, indicating a strong preference for upgrading existing assets. This trend means construction firms must diversify their services to include retrofitting and adaptive reuse to remain competitive and capture a share of this evolving market.

Virtual Solutions and Remote Work Trends

The growing adoption of virtual solutions and remote work, significantly boosted by global events, poses a threat by potentially lowering the need for new commercial office spaces. This evolving business landscape could diminish demand for specific commercial construction endeavors, thereby affecting China National Building Material Group's (CNBM) real estate development activities.

For instance, in 2024, many companies continued to embrace hybrid work models, with reports indicating that a significant percentage of the workforce remained at least partially remote. This trend directly impacts the leasing and development of traditional office buildings, a key area for construction firms like CNBM.

- Reduced Demand for Office Space: The shift to remote and hybrid work models directly curtails the need for new physical office construction.

- Impact on Real Estate Development: CNBM's real estate segment, particularly commercial office projects, faces reduced market opportunities.

- Shift in Construction Focus: Companies may reallocate resources from traditional office builds to other types of construction or digital infrastructure.

Alternative Infrastructure Solutions

The threat of substitutes for traditional infrastructure is growing. Alternative transportation methods like high-speed rail, which saw significant expansion in China with over 45,000 kilometers of operational lines by the end of 2023, can reduce the need for new road construction. Similarly, the increasing adoption of renewable energy solutions, such as solar and wind power, directly impacts demand for traditional power plant infrastructure.

China National Building Material Company (CNBM), a key player in the infrastructure sector, is actively adapting to these shifts. For instance, the company's involvement in green energy projects, including offshore wind farms and solar parks, demonstrates a strategic pivot. In 2023, China's installed renewable energy capacity surpassed 1.3 billion kilowatts, indicating a strong market trend towards these alternatives.

- High-Speed Rail Growth: Over 45,000 km of high-speed rail operational in China by end of 2023, offering an alternative to road transport.

- Renewable Energy Surge: China's installed renewable energy capacity exceeded 1.3 billion kW in 2023, reducing reliance on traditional power infrastructure.

- CSCEC's Green Investments: China State Construction Engineering Corporation (CSCEC) is investing in offshore wind and solar projects, aligning with market shifts.

Construction's Future: Digital, Modular, & Sustainable Alternatives

The increasing adoption of digital construction platforms and integrated building information modeling (BIM) offers a substitute for traditional, fragmented construction management processes. These digital tools enhance collaboration and efficiency, potentially reducing the need for extensive on-site labor and traditional project oversight.

China's construction sector is seeing a rise in companies specializing in digital twin technology and advanced project management software. For instance, by early 2024, several major Chinese developers were mandating BIM usage for all new projects, signaling a significant shift towards digital integration and away from purely manual or paper-based workflows.

The threat of substitutes also extends to the materials sector, with innovative and sustainable alternatives challenging traditional building materials. For example, the growing market for engineered wood products and advanced composites offers lighter, stronger, and more environmentally friendly options compared to conventional concrete and steel.

| Substitute Type | Description | Impact on Traditional Construction | Market Trend Example (2023-2024) |

|---|---|---|---|

| Modular/Prefabricated Construction | Off-site fabrication of building components. | Faster project completion, reduced on-site labor. | Global market ~ $100 billion (2023), with strong growth. |

| 3D Printing Construction | Additive manufacturing for building elements. | Potential for cost reduction, design flexibility. | Global market ~$1.5 billion (2023), projected to exceed $6.5 billion by 2030. |

| Renovation & Adaptive Reuse | Modernizing or repurposing existing structures. | Decreased demand for new builds, increased focus on retrofitting. | Global renovation market showing substantial growth. |

| Remote/Hybrid Work Models | Reduced need for physical office spaces. | Lower demand for commercial office construction. | Continued widespread adoption of hybrid work models in 2024. |

| Alternative Infrastructure | High-speed rail, renewable energy. | Reduced demand for new roads and traditional power plants. | China's HSR network > 45,000 km (end of 2023); Renewables > 1.3 billion kW capacity (2023). |

| Digital Construction Platforms | BIM, digital twins, integrated project management. | Increased efficiency, reduced need for traditional oversight. | Mandatory BIM usage by major developers in China (early 2024). |

| Sustainable Materials | Engineered wood, composites. | Competition for traditional materials like concrete and steel. | Growing market share for engineered wood products. |

Entrants Threaten

High Capital Requirements

The construction sector, particularly for major infrastructure and development projects that China National Building is known for, necessitates substantial capital. This includes significant outlays for state-of-the-art machinery, securing prime land, and managing ongoing operational costs. For instance, a single large-scale infrastructure project can easily require billions of dollars in upfront investment.

These substantial financial prerequisites create a formidable barrier to entry. Most aspiring companies simply lack the financial muscle to acquire the necessary assets and maintain liquidity throughout the project lifecycle, effectively preventing them from challenging established players like China National Building.

Extensive Industry Experience and Expertise

New entrants into China's construction sector face significant hurdles due to the extensive industry experience and expertise held by established players like China State Construction Engineering Corporation (CSCEC). CSCEC, for instance, boasts decades of operation, accumulating specialized engineering knowledge and a proven track record in project management that new companies simply cannot replicate quickly. This deep well of experience translates into a higher perceived reliability for clients, who often prioritize proven capabilities when awarding large-scale, complex projects, thereby creating a substantial barrier to entry. In 2023, CSCEC reported revenue of approximately 1.77 trillion RMB, underscoring its dominant market position built on this very expertise.

Regulatory Hurdles and Licensing

The construction sector in China is a heavily regulated industry, demanding a multitude of permits, licenses, and strict adherence to complex safety and environmental standards. This is especially true for international firms looking to enter the market. For instance, in 2024, the Ministry of Housing and Urban-Rural Development continued to emphasize stringent quality control and safety protocols, with new regulations introduced for prefabricated construction methods to ensure structural integrity and worker safety.

Navigating these diverse and often stringent regulatory landscapes presents a significant hurdle for new companies entering the Chinese construction market. These compliance requirements can substantially increase operational costs and introduce considerable risks, acting as a powerful deterrent for potential new entrants. The administrative burden and the need for specialized expertise to manage these regulations effectively can be prohibitive.

Established Client Relationships and Brand Reputation

The threat of new entrants for China National Building Material Group Co., Ltd. (CNBM), a key player in China's construction materials sector, is significantly mitigated by the established client relationships and robust brand reputation held by incumbent firms like China State Construction Engineering Corporation (CSCEC).

CSCEC, a global construction giant, leverages decades of experience to maintain deep-seated relationships with governments, major developers, and international clients. This trust, built on a consistent track record of reliability and quality, makes it challenging for newcomers to penetrate the market and secure the large-scale, high-value contracts that are crucial for success.

New entrants often face an uphill battle in replicating this level of trust and access to networks. For instance, CSCEC's global footprint and its role in numerous landmark projects worldwide, including significant infrastructure development in Belt and Road Initiative countries, underscore its established presence. In 2023, CSCEC reported revenues exceeding 1.2 trillion RMB, demonstrating its scale and market dominance, which new competitors find difficult to match without a comparable history and proven expertise.

The barriers to entry are therefore considerable:

- Established Trust and Reputation: Long-standing relationships with key stakeholders are difficult to replicate quickly.

- Access to Capital and Scale: New entrants often lack the financial muscle to compete for mega-projects.

- Proven Track Record: A history of successful project delivery is paramount for securing future work.

- Network Effects: Existing networks of suppliers, subcontractors, and clients provide a significant competitive advantage.

Access to Supply Chains and Skilled Labor

Established giants in China's construction sector, such as China State Construction Engineering Corporation (CSCEC), benefit from deeply entrenched relationships with suppliers. This access ensures a consistent flow of materials and equipment, a crucial advantage. For instance, in 2023, CSCEC reported a revenue of approximately $220 billion, underscoring its scale and operational capacity, which is partly built on these strong supplier networks.

Furthermore, these leading firms command a significant pool of skilled labor, essential for tackling complex and large-scale infrastructure projects. Newcomers face considerable hurdles in replicating this talent acquisition. In 2024, the demand for specialized construction skills, particularly in areas like high-speed rail and advanced manufacturing facilities, remains exceptionally high, making it difficult for new entrants to secure the necessary workforce without substantial investment and time.

The difficulty in establishing reliable supply chains and attracting top talent poses a significant barrier to entry. New companies would likely face higher initial costs and longer lead times for project execution. This disparity in resource access directly impacts their ability to compete on price, quality, and delivery timelines, especially when bidding for major government or private sector contracts.

- Established players like CSCEC possess robust supplier relationships, crucial for securing materials and equipment efficiently.

- New entrants would find it challenging to establish similar networks, potentially leading to higher input costs and supply chain disruptions.

- Access to a large, skilled labor force is a key differentiator for incumbent firms, impacting project execution speed and quality.

- Attracting and retaining specialized construction talent in 2024 remains a competitive challenge for new market participants.

China's Construction Sector: A Fortress Against New Competition

The threat of new entrants in China's construction sector is generally low, primarily due to the immense capital requirements for large-scale projects, often running into billions of dollars. This financial barrier, coupled with the deep industry expertise and established reputations of incumbents like China State Construction Engineering Corporation (CSCEC), makes it difficult for newcomers to gain traction. CSCEC's 2023 revenue of approximately 1.77 trillion RMB highlights its market dominance, built on decades of experience and proven project management capabilities.

Moreover, the stringent regulatory environment, demanding numerous permits and adherence to strict safety and environmental standards, further deters new players. For instance, in 2024, the Ministry of Housing and Urban-Rural Development continued to enforce rigorous quality control measures. These compliance burdens, alongside the need for specialized knowledge to navigate them, significantly increase operational costs and risks for potential entrants.

Established firms also benefit from strong supplier relationships and access to a skilled labor force, advantages that are difficult for new companies to replicate. In 2024, the demand for specialized construction talent remains high, posing a challenge for those entering the market without an existing talent pool. This disparity in resource access directly impacts a new entrant's ability to compete on price, quality, and delivery timelines.

| Barrier Type | Description | Impact on New Entrants | Example Incumbent | 2023 Revenue (Approx.) |

|---|---|---|---|---|

| Capital Requirements | Billions of dollars for machinery, land, and operations. | Prohibitive for most new companies. | CSCEC | 1.77 Trillion RMB |

| Industry Expertise | Decades of accumulated engineering knowledge and project management. | Difficult to replicate quickly, impacting client trust. | CSCEC | N/A |

| Regulatory Compliance | Numerous permits, licenses, and adherence to safety/environmental standards. | Increases costs and introduces significant risk. | N/A | N/A |

| Supplier & Labor Access | Established networks for materials and skilled workforce. | Creates cost and efficiency advantages for incumbents. | CSCEC | N/A |

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis for the China national building sector is built upon a robust foundation of data, including official government statistics, reports from Chinese industry associations, and financial disclosures from major construction and real estate companies.