Commerce Bank PESTLE Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Commerce Bank Bundle

Make Smarter Strategic Decisions with a Complete PESTEL View

Navigate the complex external landscape impacting Commerce Bank with our comprehensive PESTLE analysis. Understand how political shifts, economic volatility, and technological advancements are shaping the financial sector, influencing Commerce Bank's strategic decisions and market position. Gain a critical advantage by downloading the full report, packed with actionable intelligence to inform your own business strategy.

Political factors

Government Policy and Regulatory Environment

The upcoming US presidential administration in 2025 signals a potential shift in the regulatory environment for banks. A move toward deregulation could reduce compliance costs for institutions like Commerce Bancshares, but also necessitates a proactive approach to evolving supervisory expectations and strong risk management practices.

Financial institutions will need to remain focused on resolving existing supervisory concerns and showcasing consistent improvement in 2025. This focus is crucial for maintaining trust and operational stability within the banking sector.

Interest Rate Policy and Monetary Stance

The Federal Reserve's monetary policy, particularly its interest rate decisions, significantly shapes Commerce Bancshares' financial performance. Following a period of rate cuts in late 2024, the Fed maintained a steady interest rate stance through mid-2025. The ongoing trajectory of inflation and labor market indicators in the latter half of 2025 will be crucial in determining any future adjustments to these rates.

These policy shifts directly influence Commerce Bancshares' net interest income, a key driver of profitability. Higher interest rates generally benefit banks by widening the spread between what they earn on loans and what they pay on deposits, while lower rates can compress this margin. The anticipation of future rate movements also impacts lending demand and loan growth strategies for the bank.

Geopolitical Risks and Trade Policies

Global geopolitical uncertainties and evolving trade policies can introduce volatility into financial markets and impact economic stability, even at a regional level. For instance, ongoing trade tensions between major economies in 2024 continue to create headwinds for international commerce, potentially affecting supply chains and investment flows that indirectly influence the Midwest's economic landscape.

While Commerce Bancshares primarily operates in the Midwest, broader economic shifts influenced by these factors can affect consumer and business confidence. In 2024, a slight dip in consumer sentiment, partly attributed to global economic uncertainties, could lead to reduced demand for financial services like mortgages and business loans, thereby impacting the bank's revenue streams and potentially increasing credit risk.

Government Support and Stimulus Programs

Future government initiatives, while not explicitly detailed for 2025, could significantly impact economic activity and liquidity within the banking sector. These programs, if enacted, may bolster specific industries or consumer groups, thereby influencing loan demand and credit risk profiles for institutions like Commerce Bancshares.

For instance, the U.S. government's continued focus on infrastructure investment, as seen in the Infrastructure Investment and Jobs Act, could stimulate economic growth and create lending opportunities. Additionally, any potential future stimulus aimed at housing markets or small businesses could directly benefit a regional bank like Commerce Bancshares, which has a strong presence in these areas.

- Government fiscal policy, including potential future stimulus measures, can directly influence consumer spending and business investment, impacting loan growth for Commerce Bancshares.

- Regulatory changes stemming from government oversight, such as adjustments to capital requirements or lending standards, will continue to shape the operational landscape for banks.

- Federal Reserve monetary policy, including interest rate decisions, remains a critical government-influenced factor affecting borrowing costs and the overall economic environment for Commerce Bancshares.

Bank Merger and Acquisition Regulatory Environment

A shift towards a potentially more lenient regulatory climate for bank mergers and acquisitions (M&A) could significantly influence Commerce Bancshares' strategic landscape. This evolving environment, particularly under a new administration, might see an uptick in M&A activity across the banking sector. For Commerce Bancshares, this could translate into both avenues for growth through strategic acquisitions aimed at expanding its geographic footprint or service offerings, and the potential for intensified competition as larger, consolidated entities emerge.

The Federal Reserve and the Office of the Comptroller of the Currency (OCC) are key bodies influencing this environment. For instance, in 2023, the OCC approved several significant bank mergers, indicating a willingness to review such proposals. The Biden administration's approach to antitrust and industry consolidation, while generally cautious, has shown some flexibility in specific sectors when deemed beneficial. The overall trend in 2024 and projected into 2025 suggests continued scrutiny but also potential for deals that meet specific criteria, such as enhancing consumer benefits or promoting financial stability.

- Regulatory Approvals: Historically, regulatory approval has been a critical hurdle for bank M&A. A more permissive stance could streamline this process.

- Competitive Landscape: Increased M&A activity could lead to fewer, larger competitors, potentially impacting market share and pricing for Commerce Bancshares.

- Strategic Opportunities: Commerce Bancshares may find opportunities to acquire smaller, regional banks or specific business lines to bolster its market position.

- Economic Impact: Consolidation can lead to efficiencies, but also raises concerns about reduced competition and potential impacts on local communities.

Government Policy: Shaping Bank Growth and Operations

Government fiscal policy, including potential future stimulus measures, can directly influence consumer spending and business investment, impacting loan growth for Commerce Bancshares. Regulatory changes stemming from government oversight, such as adjustments to capital requirements or lending standards, will continue to shape the operational landscape for banks. Federal Reserve monetary policy, including interest rate decisions, remains a critical government-influenced factor affecting borrowing costs and the overall economic environment for Commerce Bancshares.

What is included in the product

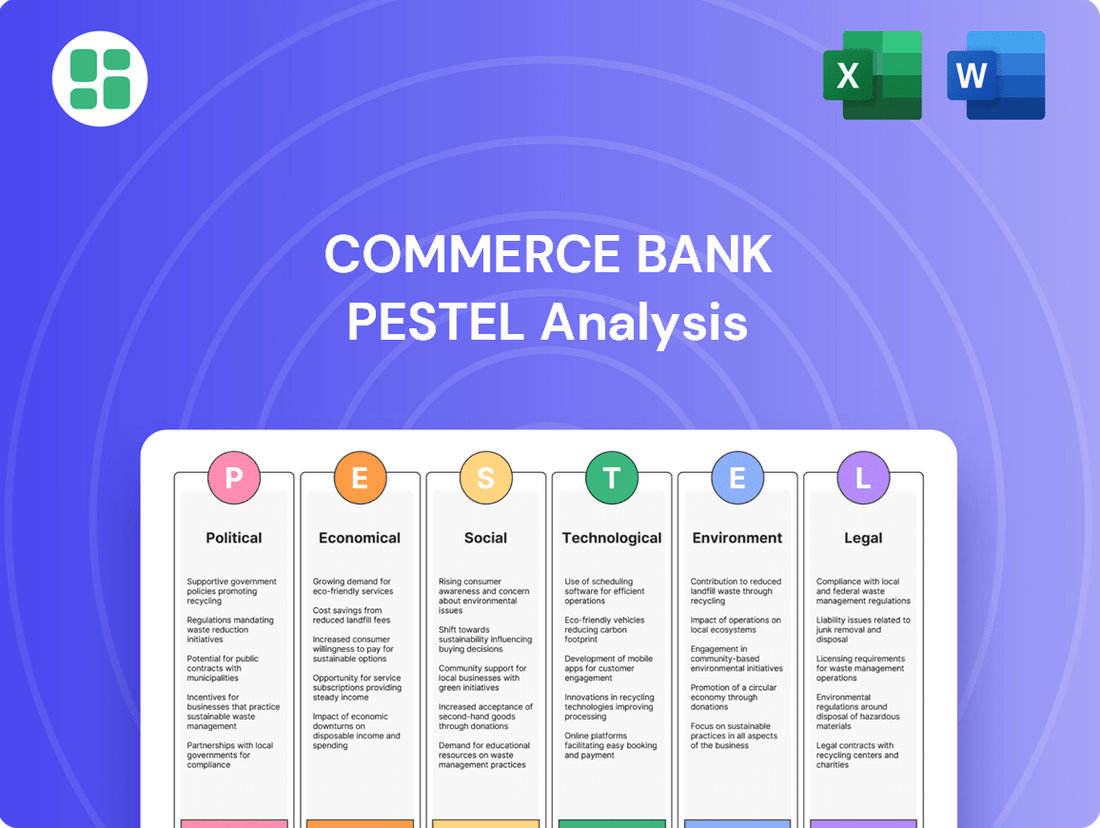

This PESTLE analysis provides a comprehensive examination of the external macro-environmental forces impacting Commerce Bank, detailing how Political, Economic, Social, Technological, Environmental, and Legal factors present both challenges and avenues for strategic growth.

A PESTLE analysis for Commerce Bank offers a clear, summarized version of external factors, relieving the pain of information overload during strategic planning.

By visually segmenting Commerce Bank's PESTLE analysis, stakeholders can quickly interpret market dynamics and potential risks, alleviating the burden of sifting through raw data.

Economic factors

Interest Rate Environment and Net Interest Margin

The Federal Reserve's monetary policy, particularly its stance on interest rates, significantly shapes Commerce Bancshares' financial performance. Projections for 2025 indicate a potential for gradual rate reductions.

These anticipated rate cuts could compress the bank's net interest margin, a key profitability driver. However, lower borrowing costs might also spur increased demand for loans, potentially offsetting margin compression through higher loan volumes.

For context, in the first quarter of 2024, Commerce Bancshares reported a net interest margin of 3.23%, a slight decrease from 3.32% in the prior year, reflecting some of the pressures from the existing rate environment.

Regional Economic Growth and Employment Rates

Commerce Bancshares' focus on the Midwest means regional economic health is paramount. A strong U.S. economy, characterized by robust employment and controlled inflation, as seen in 2024 with a national unemployment rate hovering around 3.9% and inflation moderating, directly fuels demand for banking products and services.

This economic stability translates into higher consumer spending and increased business investment across Commerce Bank's operating regions. Consequently, this environment supports the bank's loan growth and generally improves the quality of its loan portfolio, as individuals and businesses are better positioned to manage their debt.

Inflationary Pressures and Consumer Spending

Ongoing inflationary pressures, even as they moderate, continue to impact consumer purchasing power. For instance, the U.S. Consumer Price Index (CPI) saw an increase of 3.4% year-over-year in April 2024, a slight decrease from previous months but still elevated. This sustained inflation can erode the real value of savings and influence how much discretionary income households have available.

While consumer spending has demonstrated resilience, particularly in areas like services, persistent inflation poses a risk to Commerce Bancshares. Higher costs for everyday goods can strain household budgets, potentially affecting their ability to service loans and impacting deposit growth as consumers may dip into savings or reduce new contributions. This directly influences the bank's asset quality and funding base.

Loan Growth and Credit Quality

Commerce Bank's financial health is intrinsically linked to how much it lends and how well those loans are repaid. Loan growth in both consumer and business sectors directly impacts its revenue. For instance, in Q1 2024, Commerce Bancshares reported total loans of $76.9 billion, a slight increase from the previous year, indicating steady demand.

The bank has historically maintained robust credit quality, meaning borrowers are generally paying back their loans as agreed. However, economic headwinds can challenge this. A slowdown or recession could dampen loan demand and, more critically, lead to a rise in nonperforming loans. This is especially a concern in sectors like commercial real estate, which has seen increased scrutiny in 2024 due to higher interest rates and evolving work-from-home trends.

- Loan Portfolio: As of Q1 2024, Commerce Bancshares held $76.9 billion in loans.

- Credit Quality: The bank consistently exhibits strong credit quality metrics, but economic shifts pose a risk.

- Sector Risk: Commercial real estate is a particular area of focus for potential increases in nonperforming loans in the current economic climate.

- Economic Impact: Broader economic downturns can suppress loan demand and elevate default rates across all segments.

Competition in the Financial Services Market

Commerce Bancshares operates within a highly competitive financial services sector. This includes not only traditional banks and credit unions but also a growing number of FinTech companies that are increasingly challenging established players. This dynamic environment directly impacts Commerce Bancshares' ability to maintain its market share and exert influence over pricing, particularly for loans and deposits.

The ability to attract and retain customer deposits and originate loans is crucial for Commerce Bancshares' ongoing economic success. This is especially true in its core Midwest markets, where competition can be intense. For example, as of early 2024, deposit growth across the banking sector has been a key focus, with many institutions vying for customer funds amidst evolving interest rate environments.

- Intense Competition: Commerce Bancshares faces pressure from national banks, regional players, credit unions, and digital-only FinTech firms.

- Midwest Market Dynamics: Sustaining deposit and loan growth in its primary Midwest operating regions requires strategic differentiation and competitive offerings.

- FinTech Disruption: Emerging financial technology companies continue to innovate, offering alternative payment, lending, and investment solutions that capture market share.

- Pricing Power: The crowded competitive landscape can limit pricing power for both deposits and loans, impacting net interest margins.

Interest Rates, Economy, Loans: Bank's Financial Performance Drivers

The Federal Reserve's monetary policy, particularly its stance on interest rates, significantly shapes Commerce Bancshares' financial performance. Projections for 2025 indicate a potential for gradual rate reductions, which could compress the bank's net interest margin, a key profitability driver. However, lower borrowing costs might also spur increased demand for loans, potentially offsetting margin compression through higher loan volumes.

Commerce Bancshares' focus on the Midwest means regional economic health is paramount. A strong U.S. economy, characterized by robust employment and controlled inflation, directly fuels demand for banking products and services. This economic stability translates into higher consumer spending and increased business investment across Commerce Bank's operating regions, supporting loan growth and improving asset quality.

Ongoing inflationary pressures, even as they moderate, continue to impact consumer purchasing power. For instance, the U.S. Consumer Price Index (CPI) saw an increase of 3.4% year-over-year in April 2024, a slight decrease from previous months but still elevated. This sustained inflation can erode the real value of savings and influence how much discretionary income households have available, potentially affecting loan servicing and deposit growth.

Commerce Bank's financial health is intrinsically linked to its loan portfolio. As of Q1 2024, Commerce Bancshares held $76.9 billion in loans, a slight increase from the previous year. While the bank has historically maintained robust credit quality, economic headwinds, particularly in sectors like commercial real estate, could challenge this and lead to a rise in nonperforming loans.

| Metric | Value (Q1 2024) | Previous Period | Trend |

| Total Loans | $76.9 billion | Slight increase year-over-year | Growth |

| Net Interest Margin | 3.23% | 3.32% (Q1 2023) | Slight Decrease |

| U.S. Unemployment Rate | ~3.9% (2024 Avg.) | N/A | Low and Stable |

| U.S. CPI (YoY) | 3.4% (April 2024) | Higher in prior months | Moderating but Elevated |

Same Document Delivered

Commerce Bank PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This comprehensive Commerce Bank PESTLE analysis breaks down the Political, Economic, Social, Technological, Legal, and Environmental factors impacting the bank. Gain immediate access to actionable insights for strategic planning.

Sociological factors

Changing Consumer Preferences for Banking Services

Customers are increasingly prioritizing digital convenience and personalized interactions. For instance, by the end of 2024, mobile banking adoption is projected to reach 70% among U.S. adults, highlighting a significant shift away from traditional branch visits. Commerce Bancshares needs to ensure its digital platforms offer seamless, intuitive experiences, including AI-driven personalized financial advice and easy access to customer support.

Demographic Shifts and Regional Population Trends

The Midwest, Commerce Bank's core territory, is experiencing nuanced demographic shifts. For instance, while some rural areas may see population declines, urban centers are often attracting younger professionals and families. This means a growing demand for services like first-time homebuyer mortgages and digital banking solutions, especially among the 25-44 age bracket, which is projected to remain a significant consumer group through 2025.

An aging population in certain Midwest regions also presents opportunities for wealth management and retirement planning services. As baby boomers continue to age, their financial needs evolve, creating a market for specialized products. Data from the U.S. Census Bureau indicates that the proportion of individuals aged 65 and over in key Midwest states is steadily increasing, highlighting the importance of catering to this demographic.

Household formation trends are also critical. An increase in single-person households or smaller family units, often driven by urbanization and changing lifestyle preferences, can impact the demand for certain loan types and deposit accounts. Understanding the average household size and its composition within Commerce Bank's service areas allows for more targeted product development and marketing efforts.

Financial Literacy and Digital Adoption Rates

Financial literacy directly impacts how customers utilize digital banking services. In the US, a 2023 FINRA study found that 60% of Americans feel confident managing their finances, but only 46% could answer three basic financial literacy questions correctly. This gap highlights a challenge for banks like Commerce Bank in encouraging adoption of their online and mobile platforms, as a solid understanding of financial concepts is often a prerequisite for effective digital engagement.

Digital adoption rates are also crucial. As of early 2024, approximately 85% of US adults use the internet, with smartphone penetration exceeding 80%. However, the adoption of digital banking specifically can vary by demographic and geographic location within Commerce Bancshares' operating regions. For instance, while younger generations are highly adept at using mobile banking apps, older demographics might require more tailored support and education to feel comfortable with these technologies, influencing overall customer engagement strategies.

Trust and Reputation in the Banking Sector

Public trust in banks is paramount, and recent events continue to shape perceptions. Following the regional banking turmoil of early 2023, where several institutions faced significant challenges, consumer confidence in the stability of the financial sector saw a dip. For example, a Gallup poll in April 2023 indicated that only 45% of Americans had a great deal or quite a lot of confidence in banks, a notable decrease from previous years.

Commerce Bancshares, Inc. (CBSH) has historically leveraged its strong reputation built over decades of operation. Their emphasis on community involvement and personalized customer service, evident in their consistent customer satisfaction scores, plays a critical role in fostering and maintaining this trust. This is particularly important as the banking industry navigates evolving customer expectations and the digital landscape.

The bank's proactive approach to cybersecurity and data protection is also a key factor in reassuring customers. In an era where data breaches are a constant concern, Commerce Bancshares' investments in robust security measures help to solidify its image as a reliable and trustworthy financial partner. This commitment is essential for retaining existing clients and attracting new ones who prioritize the safety of their financial information.

Commerce Bancshares' enduring presence and commitment to ethical practices are crucial sociological assets. Their ability to weather economic storms and maintain a stable operational record contributes significantly to public perception. For instance, as of the first quarter of 2024, Commerce Bancshares reported a strong capital position, with a Common Equity Tier 1 (CET1) ratio of 12.5%, demonstrating financial resilience that underpins customer trust.

Workforce Dynamics and Talent Retention

The availability of skilled talent, especially in tech and specialized financial services, is crucial for Commerce Bank's operations and innovation. In 2024, the demand for financial analysts and software developers remained high, with reports indicating a 15% increase in job postings for these roles compared to the previous year. Retaining these valuable employees is equally important.

Commerce Bank must adapt to changing workforce expectations. Offering flexible work arrangements, such as hybrid or remote options, is becoming a standard expectation. For instance, a 2025 survey found that 70% of finance professionals prioritize work-life balance and flexible schedules when considering new employment. Investing in continuous professional development also plays a key role in attracting and keeping top performers.

- Talent Availability: High demand for tech and finance specialists in 2024.

- Retention Challenges: Keeping skilled employees is vital for innovation.

- Evolving Expectations: 70% of finance professionals value flexibility in 2025.

- Development Focus: Professional growth is key to attracting and retaining talent.

Future of Midwest Banking: Digital & Demographic Imperatives

Customer expectations are increasingly shaped by digital experiences and a desire for personalized interactions. By late 2024, mobile banking adoption in the U.S. is expected to hit 70%, underscoring a move away from physical branches. Commerce Bank must ensure its digital platforms provide smooth, user-friendly experiences, incorporating AI for tailored financial advice and accessible customer support.

Demographic shifts in the Midwest, Commerce Bank's primary market, present both challenges and opportunities. While some rural areas may experience population decline, urban centers are attracting younger professionals and families. This trend fuels demand for services like first-time homebuyer mortgages and digital banking solutions, particularly among the 25-44 age group, a key consumer segment through 2025.

The aging population in parts of the Midwest creates a market for wealth management and retirement planning. As baby boomers age, their financial needs change, driving demand for specialized products. The U.S. Census Bureau data shows a consistent rise in the 65+ population in key Midwest states, emphasizing the need to cater to this demographic.

Household formation patterns are also evolving, with an increase in single-person households and smaller family units, often linked to urbanization and changing lifestyles. This can affect demand for specific loan types and deposit accounts. Understanding these shifts allows Commerce Bank to develop more targeted products and marketing strategies.

Technological factors

Digital Transformation and Online Banking Platforms

The banking sector's digital transformation demands ongoing investment in advanced online and mobile platforms. Commerce Bancshares must prioritize these digital offerings to stay competitive, ensuring customers can easily manage accounts, make payments, and apply for loans through user-friendly interfaces. This focus is vital for attracting and keeping customers in today's technology-centric financial landscape.

Cybersecurity Threats and Data Protection

The financial industry is grappling with an increasing volume and sophistication of cyber threats, such as ransomware, distributed denial-of-service (DDoS) attacks, and phishing schemes. For instance, the financial sector experienced a 13% increase in ransomware attacks in the first half of 2024 compared to the same period in 2023, according to industry reports.

Commerce Bancshares must invest heavily in cutting-edge cybersecurity defenses and robust data protection strategies. This is crucial to shield sensitive customer data, preserve client confidence, and adhere to evolving regulatory mandates like the Gramm-Leach-Bliley Act and upcoming data privacy laws.

FinTech Innovation and Competition

The financial technology, or FinTech, landscape is evolving at an incredible speed, introducing new ways to bank and manage money. Innovations like embedded finance, where financial services are integrated into non-financial platforms, and open banking, which allows secure data sharing between financial institutions and third-party providers, are reshaping customer expectations. Biometric authentication, using fingerprints or facial scans, is also becoming more common for secure access. For Commerce Bancshares, this means a constant need to assess these advancements. In 2024, FinTech investment globally reached significant figures, with venture capital funding continuing to pour into startups developing these cutting-edge solutions, highlighting the competitive pressure and the potential for strategic partnerships to enhance customer experience and operational efficiency.

Artificial Intelligence (AI) and Automation Adoption

Commerce Bancshares is navigating the increasing integration of Artificial Intelligence (AI) and automation across the financial sector. This technology is transforming banking operations, from enhancing customer service through chatbots to bolstering fraud detection and refining data analytics capabilities. For instance, by 2024, financial institutions globally are projected to invest billions in AI technologies to streamline processes and offer more tailored customer experiences.

To maintain a competitive edge, Commerce Bancshares must strategically invest in these advancements. This includes developing robust AI fair use policies to ensure ethical deployment and mitigate risks. The bank's ability to leverage AI for personalized services and operational efficiencies will be a key differentiator in the evolving financial landscape.

The adoption of AI and automation presents several key opportunities and considerations for Commerce Bancshares:

- Enhanced Efficiency: Automating routine tasks can significantly reduce operational costs and speed up service delivery.

- Personalized Customer Experiences: AI-driven analytics allow for tailored product offerings and proactive customer support.

- Improved Risk Management: Advanced AI models are proving effective in identifying and preventing fraudulent activities and managing credit risk more accurately.

- Competitive Advantage: Early and effective adoption of AI can position Commerce Bancshares ahead of competitors in terms of service quality and operational agility.

Payment Processing and Blockchain Technology

The financial landscape is rapidly evolving with advancements in payment processing. Real-time payment networks, such as Zelle, which Commerce Bancshares is a part of, are becoming increasingly popular, facilitating instant fund transfers. As of Q1 2024, Zelle reported over 2.4 billion transactions valued at more than $700 billion. This trend highlights the growing consumer demand for speed and convenience in financial transactions.

The emergence of central bank digital currencies (CBDCs) and broader blockchain applications presents both opportunities and challenges for traditional payment processors. While still in developmental stages in many regions, the potential for CBDCs to streamline cross-border payments and offer new financial services is significant. For instance, several countries, including China with its digital yuan, are actively piloting CBDCs, indicating a global shift towards digitalizing currencies.

Commerce Bancshares must adapt its payment processing infrastructure to integrate these emerging technologies. Staying competitive means embracing innovations that enhance efficiency, security, and user experience. This includes exploring how blockchain technology could potentially reduce transaction costs and settlement times, or how to best leverage real-time payment rails to offer superior services to both consumers and businesses.

- Zelle's Transaction Growth: Zelle processed over 2.4 billion transactions in Q1 2024, valued at over $700 billion, demonstrating a strong consumer preference for real-time payments.

- CBDC Development: Countries like China are actively piloting CBDCs, signaling a global trend towards digital currencies that could reshape payment ecosystems.

- Blockchain Potential: Blockchain technology offers the possibility of reducing transaction costs and speeding up settlement times, which Commerce Bancshares needs to consider for future competitiveness.

Securing Digital Banking: Combating Rising Cyberattacks

Commerce Bancshares must continuously invest in its digital infrastructure, focusing on user-friendly online and mobile platforms to meet evolving customer expectations. The bank is also actively addressing the growing threat of cyberattacks, a significant concern in the financial sector, with industry reports indicating a 13% rise in ransomware attacks in early 2024. To combat this, robust cybersecurity measures and data protection strategies are paramount for maintaining customer trust and regulatory compliance.

Legal factors

Banking Regulations and Compliance Requirements

Commerce Bancshares, like all financial institutions, navigates a stringent regulatory landscape. The Dodd-Frank Wall Street Reform and Consumer Protection Act continues to shape compliance, imposing rigorous requirements on capital adequacy and risk management. For instance, as of Q1 2024, Commerce Bancshares reported a Common Equity Tier 1 (CET1) capital ratio of 12.5%, well above regulatory minimums, demonstrating a commitment to financial stability and adherence to these critical banking regulations.

Consumer Protection Laws

Commerce Bancshares, like all financial institutions, must strictly adhere to consumer protection laws. This includes regulations around fair lending practices, ensuring all customers have equal access to credit, and robust data privacy measures to safeguard sensitive customer information. Transparent disclosure of financial products, detailing fees, interest rates, and terms clearly, is also paramount to maintaining customer trust and avoiding regulatory penalties.

Regulatory bodies such as the Consumer Financial Protection Bureau (CFPB) play a significant role in shaping these legal landscapes. For instance, the CFPB's ongoing focus on combating unfair, deceptive, or abusive acts or practices in the financial sector means Commerce Bancshares must continuously review and update its customer interaction protocols. In 2023, the CFPB reported a record number of consumer complaints, highlighting the continued importance of compliance in maintaining a positive customer relationship and avoiding costly litigation.

Anti-Money Laundering (AML) and Sanctions Compliance

Commerce Bancshares, like all financial institutions, faces ongoing legal challenges in adhering to Anti-Money Laundering (AML) and sanctions regulations. These rules are constantly being updated, requiring continuous investment in systems and training to ensure compliance. For instance, in 2023, the Financial Crimes Enforcement Network (FinCEN) continued to emphasize robust transaction monitoring and suspicious activity reporting (SAR) filings.

Maintaining strong AML and sanctions compliance programs is crucial for mitigating risks associated with financial crime. This includes implementing sophisticated detection mechanisms and thorough reporting processes to prevent illicit activities. Failure to comply can result in significant fines; for example, numerous banks faced penalties in the hundreds of millions of dollars in recent years for AML deficiencies.

Data Privacy and Cybersecurity Laws

Data privacy and cybersecurity laws are increasingly shaping the financial landscape. With cyber threats on the rise, regulations like the California Consumer Privacy Act (CCPA) and similar state-level acts are imposing stricter requirements on how financial institutions handle customer data. Commerce Bancshares must diligently adapt its data protection protocols and cybersecurity infrastructure to meet these evolving legal standards and safeguard sensitive information.

Compliance with these regulations is not just a legal necessity but a critical factor in maintaining customer trust. For instance, the financial services sector experienced a significant number of data breaches in 2023, highlighting the urgent need for robust cybersecurity measures. Commerce Bancshares' commitment to adhering to these stringent data privacy and cybersecurity laws directly impacts its operational integrity and reputation.

- Increased Regulatory Scrutiny: Financial institutions face growing oversight regarding data handling and breach notification protocols.

- Customer Data Protection: Laws like CCPA mandate specific rights for consumers concerning their personal information.

- Cybersecurity Investment: Compliance often necessitates significant investment in advanced security technologies and personnel.

- Reputational Risk: Failure to comply can lead to substantial fines and damage to customer confidence.

Merger and Acquisition Regulatory Approvals

Commerce Bank's future growth through mergers and acquisitions, like its announced agreement with FineMark Holdings, Inc. in late 2023, hinges on navigating a complex web of regulatory approvals. These processes are critical for ensuring fair competition and financial stability within the banking sector.

The legal landscape for bank consolidation is constantly evolving, impacting both the feasibility and the duration of these strategic initiatives. For instance, the U.S. banking industry saw significant regulatory scrutiny in 2024 following several regional bank failures in 2023, potentially leading to more stringent review of M&A deals.

- Regulatory Hurdles: Deals require sign-off from bodies like the Federal Reserve, Office of the Comptroller of the Currency (OCC), and potentially state banking departments.

- Antitrust Concerns: Regulators assess whether a merger would reduce competition or create a monopoly, especially in concentrated markets.

- Capital Requirements: Acquired entities and the combined bank must meet specific capital adequacy ratios, a key focus for regulators in 2024 and beyond.

Banking Faces Heightened Regulatory Scrutiny and Compliance Demands

Commerce Bancshares operates within a highly regulated environment, necessitating strict adherence to consumer protection laws, including fair lending practices and robust data privacy measures. For example, the Consumer Financial Protection Bureau (CFPB) continues to focus on combating unfair or deceptive acts, underscoring the need for continuous review of customer interaction protocols, as evidenced by the record number of consumer complaints reported by the CFPB in 2023.

Anti-Money Laundering (AML) and sanctions compliance remain critical, with regulatory bodies like FinCEN emphasizing robust transaction monitoring and suspicious activity reporting. Failure to comply can result in significant financial penalties, as demonstrated by numerous banks facing substantial fines in recent years for AML deficiencies.

Data privacy and cybersecurity laws, such as the CCPA, impose stricter requirements on handling customer data. Commerce Bancshares must adapt its data protection and cybersecurity infrastructure to meet these evolving legal standards, especially given the significant number of data breaches experienced by the financial services sector in 2023.

Mergers and acquisitions, like the announced agreement with FineMark Holdings in late 2023, are subject to extensive regulatory approvals from bodies like the Federal Reserve and OCC, with increased scrutiny in 2024 following regional bank failures in 2023.

Environmental factors

ESG (Environmental, Social, Governance) Pressures

Commerce Bancshares, like all financial institutions, faces growing pressure from stakeholders and regulators to prioritize Environmental, Social, and Governance (ESG) factors. This focus directly influences public perception and operational strategies. For instance, in 2023, the banking sector saw increased scrutiny on its financing of fossil fuels, a trend likely to continue and intensify through 2025.

Integrating sustainability into its core strategy is no longer optional for Commerce Bancshares; it's essential for sustained success and attracting capital. This includes fostering responsible banking practices, such as offering green financing options and actively managing climate-related risks. By Q1 2024, many large banks reported increased investment in sustainable finance initiatives, signaling a clear market shift.

Transparent ESG reporting is also paramount. Investors increasingly demand clear data on a company's environmental impact, social responsibility, and governance structures. Commerce Bancshares' commitment to this transparency will be a key differentiator in attracting socially conscious investors and maintaining a positive brand image in the evolving financial landscape.

Climate Change Risks and Sustainable Finance

Climate change presents significant risks for Commerce Bancshares. Physical risks, such as increased severe weather events in the Midwest, could impact the value of real estate collateral in their loan portfolios. For instance, intensified flooding in areas like the Missouri River basin, a key region for Commerce Bank, could lead to higher loan defaults.

Transition risks, driven by policy shifts towards a low-carbon economy, also pose challenges. As regulations tighten on carbon emissions, industries that are heavily reliant on fossil fuels may experience declining profitability, affecting their ability to service debt held by Commerce Bank. This could necessitate adjustments to lending criteria and investment strategies.

In response, Commerce Bancshares will likely need to enhance its assessment and management of these climate-related risks. Exploring opportunities in sustainable finance, such as financing renewable energy projects or offering green bonds, could mitigate these risks and potentially open new avenues for growth. The global sustainable finance market saw significant growth, with sustainable debt issuance reaching an estimated $1.5 trillion in 2024, indicating a strong demand for such products.

Carbon Footprint and Operational Sustainability

Commerce Bancshares, like other financial institutions, faces growing pressure to quantify and shrink its operational carbon footprint. This includes scrutinizing energy use in its branches and corporate offices, as well as the environmental impact of its supply chain. For instance, the banking sector is increasingly investing in green building certifications and renewable energy sources to demonstrate commitment to sustainability.

Environmental Regulations and Reporting

Commerce Bancshares, like all financial institutions, must navigate an increasingly stringent environmental regulatory landscape. The European Union's Corporate Sustainability Reporting Directive (CSRD), for instance, is setting a precedent for mandatory sustainability disclosures, which could influence global reporting standards. This means banks will need to bolster their systems for tracking and reporting their environmental impact, moving beyond voluntary initiatives to meet potentially new compliance requirements. For example, as of 2024, many large companies are already grappling with the complexities of Scope 3 emissions reporting, a significant challenge for financial institutions whose financed emissions often dwarf their direct operational footprint.

Preparing for this heightened transparency demands a proactive approach to data collection and management. Commerce Bancshares should anticipate a greater need for granular data on its lending portfolios' environmental performance, client emissions, and the climate-related risks embedded within its assets. This could involve significant investment in data analytics and reporting infrastructure to ensure accuracy and compliance. By 2025, the expectation for financial sector environmental disclosure is likely to be considerably higher than in previous years, with regulators and investors demanding quantifiable metrics.

- Enhanced Data Collection: Commerce Bancshares will need robust systems to gather and verify environmental data across its operations and lending activities.

- Regulatory Compliance: Staying ahead of evolving regulations, such as those influenced by CSRD, is crucial to avoid penalties and maintain market trust.

- Stakeholder Expectations: Increased demand for transparency from investors and customers necessitates clear and accurate reporting on environmental performance.

- Climate Risk Management: Integrating climate-related risks into financial reporting and strategic planning will become paramount.

Reputation and Greenwashing Risks

Public scrutiny of environmental commitments is intensifying, requiring banks like Commerce Bancshares to genuinely integrate sustainability into their operations to avoid accusations of greenwashing. Failure to do so can significantly damage reputation and erode stakeholder trust. For instance, a 2024 report by the Financial Times highlighted that investors are increasingly demanding verifiable data on ESG (Environmental, Social, and Governance) performance, with a notable increase in shareholder resolutions targeting companies perceived as making misleading environmental claims.

Commerce Bancshares' environmental initiatives must therefore be authentic and demonstrably measurable. This means moving beyond mere policy statements to tangible actions and transparent reporting. For example, detailing specific reductions in carbon emissions from operations or investments in renewable energy projects can build credibility. A 2025 analysis by McKinsey noted that companies with strong, transparent sustainability practices saw an average 5% higher valuation compared to peers with weaker ESG credentials.

- Reputational Damage: Accusations of greenwashing can lead to negative press and loss of customer loyalty.

- Investor Scrutiny: Investors in 2024-2025 are increasingly prioritizing verifiable ESG data, impacting access to capital.

- Stakeholder Trust: Authentic environmental initiatives are crucial for maintaining trust with customers, employees, and the wider community.

- Regulatory Risk: Evolving regulations around environmental disclosures could penalize companies with non-compliant or misleading practices.

Navigating Sustainability: Risks and Opportunities

Commerce Bancshares faces increasing regulatory pressure and stakeholder expectations regarding environmental impact, particularly concerning climate-related risks and carbon footprint reduction. By 2025, financial institutions are expected to provide more granular and verifiable data on their environmental performance and financed emissions, with a growing emphasis on combating greenwashing. This necessitates robust data collection, transparent reporting, and authentic integration of sustainability into core business strategies to maintain investor trust and market standing.

| Environmental Factor | Impact on Commerce Bancshares | Data/Trend (2024-2025) |

|---|---|---|

| Climate Change Risks | Physical risks (e.g., Midwest flooding) and transition risks (e.g., fossil fuel industry impact) affect loan portfolios and necessitate strategy adjustments. | Increased frequency of severe weather events in key operating regions. Global sustainable finance market growth estimated at $1.5 trillion in 2024. |

| Regulatory Landscape | Evolving environmental disclosure requirements (e.g., CSRD influence) demand enhanced data management and compliance systems. | Growing expectation for financial sector environmental disclosure; many companies grappling with Scope 3 emissions reporting as of 2024. |

| Stakeholder Expectations & Greenwashing | Demand for verifiable ESG data and authentic sustainability initiatives to build trust and avoid reputational damage. | Investors increasingly prioritize verifiable ESG data; companies with strong sustainability practices saw an average 5% higher valuation in a 2025 McKinsey analysis. |

PESTLE Analysis Data Sources

Our Commerce Bank PESTLE Analysis is meticulously constructed using data from reputable financial institutions like the Federal Reserve and the FDIC, alongside reports from leading economic forecasting firms and industry-specific publications. This ensures a comprehensive understanding of the political, economic, social, technological, legal, and environmental factors impacting the banking sector.