Columbia Bank Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Columbia Bank Bundle

Go Beyond the Preview—Access the Full Strategic Report

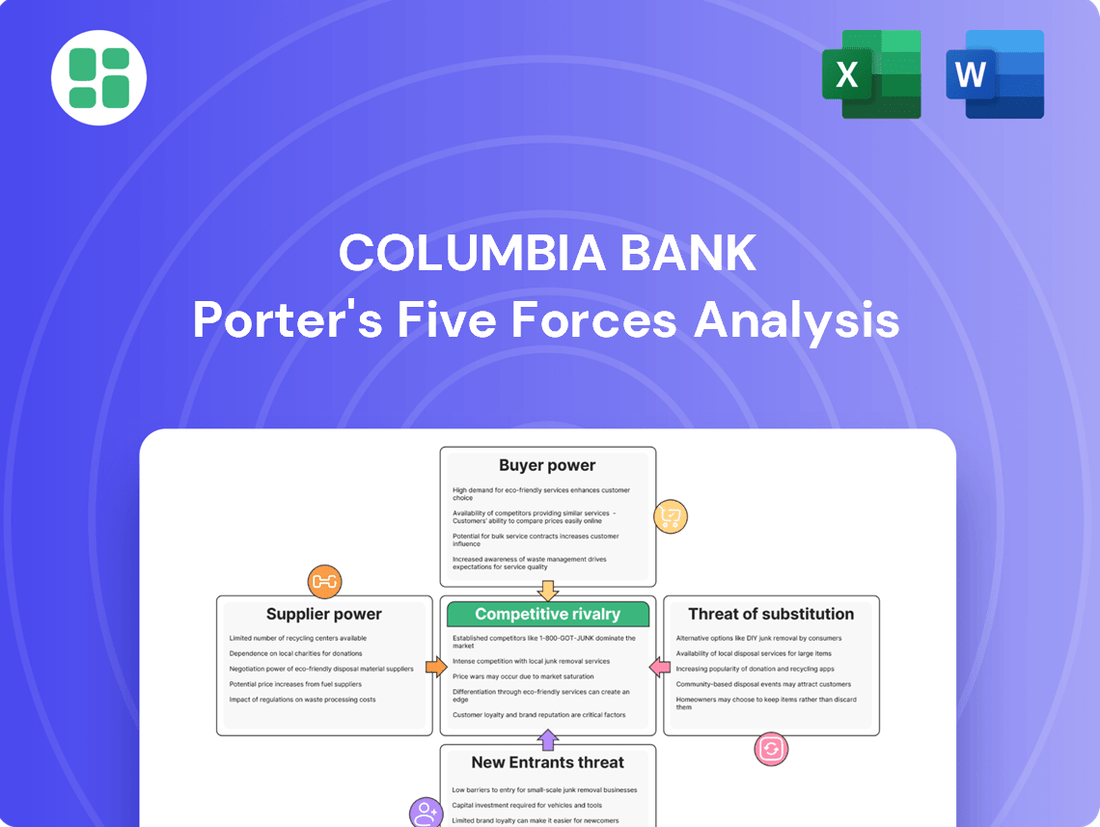

Columbia Bank operates within a dynamic financial landscape, facing pressures from rivals, evolving customer demands, and the constant threat of new entrants disrupting traditional banking models. Understanding these forces is crucial for navigating the competitive terrain.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Columbia Bank’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Access to Capital Markets

Columbia Bank's access to capital markets is a crucial factor influencing its bargaining power with suppliers, particularly those providing funding. The bank's ability to tap into wholesale funding, bond markets, and interbank lending directly affects its operational flexibility and cost of capital. For example, in the first quarter of 2025, Columbia Bank experienced a notable increase in deposits, which allowed it to reduce its reliance on more expensive wholesale funding sources, thereby strengthening its position.

Technology and Software Providers

Technology and software providers wield considerable bargaining power over banks like Columbia Bank, especially as digital transformation accelerates. The increasing reliance on sophisticated platforms for core banking functions, from deposit accounts to loan processing, means banks need reliable, cutting-edge solutions. In 2024, the global banking software market was valued at over $60 billion, highlighting the significant investment banks make in these technologies.

The specialized nature of many banking software solutions, coupled with the immense switching costs involved in changing core systems, further amplifies supplier leverage. These costs can include data migration, system integration, employee retraining, and potential disruption to operations. This makes banks hesitant to switch providers, even if better terms are available elsewhere, solidifying the power of existing technology partners.

Human Capital and Talent Pool

The availability of skilled banking professionals, such as loan officers and IT specialists, directly impacts Columbia Bank's ability to operate efficiently and deliver quality services. A scarcity of talent, particularly in specialized areas like cybersecurity or data analytics, can significantly increase recruitment costs and lengthen hiring timelines. For instance, in 2024, the U.S. Bureau of Labor Statistics projected a 10% growth for financial managers, indicating a competitive landscape for experienced professionals.

Regulatory and Compliance Service Providers

Regulatory and compliance service providers wield significant bargaining power over banks like Columbia Bank. The banking sector is heavily regulated, necessitating specialized legal, software, and audit services. For instance, the Dodd-Frank Act and subsequent regulations have increased the demand for compliance expertise.

The complexity and constant evolution of banking regulations, particularly with potential policy shifts anticipated around 2025, amplify the influence of these suppliers. Banks must rely on these providers to navigate intricate legal frameworks, making switching costs high.

- High Demand for Specialized Expertise: Banks require niche legal and compliance professionals.

- Switching Costs: Transitioning to new compliance software or legal counsel can be time-consuming and expensive.

- Regulatory Uncertainty: Evolving regulations create ongoing reliance on experienced providers.

- Limited Number of Qualified Suppliers: The specialized nature of banking compliance often means fewer viable options.

Data and Information Service Providers

Data and information service providers hold considerable sway over banks like Columbia Bank. Access to accurate financial data, credit reports, and market intelligence is non-negotiable for effective risk management and strategic decision-making. For instance, in 2023, the global financial data market was valued at approximately $30 billion, highlighting the critical nature of these services.

These suppliers, including credit bureaus and specialized financial data platforms, are indispensable for Columbia Bank's core functions such as lending and wealth management. The unique and often proprietary nature of the data they offer can significantly amplify their bargaining power, as alternatives may be scarce or less comprehensive.

- Critical Data Dependency: Columbia Bank relies heavily on external data providers for credit scoring, market analysis, and regulatory compliance.

- Proprietary Data Assets: Some information services possess unique datasets that are not easily replicated, giving them an advantage.

- Market Concentration: A few dominant players often exist in specialized data segments, limiting competition and increasing supplier leverage.

- High Switching Costs: Integrating new data systems can be complex and expensive, discouraging banks from frequently changing providers.

Supplier Power Shapes Banking's Future

Suppliers of specialized banking software and technology often possess significant bargaining power due to high switching costs and the critical nature of their services. In 2024, the global banking software market exceeded $60 billion, underscoring the substantial investment banks make in these solutions, which are essential for core operations.

Data and information service providers also exert considerable influence, as banks like Columbia Bank depend on accurate financial data for risk management and decision-making. The global financial data market was valued around $30 billion in 2023, with some providers holding proprietary datasets that limit alternatives and increase supplier leverage.

The bargaining power of regulatory and compliance service providers is amplified by the complex and evolving regulatory landscape. Banks must rely on these experts to navigate intricate legal frameworks, and the specialized nature of these services, coupled with high switching costs, solidifies supplier influence.

Finally, the availability of skilled banking professionals, particularly in specialized fields, can strengthen the bargaining position of these suppliers. A shortage of talent, projected to grow by 10% for financial managers in the U.S. by 2024 according to the Bureau of Labor Statistics, increases recruitment costs and hiring times for banks.

| Supplier Category | Bargaining Power Factors | Impact on Columbia Bank | 2024/2025 Data Point |

|---|---|---|---|

| Technology & Software | High switching costs, specialized solutions | Increased reliance, potential for higher costs | Global banking software market > $60 billion |

| Data & Information Services | Proprietary data, market concentration | Critical dependency, limited alternatives | Global financial data market ~ $30 billion (2023) |

| Regulatory & Compliance | Complex regulations, specialized expertise | Ongoing reliance, high integration costs | Increased demand due to evolving regulations |

| Skilled Labor | Talent scarcity, specialized skills | Higher recruitment costs, longer hiring | Financial manager roles projected 10% growth (U.S.) |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Columbia Bank's unique position in the financial services industry.

Quickly identify and mitigate competitive threats with a dynamic, interactive Porter's Five Forces model tailored for Columbia Bank's unique market landscape.

Customers Bargaining Power

Low Switching Costs for Basic Services

For fundamental banking products such as checking and savings accounts, customers generally experience minimal costs when switching providers. This is particularly true with the proliferation of digital banking platforms, making it easier than ever to move funds and services. In 2024, the average consumer switched their primary checking account every 5.7 years, a figure that has remained relatively stable but highlights the underlying ease of transition.

This low barrier to entry for customers allows them to readily explore competitors offering more attractive interest rates or superior convenience. Consequently, banks must actively work to retain their customer base by offering more than just basic transactional services. Columbia Bank’s strategy to foster enduring customer relationships and deliver tailored, personalized service is a direct response to this, aiming to elevate the perceived value of their offerings beyond simple pricing.

Availability of Alternative Financial Service Providers

Customers, especially small and medium-sized businesses and individuals, now have a much wider selection of financial service providers than ever before. Beyond traditional banks, options like fintech startups, online lenders, and credit unions are readily available, giving customers more power to choose.

These alternative providers often distinguish themselves with niche services, quicker loan approvals, or more competitive fee structures. For instance, in 2024, the fintech sector continued its rapid expansion, with reports indicating that over 60% of consumers globally have used at least one fintech service, directly increasing customer leverage against established institutions.

The small and medium-sized enterprise (SME) lending market, in particular, has experienced a significant influx of alternative platforms. These platforms are actively competing for market share, often by offering more flexible terms or streamlined application processes, thereby enhancing the bargaining power of business clients seeking capital.

Price Sensitivity and Interest Rate Environment

Customers are keenly aware of interest rates, actively comparing loan costs and deposit returns across different institutions. This price sensitivity intensifies when interest rates are volatile, pushing them to seek out the best available deals.

Columbia Bank experienced this firsthand in Q1 2025, as its net interest margin decreased. This dip was driven by earning asset yields that couldn't keep pace with funding costs, indicating customers were indeed shopping around for better rates.

Information Transparency and Digital Access

The internet and mobile banking apps have significantly boosted customer power by providing easy access to information. Customers can now compare rates, fees, and services across various banks with just a few clicks. This transparency erodes information asymmetry, empowering customers to make better choices and increasing their leverage.

Digital platforms are now central to how banks attract and keep customers. For instance, in 2024, the average customer acquisition cost for a new checking account in the US was estimated to be around $150-$250, with digital channels often proving more efficient. This makes it easier for customers to switch to a competitor offering better terms, as the friction of switching has been dramatically reduced.

- Unprecedented Information Access: Customers can readily compare financial products and services online, fostering greater price sensitivity.

- Reduced Switching Costs: Digital platforms simplify the process of opening new accounts and closing old ones, lowering the barriers to switching banks.

- Enhanced Negotiation Power: With readily available market data, customers are better positioned to negotiate terms or seek more favorable offers from their current bank.

- Digital Acquisition and Retention Focus: Banks invest heavily in digital experiences to attract and retain customers, acknowledging the increased bargaining power driven by online transparency.

Large Corporate and Commercial Clients

Large corporate and commercial clients wield considerable bargaining power, even though Columbia Bank's primary focus is on smaller businesses. These larger clients, by virtue of their substantial transaction volumes and the complexity of their financial needs, can negotiate more favorable terms. This often translates to demands for customized loan structures, competitive rates on treasury services, and specialized cash management solutions. For instance, a large corporation might leverage its significant deposit balances to secure lower interest rates on borrowing or reduced fees for payment processing. This ability to negotiate impacts Columbia Bank’s net interest margin and overall profitability for these key relationships.

Columbia Bank's strategic intent to expand its presence in the middle-market and corporate banking sectors directly addresses this dynamic. By actively pursuing and cultivating these larger client relationships, the bank aims to offset the inherent bargaining power of these entities with the increased revenue and diversified service offerings they represent. As of the first quarter of 2024, Columbia Bank reported a 12% increase in commercial loan originations, signaling a deliberate push into this segment, which is crucial for driving growth and managing the competitive pressures from these powerful customers.

- Volume-Driven Negotiations: Large clients can leverage their substantial business volume to demand better pricing on loans and services.

- Tailored Solutions: These clients often require customized financial products, giving them leverage in the negotiation process.

- Impact on Profitability: Favorable terms negotiated by large clients can compress interest margins and service fee revenue for the bank.

- Strategic Growth Area: Columbia Bank's focus on middle-market and corporate clients aims to capitalize on the revenue potential of these relationships despite their bargaining power.

Customer Power: Navigating Low Switching Costs and Fintech Growth

Customers possess significant bargaining power due to low switching costs and increased access to information, readily comparing rates and services. In 2024, the average consumer switched their primary checking account every 5.7 years, underscoring this ease of transition.

The rise of fintech and alternative lenders further amplifies customer leverage, offering competitive pricing and specialized services. Over 60% of global consumers used fintech services in 2024, highlighting this shift.

Columbia Bank's strategy of personalized service and digital engagement aims to mitigate this power by increasing customer stickiness and perceived value beyond mere price. This is crucial as the bank saw its net interest margin decrease in Q1 2025, partly due to funding costs outpacing earning asset yields.

| Factor | Impact on Columbia Bank | 2024/2025 Data Point |

|---|---|---|

| Switching Costs | Low, enabling easy comparison shopping | Average checking account switch: 5.7 years |

| Information Access | High, via digital platforms | 60%+ global consumers used fintech in 2024 |

| Provider Options | Numerous (banks, fintech, credit unions) | Continued fintech sector expansion |

| Price Sensitivity | High, especially with volatile rates | Q1 2025 Net Interest Margin decrease |

Preview the Actual Deliverable

Columbia Bank Porter's Five Forces Analysis

This preview showcases the complete, professionally written Porter's Five Forces analysis for Columbia Bank, exactly as you will receive it upon purchase. You're looking at the final document, ensuring no surprises and immediate usability after your transaction. This comprehensive analysis is ready for your strategic planning needs.

Rivalry Among Competitors

Fragmented Regional Banking Market

The regional banking landscape is highly fragmented, featuring a mix of regional banks, community banks, and even large national institutions vying for customers. This means Columbia Bank faces competition from many directions, each with its own strengths and customer base.

Columbia Banking System's recent acquisition of Pacific Premier Bancorp, a significant move announced in 2024, highlights this intense competition. This deal aims to bolster Columbia's presence, particularly in the lucrative Southern California market, signaling a strategic push for scale and market share in a crowded field.

The ongoing consolidation, exemplified by Columbia's acquisition, underscores the dynamic nature of the regional banking sector. Banks are actively pursuing mergers and acquisitions to gain a competitive edge, expand their geographic reach, and achieve greater operational efficiencies.

Product and Service Differentiation

Product and service differentiation in the banking sector, while challenging due to the commoditized nature of many core offerings, remains a crucial battleground. Columbia Bank, for instance, emphasizes building long-term relationships and delivering personalized financial services as its primary differentiator.

However, this approach is met with intense competition. Many rivals are investing heavily in unique digital experiences, rolling out specialized lending products tailored to specific industries, or focusing on providing superior customer service to capture and hold onto clients. For example, in 2024, many regional banks reported increased spending on digital transformation initiatives, with some allocating over 15% of their IT budgets to enhancing online and mobile banking platforms.

Industry Growth Rate and Loan Demand

While the U.S. banking sector experienced modest loan growth in 2024, a projected decrease in interest rates for 2025 is anticipated to stimulate loan demand. This anticipated upswing in lending activity could heighten competitive pressures as financial institutions actively seek to capture new market share.

Columbia Bank demonstrated resilience in 2024, reporting sustained growth within its commercial loan portfolio. This indicates a strong performance despite broader industry trends, positioning the bank favorably as demand is expected to rise.

Regulatory Environment and M&A Activity

The regulatory environment significantly shapes competitive rivalry. Potential shifts in U.S. presidential administration policies could alter the banking landscape. For instance, a more lenient regulatory stance might encourage bank mergers and acquisitions, leading to increased consolidation and stronger competition from larger, well-capitalized institutions.

Merger and acquisition activity within the banking sector is anticipated to pick up pace, particularly in the latter half of 2025. This trend suggests that banks will face heightened competition as the market consolidates. For example, the first half of 2024 saw a notable increase in M&A announcements, with reports indicating over $50 billion in announced deals in the U.S. banking sector alone by mid-year.

- Regulatory shifts can either intensify or ease competitive pressures.

- Increased M&A activity, projected for late 2025, will likely consolidate the market.

- Consolidation could introduce larger, more formidable competitors.

- Banks must adapt to evolving regulatory frameworks and competitive structures.

Digital Transformation and Fintech Integration

The banking sector is experiencing intense rivalry driven by digital transformation and the rapid integration of fintech solutions. This forces established institutions like Columbia Bank to accelerate innovation to meet evolving customer expectations and stay ahead of agile new entrants.

Regional banks are actively pursuing partnerships and collaborations with fintech firms to enhance their digital capabilities, rather than solely relying on organic growth. This strategic approach allows them to quickly adopt new technologies and offer more sophisticated digital services.

Banks that successfully harness technology to elevate customer experience, streamline operations, and introduce novel products are poised to gain a significant competitive advantage. For instance, in 2024, the global fintech market was valued at an estimated $1.1 trillion, highlighting the immense growth and competitive pressure within this space.

- Digital Adoption: A significant portion of banking customers now expect seamless digital interactions, pushing banks to invest heavily in mobile banking apps and online platforms.

- Fintech Collaboration: Partnerships with fintech companies are becoming crucial for banks to offer specialized services like digital payments, peer-to-peer lending, and AI-driven financial advice.

- Operational Efficiency: Technology adoption, such as robotic process automation (RPA), is enabling banks to reduce costs and improve efficiency, with RPA adoption in financial services projected to grow substantially by 2025.

- Customer Experience: Banks prioritizing personalized digital experiences and user-friendly interfaces are seeing higher customer retention rates and increased market share.

Banking Competition Intensifies: M&A, Fintech, and Rate Shifts Drive Rivalry

The competitive rivalry for Columbia Bank is intense due to a fragmented regional banking market and ongoing industry consolidation. Banks are actively pursuing mergers and acquisitions to expand their reach and efficiency, as evidenced by Columbia's 2024 acquisition of Pacific Premier Bancorp to strengthen its position in Southern California. This drive for scale means Columbia faces formidable competitors, many of whom are investing heavily in digital transformation and specialized products to capture market share.

The banking sector's competitive intensity is further fueled by rapid fintech integration and evolving customer expectations for seamless digital experiences. Banks that prioritize technology for enhanced customer service and operational efficiency, like those investing over 15% of IT budgets in digital platforms in 2024, are gaining a significant edge. The global fintech market's estimated $1.1 trillion valuation in 2024 underscores the pressure on traditional banks to innovate or risk losing ground.

Anticipated interest rate shifts in 2025 are expected to boost loan demand, likely intensifying competition as institutions vie for new business. Furthermore, a projected increase in merger and acquisition activity, particularly in late 2025, will likely consolidate the market, potentially introducing larger, more powerful competitors and requiring banks like Columbia to remain agile and strategically focused.

SSubstitutes Threaten

Fintech Companies and Digital Lenders

Fintech companies represent a potent substitute threat to traditional banking services, including those offered by Columbia Bank. These agile digital firms specialize in areas like payments, lending, and wealth management, often leveraging technology to offer more competitive pricing and user-friendly experiences.

For instance, the online lending market has seen substantial growth. In 2024, the global fintech market was projected to reach over $33 billion, with digital lending being a significant component. Many small and medium-sized businesses, a core customer base for Columbia Bank, are finding fintech lenders to be a faster and more flexible alternative for securing capital compared to traditional bank loans.

Credit Unions and Community Development Financial Institutions (CDFIs)

Credit unions and Community Development Financial Institutions (CDFIs) present a significant threat of substitutes for Columbia Bank. Credit unions, operating on a not-for-profit, member-owned model, often provide lower fees and more favorable interest rates on loans and deposits, directly competing with Columbia Bank's retail banking services. For instance, as of late 2023, the average interest rate on savings accounts at credit unions was often higher than at traditional banks, attracting depositors seeking better returns.

CDFIs, meanwhile, focus on serving low-income individuals and communities, offering specialized financial products and services that can substitute for traditional banking offerings, especially for small businesses and individuals in underserved areas. Their community-centric approach and tailored lending practices can be highly attractive to specific customer segments that Columbia Bank also targets, potentially siphoning off market share through a more personalized and mission-driven value proposition.

Direct Investment and Crowdfunding Platforms

Crowdfunding and direct investment platforms present a significant threat of substitutes for traditional bank lending, especially for businesses needing capital. These platforms allow companies, particularly startups and smaller enterprises, to bypass the often stringent requirements of bank loans, providing a more accessible route to funding. For instance, the global crowdfunding market was projected to reach over $13 billion in 2023, demonstrating its growing importance as an alternative financing channel.

Peer-to-Peer (P2P) Lending

Peer-to-peer (P2P) lending platforms present a significant threat of substitutes for Columbia Bank, particularly in consumer and small business lending. These platforms connect borrowers directly with individual lenders, often bypassing traditional banking intermediaries. This disintermediation can lead to more competitive interest rates for borrowers and potentially higher yields for lenders compared to conventional savings accounts or certificates of deposit.

The P2P lending market has seen substantial growth. For instance, by the end of 2023, the global P2P lending market size was estimated to be around $100 billion, with projections indicating continued expansion. This growth signifies an increasing acceptance and utilization of P2P platforms as alternatives to traditional bank loans. While P2P lending often focuses on smaller loan amounts, it directly competes with a core segment of Columbia Bank's retail and small business loan portfolio.

- Growing Market Share: P2P lending platforms are capturing a larger share of the consumer and small business loan market, offering an alternative to traditional banking services.

- Competitive Rates: P2P platforms often provide more attractive interest rates for both borrowers and lenders due to lower overhead costs compared to established banks.

- Technological Advancement: Innovations in fintech continue to enhance the user experience and efficiency of P2P lending, making it a more compelling substitute.

- Increased Accessibility: P2P lending can offer faster approval processes and greater accessibility for individuals and small businesses who may face challenges securing traditional bank financing.

Internal Financing and Cash Management

Established companies can significantly reduce their reliance on external financing by effectively managing their cash flow and utilizing retained earnings. For instance, in 2024, many corporations focused on optimizing working capital, with some reporting substantial improvements in cash conversion cycles, thereby lessening the need for bank credit lines.

Individuals also present a substitute threat. Many consumers increasingly turn to personal savings, peer-to-peer lending platforms, or even readily available credit cards for immediate financial needs, bypassing traditional bank loans or overdraft facilities. This trend was evident in 2024 with continued growth in digital payment solutions and alternative lending avenues.

- Internal financing through retained earnings: Companies reinvesting profits reduce borrowing needs.

- Efficient cash management: Optimizing receivables, payables, and inventory frees up internal cash.

- Personal savings and credit cards: Individuals use these for short-term needs, substituting bank products.

- Alternative lending platforms: P2P lending and other fintech solutions offer substitutes for traditional loans.

The Substitute Surge: Redefining Banking Competition

The threat of substitutes for Columbia Bank is substantial, encompassing a range of financial services and products that offer alternatives to traditional banking. Fintech innovations, credit unions, crowdfunding, P2P lending, and even internal corporate financing all chip away at the bank's traditional customer base and revenue streams.

For example, the burgeoning fintech sector, with a projected global market exceeding $33 billion in 2024, directly challenges Columbia Bank's offerings in payments, lending, and wealth management. Similarly, the global crowdfunding market, estimated to surpass $13 billion in 2023, provides an accessible alternative for businesses seeking capital, bypassing conventional bank loans.

The increasing reliance on internal financing by corporations, demonstrated by a focus on working capital optimization in 2024, also reduces demand for bank credit lines. This multifaceted competitive landscape underscores the need for Columbia Bank to continually innovate and adapt its services to remain relevant.

| Substitute Category | Key Characteristics | Impact on Columbia Bank | Example/Data Point (2023-2024) |

|---|---|---|---|

| Fintech Companies | Agile, tech-driven, competitive pricing, user-friendly | Direct competition in payments, lending, wealth management | Global fintech market projected >$33 billion (2024) |

| Credit Unions | Member-owned, not-for-profit, lower fees, better rates | Competition in retail banking, deposits, and loans | Higher savings account rates than traditional banks (late 2023) |

| Crowdfunding/Direct Investment | Bypass traditional lending, accessible funding for businesses | Alternative financing for startups and SMEs | Global crowdfunding market estimated >$13 billion (2023) |

| P2P Lending | Disintermediation, direct borrower-lender connection | Competition in consumer and small business loans | Global P2P lending market size ~ $100 billion (end of 2023) |

| Internal Corporate Financing | Retained earnings, efficient cash management | Reduced demand for bank credit lines and loans | Focus on working capital optimization by corporations (2024) |

Entrants Threaten

High Regulatory Barriers

The banking sector faces formidable regulatory hurdles, including stringent licensing, rigorous compliance mandates, and substantial capital reserve requirements. These factors create a high barrier for any new traditional bank seeking to enter the market, making it a costly and complex undertaking. For instance, as of late 2024, the average capital adequacy ratio for major U.S. banks remains well above the regulatory minimums, underscoring the significant capital commitment required.

Significant Capital Requirements

Launching a new bank demands immense upfront investment. This includes setting up physical branches, acquiring cutting-edge banking technology, and crucially, meeting stringent regulatory capital reserves. For instance, Columbia Banking System reported total assets exceeding $50 billion as of the first quarter of 2024, underscoring the sheer scale of financial resources typically managed by established institutions.

These substantial capital requirements act as a significant barrier, deterring many aspiring entrepreneurs from entering the banking sector. The need for extensive funding to cover operational costs and regulatory compliance makes it a challenging landscape for new players to navigate and compete effectively.

Brand Loyalty and Trust

Existing financial institutions, including Columbia Bank, enjoy a significant advantage through established brand loyalty and customer trust. In 2024, a survey by Brand Finance indicated that the top 100 most valuable banking brands globally saw a collective increase in brand value, highlighting the enduring importance of reputation in the sector. This deep-seated trust is hard-won and acts as a substantial barrier for newcomers aiming to attract depositors and borrowers.

New entrants must invest heavily in marketing and customer acquisition to even begin to chip away at the loyalty enjoyed by established players like Columbia Bank. Building a reputation for reliability and security in financial services takes years, if not decades, a timeline that can deter potential competitors. Columbia Bank's focus on its community roots and long-standing customer relationships, a strategy that has proven effective for regional banks, further solidifies its position against potential disruptors.

Economies of Scale and Network Effects

Established banks like Columbia Bank leverage significant economies of scale. This translates to lower per-unit costs in areas like technology infrastructure, marketing campaigns, and regulatory compliance, making it difficult for new, smaller entrants to match their pricing and service offerings. For instance, in 2024, the cost of processing a single transaction for a large incumbent bank might be fractions of a cent, whereas a startup could face much higher initial per-transaction costs.

Furthermore, network effects play a crucial role. Columbia Bank’s extensive customer base and established branch network, which it is further expanding in 2025, create a powerful moat. Customers value the convenience of widespread access to services and the trust associated with a large, familiar institution. This makes it challenging for new entrants to attract a critical mass of users quickly enough to compete effectively.

The threat of new entrants is thus moderated by these entrenched advantages:

- Economies of Scale: Incumbent banks can achieve lower operating costs per customer due to their size, impacting pricing power.

- Network Effects: A larger customer base and physical presence enhance service value and brand loyalty, creating barriers to entry.

- Capital Requirements: The significant capital needed to establish a comparable operational scale and regulatory compliance further deters new players.

Technological Disruption by Fintech

Fintech companies pose a significant threat of new entrants, challenging traditional banking models. They often leverage technology to offer specialized services, sometimes operating with fewer initial regulatory burdens than established banks.

These agile disruptors can carve out profitable niches, offering services like digital payments, peer-to-peer lending, or specialized investment platforms. For instance, the global fintech market was valued at approximately $11.2 trillion in 2023 and is projected to grow substantially, highlighting the scale of this competitive force.

- Niche Market Entry: Fintechs can enter specific segments, like international money transfers, with lower overhead than traditional banks.

- Regulatory Arbitrage: Initially, some fintechs may operate under lighter regulatory frameworks, allowing for faster innovation and market penetration.

- Scaling Challenges: As fintechs grow, they increasingly face comparable regulatory requirements and the need for substantial capital, aligning them more closely with traditional players.

Capital & Compliance: Banking's High Entry Barriers

The threat of new entrants for Columbia Bank is significantly mitigated by high capital requirements and extensive regulatory compliance. New banks need substantial funding for operations and to meet capital adequacy ratios, which remained robust for major U.S. banks in 2024, often exceeding minimums. This financial barrier, coupled with the need to build brand trust and achieve economies of scale, makes it challenging for newcomers to compete effectively against established players.

Porter's Five Forces Analysis Data Sources

Our Porter's Five Forces analysis for Columbia Bank leverages insights from financial statements, investor relations materials, and industry-specific market research reports. We also incorporate data from regulatory filings and economic indicators to provide a comprehensive view of the competitive landscape.